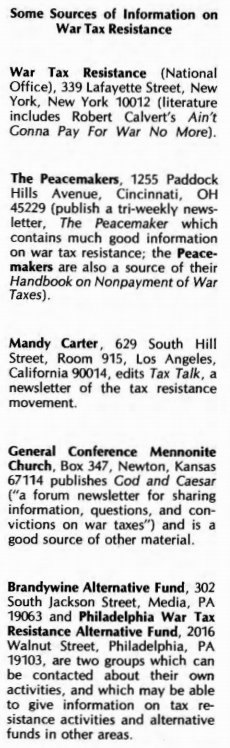

Tax resistance in the “Peace Churches” →

Quakers →

20th–21st century Quakers →

Friends Journal

Here are a couple of newspaper articles that give a glimpse of how American Quakers addressed war tax resistance at the New York Yearly Meeting gathering at Lake George in , where “the tragic situation in Viet Nam” was high on the agenda:

A report published after the meeting called on members of the Society of Friends to exercise their consciences and offered support to those Quakers whose actions resulted in financial or personal loss.

“We call upon Friends to obey the Inner Light even when this means disobeying man’s laws, and to risk whatever penalties may be incurred,” said the report.

“We call upon Friends to examine their consciences concerning whether they cannot more fully dissociate themselves from the war machine by tax refusal or changing occupations.”

“We call upon Friends to urge that young men consider in conscience whether they can submit to a military system that commands to kill and destroy.”

“We call upon Friends Meetings to support acts of compromise [sic] by setting up Committees for Sufferings to keep close touch with deeply exercised Friends and their families who may need spiritual and material care because of their witness.”

So far, there has been no indication that any Friends will not pay their taxes, or refuse the draft or disobey “man’s laws.”

But if any do they will be supported by other Friends.

“I’ve thought about it but I’m not persuaded that this is an effective way.

I admire people if their conscience leads them to take that action,” says John Daniels, clerk of the Albany Society of Friends.

An Associated Press dispatch from , put it this way:

Quakers in the New York area have been encouraged to refuse to pay taxes or hold jobs that contribute to the war effort in Viet Nam.

The Society of Friends office here made public a document or “testimony” approved at an annual meeting at Silver Bay on Lake George, N.Y.

Similar to the Peace Declaration of The Friends in 1660, the message was described as perhaps the “strongest message of the 20th century by a major body within the denomination.”

In the document, Quakers were promised financial help through special committees if they changed jobs or refused to pay taxes in protest against the war.

The new “testimony” warned Quakers that they may be facing a “supreme test” that could lead to persecution such as the sect suffered 300 years ago.

Entitled “Message to Friends on Viet Nam,” the document said members of the society must “stand forth unequivocally and at all costs to proclaim their peace testimony.”

Quakers were urged to express their concern over the war to lawmakers and the world community, and to “examine their consciences concerning whether they cannot more fully dissociate themselves from the war machine by tax refusal or changing occupations.”

The 72 Friends “meetings” or congregations in New York, northern New Jersey, and southern Connecticut were called upon to “support acts of conscience by setting up committees for sufferings…”

I also made note of this Lake George meeting in my entry.

At that time I was unable to find an on-line copy of the “Message to Friends on Viet Nam,” but in renewing my search, I found that someone had uploaded a scan of the Friends Journal.

That article didn’t get me any closer to the text I was hunting for, but it did include some other interesting items, including an article by Franklin Zahn on tax resistance, and another by Thomas Bassett about the New England Yearly Meeting that shows war tax resistance was on the agenda there too:

Tax Refusal, Law, and Order

by Franklin Zahn

In the President asked for a ten per cent surcharge on income taxes that might “continue for so long as the unusual expenditures associated with our efforts in Vietnam require higher revenues.”

In words of Quaker simplicity, he was requesting a war tax.

What ought Friends to do about specific levies for war?

First, of course, they can work to prevent such legislation, using the agency they have set up for such purposes — the Friends Committee on National Legislation — and using the opportunity to tell congressmen again that Friends favor de-escalation rather than the escalation the new taxes are designed to permit.

If the President’s request becomes law, Friends may then pay under protest.

This situation might loosely be compared to that of a young man who joins the Army under protest: voicing his convictions is better than not voicing them, but it’s not a satisfactory solution.

After paying a war tax Friends may then through regular channels claim a refund, and although in the past this has never been granted on the basis of conscience, a number of California taxpayers plan to make a common court case.

Here the analogy might be to the young man who goes to court to get released from the Army — again not a very hopeful approach.

However, the young man is entitled by law to request exemption in the first place; unfortunately for Friends as taxpayers, no such legal choices are available to them.

Years ago Pacific Yearly Meeting suggested legislation embodying conscientious-objector provisions in Federal tax laws, and today some Friends are still considering such proposals, but for the foreseeable future, pacifists will have no legal tax alternatives.

Further, for most Friends there is not even a possible illegal alternative for their tax dollars, for if not paid as ordered, the dollars are frequently levied from bank accounts which unfortunately most Friends in their affluence today have.

It is as though a pacifist refused to bayonet an enemy and several strong men held the weapon in his hands and jabbed it for him.

The choice is not whether to participate in war or not, but whether to do so willingly or to drag one’s feet.

“We refuse to steal not as a protest against burglary — with consideration of how ‘effective’ we may or may not be — but simply because for us stealing is wrong.”

Many see a refusal to pay taxes voluntarily as only a protest.

Now it is true that we can designate any act we engage in as a protest against something.

We can fast and announce that our purpose is to protest the war.

A vigil, a march, a meeting, or a handing out of educational material can be a protest if so designated.

Even the young Friend who refused to carry the bayonet could refuse as a protest.

But we are not necessarily protesting anything when we refuse to do that which for us is wrong.

We refuse to steal not as a protest against burglary — with consideration of how “effective” we may or may not be — but simply because for us stealing is wrong.

Similarly, a Friend may refuse to pay taxes voluntarily, not in protest but because he feels he must not participate in war.

In Southern California’s Quarterly Meeting there are many individuals and three Meetings refusing to pay voluntarily the seven per cent war tax on telephone bills.

I do not know which are consciously doing this as a “protest” and which see it as part of the Friends’ code of conduct or way of life.

When Claremont Meeting, in its public statement, said that in refusing to pay it was following a precedent in Friends’ peace testimony, two newspapers used the term “protest” in their very good coverage and one did not.

All three papers quoted the portion of the statement that said, “Those of us who refuse to pay taxes which go to support war also are willing to accept the legal consequences of this refusal…”

Such willingness, along with complete openness, is an important part of any “civil” or, as one Friend terms it, “courteous” disobedience.

It might also be called “orderly” disobedience, for, contrary to the usual linking together of “law and order,” in these days of riots the two words are not necessarily related.

The war in Vietnam is considered by many Americans to be lawful, but to Vietnamese villagers the aftermath of a bombing raid would hardly appear orderly.

On the contrary, the refusal to pay taxes for such chaos may be unlawful, but when the decision is made openly, arrived at in the usually slow and quiet manner of Friends’ group decisions, and explained in nonevasive language with a willingness to accept penalties, it may be very orderly indeed.

Franklin Zahn, member of Claremont (Calif.) Meeting, free-lance writer, and compiler of the recent leaflet “Early Friends and War Taxes,” first refused the telephone excise tax in , during the Korean War, and had his telephone disconnected.

(In , the Internal Revenue Law was amended, permitting telephone companies to refer unpaid taxes to IRS.)

In he read this paper to Pacific Yearly Meeting’s session on civil disobedience.

New England Yearly Meeting

Reported by Thomas Bassett

Quakerism is uneasy everywhere in the face of long-continuing violence, “distress of nations, and perplexity whether on the shores of Asia or in the Edgware Road.”

Friends’ answers to problems of the Vietnam war and urban riots have ranged from evangelical mission to Quaker action.

Evangelical Friends eschew mere human “manipulation” and expect peace only when Christ reigns in human hearts.

Philadelphia and Baltimore Yearly Meetings, reinforced by AFSC and FCNL staffs in their midst, approved minutes to send medical aid to North Vietnam against the law if it could not be changed.

New England Friends were, as usual, in the middle of this scale.

The clerk opened the first plenary session with William Penn’s words on evangelism: “They were changed men themselves before they went out to change others.”

The last, eight-hour session approved a minute to oppose the President’s war surtax and urged its members to earnest consideration of whether they can conscientiously pay war taxes.

And take a look at this advertisement from the back pages:

On , I shared with you some interesting stuff from a edition of the Quaker periodical Friends Journal.

That inspired me to hunt around on-line and see if there were any other copies in the archives.

I was able to find a complete set, or close to it anyway, from .

And there’s a tremendous amount of material about war tax resistance in those pages.

War tax resistance, which had been such a core part of Quaker practice in America from the founding of Pennsylvania through the American Civil War, began to fade in , until by it seemed to belong to the same ancient past as “thee”s and “thou”s, and only an eccentric fringe of Quakers considered it a living practice.

But, from reviewing the back issues of Friends Journal, I see that the tradition had not died; it was only sleeping.

It woke up in and regained its place as a core part of the Quaker peace testimony and a frequent topic of discussion at Quaker meetings.

, hardly an issue of the journal didn’t have some discussion of war tax resistance, and there were periodic “special issues” on the subject (there was one as recently as ).

Then, , the topic started appearing less and less, and migrating into the back pages (and the obituaries — over 25% of the mentions of tax resistance in the Friends Journal are past tense references from obituaries and retrospectives… and the only such mention I found in the six issues from is in an obituary).

Have we entered a new era of forgetting, or just a calm before the next outbreak?

I should probably be careful about drawing conclusions from this data.

I have learned a lot about the content of one magazine, which gives hints as to the state of the Society of Friends, but may be biased by which Friends were subscribers and by the opinions of the magazine staff at different times.

Also: in the scans I viewed, sometimes parts of pages are obscured or damaged, and I relied on the results of automated optical-character-recognition to do my searches, so I may have missed some things.

I also was just doing a naive search for the word “tax” to find mentions worth investigating.

For this reason, I may have missed references to “contributions to the national treasury” and other such equivalent constructions that don’t use the word “tax.”

The first edition of the Friends Journal is dated , and billed itself as “Successor to The Friend () and Friends Intelligencer ().”

The Philadelphia Yearly Meeting, which had been split into an Orthodox and a Hicksite meeting , had reunified .

The new magazine reflected this merger: The Friend had been the organ of the Orthodox meeting, and the Intelligencer that of the Hicksite meeting.

, the magazine shared offices with the “Friends Peace Committee” of the Philadelphia Yearly Meeting, which may have led to some cross-pollination, and increased coverage for peace testimony concerns in the magazine.

War tax resistance in the Friends Journal in

There are few mentions of war tax resistance in the early issues of Friends Journal.

We have reached the last years of the long decline of war tax resistance in the Society of Friends that began around the time of the American Civil War.

In , the American Friends Service Committee put out an influential booklet, Speak Truth to Power: A Quaker Search for an Alternative to Violence, that mentions war tax resistance only once, in reference to its use by Quakers in (this despite the fact that war tax resisters A.J. Muste and Milton Mayer were part of the committee that wrote the booklet).

The first mention I found comes from the issue.

It is a single-sentence sardonic comment on the tax resistance of conservative Utah governor J. Bracken Lee:

“The Governor of Utah should be welcomed to the ranks of conscientious objectors, even though most Friends and other pacifists would not resist paying income tax on the ground that they were conscientiously opposed to economic aid to other countries.”

The issue mentions a lawsuit filed by Milton Mayer “to recover income tax taken from him forcibly in what he claims was a violation of his conscientious objection to war.”

The three-paragraph article is conspicuous for how much effort it seems to go to to avoid referring to Mayer as a Quaker.

Mayer is “a well-known writer,” a “Carmel, Calif., author, formerly a Chicagoan,” “who writes for leading magazines,” and “has been a lecturer for the American Friends Service Committee and at many colleges, universities and churches,” and “has been a member of the faculties of the University of Chicago and Frankfurt (Germany) and is consultant to the Great Books Foundation.”

All that resume material in the brief article, and yet no mention that he is a Quaker convert.

The article says that “his religious principles will not let him buy guns for other men to shoot” but doesn’t call these Quaker principles or refer to the Quaker peace testimony.

So it makes for a curious article: a respectful nod at war tax resistance with a pained effort to distance the Society of Friends from it.

The issue included a “symposium” on “Investments and Our Peace Testimony” which highlighted the difficulty of finding investments “free of the taint of involvement in war preparation.”

Only one of the participants, Samuel J. Bunting, Jr., explicitly mentions taxation as something that triggers the same concern.

Excerpts:

The problem has worried me ever since World War Ⅰ.

At that time, at the risk of losing a position and the chance of becoming permanently barred from my chosen profession (the investment business), I refused to sell or otherwise handle U.S. Liberty Bonds.

My firm respected my conscientious convictions, however, and the ax did not fall.

Since then I have scrutinized the activities of the corporations whose securities I have considered selling to my clients and have rejected many because of their service in military production.

Yet I still think there is no satisfactory solution of the problem for most of us.

We live in a world geared to military activities.

I see no way of escaping it except by the destruction of militarism itself and by adjudicating differences which might lead to war.

Investments are only a small fraction of the over-all problem.

Payment of taxes is another important aspect of the situation.

It is true that to some extent mortgages could be considered, but, of course, income taxes would have to be paid from the interest.…

The issue included an interesting note about the Quaker outpost of Monteverde, Costa Rica, in the form of a letter from one of the inhabitants there.

Excerpts:

You are so surprised that our group consists of so many North Americans.

The reason that most of them have established themselves in Costa Rica is not the climate, nor the possibility of finding work here, but rather an idealistic reason, typical of Quakers.

They were convinced that it was against their conscience to continue living in a country where, indirectly, they had to collaborate in arming the nation for war by means of taxation, and where it is impossible to educate their children according to principles of Quakers.

A few of them spent a year in prison for being conscientious objectors before emigration to Costa Rica.

So finally, a full-throated reference to real live Quakers who have taken action in response to their conscientious objection to paying war taxes.

Perhaps their geographical remove made this feel safer to mention.

Or perhaps the ice that had formed over American Quaker war tax resistance was beginning to crack.

The issue covered the goings-on at the Philadelphia Yearly Meeting earlier that year.

On , according to the article, war tax resistance was discussed:

It will always be unfinished business that Friends’ practice of our testimonies is not consistent with profession.

The discussion centered on the payment of income tax, particularly that portion used for military purposes.

Few present felt it right to refuse to pay, nor yet felt comfortable to pay.

Varied suggestions were presented: Send an accompanying letter expressing one’s feeling about war; live so simply that income is below tax level; make no report, but once a year send a check for nonmilitary purposes; engage in peace walks and other minority demonstrations; follow Jesus’ example of rendering unto Caesar the things that are Caesar’s; beware of taking for granted the evils deplored, such as riding on military planes; associate more closely with the Mennonites, who share Friends’ concerns; rise above one’s own shortcomings through personal devotion; work to unite with all Friends Yearly Meetings in refusal to pay taxes.

Nothing can be done unless there is a willingness to suffer unto death.

The next mention comes from the issue, and shows the cracked ice has begun to melt.

Excerpt:

Meetings [on the West Coast] in general have been reconsidering the meaning of the peace witness.

Newer activities have included… street distribution of a leaflet on tax refusal because of the amount going to arms (write Franklin Zahn, 836 South Hamilton Boulevard, Pomona, California, for samples), and a poster walk in front of the federal tax office on income tax day, …

Franklin Zahn’s name will come up frequently during the years of the thaw and resurgence of war tax resistance in the American Society of Friends.

War tax resistance in the Friends Journal in

By the glacier that had crept over war tax resistance in the Society of Friends for almost a century had started to recede, and you can see evidence of this in issues of the Friends Journal from that year.

The issue mentions the legal case against A.J. Muste based on his tax refusal .

Excerpt:

At a hearing on , A.J. Muste declared that “on grounds of Christian teaching, conviction, and conscience” he could not help to pay for the development of more nuclear arms or hydrogen bombs.

(A follow-up article noted that “The United States Tax Court ruled in that the First Amendment to the Constitution, which assures religious freedom, does not give the conscientious objector immunity from paying taxes which are to be used in part for war or preparation for war.”)

Muste, however, was a Presbyterian, not a Quaker.

It is telling that although there was some latent sympathy for war tax resistance in the Society of Friends at the time, the number of exemplars seemed to still be few.

But that would change.

Here is an article from the issue:

Several Friends have sent letters to the Collector of Internal Revenue, United States Treasury Department, Washington, D.C., declaring they cannot pay taxes for war purposes.

The following letter by Wilmer J. Young of Pendle Hill, Wallingford, Pa., is indicative of the trend and spirit of letters by other Friends, copies of which have been sent to the office of the Friends Journal:

I cannot voluntarily pay taxes which are used to prepare for the destruction of mankind.

For the past twenty-four years I have lived voluntarily on a scale which meant that I was not called upon to pay a tax on income.

In , however, due to unusual circumstances, I am eligible for such payment.

I am sending today checks to various organizations whose object is to encourage a nonviolent approach to the solution of international problems, which will more than cover the amount of my tax.

Taxes for the ordinary expenses of government, schools, roads, proper police activity, etc., I pay cheerfully and gladly.

But modern war has now become so serious a threat to mankind, that I would prefer spending the last years of my life in prison rather than deliberately supporting it.

In the issue, Frances G. Conrow briefly reviewed a seminar on “The Origin, Development, and Significance of Our Quaker Testimonies” that had been led by Clarence E. Pickett, and suggested:

In a world where there is no defense against modern war, there is need as never before for the peace testimony.

Is refusal to pay taxes for support of war effort emerging as a new testimony in support both of purity of purpose in simplicity and as a peace witness?

It goes to show how thorough the glacial forgetting of Quaker war tax resistance had been, that in war tax resistance could be described in a Quaker publication as possibly “emerging as a new testimony.”

(The same issue has an article titled “The Quaker Peace Testimony, : Some Suggestions for Witness and Rededication” that doesn’t mention taxes at all.)

In the issue, in an article on “The Peace Testimony and the Monthly Meeting” by Lawrence McK. Miller, Jr., he wrote:

Pacifist and nonpacifist Friends are also much closer to each other than they care to admit in terms of their personal involvement indirectly in preparation for war.

The tax-refusal cases are making it clear that through our federal taxes we are all contributing to the so-called defense effort.

In many other ways most of us are cooperating, if only in our reluctance to protest.

It is the pacifist in these instances who particularly must act with a sense of regret for the measure of his involvement and with real humility for the compromising position he is in.

Awareness is growing, but still the emphasis seems to be on sad-eyed, shoulder-shrugging regret, rather than resistance.

Tax refusal is largely still seen as something other people do, while Quakers are to just sorrowfully and humbly reflect on their complicity.

On , Robert J. Leach wrote to the magazine about the Geneva (Switzerland) Yearly Meeting and noted that one of the “high points” of the meeting was when an “octogenarian Friend, Elizabeth Blaser, pled with Friends to refuse to pay defense taxes.”

In the same issue where that report appeared, the pseudonymous Quaker history columnist “Now and Then” wrote about the emergence of the Quaker peace testimony in , and concluded by saying:

We may search our hearts to see whether we have allowed this testimony to grow as it should have done in three centuries or even in our own lifetime.

Have we kept abreast “the Truth,” as Friends used to call Quakerism?

Can we be satisfied with the feebleness of our efforts for peace even ?

Are there not too few Friends willing to find for our testimony more radical expression, which, whatever else it may do, will strengthen our own determination not to acquiesce in the trend to war?

Between the Fifth Monarchy rising and the cold war of a nuclear age there is a vast difference.

Should not our peace testimony become correspondingly more aggressive and more inclusive and more costly?

What will we do this anniversary year about civil defense, about biological warfare, about the hidden control by the Pentagon of our minds and property, about taxes that go to war preparation, about the suppression of the truth concerning the risks of nuclear war or even of testing?

The following years would show that many Quakers shared this dissatisfaction with the feeble state of the peace testimony, and that many saw war tax resistance in some form or another to be key to giving that testimony some backbone.

War tax resistance in the Friends Journal in

By , war tax resistance, or at least increased anxiety about paying war taxes, has surfaced in the Society of Friends, and we can see evidence of this in the pages of Friends Journal from .

Groping towards a “peace tax” plan

The war tax resister’s equivalent to the alchemist’s “philosopher’s stone” is the “peace tax” — which is capable of turning the leaden bullets of taxes for war into the golden promise of taxes only for the nice things.

Like the philosopher’s stone, its existence has been theorized a great deal and demonstrated very little.

In , Friends began their search for the legendary beast.

In the issue is a mention that the Peace Committee of the Pacific Yearly Meeting had begun circulating a preliminary plan for something it called a “civilian income tax bill” in order “to sound out the interest of the peace movement before deciding whether to press for legislation, and specifically to get reactions to the stipulation that pacifists taking advantage of paying into the suggested alternative, UNICEF, would be willing to be taxed an extra five per cent.

No other test of religious objection to military defense, such as is presently required of draft age C.O.s is proposed.”

Egbert Hayes of Claremont, California, is given as the contact person for this effort.

A follow-up article in the issue draws the comparison between this effort and the ongoing effort of some of the Amish to win a conscientious objection from the social security system, but notes that “little support has been found [for conscientious objection to military taxation] from the newspaper writers and members of Congress who defended the Amish.”

In reply to the suggestion that conscientious citizens should have a right to “vote with their tax dollars” for alternatives to war, Senator Joseph S. Clark wrote that this “would cause great harm to our country’s fiscal system.”

He may have anticipated that those “voting” in such a way would be much more numerous than the members of small sects or groups, since many who do not think of themselves as pacifists might agree that there is a dangerous disproportion between the national expenditures for military threats and for the winning of world friendship.

Some thought had been given to the possibility that if “civilian” tax payers paid their money to UNICEF, Congress might simply reduce its own $12 million contributions to UNICEF and divert that money back to the non-civilian budget.

Also:

The Claremont bill, better as a proof of sincerity than the questionnaire method used by draft boards (who are no experts in theology), calls for tax payments that are five per cent greater than the computed tax and for publication of names.

The latter we could achieve now without waiting for an act of Congress.

Willingness to take an unpopular stand before one’s community is a surer test of conscience than any judicial inquisition.

And it is exactly the thing needed if we are to influence opinion.

As shown by many cases of war-tax refusers who have had property seized, there may be no real alternative to the payment of a required number of dollars by those of a certain income level.

Some write a protest on their tax returns, but this kind of protest, like the secret ballot, is far from enough.

As John Sykes pointed out in his book on The Quakers: A New Look at Their Place in Society, the prosperity and bourgeois status of the Quakers after their years of persecution silenced them in more ways than one.

And they are not more silenced than thousands of their natural allies, unknown and isolated, having other religious or nontheistic backgrounds.

It is not a Hamlet’s conscience that “makes cowards of us all,” but the structure of society with its oligarchy or power elite controlling most forms of employment and mass media.

The article continues in this vein for a while, explaining why it’s so difficult to stand up and dissent, and how even those who work up the courage to do so are so frequently drowned out, dismissed, or ignored.

[W]hy should not each Meeting, each local peace group, write its own statement, secure signatures from as many sympathizers as possible, and distribute copies?

The actionists do not always take time for reasoning or for a dignified approach that will persuade people to hear their reasons.

But they are right: reasoning is not enough.

It takes the combination of reason and personal courage; it takes individual decisions which do not wait for either our own or enemy governments to disarm.

We can rarely escape taxes, but we can speak.

There was another movement gaining interest in Quaker circles around this time, in which people were voluntarily taxing themselves one or two percent of their incomes and sending this money to the United Nations, which, at that time, was still seen by many people to have potential as a sort of global arbitrator or adjudicator that might “take away the occasion of war” (this in the face of the fact that the U.N. had recently authorized the U.S. war in Korea).

I don’t see much evidence of overlap between the people advocating this and the people rekindling interest in war tax resistance, but the fact that this was in the air probably helped to shape the “peace tax” plans and redirection efforts that followed.

One note in the issue does seem to suggest that war tax redirection was one motivation for people participating in this voluntary U.N. tax project:

An opinion of the legal department of the United Nations has made clear that gifts to the U.N. or to its specialized agencies are not tax-deductible.

Any checks sent directly to the controller of the United Nations should be marked for a specific program to avoid having them go to the general fund of the U.N. and thereby merely reduce the assessments of member governments.

Here’s another note of interest on this topic, from the issue:

The Friends Meeting at Pittsburgh, Pa., has expressed publicly its serious concern for the Amish farmer whose work horses were recently seized by the Internal Revenue Service for nonpayment of social security taxes.

Friends see in this infringement upon an act of conscience a much broader threat against all those who will not cooperate with the government in support of war and preparation for war.

They point to the alternative of voluntary payments to special U.N. funds in addition to income tax payments.

Maurice McCrackin

In , the Presbytery of Cincinnati began defrocking the Reverend Maurice McCrackin, ostensibly because they thought his war tax resistance was unbecoming of a minister (some suspect it was his work against racial segregation that really raised the ire of his foes — his church was the first in Cincinnati to be integrated).

The Friends Journal kept an eye on the case.

In the issue, a contributor notes that the racially-mixed children’s camp “Camp Joy” was having financial difficulty because of the church action against McCracken, the camp’s administrator.

The Camp Joy Committee has this past year purchased a 314-acre farm as a new site since in the Cincinnati Park Board refused to turn on the water at the previous site, which was Park Board property, because of the income-tax stand of two staff members.

It seems unlikely that a regional park board would actually have a policy of refusing to turn on the water for clients who were behind on their federal income taxes, so I’m giving the benefit of the doubt to those who suspect that animosity to his racial integration projects was probably behind the trouble.

The issue noted that “Almost every day brings to the Journal office fresh protests or statements opposing the military venture of the United States in Vietnam.”

One of these came from McCracken:

Copies of an appeal to those who wish to withdraw their support from war (particularly the U.S. war in Vietnam) by refusing to pay all or part of their income taxes or by reducing their incomes to a nontaxable level are available from the No Tax for War in Vietnam Committee, c/o the Reverend Maurice McCrackin, 932 Dayton Street, Cincinnati, Ohio.

Incorporated in the appeal is a statement to which tax-refusers can sign their names and addresses.

Signed statements sent to Maurice McCrackin before the tax deadline will be used by the Committee as the basis for releasing to the press on that day names and addresses of the signers.

The Committee suggests also that copies of the statement be printed in publications, posted on bulletin boards, and read in meetings by those who have signed them.

The issue had a larger article about the Presbytery’s inquisition against McCracken.

Excerpts:

The presbytery has shown inconsistency and indecision… In , after Maurice McCrackin’s release from prison, the presbytery issued a statement of support, saying, “Rev. McCrackin has not broken his ordination vows.

It is not the function of the presbytery to collect taxes, and we find the West Cincinnati-St. Barnabas Church and its pastor are bearing a strong witness to Jesus Christ.”

Maurice McCrackin was tried in a civil trial in , but the charge was not his nonpayment of income tax for the past eleven years.

He was charged only with not answering a summons to come to the Bureau of Internal Revenue.

He was carried into the courtroom because he would not walk, and he would not stand before the judge.

On this charge he served a six-month term at Allenwood Federal Prison.

“All the while our community work was expanding,” he recalled in a sermon on the Sunday before the first hearing of the trial, “cold war tensions were increasing.

Nuclear bombs were fast being stockpiled, and reports were heard of new and deadlier weapons about to be made.

Fresh in my mind were the bombed cities of Hiroshima and Nagasaki.… If churches, settlement houses, schools, if anything were to survive in Cincinnati or anywhere else, something must be done about the armaments race.… I preached about the dangers which the entire world faced.… I was preaching, but what was I doing?

“If I can honestly say that Jesus would support conscription,” he concluded, “throw a hand grenade, or with a flame thrower drive men out of caves to become living torches, if I believe he would release the bomb over Hiroshima or Nagasaki, then I not only have the right to do these things as a Christian; I am even obligated to do them.

But if I believe that Jesus would do none of these things, then I have no choice but to refuse, at whatever personal cost, to support war.”

The charges are:

The Rev. Maurice McCrackin has resisted the ordinances of God, in that upon pretense of Christian liberty he has opposed the civil lawful power, and the lawful exercise of it…

He has published erroneous opinions and maintained practices which are destructive to the external peace and order which Christ hath established in the Church…

He has failed to obey the lawful commands and to be subject to the authority of civil magistrates, [all these actions being]… contrary to the Constitution of the United Presbyterian Church, U.S.A. (Confession of Faith, chapter 20, paragraph 4, and chapter 23, paragraph 4).

Specifications of these charges include the withholding of income tax, the failure to file returns, and advocating that others do the same.

“I felt free,” said Maurice McCrackin, when he was in the grip of the criminal court.

“I could not have walked.

I doubt if my feet would have functioned.

Had I walked I would have felt I was in prison, but in not walking I felt that I was free.… It may be that the authorities will again take possession of my body; but it is my earnest purpose, God being my helper, that no man, no circumstance, no place shall be allowed to take possession of my spirit and my conscience.”

In its issue, Friends Journal reported the Presbytery’s decision to suspend McCracken, and McCracken’s decision to appeal.

A follow-up in the issue noted “the strangeness of a verdict that acquiesces in the motivation of the defendant but in effect finds him ‘guilty’ for failure to test the income tax law in the civil court.

The seeds of the presbytery trial go back three years,” according to Christian Century commentator Virgie Bernhardt, a Quaker, “to reactionary forces stirred up in the community by McCrackin’s integration activities.”

A further follow-up in the issue noted that McCracken’s appeal “to the Permanent Judicial Commission of the United Presbyterian Synod of Ohio” was accepted.

The Commission “rebuked the Cincinnati presbytery for its ‘unduly severe’ judgment and the lack of proof that the minister had disturbed the peace of the Church, as the local presbytery had charged.”

They told the local presbytery to try again.

The following year, in the issue, a brief notice mentions that the United Presbyterian General Assembly approved McCracken’s dismissal, and notes that 28 members of his church have split off from the Presbyterians as a result and have formed a new church under McCracken’s ministry.

It’s hard not to see all of this attention given to an internal battle in another church as a proxy for an anticipated controversy that was just beginning to stir in the Society of Friends.

(McCracken would return to the pages of the Journal to tell his own story in the issue.)

Other war tax resistance mentions

A report on the Switzerland Yearly Meeting in the issue read: “We were stimulated by the call to action and the living witness of several Swiss Friends who regularly refuse to pay their taxes for military expenditure and then bear the consequences.”

The issue includes a letter to the editor from J.H. Davenport in which he writes, “I would be glad if through the Friends Journal it could be made known that some Friends (at least one) regret that some members feel it right to participate in so-called ‘civil defense’ activities, ‘national defense’ contracts, and the payment of income taxes, the major portion of which goes to so-called ‘defense’ activities of the national government, especially when the name of Friends is used as a sort of endorsement.

¶ I have taken the liberty of painting in the word ‘SOME’ in front of the poster that I have been carrying during my lunch hour in front of the New York City Civil Defense headquarters.

The poster now reads, more truthfully, ‘SOME Quakers say No to All War.’…”

The issue has one of the earliest mentions of a Quaker meeting formally encouraging war tax resistance:

Yellow Springs Meeting, Ohio, has been deeply concerned about support of the national defense policy through payment of federal income taxes.

Some of the members have chosen to be conscientious tax refusers.

The following is an excerpt from a statement approved by the Meeting in : “We recognize that payment of federal income tax, like service in the armed forces, is a demand which may properly move Quakers and other responsible citizens to take a position of conscientious objection.

“Provided their action is imbued with a spirit of humble honesty and loving social or religious dedication, we support both those who are conscientiously impelled to pay their taxes in full, and those who undertake conscientious resistance to war taxes.

Such conscientious resistance may take many forms: refusing to pay part or all of the tax, refusing to file a return, working only at a job where no tax is withheld from wages, intentionally keeping one’s income so low that it is not taxable, resisting coercion by tax collectors, courts, and their agents, supporting other resistors and their families, and giving public testimony and witness.

We feel that persons undertaking nonviolent civil disobedience should be prepared to accept the consequences.

“We urge Congress and the President to consider legislation permitting conscientious tax objectors to choose alternative service for that portion of their tax dollars which would otherwise be assigned to military purposes.”

War tax resistance in the Friends Journal in

An odd article leading off the issue begins: “It is timely to remind Friends that during the first third of our almost three centuries in America Friends did not pay taxes; nor were they taxed.”

The author, Godfrey Klinger, quotes a historian about the aversion of the settlers in Pennsylvania — both the Quakers and the later Dutch and Germans — to being taxed.

But Klinger seems to me to be sort of dancing around the topic of Quakers and their proper response to war taxes without ever mentioning it directly.

His concluding paragraph says:

It was only after the Quakers in the [Pennsylvania colonial] Assembly permitted themselves to be influenced by the dire predictions of the warmongers, whose real aim was to rob the Indians of their land, that taxes and conscription were imposed and much-needed capital wasted on the tools of war, a crime which, in the next two hundred years, was to reach today’s proportions of half of every man’s labor and self-respect.

In the same issue, Guy W. Solt penned an article on “Friends and Their Money” in which he asked “whether there is virtue in accumulating more money than we expect to use in our lifetime.”

Among the reasons he thinks Quakers should find wealth-accumulation to be suspect is this:

Federal and state taxes consume a large portion of our income.

In general, the more wealth we have, the more taxes we pay.

The portion of our federal taxes used for military purposes is 80 per cent, or more.

This portion is very problematic for some Friends who oppose militarism, because if they refuse to pay the portion of federal taxes used for military purposes, they may be penalized and pay far more than the regular tax.

Some Friends resent taxes because of government waste.

Regardless of our attitude toward taxes, the fact remains that Friends are responsible for a part of their tax problem if they retain more money than is needed during their lifetime.

We pay taxes on the value of our property in addition to the income from it.

An opening editorial in the issue on the subject of “Direct Action,” asked, in passing: “Does the refusal to pay taxes still deserve the name of direct action when the objector has a bank deposit waiting to be confiscated?”

A later article in the same issue, on the subject of peace activists in England, noted: “Tax refusal is difficult for us, for, if we earn, we have tax deducted before we are paid.

Some of us asked to be transferred to another schedule so that we might withhold tax and send the equivalent to the World Health Organization or another good cause, but we were informed that this was not permitted.”

A report in the issue on the “round tables” that had taken place at the Friends General Conference in New Jersey , mentioned a round table discussion on “The Visible Witness: Friends and Direct-Action Projects” at which it was noted that “Avoiding a martyr complex is important.

Vigils and tax refusals as the most conspicuous witness were discussed.”

All of these mentions are conspicuously incidental: brief surfacings of war tax resistance in the context of a discussion of something else.

In “ ‘A Place to Stand In’ ” in the issue, Mildred Binns Young cast a suspicious eye on the middle-class ordinariness of the current Society of Friends, when contrasted to the crucible of sufferings in which the Society had been born.

“If friends are now indistinguishable [from any other class of quiet, honorable, successful, comfortable, and useful citizens], is it because all the causes for which we had to stand have been won, as the right to silent worship or the right to affirm in court have been won?”

Indeed not, she says — “we are living in a time when things are as wrong as they were when Christians were being thrown to lions, and as wrong as they were when Friends for years together were lying by hundreds in filthy dungeons.

Where now are the Christians, and where the Friends, prepared to suffer in resistance to these wrongs rather than to acquiesce in them?”

Specifically:

Where are the Friends who refuse to pay the taxes that go to build the armaments we abhor, as early Friends refused to pay the tithes that supported an ecclesiastical establishment they abhorred?

A few Friends do refuse, mostly Friends with such small taxes to pay that the government can afford to ignore them; and many Friends pay the taxes, but with sorrow.

Recently I saw a letter from a young man who had served a prison term for refusing to register for the draft after the Second World War.

He had chosen his present job with great care, putting aside more lucrative offers to keep as free as possible from war-making.

But his letter says wryly: “I have just solemnized my contract to give the government $600 toward war-making.”

He meant he had just signed and filed his income tax report.

What if all the young Quaker heads of families in America had been refusing to file for this tax?

What if all the older, even the wealthiest, Quaker heads of families had been refusing it?

What if we had been prepared, as the early Friends were, to pool resources in order to take care of the families of men who lost their jobs or their land, or were imprisoned?

Friends never have failed to make it clear that, officially and as a body, they refuse to recognize war or other violence as a legitimate means of settling disputes among nations or individuals.

But what about our tacit consent to an economic system that thrives on war preparation and has not learned to exist without it?

What about our easygoing participation in — nay, our prosperity within — an economic system that, to hold its own, trades in death, manufacturing the capability to destroy all that we love, and brandishing this capability of destruction as irresponsibly as a boy brandishes a stick with a nail in it?

Granted that there no longer exists any way to refuse all complicity in this system and continue to live, how often do we consider accepting only simple subsistence from it — laying up no treasure from it, refusing to operate in it to our own advantage?

As long as we are living well on it, we are not likely to be fully committed to changing it; we talk of peace, and sometimes we talk hopefully of it, while we know that peace is no lid that can be applied over a seething volcano, no plaster to lay over a festering abscess.

And with this, no longer was the coverage of war tax resistance in the Friends Journal the sympathetic coverage of fringe (and largely non-Quaker) activists, or the solemn and sorrowful contemplation of taxpayer complicity.

The gauntlet has been thrown, and now Quakers need to declare where they stand and what they plan to do about it.

(It’s worth noting that Young was on the Board of Managers of the Friends Journal at the time, and so was well-positioned to light a fire under its coverage of, and practice of, confrontational Quaker activism.)

Baltimore Yearly Meetings

The Baltimore Yearly Meetings seem to have had a burst of interest in war tax resistance around this time, and an article in the issue gives the credit to “Mildred Binns Young’s lecture” (which I believe the just-quoted article above was based on).

One “concern” expressed at the Joint Meetings for Business of the Baltimore Yearly Meetings in “advised all member Monthly Meetings to consider the responsibilities of Friends in paying or refusing to pay their taxes, now that much of our government’s funds is spent on violence, and to consider the Meeting’s possible response to the needs of Friends and their families if individuals conscientiously refuse to pay.”

The issue reported the results of a survey of 350 adult members of the Baltimore Yearly Meetings concerning the peace testimony, and bemoaned “the lack of responsible feeling about personal financial policy, something that it would seem most persons could consider with little extra effort.”

Less than 60 per cent would refuse to invest in arms production.

Only a little over half would prefer their tax money to be used for nonmilitary purposes.

Only two or three would go so far as to undertake the difficult course of refusing tax payment on this account.

It is encouraging that not far from half would be willing to tax themselves in some degree for support of the United Nations.

(This has been a growing concern, judging by the increase in such contributions.)

Drifting a bit from to keep this line of thought intact, I find in a future issue a calendar notice for a “Open panel discussion on tax refusal… sponsored by Baltimore Yearly Meetings Joint Peace Committee” featuring the speakers “Jesse Yaukey, Lawrence Scott, and Oliver Stone.”

Remembering Quaker history

In the issue, LaVerne Hill Forbush looked back at “Suffering of Friends in Maryland, ” and noted that there were 296 cases of Friends suffering fines in one region, 34 “for refusal to pay priest’s wages, [but] the greater number of fines had to do with military assessments, under such headings as refusal to go to war, refusal to muster, refusal to sign association papers or join the militia.

War taxes were doubled or trebled when Friends refused to pay them.”

In the article that recounted the results of the survey of Baltimore Yearly Meetings members, the author spent some time recounting how the Baltimore Yearly Meeting had coped with these issues in the distant past:

In Baltimore Yearly Meeting added to the Queries: ‘Do you bear a faithful testimony against bearing arms, military services, or contributing to the support of war?’ (italics ours).

In the Yearly Meeting recorded: “Most Friends appear to be careful in maintaining our testimony against war by refusing the payment of taxes.”

War tax resistance in the Friends Journal in

Issues of the Friends Journal from give some additional hints of the reemergence of war tax resistance as a widespread practice in the Society of Friends… and also the first example of the backlash against it.

The lead editorial in the issue concerned “Taxes for War” and covered the war tax resistance of Quakers in England.

The article begins: “Friends in England are under the weight of the same concern that occupies American Friends: what can, or should, we do about taxation for military purposes?”

…short of outright refusal to pay taxes there seems no way out for those objecting to militarism.

The voluntary payments to U.N. funds, such as various Friends groups are making, will undoubtedly contribute to easing the moral burden, yet these sensitive donors would be the last ones to claim that their voluntary self-tax is a satisfactory solution to the problem.

The editorial then describes a quirk of British tax law by which if a taxpayer there “ ‘covenants’ a certain annual amount to a charity for seven years, the Internal Revenue will then, as The Friend (London) reports, pay over to the charitable organization ‘a sum equal to the tax normally payable on the amount of the covenant.’

The ‘charity,’ then, receives not only the contribution but also the tax paid upon it.

On the average a subscriber to a charity will have to pledge one half of his normal tax payment in order to recover that proportion usually allocated to armaments.”

While “far from flawless” and while “this plan exists only in England,” this plan “nevertheless affords some moral relief,” the editorial states.

This is the first in-depth discussion of a practical war tax resistance method in the pages of the Friends Journal, but it is only “practical” to most of its readers in the abstract — as something Friends in the old country might do.

As with the Journal’s earlier coverage of Quaker war tax resisters in Costa Rica, or of war tax resisters Milton Mayer, A.J. Muste, and Maurice McCracken, the magazine still seems most comfortable when talking about war tax resistance as something that other people do and American Quakers admire.

The article can be seen as a hunt for an excuse: “If only we had a law like the British do, we could resist our war taxes… maybe some day we will have one, perhaps we can even advocate for one, but until then there’s nothing we can do.”

Another example of the “there’s nothing we can do” point of view, in the same issue of the Journal, comes in a report on the Philadelphia Yearly Meeting, whose sessions were held :

Our sympathy was aroused for businessmen and taxpayers trapped in the war system and, recognizing our common sense of guilt, we acknowledged the fact that all enterprise is thus enmeshed.

The next paragraph begins “We were encouraged to break out of this trap…” but no mention of resisting war taxes follows.

The issue includes an article about the United Nations that includes this observation about those countries, like the U.S.S.R., that “have refused to contribute to U.N. projects of which they disapprove”:

There is a puzzling similarity between the attitude of these countries toward the U.N. budget and the attitude of those pacifists who refuse to pay income tax because they disapprove of some of the projects of the United States Government.

Note: “those pacifists” and not “those Friends” or “those Quakers.”

Again, there’s deniability about whether Quakers are the sort of people who do this sort of thing.

But here is a letter-to-the-editor, from Wilmer J. Young of Wallingford, Pennsylvania, that shows how war tax resistance was beginning to reawaken in the Society:

The following letter, signed by Clarence Pickett and Henry Cadbury, was sent to about twenty persons:

Dear Friend:

Many Friends have for years felt uneasy about paying that part of their income tax which goes into preparation for war.

A very few have refused to pay; but the majority of Friends have felt this to be an ineffective way to protest, or they have felt for various other reasons that this was not the way for them to bear witness for peace.

At the same time, many of them have been unhappy at not bearing a clear witness in this regard.

The signers of this letter invite thee to attend a meeting of a small group of Friends who feel concern in this matter.

We hope to discuss whether there is some action (perhaps not in violation of any law) which would be a clear indication of our position on war preparation, and might have some meaning both to the participants themselves, on one side, and to the general public, on the other.

Our consideration will of course be looking toward next year, as it is already too late for this.

Most of those invited to this meeting attended it.

There was an earnest and searching discussion for two hours.

However, no consensus appeared and no action was taken.

Some of us who are clear that we cannot pay this tax can but wonder whether it is weak intelligence or misguided conscience that has led us to our decision.

The issue included a report on “The Peace and Social Order Committee of the Young Friends Committee of North America,” which

…concerned that many Friends have lost the meaning of the peace testimony, organized a peace caravan this summer.

The seven Young Friends who joined in this Peace Caravan traveled in the Middle West asking Friends: “What does the Peace Testimony mean?

Is it relevant to our personal lives and our national policies?

If so, what is required of us?”

The article suggested some “Queries” that could be used to delve into questions like these, including this one: “Do we consider Christ’s teachings to love our enemies and do good to those who persecute us when we make decisions about our attitude toward military training and taxation for war?”

The same issue of the Journal contains the first example of backlash against war tax resistance I found in that magazine — a letter to the editor by Harold H. Perry in which he says that tax resisters are “by implication” showing a lack of support for all the good things the government does: not just the usual list of roads, schools, and the like, but even “many and considerable civilian services of the military establishments such as the work of the Corps of Engineers and much of the research that aids civilians, including medical and health benefits.”

He acknowledges that some resisters redirect their taxes to things of less-questionable benefit, but says that “[t]his may be laudable theoretically, but if widely practiced or permitted would lead to endless confusion, imbalance, and injustice.”

He concludes by encouraging Quakers to instead “work through established democratic machinery” to try to get their ideals reflected in government behavior.

A friend of mine, 43 year old Arthur Evans, a medical doctor with offices in Denver, Colorado, was sent to jail by Judge Alfred A. Arraj of the Denver district court, for his refusal to pay his part of the income tax (about 50 pct.) which would be used for the annihilation of the human race.

He sent it, instead, to the United Nations, to promote peace in the world.

In a statement circulated by him to his friends he says in part: “My lawyer, the judge, and other lawyers, tell me that there is no law, no constitutional provision that provides for the individual to refuse to pay taxes for annihilation.

So I go to jail, for I will not, I cannot in conscience be party to financing the means to annihilation.

The Jews under Hitler were taxed to buy their crematoriums. The same happens here — but it is not only the Jews who finance their means of destruction — it is almost every income earner in the United States.

This is called democratic because we are all taxed alike.”

Letters of approval have been pouring in to Dr. Evans, and since he is only allowed to write very few, his mother in Philadelphia has taken up the task of acknowledging them, sending at the same time a typewritten sheet explaining the affair in detail.

A little over a century ago, in , another man (who is now considered one of America’s greatest) was picked up in Concord, Mass. on the way to his shoemaker, and brought to jail because he had refused to pay his poll tax to a government he thought misguided and evil because it allowed slavery and was also at that time waging a war with Mexico to extend its slaveholding territory.

I mean, of course, Henry David Thoreau.

Out of that incident came his famous Civil Disobedience, which influenced Gandhi and Nehru; Thoreau’s ideas are very much alive in many parts of the globe today.

Strange, how history repeats itself!

Some day, perhaps after another century (if we escape a war of annihilation), Dr. Evans will be spoken of with appreciation and respect.

We have a way of crucifying the great while they are with us, and of exalting them after they are gone.

At present a medical doctor is doing laundry duty as a “trusty” in the Jefferson County Jail in Golden, Colorado, and he may like to hear from you.

How would the Friends Journal cover this?

Would it, as in the earlier case of Milton Mayer (see ♇ 5 July 2013), mention it but try to downplay its connection to Quaker practice?

Let’s see.

In the issue is a three-paragraph piece in the “Friends and Their Friends” section on the case:

Arthur Evans, Denver physician and member of the Society of Friends, went to jail on for three months because he has refused to pay part of his federal income taxes and because he would not produce his financial records.

For at least twenty years the doctor has paid to Internal Revenue Service only the proportion of his income tax which corresponds to the percentage of the national budget devoted to non-military purposes.

The part he has not paid to IRS he has devoted to charitable purposes and to agencies working for world peace.

Not until , when he declined to file an income tax return, has he been personally pursued by IRS, which heretofore had subtracted from his bank account amounts he was refusing to pay.

So the magazine is forthrightly recognizing this tax resister as one of its own flock, though its coverage is considerably more subdued than even the example from the mainstream media that I quoted above.

(Incidentally, if the Journal article is accurate and Evans was resisting as early as , this would put his resistance well in advance of that of the Peacemakers of , which I usually think of as the birth of modern American war tax resistance.)

The Evans case got another mention , in the issue, which reprinted excerpts from his letter to the Director of Internal Revenue (and which also explicitly identifies Evans as “a Friend”).

“We doctors have pledged to serve life,” Evans wrote:

I find no way to finance mass murder — be it called war, defense, or security — and be true to this pledge.

I care about life and the dignity of each individual, and desire to serve people everywhere, no matter who they are religiously, nationally, or racially.…

I cannot voluntarily fund that overwhelming part of my nation’s budget that finances acts based on retaliation, based on fear and hatred psychology, based on threats of injury and killing-in short, acts based on returning evil for evil.…

If this results in my going to jail for breaking laws that support injustice, slavery, death, and destruction, then in jail, with Martin Luther King, Henry David Thoreau, Peter, and Paul, I will attempt to serve wherein I can.…

“Thou shalt not kill” and “Thou shalt love thy neighbor [which includes thy enemy] as thyself” are precious laws of life to doctors and to all who would cooperate with the Christ.… Many men still believe… that they can deal with the evil acts of men by destroying the men who do these acts.

Yet I know no one who believes that conflicts… are resolved by mass murder.… The majority have not yet discovered that love is the only power that overcomes evil.…

I will continue to pay that percent of my tax liability that goes for nonmilitary acts of my government and enclose $200 toward same.

I am sending double the amount I am not paying for war to Quaker House at the United Nations for transmission to the United Nations Organization for its technical assistance program.

War tax resistance in the Friends Journal in

In the simmering issue of war tax resistance

begins to hit the boiling point in the pages of the

Friends Journal.

“Taxes for Violence”

In the issue appeared a brief

article by Alfred Andersen entitled “Taxes for Violence.” While Mildred Binns

Young’s article on revitalizing the Quaker peace testimony back in

(see

♇ 9 July 2013) had suggested war tax

resistance in the course of its larger argument, Andersen’s article was the

first one that was both devoted to the subject of war tax resistance and that

unmistakably recommended it to Quakers:

Friends have become increasingly concerned about paying taxes which finance

war. Some reasons for this are:

The Federal Income Tax provides 75 per cent of the money by which the

military is financed.

Yet there is no provision for conscientious objection to paying taxes, as

there is for conscientious objection to serving in the armed forces. It

is obvious that such a provision would be the equivalent of the existing

provision for alternative service for

C.O.s.

Many Friends took the conscientious-objector position regarding military

services when younger; now, in paying taxes, they are serving the

military in a more fundamental, though less obvious, way.

It is inconsistent for them to encourage young people to refuse military

service while they themselves continue to “serve” in this way.

Those who have merely sent the Internal Revenue a note of protest along

with their tax checks are coming to realize that integrity requires that

they follow protest with action.

Those who have withheld part of their payment in protest are becoming

aware (a) that what they do send is used for military purposes in the

same proportion as all the rest, and (b) that because they indicate to

the government the amount that they have withheld, the Bureau simply

collects it by distraint and adds interest!

Therefore, some Friends are increasingly clear that the thing wrong with

the tax law is its lack of provision for conscientious objection; nothing

short of noncooperation with the tax law itself (i.e.,

refusing to file a return until the defect is remedied) will meet the

moral challenge before us.

True democracy requires that all Federal laws provide for conscientious

objection.

All Friends have observed, and many have helped encourage, the successes

of civil disobedience to laws discriminating against Negroes. Therefore,

they feel encouraged to challenge other injustices with nonviolent

resistance. Forcing persons to finance nuclear weapons makes them

perpetrators of in justice toward all living creatures on the earth, both

in our generation and in generations to come.

Therefore, we should expect that more and more Friends will refuse to file

income tax returns until our government gives reliable assurance that

whatever money is paid will not be used for those purposes which our

consciences clearly tell us are out of moral bounds for us. As these refusals

increase, we may expect that others will join the movement, affirming that

where conscience and law conflict, conscience shall prevail.

As you can see, this not only advocated war tax resistance, but also tried to

shut the door on many perennially popular half-way measures of tax resistance

such as paying under protest or withholding a symbolic amount of

taxes — claiming that “nothing short of [total] noncooperation… will meet the

moral challenge before us.”

Several letters-to-the-editor, found in the , ,

, and issues, addressed Andersen’s argument:

Hanna Newcombe wrote about how the Canadian Yearly Meeting had been

struggling with the issue. At first, she writes, they tried to lobby the

government for “a tax law… which will channel our tax money into

nonmilitary uses,” but then they “came to the conclusion that it would not

do… since they would then simply readjust their books to use someone

else’s taxes for military purposes only, and nothing would have been

achieved.” They then adjusted their goal to be one in which taxpayers

could choose to divert their money from the national government and into

“non-governmental peace-directed activities.” Finally, “[i]n order to show

the seriousness of our purpose and the intensity of our feeling, we

offered to match the diverted amount from our own pockets, so that

essentially we, as conscientious tax-objectors, were petitioning the

government to increase our taxes!”

J. Passmore Elkinton wrote in to advance the subtle argument that because

tax money is legally owned by the government, and not the taxpayer, the

taxpayer has no moral responsibility for deciding what to do with it,

aside from the ordinary legal processes of trying to influence the

government in its decision-making. The conscription of money is not

analogous to the conscription of people, Elkinton argued, since the

ownership of money is a function of government policy to begin with, while

the ownership of one’s body is inalienable.

Daniel Smiley, while expressing sympathy for Andersen’s position, and

while claiming to be “against paying taxes for military purposes, past or

future,” says that he has not refused to pay his income taxes because

there are so many other taxes that also support war and that are embedded

invisibly in every economic action — even something like buying a loaf of

bread. If you cannot completely avoid paying war taxes (“we would have to

remove ourselves completely from the economy of our country… by becoming

hermits”), he thinks, there’s no reason to bother refusing to pay some

particular tax. Besides, if we were to redirect our income taxes to, say,

the Peace Corps, wouldn’t our contributions just end up getting replaced

by those of taxpayers who don’t share our concerns?

A later letter by Thurston C. Hughes makes almost the same argument,

even going so far as to say that the Quakers who emigrated to Costa

Rica so as not to continue paying taxes to the

U.S.

government (see ♇ 5 July 2013)

were making a vain gesture, as they still pay taxes for the police

force there, and pay taxes on any imported goods they purchase!

Lee Maria Kleiss wrote in about the compromise she had come to — refusing

to pay 55% of whatever small amount she still owed at filing time, as a

protest, and then writing to the tax collector and her political

representatives to ask them to enact some alternative for conscientious

objectors to military taxation. “Certainly some protest concerning the

inconsistency of paying for war — and especially paying to have somebody

else do a dirty job that we refuse to do — should periodically be

expressed.”

Samuel Cooper (there’s more about him below) wrote in to say that his war

tax resistance grew out of his experience as an imprisoned conscientious

objector during World War Ⅱ. “My wife and I have tried several means of

protest and withholding; latterly we have resolved the problem by living

within the non-tax income bracket.” He suggests this approach as a tenth

item for Andersen’s manifesto.

Finally, Andersen writes a response to some of the letters mentioned

above. I particularly liked his answer to Hanna Newcombe’s letter about her

Meeting’s attempt to gain a legal method for taxpayers to stop funding war

this way: “I suspect that it is only as we first commit ourselves to

stop supporting what we clearly see to be wrong, thus living up

to the moral insight we now have, that we shall be worthy of more.”

Andersen, by the way, certainly practiced what he preached. In the

issue of the

Journal is a brief note about the

IRS

seizure and auction of his home (the

IRS

got $1,500 for the property; the Andersens owed $36,000). The note

concludes: “The Andersens [Alfred and Connie] have refused to file an income

tax return for more than twenty years.”

Samuel Cooper

I’m going to deviate from my chronological system here a bit so that I can

follow the trail set down by Samuel Cooper, who wrote letters to the editor of

the Journal promoting war tax resistance:

There’s the letter I mentioned above, from

, in which he responds sympathetically to

Andersen’s argument and notes that he and his wife are practicing

low-income/simple-living tax resistance.

In , he wrote in with disappointment

over “how few Friends have refrained from payment of income taxes, knowing

that a large portion goes for past wars and preparation for future ones!”

He noted that Quakers in John Woolman’s time “suffered ‘distraint’ of

goods, rather than willing payment for war.”

In Samuel and Clarissa Cooper wrote to

ask “what should Friends do” about “income taxes and the 51 per cent of

the budget allocated to the military.”

Should Friends now stand by in acquiescence, letting a few others take

the risks of civil disobedience and possible imprisonment? One can bear

testimony, even refusing to pay part or all of the tax. If the Society of

Friends were to unite on this aspect of our peace testimony — to take a

stand not to support war any more — what might the influence and result be?

In he wrote in again:

I have been witnessing for more than twenty-five years against the payment

of part or all of the tax levied against my income. I do not presume that it

has hindered the war program by one iota, but it has said no to war

after I said no to conscription and served a time in prison. I

believe there is a real relevance, although all one’s assets are involved in

our economy. Simply buying one’s food is supporting, through hidden taxes,

the war effort. If one is working for money, then time is a

contributing factor.

There is no satisfactory way to be consistent for peace and against violence.

Our Quaker peace testimony can only be resurrected — from near death by

inaction — by corporate action, standing together instead of quibbling over

methods, expediency, and results.

Let the light of Christ shine in your heart to show the true way acceptable

to the Prince of Peace.

Also in , he wrote in about socially

responsible investing, noting that this isn’t just a matter of avoiding

stocks “in the military-industrial complex and its subcontractors” but

that because some “businesses pay nearly as much in Federal taxes as they

do to their stockholders… [they contribute] indirectly toward military

procurement.” He recommends investing in low-income housing.

In , Cooper addresses a number of points

related to war tax resistance:

“It is not the amount of money… but the principle — whether one feels

easy to support the war-minded Government…”

“[V]oluntarily living below the taxable income” is one way to

“avoid the issue” — another is to “scrutinize very critically the source

of that income.”

He says that a response to people who accuse tax resisters of not

supporting Government is that even tax resisters pay “hidden taxes in

most things we buy.”

He recommends some less-offensive investments: municipal bonds, and

bonds for “college, hospital, rest homes and such” that “yield good

income and help humanity instead of destroying.”

In , Cooper returned with a letter about

the 1,000-person-strong peace walk and vigil that accompanied the

Philadelphia Yearly Meeting . “Does

this ‘witness’ satisfy our Peace Testimony for a year? What do we

do now?” He recommends phone tax resistance as something Friends

can do to make their testimony continue through the year.

Miscellany

In the issue, Robert

Horton briefly reflected on

the voyage of the

Phoenix, a small ship that tried to interfere

with nuclear weapons testing at sea. In the course of this, he asked this

series of rhetorical questions:

“Why does one do what he doesn’t have to do?” Why did Thoreau refuse to pay

taxes and why did he write Civil Disobedience? Why

did Columbus sail an uncharted ocean? Why did Kagawa of Japan go to live in

the slums? Why did my young neighbor, married and with three children, refuse

to pay taxes for war? None of these heroic souls could see the eventual

result of their actions; there was no guarantee to them that their actions

would be effective in changing social patterns. They were true to the Inner

Light and left the result in the hands of God.

But [particular] interest to Friends is his objection to at least one half of

what is collected [by the Internal Revenue Service] being used to prepare for

the destruction of the world as we know it. He recounts the experience of a

few tax refusers whose action meets with his approval; a number of others

equally dramatic are well known to Friends. Since the great debate is going

on in the minds of many Friends and others as to effect on our society, our

times, and on us as individuals of our promoting the peace testimony on one

hand and paying for world destruction on the other, this book will at least

help clarify the issue, even though it will not contribute to peace of mind.

War tax resistance in the Friends Journal in

Three people dominated the meager Friends Journal

coverage of war tax resistance in : Johan

Eliot, Margaret Dungan, and Gordon Christiansen.

Johan Eliot

Eliot, “a member of Ann Arbor

(Mich.) Meeting,” says the

issue, “has received a

considerable amount of newspaper and radio publicity recently because of his

refusal to pay the balance of his income tax

on the ground that the major portion of his tax money goes for armaments which

threaten the world. According to an Associated Press dispatch he decided to

make this protest after

U.S. planes began

their raids on North Vietnam.”

This prompted the Journal to publish a more in-depth

explanation, penned by Eliot’s wife Francis, in its

issue. Excerpts:

The concerns of many Friends about war taxes, expressed from time to time in

letters to the Journal; the Yellow Springs (Ohio)

Meeting’s Discipline on Friends and Taxes; the Bill for a Civilian Income

Tax Fund proposed by Pacific Yearly Meeting; the historical material prepared

by Franklin Zahn of Claremont (Calif.) Meeting; The Catholic Worker and its