Then Thomas S.

Bell moved to amend the proposed section by inserting the following:

Those who conscientiously scruple to bear arms shall not be compelled to do so, nor shall they be compelled to pay an equivalent therefor, except in times of exigency, or war.

This was that compromise that would have freed conscientious objectors from militia service or militia exemption fines — except when such things would be most directly and immediately related to war and bloodshed, that is, except when their consciences would be most likely to be repulsed.

Here’s how

Bell defended this strange proposal:

Mr.

Bell of Chester said that it was with reluctance he rose to renew the consideration of this important,

though vexed question.

But representing as he did a large class of persons who were deeply interested in its fate, he deemed it to be his duty seriously

to discuss the subject, and to ask for it a fair, candid, and impartial examination.

It was now fairly before the committee.

So prominently had it presented itself to the attention of this body that the consideration of it had been anticipated.

It had been incidentally discussed — when other

questions were more immediately under consideration.

Every gentleman had then felt sooner or later he should have to meet it, discuss it, and decide upon

it.

It was a question of vast magnitude, as it affected rights immeasurable, except by that standard which is implanted in the breast of man by the

Creator: rights, not merely civil and political, but resulting from that allegiance which is due from humanity to God.

Regarding it in this point of

view, he would ask whether it ought not to be approached solemnly, and whether we should not cast away all prejudices, and eschew all passions and everything calculated to mislead the understanding?

Whether we were not to

look at the question, no matter what had been said on the subject, fairly and honestly, and in the hope of at least coming to a righteous judgment?

Such prejudices, he was aware he would have to encounter. Such prejudices — if

he was correct in applying them, — but perhaps it was too harsh a one; and

if so, he begged pardon of the committee. However, to use the word in its

mildest sense, he would say that prejudices were held by some of the members

of this committee, resulting either from education, or their habits and

morals, and which made it difficult for them to appreciate the sentiments of

those who were conscientiously scrupulous against bearing arms at any time.

What, he would enquire, was the question? It was simply this: Whether those

forming a part and parcel of the people of Pennsylvania who entertain

religious scruples against bearing arms should be placed on an equality with

our fellow citizens, who do not? We had heard something here relative to

privileged classes, and it had been intimated that the memorialists asked

for privileges and to be placed above the mass of their fellow citizens.

This is not the fact. The Friends sought only to be put on the same terms as

other persons of the community. Why did he say so? Because by the fundamental

law of Pennsylvania, as it exists, the religious scruples of all men were

respected, except in reference to the defense of the State. If gentlemen

would refer to the Bill of Rights, they would find that such was the fact. He

considered that those who had memorialized us had made nothing more than a

reasonable request. They wished to be protected equally with the rest of

their fellow citizens. Nor was this peculiar scruple relative to bearing arms

confined to one class of religionists. It had been asserted in the course of

the discussion that the large and respectable Society of Friends were the

only body that was demanding the right which they claimed. This was not the

fact, for a large society called Mennonists also asked it. The amendment now

on the table embraced all classes of men, all sects, all religious

denominations. It extended protection to the whole community. Besides those

two societies which he had named as claiming this right, there were many

others. There was a large number of people in Lancaster and other places who

entertained conscientious scruples against bearing arms. A class existed,

calling themselves German and United Brethren, which would rather surrender

all their worldly wealth than give up their notions in respect to bearing

arms. He did not in the least object to the wide scope of the amendment. He

much preferred it in its present shape than if it were less general in its

character.

What did we ask? He said we, because he felt the honor of standing

on this floor as the advocate of the memorialists; not that he entertained

the scruples which they did. What, then, he repeated, did we ask?

Liberty — religious liberty — liberty of conscience. Nothing more than this. — Freedom

of conscience — to pursue the dictates of our hearts, with a religious

intent — to worship God in our own way. We asked to be placed on the same

foundation as we are in regard to liberty of speech — to the right of

acquiring property and to the right of pursuing our own happiness — all which

rights are secured to us by the Constitution of Pennsylvania. He would repeat

that the memorialists asked nothing more. The right of conscience was of more

importance than any other which he had mentioned, because the latter sprung

from the institutions of society, whilst the former originated from the

connection which exists between the Deity and man.

And shall this protection, asked for in this enlightened age, be refused on

the ground that the feeling which originated the request is not entertained

by the whole community? A meritorious, well-deserving, and highly respectable

portion of the people had asked for it, and why should we not grant them it?

It had been said that this was a right subordinate to the right of

self-defense, — an indefeasible right as it had been called by the gentleman

from the city of Philadelphia. It is implanted in the very nature of man, and

accordingly we were struggling for this right from the first dawn of

religious liberty. Yes, whenever and wherever a ray of light had succeeded

the gloom which had overshadowed the world — men had yielded up their lives

in thousands as martyrs in the cause of religious liberty. History was full

of examples of the obstinate firmness with which men had fought for this

natural right. Look to France — to the Waldenses and the Huguenot, who turned

every house into a fortress, and every site into a battle field. In Ireland,

the best blood had been poured out like water in the sacred cause. It had

every where crimsoned the green fields of the Emerald Isle. In England, the

martyr had yielded up his life at the stake rather than surrender his

religious belief. In Scotland, the Presbyterians waged an obstinate and

exterminating war in defense of their creed and to free themselves of the

fetters which their English neighbors sought to bind upon them. Men there

fled from their homes, deserted the cottages of their affections, and

abandoned the protection of an organized government, because that protection

was accompanied by the assertion of a right to control the conscience of the

subject. All this was overwhelming proof that religious liberty was felt to

be dearer than life, and would only be surrendered with it. But among the

great illustrations of this truth might be instanced the facts attending the

first settlement of Northern America. Under the most discouraging

circumstances, thousands who had partaken of the advantages of civilization

left the land of their fathers, and abandoning the luxuries of polished life,

withdrew from the baleful shade of an oppressive government to seek a howling

wilderness and such safety as they might find at the hand of the rude savage,

rather than endure the desecration of a right which they insisted on as

sacred. Among the glories of the early history of the liberties of this

country was that here freedom of conscience was first proclaimed as among the

fundamental principles of its governments. In the reign of Charles

Ⅱ of England, Roger Williams, actuated by a

liberality of feeling in advance of the age, and which sheds lustre on his

memory, established religious liberty as one of the prominent characteristics

of the government he founded.

The memorialists asked for no privilege — no franchise — as had been alleged.

They demanded but a bare right, the possession of which their great leader — the

founder of this Commonwealth — had guaranteed to them. If they were here

importuning for the grant of an exclusive privilege, for something not

possessed by other citizens, he would be the last man to stand here as their

advocate; but they desired nothing more than the introduction of a clause to

some extent prohibiting the enactment of laws interfering with the religious

scruples they entertained, and this was nothing more than was already secured

to their fellows. This was asserted as a principle in the Constitution of

, and repeated in the existing Bill of

Rights. It was, perhaps, sufficient merely to call attention to the fact that

from the first settlement of Pennsylvania down to the present moment, it had

been observed as a rule not to be controverted that no law should be made

having the slightest tendency to interfere with or control freedom of

conscience, except in the particular instance of which, as seemed to him, the

memorialists so justly complained.

The principle, he therefore contended, was at the foundation of our

institutions, that there was no power in our government to interfere with the

rights of conscience. If this principle was correct, and none here would deny

it, what was the question for this Convention to decide? Simply this: do any

portion of our fellow citizens entertain conscientious scruples against

performing military duty, or is it merely an affectation of a scruple on

their part to avoid the burden and hazard of bearing arms? When we looked to

this question, we would find that it was one merely of veracity. Were their

professions sincere? Have those who have given us, for so many years, proof

upon proof of their sincerity, and who have suffered themselves, for the sake

of their religious scruples, to be reviled and oppressed, been all this time

practicing deceit? If their scruple was an honest one, they had a right to

maintain it, and we were obliged to secure them in the right by the aid of

the law.

Sir, said Mr.

B. in asking for

the insertion of this protective provision in the Constitution, it is not

necessary that I should refer to the character of the largest society which

claims exemption from military service. If they were here for an exclusive

favor, it might be necessary to speak of their moral and social worth, and

of the great benefits which they had conferred upon Pennsylvania, and the

important part they had acted in the establishment of our free institutions.

It might, too, be necessary to follow them into the friendly and benevolent

circle of their domestic retirement. But it was a right and not a privilege

which they asked, and he, therefore, forbore. Had we any evidence, he asked,

except our own assertions, that they are insincere in the scruples which

they profess to entertain? In the Constitution, as it now stood, there was

at least a practical recognition of the principle for which he contended,

and though it did not go so far as was demanded, yet it furnished a proof

that respect had been paid to the fact that a portion of our fellow citizens

entertained an honest scruple in regard to bearing arms.

It remained to inquire, what was the extent of this scruple. Did it go

beyond mere personal service? If it did, it was entitled to our respectful

consideration. If gentlemen would turn to the memorial, they would find that

their scruples extended to the payment of an equivalent for service, and

they put it on the natural ground that, being averse to war, they were

opposed to the means by which a state of war might be created and

maintained. They asked to be relieved not only from the duty of bearing

arms, but from the equally odious necessity of paying an equivalent for it.

Was it for us to say that this scruple was affected? Should we set up a

standard for other men’s consciences, and pronounce that this or that

scruple of conscience is unreasonable? The members of this religious,

worthy, and respectable society say that they entertain scruples of

conscience equally strong against paying an equivalent as against bearing

arms. Now, the principle which he had before indicated was strong enough to

protect every scruple which might be professed. It extended to one case as

well as to the other. If the scruple was sincere we were bound to recognize

it and protect them in it; and we had no right to pronounce that it is

unreasonable. He might perhaps ask, but he did not do it, that any society

or individual should be exempt under the rights of conscience, in time of

danger and of war, from personal service or the payment of an equivalent.

They had a right to come in and demand this, but that question was

surrounded with so many difficulties that they waived it altogether, and

only asked to be exempted in time of profound peace. But, when the

exigencies of war should require it, they remain like other citizens,

subject to the demand of the government upon them for personal service or

its equivalent. If the question was between convenience and inconvenience,

who would hesitate in his decision? If the question be between right on the

one side and mere inconvenience on the other, would the argument resulting

from inconvenience defeat the prayer of the petitioners, and deprive them of

a right which from the origin of our Constitution had been held sacred?

As to the frauds which were anticipated by some gentlemen, no man would, in

time of peace, resort to fraud for the purpose of procuring an exemption,

and in time of war it would not avail. Then, all classes would be on the

same footing, and be compelled to render personal service or an equivalent.

All they asked was freedom from the burden and vexation of this duty in time

of peace when their exemption could be productive of no ill effects. What

though one half or three-fourths of the people should, in time of peace,

affect a scruple in order to avoid militia training. Would the country lose

any thing by it? What advantage would be derived from the continuance of the

militia trainings, even though every citizen attended them? In time of war

when their services were wanted, there would be no room for fraud or the

allegation of any scruples, — for no one will be exempted, except upon

the payment of an equivalent. This feature was not a novel one in our

Constitution. This was not the only State in the Union which had set an

example of freeing from the burden of militia service, the tender consciences

of their citizens. The Constitution of Vermont, provides that “Quakers and

Shakers, the Judges of the Supreme Judicial Court, and the ministers of the

Gospel,” may be exempted from militia duty. The Constitution of New

Hampshire, says: “No person who is conscientiously scrupulous about the

lawfulness of bearing arms, shall be compelled thereto, provided he will pay

an equivalent.”

We find, therefore, that other States recognize the existence of these

scruples and protect them. Should we then, whose State was founded by this

very sect which demands the exemption, and who see everywhere around them

the evidences of their patriotism and worth, should we be behind others in

maintaining the sacred principle of freedom of conscience, which by this

society was laid at the foundation of our institutions? Should the

proposition which he had offered succeed, any defect which might arise in

its operation might be remedied by the Legislature. If fraudulent evasions

were practiced under it, the law would provide means for their detection and

punishment. Mere inconvenience ought not to be urged as an obstacle to the

adoption of the proposition.

George W.

Woodward then complained that “now we are asked to go further and to exonerate those

professing conscientious scruples, from all military taxation.” Taxation?

I thought it was a fine, not a tax.

This distinction became a battle over framing the debate.

Are Quakers petitioning to be freed from a provision that unfairly fines their conscientious scruples, or are they petitioning to be

given the privilege of a tax break?

Woodward said:

He called it taxation, because it was a mode of compelling men to contribute to public burdens.

Sir, said Mr.

W. I have always been

taught that peace is the time to prepare for war, but how can you prepare for

war without money, which is its sinew? We are called on to exempt a body of

people from the payment of the taxes in a time of peace, which are necessary

not only to prepare for war but to prevent it.

These military fines or taxes, as he called them, went into the Treasury for

the use of the Government, and he was opposed to exempting any class of

citizens from their payment. It seemed to him we should be doing great

injustice to our citizens at large, and violence to our best interests,

should we yield to any class or portion of the people, however respectable,

entire exemption both from military service and its pecuniary equivalent.

During the progress of the debate, we had heard a great deal of the freedom

of conscience. He concurred in all that gentleman had said of the freedom of

conscience and the sacredness of conscience, and he was unwilling in any

manner to interfere with the full enjoyment of his rights of conscience to

which every human being was entitled, but it struck him that the rights of

conscience were well enough secured by the Constitution as it stands, and

that this demand for further provision in behalf of conscience, which the

Friends are now pressing on us as a matter of right — for the

gentleman from Chester demands it

in their name as a matter of right — is quite unnecessary and a novelty in

Pennsylvania. I can understand how a man may have conscientious scruples

against bearing arms for the purpose of taking away the lives of his fellow

men, and there is much reason for being asked to excuse that peaceful sect

from such a duty; but, when Government asks an annual contribution either in

services or money for the purpose of preventing all necessity for violence

and force, I can not, sir, understand how it is a case for tender

consciences, nor why both money and services should be forbid by conscience.

It is a new case — to me a novelty.

There’s that old canard: Armies, arms, military training, and military spending aren’t for war — on the contrary, they’re all to prevent war!

Therefore pacifists ought to be the first to support military measures.

War is peace!

Freedom is slavery!

Ignorance is strength!

Gentlemen have referred to Penn’s Charter, wherein, as in our bill of rights, the freedom of conscience is abundantly guarantied.

Every man is permitted to adopt whatever religion and

creed he pleases, and to worship Almighty God according to the dictates of his conscience, and no man is permitted to molest or make him afraid; but nowhere in Penn’s Charter, in our Constitution or laws, do you find the principle recognized which is now sought to be introduced.

Exemption from

taxation is the last thing he would ever have expected the Quakers to ask for.

Their history informs me, sir, that they have always regarded it as a

religious duty to contribute to the support of the Government under which they lived, and that conscience, instead of interposing to shield them from the demands of Government, has bound them to a strict and faithful discharge of all the obligations of good citizens.

In Proud’s

History of Pennsylvania, gentlemen will find the following account of the ideas which this sect used to entertain, if they do not still, of their duties to Government.

Their great care and strictness, in rendering to Cæsar, according to their manner of expression, that is to the Government, its

dues; in the punctual payment of taxes, customs, and discouraging all illicit and clandestine trade; and in being at a word in their dealings: — Insomuch, that, in their particular advices to their brethren they say: — “As the blessed truth we profess, teaches us to do justly to all men, in all things; even so more especially, in a faithful subjection to the Government, in all godliness and honesty; continuing to render to the King what is his due, in taxes and customs, payable to him according to law.” — “For our ancient testimony has ever been, and still is against defrauding the King of any of the above mentioned particulars, and against buying goods reasonably suspected to be run” — “or doing any other thing whatsoever to the injury of the King’s revenue, or of the common good, or to the hurt of the fair trader; so, if any person or persons, under our name or profession, shall be known to be guilty of these, or any other such crimes or offences, we do earnestly advise the respective monthly meetings (hereafter explained) to which such

offenders belong, that they severely reprimand, and testify against such offender, and their unwarrantable, clandestine and unlawful actions” — “we being under great obligations of gratitude, as well as duty, to manifest, that we are as truly conscientious to render to Cæsar, the things that are Cæsar’s, as to support any other branch of our Christian testimony.” And so great was the importance of this affair with them, that an annual enquiry was regularly made through all parts of the British dominions, where they had members of society, whether the purport of these advices were duly put in practice, or not, and to enforce the same.

I have always supposed that these people were to be looked to for good examples of citizenship as well as for all the other virtues, and never before did I hear that conscience had taken alarm at the ordinary and reasonable demands of the kind and paternal Government we enjoy.

Why, sir,

where is this principle of exemption, if once adopted, to stop?

The Legislature of this State may think it necessary in times of profound peace

to buy arms and munitions of war — to organize and drill the militia — to encourage volunteer corps and to make large preparations against the hour of need and peril.

All this will require money, and who shall

contribute it?

Since these preparations point to war, the Friends cannot conscientiously contribute and they must be exempted, you say.

But another and another class of community come forward with the same plea of conscience, and, on the same principle, they too must be exempted from all participation in these arrangements — this peace establishment — and finally it is discovered that the State cannot be armed and put into an attitude of defense at all.

What then is to become of her?

Why, sir, war would be inevitable.

Our feeble condition would attract assaults and that greatest of human calamities would be certainly brought on us by the tender

consciences of the Commonwealth, which refused to keep up an ability of defense.

True humanity might dictate the preparations I have supposed or

more, and they would have the effect to deter hostility, prevent bloodshed, and preserve peace.

The gentleman from the city of Philadelphia, (Mr.

Scott) has shown conclusively how extensively the fact of an organized military force had operated with the enemy during the last war and how salutary such impressions may prove in future.

But you lose the benefit of such

impressions on the mind of an enemy when you deny to the government the means of making the requisite preparations, and if you excuse those who are conscientiously scrupulous, not the Quakers only, but the Menonists, the Dunkers and perhaps every man of any religious creed, may claim the benefit of the exemption, so that your government will become defenseless and powerless.

Without a formal renunciation of its authority, and without open resistance

to its demands, it will be left at the mercy of any foe who may choose to

attack it from without, or of any enemy within its bosom who may desire to

rend and overthrow it. Now, sir, I have shown from Proud’s

History what the opinions of the Society of Friends

are in respect to public contributions; and I find, in the Constitution of

, the principle adopted and recognized under

which they seem always to have acted. The 8th

section of that Constitution is in these words: “Every member of society has

a right to be protected in the enjoyment of life, liberty, and property; and

therefore is bound to contribute his proportion towards the expense of that

protection, and yield his personal service when necessary, or an equivalent

thereto; but no part of a man’s property can be justly taken from him, or

applied to public uses, without his own consent or that of his legal

representatives; nor can any man, who is conscientiously scrupulous of

bearing arms, be compelled thereto; nor are the people bound by any laws but

such as they have, in like manner, assented to for their common good.”

Mr. Chairman, this is wholesome doctrine, and these are the principles of

Pennsylvania. They pervade all our institutions; and I had hoped they were

cherished by all our people. I would respect conscientious scruples against

bearing arms where they are sincerely entertained, and would not ask any

man, in peace or war, to take up arms against his conscience; but then he

should pay a pecuniary equivalent such as the government might assess. This

is all that has ever been demanded; and this seems most reasonable and just.

I have looked in vain in our own plans of government and Constitutions, and

in the Constitutions of other States, for any such extraordinary immunity as

is now asked for a part of our fellow citizens.

But we are told we must not undertake to judge of men’s consciences; and it

is more than intimated that to argue against this “demand” of

conscience is to trespass on holy ground. I agree that conscience is a sacred

right; but when I am asked to vote for exempting a large class of our most

opulent citizens from the contribution to public burdens which other citizens

have to make, on the ground that conscience forbids them to contribute, may I

not inquire if it is a case for conscience? If an enlightened conscience

ought, or can, interpose a plea in bar in such a case? It seems to me to fall

peculiarly within the scope of our duties; and I should feel that our

constituents had reason to complain if we yielded to this mild

“demand” without investigating it closely and severely.

I know the proposition is often stated in this form: “It is wrong to take

human life. And it is the same thing to pay another for taking it as to take

it ourselves;” and in this way it is supposed the argument is just as strong

against paying pecuniary equivalents for military service as it is against

performing the service. Now two things are forgotten by this argument: First,

that the pecuniary equivalent is for the general purposes of the

government; and, secondly, that all military service, as well as pecuniary

equivalents, are designed to assist to preserve peace, and not to promote

war. Peace is the state our country desires. War is a calamity, and

government must be trusted with the means of averting it. If government finds

military preparations to be the most effectual means, where is there room for

conscientious scruples against cooperating with government?

That pious statement came less than a decade before the launch of the

Mexican-American War.

There is another view of this matter to be taken.

The people who have sent in their petitions here asking for this exemption are among our most opulent

citizens, and have a large amount of property to be protected by the government.

Can they conscientiously ask for protection when they refuse to

furnish means?

Protection and allegiance are reciprocal duties; and it seems to me that the law of allegiance binds every citizen to a discharge of all

his obligations to the government which gives him protection, until he is ready to transfer himself to another asylum.

Surely, while a body of men ask

and enjoy protection from the government for their persons and property, it would be unwise to give them the power, by an affirmation of conscientious scruples, to absolve themselves from their reciprocal duties to the government.

I have an objection to the amendment, founded on its generality. Nobody but

the Society of Friends is asking for this exemption; and if it is to be

granted, let it be to them specially and alone. The amendment goes to exempt

everybody who may profess conscientious scruples. Let us not outrun the

expectations of the public by offering universal exemption from taxation;

but if we are to have a select and privileged class among us, let us name

and specify them in our Constitution, so it may be known who are intended to

be benefitted. In the first establishment of a privileged order of men, we

ought to be more exact and specific than the amendment is; and if gentlemen

insist on pressing it, I hope they will make it so.

Much of the anti-war movement has lately turned away from marching and pleading with legislators and such and has decided to try to make the U.S. less eager to make war by exacerbating its “human resources” shortage.

I think this new focus shows promise.

It has a concrete, measurable goal that can be reached incrementally, results can potentially be seen both on a large scale and on a very human scale, and it is an actual, non-symbolic impediment to militarism, making it more difficult and more expensive.

There is a danger, though, that by focusing on encouraging desertion and conscientious objection within the military, and on discouraging recruiting, the anti-war movement will fall in to the easy habit of regarding its struggle as something that mostly involves other people — members of the military and potential recruits — changing their behavior.

One way to address this is to remind people that conscientious objection is for everyone.

A good example of this is provided by the Church of the Brethren Christian Citizenship Seminar, which was held in New York and Washington, D.C.:

Former conscientious objectors (COs) Enten Pfaltzgraff Eller and Clarence Quay shared the stories of their struggles, as did more more recent COs Andrew Engdahl and Anita Cole.

Eller and Quay each chose not to register and instead did alternative service, although Eller’s service came after a lengthy court case.

Engdahl and Cole arrived at their decisions after entering the military, and they asked for reclassification.

“When Jesus said ‘Love your enemies and pray for those who persecute you,’ that has to be now, not later,” Eller said.

“You have to struggle with where God is calling you and how you’re going to follow.”…

Several speakers addressed a different form of conscientious objection, war tax resistance.

Phil and Louise Rieman of Indianapolis and Alice and Ron Martin-Adkins of Washington, D.C., explained why they had decided not to pay the portion of their taxes that support military operations — and the consequences that can come with that choice.

Marian Franz of the National Peace Tax Fund provided additional background on this form of witness.

“If we say that war is wrong, and we believe war is wrong, then why would we pay for it?” Louise Rieman said.

“It was more than I expected,” said Chrissy Sollenberger, a youth participant from Annville, Pa.

“I didn’t think there was so much about conscientious objection to talk about.

I just thought it was saying no to being drafted, but it’s so much more than that.…

It feels like we have more power now to make those choices.”

So lately I’ve been being very urban homesteader — baking bread, brewing beer and sake, making yogurt, weeding the garden, canning soups.

I’ve been looking for a paying gig, too, which I think partially explains my sudden explosion of home usefulness: it gives me something productive to do while I wait for résumés and bids to be ignored.

What I haven’t been doing much is writing anything substantial for The Picket Line.

Sorry ’bout that.

Meanwhile all sorts of interesting things have backed up in my bookmarks, waiting for me to add some insight or context before passing them on for you to enjoy.

I think instead I’ll just let them spill out here and trust you to fill in the blanks:

Francois Tremblay wonders if taxpayers become complicit in what their tax dollars support. He weighs the arguments for both sides (no, because their participation is legally required; and yes, because their participation is nonetheless voluntary) and then engages in some spirited give-and-take with his readers.

War tax resisters Phil and Louise Baldwin Rieman died in a car accident shortly after .

There have been several remembrances of the couple on-line, such as this one from the Church of the Brethren.

Murray Rothbard writes about ending tyranny without violence (through withdrawal of consent) and the nearly 500-year-old insights of Étienne de La Boétie.

The Taxpayer Advocate said in its annual report that American taxpayers pay — above and beyond what they actually are charged in taxes — nearly two hundred billion dollars just trying to do the paperwork involved in taxpaying.

Our local paper did the math and put a number on a conclusion that should have been pretty obvious: it’s much cheaper to take public transit than to drive.

According to their figures, it costs Bay Area drivers about $1,000 per month to get where they’re going by car instead of by bus and rail.

Hell, we pay that much for rent.

A writer for Rebelión notes that Europe’s public is sick of spending so much on the military and asks, “is tax resistance not therefore justified, an investment in the struggle for what is worth the trouble of defending instead of the military costs that impede this to a great extent?” (en español)

Finally, U.S. nuclear weapons spending topped $52 billion (and that’s only counting what we’re allowed to know about).

Compare that to the budget of your favorite government agency, business, or non-profit.

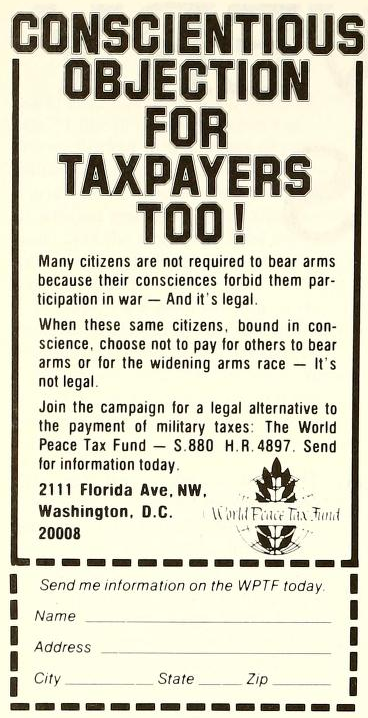

Here’s a piece from the New York Times that mostly concerns the efforts of the promoters of “Peace Tax Fund” legislation in the United States but also touches on American war tax resisters:

War Resisters: ‘We Won’t Go’ to ‘We Won’t Pay’

You could hardly find a more problematic time for pacifists who do not want their taxes spent on the military.

But the recent wave of patriotic fervor has only reinvigorated the efforts of one tiny, determined group.

“On , I was told I should lay low for a while,” said Marian Franz, executive director of the National Campaign for a Peace Tax Fund.

“Now I have been told this is the time.

As the war grows, so does the antiwar movement.”

For more than three decades, the National Campaign for a Peace Tax Fund has petitioned the federal government for a way to earmark the tax revenues that would go to the military — usually around 50 percent — for nonmilitary purposes, like education or health care.

Like conscientious objectors who in the past were offered an alternative to military service, these resisters say the First Amendment protects their ethical or religious objections to paying for war with their taxes.

Like other groups that have struggled to reconcile the obligations of citizenship with antiwar beliefs, the campaign has had a marked increase in inquiries from the public over the last year.

At the Center on Conscience and War, a Washington-based national nonprofit group that works for the rights of conscientious objectors, phone calls quadrupled right after and are now about 4,000 a month, double the usual number, said J. E. McNeil, the center’s executive director.

Mary Loehr, the coordinator of the National War Tax Resistance Coordinating Committee, an organization based in Ithaca, N.Y., that links 50 groups opposing war or weapons, has also seen a surge in interest.

“Starting , we have had a call a day from people asking for information, and our busy season is usually January through April,” she said.

“I would get 70-year-old women from the Midwest saying: ‘I don’t want to pay for this. Will it hurt my Social Security?’ ”

The debate over whether it is justifiable to withhold tax money from the military was waged on religious, philosophical and legal grounds even before supporters managed to have a bill on the matter introduced in Congress.

Derrick Bell, a visiting professor at the New York University Law School and an expert on constitutional issues, says the law doesn’t allow people to pick and choose where their tax money goes, as if they were at a buffet.

“When particular groups try to exempt themselves from having their tax money support a particular government activity, there is no legal precedent for that,” he said.

Professor Bell said the prevailing standard was that the “free exercise” of religion clause in the First Amendment was violated only if a law was shown to be irrational or unreasonable, or that someone suffered some special harm from it.

He noted, too, that even the right to be a conscientious objector to military service was established by statute and theoretically could be overturned by Congress.

“There is nothing written in stone,” Professor Bell said.

“Even the ‘free exercise’ clause has been variously interpreted.”

Opponents of the tax initiative commonly cite the fear that exempting some taxpayers for their religious beliefs would open a floodgate of claims from others objecting to federal support for everything from the arts to AIDS research.

Last year, for instance, a bill was introduced in the Illinois Legislature that would allow taxpayers who are against the death penalty to have the portion of their taxes that finances executions go to schools.

The bill, which never had any significant support, was killed.

But advocates counter that pacifism, often grounded in religious belief, is in a category by itself.

“Whenever you come up with a new issue, you hear ‘slippery slope,’ ‘Pandora’s box,’ ” said Ms. McNeil of the Center on Conscience and War, who is also a lawyer.

“There is no floodgate.

A minuscule amount of taxpayer money goes to pay for abortion or the death penalty, and other issues are political, not religious.”

In the United States, there has been a long religious and ethical tradition of opposition to war.

During the 19th century, Henry David Thoreau refused to pay taxes because he opposed slavery and the military.

The Mennonites, the Quakers and the members of the Church of the Brethren, who belong to what are known as historic peace churches because of their pacifist tradition, all refused to take part in the American Revolution.

They laid the foundation for the creation in of the Selective Service Alternative Service Program for conscientious objectors, which started with World War Ⅱ.

Until then, there was no legal recognition for conscientious objection.

During World War Ⅰ, 17 soldiers who were conscientious objectors even received death sentences in a military court, although none were carried out.

In the United States Supreme Court ruled that the criteria for conscientious objection could be broadened to include men who were not members of any religious denomination and in to include those who did not profess belief in a Supreme Being but had ethical or moral convictions against war.

Ms. Loehr, 44, who has been a war tax resister for 22 years, estimates that about 5,000 people around the country currently withhold taxes because of their objections to war and military spending.

Some tax resisters purposely keep their earnings too low to be taxed, she said, while some are self-employed and refuse to pay estimated tax; and some claim an abundance of tax exemptions so their employers cannot take the money from their paychecks.

The Rev. Michael J. Baxter, national secretary for the Catholic Peace Fellowship in South Bend, Ind., and a professor of theology at Notre Dame University, predicts resistance will rise.

“I think as the U.S. gets ready to go to war in Iraq, there will be more tax resisters,” he said.

“Sometimes during war, the place that good Christians belong is in jail.”

His group has already begun advising conscientious objectors in case the draft is revived, he said.

In June, to put a human face on their ideals, the National Campaign for a Peace Tax Fund put together a 15-page booklet featuring the smiling images and often sad tales of tax resisters across the country.

Some of the resisters profiled donate the taxes that they estimate would go to the military to other causes.

Others have been imprisoned or lost their assets because of tax evasion.

They say they have reached their convictions about the immorality of war through their religious beliefs or the influence of thinkers like the Rev. Dr. Martin Luther King Jr.

As pacifists and pastors in the Church of the Brethren, Phil and Louise Baldwin Rieman argue that contributing funds to war is the same as killing.

For 30 years they have given about 60 percent of their taxes to civil rights and peace programs, despite Internal Revenue Service threats of liens against their bank accounts, wage-garnishment letters sent to churches where they worked and government seizure of their family van.

“We will look back on war someday like we did on slavery,” said Mr. Rieman, who lives in Indianapolis.

A conscientious objector during the Vietnam War, he completed two years of alternative service.

“It feels lonely sometimes, but mostly it feels frustrating,” said Mrs. Rieman, 56, describing the couple’s long odyssey.

“We can’t buy a house, we can’t buy a car.

We don’t enjoy the feeling of religious freedom they say we enjoy in this country.”

Stanley M. Hauerwas, a professor of theological ethics at Duke Divinity School, said many religious traditions had a history of resistance to laws they considered immoral, those statutes supporting slavery being prime examples.

Even the way that the standards for conscientious objection have changed, from requiring membership in a pacifist church to simply allowing the adherence to certain ethics, shows a government grappling with what constitutes religion, Professor Hauerwas said.

Is it ethics, beliefs, membership?

The Peace Tax Fund bill would amend the Internal Revenue Code, setting up a nonmilitary fund to which pacifists could contribute the tax money that would otherwise go to the military.

Introduced in by Representative Ron Dellums, Democrat of California, it has been reintroduced every year since and had 35 supporters in the House of Representatives during Congress’s last session.

“ changed the equation once again,” said Representative Eliot L. Engel, Democrat of New York, a two-time co-sponsor of the bill who no longer supports it.

“A case could be made that if every American decided they didn’t like certain policies and decided to withhold taxes, it would be a problem.

It wreaks havoc with government.”

But Representative John Lewis, Democrat of Georgia, the bill’s current sponsor and a veteran of the civil rights movement, said should not make a difference in supporting the rights of conscientious objectors.

Other groups may have their own objections to the way federal taxes are spent, he said, but his philosophy was “you try to take the ones that have the largest meaning to the largest number of individuals.”

“We will put on a whole new effort when we come back to Congress,” said Mr. Lewis, an ordained Baptist minister.

“Look at the military budget.

We have enough bombs, we have enough missiles, we have enough guns.”

The 8 August 1981 Nashua Telegraph carried an article by Associated Press “Religion Writer” George W. Cornell.

Some excerpts:

A-bomb anniversary brings peaceful fight

New York (AP) —

In a time of military buildup, the “peace” people are marching, praying, fasting and signing petitions.

Several denominations have made “peacemaking” a current priority.

And some church leaders, including a bold bishop, have advised refusing to pay the portion of taxes that goes for arms.

[A]dvocacy of withholding so-called “war taxes” — the share of federal income taxes that go for military equipment — came not just from traditional “peace” denominations, but from a Roman Catholic archbishop.

Archbishop Raymond G. Hunthausen of Seattle, in a speech that has since evoked wide and varying reactions, suggested Christians refuse to pay the half of their federal income taxes going for armament.

“We have to refuse to give our incense — in our day, tax dollars — to the nuclear idol,” he said.

“I think the teaching of Jesus tells us to render to a nuclear-arms Caesar what Caesar deserves — tax resistance.

“Some would call what I am urging ‘civil disobedience.’

I prefer to see it as obedience to God.”

Similar suggestions have come from some other Christians, most solidly from leaders of three relatively small, but historic “peace” denominations — The Church of the Brethren, the Friends and Mennonites.

A joint meeting of them under the banner of “New Call to Peacemaking” said paying for war is wrong and asked members to “consider refusal to pay the military portion of their federal taxes, as a response to Christ’s call to radical discipleship.”

In separate denominational actions, the Church of the Brethren has supported “open, massive withholding of war taxes” and the Mennonites general conference is fighting in court against being required to withhold taxes partly used for military purposes from employes’ income.

The New York-based War Resisters League estimates 2,000 to 10,000 Americans annually hold back part of their taxes, some eventually being forced to pay but continuing to repeat the protest.

On representatives from

the IRS

testified before a Congressional committee about their efforts to improve

taxpayer compliance, and specifically to get non-filers back in the system.

Two non-filers testified in person — neither of them conscientious tax

resisters, though one went on at length about wasteful government spending,

and although he blamed his own nonfiling on negligence and wastefulness, it

was hard not to believe that resentment didn’t also play a role.

Conscientious objectors to taxation were more or less ignored by the committee

and by those witnesses who appeared before it. Representative Andy Jacobs,

Jr. submitted a statement in

support of legislation he introduced that would have created the United States

Peace Tax Fund and permitted conscientious objectors to military spending to

direct their taxes there. Here is the way he described the bill:

In some real ways, the legislation probably ought to be called The Federal

Revenue Collection Enhancement Act.

Conscientious objectors in many cases are refusing to pay their full tax

obligations because to pay the military portion would violate deeply held

religious or ethical beliefs. Most of us believe that our taxes should cover

national defense. And most of us believe that in time of American war we

should serve in the military if we are capable of doing so. But conscientious

objection has been recognized since before George Washington’s time. He

favored accommodation of the consciences of sincere objectors and recognized

that for the citizens of sincere conscience in opposition to war, there is no

choice.

This bill is a win-win proposition. It would simply allow a bona fide

conscientious objector to be assured that none of his or her taxes would go

to military purposes. Instead those taxes would be earmarked for

WIC,

Head Start, the

U.S. Institute of

Peace and the Peace Corps.

In no way would the bill change the priorities voted by the Congress. The

Defense Department would get exactly as much money as the Congress and the

President determined to be appropriate and the

WIC

Program and others listed in the bill would get no more than the Congress and

the President decided. The bill would simply allow the conscientious

objectors to pay their full taxes in good conscience.

Statements in support of the bill were also submitted by

Of the three historic “peace churches” that have included war tax resistance in their tenets, I’ve paid relatively little attention to the Church of the Brethren, the smallest of the three (the other two are Quakers and Mennonites).

While the Church of the Brethren recognizes the responsibility of all citizens to pay taxes for the constructive purposes of government, we oppose the use of taxes by the government for war purposes and military expenditures.

For those who are conscientiously opposed to paying taxes for these purposes, the church seeks government provision for an alternative use of such tax money for peaceful, nonmilitary purposes.

The church recognizes that its members will believe and act differently in regard to their payment of taxes when a significant percentage goes for war purposes and military expenditures.

Some will pay the taxes willingly; some will pay the taxes but express a protest to the government; some will refuse to pay all or part of the taxes as a witness and a protest; and some will voluntarily limit their incomes or use of taxable services to a low enough level that they are not subject to taxation.

We call upon all of our members, congregations, institutions, and boards, to study seriously the problem of paying taxes for war purposes and investing in those government bonds which support war.

We further call upon them to act in response to their study, to the leading of conscience, and to their understanding of the Christian faith.

To all we pledge to maintain our continuing ministry of fellowship and spiritual concern.

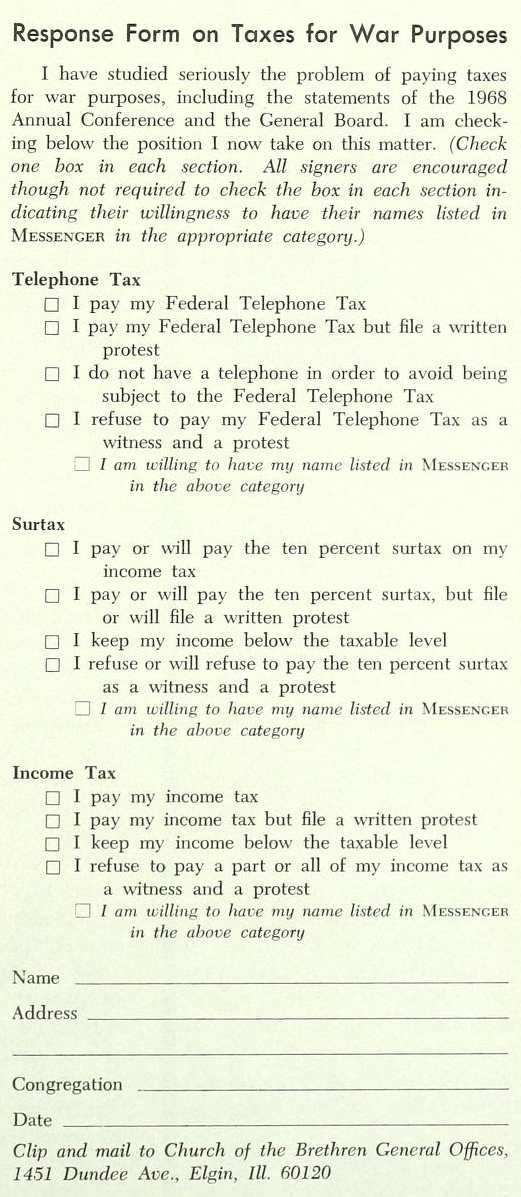

And here is the text of Taxes For War Purposes, an undated (circa 1967–8) pamphlet billed as “A Statement Adopted by the Brethren Service Commission”:

The Problem

A major and ever-growing portion of the Federal budget is going for war purposes and military expenditures.

The Federal Income Tax, Federal Telephone Tax, and other Federal taxes provide the monies for these purposes.

The percentage of the Federal budget which goes for war purposes and military expenditures ranges from 60% to 90%.

Traditionally, the source for most of this money has been the Federal Income Tax.

However, in the Congress restored the 10% tax on telephone bills to help pay for the Vietnam War and the President is now pressing for a 10% Surtax to provide still additional revenue needed to fight the war.

This situation presents a serious and growing problem of conscience for peace-minded people and conscientious objectors to war who put their trust in the power of love, nonviolence, and international cooperation rather than in military might.

They are caught in a conflict of conscience between loyalty to their land and obedience to God, between obligation to state and responsibility to Christ.

The Church’s Stance

The Church of the Brethren historically has opposed war and participation in war while at the same time it has taught responsible citizenship.

The Statement of the Church of the Brethren on War said:

“The American public may come to accept as normal and inevitable the prospect that the nation must be prepared to go to war at any moment, that every young man must spend time in military service, that an overwhelming share of our heavy Federal taxes must be devoted to military needs, and that this country must always be willing to assume the military burdens of weaker allies, actual or potential.

“Because of our complete dissent from these assumptions the Church of the Brethren desires again, as at other times in its history, to declare its convictions about war and peace, military service and conscription, the right of Christian conscience, and the responsibility of Christian citizenship.”

The Statement of the Church of the Brethren on Church, State, and Christian Citizenship said, “The Christian should appreciate and support the worthy functions which government performs.

He should willingly obey the state in matters on which he has no contrary moral conviction.

On the other hand, he should be alert to occasions when government neglects or misuses its trust from God.

When he is profoundly convinced that God forbids what the State demands, it is his responsibility to express his convictions.

Such expression may include disobedience of the State.”

The church recognizes and encourages freedom of conscience regarding war and the payment of taxes for war purposes.

Although it recommends alternative service instead of military service, it recognizes that not all members will hold the belief which the church recommends.

The same may be said regarding the payment of taxes for war purposes.

Although the church opposes the use of Federal taxes for war purposes and military expenditures, it recognizes that not ail members will hold this belief, and that even among those who do, there will be different expressions of that belief.

Present Alternatives

Four positions on the payment of Federal taxes for war purposes are evident:

paying the taxes

paying the taxes but expressing a protest to the government

voluntarily limiting one’s income or use of services to such a low level that they are not subject to Federal taxation

refusing to pay all or part of the taxes as a witness and a protest

1. Payment of taxes.

Persons who favor the government’s war and military policies willingly pay their taxes for these purposes.

Other taxpayers judge the constructive functions of government to outweigh the unacceptable activities.

Others feel that responsible citizenship requires the payment of all taxes.

Some who oppose the use of taxes for war feel that the risks and efforts involved in opposing such use of taxes are not worth the negligible results.

2. Payment of taxes under protest.

Persons who follow this alternative usually file a letter with appropriate government officials protesting the use of any of their tax money for war purposes or military expenditures.

Frequently they urge the government to use their tax money only for peaceful and constructive purposes either through the United States Government or the United Nations.

Sometimes such persons ask government leaders to amend the nation’s tax laws, especially the income tax law, to provide an alternative opportunity to those conscientiously opposed to paying taxes for war purposes to designate the use of their tax dollars for peaceful and constructive purposes either through United States Government functions or United Nations operations.

3. Limitation of income or use of service to non-taxable level.

Some persons are led by their consciences to limit voluntarily their income to such a low level that it will not be subject to Federal taxation for war purposes.

Likewise they may not install a telephone or use other services which are subject to similar Federal taxation.

They may endeavor to avoid participating in all those aspects of economic life which contribute to or support war and military operations.

This is a sacrificial position difficult to maintain but which offers a significant witness and form of protest.

4. Non-payment of taxes or portions thereof.

Persons who follow this alternative refuse to pay all or part of the taxes asked by the government.

They engage in this form of civil disobedience because they conscientiously object to the use of their money by the government for war or military purposes and because they want to make a more vigorous protest against the government’s war policy and military policy.

Sometimes these persons contribute an equal amount to the United Nations or a private peace agency as a positive witness to their position.

The Federal Income Tax and the Federal Telephone Tax are presently the taxes most frequently refused by conscientious objectors.

Refusal to pay such taxes might possibly be considered a violation of Internal Revenue Code, Section 7203, which would be a misdemeanor subject to a fine up to $10,000 and jail up to one year.

However, the experiences of conscientious objectors to Federal taxes for war purposes during the past several years indicate that the government is not interested in pressing possible criminal charges, but in trying to collect the taxes here or there with interest.

The Internal Revenue Service usually attaches the salary or bank account of the non-payer and collects the tax plus 6% interest from the date the tax was due.

The non-payment of the Federal Income Tax or portion thereof is carried out by those who have payment control over all or part of their income tax return and who refuse to pay all or a portion of the money owed.

The non-payment of the Federal Telephone Tax or a portion thereof is carried out by refusing to pay that part of one’s monthly telephone bill and sending with each remittance a written explanation of why that portion is not included.

Telephone companies have indicated that refusal to pay this tax will not result in interruption of telephone service.

Telephone companies turn over to the Internal Revenue Service the responsibility for collecting such unpaid taxes.

The phone company treats refusal as a matter between the customer and the government.

Some companies continue to carry the refused tax on the telephone bill as an “unpaid balance,” others do not.

Recommendations

We call upon all of our members and congregations to study seriously the problem of paying taxes for war purposes.

We further call upon them to act in response to their study, to the leading of conscience, and to their understanding of the Christian faith.

To all, we pledge to maintain our continuing ministry of fellowship and spiritual concern.

In order to provide further information, help and guidance to our members and congregations, we make the following recommendations:

That the Brethren Service Commission provide appropriate information and counsel to our members on all of the foregoing alternatives.

That the Brethren Service Commission in concert with other agencies continue to seek for and to help secure a provision in the Federal income tax law for a constructive alternative to the payment of income taxes for war and military purposes.

As a part of this effort we suggest that an appropriate delegation visit the President and other policymaking leaders.

That the church oppose any proposed legislation to increase Federal taxes designed specifically to support the war such as the proposed Surtax.

This opposition can be expressed by the General Brotherhood Board through testimony before congressional committees, by congregations through policy statements adopted and forwarded to legislators, and by individuals through letters and contacts with legislators.

That the Brethren Service Commission provide an opportunity for a corporate public witness by those congregations and members led to refuse to pay the Federal Telephone Tax specifically designed to support the Vietnam War.

This corporate witness could well include publicizing a list of Brethren congregations and members refusing to pay this war tax and consenting to be on such a list.

That a similar opportunity for a corporate public witness be provided in respect to any other Federal taxes enacted or about to be enacted specifically designed to support the War, e.g., the Surtax.

That those congregations and individuals who refuse to pay taxes for war purposes and military expenditures be encouraged to contribute any amount thus saved to the peace program of the church or other peace agencies as a positive witness to their opposition to war.

War tax resistance in the Friends Journal in

War tax resistance remained very much on the agenda at the Friends Journal at the beginning of the Reagan era of aggressive military build-up in .

A letter from Jenny Duskey in the issue read, in part:

I belong to a community of disciples called Publishers of Truth.

Our testimony is that Christ’s disciples can have no part in war or preparation for war, and that this means not joining the military or being drawn into legally designated “alternatives” to conscription even when the law demands, as well as not paying taxes destined for military use when we can refuse them.

“Publishers of Truth” (see also the advertisement pictured in ♇ ) was centered around Larry and Lisa Kuenning, who came to prophesy an emerging paradise on Earth, centered on Farmington, Maine.

I’m tempted to do some further research in this direction, but am afraid of getting lost in some interesting by-ways.

Lisa Kuenning was a collaborator with Timothy Leary, and for a time an important figure in the psychedelic renaissance.

Last I checked, the Kuennings were running Quaker Heritage Press, which specializes in reprints of old Quaker books.

The issue had an in-depth article by Richard K. MacMaster on Christian Obedience in [American] Revolutionary Times, that included a discussion of Quaker responses to war taxes and militia exemption taxes.

Excerpts:

The Pennsylvania Assembly voted on to recommend to conscientious objectors “that they cheerfully assist in proportion to their abilities, such persons as cannot spend both time and substance in the service of their country without great injury to themselves and families.”

This would be a subsidy to poorer Associators, men who could not supply themselves with a musket and bayonet and needed help from their neighbors.

It was a far cry from the kind of nonpolitical relief work that the sects had in mind.

The Continental Congress did not help matters when it decreed in that members of the Peace Churches should “contribute liberally in this time of universal calamity, to the relief of their distressed brethren.”

Were these distressed brethren the poor of Boston or poor families in their own neighborhood or George Washington’s makeshift army camped on the hills overlooking Boston harbor?

The Peace Churches took the Congressional resolve as a last-minute reprieve and insisted that their contributions were for the poor, even though the money would be turned over to the County Committee.

“For we gave it in good faith for the needy,” a Lancaster County Brethren pastor explained, “and the man to whom we gave it gave us a receipt stating that the money would be used for that purpose.”

The Lancaster County experience was repeated in other Pennsylvania counties and in other colonies where Quakers, Brethren, and Mennonites were numerous.

Most communities tried voluntary contributions, but in Frederick County, Maryland, and Berks County, Pennsylvania, the committees levied fines on men of military age who did not drill with the Associators.

The nonresistant sects had fallen into a trap.

No matter how they labeled them, the authorities understood their voluntary contributions as donations to the war chest.

And if contributions failed to come voluntarily, they were already preparing for compulsory payment of money as an equivalent to military service.

Time was running out on the Peace Churches by .

Soon after the elections, military associators began petitioning the Pennsylvania Assembly that

some decisive Plan should be fallen upon to oblige every Inhabitant of the Province either with his Person or Property to contribute towards the general Cause, and that it should not be left, as at present, to the Inclinations of those professing tender Conscience, but that the Proportion they shall contribute, may be certainly fixed and determined.

These petitions asked much more than an increased tax assessment on the conscientious objectors.

The petitions explicitly stated that every member of the community had an obligation to make some contribution to the common cause; the additional tax would be a concession to those who could not meet that obligation on the field of battle.

The Peace Churches rightly put their case on the high ground of religious freedom.

Quakers expressed their “Concern on the Endeavours used to induce you to enter into Measures so manifestly repugnant to the Laws and Charter of this Province, and which, if enforced, must subvert that most essential of all Privileges, Liberty of Conscience.”

They asked the Assembly not to infringe the solemn assurance given them in Penn’s Charter, “that we shall not be obliged ‘to do or suffer any Act or Thing contrary to our religious Persuasion.’ ”

The revolutionary government rose to the challenge.

All sixty-six members of the Philadelphia Committee proceeded in a body to the Assembly chamber to present their response to the Quaker address to the Speaker of the House.

The same day, the Assembly heard petitions from the Officers of the Military Association of the City and Liberties of Philadelphia and from a Committee of Privates.

They first narrowly construed the grant of religious freedom in the Charter and threw out of court the sectarian contention that religion was more than a Sunday worship service.

We cannot alter the Opinion we have ever held with Regard to those parts of the Charier quoted by the Addressors, that they relate only to an Exemption from any Acts of Uniformity in Worship, and from paying towards the Support of other religious Establishments, than those to which the Inhabitants of this Province respectively belong.

The representation from the Committee of Privates went still further.

They insisted that “Those who believe the Scriptures must acknowledge that Civil Government is of divine Institution, and the Support of it enjoined to Christians.”

Quakers ought not to question what governments did, according to this Committee of Privates, but simply obey; God had ordained the powers and thereby gave sanction to every action of the state.

The lines were thus clearly drawn between the sectarian view of supremacy of conscience and the secular view of the primacy of the state.

The Mennonites and Church of the Brethren simply set down the limits of what they could do in good conscience.

Their petition made little difference to the course of events.

The day after the Mennonite and Brethren statement was read the Pennsylvania Assembly voted to require everyone of military age who would not drill with the Associators “to contribute an Equivalent to the time spent by the Associators in acquiring the military Discipline.”

Later in , the Assembly imposed a tax of two pounds and ten shillings on non-Associators, which would be remitted for those who joined a military unit.

Under new pressure from the Associators they raised the tax to three pounds and ten shillings in .

The Pennsylvania Constitutional Convention incorporated the principle of taxing conscientious objectors as an equivalent to military service in the Declaration of Rights they adopted.

It made explicit what most Patriots already believed:

That every Member of Society hath a right to be protected in the Enjoyment of Life, Liberty and property and therefore is bound to Contribute his proportion towards the Expence of that protection and yield his personal Service when necessary or an equivalent… Nor can any Man who is conscientiously scrupulous of bearing Arms be justly compelled thereto if he will pay such equivalent.

Participation in warfare was a universal obligation, in their view, falling equally on every citizen; those who could not fight must pay others to fight in their place.…

The Assembly and the Convention clearly intended to make the Peace Churches pay for war and imposed the tax as an avowed equivalent to military service.… Religious pacifists carried the whole burden of the tax.

But a tax imposed on conscientious objectors as an equivalent to joining the army and intended for the military budget definitely infringed on the religious liberty guaranteed by William Penn’s Charter.

The war tax issue thus arose in a context of freedom of conscience curtailed for those whose Christian faith forbade their “giving, or doing, or assisting in any Thing by which Men’s Lives are destroyed or hurt.”

Maryland and North Carolina followed Pennsylvania’s example in levying a special tax on conscientious objectors; the North Carolina law made payment the grounds for exemption from actual service with the army.

Virginia and several other states required conscientious objectors to hire substitutes to take their place whenever their company of militia was drafted for combat duty.

Special tax assessments for military purposes passed every state legislature as the war dragged on.

And the rapidly depreciating Continental and state paper money that fueled a run-away inflation was itself a war tax.

Wherever Quakers, Mennonites, or Brethren lived, the problem of paying for war soon caught up with them

Could a valid distinction be made between military service and war taxes?

The Reverend John Carmichael, Scottish Presbyterian pastor in Chester County, Pennsylvania, had little sympathy with the nonresistant sects who refused to pay war taxes, but he saw no distinction between fighting and paying the cost of war.

In Rom 13, from the beginning, to the 7th verse, we are instructed at large the duty we owe to civil government, but if it was unlawful and anti-Christian, or anti-scriptural to support war, it would be unlawful to pay taxes; if it is unlawful to go to war, it is unlawful to pay another to do it, or to go do it.

Some Brethren, Mennonites, and Quakers agreed that no real distinction could be made and consequently refused to pay taxes levied for military purposes.

In his sermon, Carmichael spoke of Mennonites “who for the reasons already mentioned will not pay their taxes, and yet let others come and take their money, where they can find it, and be sure they will leave it where they can find it handily.”

They would not resist the tax collector in any way; but they could not cooperate in wrongdoing by voluntarily paying war taxes.

The law took this practice into account and permitted collectors to seize the property of those would not pay their own taxes.

Quakers officially discouraged payment of war taxes and militia fines.

Many Friends went to jail for their refusal and still a larger number allowed the authorities to take horses, cattle, furniture, farm implements and tools to pay their taxes.

They refused to accept any money from the sale of their goods over and above the tax and fine.

In the Shenandoah Valley and in other Quaker communities, their neighbors found rare bargains when the sheriff sold a Quaker farmer’s property for taxes and purposely kept the bidding low.

Virginia Yearly Meeting protested to the authorities about the sale of slaves, freed by their Quaker masters in defiance of the law, who were taken up and sold to pay their former masters’ war taxes.

Refusal to pay taxes for military purposes had a close parallel in Quaker refusal to pay taxes to support an established Church; they accepted the right of civil government to appropriate money for either purpose, but denied that civil government could coerce their consciences, even at the cost of jail sentences.

This was a minority position among English and American Friends, even after John Woolman prodded their conscience on war taxes.

Woolman’s influence can be seen in a circular letter issued by Philadelphia Yearly Meeting in , when Braddock’s defeat left Pennsylvania exposed to French and Indian raids and the Assembly ordered new taxes for mounting a fresh campaign.

The tax was a general one, including military appropriations with all the other functions of civil governments, but Friends agreed “as we cannot be concerned in wars and fightings, so neither ought we to contribute thereto by paying the tax directed by the said act, though suffering be the consequence of our refusal.”

The issue in was much clearer: the taxes were levied entirely for military purposes and intended as an equivalent to military service.

With the passage of years, Friends had the meaning of nonresistance in much sharper focus and a much greater number accepted the challenge of faithful discipleship.

Mennonites also responded to the challenge by refusing to pay war taxes.

When the Pennsylvania Assembly passed an act in to require a tax of three pounds and ten shillings from everyone of military age who refused to turn out with the militia, Mennonite opinion was divided.

Christian Funk, bishop in the Franconia congregation, allowed payment of the tax and tried to convince his brother ministers.

But refusal to pay war taxes had taken deep roots in the Mennonite tradition by .

The mere rumor that Funk permitted payment of the tax was enough to bring complaints against him at the time of preparation for the Lord’s Supper in and to lead to his ouster from the ministry.

All of the preachers and a great many other Mennonites in eastern Pennsylvania opposed payment of the tax.

Andrew Ziegler, bishop in the Skippack congregation, spoke for them, when he declared: “I would as soon go into the war, as to pay the three pounds ten shillings if I were not concerned for my life.”

Zeigler and others could see little difference between fighting and paying for war.

In the face of a long-standing tradition of paying taxes without questioning the purpose of the tax, men of faith testified from their own conscience that for them there could be no distinction between refusing to fight and refusing to pay for war.

These Mennonites, Brethren, and Quakers willingly accepted the penalty for their conscientious objection to war taxes in imprisonment and loss of property far in excess of the tax.

Their action reminded their brethren of the need for careful discrimination in rendering to Caesar the things that are really Caesar’s. They refused to let a majority vote in the legislature be their conscience and rejected the easy way of confusing Caesar’s will with the will of God.

In the same issue, Bill Durland of the Center on Law and Pacifism reviewed the attempts to get a sympathetic court hearing in the United States for the argument that conscientious objection to military taxation is a Constitutionally-protected right of citizens.

He described the founding of the Center in by himself, Robert Anthony, Bruce & Ruth Graves, Barbara & Howard Lull, Peter Herby, and Richard McSorley, and then described the various avenues of appeal the group was pursuing in the U.S. Supreme Court.

Anthony put his legal argument this way: to be compelled to pay war taxes “would force [him] to accept a creed, and practice a form of worship foreign to his convictions, and to establish as the only normative religious belief and practice, that adhered to by most Christian denominations, i.e., that it is both a Christian and an American duty to fight in just wars and pay for them.”

The Supreme Court wasn’t interested.

The Center tried again with the Graves’ case, asserting that the First Amendment’s assertion that “Congress shall make no law… prohibiting the free exercise [of religion]” means that the governmental interest in having an efficient and uncomplicated tax system is trumped by the citizen’s right to a religious practice that forbids funding war.

Again, the Supreme Court turned up its nose.

The Center then made an attempt with the Lulls & Peter Herby as petitioners.

As the First Amendment arguments had failed to make any headway, this time they made a Hail Mary pass with a Ninth Amendment argument.

“This amendment recognizes that there are certain fundamental, inalienable rights not enumerated in the Constitution which the people possess that are preexisting to any constitution, are inherent in the individual, and are not subject to divestment either partially or completely by the state.

These rights have also been called ‘natural’ and are those held by an individual in a state of absolute liberty.

In contracting to enter into a state of society, the people collectively, and the person individually, only divest themselves of those natural rights which they expressly relinquish by enumeration.”

Nice try, but the Supreme Court yet again denied cert.