Why it is your duty to stop supporting the government →

the danger of “feel-good” protests →

“symbolic” tax protests? →

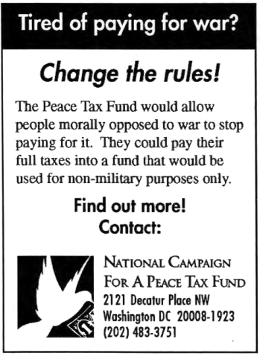

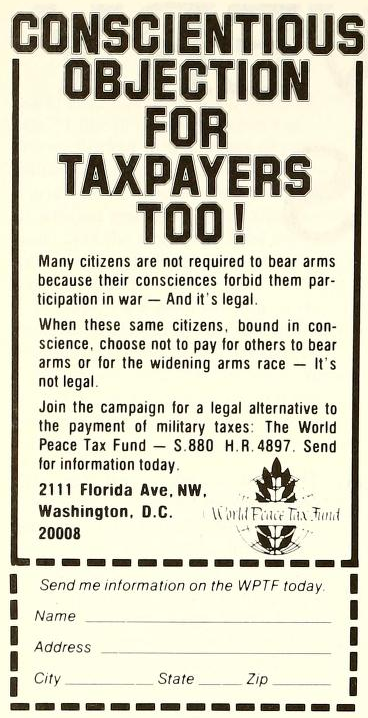

the “Peace Tax Fund,” legal conscientious objection to military taxation

In ’s Picket Line I had some discouraging things to say about ideas like the “Peace Tax Fund.”

In fact, I dismissed them as worthless and wondered why they were so popular in war tax resistance circles.

I decided that I’d better take a closer look and make sure I really understood what I was talking about.

The “Peace Tax Fund” movement is active in something like 17 countries, and bills have been introduced in at least 7 national legislatures to create such funds.

It would relieve the suffering of current war tax resisters, who would be able to go back to a legal, above-board, taxpaying life or earn a taxable income.

My most basic objection to this set of points is that I don’t believe that a bill that allows the government to have more money and to spend as much of it as it would like to on war is anything like a step in the right direction or anything war tax resisters ought to waste their time on.

My secondary objection is that quite clearly some war tax resisters would indeed be deceived into feeling that they could again pay taxes with a clear conscience if a “peace tax bill” were passed — while in reality nothing in the moral equation would have changed.

There’s no virtue in further clouding the moral challenge of taxation in this way.

Many of these other alleged benefits seem either unlikely or not worth these negative results.

The symbolic, message-sending benefits are the most plausible, but seem just as attainable without the benefit of an act of Congress.

Only one page of the many I visited when searching for information on these “peace tax funds” even attempted to squarely address the most glaring flaws of the campaign:

But this is not accurate.

When someone declared himself a conscientious objector that person did not take up arms and kill.

Perhaps somebody else was drafted to do so instead, this is true, but that person, the conscientious one, did not.

A “peace tax fund” payer, on the contrary, pays just as much money as the non-fund payer, but just cherishes the illusion that her dollars were peaceful ones.

It would be as if the government told conscientious objectors that they had to take up arms and shoot at the enemy just like everybody else, but that they didn’t have to take credit for their kills if they didn’t want to.

The government can’t solve your moral dilemma for you by making a separate slot above the basket for conscientious people to pass their taxes through.

That’s just silly, and makes “conscientious” people look not conscientious at all but naïve and easily bought-off.

So what are the alternatives?

Whether or not a “peace tax fund” is enacted, the basic problem of not wanting to contribute to activities you think are immoral remains the same, and tax resistance continues to be a good response to that problem.

If the idea of a “peace tax fund” is attractive to you, I would suggest not waiting for the government to create one for you, but to go ahead and donate money directly to charities that you consider valuable.

If merely the illusion of having paid taxes that were only used for peaceful purposes is enough for you, visualize every dollar that you paid going directly into the budget for your favorite government program (you can do this even without a “peace tax fund” bill and it will mean just as much).

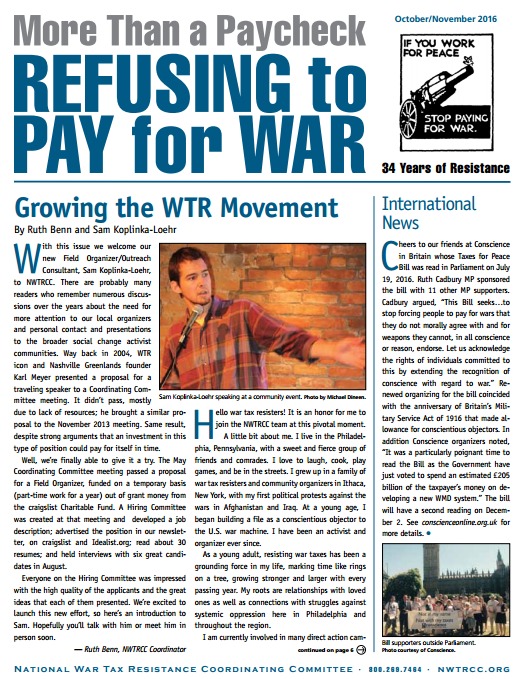

Peters was back from Hebron, where he’d been working with Christian Peacemaker Teams, and he shared photos and observations about his time there.

Peters says his tax resistance has become more confrontational in recent years, moving from a mostly-symbolic refusal to pay the phone tax to “what Gene Sharp would call ‘withdrawal of consent.’ ”

Today Peters has adopted complete non-cooperation with the IRS — he refuses to file, and instead sends letters explaining his reasons.

“We’re entering an era of ‘spiritual warfare,’ ” Peters says, “the political process is bankrupt.”

I arrived a little late and so I missed the first part of Wright’s talk, but here are some items from the notes I took:

Wright was impressed with the Conscience UK group, which he thought was the most “slick” of the groups represented at the conference, and the one that had the broadest focus in terms of war tax resistance in general.

Most other groups had a more narrow focus on Peace Tax Funds or other forms of official accommodation for conscientious objectors, although most of the peace tax campaigners were also war tax resisters.

Peace Tax Fund advocates acknowledge that there are objections to their program within the war tax resistance movement, however Wright found that at this conference there was near-unanimity about the value of a Peace Tax Fund-like program.

It is seen as a winnable battle, and potentially a valuable tool that war tax resisters can use.

The most high-profile peace tax campaign going on these days is that of the Peace Tax Seven in the UK.

Some Italian war tax resisters have had success in pursuing the conscientious objector argument in the courts, and apparently are paying a portion of their taxes to non-governmental organizations with the blessing of some judges.

These cases haven’t yet been brought to higher courts, however.

Some people who are lobbying the government or international bodies (including multiple UN human rights bodies and overlapping multi-nation European meta-governments) to try to enact some official accommodation for conscientious objectors to military taxation feel that they are unable to become war tax resisters because such “lawless” actions would hurt their credibility with those they are lobbying.

The Quaker Council for European Affairs is trying to push for an acknowledgment of conscientious objection to military taxation as a human right in the Council of Europe (which is a larger body than the European Union and is apparently more amenable to such an argument).

The Peace Tax Fund bill being considered by the U.S. Congress has a similarly tight definition of “conscientious objector” as that used to categorize people for military service by draft boards — that is, to qualify as a “conscientious objector” a taxpayer must be “opposed to participation in war in any form based upon the taxpayer’s deeply held moral, ethical, or religious beliefs or training.”

Non-pacifists who nonetheless conscientiously object to the way their money is being spent on wasteful, reckless belligerence would not qualify.

Best slogan from the discussion: “War Tax Resistance — it’s a direct action you do every day.”

In response to my critique of the Peace Tax Fund bill that I posted here , someone responded:

The Peace Tax Fund would not achieve anything “real” until enough had checked the box to actually make it impossible for Congress to fund the Pentagon to the extent it wished.

That is an interesting possibility, however, and would be a direct gauge of a war’s popularity on a year-to-year basis.

A so-called just war would see just the true pacifists — and we all know we are a very slender slice of the citizenry — checking the Peace Tax Fund.

A highly unpopular war might actually produce millions of such reactions.

Would that have an effect?

Possibly.

This brings up a couple of issues.

One is that the Religious Freedom Peace Tax Fund Act does in fact restrict the use of the “Religious Freedom Peace Tax Fund” to those taxpayers who are “designated conscientious objectors” — a category that includes only a taxpayer

who is opposed to participation in war in any form based upon the taxpayer’s deeply held moral, ethical, or religious beliefs or training (within the meaning of the Military Selective Service Act (50 U.S.C. App. 450 et seq.), and who has certified these beliefs in writing to the Secretary of the Treasury in such form and manner as the Secretary provides.

I had a heck of a time tracking down this “50 U.S.C. App. 450 et seq.” but I think this is the important part:

So if the Religious Freedom Peace Tax Fund bill becomes law, only those taxpayers who “by reason of religious training and belief” are “opposed to participation in war in any form” will be able to take advantage of its provisions.

The first half of this qualification isn’t as daunting as it may first appear, since the courts, in their reluctance to get their hands dirty in deciding what sorts of religious beliefs are worthy and which are not, have allowed a lot of pretty vague and individualistic spiritual bents to qualify as “religion” for the purposes of such a test.

The second half, though, pretty much locks out all but the committed pacifist.

Keep that in mind.

Now, just to satisfy curiosity, let’s see how many such pacifists there would have to be in the United States for the Religious Freedom Peace Tax Fund bill “to actually make it impossible for Congress to fund the Pentagon to the extent it wished.”

The bill would establish a “Religious Freedom Peace Tax Fund” that would receive all taxes paid by these conscientious objectors, and the money in this fund “shall be allocated annually to any appropriation not for a military purpose.”

MILITARY PURPOSE — For purposes of this Act, the term “military purpose” means any activity or program which any agency of the Government conducts, administers, or sponsors and which effects an augmentation of military forces or of defensive and offensive intelligence activities, or enhances the capability of any person or nation to wage war, including the appropriation of funds by the United States for—

the Department of Defense;

the Central Intelligence Agency;

the National Security Council;

the Selective Service System;

activities of the Department of Energy that have a military purpose;

activities of the National Aeronautics and Space Administration that have a military purpose;

foreign military aid; and

the training, supplying, or maintaining of military personnel, or the manufacture, construction, maintenance, or development of military weapons, installations, or strategies.

A while back, the National Priorities Project conducted a break-down of the federal budget that gives a fairly good idea of what would fall in this “military purpose” category.

I use their numbers rather than the numbers gathered by the War Resisters League because the WRL includes veterans benefits and a portion of the interest on the national debt as military expenses, while the National Priorities Project and the Religious Freedom Peace Tax Fund bill do not.

The National Priorities Project estimates that “[m]ilitary spending consumes 26 cents out of every individual income tax dollar.

It makes up about 20% of total federal spending and over half of the discretionary budget.”

A simple way of looking at the Peace Tax Fund is that the government sets up two sources of money in the treasury.

One, the Peace Tax Fund, can only be spent on non-military purposes.

The other one, the “general fund,” can be spent on anything.

The only way this would actually have an effect on military spending is if the general fund becomes smaller than the amount spent on the military.

If that happens, the government would either have to borrow money to make up the difference (which they certainly could do) or dip into the Peace Tax Fund (which would be illegal) or reduce military spending (which would be grand).

So the question is: How many people would have to become conscientious objectors to military taxation for this to happen?

If, for simplicity’s sake, we assume that likely conscientious objectors to military taxation currently pay on average about the same amount of taxes as everyone else, in order to cut in to that 26% of every tax dollar that is spent for military purposes, more than 74% of these taxpayers would have to declare themselves conscientious objectors, who “by reason of religious training and belief” are “opposed to participation in war in any form.”

Nowhere near three-quarters of Americans feel this way, and so the law will have no effect at all on the military budget.

Furthermore, if three-quarters of Americans did feel this way, there would be no need for such a silly law in the first place as we would all already either be living productive and sane lives in a peaceful tomorrow of harmony and understanding, or living in barbed-wire collective labor camps under the control of our foreign overlords, depending on your brand of speculative fiction.

So if you do support the Religious Freedom Peace Tax Fund bill, don’t do so because you think it might some day deprive the missile-makers and war profiteers of their turn at the feeding pail.

That just isn’t going to happen.

It was often claimed in the founding period — and it is claimed today by jurists like Justice Souter and by scholars like Noah Feldman — that citizens have a right of conscience not to pay taxes that will be used to advance religious teachings which they do not believe.

But advocates of this position typically reject the corresponding claim that citizens have a right of conscience not to pay taxes that will be used to advance non-religious (or, in their view, anti-religious) teachings in which they do not believe.

Are these positions reconcilable?

This essay investigates the question and concludes that they are not.

Nor is it a tenable position to hold that conscience is violated by the use of a citizen’s tax dollars to promote any beliefs, religious or non-religious, that particular taxpayers reject.

So jurists and scholars would do well to drop the selective and opportunistic appeal to the ostensible connection between taxes and conscience.

The Peace Pledge Union (PPU), founded in by the Revd Dick Sheppard, was discussing the possibility of a “war tax resistance” campaign .

PPU’s interest stemmed from prosecution of members for failure to pay income tax and Sheppard wished to establish a general defence of conscientious objection.

Though the defense was tried by individuals, the idea of “tackling the Income Tax question on a grand scale” lapsed with Sheppard’s untimely death in ….

After the Second World War, however, the question was brought onto the agenda by the Quakers, again contesting income tax assessments.…

In Cheney v. Conn (), a Quaker assessed for income tax put up the defence that the assessment was illegal because a portion would be used for armament — an unlawful purpose.

Not surprisingly, the defence failed on the ground that the words of the Finance Act were unambiguous.

Some years later, the Quakers tried to move the argument on to new ground, bringing in the Genocide Convention and Genocide Act .

Their case was lost in the Court of Appeal where, on the same day, a similar case based on an alleged violation of a fundamental civil right to protest was also lost (Langran v. Hayler, Surrendan v. Hibbs ()).

In parallel actions Quakers filed applications in the European Commission of Human Rights under Article 9 of the European Convention (freedom of conscience).

The Commission too was unresponsive, holding the applications inadmissible…

About the same time the Peace Pledge Union was running a similar campaign.

In , after some reluctance, Council had finally resolved to contest PPU’s liability to pay tax on behalf of its employees…

This, the longest running tax resistance case, gained the PPU substantial publicity but was eventually lost in Bloomsbury County Court…

I wrote up some of my impressions of of ’s NWTRCC meeting in Las Vegas.

I took notes on-and-off through and I’ll write up those things I remember that might be of interest.

The New Pamphlet I’ve Been Working On

I was at the meeting in part to present a first draft of a new edition of NWTRCC’s “Practical War Tax Resistance” pamphlet #5 on low-income / simple-living as a war tax resistance technique.

On night we distributed a few copies of this draft and over the course of I had a chance to sit down with a number of people and listen to their suggestions for improvement.

(If you would like to review the document, send me email and I’ll send you a copy of the draft.)

I’m aiming to have a final draft ready in , and with any luck we’ll have our new edition back from the press .

Not Much Evidence of a Tax Resistance Groundswell

Despite the growing anti-war sentiment in the country, there has been no evidence of a corresponding groundswell of interest in war tax resistance.

For the most part, people reported that their local groups were treading water in terms of membership and outreach.

There was more resignation than frustration expressed on this point, as most of us have become used to being, as we’d characterize it anyway, well ahead of the curve on this.

Many people also expressed that they often hear about lone-wolf tax resisters who for whatever reason never feel the need to align themselves with tax resistance organizations, so that the actual number of tax resisters is hard to gauge.

Survey in Progress

, NWTRCC started conducting a survey, informally, often at rallies, protests, and other activist events, to get a feel for what makes people choose or avoid tax resistance, and to do some concept testing of a possible large-scale one-year tax resistance campaign.

Of the few hundred people who have responded to the survey thus far, 47% are not doing any tax resistance now, and of that group, 61% would “consider participating in a one-year commitment to refuse a portion of your federal income taxes and redirect your taxes to a humanitarian cause if thousands joined you publicly” on a particular date.

All this sounds pretty good, and we plan to continue the survey , but even if we find a potential for this sort of tax resistance avalanche, NWTRCC alone doesn’t really have the resources to organize and launch it.

My hope is that we can package these persuasive survey results along with offers of our own specialized expertise and sell the idea of such a campaign to one of the larger national anti-war groups who could launch a campaign like this in a heartbeat if they cared to.

My own feeling is that this sort of thing is exactly the sort of sustained nationwide civil disobedience campaign the peace movement has been looking for; they just don’t know it yet.

Phone Tax Resistance Going Out of Style

Phone tax resistance has been a useful way of getting potential resisters to take the first step.

It’s pretty easy to do, and the risks are very low, and so many tax resisters have gotten their feet wet in this way.

However the proliferation of phone companies and phone plans, and the recent abolition of the phone tax on long-distance, have muddied the waters a bit.

There’s a pretty good chance that the excise tax on local service is on the way to the trash heap as well, so NWTRCC has begun to deemphasize phone tax resistance and the Hang Up On War campaign.

We’re still looking for the next “gateway” resistance tactic — any ideas?

Dan Jenkins Tries to Get the Courts to Recognize COMT

Some folks are trying to improve NWTRCC’s multimedia educational and persuasive offerings.

This is a good thing (our local tax resistance group still uses a slide show made during the Reagan administration, complete with a tape recording that goes “beep” when you’re supposed to flip to the next slide).

Alas, I was in a different workshop when this was being discussed, so I didn’t learn as much about this as I could have, but the project also includes a video contest — anyone can enter by producing a short video on the topic of war tax resistance — with cash prizes for the winning entries.

I’ll post more details on The Picket Line when the contest officially launches .

A New Flyer on W-4 Resistance

NWTRCC’s produced a new flyer on W-4 resistance (adjusting the withholding allowances on your W-4 form so that your employer sends less of your paycheck to the IRS) that may be helpful to folks who would like to resist their income tax but who find themselves with nothing but a refund to resist when April 15th comes around.

Tax Resisters and Student Financial Aid

A preliminary fact sheet was distributed that covers the implications for war tax resisters who are participating in student financial aid programs, or whose children are.

It’s not ready for publication just yet, but looks like it will be a useful resource when the time comes.

A Report from the International Conference on War Tax Resistance and Peace Tax Campaigns

We also got to read Larry Rosenwald’s report back from the International Conference on War Tax Resistance and Peace Tax Campaigns which was held in Woltersdorf, Germany .

He was struck by the differences between the tax resistance movement in the United States and its counterparts in the rest of the world (Europe in particular).

In Europe, the movement is focused more on using the law and the courts (national and international) to legalize some form of conscientious objection to military taxation, and less focused on civil disobedience and forms of extralegal conscientious objection.

They find it confusing that in the United States there’s both a Peace Tax Fund campaignand an organized war tax resistance movement.

The folks at wiseGeek have tried to extend the “Peace Tax Fund” concept to its natural conclusion: allowing taxpayers to allocate their tax payments to programs of their choice.

Personal Tax Earmarking they call it.

It, too, would be largely symbolic and not substantial, but it might have a good educational effect.

Stephen Douglas Smith of the University of San Diego School of Law has written a paper — Taxes, Conscience, and the Constitution — in which he asserts that, whatever the virtues of conscientious tax resistance, there’s nothing in the Constitution that supports it as some sort of right that the government must respect:

It was often claimed in the founding period — and it is claimed today by jurists like Justice Souter and by scholars like Noah Feldman — that citizens have a right of conscience not to pay taxes that will be used to advance religious teachings which they do not believe.

But advocates of this position typically reject the corresponding claim that citizens have a right of conscience not to pay taxes that will be used to advance non-religious (or, in their view, anti-religious) teachings in which they do not believe.

Are these positions reconcilable?

This essay investigates the question and concludes that they are not.

Nor is it a tenable position to hold that conscience is violated by the use of a citizen’s tax dollars to promote any beliefs, religious or non-religious, that particular taxpayers reject.

So jurists and scholars would do well to drop the selective and opportunistic appeal to the ostensible connection between taxes and conscience.

Daniel Jenkins is trying again, with a new set of arguments that I’ll try to summarize here.

Take note: I’m not a lawyer, so I may be missing a lot of legal nuance.

Jenkins’s examination of early war tax resistance in America, “The Liberation of Nathan Swift,” can be found in the book We Won’t Pay!: A Tax Resistance Reader.

In , Jenkins withheld part of his federal income tax from the IRS, putting it instead in an escrow account and informing the IRS that he would surrender it to them on the condition that the money would only be used for non-military spending.

In , the IRS sent Jenkins one of their intent-to-levy letters and Jenkins filed a Collection Due Process request.

The IRS quickly denied relief, so Jenkins appealed to the Tax Court, which shot down the appeal in , adding a $5,000 “frivolous filing” penalty to boot.

Jenkins then appealed to the 2nd Circuit Court of Appeals. , that court upheld the Tax Court’s ruling, and Jenkins asked the Supreme Court to take his appeal.

The state of law and precedent is, as far as I can tell, something like this:

The First Amendment says, in part, that “Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof…” So people whose religious beliefs prohibit their participation in certain government programs have asked the courts to exempt them.

For instance, in Wisconsin v. Yoder (), the Supreme Court ruled that a state compulsory education law violated the freedom of religion of the Amish people who challenged the law, “for the Wisconsin law affirmatively compels them, under threat of criminal sanction, to perform acts undeniably at odds with fundamental tenets of their religious beliefs.”

A challenge to tax laws came a decade later.

In U.S. v. Lee (), the Supreme Court ruled that the Old Order Amish could not use the same argument to get out of paying Social Security taxes because:

While there is a conflict between the Amish faith and the obligations imposed by the social security system, not all burdens on religion are unconstitutional.

The state may justify a limitation on religious liberty by showing that it is essential to accomplish an overriding governmental interest.

And

The tax system could not function if denominations were allowed to challenge it because tax payments were spent in a manner that violates their religious belief.

Because the broad public interest in maintaining a sound tax system is of such a high order, religious belief in conflict with the payment of taxes affords no basis for resisting the tax.

I would have thought that even this would have blasted a big hole in the argument that the uniform application of the tax laws is “essential” and that “[t]he tax system could not function” without it.

After all, if the tax system survived the legislative exception Congress carved out for self-employed Old Order Amish, there’s no reason to expect that it would collapse under the burden of a court-carved exception for the non-self-employed variety.

But the Supreme Court thought otherwise.

And that seemed to pretty much shut the door.

But in Congress passed the Religious Freedom Restoration Act, which instructed the courts to apply “strict scrutiny” to cases “where free exercise of religion is substantially burdened” by the government.

So conscientious objectors to military taxation started trying again.

In , the 2nd and 3rd Circuit Courts of Appeal turned down appeals that recrafted the old conscientious objection to military taxation legal arguments to see if they could be slipped in under the new Religious Freedom Restoration Act standard.

Both circuits said “no dice,” and in the Supreme Court decided not to review these decisions.

And that’s where that stood.

In , the Supreme Court decided Gonzales v. O Centro Espírita Beneficente União do Vegetal.

União do Vegetal is a religious group that uses ayahuasca in their ceremonies, a hallucinogenic tea that contains dimethyltryptamine, a substance banned by federal law.

The group challenged the application of that law to the participants in their ceremonies, basing their challenge on the Religious Freedom Restoration Act.

The government responded that, as with the tax law in Lee, the uniform enforcement of the Controlled Substances Act was essential to an overriding governmental interest.

Last year the Supreme Court ruled, unanimously, that the government was wrong, and that the Religious Freedom Restoration Act requires the government to carve out an exception to the Controlled Substances Act to accommodate the religious practices of União do Vegetal because the government had failed to show that the uniform enforcement of the Act was sufficiently essential to a sufficiently compelling governmental interest.

So when Jenkins filed his 2nd Circuit appeal, he used the O Centro ruling to try and distinguish his 1st Amendment / Religious Freedom Restoration Act arguments from those that the same circuit rejected in .

One problem with this, that the court pointed out when it rejected Jenkins’s appeal, is that when the Supreme Court decided O Centro, it explicitly distinguished the case before it from the tax case Lee.

The Court said that in contrast to the current case, Lee showed “that the Government can demonstrate a compelling interest in uniform application of a particular program by offering evidence that granting the requested religious accommodations would seriously compromise its ability to administer the program” and that the tax code was such a program.

Jenkins hopes he can convince the Supreme Court to take another look at Lee, which was decided on Constitutional grounds, and see if its logic still holds up under the Religious Freedom Restoration Act’s standards.

He wants the court to view the question this way:

Does Lee, or the logic of the circuit courts that relied on Lee, give the IRS a blanket exemption from the Religious Freedom Restoration Act when the Act itself does not allow for such an exemption?

If not, then his case should be decided on the merits, which requires a closer look at the extent to which his religious beliefs are violated by the law, and the extent to which accommodating those beliefs would compromise the IRS’s ability to collect taxes.

He’s got another argument, too, that’s very interesting, but I’m on much shakier ground in trying to summarize it because it relies on the Ninth Amendment, where even lawyers and judges fear to tread.

This amendment reads:

The enumeration in the Constitution, of certain rights, shall not be construed to deny or disparage others retained by the people.

This could mean anything or nothing, depending on who you ask.

Jenkins hopes that there’s a majority on the Supreme Court who are ready to give the Ninth Amendment some teeth.

Appealing to the Court’s conservative majority, Jenkins, in his Supreme Court petition, encourages them to interpret this amendment as über-conservative jurist Robert Bork suggested:

Ninth Amendment scholars propose giving content to its promise to preserve unenumerated rights by looking to this country’s history and tradition.

For example, in The Tempting of America: The Political Seduction of the Law (The Free Press ), Robert Bork observes that “[t]he Ninth Amendment appears to serve a parallel function [to the Tenth Amendment’s guarantee of federalism] by guaranteeing that the rights of the people specified already in the state constitutions were not cast in doubt by the fact that only a limited set of rights was guaranteed by the federal charter.”

Jenkins then goes on to argue that “that the individual right of religious conscience not to be compelled to participate in or support military activity was well recognized at the founding of this nation.

For example, the New York State Constitution of , which predates and is independent of the United States Constitution and the Bill of Rights, expressly protects persons with ‘scruples of conscience’ from forced military service and requisition for armament.

The constitutions of other colonial states also contain liberty of conscience guarantees and religious exemptions from the ‘bearing of arms’.

This constitutional right of conscientious objection was preserved by the states at least until the formation of the first permanent national army.

It was also preserved and protected by the actions of the early Congress and by the Civil War Congress that instituted the first federal universal military service draft.”

Jenkins has done an impressive amount of research into the history of conscientious objection to military taxation in the United States (see, for instance, The Liberation of Nathan Smith).

With this, he hopes to prove that conscientious objection to military taxation was among the “rights… retained by the people” at the time the Constitution was ratified.

But for this to work as a legal argument, the Supreme Court not only has to find this evidence compelling, but has to accept Jenkins’s invitation to wade into the Ninth Amendment — something that Court has generally been averse to.

I’ve lately been reading For Peace and Truth, a collection of short excerpts translated from the notebooks and letters of Pierre Ceresole.

Ceresole seems to be best-known today as the founder of Service Civil International, which organizes volunteers to do beneficial work around the globe to promote a more peaceful world.

He was a Swiss pacifist conscientious objector and war tax resister through both World Wars, and was frequently jailed for this (Switzerland, though a notoriously “neutral” country, had a program of mandatory military service and military taxes).

He also, much like Ammon Hennacy in the United States, refused to go along with air raid drills and other war preparation measures — Ceresole would be regularly arrested for placing lighted candles in the window of his home when the power was cut for blackout drills.

For Peace and Truth is mostly short excerpts — many are one- or two-sentence aphorisms — from notebooks that he wrote for himself, documenting how he prodded himself along as he struggled to be a better Christian.

The following are some that caught my eye, though as I am a nonbeliever my eyes tended to skip quickly through the ones that deal mostly with God stuff, so this isn’t a representative sample:

You say: How sad to think that the noblest altruism is, after all, merely a refined kind of selfishness.

I say: How good to think that selfishness, when it is purified and stops being stupid, is exactly the same thing as the noblest kind of altruism.

I have been carried this tremendous distance by the efforts of all the working men who, gritting their teeth, have laid rails in the desert, forged the machines, assembled the hulls of steamers; of all the engineers who directed their labour, of all the research workers who unlocked the secrets of physical science.

We owe to this immense army of men this conquest of vast distances, continuing without intermission for weeks, yard by yard, at a speed which would absolutely annihilate any human lungs; this merciless, relentless speed is the quintessence, the concentrated result of the efforts of all these men. Though they are now dead, they are potently alive.

Their effort has triumphed.

I must not have a closed mind even about the doctrine of not killing; it is possible that an occasion might arise when I had to kill.

It doesn’t seem likely; but if, after careful consideration, my conscience told me to kill, I ought to be able to do so.

The only absolute is the eternal: we must listen inwardly to this.

There is no other way.

Our world is characterized by the temporary acceptance of the most stupid and criminal things.

And people say: “It will always be like this!” — which means:

I am a coward and a criminal and I fully expect to remain one indefinitely.

All this deliberately willed morality is horrible.

You have no right to be moral if it is not your joy, your highest form of artistic expression.

Wrestle for the good life exactly as the poet wrestles to create a beautiful verse, in the same spirit, for the love of the thing itself.

I have the right to dissociate myself from the state at war if I also do so when it wishes to defend my property.

The basic falsity of these long-range methods of war.

If everyone was obliged to thrust his bomb or his piece of shrapnel personally into the body of his enemy, he would realize the horror of what he was doing.

At present the horror gets lost in transit.

All that remains is a beautiful scientific problem.

A dedicated life is only healthy and holy if it is sufficiently simple for the “inspired” person to be able himself to provide all the labour involved in supplying his material needs, or its equivalent.

Reduce and simplify your needs to the point where you can easily satisfy them yourself, so that those who live or claim to live for the Spirit do not thereby add to the burdens of other men, taking away from them the possibility and perhaps the very desire to develop their spiritual life also.

What will it benefit the world if, in developing your spiritual life, you add to the material burdens of others by a corresponding amount? and if, in rising yourself towards the Eternal you as it were oblige someone else to descend correspondingly in the opposite direction.

You will simply have created or increased a state of inequality and injustice without increasing the sum total of spiritual living.

The wrong and anti-natural character of the totalitarian State is shown by its drawing its real support from the mass, from mass-thoughts and mass-feelings as perceived by an individual; but this is not life manifesting itself in spontaneity, the action of God through the heart of a man, natural action in the depths of the individual, of the personality.

Mr. G.H. (member of the Salvation Army) writes: “I often ask myself what would happen to my two sons, pilots in the (British) R.A.F., if ever war broke out; but I tell myself that God can preserve them from all mishap, and I place my trust in him.”

Touching confidence in the partiality of God who will exert himself to protect Mr. G.H.’s sons against “mishap” — the self-same kind of mishap it is their (freely chosen) job to do their best to inflict on others.

So then you consider yourself cleverer than the millions who think they are bound in honour to defend their country?

But after all there are even more millions who believe themselves bound to attack it.

That restores the balance.

We make no progress for peace because we lack the courage to do as much as the soldier, however misguidedly, does for his cause.

During World War Ⅰ, Ceresole at first was paying the special tax that the Swiss government demanded from men who were exempt (for whatever reason) from military service.

After a Swiss conscientious objector was imprisoned for his stand (Switzerland at the time had no legal accommodation for conscientious objectors), Ceresole decided to express his solidarity by refusing to go along with this substitute tax for military service.

In a Sunday School class at my church, someone told the story of how wealthy Russian Mennonites long ago avoided serving in the military by hiring replacements.

“What’s the difference?” someone muttered.

Others in the class agreed.

It seemed that in the eyes of God, there would be little difference between serving in the military and paying someone else to serve in the military.

“Then why don’t we talk about our war taxes?” muttered another person in the class.

“Because that would be too relevant,” was the sarcastic reply.

Ceresole worked with others in Switzerland to try to get some legal protection for conscientious objection, without much success.

In addition to trying to get the government to allow objectors to do some sort of alternative civilian service in lieu of military training, they also tried to remedy the problem of the special military tax that exempt men were required to pay.

Their approach was an interesting one, and one that modern “Peace Tax Fund” promoters might consider:

“The petition [suggested] the creation of a special civilian tax for those refusing to pay on conscientious grounds; this was to be one-third greater than the corresponding military tax, and the proceeds were to be exclusively used for the support of the proposed civilian service.”

Myself, I’m of the opinion that paying your taxes into a “Peace Tax Fund” is no better than just sending them to the IRS without such a ribbon on top.

So to me the proposal from the Swiss conscientious objector movement that I’ve just described would be one-third worse.

But if I believed in the logic behind the “Peace Tax Fund,” I think I’d also be inclined to be willing to pay a premium for my conscience’s sake, and I would think that this would make it easier to sell the proposal to the public and to skeptical taxspenders.

In , in the middle of the United States Civil War, the United States Senate met and debated, among other things, Quaker conscientious objection.

They didn’t seem to be particularly well-informed as to the extent of or the reason for Quaker objection to paying military fines, but it’s interesting how much attention they gave the subject at such a time.

The following amendment to the conscription law was being considered:

That ministers of the gospel and members of religious denominations conscientiously opposed to the bearing of arms, and who are prohibited from doing so by the rules and articles of faith and practice of said religious denomination, may, when drafted into the military service, be considered non-combatants, and shall be assigned by the Secretary of War to do duty in the hospitals, or to the care of freedmen, or shall pay the sum of $300 to such person as the Secretary of War shall designate to receive it, to be applied to the benefit of the sick and wounded soldiers; and such drafted persons shall then be exempt from draft during the time for which they shall have been drafted.

John C. Ten Eyck

“We must not only relieve them from the draft, but from the liability of paying the commutation money”

Senator John C. Ten Eyck of New Jersey told his colleagues that this would not go far enough to satisfy Quaker conscientious objectors:

One of the objects of the amendment is to relieve the religious Society of Friends from the burden of this bill, and the Senator from Rhode Island has stated very truly the difficulties to which members of that society have been heretofore subjected, and the persecutions, to adopt his language, that have been heaped upon them in regard to the performance of military service.

If we intend to do them a favor and to relieve them from the consequences of this act, I respectfully submit that we must go further.

We must not only relieve them from the draft, but from the liability of paying the commutation money, for I have always understood that Friends, as they call themselves, not only object to the performance of military service, but to the payment of any fine or commutation in lieu thereof; and many of them, even who were possessed of large estates, have lain for months in jail rather than violate what they understood to be a principle of their faith by paying a miserable fine of from one to five dollars for not discharging military duty under the militia system in the several States.

I think it will not reach or answer the purpose that certain gentlemen have in view, to so amend this bill as to relieve them from the discharge of military service by the payment of the commutation.

In all the petitions and in all the proceedings as published coming from this very large respectable class of citizens in the United States, I have seen the objection raised to both features of the bill, and, to adopt their language, they bear testimony as strongly against the payment of the money as they do against going into the field.

So, without stating how I shall vote myself upon this amendment, I suggest that if we design to respect their conscientious scruples and to relieve them on account of them, we must relieve them also from the payment of the commutation money.

When this matter was before the Senate a year ago, I voted against relieving them.

James Harlan

“They say, ‘We might as well bear arms as hire a man to bear arms in our stead’ ”

Senator James Harlan of Iowa hoped that the clause allowing conscientious objectors to do hospital service might be acceptable to Quaker conscientious objectors:

I think the amendment, as modified, meets the case suggested by the Senator from New Jersey.

This amendment relieves the party drafted in the case named from military duty entirely, and provides that he may serve in the hospitals, or that in lieu of this hospital service he may pay a sum of money to be applied for the relief of sick and wounded soldiers.

The objection made by Friends to paying money has been to paying it as an equivalent for military service.

They say, “We might as well bear arms as hire a man to bear arms in our stead.”

This amendment, if I understand it, relieves them from the performance of military duty entirely, but it provides that they shall perform duty in the hospitals, and then gives them the alternative of paying money rather than performing this hospital service.

Henry B. Anthony

“These opinions may seem very absurd; I know they do, by Senators smiling around me; but they are opinions that have been entertained for two hundred years by as intelligent men as have ever spoken the English language”

Senator Henry B. Anthony of Rhode Island thought that maybe by hypothecating the militia exemption fine to humanitarian purposes they could evade Quaker scruples:

I would say, in justice to the scruples which the Friends have as to the payment of money, that I do not think they object to a military fine being collected from them by warrant of distress, as, I think, the lawyers call it, or by taxation.

They do not pay them voluntarily, but they do not go to prison rather than have their property levied upon.

But under the enrollment bill a man must either serve or pay $300 for the procuration of a substitute.

They can see a difference, but no great difference in principle, between serving themselves and hiring somebody else to serve for them.

The money which they pay is “for the procuration of substitutes.”

If the money could be appropriated to any hospital purposes, to any purpose towards which they can conscientiously contribute, they have no objection.

These opinions may seem very absurd; I know they do, by Senators smiling around me; but they are opinions that have been entertained for two hundred years by as intelligent men as have ever spoken the English language, and men have borne every persecution that the old martyrs ever bore in defense of these principles — educated, intelligent men; and I think we ought to respect them.

James H. Lane

“The attempt to collect money from the Quakers in lieu of military service will cost the Government ten dollars where they obtain one, if they get it at all”

Kansas Senator James H. Lane agreed with Senator Harlan that drafting Quakers to serve in hospitals was the answer:

I have had some dealings with the Quakers, and I desire to say… that it is perfectly ridiculous to attempt to force a Quaker into the ranks of the Army.

It cannot be done, or if you should succeed in doing it, he would be worthless as a soldier.

Besides, the attempt to collect money from the Quakers in lieu of military service will cost the Government ten dollars where they obtain one, if they get it at all.

It is a losing business to attempt to collect money from Quakers in lieu of military service.

But if you adopt the proposition of the Senator from Iowa, giving them the privilege of serving in hospitals, and permitting them to pay their money in lieu of hospital service, they will promptly and cheerfully come forward and pay that money, their conscientious scruples not being violated by such payment.

Lazarus W. Powell

“If a man cannot conscientiously go to war, and cannot conscientiously give money to carry on war, how can he conscientiously pay the taxes that the Government imposes for the purpose of carrying on the war?”

Senator Lazarus W. Powell thought either his colleagues or the Quakers or both must be crazy.

Ironically, perhaps, his characterization of the Quaker point-of-view was in many ways the most accurate yet.

And his reductio charging that paying taxes to a government that is conducting a war is no different from paying commutation fines to pay for a conscription substitute is, instead, a pithy argument for war tax resistance:

I was in favor of exempting Friends; but I cannot understand the subtle logic of gentlemen who seem to think that if you compel a Friend to pay $300 commutation money in lieu of hospital service he can do it conscientiously when he cannot pay the money in lieu of military service.

The hospital service is just as much an attendant upon war as any other service connected with the Army.

You frequently have to detail soldiers to attend to your sick and wounded.

Assigning them to hospital service and to military service is in effect the same.… How a man can conscientiously pay the taxes that the Government imposes for the purpose of raising men and paying them and buying munitions of war, when he cannot conscientiously pay the commutation money, is a matter that I cannot well comprehend.

I cannot see any difference.

If a man cannot conscientiously go to war, and cannot conscientiously give money to carry on war, how can he conscientiously pay the taxes that the Government imposes for the purpose of carrying on the war?

Why, sir, if a man can conscientiously pay the taxes, he can just as conscientiously pay commutation money.

As the law now stands, a man can exempt himself from military duty by paying commutation money.

That is but a form of taxation for the purpose of getting soldiers into your Army.

The money goes to hire substitutes or to pay bounties.

So the money that is raised by taxation is taken out of your Treasury for the purpose of paying bounties to soldiers and paying them their monthly stipend or wages.

Where is the difference?

There is none.

Senator Anthony thought the best approach might be to take advantage of the fact that Quakers typically would put up with distraints of their property without resistance:

I offer another amendment, to insert the following as new sections:

And be it further enacted, That any person drafted into the military service of the United States, who is conscientiously unable to perform military service, or pay commutation therefor, by reason of his religious scruples against bearing arms, may apply by petition to any judge of any court of the United States for the circuit or district wherein he resides, setting forth the facts; whereupon the said judge shall proceed summarily to hear and determine the case; and if it shall appear that such petition is true, and that such petitioner shall have maintained a consistent character in accordance with his well-known religious professions, incompatible with military service, the judge shall certify the fact to the board to enrollment for the enrollment district in which such petitioner shall reside, and upon the receipt of such certificate the board of enrollment shall take no further proceedings, nor shall any proceeding whatever be taken to enforce such conscientious person into the military service of the United States under that draft, or for the period of three years from the date of such certificate.

And be it further enacted, That at the time of issuing such certificate by a judge of the district or circuit court, as aforesaid, or as soon thereafter as practicable, such judge shall issue an order to the clerk of the district or circuit court of which he is the judge, to issue a warrant of distress directed to the marshal of the district, or to his deputy, against such conscientious person for the sum of $400, with all lawful costs upon the said petition and warrant, and the same shall be served by levying the same upon the goods, chattels, moneys, lands, and tenements of such conscientious person, and when recovered, the said penalty shall be paid into the Treasury of the United States, and the costs to the persons entitled to receive the same.

The effect of this amendment is, that a person conscientiously scrupulous against bearing arms is relieved from the obligation to pay $400 for the procuration of some other person to do that which he believes God has forbidden him to do, and provides that the fine shall be collected by warrant of distress.

He then submits to the law, the law takes his property, and he makes no complaint or opposition; but he is not required to do it voluntarily, and that is a great relief to the consciences of a great many intelligent men.…

James R. Doolittle

“I do not understand any Quaker in the world to object to ministering to the wants of those who are sick or who are wounded in war”

Mr. Doolittle. The bill as it stands does not require them to go as combatants at all, but simply gives them their choice, either to take care of the sick and wounded, or pay over their $400 for the purpose of providing for the wants of the sick and wounded.

I do not understand any Quaker in the world to object to ministering to the wants of those who are sick or who are wounded in war.

They are willing to do everything to alleviate the results of war.

What they object to is bearing arms and being instrumental in the killing of men themselves.

Mr. Anthony. A great many of them object to rendering any service which relieves another man from the obligation of that service and enables him to go into the Army.

Mr. Johnson. That is going too far.

Mr. Anthony. It is going too far, I know, but it is no further than very honest and very intelligent men go.

They have held these opinions, and their ancestors before them, for a great many years.

As it is the same thing to the Government, and will be a material relief to them, I cannot see any objection to the amendment.

Reverdy Johnson

“That is going too far”

Senator Ten Eyck tried to reassert his point:

Mr. President, I think these persons ought either to be exempted altogether or not exempted at all.

I have on my table a memorial placed there this morning, which comes from the meeting representing the Ohio Yearly Meeting of Friends, held at Damascus on , in which these memorialists state—

That the Society of Friends has from its rise been conscientious against fighting or bearing arms under any circumstances, or paying an equivalent in lieu thereof.

After stating the grounds of their belief, the memorial winds up by saying:

We therefore respectfully ask for exemption from military service, and from all penalties for the non-performance thereof.

Congress finally decided to go with the original plan of allowing conscientious objectors to be drafted into noncombatant roles or to pay a commutation fine.

In , a convention met in Harrisburg,

Pennsylvania to rewrite the state constitution. The previous constitution had

been enacted in , and had contained a section

reading:

The freemen of this commonwealth shall be armed and disciplined for its

defence. Those who conscientiously scruple to bear arms shall not be compelled

to do so, but shall pay an equivalent for personal service.

Whether to retain, omit, or alter this section was a hot point of debate over

the course of the convention. This debate is a valuable record of how people

of the time who were not Quaker pacifists or war tax resisters tried to come

to grips with the arguments for conscientious objection and conscientious

objection to military taxation.

I’ve reproduced excerpts from this debate in the following pages:

Joseph Chandler, Benjamin Martin, and William Darlington defend the Friends, John Fuller disagrees, and Charles Brown tries to bring things down to earth

John Cummin says William Penn did not found a pacifist state, Ephraim Banks makes a curious Shakespeare allusion, John M’Cahen and Emanuel Reigart stand up for government prerogatives, James Porter puts in his two cents, and Benjamin Martin tries to calm them down

Benjamin Martin and John M’Cahen continue to disagree about the proposed amendment

William Darlington and James Biddle stand up for Quaker consciences and cite precedent, John Fuller notes that the proposed compromise makes no sense on conscientious grounds, James Porter says that it does however jibe better with the U.S. Constitution, John Cummin expresses contempt for the Quaker peace testimony, Ebenezer Sturdevant lands a blow or two himself, Thomas Bell modifies his amendment, and Walter Forward defends the right of conscience

Walter Forward resumes his remarks, Ephraim Banks says conscience has been pushed too far, Emanuel Reigart says Quakers should not enjoy an exclusive state-granted privilege, James Merrill stands up for respecting conscience in the law

Samuel Purviance says it’s a fine and not a tax, George Woodward unleashes the mighty power of his rhetoric (and who is this guy, anyway?), Walter Forward rises to defend himself, and Andrew Cline denies that there is such thing as a right of conscience

Thomas Bell says maybe they should just leave it up to the legislature, but John Cummin isn’t buying that for a minute

James Porter thinks Bell’s proposal is just fine, and Joseph Chandler agrees, but the amendment is rejected

John Cummin can’t resist trying to get in the last word against the dastardly Quakers (and against his exasperated colleagues)

The wha? Everyone knows what the first two amendments are about. What’s

that third one again?

No Soldier shall, in time of peace be quartered in any house, without the

consent of the Owner, nor in time of war, but in a manner to be prescribed

by law.

You’ll have to follow the link above to see how No Third

Solution stretches this amendment to cover the federal government

demanding tax money to maintain a standing army. Seems quite a stretch to me.

Some war tax resisters resist in this way:

They calculate how much federal income tax they owe, then they determine what percentage of income tax revenue the federal government spends on war, and then they hold back that percentage of their income tax while paying the rest.

This is a variety of protest that relies on symbolism and on the emphatic value of civil disobedience.

But sometimes these resisters claim that what they are doing is not merely a protest but is a variety of conscientious objection — an attempt to practically withdraw support from immoral government policies, or to evade complicity with those policies.

Looked at in that way, the tactic they’ve chosen seems disconnected from the ends they claim to be pursuing.

If they withhold 50% of their income tax, for instance, because they believe that that is the percentage of income tax revenue the federal government spends on the military, the remaining 50% that they do pay isn’t any less likely to be spent on the military or to expose the payer to any less complicity.

The separation of the bad money they’ve held back from the good money they’ve sent in is only in their mind.

It’d be like using half a can of orange paint to paint one chair, and half of it to paint another chair, and expecting to end up with a red chair and a yellow chair.

The people who practice this variety of war tax resistance aren’t idiots — they know that the government isn’t doling out each individual taxpayer’s tax dollars one-by-one with the Defense Department last in the queue (“sorry, General, but it looks like we’ve run out!”).

And they’ll acknowledge this if you ask directly.

But from time to time, many seem to forget that they’re engaged in a symbolic protest, and they deploy the rhetoric of conscientious objection to explain their position.

This was a particularly difficult problem with the Quaker war tax resisters I’ve been studying.

The most typical Quaker war tax resistance position went something like this:

We must refuse to pay any tax that is levied for the purpose of supporting war or the military, but we must cheerfully pay taxes for the support of civil government even when that government uses some of that tax money to fund a budget that includes military and war spending.

Or, as “Philalethes” put it: “we ought not to ask Cæsar what he does with his dues or tribute, but pay it freely.

But if he tells me it is for no other use but war and destruction, I’ll beg his pardon and say ‘my Master forbids it.’ ”

When resisters would deploy their most daunting rhetoric of conscience and pacifism to defend the first prong of this forked position, their critics would respond by wondering why such passionate reasoning wouldn’t apply equally well to the second.

Attempts to answer this objection by asserting the harmlessness or blamelessness of paying a mixed tax would then threaten to undermine the force of the conscientious objection argument, which seemed to rely on a heartfelt refusal to be involved even indirectly in bloodshed.

As one critic put it:

Why might they not as well resist the payment of a tax which goes to the support of the army or navy of the United States?

If they have any conscientious scruples at all upon the subject, they must be carried out or they are good for nothing.

What difference is there, in principle, between killing a fellow man in war and paying another man to kill him?

And, again, do not the Friends pay one man to kill another when they pay their share of the general tax towards the support of the government and the means of national defense?

There came to be a hotly disputed science of discerning the difference between war taxes and “mixed” taxes, the former being ones that would trouble a good Quaker conscience to the extent of civil disobedience, but the latter being ordained and blessed by Jesus and the Apostles.

The problem was that the nature of the difference between these taxes was difficult to pin down.

If the government raised taxes across the board as it was going to war and raising military spending to match, was this a war tax, or since it was just going into the general budget as before (although a higher percentage of this budget was being spent on war than usual) was it no less objectionable now than it had been before?

What if the government, in the course of raising taxes, had explicitly said that the latest tax hike was for the war?

Would that matter, and if so, how is it that your conscientious objection might be triggered by something of so little weight as a legislative preamble?

In many cases it was indeed the case that the words uttered while money changed hands were thought to be more important than the actual, practical transaction.

Thus, for instance, the Pennsylvania Assembly would not fulfill requests of money for fortifications or other war expenses, but would respond to these requests by granting money “for the King/Queen’s use.”

In this way, although the practical, real-world effect was the same, the Quaker consciences were spared.

“We did not see it,” one said, “to be inconsistent with our principles to give the Queen money notwithstanding any use she might put it to, that not being our part but hers.”

But what of those militia exemption fines that Quakers so regularly refused to pay?

These were fines that conscientious objectors (or, often, anyone with enough money and better ideas of how to spend his time) could pay in lieu of otherwise mandatory military service.

Most of the writings about Quaker war tax resistance that I’ve collected are about resistance to these fines.

But if the fines went into the general fund just like any other tax, as they sometimes did, on what ground could a Quaker object to the one and not the other?

In fact, the evolution of Quaker resistance to militia exemption taxes underwent an interesting shift over time from conscientious objection to a more confrontational civil disobedience.

At first, Quakers justified their resistance to these taxes by saying that they could neither bear arms nor pay a substitute to bear arms in their place, or that they could not pay a tax that was specifically designated for war purposes as this would mean actively participating in war.

But over time, this justification underwent a shift (one that was subtle enough that I have found no records that try explicitly to justify it).

Quakers came to object to militia exemption taxes even when these taxes went into the government’s general fund, or even if they were specifically designated for humanitarian purposes that Quakers would not otherwise object to.

They objected to these taxes, not because the taxes would make them participants in war but because, as the Meeting for Sufferings of the Philadelphia Yearly Meeting put it in :

Believing that liberty of conscience is the gift of the Creator to man, Friends have ever refused to purchase the free exercise of it by the payment of any pecuniary or other commutation to any human authority.

This is a much more radical position. No longer was resistance to militia exemption taxes just a refusal to participate in the wars and fightings of the powers of the world; instead, it became a notice that those powers had overstepped their bounds when they pretended to regulate and tax conscientious scruples.

People trying to extract war money from Quakers occasionally tried to “hack” this odd protocol by which they could approve of “mixed” taxes in most circumstances.

For instance, in when Benjamin Fletcher tried to get the Pennsylvania Assembly to cough up some money to fight the French & Indians, he wrote:

[I]f there be any amongst you that scruple the giving of money to support war, there are a great many other charges in that government, for the support thereof, as officers salaries and other charges, that amount to a considerable sum:

Your money shall be converted to these uses, and shall not be dipped in blood.

You’ll recognize this as the same sort of promise held out by today’s proponents of the Peace Tax Fund Act:

Give the government your money and in return the government pledges it will spend your money only on the good stuff and will spend someone else’s money on the stuff you don’t like.

It took some fortitude to look at mixed taxes and to say that the mixture of taxes for war with taxes for civil government didn’t wash the blood off the former but further bloodied the latter.

The “epistle” of John Woolman and others to their fellow Friends introduced this position:

[T]hough some part of the money to be raised by the said Act is said to be for such benevolent purposes as supporting our friendship with our Indian neighbors and relieving the distresses of our fellow subjects… and we could most cheerfully contribute to those purposes if they were not so mixed that we cannot in the manner proposed show our hearty concurrence therewith without at the same time assenting to, or allowing ourselves in, practices which we apprehend contrary to the testimony which the Lord has given us to bear for his name and Truth’s sake.

Job Scott “believed a time would come, when Christians would not so far contribute to the encouragement and support of war and fightings as voluntarily to pay taxes that were mainly, or even in considerable proportion, for defraying the expenses thereof.”

And Moses Brown worried that this might mean completely unraveling the distinction that allowed Quakers to think of themselves as both conscientiously objecting to supporting war, but also obeying the Biblical instructions to “render unto Caesar” and “pay ye tribute”:

[S]ome Friends refuse all taxes, even those for civil uses as well as those clear for war and others that are mixed, and thereby dropping our testimony of supporting civil government by readily contributing thereto, it has been a fear whether this variety of conduct won’t mar rather than promote the work.

Could we be more united in the ground of our testimony and in our practice in it, I should have more hopes of its speedy obtaining in society.

A time will doubtless come when a smaller proportion will be for war than at present when the greater part being for civil uses, friends may pay as there is and ought to be according to the apostle, a conscientiousness in paying to the support of civil government as well as refuse that for war…

Then he anticipates the “Peace Tax Fund” idea, or something like it:

…to refuse the payment of such when even a lesser part be mixed for war before we applied to the authority to separate them would not at present be my place, but probably before that time come when the lesser part will be for war friends may be agreed to ask a separation which, if it should be refused, we might be united in refusing even those the greater part of which may be for civil uses.

Joshua Maule sparred with other Friends about this issue.

When the government added a war surtax to the regular tax bill, many Quakers were untroubled by paying it: although it bore the name of a war tax, it was collected in the same way as the general tax they’d been paying all along, and like that tax, it was deposited in the general fund and spent at the whim of the legislature.

But Maule felt that by calling it a war surtax, the government had brought it into inevitable conflict with the Quaker conscience, and he lashed out at more accommodating Friends.

“[T]hat [tax] for the war and bounty was not mixed with any other,” he wrote, “until those who paid it voluntarily mixed it themselves and thereby made it their own act to pay the price for men to go forth to the field of human slaughter.”

The way Maule figured it:

[I]f I owe a just debt, I must pay it; if the person receiving the money uses it for a bad purpose, the accountability is with him; but if he demand money of me avowedly to be used in any way to the plundering of my neighbor, destroying his property, or taking his life, then if I furnish money thus demanded I become an accomplice in the evil work and accountable for the sin.

I consider our civil taxes a just debt that should be promptly paid, but I am satisfied that no human authority has either a moral or a religious right to demand of me money or means of any kind to aid in destroying the lives and property of my fellow-men.

But note that Maule only refused to pay the surtax — that portion of his total tax that was “avowedly” being raised for war.

Certainly, though, the government was “avowing,” with every budget, that it was going to be spending some portion of both the surtax and the regular tax on the very same things.

And so those who disagreed with Maule shot back that he was playing plenty of money “to aid in destroying the lives and property of [his] fellow-men” and he knew it, so won’t he please give it a rest.

Nathan Hall put it well when he wrote to Maule:

[W]hether we pay less or more of that tax, a certain proportion of it goes for military or war purposes; and it avails nothing to say: “We did not pay it for that purpose, and if wicked and bad men so apply it, it is their lookout, not ours.”

We can say that of all the tax as well as a part.

If the law had said so many dollars to be raised for war purposes, instead of such a portion of each and every dollar, it would have been plain and not a mixed tax.

Such is not the case; it is all collected together and thrown into one general treasury, where it remains till it is apportioned out for the different purposes designated by the law.

There might be as many different classes of objectors or withholders of tax as there are purposes for which it is appropriated, and the officers of government know nothing of the nature or cause of any of them; they would only know there was a deficiency, and apply that on hand in due proportions for their different purposes, and the deficiency, when collected, in like manner.

To illustrate it more fully I will suppose a case which I believe is strictly parallel, thus:

We both have a testimony against the use of ardent spirits, but are, being very thirsty, placed in a situation where we can get no water except some that has a small portion of whiskey in it.

Being under the necessity of taking something, you may, by inquiry and calculation, find what proportion of the objectionable article is contained in it, and leave just that much in your bowl; while my understanding will be that in partaking I partake of both good and bad, and in refusing refuse both.

So that with me the question is and has been, not what portion I should pay so much as whether any at all.

When I was speaking at the Abundance League a while back about my tax resistance, one horrified liberal — alarmed at the enthusiasm those around her were showing for the stand I’d taken — launched into a defense of government spending on things like roads and general infrastructure.

I thought what a shame it was that such valuable things as these had to be bought at such high prices from their monopoly supplier so as to support their “one Iraq war free with purchase” promotion deal.

A new edition of NWTRCC’s newsletter, More Than a Paycheck, is out.

The contents include:

Some brief notes on the “economic stimulus” checks, frivolous filing warnings from the IRS that some war tax resisters have been receiving, the IRS’s expanded snitch payment program, limits on the IRS’s ability to seize pensions before they come due, and increasing IRS interest in offshore bank accounts

Some news about the status of the Religious Freedom Peace Tax Fund Act and about Joshua Goldberg’s war tax resistance in Canada

Notes from resisters, including Greg Reagle responding to critics who say that war tax resistance isn’t effective, Melissa Jameson relating stories about how her resistance relates to those around her, and a summary of the story of resister Charles Merrill

Some committee business including an announcement of the upcoming national meeting in Eugene, Oregon in and an invitation to readers to help shape the future direction of the War Tax Boycott project

There were about 60 people from 14 countries — about standard for these

conferences. Sadly I have to report that our efforts to get George Rishmawi

from Palestine to the conference ended in a refused visa, so that he could

not travel to the conference. The British organizers tried really hard to get

thru the red tape but to no avail. Two people from Ghana were refused visas

also.…

…As with most conferences (at least in my humble opinion) the time spent

talking with folks at meals and between the organized sessions is at least as

important as anything that comes up in the sessions. Quite a few of my

conversations were with individuals from other countries who are war tax

resisters, who refuse to pay at least some of taxes due to their respective

governments. Many combine their refusal with redirecting the money to some

kind of fund for nonviolent defense or peace-building funds.

As we have found in the past, it is more difficult to resist in most

countries because of the way taxes are pulled from paychecks. Those who

resist tend to be self-employed. In general, collection is much faster in

other countries than has been our experience in the

U.S. (at least up

to now), and many organizers at this conference make no effort to build

WTR, seeing

it as futile. The majority of people at the conference are working on

peace tax fund

campaigns or looking for ways to take their complaint of being forced to pay

for war through some court system or

U.N. body. I

think 5 of the Peace Tax Seven

were in attendance, and they are slowly making their way into the European

Court of Human Rights. Daniel Jenkins from the

U.S. reported on

the effort to bring a formal complaint to a

U.N. body. The

Germans have a resister or two in their circles, but are focusing on a new

effort of 10 people to take a complaint to a German high court based on the

budget being a violation of fundamental

rights because of the military spending. The Germans are trying to get away

from appealing through the tax system and instead trying this more direct

route to the government officials who create the budget. In Norway peace tax

fund campaigners are appealing to their local councils; if the council

accepts their complaint as an “initiative of national interest” then the

council can send a complaint up to the next level of the government system.

I attended two workshops that related more generally to organizing, with both

having some focus on how to widen our efforts. Groups and campaigns in every

country seem to face issues similar to our own. “How to bring in more young

people” was the topic of one workshop. While no group seemed to be doing any

better than many of us here in the

U.S., many are

looking for answers in the internet, such as getting into Facebook and other

networking sites, and upgrading our websites. The Danish peace tax fund

campaign has been working with the model

U.N. program in

high schools with some success at making “the right not to pay for war” a

topic in those discussions. One person noted that the activists groups that

seem to be most successful at drawing in young people are the ones that give

new members something to do immediately and regularly. There was also a good

deal of discussion of language, in particular the use of the word

“conscience,” and whether that is a word that resonates with young folks

today. Because the hosting group was Britain’s “Conscience: the peace tax

campaign,” it was the local folks who were having this discussion among

themselves and also bringing it to the conference. “Taxes for Peace Not War”

was a slogan that many people appreciated due to the positive spin.…

…There were small group sessions to talk about the common ground between war tax resisters and peace tax campaigns and develop ideas about how we can all work together more across international boundaries.

I don’t know if any of the groups came up with any brilliant insights on this.

My group did spend quite a bit of time comparing our tax systems and learning more precisely what each of our organizations do.

It’s hard to figure out how to work together without understanding more about each situation; there’s a lot of confusion about why there is such a “strong” war tax resistance movement in the U.S. as compared to other countries.