How you can resist funding the government →

about the IRS and U.S. tax law/policy →

how the government deals with tax resisters →

interest and penalties for failure to pay

As I mentioned I’ve decided to stop paying my self-employment tax.

I just got my first letter from the IRS indicating that they noticed.

When I filed my 1040, I indicated that I believed that I was supposed to pay $3,271 in self-employment tax last year.

I paid $2501.01 of that, and then decided to stop. $769.99 was still due.

The IRS has charged an additional penalty of $7.70 and interest of $6.52.

The penalty was dated , based on a ½% monthly charge.

The interest runs from at 7% yearly.

I’m getting 4.15% on my savings account, so to figure out what I’m really being penalized here you have to subtract what I’m earning on the money I’m not paying them from the penalty they’re imposing.

Naïvely (that is, not adjusting for compounding), then, the real penalty per day is:

amount I owe × (daily penalty percent + daily interest percent − daily interest I get on the same amount in my savings account)

or:

amount I owe × (0.0164% + 0.0191% − 0.0114%) = amount I owe × 0.0241%

Or, in short, the IRS intends to penalize me something on the order of two-and-a-half cents per hundred dollars I owe, per day.

My unpaid self-employment tax will continue to balloon with each passing year.

Come , I’ll probably owe another $3,500–$4,000 in self-employment tax, with another $150 in penalties on top of that.

Assuming the penalty rate is roughly the same then as it is now, the penalties on this new amount will run something like $1.15 per day.

That strikes me as something approaching if not surpassing real money, and might be enough to dissuade me from this part of the project if it weren’t for two other considerations:

They have to actually get their hands on the money.

It’s gonna cost ’em.

The first of these considerations is at this point pretty much a hypothetical.

I haven’t gone to any trouble to hide my assets, and I’m sure in this post-Patriot Act era, it won’t take much effort for the IRS to find my bank account.

Still, if they follow their standard operating procedure, it will cost ’em $0.45–$4.79 every time they send me one of their notices, and even more if they have to go to the trouble to seize the money.

If they turn me over to one of the private debt collectors they’re considering, these bounty hunters will take about a quarter of what they collect for themselves.

So while this may not be a smart investment move for me personally, when it comes to my goal of keeping as much of my money as I can out of the hands of Uncle Sam, the numbers still may add up.

Another month, another letter from the IRS.

According to their records, I still owe them $793.40, to which they have added a penalty of $3.84 and interest of $5.35.

I haven’t had a letter from the IRS , but I got a new one .

It only covers the unpaid tax from my return and makes no attempt to combine this with what I didn’t pay the previous year.

This seems to me a strange way to go about it, but I don’t make the rules.

When I filed my return, it showed that I was assessed $3,922 in taxes ($3,952 in self-employment tax minus $30 for the phone tax refund).

To this was added $172 as a penalty for failure to pay the self-employment tax in quarterly installments during the year.

This latest IRS notice shows an additional penalty of $39.22, “for Paying Taxes Late” (aren’t they optimistic!), which is based on two months of ½% of that $3,922 per month, which will continue to accumulate until it reaches 25% of $3,922 ($980.50) at which point the penalty maxes out.

Also added is $37.13 in interest, which they’re currently racking up at an 8% annual rate and which doesn’t have a ceiling and so will continue to rise until they seize the money from me or until the statute of limitations runs out.

They also sent along a copy of Form 2210: Underpayment of Estimated Tax by Individuals, Estates, and Trusts and an instruction booklet for that form.

These would be useful if I wanted to contest the $172 penalty (if, for instance, I earned all my money in the last quarter of the year and this was the reason why I didn’t make quarterly estimated tax payments).

Finally, they sent along the one-page Publication 1: Your Rights as a Taxpayer and a small Notice 1212 promoting their automated telephone service.

I don’t plan to reply to this.

The numbers all seem accurate, and their avenues of appeal don’t really apply to someone in my situation.

Between this and what I didn’t cough up last year, the IRS is now after me for roughly $5,000.

I got two certified “sign here please” letters from the IRS, one concerning the taxes I didn’t pay for , the other for . Other than the difference in the years and figures, they were identical packages:

A copy of Notice 1219-B: Notice of Potential Third Party Contact which lets me know that the IRS “may contact other persons, such as a neighbor, bank, employer or employees, and will generally need to tell them limited information, such as your name.”

It also tells me that I have the right to ask for a list of the people they contacted.

Later on in the process, I’ll try to remember to do this.

A copy of Notice 1212 which encourages me to use the IRS’s automated telephone service.

A copy of Publication 594: What You Should Know About The IRS Collection Process and of Notice 1367: Updated Information for Publication 594 which lets me know that the fee they charge for entering into a pay-by-installment plan has gone up and the rules for Offers in Compromise have changed.

A three-page letter listing the balance due, itemizing the latest interest and penalties (though not the cumulative totals of these, which I’ve had to calculate myself by going back to the figures on previous notices), and giving the same “Urgent !!” message as I got .

A hopeful return envelope.

I refused to pay $769.99 of my self-employment taxes for .

Since then, the IRS has added $100.09 in penalties and $84.02 in interest, bringing the total to $954.10.

I refused to pay an additional $4,094 for , which includes a $172 penalty for failure to pay the self-employment tax in quarterly installments.

Since then, the IRS has added $78.44 in penalties and $101.60 in interest, bringing the total to $4,274.04.

So, in sum, the IRS is after me for $5,228.14, of which $536.15 is interest & penalties.

For previous installments in the nasty-letters-from-the-IRS series, see:

I got another one of those certified, sign-here-please letters from the IRS .

This one was substantially more beefy than the previous ones:

CALL IMMEDIATELY TO PREVENT PROPERTY LOSS

FINAL NOTICE OF INTENT TO LEVY AND NOTICE OF YOUR RIGHT TO A HEARING

WHY WE ARE SENDING YOU THIS LETTER

We’ve written to you before asking you to contact us about your overdue taxes.

You haven’t responded or paid the amounts you owe.

We encourage you to call us immediately at the telephone number listed above to discuss your options for paying these amounts.

If you act promptly, we can resolve this matter without taking and selling your property to collect what you owe.

We are authorized to collect overdue taxes by taking, which is called levying, property or rights to property and selling them if necessary.

Property includes bank accounts, wages, real estate commissions, business assets, cars and other income and assets.

WHAT YOU SHOULD DO

This is your notice, as required under Internal Revenue Code sections 6330 and 6331, that we intend to levy on your property or your rights to property 30 days after the date of this letter unless you take one of these actions:

Pay the full amount you owe, shown on the back of this letter.

When doing so,

Please make your check or money order payable to the United States Treasury;

Write your social security number and the tax year or employer identification number and the tax period on your payment; and enclose a copy of this letter with your payment.

Make payment arrangements, such as an installment agreement that allows you to pay off your debt over time.

Appeal the intended levy on your property by requesting a Collection Due Process hearing within 30 days from the date of this letter.

WHAT TO DO IF YOU DISAGREE

If you’ve paid already or think we haven’t credited a payment to your account, please send us proof of that payment.

You may also appeal our intended actions as described above.

Even if you request a hearing, please note that we can still file a Notice of Federal Tax Lien at any time to protect the government’s interest.

A lien is a public notice that tells your creditors that the government has a right to your current assets and any assets you acquire after we file the lien.

We’ve enclosed two publications that explain how we collect past due taxes and your collection appeal rights, as required under Internal Revenue Code sections 6330 and 6331.

In addition, we’ve enclosed a form that you can use to request a Collection Due Process hearing.

We look forward to hearing from you immediately, and hope to assist you in fulfilling your responsibility as a taxpayer.

That came in duplicate, with the sum of my unpaid taxes listed on the back.

Uncharacteristically, they included both years in the same letter (often they send out one letter per year, so that long-time resisters may get ten certified letters on a single day):

Account Summary · DAVID M GROSS · 567-68-0515

Type of Tax

Period Ending

Assessed Balance

Accrued Interest

Late Payment Penalty

Total

Total Amount Due

$5,375.49

1040

$784.21

$89.86

$107.79

$981.86

1040

$4,170.35

$125.23

$98.05

$4,393.63

Their “Assessed Balance”s seem a little high to me. I’m assuming that’s supposed to be the amount I owed when I filed around April 15th of the following year.

My records say these amounts were $770 and $4,094.

So either they’ve got a different idea of “Assessed Balance” than I do, or they’ve got a bug, or they’re trying to pull a fast one by ratcheting up the values in the hopes that I won’t notice.

Quite possibly, if I don’t object, they’ll be able to stick me with whatever numbers they come up with.

Dirty pool, but I wouldn’t put it past them.

The $4,000+ that I was assessed for includes a $172 penalty for failure to file my quarterlies that year, so the total interest and penalties that I’ve accrued so far by refusing to pay taxes is almost $600.

For previous installments in the nasty-letters-from-the-IRS series, see:

complaining about my past-due amount and threatening to issue a levy, I noticed that their accounting seemed a little off.

They’d divided up what they thought I owed them into three categories: “Assessed Balance,” “Accrued Interest,” and “Late Payment Penalty.”

But the “Assessed Balance” seemed to me to be higher than it should have been.

As it turned out, the “Assessed Balance” figures in this most recent letter included the interest and penalties the IRS had added in the first letter they sent me.

So I sent them a note about this .

This was the first time I’d responded to any of their nagging.

My note read:

To whom it may concern:

I recently received the enclosed “Letter 1058” (“Final Notice of Intent to Levy”).

I am writing to dispute the amounts involved.

According to the table on the back of this letter, the “Assessed Balance”s for tax years were $784.21 and $4,170.35 respectively.

According to my records, these should be $770 and $4094.

I believe you have erred by incorrectly including some of the early penalty and interest amounts in the “Assessed Balance” total, rather than correctly adding those to the totals in the “Accrued Interest” and “Late Payment Penalty” columns.

For example, the first “Request for Payment” letter I received from you regarding my unpaid balance correctly showed $769.99 as my assessed balance for that year, and added $7.70 in penalty and $6.52 in interest, for a total of $784.21. This matches the current figure you are reporting as my “Assessed Balance” for that year.

I suspect this is not coincidental, and that this is probably the source of the error for the balance as well.

I have not attempted to double-check the interest and penalties figures that you listed in the recent “Letter 1058” and so I reserve judgment as to their accuracy.

But given the discrepancy in the baseline figure, I would not be surprised to find that these are inaccurate as well.

It occurs to me that “Assessed Balance” may be a term with a special meaning within the IRS and that I may be wrong in presuming to apply a common-sense definition to it.

If so, please let me know what the correct use of this term is.

Otherwise, please correct your figures and send me an accurate accounting of my current balance.

Sincerely, David Gross

On , I got the IRS’s reply:

Dear Taxpayer [sic]:

Thank you for your correspondence received .

We have not resolved this matter because we haven’t completed all the processing necessary for a complete response.

However, we will contact you again within 45 days with our reply.

You don’t need to do anything further now on this matter.

If you have a current installment agreement with us, please continue to make scheduled payments while waiting for our response.

Even if you do not have a formal installment agreement, you may make payments to reduce the balance owed and minimize interest and penalty charges.

To help us apply payments properly, make checks or money orders payable to the United States Treasury, and clearly print your name, the tax year on which you owe, and your Social Security or Employer Identification number on the check.

Following this was some how-to-contact-us boilerplate, then “We apologize for any inconvenience we may have caused you, and thank you for your cooperation.”

The letter was signed by the department manager for Automated Collection System (ACS) Support, Collection Operations.

They also, in their optimism, sent me a payment voucher, noting (in all-caps, which I’ll spare you), that I should “cut out and return the voucher at the bottom of this page if you are making a payment, even if you also have an inquiry.”

I believe, in IRS lingo, this is known as an “interim response” — specifically a letter 2645C. My best guess is that a low-level IRS employee scanned my letter in, dated it, gave it a rough categorization, and entered it into their “Correspondence Imaging System” database, but no qualified employee has had a chance to look at it yet, so their computer system automatically generated a “your call is very important to us, please stay on the line” message for me.

Sorry if this is dull, but I hope to keep posting a full account of my interactions with the IRS here so that people know what they can expect.

Thusfar, these encounters have hardly been of the edge-of-your-seat variety.

For previous installments in the nasty-letters-from-the-IRS series, see:

afternoon I got the first communication from the IRS that did not appear to have been automatically generated by computer.

It was a large-sized envelope that was mailed from the IRS’s Covington, Kentucky office at a cost of 97¢ and that had my name and address lettered on the front by hand in ball-point pen.

Inside, though, the personal touch was less-evident.

Enclosed were four 8½″x11″ sheets, containing two printouts from the IRS’s internal Employee User Portal web application.

The IRS employee who generated these printouts had “IRS Employee Number: PQVCB”.

The printouts show my tax balances as of .

My best guess is that this is their attempt to answer my letter of in which I disputed their figures.

But these printouts merely restate their figures without addressing the discrepancy I pointed out to them.

And there is some new strange accounting that leaves me scratching my head.

The numbers are fairly straightforward, if you accept their idea of what the “Assessed Balance” is:

ACCOUNT BALANCE:

784.21

ACCRUED INTEREST:

89.48

AS OF:

ACCRUED PENALTY:

107.80

AS OF:

ACCOUNT BALANCE PLUS ACCRUALS:

981.49

** INFORMATION FROM THE RETURN OR AS ADJUSTED **

EXEMPTIONS:

01

FILING STATUS:

Single

ADJUSTED GROSS INCOME:

14,064.00

TAXABLE INCOME:

5,864.00

TAX PER RETURN:

3,271.00

SE TAXABLE INCOME TAXPAYER:

21,375.00

SE TAXABLE INCOME SPOUSE:

0.00

TOTAL SELF EMPLOYMENT TAX:

3,271.00

RETURN DUE DATE OR RETURN RECEIVED DATE (WHICHEVER IS LATER)

PROCESSING DATE

TRANSACTIONS

CODE

EXPLANATION OF TRANSACTION

CYCLE

DATE

AMOUNT

150

RETURN FILED AND TAX ASSESSED

$3,271.00

430

ESTIMATED TAX DECLARATION

−$625.25

430

ESTIMATED TAX DECLARATION

−$625.00

430

ESTIMATED TAX DECLARATION

−$625.38

430

ESTIMATED TAX DECLARATION

−$625.38

276

FAILURE TO PAY TAX PENALTY

$7.70

196

INTEREST ASSESSED

20062008

$6.52

971

INTENT TO LEVY COLLECTION DUE PROCESS NOTICE LEVY NOTICE ISSUED

$0.00

In the tax year, though, something

unexpected crops up:

ACCOUNT BALANCE:

4,170.35

ACCRUED INTEREST:

123.34

AS OF:

ACCRUED PENALTY:

98.05

AS OF:

ACCOUNT BALANCE PLUS ACCRUALS:

4,391.74

** INFORMATION FROM THE RETURN OR AS ADJUSTED **

EXEMPTIONS:

01

FILING STATUS:

Single

ADJUSTED GROSS INCOME:

13,466.00

TAXABLE INCOME:

5,016.00

TAX PER RETURN:

3,952.00

SE TAXABLE INCOME TAXPAYER:

25,829.00

SE TAXABLE INCOME SPOUSE:

0.00

TOTAL SELF EMPLOYMENT TAX:

3,952.00

RETURN DUE DATE OR RETURN RECEIVED DATE (WHICHEVER IS LATER)

PROCESSING DATE

TRANSACTIONS

CODE

EXPLANATION OF TRANSACTION

CYCLE

DATE

AMOUNT

150

RETURN FILED AND TAX ASSESSED

$3,952.00

766

REFUNDABLE CREDIT

−$25.61

776

INTEREST DUE TAXPAYER

−$4.39

170

ESTIMATED TAX PENALTY

$172.00

276

FAILURE TO PAY TAX PENALTY

$39.22

196

INTEREST ASSESSED

$37.13

971

INTENT TO LEVY COLLECTION DUE PROCESS NOTICE LEVY NOTICE ISSUED

$0.00

What are these two items about?

766

REFUNDABLE CREDIT

−$25.61

776

INTEREST DUE TAXPAYER

−$4.39

Here again, I’ve only got guesswork to go on.

Like most people, I applied for a $25.00 refundable credit for overpaid telephone excise taxes.

That was the only refundable credit I applied for, and it’s close enough to the $25 in the table above that I have to guess that’s what it’s referring to.

Where the other 61¢ comes in, I have no idea.

And how an additional interest charge comes into play is a mystery to me as well.

Do you suppose they’ll keep compounding this interest as well until they manage to seize money from me or until the statute of limitations runs out?

In any case, it’s bafflingly weird.

It looks like if you paid your taxes like you were supposed to , you could get a $25.00 credit, but if you filed your taxes but didn’t pay, the IRS computer says you’re due a $30.00 credit instead!

And “PQVCB” is a number.

And “Assessed Balance” equals the actual assessed balance plus the first of the penalty & interest values but not the rest of them.

Strange things happen in the IRS’s Mathmagic Land.

For previous installments in the nasty-letters-from-the-IRS series, see:

I got another CP 504 notice from the IRS a couple of days ago.

Nothing exciting or interesting, just them letting me know that I’d neglected to include a check with my return — pretty much the same package I described in my post but with a new set of numbers attached.

For the record, I didn’t pay $3,695 in , and so I got dinged with an estimated tax penalty of $168 when I filed my 1040. , they’ve added an additional $62.94 in interest & penalties.

His latest is #86: Withdrawal of bank deposits, and he shares the story of how he’s withdrawn the money from his IRAs in support of his tax resistance.

…the IRA system is part of the whole IRS structure and allows me another chance to take money that I can refuse to pay taxes (and penalties) on now as protest.

Sure, when they catch up with me it adds to my pile of infractions, but that’s part of the point, and I’ll have pulled even more of my consent from the matrix of control and war enabling the government’s revenue represents.

Part of my strategy for keeping my money out of the government’s hands has been to use tax-deferred retirement accounts like the IRA.

One of the unintended consequences of this is that I now have a retirement nest egg that may hatch into a sitting duck for IRS seizure.

Under the rules of the game, (with some exceptions) I can’t withdraw this money until retirement-time.

Meanwhile it sits in a brokerage account, vulnerable to government seizure, and there’s precious little I can do to protect it.

If I were to withdraw all the money, NTodd-like, the IRS would add a big hunk of taxes due and penalties to what I’m already deciding not to pay voluntarily.

I suppose I could do this, or at least try to do it (I’m worried that there may be some automatic-withholding process that gets triggered when you try to cash in an IRA early and all at once).

Then I could keep the money in a mattress, metaphorically-speaking, and safe from the grasp of the IRS.

This is a bigger commitment than I’m prepared to make just now, but I’m considering it.

The IRS Miscalculates Interest and Penalties But Fails to Correct These Errors Due to Restrictive Abatement Policies.

A TAS study has found that the IRS is miscalculating the failure to pay penalty and could be negatively impacting about two million taxpayer accounts annually.

Moreover, the IRS’s manual calculations of interest yields an accuracy rate of only 67.7 percent, which means nearly one out of three restricted interest accounts are incorrectly computed.

The IRS is aware of, but has failed to correct, certain systemic problems that cause penalty and interest miscalculations.

These incorrect calculations lead numerous taxpayers to believe they have fully paid what the IRS says they owe, only to receive subsequent bills for accruals of interest, penalties, or both.

The IRS bears the cost of these inaccurate calculations, not only through rework by employees but also by taxpayers’ reduced confidence in the IRS.

The National Taxpayer Advocate recommends that the IRS consider allocating adequate resources toward planning and programming to resolve common penalty and interest computation issues, revising pertinent Internal Revenue Manual sections so all taxpayers are entitled to accuracy reviews of interest and penalty calculations, and re-evaluating the overly complex restricted interest procedures to make certain that all taxpayers receive accurate interest charges.

I know in my case I’ve suspected that the IRS has been figuring the penalties & interest incorrectly — in part because they have incorrectly wrapped the first dose of penalties & interest into the initial assessment.

However, the process isn’t transparent enough for me to verify my suspicions.

Among the other things in the TAS report were a call to eliminate the outsourcing of delinquent tax collection and a recommendation that the IRS develop some way to tax transactions taking place in virtual worlds such as multi-player on-line video games.

I got four letters from the IRS that purported to sum up my total unpaid taxes, along with interest & penalties, for , , , and .

Their numbers didn’t add up consistently even within their own printouts, though, so I thought I’d dig a little deeper.

I requested my “tax account transcripts” for those years from the IRS.

(This is easy to do: you can request your transcripts from the IRS website.)

They arrived on (in four separate envelopes, naturally, as the agency’s way of reminding me how respectfully it spends taxpayer dollars).

These are interesting artifacts, but in many ways they only add to my bewilderment.

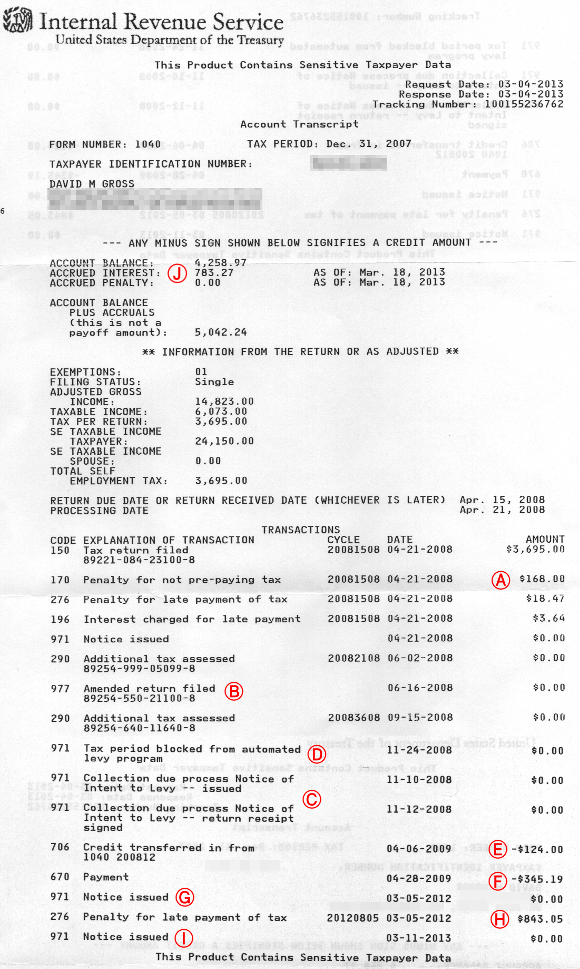

I’ll show you one of the transcripts they sent me below, and add some comments and explanations.

The original transcript was two pages — I’ve pasted them together in this illustration.

I added the red circled letters for my annotations below:

First, a note: In there was

a weird glitch in which the

IRS

erased the “personal exemption” from my

return. Perhaps somebody tried to claim me as a dependent on their tax return,

or accidentally filled in my social security number for that of their actual

dependent, or maybe it was just a snafu — I

never did get an explanation. I simply filed an amended return reinstating

my personal exemption and left it at that. It didn’t effect the bottom line in

any case, so I didn’t give it much thought afterwards.

The transcript shows my initial tax assessment ($3,695.00), the penalty

immediately assessed on me for not having paid any of this in quarterly

installments ($168), the initial late payment penalty for not having enclosed

a check with my tax return ($18.47), and a small amount of interest that had

accumulated at the time of their first delinquency notice to me ($3.64). All

of that matches my records. (Ⓐ)

In June they erased my personal exemption, then took note of my amended return

in which I reinstated it (Ⓑ). I didn’t get

official word that they’d accepted my

amended return until . I think

their phrase for “we changed the numbers on your tax return” is “Additional

tax assessed” since it appears twice on the transcript around here, once to

omit the personal exemption and once to reinstate it, though neither of these

occasions actually resulted in an assessment of additional tax.

On I got an “Intent to Levy” letter from the

IRS for

the tax year. This also does not show up on

the transcript. That letter listed $166.28 in accumulated penalties and $98.46

in accumulated interest, and asserted that my original tax due was $3,885.11

(which actually is the amount of my original tax due, plus the failure to file

quarterly penalty, plus the initial late payment penalty, plus the first

amount of interest that accumulated).

On I got a “final notice of intent to levy” letter. This

is mentioned in the transcript: both the date it was issued, and the

date the

IRS

was notified that I signed for the letter (Ⓒ). By this time, the accumulated

penalties & interest on the original $3,695 tax bill had risen to a bit

over $572.

Here something peculiar shows up in the transcript: “Tax period blocked from

automated levy program” (Ⓓ). This, just two weeks after they’d issued me a

“final notice of intent to levy.” I’m not sure how to interpret this. (Note

also that this appears out of chronological order in the transcript, just from

perverseness I suspect.) There’s also one of these on my

transcript.

When I filed my return in (for the

tax year) I had so little income to report

that I actually was one of those “lucky duckies” who not only owed no taxes

but qualified for a refundable earned income tax credit: a whole $124. The

IRS

seized this refund and applied it to my unpaid

taxes. This shows up on the transcript (Ⓔ).

They also credit me for a “Payment” of $345.19 on

(Ⓕ). This was actually

a levy of a bank account of mine…

so apparently that “block” issued in

had been released or had expired

by then, or perhaps this levy was not one of the “automated” variety.

I got another letter from the

IRS in

complaining about

the unpaid balance, and then

another in

. These don’t show up in the

transcript either.

The

IRS

tried to seize another bank account , but I’d long since closed it. By then, the interest and

penalties had risen to $985.14. Neither an indication of the levy attempt,

nor any amounts of interest & penalties from this period show up on the

transcript.

The next thing that does show up in the transcript, after

, is

a “reminder of overdue taxes” that they

sent me (Ⓖ). This is

accompanied, in the transcript, with a late payment penalty of $843.05 (Ⓗ).

The transcript also notes

the letter it sent me

, though it gets the

date wrong (Ⓘ).

The transcript also has a summing-up section (Ⓙ), which just makes things

worse:

ACCOUNT BALANCE PLUS ACCRUALS

(this is not a payoff amount): 5,042.24

Why does the interest “accrue”, but the penalty just gets added to the account

balance? If they just are going to add the penalty to the account balance, why

do they bother to have an “accrued penalty” line on the transcript? Why, if

this is their policy, do I only have a zero accrued penalty amount on my

and

transcripts, while my and

transcripts do show accrued

penalties?

The account balance does seem to add up to my original tax owed plus

that original set of penalties and interest (Ⓐ), plus the $843.05 in penalties

(Ⓗ), minus what they managed to seize from me (Ⓔ) & (Ⓕ). I can’t tell you

how surprised I was to find some set of numbers on the page that added up to

another number on the page in a semi-intuitive way, though it took me a while

to develop the correct formula, and I couldn’t tell you why they stuff that

original interest amount in there.

I was a little puzzled at first as to why they stopped assessing penalties

, but I think by that point the

penalty had reached its legal maximum — 25% of the unpaid amount. From here on

out there will be no more penalties on my

taxes, though the interest will continue to accrue.

Congress has engaged in its traditional year-end brinkmanship, passing a set of

retroactive extensions of popular tax breaks. These also included some changes

that may be of interest to tax resisters. For example:

Tax penalties for failure to file and failure to pay will now be indexed

for inflation, as of .

Congress has created a new variety of tax-advantaged savings accounts,

designed to help people fund accounts for disabled people. If I’m

interpreting what I’ve read about this correctly, the tax advantages are

modest: deposits to these trust funds are not deducted from taxable income,

but any investment gains on the amounts in the funds, as well as the

principle, are not taxable to the disabled person they are given to if they

are withdrawn for the purposes of paying the qualified expenses of that

person.

Meanwhile, the IRS has begun pronouncing doom and gloom as a result of the latest cuts to its budget.

Quick to appeal to American’s bottom-line, IRS Commissioner John Koskinen said that people may experience delays in getting their income tax refunds.

With any luck this will encourage more people to reduce their withholding so they aren’t owed refunds at tax filing time.

Koskinen says the cuts will hurt the IRS enforcement arm:

“In some ways,” he said, “these budget cuts are really a tax cut for tax cheats.

Because to the extent we have fewer people to audit and enforce the tax code, that means some people cutting corners on their taxes or not complying are going to get away with it.”

Ruth Benn reflects on “The Mysterious Ways of the IRS” — the agency seems arbitrary and unpredictable at times in the ways it responds to war tax resisters.

The three activists who boldly broke through security at the Oak Ridge nuclear weapons plant in have had their sabotage convictions reversed on appeal and are no longer being imprisoned.

One article about their successful appeal concluded:

“They are still obligated to pay the government a fine of $52,953 for the break-in at Y-12.

But they took vows of poverty decades ago, don’t have bank accounts, and have neither the means nor the intention of paying it.”

The War Tax Talk blog has reprinted an op-ed debate that was published in the Sunday Republican of Springfield, Massachusetts back in .

It features Juanita Nelson dueling with a U.S. Air Force Reserve Lieutenant-Colonel over the question: “Is it ever right to refuse, on principle, to pay taxes?”