Tax resistance in the “Peace Churches” →

Mennonites / Amish →

Cornelia Lehn

’s Picket Line

was all about Mary McDowell, but it also briefly mentioned three people

involved in the early years of the modern American war tax resistance movement

whom I hadn’t heard of before: Sander Katz, Edith Aldis, and Gerhard Friesen.

You’d think a name like “Sander Katz” would make for easy Googling, but in fact there is a “Sandor Katz” who is well-known today for, for instance, his fine do-it-yourself guide Wild Fermentation.

Google tends to want to assume you’re just misspelling his name if you try to hunt for “Sander Katz.”

Katz is listed as the editor of a collection of Freud’s essays “on war, sex,

and neurosis” with an introduction by

Paul Goodman.

He is also listed as one of two editors of Complex: The

Magazine of Psychoanalysis and Society (and he’d occasionally

contribute articles as well, for example: “Comparative Sexual Behavior: Is

orgasm for the human female normal?”). He was also on the editorial committee

of a magazine called Alternative that published

and was associated

with the “Non-Profit Association of Libertarians” and the “Committee for

Non-Violent Revolution.” Other members of that committee included war tax

resisters David Dellinger, Ralph DiGia, and Roy Kepler.

In , the syndicated columnist

Robert Ruark spent

several column inches denigrating Katz, who had just been sentenced to a one-year prison term for refusing to register for the

military draft (and then Ruark put out

another column’s worth when Katz was released eight months later).

“I know something about this particular rugged individualist,” Ruark wrote,

“who served 19 months in jail during the last war for refusal to report for

induction. His name is Sander Katz, and he is one of the long-hairs who stroll

the [Greenwich] Village streets, lost in reverie and a turtle-neck sweater.”

Katz was imprisoned because he said he opposed the draft on “social, political,

and philosophical grounds” and the law at that time only recognized

conscientious objection for religious reasons.

, Katz, along with several dozen

others, burned his draft card during a “Break With Conscription Committee”

demonstration in New York City. , Katz was arrested, along with several others, for picketing

at a draft registration center.

I found a few more newspaper articles about Edith Aldis, all based on the same

template. The Long Island Star-Journal of

for instance, which also

mentions Gerhard Friesen:

Topeka,

Kan.

(UP) — Kansas

Internal Revenue officials had two “conscientious objectors” on their hands

today when Miss Edith Aldis and the

Rev. Gerhard Friesen defied

federal income tax laws on grounds that “too much of the money goes for

military armament.”

Both have signed a statement issued by the Tax Refusal Committee of

Peacemakers, a pacifist movement with headquarters in New York.

Miss Aldis said she paid 10 per cent of her taxes, the amount estimated for

use for non-military spending. Friesen said he would pay only direct taxes on

the “principal of the thing,” because other levies are “a part of the plan to

destroy our country.”

I found a few more things about Friesen as well.

I even saw one mention of his war tax resistance (too brief to quote, alas) that said that he had begun resisting in !

Her father, she said, “was ahead of his time” in advocating war tax

resistance and speaking out at Mennonite conferences against profiteering

from the war economy. “His conscience would not let him support the military.”

She said her father would have approved the

action by the General Conference Mennonite Church to honor employee Cornelia

Lehn’s request to not have her income taxes withheld from her paychecks.

The Friesens practiced war tax resistance by living simply, giving generously,

and usually not earning enough to owe taxes.

Although as a youth she was embarrassed by her father’s outspokenness to

audiences unreceptive to his message, Martha embraced her parents’

convictions about Christian discipleship and peacemaking and taught them to

her children. She files tax returns but usually has a zero taxable income due

to living simply and giving 50 percent of her income to charity. She has also

advocated for the Religious Freedom Peace Tax Fund legislation.

Bethlehem,

Pa.

(AP) — In an action primarily protesting

U.S. military

policies, the General Conference Mennonites has became [sic.]

the first mainstream Christian church to refuse to withhold federal taxes

from employees’ paychecks.

Delegates to the church’s international convention

voted 1,128 to 457 to authorize

church officials to violate federal law by refusing to withhold federal taxes.

A denomination spokesman said the church has tried for four years to secure

legislative, administrative, and judicial approval for its employees to refuse

to pay their taxes as a protest against the use of the money for military

hardware.

A group of Quakers — the American Friends Service Committee — also has

refused to withhold taxes, according to Margaret Bacon, a spokeswoman for the

Philadelphia-based group. The AFSC provides world-wide relief and works for social change.

But Dean M. Kelley, director for religious and civil liberty of the National

Council of Churches, said none of the council’s 31 member denominations had

previously refused to forward employees’ taxes to the federal government.

The 66,000-member General Conference Mennonite Church and the 93,000-member

Mennonite Church are holding their international meetings this week at Lehigh

University. The conferences are the first time the two churches have ever met

together.

Larry Cornies, news director for the General Conference Mennonites, said the

church has been considering the issue of tax withholdings for five years.

The catalyst came in , when Cornelia Lehn,

then director of children’s education for the church, asked the church to not

withhold taxes from her paycheck, Cornies said. She has since retired to

British Colombia.

, the church has decided a

U.S. Supreme Court

test case would be unsuccessful and a tax withholding bill could not get

through Congress, he said.

Cornies said a bill to let taxpayers earmark their taxes for a World Peace Tax

Fund, to be used only for peaceful purposes, “doesn’t look like it’s got much

of a chance.”

The National Council’s Kelley said the only denominations considering refusal

to let taxes be withheld are the “peace churches” — the Mennonites, the Church

of the Brethren, and the Quakers.

“Most of the mainline denominations are not pacifist,” he said.

The Mennonites decided not to approach the Supreme Court after the justices

ruled against an Amish employer from New Wilmington,

Pa., who had refused to

withhold Social Security taxes from Amish employees.

“Then it gratuitously added something to the effect that ‘if we let this take

place, people would be able to insist that they were entitled to withhold

paying of taxes on expenditures they object to, such as war and armaments,’ ”

Kelley said.

The (Lexington, North

Carolina) Dispatch carried this shorter and slightly

different version of the report:

Bethlehem,

Pa.

(AP) — To

protest funding of

U.S. military

activity, the General Conference Mennonites have voted to refuse to withhold

federal taxes from employees’ paychecks.

Dean M. Kelley, director for religious and civil liberty of the National

Council of Churches, said the

66,000-member General Conference Mennonites are the only denomination

belonging to the council ever to have taken such action.

A Quaker group, the American Friends Service Committee, also refuses to

withhold employees’ federal taxes.

A spokesman for the pacifist General Conference Mennonites said the church

has tried for four years to secure legislative, administrative, and judicial

approval for its employees to refuse to pay their taxes as a protest against

use of the money for military hardware.

Delegates to the church’s international convention

voted 1,128 to 457 to authorize

church officials to violate federal law by stopping the withholding of federal

taxes.

Larry Cornies, news director for the General Conference Mennonites, said the

church began considering the issue in , when

Cornelia Lehn, then director of children’s education for the church, asked

that taxes not be withheld from her paycheck. Ms. Lehn has since retired to

Canada.

Gene Harris, spokesman for the Internal Revenue Service in Philadelphia, said

of the Mennonite’s vote: “It’s a violation of the law. If they actually do

that, they could be prosecuted in court. It’s happened before and the

IRS has

won the case. But they would have to be audited first.”

According to the Toledo Blade, it was

, not , when

the Conference began mulling over war tax resistance. Here is an article from

their edition:

Bluffton,

O. — The General

Conference Mennonite Church, holding its 41st

triennial conference here, passed a resolution

calling for “serious study

of civil disobedience and war tax resistance during the next 18 months.” The

vote was 1,178½ yes to 453½ no.

The conference Monday rejected a proposed amendment to the resolution that

would have allowed the denomination as an employer to refuse to withhold the

so-called “war portion” of an employee’s income tax, if the employee

requested it, during the 18-month study period.

The denomination employs about 50 persons at its Newton,

Kan., headquarters, Lois

Barrett, spokesman, said.

The resolution was drafted because one employee at the headquarters, Cornelia

Lehn, had requested that the

war-tax portion of her taxes not be withheld from her salary, making it

possible for her to “follow her conscience in this matter.”

The “war portion” refers to the percentage used by the Government for military

purposes, according to the resolution.

War tax resistance in the Friends Journal in

There was plenty about war tax resistance in the Friends Journal in , but it seemed to involve tax resisting Mennonites as least as often as tax resisting Quakers.

The issue announced that the Center on Law and Pacifism was organizing a critical mass style tax resistance action:

The Center… has prepared and has available a “Conscience and Military Tax Resolution,” which may be signed by any conscientious objector to military taxes, witnessed (not necessarily notarized), returned to the Center.

When officially notified by the Center that there are 100,000 such resolutions on file, the signer may carry out his or her resolve to withhold the military portion of the federal income tax.

Alternatively, he or she may deposit the withheld taxes in an escrow account for the World Peace Tax Fund, pending passage by Congress of the WPTF Bill, deposit them in an alternative fund or donate them to some other peace purpose.

The issue was all about anti-war work, and it opened with an article on the history of Quaker war tax resistance by editor Ruth Kilpack.

Excerpts:

[W]e should not suppose that this is a new concern among Friends and members of other Peace Churches, who, by the very nature of our faith, have a conscience tender to such questionings.

For Friends, the searching extends back to the seventeenth century, when Robert Barclay, the English Quaker apologist, wrote in :

We have suffered much in qur country because we neither ourselves could bear arms, nor send others in our place, nor give our money for the buying of drums, standards, and other military attire.

This was the so-called “Trophy Money,” that could be distinguished as such.

But common or “mixed” taxes could not so readily be dealt with, since most Quakers believed it was their duty to pay taxes, and the part allocated to the military could not be separated out from the whole.

Today, like those earlier Quakers, we find ourselves in the same dilemma.

Law-abiding citizens, we continue to find ourselves troubled by the demand that we pay taxes for purposes we cannot in conscience condone.

We cannot pretend that we accept war as a legitimate function of the civil government which we support, and, just as some of our members have refused to serve in the armed services, many are beginning to question the contribution of our money for purposes we eschew for moral, humane, and religious reasons.

Quakers struggled with all these same questionings in the mid-eighteenth century and the period prior to the American Revolution.

One of the most articulate on the subject of war taxes was Samuel Allinson, a young Friend from Burlington, New Jersey, who in wrote “Reasons against war, and paying taxes for its support.”

The Samuel Allinson essay “Reasons against war, and paying taxes for its support” can be found in the book American Quaker War Tax Resistance.

Thus, in words written , he deals with the question of “a remnant who desire to be clear of a business so dark and destructive, that we should avoid the furtherance of it in any and every form.”

He describes it as a “stumbling block to others, [which] ought carefully to be avoided,” and sees such avoidance as advancing the Kingdom of the Messiah, that “his will be done on earth as it is done on heaven; a state possible, I presume, or he would not have taught us to pray for it.”

Further, says Samuel Allinson,

We have never entered into any contract expressed or implied for the paym[en]t of Taxes for War, nor the performance of any thing contrary to our Relig[ious] duties, and therefore cannot be looked upon as disaffected or Rebellious to any Gov[ernment] for these refusals, if this be our Testimony under all, which many believe it will hereafter be.

And finally, Samuel Allinson points out that even though earlier Friends paid their taxes (including that going to the military), that is no good reason for our continuing to do so.

It is not to be wondered at, or an argument drawn against a reformation in the refusal of Taxes for War at this Day, that our Brethren formerly paid them; knowledge is progressive, every reform[atio]n had its beginning, even the disciples were for some time ignorant of many religious Truths, tho’ they had the Company and precepts of our Savior…

Friends, we find ourselves in the very position of the Friends being addressed by Samuel Allinson two centuries ago.

For myself, I cannot think it is by sheer accident that I have stumbled upon his words now.

Neither is it by accident that a growing “remnant” of Friends are awakening to the ambivalence we feel in what we profess and what we practice regarding our involvement in the awesome “stumbling block” of nuclear warfare in our own age.

Friends in the past responded to the threats of the age in which they lived according to the light they had.

We of our generation have been given even greater light, and we must respond accordingly.

Given our heritage, if we don’t respond, who will?

In the meantime, I ask you to think on these things and, to paraphrase George Fox’s advice to William Penn, “Pay thy tax as long as thou canst.”

In the issue, Keith Tingle told readers that they should know “how easy it is to do” war tax resistance… at least in his experience:

My own experience in military tax resistance has been rewarding thus far.

By claiming a tax credit for conscientious objection to war on my income tax form, I was refunded $260 from my taxes.

Now that the IRS has discovered its mistake, I am resisting through federal tax court the recollection of this money.

My appearance in tax court has been reported favorably in three local newspapers, providing an opportunity to publicize the Quaker peace testimony, the history of war tax resistance, the economic impact of military spending, the pacifist position on the military draft, the concept of the World Peace Tax Fund, and the legal assistance offered by the Center on Law and Pacifism.

This has been accomplished with a total expense of about $30 and about thirty hours of time.

I have enjoyed the dedicated support of the Committee on War Tax Concerns of Friends Peace Committee and the legal guidance of lawyer Bill Durland at the Center on Law and Pacifism…

The issue noted that conscientious objection to military taxation was on the agenda at the Kent General Meeting in Canterbury, England — though from the sound of it, this was mostly in a theoretical way: presenting the argument that such a thing was a logical and practical counterpart of conscientious objection to military service.

That issue also reported on the case of Cornelia Lehn, an employee of the General Conference Mennonite Church who was trying to convince her employer to stop withholding federal income tax from her salary:

There was a “neither yes nor no” vote on this request by the 500 delegates present.

Those who favored a strong tax resistance program did not Nor did those who wanted members to unquestioningly pay taxes as a Christian duty.

There was a feeling, however, that neither side really lost.

Thirty percent of the delegates were ready for the conference to take action in “some sort of civil disobedience and tax resistance” and it was hoped the number will grow.

I’m struck by this last phrase — “it was hoped the number will grow” — which makes a pretty clear editorial statement of sympathy for those who favored corporate resistance by the Conference and antipathy for “those who wanted members to unquestioningly pay taxes as a Christian duty.”

At this time, few if any Quaker Meetings or organizations were willing to go out on that limb, in spite of strong urgings from Quaker war tax resisters that they do so.

But I don’t remember the Journal betraying an editorial bias when it reported on this debate in Quaker institutions.

One case in point is a report on the New England Yearly Meeting in which the lukewarm statement is made that “We approved a minute asking New England Friends to give prayerful consideration to non-payment of war taxes.”

The New York Yearly Meeting went so far as to “discuss” a “minute on Refusal of Taxes for Military Purposes” and to note that it “was to be commended for consideration by all monthly meetings and individuals.”

The issue had a followup in which the General Conference of the Mennonite Church was proposing launching a lawsuit in which it would seek a judicial ruling to legalize conscientious objection to military taxation, while at the same time it would increase its efforts to pass the “World Peace Tax Fund” legislation.

Maurice McCracken had a piece of autobiography in the issue.

Naturally, it touched on his tax resistance:

I had decided that I would never register again for the draft nor would I consent to being conscripted by the government in any other capacity.

In contradiction to this position, each year on April 15 I was letting the government conscript my money.

Thus I was voluntarily helping the government do what I vigorously declared was wrong.…

Realizing this inconsistency, I decided that in good conscience I could no longer make full payment of my federal taxes.

At the same time, I did not want to stop supporting civilian services supported by the government.

So, in my tax returns I continued to pay the small percentage allocated for civilian use.

The amount that I formerly had given for war purposes I hoped now to give to such causes as the American Friends Service Committee and to support other works of mercy and reconciliation which help remove the roots of violence and war.

As time went on I realized, however, that this was not accomplishing what had been my hope; for year after year the IRS ordered my bank to release money from my account to pay the money I had held back.

I then closed my bank account, and at this point it came to me with complete clarity that by so much as filing tax returns I was giving the IRS assistance in the violation of my own conscience, because the very information I was giving on my tax forms was being used in finally making the collection.

There is something else that those who withhold a portion of their tax on conscientious grounds should realize.

The IRS does not practice line budgeting.

All that it collects goes where the government wants it to go, which in ever-increasing proportion goes to finance wars, past, present and future.

I have not filed any tax returns, nor have I paid any federal income tax.

On , on charges growing out of my refusal to pay this tax, I was given a six-month sentence, which I spent at Allenwood, Pennsylvania, which is run by the Lewisburg penitentiary.

Some two years my release from Allenwood, in , the Presbytery of Cincinnati, on charges quite unrelated to the real issues, suspended me as a minister.

In , this action was upheld by the General Assembly, the highest court of the denomination.

In the presbytery declared my ordination to the ministry no longer valid, making a highly questionable presumption that they could cancel out whatever spiritual grace the Holy Spirit had bestowed on me when I was ordained at a meeting of Chicago Presbytery back in .

For nearly eighteen years our congregation has been a member of the National Council of Community Churches.

I have been accepted as a minister in full standing, and whatever validity my ordination had back in , is, for them, still valid.

A note in the issue recognized 86-year-old Pearl Ewald’s persistent activism: “Pearl Ewald continued her activities for peace, civil rights and war tax resistance, despite a recurring heart condition.

She has been arrested and jailed more than once for stubbornly refusing to discontinue her witness.

On one occasion, although desperately in need of medical attention, she refused to be admitted to a hospital, because it was a segregated institution.”

That same issue mentioned the case of Mennonite war tax resister Bruce Chrisman, “who was convicted of failure to file an income tax return in , was sentenced to one year in Mennonite Voluntary Service,” to which I can only think: “Please don’t throw me in the briar patch, Your Honor!”

“I’m amazed,” said Chrisman.

“I feel very good about the sentence.

The alternative service is probably the first sentence of its kind for a tax case.

I think it reflects the testimony in the trial and its influence on the judge.”

Chrisman could have been sentenced to one year in prison and a $10,000 fine.

A letter from Mildred Thierman in the same issue challenged Friends:

Could we now unite this year in sending a flood of personal declarations to President Carter and our government, saying that we can no longer, in conscience, allow part of our taxes to be used for the purchase of annihilating weapons?

Can we back this up by joining together in significant numbers to withhold whatever portion of our income tax fits our circumstances, in order to make our protest noticed?

A review of Conscience in Crisis: Mennonites and Other Peace Churches in America, , Interpretation and Documents in the issue, summarized its version of the history of Quaker war tax resistance this way:

Testimony against participation in the military and refusal to pay Trophy Money — the English tax to raise money for military regalia (arms were, by law, furnished by the individual soldiers) — were traditional Friends’ observances by the beginning of the period covered by Conscience in Crisis.…

…Friends and other Peace Church members were, by and large, loyal subjects.

They paid taxes “for the King’s use” — including the royal decision to make war.

Friends began to question payment of taxes more broadly.

The essential issue, according to the authors, was that “the individual is responsible for the actions of his government in a free society.”

Israel Pemberton, John Pemberton, John Churchman, John Woolman, and nineteen other Friends petitioned the Assembly on the issue of taxes in :

…Yet as the raising Sums of Money, and putting them into the Hands of Committees, who may apply them to Purposes inconsistent with the peaceable Testimony we profess, and have borne to the World, appears to us in its Consequences to be destructive of our religious Liberties, we apprehend many among us will be under the Necessity of suffering rather than consenting thereto by the Payment of a Tax for such Purposes…

By the time of the Philadelphia Yearly Meeting sessions, Friends decided not to discuss the issue of “mixed” taxes because of a significant lack of consensus.

Yet, Friends were increasingly beginning to question less direct forms of support for war not traditionally inconsistent with the peace testimony.

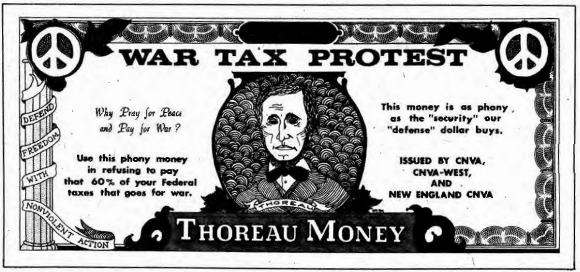

an illustration from the issue of Friends Journal

In the issue, Alan Eccleston wrote of his calling as a peacemaker, and how that manifested for him.

Excerpts:

For me personally, the witness to peace has led to war tax resistance.

Over the past six years of this witness I have been — and still am — strengthened by others who are not, themselves, war tax resisters.

The witness of war tax resistance is one that raises fear.

We have been conditioned to fear the Internal Revenue Service as something nearly equivalent to a ruthless secret police, in its imagined power to terrorize.

Most of us, unwilling to admit, even to ourselves, that fear alone would block us from a spiritual witness, find other reasons for willingly paying to produce weapons that can annihilate all humankind.

Based on my own experience, I would say fear imagined is greater in most people than fear actually experienced, and that this is by a factor of ten, at least — maybe 100. Fortunately, borrowing from each other’s experience and knowing others will be there to help us, we can find the courage to move ahead.

Then comes the surprise.

With dread and foreboding we make our stand.

Then, gradually, we become aware that a great weight has been lifted from us.

That nagging, cumbersome burden of blocking from consciousness our own complicity with this evil has fallen away.

We are lighter, more open, more truthful.

We are free, at last, to speak truth to power.

When this affirmation is truly clear in our lives, it will be seen and felt by the president and by Congress.

As in , when C.O. status was incorporated in the Selective Service Act, the tax laws will then be amended to create C.O. status for taxpayers and a “World Peace Tax Fund.”

That legislation, approved by the world’s leading arms supplier, will move the world one step closer to peace.

That portion of our population (approximately four percent during the Vietnam War) which is pacifist would then contribute to peace, not war, and these contributions would total in excess of $2.3 billion every single year — year after year.

For the first time in history, peace programs would have a significant budget.

The funds could be used to support: a National Academy of Peace and Conflict Resolution; research to develop and evaluate non-military, nonviolent solutions to international conflict; disarmament; retaining workers displaced by conversion from military production; international exchanges for peaceful purposes; improvement of international health, education and welfare; and education of the public about the above activities.

The Friends General Conference in drafted “A Statement of Conscience by Quakers Concerned” and collected signatures.

The statement said, in part:

We advocate conscientious refusal to register for the draft and wish young men of draft age throughout the United States to know that if, after thoughtfully considering the reasons and consequences, they refuse to register, we will give them practical and moral support in every way we can, even though our willingness to do so may result in our prosecution, fines and possible imprisonment for disobeying a man-made law that leads us in the direction of war.

Mary Bye wrote in response that although she signed the statement, it felt to her to be something “like a hollow gesture.”

[M]aybe we [adults] should make sure about the beam in our adult eyes before we concentrate on the motes in those bright young eyes of the nineteen- and twenty-year-olds.

“[W]hat would be our reaction to young Quakers pointing out that since it takes money as well as men to fight a war, they encourage Friends beyond draft age to refuse war taxes?

Finally, the issue presented the case of Ruth Larson Hatcher.

Excerpt:

Not wishing to contribute tax money for war-making purposes, she managed for years to have an income just sufficient for survival but not large enough to require payment of taxes.

Then in a friend persuaded her to accept the management and bookkeeping of a children’s art center.

Conscientious and religious beliefs caused her to oppose acceptance of insurance benefits under Social Security, as well as the payment of taxes for war.

Her claims for exemption under various sections of the Internal Revenue code of as well as under the First and Fifth Amendments were routinely rejected, until a Supreme Court judge approved her use of Form No. 4361. It seems that this form (and another previously ignored by the authorities) had been used by an Amish sect to avoid the taxes (and payments) of the social security system.

Although the Court of Appeals handed down the opinion that exemptions were enacted to accommodate individuals commanded by their conscience or their religion to oppose acceptance of insurance benefits, it refused to accept that this was the exact status of petitioner Ruth Hatcher.

It’s a little unclear what took place here, but it sounds like this is saying that the courts left an opening for people who were not members of sects that qualified for an exemption from the social security system but who held similar beliefs to gain the same exemption.

Interesting if true.

I was able to find the appeals court decision that ruled against Hatcher, and the earlier Tax Court decision to the same effect, and the District Court decision that affirmed the Tax Court decision.

I was not able to find any record of Supreme Court action on the case, but I did find some other cases that cited the Appeals Court decision as precedent, which seems to suggest that the Supreme Court didn’t overturn it (as the above excerpt implies).

This is the twenty-third in a series of posts about war tax resistance as it

was reported in back issues of The Mennonite. Today

brings us up to 1976.

The question of whether the Mennonite General Conference should stop

withholding taxes from the paychecks of conscientiously objecting employees

continued to bedevil the Conference and its various committees and commissions

in . After the American Friends Service

Committee won a District Court ruling about withholding from its objecting

employees, the General Conference was pressed to adopt such a policy. But that

ruling was swiftly overturned by the Supreme Court, and so the Conference

seemed to lose its nerve.

In the executive committee of

the General Conference’s Commission

on Home Ministries decided to put on its agenda for their full-commission

meeting in a “recommendation

that the General Conference not withhold the military portion of income taxes

from the paychecks of those employees who do not wish to pay war taxes

voluntarily. This would mean that such employees, rather than the conference,

could be responsible for the decision of whether to pay war taxes to the

government.”

That proposed recommendation

was

approved at the meeting, “but referred for further study by the Division of

Administration and the General Board.”

A article covered the slow

progress of the proposal through the Conference bureaucracy:

Should General Conference employees have the right not to have war taxes

withheld by the conference from their paychecks?

For the time being, the answer is still no, pending further study and the

securing of more legal counsel.

The peace and social concerns reference council of the Commission on Home

Ministries raised the issue of war-tax withholding by the conference. The

reference council recommended that the General Conference central offices

allow persons the right not to have taxes withheld (in line with research done

last summer by a law student), that other Mennonite institutions be invited to

participate in similar action, and that congregations and individuals be

invited to consider war tax resistance.

“Freedom of religion includes freedom from the church forced by the state to

act as a tax collection agent, particularly when taxes are used for purposes

which are in conflict with the kingdom,” said the reference council statement.

“The Anabaptist concept of separation of church and state would also suggest

that the church not perform this kind of state function.”

The Commission on Home Ministries, in its annual session in

, approved the recommendation

with some reservations. The Division of Administration had even more

reservations about the recommendation.

DA

members questioned the legal findings of last summer and asked for further

consultation with a tax attorney with more experience in this area.

Specifically they wanted to know the cost of possible litigation, whether a

revenue ruling should be requested from the Internal Revenue Service, possible

civil and criminal sanctions against the General Conference, the effect on the

conference’s tax-exempt status, and the chances of success in the event of

litigation.

“Conscience is a personal thing, and we’re not together on what we want to do

with this,” said

DA

chairman Howard Baumgartner of Berne, Indiana. “CHM

is asking that the business manager be put on the spot. What if his conscience

doesn’t permit him to break this law? My conscience tells me to pay my tax.”

In the closing minutes of its sessions, the General Board, acting on the

recommendation of the

DA,

asked the

DA to

do further study on the legal aspects of failure to withhold taxes and to

bring back some information at the General Board’s

meeting.

“I’m not willing to face the legal consequences until we’re fairly united on

this,” said conference president Elmer Neufeld of Bluffton, Ohio.

At present, the General Conference central offices withhold all state and

federal income taxes from the paychecks of nonordained employees. Such persons

cannot choose whether to pay or not to pay any war taxes they owe because the

government already has the money, or most of it.

Editor Larry Kehler, in the

issue called this a “red flag”:

Although some leaders from other denominations may be beginning to notice and

listen to the Anabaptist-Mennonite point of view as an attractive option, the

Mennonites may be losing their testimony as a peace church. One committee at

the Council of Commissions stated, for example, in its opinion there was no

“corporate conscience” within the General Conference against the payment of

war taxes.

And Peter J. Ediger summed things up in his prose-poem fashion:

It came to pass that an employee of the General Conference Mennonite Church

requested that taxes for the military not be withheld from her paycheck.

And officers of the conference said, “What shall we do?”

And the Commission on Home Ministries was asked to study the matter

and make a recommendation.

And the commission hired a student of law to research the options;

and the commission joined with other Mennonite groups in calling for a study conference on war tax questions.

And from the research and the conference came a clear recommendation

that the General Conference allow persons the right

not to have war taxes withheld.

And when this recommendation was brought to the Commission on Home Ministries

there was a consensus of support and agreement to recommend its adoption to the General Board.

And the recommendation was brought to the Division of Administration.

And lo, their response was as follows:

“Motion that the request of CHM for right not to have taxes withheld

from salaries of employees who submit such request be refused…”

and listing six recommendations asking for more legal counsel.

And so the conflicting recommendations were brought to the General Board.

And the General Board was occupied with many weighty matters.

The agenda was long and the time for discernment was short

and war taxes was the last item on the agenda

and five minutes was left for this item

and no action was taken.

And the conference goes on with business as usual

continuing collection of money for making of war

seeking its guidance more from the law of the land

and less from the law of the Lord.

Do we really want the laws and lawyers of our society

to define the perimeters of our discipleship?

The

General Board executive committee met in

and “allotted two hours at the

full board session in … for discussion of

whether the conference should honor an employee’s request that federal income

taxes not be deducted from her paycheck. Theological input on the payment of

war taxes was also requested.”

The way this was put in

an

announcement just before the board meeting was: “The Division of

Administration… wants to continue its policy of not honoring employees’

requests that the portion of their federal taxes which goes for war not be

taking out of their paychecks.”

The board met and… kicked the can further down the road.

After almost three hours of discussion by the General Board of the General

Conference, a decision is still pending on whether the conference should honor

an employee’s request that the portion of her income taxes that goes for war

not be taken out of her pay.

The board had set aside two hours at the end of its midyear meeting

in Washington, Illinois, to

consider the issue of war tax withholding. Marlin Miller of Goshen Biblical

Seminary had been invited to give biblical input, and Division of

Administration members Howard Baumgartner and Elvin Souder, both attorneys, to

give legal recommendations.

The issue was whether the General Conference business office should violate

U.S. law by

refusing to take from an employee’s paycheck the portion (almost half) of her

federal income taxes which would go for military purposes. Such action would

allow the employee to refuse to pay such taxes and would make her personally

liable for nonpayment of tax.

The law at present requires employers to withhold income and Social Security

taxes from employees’ salaries — except in the case of ordained employees, who

may legally consider themselves self-employed and are thus personally

responsible for making, or not making, quarterly tax payments. A number of

ordained employees at the General Conference offices are already refusing war

taxes in this manner.

Nonordained employees have no way of refusing war taxes except by falsifying

their tax returns or the number of exemptions they claim.

The General Board did not vote on a normal motion on the war tax matter, but

straw poll showed a slight majority in favor of allowing all employees the

right to refuse war taxes, in spite of the possible consequences to the

conference or its officers for breaking the law. But the board was not willing

to act officially until it reached greater consensus.

“We are facing an issue of our own integrity as a people and as a church,”

said board member Peter Ediger of Arvada, Colorado. “It is a situation not

unlike that of our grandfathers in World War Ⅰ. Because some of them had the

courage to say no, laws were enacted to permit conscientious objection to

military service. And it is an evangelism issue. Our world desperately needs

the good news that there is an alternative to violence and war. We can do this

with the kind of integrity that perhaps no other corporate group in our world

can.”

Some like Irene Dunn of Normal, Illinois, were not ready to decide personally

about payment of war taxes, but wanted to allow General Conference employees

freedom of conscience concerning war taxes.

Others wanted to postpone the issue. “It’s my feeling we should take a

recommendation to the triennial conference,” said board president Elmer

Neufeld of Bluffton, Ohio.

In the end the decision was postponed — probably until the

board session.

Marlin Miller, himself a tax refuser for seven years, told the board that the

legality of refusing war taxes was not the highest morality. “If we are clear

on the moral principles, we will find a way to deal with the legal matters,”

he said.

His biblical study focused on Mark 12:13–17

(in which Jesus tells those who are trying to trick him, “Render to Caesar the

things that are Caesar’s, and to God the things that are God’s”) and

Romans 13.

There is no unambiguous word in the New Testament on whether the Christian

should pay all taxes he said. But likewise, there is no clear statement in the

New Testament on not going to military service. “Taxes are due to the

governing authorities, but there is still a need for moral discrimination,”

Mr. Miller said.

Howard Baumgartner told the board that, if it decided to allow an employee not

to pay her war taxes, it might want to test the constitutionality of the

withholding law in the

U.S. courts. An

earlier similar case from the American Friends Service Committee had been

thrown out on technical grounds without testing the tax law itself.

Elmer Neufeld, president of the General Conference, sent

a

letter to all General Conference pastors on the subject:

Should the conference withhold taxes for war?

Some time ago I reviewed a number of the court-martial records of the

Mennonite men in the United States in World War Ⅰ who were tried for refusing

to participate in military service. These were our fathers and fathers’

fathers who had committed their lives to the way of the cross and who held

with the saints of all ages that there is a law of God which stands above the

human laws of the nation.

There was no legal provision for conscientious objection to military service

and war, so they simply took their stand in humble obedience to Christ and

accepted the consequences. Gerhard M. Baergen… guilty. Abraham Goertz… guilty.

Russell A. Lantz… guilty. John T. Neufeld… guilty. Carl A. Schmidt… guilty.

Walter Sprunger… guilty. And so on.

It is through the sacrifice of these sturdy men of conscience that the United

States came to provide a legal alternative to military service and war for

those with scruples against participation. It is through their sacrifice that

many of us were able to use this legal alternative in World War Ⅱ and again in

the Korean and Vietnam wars.

Now we face a new situation. For the first time

, except for a brief lull

following World War Ⅱ, our churches in the United States no longer face the

conscription of young men for military service. For this many have worked and

for this we are grateful. However, it is clear that conscription for military

service was not terminated because the United States has come to rely less on

military power. In fact, the United States has come to be militarily the most

powerful nation in the world and is exporting more armaments than any other

nation in the world. All of this is possible with well-paid volunteer armed

forces and a heavily financed industrial military complex. The military

complex is able to get along without our young men as draftees, but it insists

on having our finances to support its multibillion dollar operation.

More and more there are those among us whose consciences no longer allow them

freely to support this military machine. Though they realize that Christians

have usually paid their taxes through the centuries, even to strongly

militaristic governments, they believe that the vast sums required today are

too much, that it is once more time to withstand the military powers that

threaten to destroy all of humankind, that Caesar is demanding not only what

belongs to Caesar, but also what belongs to God.

I was deeply impressed as we went about the circle of General Board members

and staff [at the meeting] that

almost all had struggled with this issue of conscience and that most had in

some way protested the vast sums being required for military purposes. Though

it is appropriate for us as a people to counsel together whether it is right

in the sight of God to keep paying these war taxes, this is also an issue on

which individuals and families will make their own decisions — and we will not

all make the same decisions.

However, as a conference we face a more complex question. Not only must our

individual members and families decide what to do about war taxes, but the

conference as an employer must collect taxes, including taxes for war, for the

government. We are collecting taxes not only from those who are willing to pay

the whole amount to the government, but also from those who have Christian

convictions against supporting the military in this way. Cornelia Lehn is one

such person. (See below.) A number of ordained ministers working for the

conference are self-employed for tax purposes and thus can make their protest

in whatever way seems appropriate. But for others this is not possible.

So the issue before the General Board in

was whether the General

Conference as an employer should continue to withhold federal income tax

money, even from those employees who have conscientious objection to this, and

send that money to the government.

The Commission on Home Ministries recommends that the conference should no

longer withhold taxes from those employees who have convictions against such

payments. On the other hand, the Division of Administration has serious

concerns about the consequences for the conference in violating the laws of

the land.

The General Board in its meeting

had a long and intensive discussion, with representatives of the Commission on

Home Ministries and the Division of Administration and with counsel on

biblical principles from Marlin Miller, president of Goshen Biblical Seminary,

as well as Erland Waltner, president of Mennonite Biblical Seminary.

A larger and larger majority of General Board members have serious

reservations about serving as a tax collector from those employees who have

Christian convictions against the payment of such taxes. At the same time we

were sensitive that we were being called to make a decision not only for

ourselves but for the whole conference and that we have not yet had adequate

dialog with our congregations about this issue.

What is the will of God for the General Conference in this issue? What is your

counsel for the General Board? We did not act because it was clear that we had

not come to consensus, but the issue will continue to face us and we will

continue to struggle for the right decision.

One possible course of action is for the General Board in its

meeting to formulate a recommendation

to be sent to the congregations for study and for corporate consideration at

the triennial sessions of the General Conference in

.

I want to touch on a related question: Is this one of those conference issues

which is of concern only to the United States and not to Canada? Will our

brothers and sisters in Canada feel like washing their hands of this issue? Or

is this one of those cases when one part of the body is in trouble and the

whole body struggles together? May it in fact be possible that the Canadians

can help those of us in the American churches see ourselves a bit more

objectively?

Can we possibly come to the place, in the words of the Acts of the Apostles,

that it seemed good to the Holy Spirit and to us together that we should

decide this issue in a certain way? Surely if we search together in openness

and honesty and in a spirit of prayer, God will not forsake his people.

A letter from Conference employee Cornelia Lehn was also enclosed in Neufeld’s

letter:

I work for the General Conference Mennonite Church at 722 Main

St., Newton, Kansas. Each month

a certain percentage of my salary is deducted for income tax purposes before I

receive it. The business office is legally requested to do so for all

employees except for those who have been ordained to the ministry.

We are told that approximately 50 percent of the income tax deducted goes to

buy armaments. When I first started working here, this did not bother me too

much, even though I believed strongly in nonresistance. After all, did not

Jesus himself pay taxes

(Mt. 17:24-27)?

Why then should I refuse to do so?

The whole question of personal responsibility began to tear at my heart and

mind, however. We held the people condemned at Nuremberg responsible for their

deeds, although they had just “obeyed the government.” We held Captain Calley

responsible for his deeds at My Lai, though he, too, thought he had obeyed the

government. Why should I not be held responsible to obeying the government

when it was asking me to do an evil thing? Though Jesus paid taxes, the spirit

of his teachings is to do good, not evil, to our fellow human beings. I became

convinced that allowing my money to be used for armaments could not be God’s

will and that if it was used in that way I must bear at least part of the

responsibility.

The big question then was how to get out of being involved in this crime. I

could not refuse to pay a portion of my tax, since the whole tax was already

withheld. I asked our conference office not to withhold from my paycheck that

portion of the income tax that goes for war, but they could not grant that

request. I considered the options, such as reducing my paycheck to the point

where I would not need to pay any taxes or reducing it to the point where I

would need to pay only half the taxes I do now.

Finally I decided to give half of my income to relief and other church work

and thus force the Internal Revenue Service to return that portion of my tax

which they had already slated for military purposes.

I realize, of course, that this is not the perfect answer. Of the 50 percent

that IRS

still has of my income tax, half will again be used to meet the military

budget. It is, however, the best answer I know at this time. Finally I could

no longer acquiesce and be a part of something so diabolical as war. I had to

take a stand against it.

I wish that my church, which believes in the way of peace, would as a body no

longer gather money to help the government make war. I wish all the members of

our church would stand up in horror and refuse to allow it to happen. Then the

conference officers would be in a position to say to the government, “We will

not give you our sons and daughters, and we will not give you our money to

kill others. Allow us to serve our country in the way of peace.”

Don

Kaufman wrote in to the magazine on to praise Neufeld’s letter and to say that the dialogue about the

issue had been beneficial to the community, but also to criticize the church

for its timidity in the face of the law:

[A]s Christians we seem to be far more accountable to the government than we

are to the church. I have sometimes wondered why it is that we are more

willing to allow the secular authorities to shape us and to “keep us in line”

than we are to receive guidance from our brothers and sisters in Christ. The

major exceptions to this in the General Conference Mennonite Church appear to

be the intentional communities of faith like Fairview Mennonite House and the

New Creation Fellowship, where economic discernment is more obviously a part

of the Christin commitment.

This is the twenty-fourth in a series of posts about war tax resistance as it was reported in back issues of The Mennonite.

Today brings us up to 1977.

In our last episode we watched various executive committees and commissions and boards in the Mennonite General Conference pass the buck back and forth as the Conference impatiently waited to learn whether they would or would not continue to withhold taxes from the paychecks of their conscientiously objecting employees.

The board [General Board, I think ―♇] was sharply divided on whether to grant the employee’s request and thus risk violating tax regulations.

Board members also could not agree on whether the issue should be decided by the board or wait for action by the entire conference at the triennial sessions in .

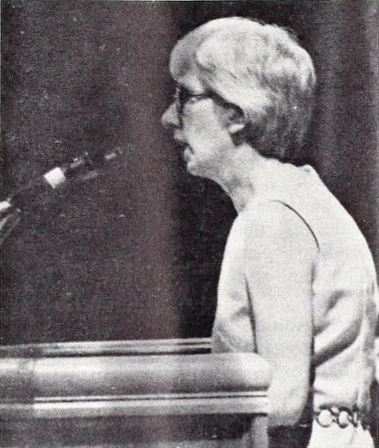

Cornelia Lehn, the employee bringing the request, met with the board for the first time and told them, “It was also a very difficult decision for me over a long period of years.

Finally I gave up seeing through the difficulties; for me, I simply had to obey God and leave the consequences up to him.”

The resolution reviews the history of General Conference discussion of the war tax issues from a sentence in the statement “The Way of Peace” [see ♇ 22 July 2018] to General Board deliberations on an employee’s request that war taxes not be taken out of her paycheck.

The resolution asks that congregations and regional conferences “commit ourselves to a serious study of civil disobedience during , that the Commission on Home Ministries help facilitate such a study… and that a midtriennium miniconference be convened for congregations to report on their study and to recommend actions related to civil disobedience and war tax resistance, including the question of Mennonite institutions serving as war tax collectors for the state by withholding these taxes from employees.”

In three separate votes, the delegates first turned down, 1,190 to 336, an amendment which would have adopted an interim policy for eighteen months “instructing the conference to honor the requests of those employees who ask not to have withheld from their salaries that portion of federal income tax they believe helps the government prepare for war.”

The next evening, delegates adopted, 1,178½ to 453½, the main motion.

Its effect is to delay any action on the request of conference employee Cornelia Lehn that federal income taxes that would go for war not be taken out of her paycheck.

It also calls for a midtriennium official delegate conference to recommend actions related to civil disobedience and war tax resistance, including the question of Mennonite institutions serving as war tax collectors for the state by withholding these taxes from employees.

A second resolution that evening gave General Conference endorsement to the World Peace Tax Fund Act in the U.S. Congress and encouraged similar legislation in Canada, if appropriate.

The act would allow conscientious objectors to war to designate the military portion of their taxes into the peace fund.

The resolution also “continue(s) to support individuals who feel compelled by Chrisian conscience to adopt other methods of witness against payment of war taxes such as voluntary reduction of income or nonpayment of war taxes.”

Cornelia Lehn tells of her struggle with war taxes.

Discussion of the war tax withholding issue began with a testimony by Ms. Lehn, who writes and edits children’s curriculum for the Commission on Education, who first came to the conference business manager two years ago with a request that she be allowed to resist payment of war taxes.

Presently the business office is following federal regulations that estimated taxes be withheld from each employee’s paycheck.

The regulations do not apply, however, to ordained persons employed by the conference, some of whom are resisting voluntary payment of war taxes without implicating the conference as a whole.

“It is a long journey from the little Mennonite village in the Ukraine, where I was born, to Newton, Kansas,” she began.

“It was a long pilgrimage until I came to the conviction to resist war taxes and was able to act on it.”

Ms. Lehn told of her struggle with the command to pay taxes, on the one hand, and the knowledge that her tax dollars were being used for killing.

“I can’t extricate myself from the system, but I finally have to take a stand against a demonic armaments race,” she said.

“I do not know where this will lead, but… for my part, I must obey the Spirit of God as I understand it to be revealed in the Bible and leave the consequences to God.”

Delegates kept coming to the microphones to speak to the resolution until debate was cut off.

“As a pastor, I could not advocate civil disobedience,” said Dan Dalke of Bluffton.

“The taxes Jesus said to pay were to the Roman Government,” said a former IRS employee.

“I have proper respect for laws, but I also recognize that if Felix Manz, Conrad Grebel, and Menno Simons had had greater fear for the law than for God, we would probably not be here today,” commented Lauren Friesen, pastor from Seattle.

“This morning we passed a resolution supporting missionaries for acting faithfully in oppressive situations abroad,” said Steve Linscheid of Goessel, Kansas.

“We should not expect more from our missionaries than we are willing to do ourselves.”

“Many people are concerned about our tax dollar, but we should work much harder trying to come to a common mind with other Mennonite groups,” said Henry A. Fast of North Newton, Kansas.

“We should keep on pushing the World Peace Tax Fund Act.”

Donovan Smucker of Kitchener, Ontario, cited many Christians throughout the ages who have obeyed God rather than man and said, “The problem is, When do you stop the democratic process that is pushing you into something that is evil?”

“It’s best to work through the system and use the privileges we already have,” said Art Waltner.

“Our right to conscientious objection to military service did not come through petition in Washington,” Ted Koontz of Boston reminded the delegates.

“It came because our forefathers spent years in prison in World War Ⅰ.”

The World Peace Tax Fund resolution, which supports legislation to allow people to resist war taxes without breaking the law, passed later in the evening by voice vote without audible opposition.

Most of the U.S. district conferences had already adopted resolutions supporting the proposed legislation.

In a way, this was more of a triumph than a defeat for the promoters of war tax resistance.

If the triennium had voted the other way, one employee, and maybe a handful more, would have benefited somewhat from the new policy.

But by voting this way, the triennium prompted discussions in every Mennonite congregation about whether or not war tax resistance was the right thing to do.

There was… lengthy deliberation about the midtriennium civil disobedience conference called for by a Bluffton resolution.

One of the main concerns was whether Canadian churches would see the issue of civil disobedience and war tax as relevant to them.

Would they send delegates?

Another worry was whether delegates would carry a large number of proxy votes.

The constitution of the General Conference allows for a quorum with 50 percent representation, and since one delegate can carry up to twenty-five votes by proxy, it would be possible for forty persons to make a decision affecting the whole conference.

About 1,000 votes are needed for a quorum.

The hope was expressed that the study process being initiated would create good interest and also broadly based, informed representation.

Beginning in an attitudinal survey on civil disobedience is scheduled.

A study guide is to be ready by for use in Sunday school sessions and other study groups.

A definite place and time for the midtriennium conference will be decided later, though is a strong possibility.

Already the executive committee is faced with a question of civil disobedience.

Only a few days prior to the meeting the Newton office received notice from the Internal Revenue Service of the United States to pay personal income taxes owed by Heinz Janzen (general secretary) and his wife, Dorothea Janzen.

Since Heinz is ordained, it is legal for him to categorize himself as self-employed, and hence, his salary check from the General Conference has no income tax deductions.

he has been refusing to pay the military portion of his income tax, placing it in a bank account, and informing the IRS of his reasons.

Until this levy arrived the IRS has simply confiscated the bank accounts of such persons and withdrawn the unpaid portion from the accounts.

Now the IRS has demanded that the General Conference employer be responsible for paying Heinz’s unpaid tax out of Heinz’s salary check.

The executive committee decided to delay a decision on the IRS levy until the meeting of the General Board.

They were concerned that any action in the current case is not to be seen as a predetermination of the issues which by Bluffton conference resolution are to come before the midtriennial conference.

They did, however, see the levy as different from the request of General Conference employee Cornelia Lehn to have the military portion of her tax not withheld from her salary check by the General Conference.

The Janzen case is seen as civil disobedience by individuals and not by the incorporated body, the General Conference.

This is the twenty-fifth in a series of posts about war tax resistance as it was reported in back issues of The Mennonite.

Today I’m going to try to cover 1978.

I say “try” because there was a frenzy of war tax resistance activity reported in The Mennonite .

Maybe I can try to sort it thematically…

A New Call to Peacemaking

“A New Call to Peacemaking” was an initiative coordinated by Mennonite, Quaker, and Brethren activists that began in and would eventually culminate in a statement urging people, Christians in particular, to refuse to pay taxes for war.

The Mennonite General Conference’s Peace Section,

U.S. division, met

and its executive secretary, John K. Stoner, reported that the Call

“has

gained widespread support.”

Invited to the meeting are 300 persons — Brethren, Friends, and Mennonites.

Named the New Call to Peacemaking, this coalition of historic peace churches

believes that “the time has come for all Christians and people of all faiths

to renounce war on religious and moral grounds.”

During the last year twenty-six regional New Call to Peacemaking meetings, involving more than 1500 persons, took a new look at the teachings of their churches.

They gave special attention to war and violence which they continue to see as denials of the life and teachings of Jesus Christ.

Not surprisingly the groups agreed to urge upon all governments “effective

steps toward international disarmament.” However, none of the regional

meetings expressed the hope that politicians, soldiers, and diplomats would

put an end to war. Rather, the thought was that people at the grass-roots

level must demand a change in the system. Further, the idea was often

expressed that tax resistance and civil disobedience are necessary tactics in

convincing governments that a new order can bring security in place of the

present insecurity.

A New Call to Peacemaking conference which convened at Old Chatham, New York, last April, asked itself rhetorically, “Are we going to pray for peace, and pay for war?” A similar conference in Wichita, Kansas, gave its encouragement to “individuals who feel called to resist the payment of the military portion of their federal taxes.”

When the national conference convenes in Green Lake it will be receiving

requests from the regional meetings for a strong position on tax resistance

proposals. It will also be asked to give guidance to individuals and church

organizations on approaches to tax resistance. Theological, economic, and

social justice issues are also on the agenda.

“Citizens should organize themselves and act without waiting for government, especially the major powers, to take positive action,” says Robert Johansen in a paper being studied by the Green Lake delegates.

In another document prepared for the Green Lake meeting, Lois Barrett, a

Mennonite journalist from Wichita, Kansas, notes that the peace churches have

long “recognized refusal to pay war taxes as one of many valid witnesses

against war.”

In the Church of the Brethren recommended “that all who feel the concern be encouraged to express their protest and testimonies through letters accompanying their tax returns, whether accompanied by payment or not.” In the General Conference Mennonite Church said, “We stand by those who feel called to resist the payment of that portion of taxes being used for military purposes.”

The number of persons within the peace churches actually withholding a portion

of their taxes is still thought to be small, but it is growing. The Internal

Revenue Service will not release figures on the number of tax resisters in the

United States.

Members of the Green Lake planning group include John K. Stoner, Mennonite Central Committee, Akron, Pennsylvania; Lorton Heusel, Friends United Meeting, Richmond, Indiana; and Chuck Boyer, Church of the Brethren, Elgin, Illinois.

Coordinator for the New Call to Peacemaking is Robert J. Rumsey, Plainfield, Indiana.

After the gathering, The Mennonite seemed surprised at how tame and nonconfrontational it ended up being (they titled their article “Peacemakers shy away from shocking anyone”).

Excerpts:

The Green Lake conference is part of a cooperative effort by the historic peace groups to do five things — stir up rededication to the Christian peace witness, clarify the biblical basis for it, extend a call to the larger church to see peacemaking as a gospel imperative, propose actions the U.S. Government can take for peacemaking, and determine contemporary positive strategy for peace and justice.

Planning for the consultation began in and has included 26 regional meetings in 16 different areas of the United States.

Over 1500 people were involved in these meetings.

[Church of the Brethren theologian and professor Dale] Brown said one new way of expressing a peace witness was to protest the country’s military expenditures by withholding income taxes.

Tax resistance, he reflected, is an important symbol because it involves our pocketbooks and enlarges the peace witness beyond what 17- and 18-year-old youth do in response to conscription.

[T]he findings committee created a final document satisfying the diverse peaceniks.

For the conservative the final statement was too radical; for the activists it was too limp.

There are two main thrusts to the document — actions that are directed inward

among the peace churches to enhance the integrity of the peace witness, and

actions that are directed outward to enlarge the visibility of the peace

witness.

At the end of the national New Call to Peacemaking conference delegates urged all Friends (Quakers), Mennonites, and Brethren to firmly oppose militarism and to become personally involved in the struggle for justice for the oppressed.

Included in the final paper approved is a call to the 400,000 members of the three peace church

traditions “to seriously consider refusal to pay the military portion of their

federal taxes as a response to Christ’s call to radical discipleship.” This

statement is as strong as the 300 delegates could jointly affirm.

Other parts of the war tax statement are equally muted.

In the first draft of the paper, church and conference agencies were asked to “honor” the requests of employees who do not want the military portion of their taxes remitted to the government.

In the final draft, however, “honor” is changed to “enter into dialogue with.” Several evangelical Quakers were especially antagonistic to even including a reference to war tax resistance in the final document.

Yet tax resistance received new encouragement from the conference.

About 60 persons attended a Saturday afternoon workshop which detailed tax resistance strategies.

Studying the War Tax Issue and Christian Civil Responsibility

The Mennonite General Conference had been asked to stop withholding taxes from the paycheck of one of its conscientiously objecting employees.

This led to a long debate over the advisability of such a policy that caused arguments about war tax resistance to echo throughout the Conference in .

A special General Conference delegate session was scheduled to convene in just to respond to this single issue.

In preparation for that session, congregations had been encouraged to put some

serious effort into understanding the subject, and some studies were written up

to help guide these investigations.

A Christian’s response to civil authority will be given concentrated emphasis by the General Conference during .

The study is an outcome of a resolution at the triennial conference in Bluffton, Ohio, .

That resolution called for a thorough study of civil disobedience which is intended to state an official position of the General Conference with respect to that portion of income taxes which are used for funding military expenditures, and in general, to research the whole question of obedience-disobedience to civil authority.

Responsibility for the study has been given to the peace and social concerns

committee of the Commission on Home Ministries. They, however, requested that

a special obedience-civil disobedience committee be formed to give general

direction and leadership. This latter group consists of Palmer Becker, Ted

Stuckey, John Gaeddert, Harold Regier, Perry Yoder, and Heinz Janzen.

To date three major aspects of the study have been planned — an attitudinal survey, an invitational consultation in , and a study guide to be ready by .

Included in the survey are twenty-eight questions with responses varying from

“strongly agree” to “strongly disagree” chosen to provide an inventory of

congregational attitudes towards the authority of the church, and of the

state. It will also indicate attitudes to particular issues such as abortion,

capital punishment, and payment of taxes for military purposes. A copy of the

questionnaire will be sent to every congregation to be duplicated locally.

A second major happening is scheduled for at Mennonite Biblical Seminary, Elkhart, Indiana.

An invitational consultation will bring together about thirty participants, including persons not committed to civil disobedience.

The gathering will include administrative personnel from the General Conference, lawyers, biblical scholars, as well as representatives from Mennonite Central Committee and the Mennonite Church.

It is expected that the study guide will evolve from the proceedings of the

consultation. Five of the thirteen lessons in the guide will focus on

peacemaking in a technological society. What sort of peacemaking should

Mennonites be about in an age of nuclear warfare and worldwide arms shipments?

The remaining eight lessons will center about the meaning of civil

disobedience. Was it practiced in the Bible? Is nonpayment of taxes a case in

point?

The study process will culminate in the special midtriennium conference scheduled for .

That gathering will be an official decision-making conference to which congregational delegates will come.

At that point a decision on the meaning and practice of civil disobedience will be made.

After the conference the questionnaire

will again be used to determine whether the churchwide discussion on

obedience-civil disobedience has generated any changes in attitudes.

A few more details came after the Commission on Home Ministries met in , and, according to The Mennonite:

Perry Yoder, part-time CHM staff member, outlined the process planned for dealing with the war tax or civil responsibility issue raised at the Bluffton conference.

Because of this issue’s “divisive and emotional potential in the conference,” a survey instrument has been designed to get congregational input; a consultation at the seminary will work toward a study guide, and congregations will be encouraged to use the study in preparation for a special General Conference delegate session at Minneapolis, called solely for the purpose of responding to the Bluffton resolution on tax withholding.

Another article said this study guide would be “available [and] will look at present militarism in North America, previous acts of dissent by Mennonites, and biblical texts on dissent, payment of taxes, and corporate action.”

During the first session on , board members locked onto the planning for the midtriennium conference on war taxes and civil responsibility.

Uneasiness about the process erupted quickly.

The structure of the invitational consultation on the issue was strongly faulted, as was the conference itself.

Board member Ken Bauman, pastor of First Mennonite Church in Berne, Indiana,

galvanized his colleagues with his allegations. “The consultation is not

structured for dialogue — it is monologue. The way it has been set up upsets

me deeply.” Later he declared that the Commission on Home Ministries should

not serve as the launching pad for the study and the planning leading to the

conference in . “Why ask

CHM?

The image of

CHM

is stacked. It should be the responsibility of the General Board.”

His assessment was the beginning of a fruitful debate which occupied several more sessions of the General Board, one session of CHM and hallway discussions.

The debate crystallized about several key questions. What is wrong with the

study process initiated by the obedience-civil disobedience committee of

CHM?

Is the issue of war taxes so divisive that a schism in the General Conference

is inevitable? Is the delegate

conference viable?

By , perhaps symbolically, the hard-hitting process of charge and countercharge had evolved into understanding and affirmation of the original plans.

On paper, little had changed, but in the minds of those who spoke for the “unheard,” — the “conservatives,” the “common person,” and the Canadians — there was a restoration of confidence in the process.

Tenseness was dissipated.

The mood became one of working together.

The consultation will meet at Mennonite

Biblical Seminary, Elkhart, Indiana. About twenty-five persons are invited.

These include theologians and biblical scholars, attorneys, administrative

staff of the General Conference, several

MCC

staff, and representatives from the Mennonite Church and the Mennonite

Brethren Church. The proceedings of the consultation are to serve as the basis

for a study guide on civil disobedience.

The committee planning the consultation and the midtriennium conference was called in to justify its ideas.

One member, Perry Yoder, observed, “Getting people to participate is very difficult.

People are very tense about this.”

“We thought the trust level would be quite high,” said another member, Harold

Regier. “Requests for speakers were made on the basis of scholarship and the

purpose is biblical. It is not a matter of pro or con.”

“We don’t know where the scholars will come out,” declared Don Steelberg, chairperson of CHM. (A complete list of scholars invited is not yet available — some are still considering the invitation.)

It was noted that since the concern on abortion had been handled insensitively

at the Bluffton conference, there was fear that the same thing would happen

with the issue of war taxes. So why should those who oppose withholding war

taxes bother to participate? They won’t be heard anyway.

Another fear was that the Canadians would also stay away. “My gut reaction is that it is a U.S. issue,” said board member Loretta Fast.

She was challenged on that.

“Don’t Canadians also pay military taxes?” queried Ben Sprunger.

“Yes,” replied another Canadian board member, Jake Klassen, “but we have not gone through the trauma and frustrations of the Vietnam War."

Hence, if both the Canadians and those opposed to withholding war taxes stayed

away from the delegate