How you can resist funding the government →

my tax resistance →

levies, liens, seizures

I got another letter from the IRS .

This is the letter that ought to be preceded by a drum roll and delivered with the sound of a falling guillotine blade.

It’s not supposed to be followed by a laugh track, but in this case it is.

Read on.

The letter is a Form 8519: “Taxpayer’s Copy of Notice of Levy.”

If they followed procedure, they sent this notice out to me soon after they filed a similar notice (a 668-A) with Wells Fargo Bank, which holds the account from which they intend to seize my money.

Wells Fargo, in turn, is supposed to turn over the amount of the levy to the IRS 21 days after receiving this notice.

“No withdrawals may be made on levied upon deposits during the 21-day holding period,” so I can’t just pull my money out of the account now so as to foil the levy.

They’ve figured the total with interest and penalties out to , and they’re after $5,603.06 all told.

Here’s the gigglicious part:

I’ve had this bank account .

It was my first checking account.

But I started to get annoyed with Wells Fargo because they keep changing their rules around in an effort to stick me with a monthly fee, and because their account features aren’t much to get excited about in this day and age.

I mostly like ’em because they have ATMs all over the place in San Francisco.

Several days ago I decided I was going to switch to another bank, and began making the switch — transferring out my remaining balance, changing any automatic deposits and withdrawals, etc.

To make a long story short: Last I checked, I have a total of $5.16 left on deposit at Wells Fargo.

I’m sure they won’t just give up when they discover that their first attempt to seize my assets got them pocket change.

They’ll hunt down something else with my social security number attached to it and try to gobble it up as well.

But I still think it’s funny.

I imagine that I would not be laughing so hard if I had written any checks on this account that hadn’t cleared yet — that would be expensive and embarrassing.

There are some additional risks like these that come from playing chicken with the IRS.

Wells Fargo may also try to hit me with some sort of fee for putting up with the IRS paperwork.

I’ll keep you posted.

Periodically, I plan to tally up these sorts of costs along with the penalties & interest as a way of trying to assess the worth of this method of tax resistance.

My bank has finally gotten around to writing me a letter explaining what happened to my old checking account.

The upshot is that the IRS seized $5.16 in a levy (which was all I had in the account at the time), and Wells Fargo charged me $75 to reimburse them for the trouble.

This put my account into negative territory, so they’ve since charged me another $31.50 in overdraft fees.

(Do these charges seem high to you? Me too.

That’s a big reason why I decided to leave Wells Fargo behind.

They seem to have adopted a “squeeze every penny you can out of your customer” business model.)

So add these to the “costs” in my cost/benefit analysis of this tax resistance method.

I got levied again .

, as you may remember, the IRS comically levied an account I was in the process of closing, and so they only ended up with $5.16. This time it’s more serious: they hit a savings account I have, and in the process managed to tap into a joint account my sweetie & I have at the same bank that we use for household expenses.

This time they’ll get about $4,350 — still short of the $5,700 or so that they’re looking for, but a much bigger dent.

The bank has frozen both accounts, and plans to cut a check to the IRS .

Until that happens, we can’t withdraw from either account, and if we deposit any money it’s in danger of being swept up into the levy.

(This contradicts some other things I’ve read about levies, which say that a levy only applies to the amounts that are in the accounts at the time the levy is received, and any additional deposits aren’t affected unless another levy comes in.)

There are two or three outstanding charges that I charged to a credit card that’s linked to the joint account.

I’m not sure how that’s going to play out.

In addition, the bank’s policy states that “You’re responsible for any losses, costs, or expenses we incur as a result of any dispute or legal proceeding involving your [account].”

I have no idea what that might translate to in dollars and cents, but I assume I’ll find out.

Inconvenience-wise, we’re no longer going to be able to use the joint account to pay our bills, buy groceries, and so forth.

We’ll have to go back to accounting for that differently and settle our accounts manually.

In retrospect, it clearly wasn’t a smart idea for me to put my name on our joint account (and then to tempt fate further by having that account at the same bank as my own interest-bearing savings account).

Live and learn.

I received a notice of levy from the

IRS.

(Form 8159 — Taxpayer’s Copy of Notice of Levy.)

In , they levied an

account I was in the process of closing, and ended up with about five dollars.

In they levied another bank account

and emptied it out to the tune of about $4,350. This new levy is the first one

since then.

They’re trying to get $1,385 and they’ll probably get it all, as I have more

than that in this account.

This should effectively close out my delinquent taxes for

, with them managing to seize

all of what I didn’t pay in those years, plus interest and penalties. They

don’t seem to be trying to chase me down for what I didn’t pay last year. I

think this must be because I had to file a corrected return because they

incorrectly modified the return I filed in

— see

The Picket Line for

for details about that — and this corrected return is probably still making its way through the system.

The three accounts they’ve gone after are three accounts for which they would

have gotten 1099 forms reporting interest in previous tax years. That’s no big

surprise.

The total they’ve seized includes $4955 in delinquent taxes and $814 in

interest and penalties. (This includes the seizure of a small, incorrectly

refunded California state tax payment, if you’re wondering why these numbers

don’t all add up right.)

What have I learned?

that the

IRS

will come after accounts it learns about via 1099s

that the amount of time that passes between levies varies, in the case of

my three levies, from one month to six

that once it’s started issuing levies the agency will try to keep going

until it runs out of delinquent taxes to pursue or sources to levy, even

if the amount being pursued falls to a fairly low level

that if a corrected tax return is still being processed, even if the

ultimate tax shown on the return is not being disputed, this may put the

collection process on hold for that return

If you’re wondering why I’m bothering to resist taxes in this way, since the

government has been effective at seizing the money with icing on top anyway,

see The Picket Line

for for an in-depth

look at some of the reasoning behind this.

As I mentioned , the IRS levied my bank account. , my bank cut the U.S. Treasury a check for $1,384.71 and debited my account by that much.

In-between, there was a period of a few days in which the account was completely frozen.

After that, I was able to make ordinary withdrawals and pay bills and such, but I had to get a special phone authorization to transfer money between accounts (even if the amount was small enough that it left enough to satisfy the levy).

Overall, the process was pretty painless, except for that part about the government getting my money.

Heh heh.

I should have known better.

Two days after I compose a nice Picket Line entry speculating why the IRS had sent me a “final notice of intent to levy” and then three months later hadn’t done anything about it… they send me a notice of levy!

But here’s the thing.

Remember how back in when I got my first IRS levy the IRS tried to clean out a bank account that I was in the process of closing?

How they ended up getting a grand total of $5.16?

Well, they went after that account again.

And I did close it, over a year ago, and never reopened it.

So this time they’re going to get even less.

But at least I know they haven’t forgotten me.

So if you remember from the last episode of Days of our Levies, the IRS sent me a levy notice telling me they planned to seize a bank account I closed in .

That having failed to work out as planned, they’re back for another try.

I got another levy notice.

They’re going after a relatively new account, so they must finally be operating off of my latest set of W-2s. Still, there’s not much there to seize.

They’ll get less than 10% of what they’re after at worst.

Wonder what they’ll try next.

I just got official word that the IRS levied $345.19 from a bank account of mine.

That’s only about 7½% of what they were hoping to find, but I’m still sad to see it go.

The IRS, repeating a trick it’s tried before, has sent a notice of levy to a bank I no longer do business with asking them to turn over funds from an account I long since closed.

I got a letter the other day from my health insurance company, letting me know that their IT vendor, IBM, had lost track of a bunch of hard drives on which were a bunch of client records, possibly including mine.

They extended me an offer to join something called an “identity protection network” on their dime, and encouraged me to go take a look at my credit report to see if anyone else was trying to get loans or credit cards or what have you by using my identity.

So far there’s nothing suspicious looking there, but in the course of looking at my credit report I noticed that there’s a section on it entitled “Public Records” that is meant to list things like “bankruptcies, liens or judgments… from federal, state or county court records.”

That section is blank on my credit report, which seems to indicate that the IRS either has not filed a lien for my back taxes, the sort of lien they file doesn’t show up in public records like this, or the credit reporting agency hasn’t managed to find out about it (I’m not sure which).

In any case, so far as the credit reporting agency (and anyone who requests their report on me) is concerned, I don’t have any tax lien.

I got three letters from the IRS today — the first I’d heard from them since .

Back then, they were sending me notices of “intent to levy” but they seem to have had some reluctance to transform their intentions into action, since no levies were forthcoming.

The latest batch of letters is even tamer.

They’re just “Reminder of overdue taxes” letters for , , and (in I didn’t make enough money to owe taxes).

They’re mostly notable for the improvement in their layout.

The letters have a section with a chart that shows how the interest charges have accumulated during different spans with different interest rates (the interest rates have vacillated some, with the trend declining from a high of 6% in to 3% ).

Tax Year

They think I owed*

Subsequent interest and penalties

Total

Seized

Outstanding

13,708

1,657

15,365

6,072

9,292

* may include an initial late payment penalty

$784

$255

$1,039

$1,039

$0

4,170

559

4,729

4,729

0

3,695

633

4,328

304

4,023

0

0

0

0

0

1,203

87

1,290

0

1,290

3,856

123

3,979

0

3,979

To this you can add another $4,000 or so for , but they don’t know about that yet.

That may explain their lack of attention, as my $9,292 outstanding balance is below what I understand to be the threshold at which the IRS feels moved to take action these days.

It wouldn’t be the IRS if they didn’t screw up something, and I notice that their software failed to correctly credit me for the partial seizure in in their page one total (though it does show up in the course of the itemized interest calculations on page two).

I got four letters from the IRS that purported to sum up my total unpaid taxes, along with interest & penalties, for , , , and .

Their numbers didn’t add up consistently even within their own printouts, though, so I thought I’d dig a little deeper.

I requested my “tax account transcripts” for those years from the IRS.

(This is easy to do: you can request your transcripts from the IRS website.)

They arrived on (in four separate envelopes, naturally, as the agency’s way of reminding me how respectfully it spends taxpayer dollars).

These are interesting artifacts, but in many ways they only add to my bewilderment.

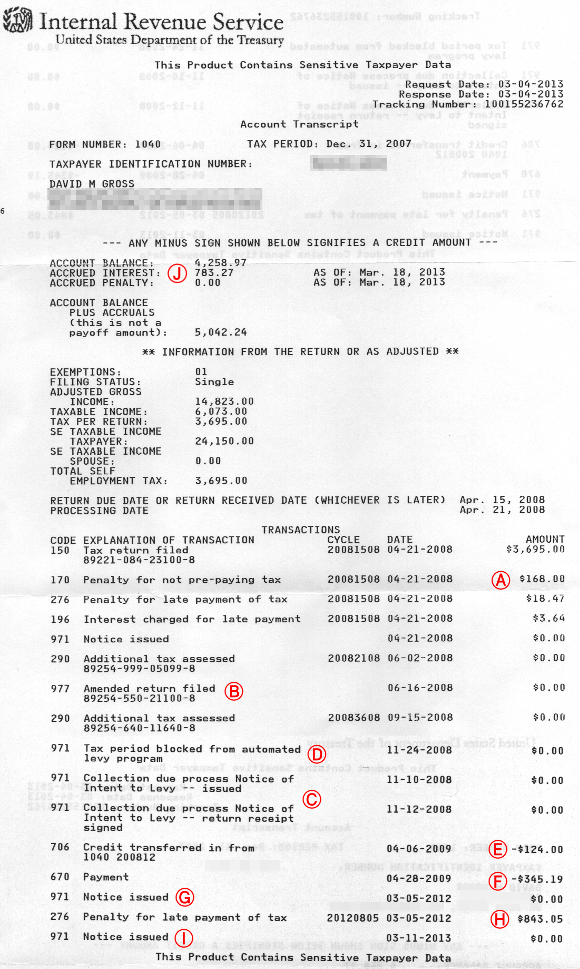

I’ll show you one of the transcripts they sent me below, and add some comments and explanations.

The original transcript was two pages — I’ve pasted them together in this illustration.

I added the red circled letters for my annotations below:

First, a note: In there was

a weird glitch in which the

IRS

erased the “personal exemption” from my

return. Perhaps somebody tried to claim me as a dependent on their tax return,

or accidentally filled in my social security number for that of their actual

dependent, or maybe it was just a snafu — I

never did get an explanation. I simply filed an amended return reinstating

my personal exemption and left it at that. It didn’t effect the bottom line in

any case, so I didn’t give it much thought afterwards.

The transcript shows my initial tax assessment ($3,695.00), the penalty

immediately assessed on me for not having paid any of this in quarterly

installments ($168), the initial late payment penalty for not having enclosed

a check with my tax return ($18.47), and a small amount of interest that had

accumulated at the time of their first delinquency notice to me ($3.64). All

of that matches my records. (Ⓐ)

In June they erased my personal exemption, then took note of my amended return

in which I reinstated it (Ⓑ). I didn’t get

official word that they’d accepted my

amended return until . I think

their phrase for “we changed the numbers on your tax return” is “Additional

tax assessed” since it appears twice on the transcript around here, once to

omit the personal exemption and once to reinstate it, though neither of these

occasions actually resulted in an assessment of additional tax.

On I got an “Intent to Levy” letter from the

IRS for

the tax year. This also does not show up on

the transcript. That letter listed $166.28 in accumulated penalties and $98.46

in accumulated interest, and asserted that my original tax due was $3,885.11

(which actually is the amount of my original tax due, plus the failure to file

quarterly penalty, plus the initial late payment penalty, plus the first

amount of interest that accumulated).

On I got a “final notice of intent to levy” letter. This

is mentioned in the transcript: both the date it was issued, and the

date the

IRS

was notified that I signed for the letter (Ⓒ). By this time, the accumulated

penalties & interest on the original $3,695 tax bill had risen to a bit

over $572.

Here something peculiar shows up in the transcript: “Tax period blocked from

automated levy program” (Ⓓ). This, just two weeks after they’d issued me a

“final notice of intent to levy.” I’m not sure how to interpret this. (Note

also that this appears out of chronological order in the transcript, just from

perverseness I suspect.) There’s also one of these on my

transcript.

When I filed my return in (for the

tax year) I had so little income to report

that I actually was one of those “lucky duckies” who not only owed no taxes

but qualified for a refundable earned income tax credit: a whole $124. The

IRS

seized this refund and applied it to my unpaid

taxes. This shows up on the transcript (Ⓔ).

They also credit me for a “Payment” of $345.19 on

(Ⓕ). This was actually

a levy of a bank account of mine…

so apparently that “block” issued in

had been released or had expired

by then, or perhaps this levy was not one of the “automated” variety.

I got another letter from the

IRS in

complaining about

the unpaid balance, and then

another in

. These don’t show up in the

transcript either.

The

IRS

tried to seize another bank account , but I’d long since closed it. By then, the interest and

penalties had risen to $985.14. Neither an indication of the levy attempt,

nor any amounts of interest & penalties from this period show up on the

transcript.

The next thing that does show up in the transcript, after

, is

a “reminder of overdue taxes” that they

sent me (Ⓖ). This is

accompanied, in the transcript, with a late payment penalty of $843.05 (Ⓗ).

The transcript also notes

the letter it sent me

, though it gets the

date wrong (Ⓘ).

The transcript also has a summing-up section (Ⓙ), which just makes things

worse:

ACCOUNT BALANCE PLUS ACCRUALS

(this is not a payoff amount): 5,042.24

Why does the interest “accrue”, but the penalty just gets added to the account

balance? If they just are going to add the penalty to the account balance, why

do they bother to have an “accrued penalty” line on the transcript? Why, if

this is their policy, do I only have a zero accrued penalty amount on my

and

transcripts, while my and

transcripts do show accrued

penalties?

The account balance does seem to add up to my original tax owed plus

that original set of penalties and interest (Ⓐ), plus the $843.05 in penalties

(Ⓗ), minus what they managed to seize from me (Ⓔ) & (Ⓕ). I can’t tell you

how surprised I was to find some set of numbers on the page that added up to

another number on the page in a semi-intuitive way, though it took me a while

to develop the correct formula, and I couldn’t tell you why they stuff that

original interest amount in there.

I was a little puzzled at first as to why they stopped assessing penalties

, but I think by that point the

penalty had reached its legal maximum — 25% of the unpaid amount. From here on

out there will be no more penalties on my

taxes, though the interest will continue to accrue.

I got a new (for me) kind of letter from the IRS today.

It was headlined as follows:

Your account has been assigned for enforcement action

Please call us about your unpaid taxes

It was sent by regular mail (not certified mail, like the IRS occasionally uses).

It consolidated all of my unpaid tax years (often the IRS will send a different letter for each tax year).

There was a lot of boilerplate, but the important text seemed to be:

We’re trying to collect unpaid taxes from you for the year(s) shown in the billing details below.

We have assigned your account for enforcement action.

Enforcement action may include seizing your wages or property.

It’s important that we hear from you within 10 days.

The letter leaves it ambiguous to whom they have assigned my account.

I looked for some indication of whether they might have assigned it to one of the semi-private debt collection agencies the IRS is now required to send some accounts to.

I didn’t find anything to indicate this.

But the text about “Enforcement action may include seizing your wages or property” — things the semi-private companies cannot do — suggests that maybe they’re keeping my account in-house.

I’ve heard (but not verified) that the semi-private companies are only being assigned accounts totaling less than $50,000. Mine, according to the letter, currently stands at $51,707.53, so I may have missed the cut-off.

Too bad.

I was hoping to document that process for you.

So given that the last time I got one of these notices, it was quickly followed by seizure attempts, and that I haven’t gotten one of these letters or been bothered by any seizure attempts since 2009, I should probably brace for trouble.

I used the IRS’s “Get Transcript” service to check my latest “Wage & Income Transcript” to see what assets and revenue sources the agency knows about for certain.

I was a bit surprised to find that they apparently don’t have anything about my most significant source of income for last year.

I’m guessing they just lost or mishandled the paperwork.

Lucky me.

What do they know about?

a small Roth IRA

that I transferred $5,000 from my regular IRA into my Roth IRA at a brokerage different from the one that holds that small Roth

my Health Savings Account

a Lending Club account that by now has less than $100 in it

the royalties I get from Amazon for the sales of my books

The IRS tends not to go after IRAs and HSAs until they get desperate.

As the clock is ticking on the statute of limitations for the oldest year in my account, though, they may be getting to that stage.

If they go after my Lending Club account and my book royalties, they’ll be pretty disappointed by how little they end up with.

I can partially stymie them in that case by putting all of my books on sale and stopping the royalties.

If they clean out my retirement accounts there’s not much I can do about it.

The worst thing would be if they hit my HSA.

Not only would they take my money but I’d get hit with a penalty for using my HSA for non-health-related spending (I’m not sure if I could ameliorate this by quickly making a deposit to the account to make up for it).

The IRS has filed a federal tax lien against me.

They could have done this years ago, so it’s something of a mystery as to why they waited so long.

They may have decided to strike now because the oldest of my unpaid federal tax amounts will hit the statute of limitations and become uncollectible in a few months, or it may be because the total amount they’re after me for has popped over the $50,000 threshold and that has made them kick things into a higher gear.

The letter announcing the tax lien came to me by certified mail , but I wasn’t around to sign for it so didn’t have a chance to look at it until I picked it up at the post office .

The lien itself was filed by the IRS in our local County Recorder’s office back on .

The lien pursues me for amounts for tax years , but peculiarly does not seem to cover the entire amount for any of those years.

I can go to the View Your Tax Account feature at the IRS website to get the latest figures of my account balances.

Compare that to what the agency is seeking from me in their lien:

Year

My Tax Account

Tax Lien

53,389.87

50,437.23

2007

5,971.68

5,732.50

2009

1,932.50

1,863.87

2010

5,984.57

5,772.02

2011

6,048.27

5,833.45

2012

6,384.13

6,157.39

2013

8,381.43

8,083.75

2014

7,582.57

7,126.38

2015

6,449.96

5,689.67

2016

4,654.76

4,178.20

I don’t know how to explain the discrepancy.

It’s much too large for it to be just the result of interest and penalties that have accumulated since the lien was filed.

Maybe the process of filing a lien is so lengthy that those figures represent accurate numbers from months and months ago when the process began.

How does this affect me?

If I owned any serious property, this could be one step in the IRS’s attempt to seize it from me.

I don’t, so this isn’t much of a worry.

I suppose they might try to seize payments from my business clients or royalties from the sales of my books, but I think they could have done that anyway if they were on top of things.

This lien will likely show up on my credit report, so if I had any plans to try to finance any big purchases, that could get in my way.

If I were to win a court settlement, inherit an estate, or in some other way come into money in a way that’s mediated by the government, the IRS would be likely to intervene and take the money for themselves.

I’m not sure what will happen if the statute of limitations strikes my 2007 account before they are able to collect.

Will the whole lien be invalidated at that point, or will I need to challenge it for that to happen, or will the agency refile the lien with new totals?

As I noted , after 15 years of my resisting taxes, the IRS finally got around to filing a tax lien against me.

This so far has had little practical effect.

But the filing amounted to a public notice of my tax debt, and it was noticed by those who prey on such people.

I’ve been getting lots of calls from spoofed numbers in the same area code as my phone.

I don’t answer, and they almost never leave messages, so I don’t know if they’re scammers trying to impersonate the IRS in order to extort money from me (a common fraud these days) or “pennies on the dollar” tax debt resolution specialists.

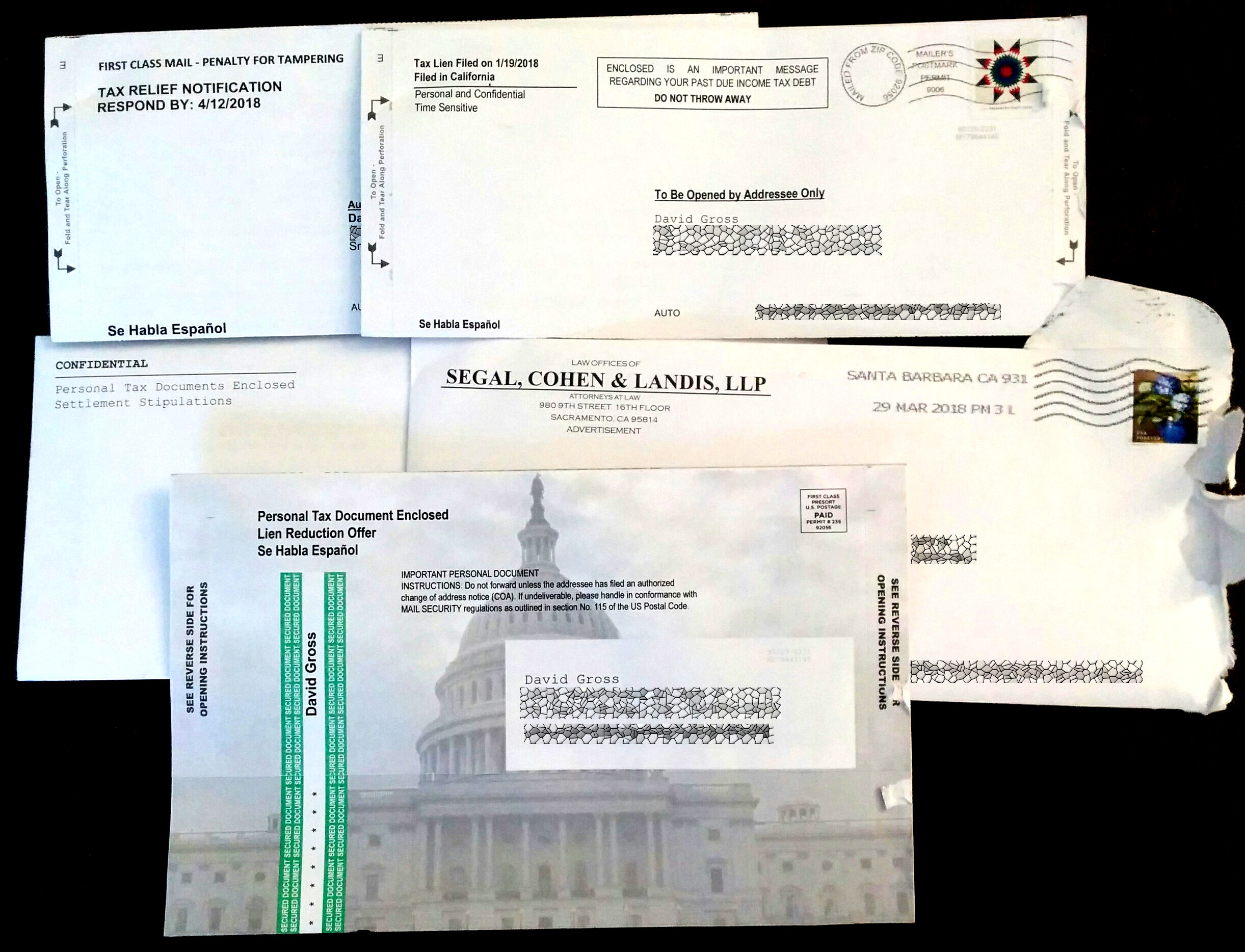

yesterday’s mail

I’ve also recently started getting a lot of mail from the latter sort of predator.

The photo here shows five letters I got yesterday (Update: I got seven more on ).

Most of them try to mimic the look of official notices from the IRS or other governmental offices.

One more honest one came from a law office and didn’t try to hide itself.

I didn’t open most of them, as they’re all more or less the same thing: invitations to let them negotiate my tax debt with the IRS and promises that they can get the debt dramatically reduced for me (for a fee, of course).

The IRS does have an Offer in Compromise program, which I might qualify for, and which would allow me to settle my tax debt for less, maybe even much less, than I owe.

But it would require that I start paying them something, which I’m not prepared to do.

So it’s a non-starter.

I got a certified letter (one I had to sign for) from the IRS today.

It announces that the agency has filed a “Federal Tax Lien” with my local county recorder.

The lien was prepared on but only filed .

I suppose I can expect them to do this each year now.

I wonder if I’ll get another flood of junk mail and spam calls from people offering to solve my tax debt problems cheap.

I got another “Notice of Federal Tax Lien Filing” notice in the mail yesterday.

It came by certified mail so I had to pick it up at the post office today.

It covers and so is meant to extend the previous lien they had filed which, last I checked, covered .

The amount is due to reach the statute of limitations expiration date in a few months, so they’d better hurry.

The “Notice of Federal Tax Lien” was filed with my local court system by the IRS.

It is meant to put the general public on notice that “there is a lien in favor of the United States on all property and rights to property belonging to this taxpayer.”

The agency first filed a lien against me in 2018 and then extended it last year.

This did not prevent one of my unpaid tax years from being erased by the statute of limitations.

If I needed to borrow a lot of money for some reason, I imagine the bank I was trying to borrow from would probably raise an eyebrow when they learned of the lien, but so far none of my projects has involved borrowing money and I don’t anticipate this changing.

The liens have had no practical effect on my life thusfar.

The only real effect has been that I get a lot of junkmail from legal firms claiming to be able to settle my taxes for pennies on the dollar.

The notice came with a bunch of inserts: Publication 594 (The Collection Process), Publication 1450 (Instructions on Requesting a Certificate of Release of Federal Tax Lien), Publication 1660 (Collection Appeal Rights), Form 668 (Notice of Federal Tax Lien), and Form 12153 (Request for a Collection Due Process Hearing).

As I noted a little over a month ago, the IRS filed a new tax lien against me in our local court system.

This was a renewal of the lien they had filed the previous year, with updated numbers.

It hasn’t had any practical effect on my life or my resistance and has not been a cause for alarm.

However, it has prompted an asston of junkmail.

Just today I got seven different pieces of mail from various outfits offering to settle my tax debt for pennies on the dollar (for a fee).

Over the weekend I got several more.

The lien must have just gotten published somewhere.

Most of these are designed to look official rather than commercial:

“URGENT DOCUMENT ENCLOSED: BACK TAX NOTICE” reads one envelope.

“VIOLATION SUMMARY ENCLOSED” reads another.

“Tax Debt Urgent Notice” reads a third.

“SUMMONS ENCLOSED — DELINQUENCY NOTICE” announces a fourth.

It must be a lucrative business, to have all these companies sending all this carefully-misleading mail.