How you can resist funding the government →

about the IRS and U.S. tax law/policy →

IRS incompetence →

enforcement effort/results →

statute of limitations on collections

A Congressional fight is ramping up over the IRS’s new privatized debt collection program.

One of the program’s defenders, Senator Chuck Grassley, sent a letter to his colleagues setting out his position.

There were some interesting statistics in the letter that I haven’t seen elsewhere.

For instance: “Every year, over $20 billion of unpaid taxes are lost due to the tolling of the 10-year statute of limitations.”

And:

[T]he average fully trained field function collection officer costs the government approximately $154,000 a year.

This includes salary, bonus, benefits, taxes, and a portion of direct overhead cost like supervision and administrative services, rent, travel, technology, telecommunications, postage, training, recruitment and other costs of business (not including a percentage of the Washington bureaucracy).

The Treasury Inspector General for Tax Administration found that in , these folks collected on average $577,000 each.

Now, that is an excellent return on investment, but simple math shows that for every dollar collected by these important IRS collection personnel, it cost the government conservatively 26 cents.

Senators Max Baucus and Chuck Grassley, the top Democrat and Republican on the Senate Finance Committee, issued a press release to convey their outrage or what-have-you.

Grassley summarized the new report this way:

For , while collections increased by $10 billion, unpaid debts

increased by the same amount. During this same time, the

IRS

wrote off from 31 percent to 46 percent of unpaid debts because it

essentially ran out of time to collect these debts. For

, the

IRS

classified only $100 billion out of $290 billion of unpaid tax debts as

collectible. Of the $100 billion potentially collectible debt, the

IRS is

actively pursuing only $25 billion with $2.5 billion being shelved because

of a claimed lack of resources. The longer a debt is outstanding, the less

likely it will be collected. Any business person can tell you that. Knowing

that the

IRS

isn’t going to collect the debt also gives tax cheats additional

incentives not to pay.

The senators conclude: “When all is said and done, over half of the tax debt

inventory that the

IRS

resolves will come from writing off the tax or being prevented from collecting

it under the 10 year statute of limitations.” The numbers in the report

specify this a little more precisely: 20–28% of these tax debts were “abated…

which may have been appropriate” and 31–46% were “written off due to statutory

limits on how long

IRS

could pursue the debt.” Only between 34–41% of the tax debts that were

“resolved” involved the

IRS

actually getting its hands on the money.

Expect the next Congress to try to come up with some ways to squeeze a little

more blood from that stone.

The report has some interesting background details on the

IRS

collection process, and a nice flowchart (see page 7 of the report) of how tax

debts get routed around (and sometimes stall) in the process.

Here, for instance, is the initial phase of the process for people who do not

file, spelled out nicely:

IRS

first is to send a “30-day letter” that includes a proposed assessment of

tax, penalty, and interest. The letter is to instruct the taxpayer on

possible ways to respond, such as by accepting the proposed assessment;

filing an original return; providing evidence that there is no filing

requirement; or appealing the proposed assessment to

IRS’s

Office of Appeals. If no response is received to the 30-day letter within the

allotted time,

IRS is

to send a 90-day statutory notice. The statutory notice is to contain

information similar to the 30-day letter and information on the taxpayer’s

right to petition the Tax Court. If

IRS

does not receive a response within the allotted time, the tax, penalty, and

interest on the return are to be assessed.

IRS’s

practice is to send up to four balance-due notices at 5-week intervals for

the amount owed. Six weeks after the fourth balance-due notice,

IRS is

to forward any unpaid accounts to

IRS

staff who are to try to collect the unpaid amounts through other phases of

the collection process — the telephone or in-person contact phases.

There were also some nuggets of information about new

IRS

enforcement-related projects. A few caught my eye:

Electronic Lien — to process over a million liens each year

Streamline and expedite lien filing, reduce lost lien reports, and ensure

prompt payment of lien filing fees by making process electronic.

Reduce costs for lost lien research and analysis by 15 percent in

and 40 percent in

. Similar savings in these 2 years in

lien filing fees. Collect additional revenue by raising

IRS’s priority against other creditors.

Bulk Electronic Levy

Automate the process for delivering levy notices to and processing

responses and remittances from financial institutions and large

employers, including the posting of levy payments to taxpayer

accounts.

Reduce the cycle time for sending levies. Reduce mailing costs. Expedite

posting of payments to taxpayers’ accounts.

Camera cell phones

Improve (1) productivity of revenue officers in determining asset

valuation, (2) communication between

IRS

and taxpayers, and (3) employee safety on field visits.

Increased employee and taxpayer satisfaction.

I assume that last bit means that when the

IRS

comes a-callin’, they’ll be whipping out their phone cameras to snap a quick

picture inside your doorway or outside your driveway so they can look at the

photos later and see if anything is worth stealing.

Some war tax resistance news that has scrolled by on my screen in recent days:

Erica Weiland, at the War Tax Talk blog, has

uncovered a case of successful war tax resistance from the archives of

NWTRCC’s

newsletter. The anonymous resister in question filed income tax returns,

refused to pay the amount “owed,” and then began to watch those unpaid

amounts disappear behind the statute-of-limitations curtain and beyond the

reach of the

IRS.

The resister made some attempts to make collection more difficult — not

owning big-ticket property, setting up a “gift annuity” and outright giving

money away to make current assets less-collectible, moving accounts from

bank to bank — but in part it seems to be

IRS

negligence or laziness that gets the credit. Good enough for government

work!

Canada’s Globe and Mail published

an obituary for Eldon Comfort,

a World War Ⅱ vet who became an anti-war activist. It quotes from a letter

he sent to the minister of revenue in :

Today, modern technology has introduced weapons of mass destruction. Their

cost is staggering. … So, in a very real sense when I pay my income tax, I

am complicit in the deployment of such armaments.

I am, therefore, claiming conscientious objection to the conscription of

my tax for military purposes. The percentage of the federal budget

designated for

DND

is deemed to be 8.1 per cent, so I have reduced my income tax by that

amount. This portion is being directed to

Conscience Canada’s peace

tax fund.

When the Canadian military operations were restricted to peacekeeping (in

its restricted sense), to search and rescue, and to succour during

national natural disasters, I had no quarrel with paying my taxes in full.

When the priority for the resolution of conflict, once again, becomes a

peaceful and diplomatic enterprise, I shall resume full payment.

Greg Slepak recognizes that by paying his taxes he becomes complicit in

what the government does with his tax money, but he has chosen a different

approach to that of conscientious war tax resisters. Instead of no longer

paying for the government’s misdeeds, he has identified one of the victims

of these misdeeds and

attempted to compensate him in proportion to how much he’d victimized him.

“To such a person, I have a sense of… indebtedness, as though I

owe him something. After thinking on it, I realized there might be some

truth to that.”

I recently became aware that a biography of Maurice McCrackin has been put on-line, including a chapter that covers his introduction war tax resistance and the early days of the Peacemakers group.

His tax resistance began, according to the book, when Wally Nelson noticed the pacifist minister removing toy guns and other war toys from those in a donation pile, and told him: “Do you ever think that next March 15 [then the income tax filing deadline] you’ll be paying for real guns?”

The next chapter covers his imprisonment for refusing to cooperate with an IRS summons.

Another chapter concerns his removal as a minister by officials of his Presbytery who were upset about his war tax resistance.

Matt Hisrich at the Quaker Libertarians blog takes issue with Quaker organizations who frame their opposition to government military spending in terms of reallocating that spending to other government priorities.

Excerpts:

This approach puts forth the false notion that national governments sit

atop vast reserves of wealth that should be spent on nonviolent rather

than violent ends.…

National governments cannot spend new wealth without either issuing new

debt (that will have to be repaid) or extracting it directly from

taxpayers through the implicit or explicit threat of violence. If Quakers

(or anyone else for that matter) want to be known as “Champions of Peace,”

it would be better to strive toward a reduction in the war spending that

seeks to keep funds in the hands of individuals to peacefully pursue their

own ends instead of merely shifting line items in national budgets. The

former focuses on individual and local empowerment, and the latter focuses

on somehow “winning” in the national political game.

While movement folks talk about the intersectionality of racism, sexism,

classism, homophobia, war, climate change, and economic exploitation, too

often we do not go beyond the rhetoric. We are inviting people involved in

resisting these serious problems to make time to engage in dialog with

those involved in other issues and movements. We need to explore how we can

work together.

There have been some interesting posts on the NWTRCC blog in recent weeks:

Tax Collection Phone Call Cons — international grifter call centers are siphoning money from gullible Americans by impersonating the IRS. War tax resisters may be particularly vulnerable as an angry call from the IRS is almost expected. Here’s what you need to know to keep from getting scammed.

Understanding common IRS collection letters — the IRS doesn’t tend to call you. They prefer to send you letters. Here’s a field guide to some of the variety of letters war tax resisters tend to see.

Join NWTRCC at the SOAW border convergence! — NWTRCC will be among the groups represented at a protest of U.S. border militarization and its treatment of new immigrants, migrant workers, and refugees .

Reasons to Celebrate — NWTRCC coordinator Ruth Benn celebrates another year of refused taxes sliding off of the statute-of-limitations 10-year limit and forever out of the IRS’s reach.

Ammon Hennacy and other early modern war tax resisters — Erica Weiland discusses some of the personalities and actions of the war tax resistance movement that began to coalesce in the United States around the end of World War Ⅱ, as found in Ammon Hennacy’s writings.

The Wealthy Accountant lists 10 ways to legally stop paying taxes — basically a list of varieties of income that are not taxed. You may find this useful food for thought.

The Keene, New Hampshire government has thrown all sorts of resources into trying to get a restraining order against the “Robin Hoods” who follow their parking enforcement officers around time, feeding the meters ahead of them and preventing them from writing lucrative tickets. So far, no luck, but they’re making one more desperate appeal to the state supreme court.

The tactic of paying your taxes in wagonloads of pennies or other small-denomination money, as a way of protesting and of obstructing the tax bureaucracy, is usually the one-off protest of a single fed-up person. But lately in Illinois, it’s become an organized and ongoing tactic:

Residents have to stick around if they pay property taxes in dollar bills — “Treasurer Glenda Miller announced a policy requiring people who pay their tax installments in large sums of cash to be physically present while the money is being counted. Miller said in a news release that the policy is for the protection of both the taxpayer and her staff.… ‘The five hours that it took for my staff to count the cash prevented her from continuing her regular office duties,’ Miller said.”

Tax protest group rallies, pays McHenry County property taxes in $1 bills — “Because Illinois has more units of government than any other state — property tax bills easily can have 10 or more bodies on them — attending all or most of their meetings to ask for tax relief is a huge undertaking for a taxpayer.”

Google Translate is only giving me a hint of what’s going on here but it included what sounds like an hours-long sit-in to block a tollgate, followed by arrests, in India.

I’ve been refusing to pay federal taxes for many years now, and this year I got

to experience one of those rare and beautiful triumphs we tax resisters

sometimes have: One of the tax debts the

IRS has

been pursuing me for fell off of the ten-year statute of limitations.

In I filed my federal tax return, showing

that I owed $3,695 in self-employment tax. I didn’t enclose a check. The

IRS came

after me with its usual series of exasperated demand letters, eventually adding

about $2,800 in interest & penalties to the original total. They even

successfully seized $469 from a bank account once.

But then they seemingly lost interest in the chase. At any time they could have

seized money from my

IRA

or tapped the client who sends me most of my self-employment revenue. But they

just plain dropped the ball.

I had allowed myself to hope that this would happen, but I didn’t really expect

it. I got away with it. I didn’t pay my taxes, weathered the

IRS

threats, called their bluff, and walked away without having to pay. That’s

pretty fantastic.

Here’s how I’m celebrating:

Enclosed, please find a check for $3,226 made out to the

Prisoners Literature Project. As a

former volunteer with PLP I

know how well this money will be spent.

Several years ago, I became unwilling to continue to offer financial support

to the U.S.

government by voluntarily paying taxes to it. In

, for example, I filed a tax return showing

that I owed $3,695, but I refused to write the check. The

IRS

has periodically sent me threatening notices about this, has added significant

penalties and interest to the total, and has even managed on one occasion to

seize $469 from my bank account. But , the ten year statute of limitations on that tax debt expired

without the

IRS

managing to collect the remaining $3,226.

That is to say: I totally got away with it.

I’m grateful for the opportunity to share my good fortune with the Prisoners

Literature Project and with those the Project serves.

Sincerely,

David M. Gross

P.S. My check comes to you via the People’s Life Fund, which operates as a way for conscientious tax resisters like myself to coordinate in order to redirect their taxes from harmful government spending to beneficial causes.

Links have been piling up in my bookmarks as I spent

poring through

back issues of The Mennonite.

International Tax Resistance News

A new law in Samoa requires previously untaxed church

ministers to pay income tax. Many, including those from the country’s

largest church,

are refusing to pay.

The United States government has begun

denying passports to people with large tax debts.

If you’re one of the 362,000 or so Americans who owe more than $51,000 and

you haven’t entered into an installment payment plan (I’m one of those),

you will likely soon find that you cannot successfully apply for or renew

your passport. While the government also has the legal authority to revoke

existing passports from such people, it is not yet exercising that

power.

Guerrilla electricians in Greece continue to

reestablish electric power

to households who have had their power cut off for inability or

unwillingness to pay the state utility monopoly’s bills which have been

inflated to support the state’s austerity budget policies.

Veterans of the successful campaign to abolish the

“écotaxe” in Brittany held

a celebratory picnic

on the anniversary of the destruction of one of the highway portals that

would have enforced the hated tax. In part the picnic was meant to show

solidarity with those who had been convicted of criminal charges for the

parts they played in destroying such portals, and in part it was meant as a

show of strength to let the government know they would not tolerate any

attempts to reestablish the tax.

The increasing use of traffic-ticket-issuing cameras worldwide as a

government revenue booster has led to a rash of direct action by the victim

population. This usually takes the form of destroying, disabling, or

blocking the cameras. Here are several recent examples:

Launched on as another variety of civic struggle against the dictatorship, the proposal to carry the thesis of civil disobedience to the extreme of applying a “tax strike” is still in force, but has not yet switched on, except in the Mercado Oriental.

On that date, the Academy of Sciences, and the Academy of Legal and Political Sciences, called for “civil disobedience as a national imperative to be put into operation immediately,” inviting employers, workers, students, and taxpayers to immediately suspend the payment of taxes to DGI, DGA, and city hall, in particular “withholding of Income Tax from salaries.”

Although the call for tax resistance enters the popular imagination as a civil form — and for that reason a legitimate one — of resisting the regime of Daniel Ortega, neither businesses nor individuals have responded with determination to the proposal, from fear or from caution.

Caution as demonstrated by the sources consulted for this article, who requested anonymity as they explained that people, business-owners and managers in particular, are afraid that the tax administration will fine them or, worse yet, temporarily take over operation of their companies or shutter their business.

Not all of the sanctions are catastrophic.

There are cases in which the fine applied is equivalent to 2.5% of the amount not paid in the case of the monthly advance payment of the business income tax, or 5% in the case of the value-added tax or of income tax withheld from the salaries of employees.

“Technically, it’s an invalid appropriation of withholdings, and can be criminally sanctioned,” in addition to being shut down, fined, or temporarily put under government management, explained a source with extensive experience in tax matters.

That said, this source sees a variety of reasons to doubt that they would decide to take such extreme measures, beginning with “as far as I know, they have never applied them to anyone.”

Another is that to close a business means sending its workers into unemployment, which implies that they will not receive taxes from the business or from those consumers.

But beyond believing in the mercy that any of these reasons implicitly assumes, the source points out fact that is easier to accept:

“If the resolution is massive, the tax administration simply does not have the capacity to audit and penalize everyone at once.”

Larger Companies Have More Fear

If it is decided to penalize only some in order to set a precedent that strikes fear into the others, surely one of the larger ones will be chosen, which not only has more ability to defend itself in the courts, but also to negotiate, precisely because of its size.

Another source asserts that “although it may seem obvious, the businesses that take the least risk are the most powerful ones, for the simple reason that they are not big taxpayers but big tax collectors.

“The DGI, does not want to be bothered with them, because if they weaken them, this affects tax revenues, principally value-added tax withholding.”

When the big companies that could take such measures don’t apply them, despite their intrinsic power, they are demonstrating “the cowardly face of big capital.

If they would decide, the blow to DGI would be immense,” s/he says.

Róger Arteaga, former director general of Revenue, agrees, saying that “big capital has not wanted to go all-in.

It is true that it gave its approval to the strike, but did so with fear and only temporarily.”

There is at least one group that risks more in a tax strike: import and export companies, which require clearances that can only be obtained once they have paid the corresponding taxes.

“If one of these business doesn’t make its monthly statement, or makes it but doesn’t pay, it falls into insolvency, and can neither import nor export.

The only importers who could afford that ‘luxury’ would be those that have sufficient product already on hand, especially at times like these, when there is little movement of inventory,” explained one of our sources.

Small- and medium-sized businesses — both fixed-quota and general regime — can stop paying taxes as long as the situation does not normalize, and while this makes them vulnerable to penalties, it is not likely that this will occur, especially, again, if a critical mass applies this measure of fiscal chastisement.

How long can the government last without taxes?

Our sources note that before making tax payments, the employer must guarantee the salary of its employees, and that the decision not to pay taxes is “protected by the higher legal concept, legally enshrined in the national legislation, as the Act of God and the Force Majeure.

Nobody is obligated to do the impossible, and the reason for this impossibility lies outside the control of the employer or employee.”

Citizens, on their part, could put pressure on big and medium-sized business, offering to act together if the Treasury moves against them.

“In this context, big capital must play a consistent role, acting firmly in the face of a Treasury that has granted them such special privileges.

It would be their most authentic repentance for the eleven years of tax advantages they have taken in the shadow of power.

That stain should be washed out right away,” they say.

As an expert, Arteaga proposes “that the businesses do not charge value-added tax, and the citizens not pay it.

Income tax also.

There are penalties, but the penalties and decisions of this government must be ignored, as they have no legitimacy.

How long can the government last without taxes?” he asked.

“Tax resistance aims to respond to Ortega’s claim that he will stay on through : we must find a solution, and one of these is for the private sector finally to decide on civil disobedience of a monetary and tax nature,” he explained.

Pedro Muñoz Fonseca, president of the executive committee of Costa Rica’s Social Christian Unity Party, urged Nicaraguans to use tax resistance against their government:

Social Media Tax Protest in Uganda

The government of Uganda has imposed a 5¢-per-day tax on using social media and

other services. This was designed as both a revenue measure and a way of

reducing what Ugandan president Yoweri Museveni calls lugambo

(“fake news”). Amnesty International has been among those to see through the

government’s rhetoric and cast the tax as

“a

clear attempt to undermine the right to freedom of expression.”

Robert Kyagulanyi, a Member of Parliament better known by his musician

stage name Bobi Wine, whose election is in part credited to his success on

social media, has been at the forefront of protests against the tax.

He was arrested, along with

three reporters when a march protesting the tax was attacked by police

with tear gas and rubber projectiles, but they managed to escape.

Ugandan protest marchers wearing shirts featuring a smart phone screen that

reads “This Tax Must Go”

War Tax Resistance Around the World

ABC reports on war tax resisters in Valencia — “the new refuseniks”.

War tax resisters there typically refuse to pay some percentage of their taxes, often basing this on the percentage of the federal budget that is spent on the military and similar items, and redirect this money to more worthy charities.

They declare this deduction on their tax forms in such a way that the tax agency typically does not treat it as illegal tax evasion but as an error or mistake.

The Global Day of Action on Military Spending Final Report has been released.

It gives a summary of the various events that took place around the world, including several by war tax resisters and groups promoting war tax resistance.

There’s a new NWTRCC newsletter out, with content including:

Ideas & Actions concerning weapons-free investing, responding to arguments against war tax resistance, a fast for nuclear disarmament, and more

You can now listen to audio excerpts from the upcoming documentary The Pacifist, about war tax resister Larry Bassett, on Spotify.

Erica Leigh pores through back issues of Conscience, the newsletter of the Conscience and Military Tax Campaign, an American war tax redirection group that slightly predates the founding of the National War Tax Resistance Coordinating Committee.

Raymond Hunthausen has died.

As Catholic archbishop of Seattle, he took a remarkably strong stand on nuclear weapons — famously calling the Trident nuclear submarine program being developed nearby “the Auschwitz of Puget Sound” — and began practicing war tax resistance in response.

This earned him enemies in Washington and in the Catholic hierarchy. Here are some of the obits and remembrances:

A biography of Hunthausen, A Disarming Spirit, will be released soon.

David McReynolds has died.

He was a long-time War Resisters League and Socialist Party activist and was also on the staff of the Committee for Nonviolent Action which helped to spearhead war tax resistance as a tactic during the campaigns opposing the American war in Vietnam.

He was among the signers of the “Writers and Editors War Tax Protest” in and of a similar public pledge .

David Paul Irish has died.

He was active with the Fellowship of Reconciliation, Women’s International League for Peace and Freedom, Peace Brigades International, and Witness for Peace.

He was an advocate for war tax resistance in the Society of Friends, drafting a minute in favor of of war tax resistance that the Twin Cities and Minneapolis Meetings approved in .

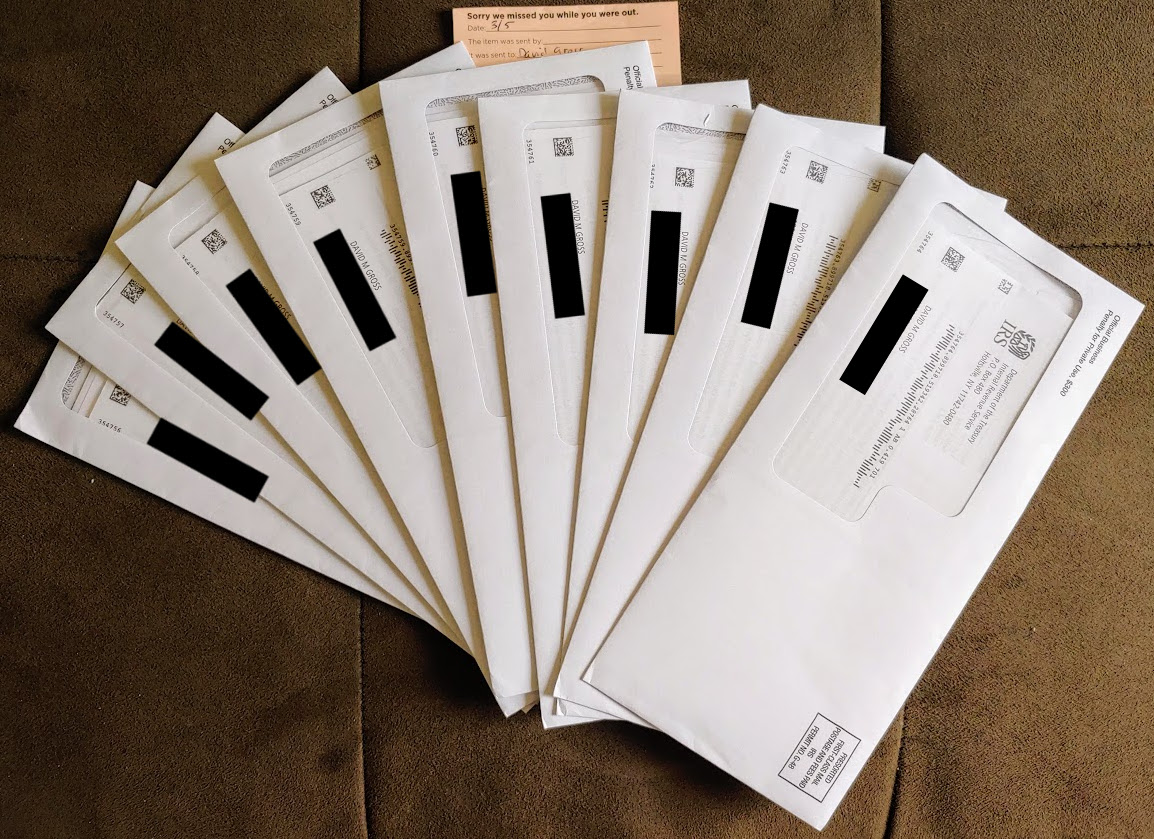

Another day, another nine freaking envelopes from the IRS.

Because it’s the government, the IRS sends me one notice, for each tax year for which I have refused payment, each in its own envelope with its own return envelope and three pages of boilerplate.

The letters simply tell me the balance due for each year.

A single four-page letter covering all the years would have conveyed the same information at less expense and bother, but they want to remind me how wastefully they squander the money other people give them.

However, for me there was a silver lining in all this boondoggletry.

The nine envelopes I got today covered tax years 2010–2018 (I haven’t filed for 2019 yet).

Tax year 2009 was missing.

This suggests to me that perhaps as far as the IRS is concerned, that year has already hit the ten-year statute of limitations expiration date for collection action and they have given up on it.

I won’t formally declare victory for another couple of months as I know a lot of times one of leviathan’s claws doesn’t know what the other claws are doing.

I note for example that in the IRS’s on-line tool for checking your tax balance my 2009 tax year still shows as due.

But it’s a promising sign.

Meanwhile, the agency still doesn’t have all of its tax forms ready for tax year 2019.

I ordered forms back in January , and they’ve been sending them to me in dribs and drabs since then, along with notices saying the rest are not yet available.

I currently owe the IRS something in the neighborhood of $73,350.

That’s $2,165 less than it was a few weeks ago because my oldest remaining tax debt fell off the statute of limitations ledge this month and became forever uncollectible.

Of what remains, about $51,000 is the original tax I owed, and the rest is penalties & interest.

In spite of that, I fully expect the IRS to send me a $1,200 “stimulus” payment (and a signed letter from our Dear Leader congratulating himself for giving it to me) before too long.

And today, I got a $8,100 “Paycheck Protection Program” loan.

Although it is technically a loan, it is designed in such a way that I am not expected to pay back the principal (I think I am on the hook for the 1% interest).

Even better, unlike most forgiven loans, this one will apparently not count as taxable income.

It’s just free money from The Man.

I’m a little astonished.

One bureau of the government sends me pleading letters demanding that I pay up, while others eagerly shove bundles of cash at me.

If you are a Schedule C / 1099 / sole proprietor / passthrough business whose livelihood is threatened by the whole pandemic thing, you should really look into this.

It seems to be a first-come/first-served sort of program, and the word is getting out in a sort of haphazard way, so tell your friends as well.

Recent links of note:

Some more details have emerged about the Biden administration plan to beef up the IRS enforcement budget.

Treasury Secretary Janet Yellen says the administration is seeking a $1.2 billion / 10.4% total increase in the agency budget, most of which would go to tax enforcement.

Every once in a while, the IRS crunches the numbers and tries to figure out the size of the “tax gap” — the difference between what Americans owe and what they actually cough up.

The problem is that there are a lot of unknowns — unpaid taxes that the government currently has no way of knowing that it is owed.

So it has to make guesses and extrapolations.

Now, in testimony to a Congressional committee, IRS Commissioner Charles Rettig has admitted what I’ve long suspected: the agency’s estimates of the “tax gap” have been far too low and the real number is more than double what has been reported.

Meanwhile, the IRS is still struggling to get through its backlog of tax year income tax return filings as this year’s tax filing season hits its peak.

This is further complicated this year by the agency’s role in administering a new stimulus check dispersal, and last-minute retroactive changes to the tax laws that made some already-filed returns incorrect and that gave the agency responsibility for rolling out a new tax credit.

I got a letter from the IRS that informed me they had notified the State Department that because I have a “seriously delinquent federal tax debt” that I ought to be denied a passport.

That in itself was a little peculiar, because they had already gone through this process back in .

Why, I wondered, are they doing it again?

By the terms of the law, such a notification to the State Department isn’t the sort of thing that expires and has to be periodically renewed, but is supposed to remain valid until revoked by the IRS.

So I did a little digging.

I looked at my account transcripts at irs.gov and discovered that, oddly, the agency had indeed issued its certification of my seriously delinquent federal tax debt in , but then had done it again in and then had reversed that certification in before again reapplying it .

There’s no rhyme or reason to that as far as I can tell.

My tax debt never fell below the threshold at which they are supposed to make this notification, and even if it had, the way the law is written makes the certification a sort of ratchet: it turns on when your tax delinquency reaches a certain dollar-amount threshold, but then doesn’t turn off until that amount gets all the way down to zero (or you enter into a payment plan or other such formal agreement).

This seems to have just been a glitch of some sort.

But that’s not the only interesting part of the notice I got yesterday.

It also contained a table of the tax years they’re pursuing me for.

It looks like this:

Your billing details

Tax period ending

Form number

Amount you owe

Additional interest

Additional penalty

Total

12/31/2010

1040

0.00

12/31/2011

1040

6,987.57

42.06

0.00

7,031.63

12/31/2012

1040

7,377.70

44.40

0.00

7,422.10

12/31/2013

1040

9,685.85

58.29

0.00

9,744.14

12/31/2014

1040

8,750.76

52.66

0.00

8,803.42

12/31/2015

1040

7,639.13

45.97

0.00

7,685.10

12/31/2016

1040

6,076.56

36.57

0.00

6,113.13

12/31/2017

1040

7,410.80

44.60

0.00

7,455.40

12/31/2018

1040

7,833.64

47.14

174.03

8,054.81

Two things to notice about this table: First, the blanks in the tax year 2010 row.

That’s further verification that the 2010 tax year has slipped beyond the statute of limitations deadline and that the IRS considers it permanently out of reach.

Second: the years stop at 2018.

The 2019 tax year is conspicuously missing.

That suggests to me that they’re still sitting on the tax return I filed more than a year ago, having not yet gotten around to entering it into their databases.

It’s further evidence of just how badly things are going for them over there.

IRS Circumvents “Statute of Limitations” by Ruth Benn.

Normally, the IRS has ten years to collect unpaid taxes from you before they have to give up.

Also, normally, if you decide to voluntarily pay your taxes, you can also decide for which tax year you are paying them, and by IRS policy, they’ll respect that.

Ruth Benn’s tax resistance takes the form of refusing to pay her income tax, but voluntarily paying her self-employment tax.

As the ten year statute of limitations approached on one of her unpaid years of income tax, the IRS tried to pull a fast one and used some sleight-of-hand to apply the money Benn was paying for the current year’s self-employment tax to the expiring year’s income tax amount.

She is hoping to get the agency to change its mind and to respect its own policy, and promises to keep us up to date on how the red tape tangles.

Counseling Notes.

Including a reminder that Social Security levies can continue past the ten-year statute of limitations date because the levy is considered “continuous” when it is first applied (not reapplied with each new Social Security check).

Democrats are keen to force banks to report how much their customers have put into and taken out of their accounts each year.

They hope this will bring to the surface some of the money in the underground economy that the government has been frustrated when trying to tax.

This proposal has gotten a lot of pushback, and has been an on-again / off-again part of the budget package currently oozing through Congress.

The latest guesswork suggests that the Democrats may reactivate the proposal but restrict it to accounts with $10,000 or more in them.

There’s a nice website that’s been established by the caretakers of The Nelson Homestead — the modest home of war tax resisters Juanita & Wally Nelson in Deerfield, Massachusetts.

It has good recaps of the lives and activism of the Nelsons, including photos.

The Biafra Nations League, which is trying to establish a break-away nation more representative of the Igbo people, has issued an ultimatum to oil firms in the area, ordering them to stop paying taxes to Cameroon and Nigeria, which currently claim sovereignty over the region.

Argentina legalized abortion .

Now a group of Argentine legislators have proposed a law that would permit a sort of conscientious objection to taxpayer-involvement in abortion, of a similar sort to what is proposed in the “Religious Freedom Peace Tax Fund Act” in the U.S.

The human war on traffic ticket robots continues, with robots taken out of service by human rebels in the U.S., Italy, France, and Germany & France in recent weeks.