Tax resistance in the “Peace Churches” →

Quakers →

20th–21st century Quakers →

George Lakey

War tax resistance in the Friends Journal in

By , though there was still no consensus in the Society of Friends about whether paying taxes was the right thing to do (and if not, how best to resist it), the issue had become impossible to avoid.

The issues of the Friends Journal published that year reflect this, with most of them including at least a mention of war tax resistance or of the dilemma for Quaker taxpayers.

War tax resistance was again on the agenda of the Philadelphia Yearly Meeting’s annual conference , but the Journal only includes the topic in a list of “special concerns” that were covered on , without giving any details of how the conversation went.

In the opening article in the issue, “Tithing for Peace” by Alan Strain, the author expresses his anguish over how much he has “tithed for war and instruments of war… several dollars each day to create a warfare state in which fear and violence have become ever more accepted and expected.”

However: “I cannot see how to disentangle myself from this madness… I cannot even see a way to end my involuntary tithing for war.”

Rather than resist the war tithe, he has decided to try to match it with a peace tithe: “giving this amount to private or public agencies working to remove the causes of war and to develop the conditions and institutions of peace.”

In that same issue, a note about the Canadian Friends Service Committee’s humanitarian efforts in Vietnam includes a parenthetical remark that some of the $60,000 donated to the cause came from “two U.S. churchmen who sent money normally used to pay income taxes.”

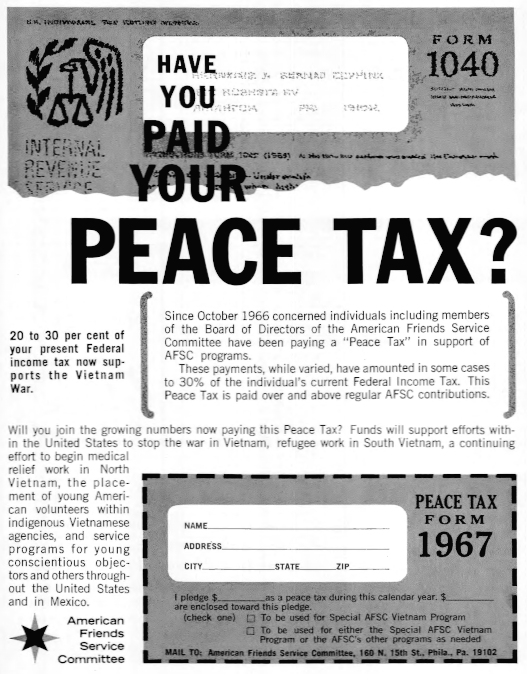

In the issue, the American Friends Service Committee tried to capitalize on the new craze with this ad:

In the Baltimore Yearly Meetings approved a minute “including refusal to pay the surtax for the war if such a tax is imposed.”

An article by Cynthia E. Kerman on “The Rationale of Protest” in the issue made note in passing of the communicative possibilities of war tax resistance: “Tax refusal, for instance, may be a means of speaking to people — not only of purifying our lives.”

In the issue, a letter from Lucy P. Carner picked up where Cynthia E. Kerman left off, asserting that there are “possibilities for witness inherent in tax refusal” that are not immediately obvious to people who are looking for a quick fix “to put a stop to war.”

Excerpts:

Tax refusal enables one to “speak truth to power.”

A letter to the Revenue Service protesting the tax, but paying it, is likely to get less attention than one explaining why one is not paying a portion of the tax.

In the latter case, the Revenue Service has to do something about it.

A representative of the service has to make a telephone call reminding the taxpayer of his delinquency.

Here is another opportunity to witness.

“You mean you do not intend to pay?” said the incredulous voice of the representative.

I explained to him what I had already written to his office.

“Yes, I know that you will eventually get the money from my bank.

That isn’t your fault and you have very courteously fulfilled your duty.

But this is my way of saying that I think the war is wrong.

Only for that reason would I break the law — I’m not accustomed to breaking laws.”

“Yes,” said he, rather helplessly, and hung up.

A few months later a bank official will send a letter saying how much the bank would regret allowing the tax collector to take money from my account and won’t I please pay up and avoid this embarrassment.

Here is another opportunity to write my objection to the war.

Refusal to pay the additional Federal tax on my telephone bill provides similar opportunity to make my voice heard.

Tax refusal, then, is a manner of speaking to government officials, to banks and business concerns.

It is a nonviolent way of reaching the hard-to-reach, for it has nuisance value.

It deserves wide consideration as one way of bearing witness to one’s conscientious objection to war.

The lead editorial in that same issue, by Ruth A. Miner, suggests that instead of resisting war taxes, Quakers should pay an additional tax — “the same amount (or a practicable fraction of it — or even more!)”

— to the United Nations.

This, she suggests, would be in the spirit of Jesus’s suggestion that “whoever compels you to go one mile, go with him two.”

That issue was also the first to feature the ad from “Southern California Business Service” (see ♇ 1 July 2013) that included the message: “A word about tax refusal: Since we limit our income to avoid paying income tax, our rates are low — and — in hiring our help we actively seek out C.O.s and/or tax refusers.”

Phone tax resistance

James B. Osgood, in a letter-to-the-editor in the issue, takes note of the American Friends Service Committee’s “stickers which one can attach to one’s phone bill to make payment of the war tax under protest” (see ♇ 13 July 2013).

This form of protest is better than nothing, but its practical effect is next to nothing.

No real witness is made; no war funds are withheld from the government; no one’s reputation is put on the line.

Those of us who have refused to pay the ten per cent tax hope that others joining us will make a great visible witness and will cause sufficient trouble to the government to give it pause for thought over both collection and prosecution of those who conscientiously refuse.

This, however, will require a real step forward, not a mere licking of a label.

Maris Cakars of the Committee for Nonviolent Action also wrote in, and his letter appeared in the following issue.

He believed that there were “hundreds” of telephone tax resisters who had not notified the Committee of their resistance, and hoped they would speak up so that the campaign could move on to its next phase: “placing advertisement in newspapers and holding press conferences.

For this phase to have maximum impact it is important for us to have as complete a list of tax refusers as possible.”

The issue announced that the Claremont (California) Meeting had decided to resist the telephone tax on its meetinghouse phone.

In the issue was a letter from a representative of 57th Street Meeting in Chicago, in which they noted that two other Meetings had contacted them about actions they had taken in response to their call for phone tax resistance, and said “we would be pleased to act as a clearinghouse on positions taken by Meetings on telephone-tax refusal…”

In the issue, George Lakey wrote an article about why he was joining the crew of the Phoenix to illegally (by U.S. law) bring humanitarian aid to North Vietnam.

He described the escalation of his activism, from letter-writing and congressman-lobbying to his current action.

Along the way, he says, “I stopped paying the telephone tax.”

War tax resistance internationally

The issue noted that Quakers in The Netherlands had formed a “Conscientious Objectors’ Committee Against Paying Taxes for Defense Purposes” which was trying to come up with some sort of government-approved “peace tax”-style plan.

I got a wry smile out of the closing sentence: “In The Netherlands it is not permitted to affix protest stickers on tax forms; instead one must use a written announcement of protest.”

The fourth Friends World Conference was held .

The “Protest and Direct Action group” there “called upon Friends in countries party to the [Vietnam] conflict to ‘go as far as conscience dictates in withholding support from their governments’ war-making machinery,’ first by direct communication with those against whom the protest is made, and then if necessary by public witness and individual action, including the possibility of refusal to pay taxes for war.”

“Corporate Witness and Individual Conscience”

The lead (guest) editorial in the issue was “Corporate Witness and Individual Conscience” by Lindsley H. Noble.

It cautioned Quaker corporate bodies (like Meetings) that were contemplating civil disobedience actions like phone tax resistance.

For one thing, he says, a Quaker group should make sure to have the consent of all of its members before it takes such a drastic step, something he thinks some groups have been careless about.

Secondly, even if every member of the group consents to civil disobedience, the group as a corporation has a different relationship to the state than individuals do.

While individuals and their consciences predate and arguably supersede the state, corporations are creatures of the state and are therefore necessarily subordinate to them.

Quakers incorporate their meetings in part in order to get government privileges associated with legal incorporation.

“In voluntarily putting ourselves under the law to receive these subsidies do we not morally forego corporately the right to refuse to obey other laws not to our liking?”

If Quakers, as a group, find a law so intolerable that they must disobey it as a group, he says, they should first legally detach themselves — “withdraw from our contract with the state and give up our subsidies before setting out on this path.”

This led to months of discussion in the letters-to-the-editor sections of future issues, in particular:

Victor Paschkis thought that Noble’s argument failed on both points.

First, his call for groups to reach consensus before taking a civilly disobedient stand should be understood for what it is — merely a preference for the law-abiding status quo.

After all, “inaction in a given situation may violate the conscience of some members just as action may violate the conscience of others.”

Secondly, a Quaker Meeting, whether or not it has incorporated under the laws of the state, still has a yet higher allegiance to God that must be taken into account.

Also, what’s the point of having Meetings if they do not have “corporate insight” greater than the sum of their parts?

Stephen G. Cary mirrored some of this: “There are times when inaction speaks to the world as clearly as action.

In these situations inaction does not leave us neutral, but committed by default.

Responsibility is not a one-way street, resting only on Friends who wish an action taken.

Those who oppose the action are committing the Meeting, too.

I do not suggest that the proponents’ views should necessarily prevail; I only want it recognized that responsibility to conscience cuts both ways and requires both sides to search their hearts.”

He is also suspect of the idea that corporate entities have no responsibility to disobey unjust laws: “Does the Nuremburg principle have no bearing on the institutions of society?

I prefer to regard the corporation as the creature of those who create and operate it, and the fact that the state charters it does not make the state its ultimate master.”

Marie S. Klooz also defended “corporate witness” as being not exactly “the witness of a corporation” but the collective witness of the corporation’s “component members.”

Such a thing is not only justifiable, but is particularly important to Quakers: “Each member is supposed to test his light by the corporate light.”

And: “If the light requires social action, it is our duty to labor lovingly with those whose light differs, not to refrain from action.”

It is no more necessary for a Meeting to divest itself of its corporate charter to be civilly disobedient, than it is necessary for an individual to first renounce his citizenship.

Pat Foreman found himself uncomfortable with the peace testimony “as interpreted by most Friends” and thinks Quakers like him “sometimes have the feeling that we are being shunned.”

He wants “to remind Friends that Quakerism is a religion and not a prodigious committee.”

Evan Howe thought that dissenters were asking too much if they were asking Quaker Meetings to give up their corporate privileges in order to engage in civilly disobedient actions under the direction of the “sense of the Meeting.”

Such a “surrender of subsidies, as I see it, while apparently a demand of conscience, is rather a surrender of conscience with the ultimate consequence of destroying the society.

I do not believe that dissent gives anyone that right.”

Norman J. Whitney stressed that “Meetings do have a responsibility for corporate witness if the integrity of our testimonies is to be maintained.

It is not enough to shift responsibility to ad hoc committees or special groups among us.”

Roy W. Moger suggested that Noble had hit on a truth when he suggested that legal incorporation was a sort of “trap” that the Religious Society of Friends had fallen into, “thereby placing our conscience in jeopardy.”:

I wonder if the Religious Society of Friends should not begin to unincorporate and remove itself from the trap into which it has fallen, so that Friends can once more seek dependence upon the Holy Spirit, act under guidance of that Spirit as a corporate body, and not have to say, “As a group we dare not take corporate action [and offend the state] because our corporate life depends upon the State, and we are obligated to obey.

The individual can alone take the risk and break the law of the State if he feels the law of the State breaks the law of God.”

Roger S. Lorenz said that because there is a good argument that the Vietnam war is itself illegal, both under international and under domestic law, what it means for a person (or a corporation) to remain within the law under our circumstances is no easy question to answer.

David Hartsough

Over the years, starting in , David Hartsough contributed several pieces to the Friends Journal touching on war tax resistance:

In the issue, he set out a simple, compelling case for war tax resistance — “is it not our responsibility to set the example and refuse to pay our taxes for the weapons and ammunition which inflict this suffering?”

He also suggested that if enough people were to refuse, the government would probably legalize some form of conscientious objection to military taxation.

In the issue, he paraphrased George Fox’s advice to William Penn: “Pay the military portion of thy tax as long as thou canst.”

He suggested that people begin now by resisting the phone tax, and then prepare to resist “the 69.2 percent of our income taxes which go for war” .

In the issue, he told the story of what happened when an IRS agent came to his office to try to collect his unpaid income taxes.

Excerpts:

We talked about the Nürnburg trials, in which the Americans told the Germans that they should obey their consciences rather than their state.

I told him I felt that when we are bombing and burning people and their homes in Vietnam, I cannot condone this action by paying other people to do it.

“I want to make it clear that I have no argument with you on your position about the war,” he said.

“I do not argue that you shouldn’t follow your conscience.

But it is my responsibility to get this money.”

…he gave me a financial statement to fill out.

I refused.

He reminded me: “It’s my job to get this money in any way I can.

I don’t like to do this, but we can take any property you have — your house, your car, or whatever.”

“I have a bicycle downstairs,” I said, “and the suit I’m wearing.”

“No, no, I wouldn’t take your bike or your suit.”

He also expressed concern about the dangers of the poorer neighborhood where I live — a concern beyond his responsibility.

“I guess I’ll have to do what I believe is right,” I said when he was leaving, “and, friend, you will have to do what you believe is right.”

He left without collecting the overdue tax or taking any of my property.

In the issue, he penned another exhortation: “Let us, like Friends through the years, blaze the trail and set the example for others, rather than wait until there are masses of people taking this action.”

He recommended redirecting taxes to the American Friends Service Committee or the Friends Committee on National Legislation, which “will do a much better job of putting our beliefs into action than does the Pentagon.”

David & Jan Hartsough returned to the Journal in with a letter expressing the same basic argument, and giving some details as to how their tax resistance technique had evolved: “Each year we write a check to the Department of Human Services (rather than the IRS) for the 50 percent of our taxes that we do pay.

Along with the check, we send our 1040 form to the IRS and ask them to spend all that money for healing and education, not for killing.

And the other 50 percent (the war portion), we refuse to pay.

Instead, we contribute those funds to organizations helping to feed the hungry, heal the sick, house the homeless, and work for justice and peace in the world.”

War tax resistance in the Friends Journal in

War tax resistance kept charging on through the early

issues of the Friends

Journal, though there was some indication of post-Vietnam War war tax

resister fatigue.

The issue gave an overview of

how various Friends in various places were meeting the war tax challenge:

“Friends in Illinois and Massachusetts, for example, have shared letters

to the

IRS,

to their elected representatives, to newspapers, and to the meetings in

which they have expressed the wrongness of militarism and their

conscientious refusal to support governmental expenditures for military

purposes.”

In Philadelphia, “when the

IRS

seized a car owned by Margaret (Meg) Bownan… [this] was met by many

members of the meeting and other supporters who went with her down to the

garage where the auction was held. A bouquet of bittersweet was placed on

the car’s hood, cranberry juice and cookies were passed out to everyone

(and graciously accepted by the police and the

IRS

representatives), and meeting members formed a special support corporation

and bought the car so that Meg and others may use it in their travels in

and about the city.”

Robert Anthony was fighting a Tax Court battle from Moylan, Pennsylvania,

with First Amendment freedom-of-religion arguments: “compelling the

payment of that part of the income tax that is used for war or war

preparation makes it impossible for a Quaker to practice his

religion.”

Thomas L. Carter of Santa Barbara, California, quoted Peter J. Ediger in a

parable about the Quaker peace testimony:

The devil took the Quakers to a very high mountain, the mountain of

academic-socio-economic success and showed them all the kingdoms of the

world, and the glory of them; and he said to the Quakers all this will I

give you…

financial security

acceptance in your society

many opportunities for doing good

tax exemption for your worship centers and your service programs

many other benefits too numerous to mention

if you will fall down and worship me…

bless the armies which protect your privileges

pay taxes without question for my armies around the world (a few

words of dissent to support your moral image are OK as long as you

refrain from any form of civil disobedience)

And the Quakers said (multiple choice/check one):

we want to keep our service program going, so…

we’re uneasy with your terms, but we like the benefits…

would you serve as one of our Trustees? We need more practical minds

like yours…

as children of God and members of the Religious Society of Friends

we are under obligation to free ourselves from this complicity.

In the issue, the clerk of the

Nashville (Tennessee) Friends Meeting wrote in about that Meeting’s decision

to disregard the legal exemption on local property taxes for church property

and to go ahead and pay the property tax on its meeting house.

The meeting’s decision had, according to Bob Lough, the clerk, four reasons

behind it:

The sense that churches are just as much the beneficiaries of city

government services (like “fire protection, road maintenance, libraries,

schools, social services, parks,

etc.”) as

anyone else.

That “a position in favor of paying taxes form which we are exempt may

enhance our credibility as tax resisters. we decided to continue refusing to pay the excise tax on

the meeting telephone as symbolic of our opposition to a foreign policy

which we cannot support.”

Being in favor of the separation of church and state, the meeting was

opposed to the implicit government subsidy of religious bodies owning

property that the tax exemption represented.

The meeting also felt that the property tax exemption for religious bodies

had encouraged churches to become property owners — erecting “modern day

‘steeplehouses’ which resemble country clubs more than places of Christian

service.”

The piece concluded by encouraging other meetings to consider following their

lead. “As Quakers we are noted for being conscientious about taxes, and

resistance of taxes for war-related purposes has a long history in our

tradition. Perhaps our tax record should not merely reflect our opposition to

the evils we see in society, but also demonstrate that we have a

responsibility that calls for support as well as dissent.”

an ad from the 1 February 1977 issue of Friends Journal

Ross Roby wrote in again (see ♇ 24 July

2013 for his earlier letter) to express his puzzlement about why Quakers

hadn’t gotten all enthusiastic about the World Peace Tax Fund bill. “[T]he

National Council for a

W.P.T.F. is

still operating on a shoe-string and still being warned by sympathetic

Congressmen that there is little apparent concern about the bill if they can

judge by their mail.”

Has Friends Journal any interest in developments in

the W.P.T.F.

bill…? There have been frequent opportunities in the last year for the

Journal to support and encourage lobbyists for the

W.P.T.F.,

and the chance was again present in the article of

on “Friends and the

IRS.”

For some inexplicable reason, the Journal has again

missed an opportunity to remind us that the tax laws can be changed by

legislative action — that the

W.P.T.F.

bill is a reasonable way to put conscientious objection as an alternative in

every citizen’s form 1040!

Again, Roby seemed blind to the real concerns that Quakers and other

conscientious war tax resisters might have with the plan advocated by the

“peace tax fund” advocates.

In the issue, George Lakey shared

his annual letter to the

IRS,

accompanying the letter with a telling comment: “I thought you might like to

print part or all of it to remind your readers that some of us Quaker tax

refusers are still doing it!” Although from my perspective, the

coverage of Quaker war tax resistance in the

Journal seems to be going strong, it seems that from

the perspective of this particular Quaker tax resister the practice had begun

to wane in the post-Vietnam War period. Excerpts:

Again I am asked to pay taxes to support an approach which reduces my actual

security as a human being… for paying taxes to this government means giving a

license for various kinds of international misadventures.

I see no reason, therefore, to change my own policy of refusing federal income

taxes. I very much support the principle of taxation, and encourage the

government to tax at a much higher rate the corporations whose interests it so

faithfully serves. Since it does not serve my interests nearly so well, I

withhold my hard-earned money until I see a basic change in values. I want to

see the government focused on human security, not “national”

security. I want to see the government make a serious commitment to

environmental quality. I want to see in all its policies the government taking

the side of life, not death.

To implement my tax refusal policy, I return the form only partially filled

out, lacking the financial information which would enable you to collect the

tax.

Virginia Snow Mountain and Darrell Bluhm shared their letter to the

IRS in

the same issue. Excerpts:

We have given ourselves a War Crimes Tax Credit for the amount your charts

would otherwise have had us owe and we request that you refund us the money

withheld from our incomes last year.

…Through our involvement with the Religious Society of Friends and our

personal experience of the Divine Spirit we have come to know that all life

is sacred. We are called to live in such a way as to “remove the cause of

war.”

…[O]ur vocations involve the nurture and education of children. Daily we work

to help guide young people to grow up to be peaceful, responsible adults.

They are our joy and our hope for the future. It is unthinkable to us that

any part of the wages that we earn in this work should be used to support

weapons systems or armies whose effect is to injure and kill people, or to

add to the great potential for nuclear holocaust that already exists with our

huge stockpiles of weapons. Knowing that more than half our tax dollar goes

to the death and destruction the American military represents has caused us

to conclude that we will no longer pay our Federal taxes. We cannot support

the military’s protection of corporate profit at the expense of human needs.

That issue also reprinted the text of a “petition” written by R.L. Anthony

(and invited others to sign or use it):

Members of the Religious Society of Friends (Quakers) since the Society’s

beginning have been guided by a belief in the sacredness of life and have

implemented this by seeking ways of peace. This compels in conscience their

refusal to participate in war.

I believe the U.S.

tax laws deny us the constitutional right to religious freedom by

not providing under law an alternative to paying that portion of the income

tax devoted to war preparation.

If I should at present follow my conscience and my religious beliefs by

refusing taxes for war, I would have to face the prospect of forced

collection or legal prosecution and penalties. I believe the

U.S. tax laws

thereby deny me the free exercise of my religious beliefs.

In keeping with my beliefs and conscience, I wish to pay the war portion of

my income tax to a peace fund, such as the World Peace Tax Fund

presently in a committee of Congress, set up as a legal alternative under

U.S. law. I would

make this alternative payment instead of the war portion of my income tax if

the U.S. tax laws

provided such an alternative for all citizens conscientiously opposed to war

and the taking of life.

I wish my position made known to all branches of government concerned,

including the U.S.

Congress, the courts and the

IRS.

In the issue, Allyn Eccleston

compared the reemerging Quaker opposition to paying for war to the emergence

of Quaker abolitionism in American in the

.

Excerpts:

Today we have a different impediment in our relationship with God and we are

called, each one of us, to hold it to the light and test whether we feel at

ease. Our continued commitment to a world-wide arms race not only deprives

the world of comparable expenditures for human service, it enslaves the world

in a struggle for real and symbolic power that engenders hatred, fear and

greed. We are the masters in an arms race that enslaves the people

of this earth.

Do I feel at ease knowing that approximately fifty cents of each of my tax

dollars goes to military expenditures?

Do I feel at ease knowing the United States spends more money on armaments

than any country in the world?

Do I feel at ease knowing United States arms merchants have been peddling

ever more sophisticated weaponry to other nations, totalitarian and

democratic, undeveloped and developed, poor and rich; that in Greece, Turkey,

the Near East, and Latin America we have armed both sides of existing (or

potential) conflicts, as well as equipped and trained some of the most

repressive governments in existence?

Our country’s dependence on military manpower has been reduced even to the

point where conscription is no longer necessary. During the Vietnam conflict

it became the explicit policy of the United States to substitute wealth and

technology for manpower. This policy is directly responsible for more

indiscriminate killing and destructiveness (in ways contrary even to the

international conventions of warfare). We annihilated women, children, old

people and, in designated areas, all living things, and we did this by remote

control, thereby removing and insulating the killers from the acts.

Regardless of who actually handled the equipment, it is you and I and every

other taxpayer who paid for the weapons and are therefore responsible.

It is not as though a madman picks up our sledgehammer or another useful tool

and hits someone over the head with it. When soldiers, hired by us, use our

weapons to kill, it is not misuse-that is what the equipment is designed and

purchased for. And we must presume any future use will be as destructive (at

least) as what we witnessed in Vietnam.

It isn’t necessary to document for Friends why the preparation for conflict

is more likely to lead to war than to peace or how the evils of hatred, greed

and fear can be addressed by practical demonstrations of love, self-sacrifice

and self-confidence. Let us search for steps we might take that would set us

on a new course.

There are approximately 150,000 Friends in the United States. What would

happen if 30,000 Friends felt moved to take some step, however small, to

register their “dis-ease” in a meaningful way?

Suppose you are one of these Friends moved to register public dissent and

dismay by enclosing a personal statement with your tax return. If you owe the

government money, the letter would specify that at least a token amount has

been withheld as a testimony for peace. To be more effective, you would also

send copies of the statement to your senators, to your congressperson and to

your newspaper.

In addition to increasing the effect of your witness, this public declaration

protects you against accusation of intent to defraud the government.

Withholding some portion of your tax does subject you to the seven percent

interest charge plus a possible monthly penalty of one-half of one percent

per month up to twenty-five percent of the amount not paid. Therefore, it is

you who must determine the appropriate amount to withhold for your witness.

Some Friends might feel they should begin with one percent of their total

tax; others might be led to withhold ten percent or the actual percentage of

the budget allocated to military expenses.

If you are moved to witness this year but cannot withhold from the government

(because your money was already collected), you might consider requesting a

refund (form 843) of the amount you would have withheld. Whether you receive

a refund or not, the witness will have been strengthened. In the current tax

year, you can legally assure that you will owe some money to the government

by declaring expected allowances on your W-4 form at a level that takes your

peace witness into account.

If the burden of the witness gets too heavy, you can, and should, stop the

process by making the payment or by allowing the

IRS to

find and take payment from your bank account. (Beyond late-payment penalties,

the IRS

cannot take punitive action once you have paid the assessed tax.) The witness

already made to yourself and your friends, and the strength and truth gained

by this witness, will have moved us that much closer to world peace. We will

have another opportunity to witness next year, and the next and the next.

Each year we will have more knowledge and more strength and, if we are

mindful of the light, more love. And this will sustain us for as many

generations as it may take.

Some Friends will argue that since the government gets the money plus penalty

charges anyway, tax refusal is counterproductive. This is not so. The whole

system of tax collection is computerized and is dependent on voluntary

cooperation. By requiring the system to take special steps to collect your

tax, your message is felt. The message gains weight as the

IRS is

forced to put more and more time and attention on this matter. Friends may

feel easier about the extra money collected if they view it as a contribution

toward the government’s higher administrative costs. (There is no way the

additional money can be diverted into military expense.)

It will concern some Friends that this action is “against the law” or it

isn’t proper to claim a deduction for “peacework” if the money isn’t actually

spent or that there is no item under “Credits” where one could appropriately

list “peace witness.” True enough, the way of the tax refuser is not clean

and simple. We are confronting a system we believe to be immoral and, as

Friends have always done in similar situations, we must compromise, following

the path we believe moves us closer to the ideal.

This is why a tax refuser needs the insight, information and support of other

(Friendly) resisters. We need to discuss the pros and cons of the

alternatives open to us and to help each other in our witness.

IRS

regulations and procedures change. Individual circumstances change. If one is

isolated it can be confusing and lonely. It is important to stay in touch

with others, by mail, if necessary.

Regardless of the impact on the government, our witness will have an

immediate impact on each of us and on our meetings. This impact is likely to

differ from that which we may have experienced in visiting prisons,

counseling conscientious objectors, sorting clothes for AFSC,

or work in other worthwhile programs in which we minister and offer aid to

others. In tax refusal, we are concerned with our own brokenness and are

committed to a healing ministry of ourselves, not by words, but by deeds.

In addition to the most important witness of tax refusal, every Friend should

consider actively supporting the World Peace Tax Fund. If passed, this bill

would grant conscientious objector status to taxpayers in much the same way

as a conscientious objector status was granted to draft resisters and would

allow the military expense portion of a conscientious objector’s tax to be

diverted to a World Peace Trust Fund (for peace education and research, and

humanitarian use).

Those of us who are clear on this issue must act and we must support each

other. We must make our testimony public that others may find clarity and

courage. And when we are given the opportunity, we must lovingly and

patiently labor with other Friends who have not yet been moved to hold this

issue to the light.

The IRS

readily admits the whole tax system is dependent on voluntary cooperation.

Ultimate control is in our hands (not the Pentagon’s)! Whether we want to

acknowledge it or not, we are the masters, the slave masters. We can learn

from the early Quakers. We must seek truth in the light and speak truth to

power.

Finally, the issue gave the

unsurprising news that the “Ann Arbor Monthly Meeting was recently denied a

claim for exemption from payment of war taxes,” which it had asserted on

religious freedom grounds. Cleverly, at least from a propaganda point of

view, “[t]hey supported their claim by citing the

Buckley vs. Valeo

case where the Supreme Court decided it was unconstitutional to limit how much

money of his own a candidate can spend for his campaign, thus establishing

money expenditures as a means of free expression.”

War tax resistance in the Friends Journal in

There was a resurgence of war tax resistance news in the

Friends Journal in ,

including an interesting series of articles on the voluntary simplicity / low

income lifestyle as a tax resistance tactic, and the beginning chapters of

the tale of Quaker war tax resister Priscilla Adams.

A note in the issue plugged the

“Conscience and Military Tax Campaign Escrow Account”:

Established in by the Nonviolent Action

Community of Cascadia, the account allows war tax resisters to set aside

refused military taxes in a secure fund. Deposits may be retrieved at any

time (to replace assets seized by the

IRS,

for example), and interest from the account is used to promote war tax

resistance and support peace and social justice activism. Depositors’ funds

are reinvested in socially responsible institutions assisting low-income

communities and minorities. The CMTC Escrow Account is the largest and most

geographically diverse war tax redirection fund in the United States.

War tax resistance is an act of civil disobedience, and resisters potentially

face fines, levies, and seizure of assets. However, the escrow account itself

is a trust fund, and as such is confidential and entirely legal. Depositor

records are not available to the

IRS,

and individual deposits are considered to be anonymous portions of a larger

fund invested in fully insured institutions. Participants receive records of

their transactions, annual statements, and a free subscription to

NACC’s quarterly war tax resistance magazine.

(I wouldn’t rely on any of that as solid legal advice. My understanding is

that the

IRS

sometimes treats “warehouse banks” like these as illegal operations that they

can seize wholesale under the theory that they’re being operated for money

laundering or tax evasion purposes.)

In a letter in the issue, William Kriebel

called out Quakers on their careless or politically-correct use of of language;

in particular he claimed: “There are no ‘war taxes.’ All income tax money goes

into the treasury without earmarking for the military. Taxation is a legitimate

power of any government. Our points of protest really are the decisions

(budget-making, appropriation) to use money out of the common fund for military

purposes.”

An article on the Quaker Council for European Affairs in the same issue noted

in passing that “conscientious objection to war taxes” was one of the “studies

for publication” that the organization had produced. Another article in that

issue noted that the National Association of Evangelicals had endorsed the

Peace Tax Fund bill:

“At first this was just a lonely struggle for the peace churches,” said

Marian Franz, director of the campaign, “then we got the support of the

mainline churches, which represent over 12 million people. Now we have

support from more conservative religious organizations, who, until recently,

had seemed to be unlikely allies.” Marian attributes the recently attained,

broad base of support to a change in tactics from an issue of conscientious

objection to an issue of religious liberties. Marian explained that “having

this broad base of support means that members of Congress, even conservative

members, take the issue more seriously.”

On , there was a benefit premiere

showing of An Act of Conscience, a documentary on

the Kehler/Corner house seizure and subsequent occupation. There was some

tangential Quaker involvement in the benefit (it was sponsored by several

organizations, including a regional AFSC office, and some Massachusetts

Quakers took part in the occupation), and the benefit screening was covered

in a note in the issue.

In the lead editorial in the issue,

editor Vinton Deming paid tribute to Eleanor Webb:

Eleanor Webb, who died , was clerk

of the Journal board when I was appointed

editor-manager in .… It was Eleanor… who

stood firmly in support of staff who resisted paying the military portion of

their federal taxes.

One of the feature articles in the issue

was written by David R. Bassett and told his story as “The Founder of the

Peace Tax Fund Movement.” Excerpts:

marks the 25th year since the

introduction of the Peace Tax Fund Bill in the

U.S. Congress. I

have been involved in the initiation of this legislation, a laborer in the

centuries-long effort to establish on earth the type of peaceful world

envisioned by Jesus and George Fox. I firmly believe that, on some

significant day in the future, some nation will for the first time pass a

Peace Tax Fund Bill, thereby establishing legal recognition of the right of

conscientious objection to the payment of military taxes. Once this is

accomplished, other nations will follow suit. I consider this goal as one of

the crucial and route-determining “trail-signs” on the path to that time and

place where the world will realize that ahimsa (soulforce)

is the preferred way to resolve conflict and to govern communities, and where

conscientious objection to war and other forms of violence will be considered

the norm.

[My] orientation as a conscientious objector to war and of preventing

preventable suffering impelled Miyoko and me, beginning in

, to wrestle with the fact

that each year we were paying (through our federal taxes) to support the

Viemam War and the military system generally. In fact, some 50 percent of

those tax moneys went to support

U.S. military

systems! One of my most graphic memories of that time was, while working many

nights at Queens Hospital in Honolulu, hearing

U.S. Air Force jet

tankers, fully laden with jet fuel, flying over the heavily populated part of

Honolulu on their way to Indochina.

Conscientious objection to payment of military taxes

In , with the Vietnam War continuing, we

moved to Ann Arbor to work at the University of Michigan. We became members

of the Ann Arbor Meeting and found there a number of people who were actively

grappling with the issue of whether to continue to pay the military portion

of federal taxes for a war that we opposed. I came to realize that any

nation’s military programs are made possible the, monetary resources that, in

the analysis, are extracted from the nation’s citizens by taxation. It also

became clear to me that one who was conscientiously opposed to military

systems must not allow his or her funds to be used for this purpose.

Surveying the pervasive role of our military system not only in our foreign

policies, but in its effects on our economy, our environment, and on the

nation’s culture and spirit, I carne to feel that this issue was central to

our times. Conscientious objection to payment of military taxes is as

important to be established as was the ending of slavery and of apartheid and

the establishment of women’s right to vote. At the same time, I held then,

and still hold, the view that the federal government is capable of carrying

out many beneficial and constructive programs and that I am willing, indeed

obligated, to pay my full share of taxes to support those programs.

I came to know that it would not be enough simply to focus on reductions in

military spending by influencing legislators and electing new ones (though

this was obviously necessary). The challenge was to extend the right of

conscientious objection to war to include not only one’s physical body, but

also one’s economic resources. I knew further that there had been repeated

resistance in the

U.S. courts to

such change and concluded that, while civil disobedience in this area

(i.e., war tax resistance) would continue to be essential, the

principal focus of attention should be to change the tax laws.

During the year , there was for me

a struggle with my conscience, not in regard to what I believe on this issue

but whether to take some action and what that action should be. Should I live

below a taxable income level? move to Canada? engage in war tax resistance?

take our civil disobedience actions into the judicial system? or attempt to

change the federal tax laws? Miyoko and I knew that to embark on any of these

actions would require great amounts of time and energy; that each course

would require some changes and risks, not all of which we could anticipate at

the outset; and that none were assured of “success.” I knew that to commit

the time necessary to move this issue forward might conflict with my hopes of

making progress in academic medicine and in research into the causes of

atherosclerosis. We gradually came to the view that it seemed wisest to try

to resist paying the military portion of our taxes and to begin to

take steps to bring about legislative change.

It was the quiet voice of conscience that kept nagging me almost every day, as

I found one or another reason not to take some action. Finally, in the

, I phoned Professor

Joseph Sax at the University of Michigan Law School and outlined to him the

basic idea: the need to change the federal tax laws so as to have Congress

grant legal recognition to the right of conscientious objection to

the payment of military taxes, while enabling the taxpayer to pay the full

amount of his or her tax with assurance that those tax monies would

not be used for military expenditures. Professor Sax sketched out how this

might be accomplished. Over a period of eight to nine months, with the

assistance of Michael Hall, we began the process of drafting what became the

World Peace Tax Fund Bill.

Other Ann Arbor Friends, Joe and Fran Eliot and Bob and Margaret Blood, had

been considering drafting a bill. A brief written for them by Thomas Towe (a

Quaker law student) proved a helpful resource. It was not hard to draw

together a working committee of seven or eight people during

to work on

this legislation and to take the initial steps in deciding how to bring the

bill to Congress, how to publicize it, and how to raise funds. We were

encouraged when Ann Arbor’s Interfaith Council for Peace decided to support

the legislative effort and appointed two very effective members to meet with

us on a regular basis.

The World Peace Tax Fund Bill was first introduced in the

U.S. Congress on

, with Representative Ronald

V. Dellums as the lead sponsor, with nine other cosponsors. The Peace Tax

Fund office moved from Ann Arbor to the Florida Avenue Meetinghouse in

Washington,

D.C., in

. The bill was first introduced in

the Senate in , with Senator Mark Hatfield

as its sponsor. In the bill was renamed the

U.S. Peace Tax

Fund Bill. A dedicated staff, led for the past 14 years by Marian Franz, has

coordinated the lobbying effort. The orientation and the gifts that she

brings to her work are evident in her book, Questions That Refuse To Go Away.

A sidebar noted resources available from the National Campaign for a Peace Tax Fund, and also made note of the international conferences at which similar plans proposed in other countries are discussed.

The same issue also contains Clare Hanrahan’s article “Wholesome Poverty: A Revolutionary Adventure.”

Unfortunately, in the archived PDF, some of the opening paragraph is obscured by an insert card.

The article appears to begin with Hanrahan saying that she initially adopted a lower-income simple-living lifestyle in order to resist war taxes, but then came to believe that frugality and thrift and anti-consumerism and simplicity had a larger role to play in the pursuit of “a just and sustainable global community.”

It continues:

When I must work for wages, I do so as an independent contractor so that I can maintain control over tax withholdings.

I redirect a fair percentage of cash wages and many hours of volunteer time to support life-affirming projects at home and abroad.

Self-employment suits my temperament and has enabled me to develop skills and to pursue interests I may never have had the time for in a conventional career.

I’ve tried to be resilient and open to any honest labor.

If I’m asked what I do for a living, each day I can provide a different answer.

One day I might be gathering and saving seeds for next year’s garden or harvesting wild herbs for a winter tea; another day might be spent in household repair, community organizing, or researching and writing a grant for a nonprofit organization.

I’ve learned the wisdom in giving due time each day to labor of the mind and of the body and to quiet reflection that feeds the spirit.

I value my free time and open schedule far more than any accumulation of cash or property, security, or prestige.

The freedom to choose how I will be with each moment is a gift and a challenge that I count as my greatest wealth.

Living on the edge, more or less, over the years I have honed the skills and nurtured an attitude of wholesome poverty.

Meeting basic needs without a substantial cash flow has been least stressful when I’ve lived within a stable community where interdependence and cooperative values are practiced.

But during my nomadic years I learned to trust in the kindness of strangers and the serendipity of life.

I came to value the gifts of the pilgrim spirit and to recognize the importance of the itinerant wayfarer in the lives of the comfortably settled.

I’ve lived and traveled aboard small sail boats, in a tipi, in rural cabins, and in derelict inner-city housing, trading cleanup and repair for rent.

I’ve made do in the back of an old school bus and afloat on a homemade houseboat on a Mississippi backwater.

I’ve worked in a cooperative shelter for displaced women and children, with room and board as compensation, and I’ve battered for home and garden space by exchanging pet and plant care.

My primary transportation is the slow way.

As a pedestrian, a bicyclist, and a bus rider, I keep a less frantic pace, and the more personal contact with those I encounter enriches the journey.

I can borrow a car or catch a lift from a friend if necessary, and by paying my fair share of the cost, the cooperative way serves each of us.

Nutritious food is available in surprising abundance if one is willing to look to unconventional channels:

I’ve participated in grassroots distribution networks of urban gleanings, intercepting the produce, grains, and other surplus foods otherwise lost.

Best of all, I’ve learned to grow my own food in community gardens and backyard plots whenever I had the opportunity.

As a worker-member at the local coop I claimed a significant reduction on food purchases, and by eliminating meat from my diet, the cost of my sustenance is affordable and sustainable.

Insurance against old age, disability, accident, or disease has never been an affordable option, nor one in which I place my faith.

Catastrophic illness or accident or the incapacities of age could happen to anyone.

Yet time and again, I’ve been sustained through economic precarity with help that comes at just the right moment.

This has happened so often that I live with a trust that keeps fear at bay.

I have learned to lean into the present moment, focused on the work before me, while keeping a well-honed sense of the adventure of it all and a very real faith in the unfolding process.

The inherent goodness of the universe has been made visible through the most unlikely of allies, and the travelers I’ve met along the way have been the wisest of teachers.

Peace Pilgrim, writing in her pamphlet, Steps Toward Inner Peace, recalled a visit to a city that had been her home:

In the poorer sections I am tolerated.

In the wealthier sections some glances seem a bit startled, and some are disdainful.

On both sides of us as we walk are displayed the things that we can buy if we are willing to stay in the orderly lines, day after day, year after year…

Thousands of things are displayed — and yet the most valuable things are missing.

Freedom is not displayed, nor health, nor happiness, nor peace of mind.

To obtain these, my friends, you too may need to escape from the orderly lines and risk being looked upon disdainfully.

Stepping outside the tyranny of “orderly lines” and daring to risk the uncertainties of disaffiliation can make of our very lives a revolution.

The way to the just and sustainable global community that we seek will open before us as we walk.

Another article in the same issue took the “voluntary simplicity” idea and ran with it.

Starting with Jesus’s one-sentence summary of his teachings — love your neighbor as much as you love yourself — the authors took this to mean “taking our fair share of global resources and no more.”

This starts with refusing war taxes because militarism is directly destructive of “our global neighbors.”

But that’s just step one of a six-step process.

Step two would be to imagine the world’s resources shared equally, which, the authors assert, means “an annual ‘fair share’ of just over $3,000 per person.”

But because the world is not using its resources in an environmentally sustainable way, step #3 is to reduce this fair share some more, to a more sustainable level: $1,800 per person per year.

But since that much money would go further in a place like the United States, where it’s relatively easier to live off the cast-offs of the wealthy, level #4 “challenges us to live on even less than level three, since we have an easier time doing so in a society with a relatively affluent public infrastructure.”

We’re not done yet.

Level #5 considers the non-monetary wealth most Americans enjoy because of the relatively high levels of medical care and education they have had access to.

“With such advantages (and others), we ought to be able to live on less resources than folks who lack education and have chronic medical problems.”

Finally, level #6 is for those who are not hampered by disabilities, encouraging them to sacrifice yet more so as to leave more for those who have to struggle harder.

Challenging? Certainly.

Even the authors only seem to have made it half way to step #2, limiting their income as a couple to $12,000 a year.

Some other choices they made were to “keep the majority of our savings in the form of non-interest-bearing loans” so as to avoid the sin of usury, and to “give away each year an amount equal to what we spend on ourselves.”

(A letter-to-the-editor in the issue criticized this radical simplicity, saying it smacked of “intelligent, able-bodied adults who consciously decide to let others subsidize” the benefits of society.

In particular: “In reducing their income to avoid paying taxes to support the military, this couple also avoids paying taxes that support the other half of the federal budget.

So, there goes their support for many of the roads they use, for medical research they might avail themselves of through that subsidized doctor, for other federally supported scientific and social research, for national parks, and so forth.

The authors are obviously well educated.

Their education was probably supported by local, state, and federal subsidies.

One wonders if they are repaying society for the educational benefit they’ve received.”)

Another brief note in the issue reported on the results of a “penny poll” that had been “conducted by Christian Peacemaker Teams in Elkhart, Ind.” and had indicated that those polled implicitly supported huge reductions in military spending.

A letter-to-the-editor from Marjorie Schier and Suzanne Day of the “Philadelphia Yearly Meeting War Tax Concerns Support Committee” published in the issue summarized the war tax issue as they saw it:

Resisting taxes

When a draft call finds some conscientious objectors unable to participate in war, the government not only has provided them alternatives, but also has proceeded to draft others who will participate.

It is individual conscience that makes the difference, not how the government allocates the recruits.

Some Friends have been unable to enlist, and some cannot voluntarily send dollars in federal tax for military uses.

Interacting with the federal government through tax resistance as witness for peace is more than symbolic; it can be earnest, meaningful religious conscience in action.

However, it does not change how the government allocates its resources, and efforts to witness for changed priorities are also significant.

Many Friends and others work for passage of the Peace Tax Fund Bill by the U.S. Congress because it would not only provide a legal opportunity for pacifists to pay their full federal tax without supporting war, but also give the government an indication of the numbers of citizens exercising this option.

Yes, the federal tax on telephone service is refused by many pacifists (with

a note of explanation accompanying the refusal and redirection of the money

for constructive purposes) because that tax was specifically reinstated to

support the war in Vietnam. Federal bookkeeping does not distinguish certain

tax streams for specific purposes, and has not since John Woolman wrestled

with this same issue. Nevertheless, many Friends are prompted to take a stand

for peace via taxes and thereby find a forum for disclosing that witness with

meetings, governmental representatives, families, and neighbors.

An obituary notice for Abram Bresel Goldstein in that same issue noted that

“[t]hough he worked briefly for the Internal Revenue Service, Abram left that

position during the Korean War to avoid aiding the collection of taxes for

war.”

On , NWTRCC and

the War Tax Concerns Support Committee of Philadelphia Yearly Meeting sponsored

a seminar on “Corporate Conscience and War Taxes” at the Moorestown, New

Jersey, Meeting (according to a calendar listing in the

issue).

Priscilla Adams

The war tax resistance of Quaker Priscilla Adams became a cause célèbre that

played out over in the

Friends Journal starting in

. I’ll break with my chronological examination of the Journal for a while to follow this thread.

The issue introduces Adams and her

legal case:

Priscilla Adams, a war tax resister and member of Haddonfield

(N.J.) Meeting, is

challenging the

IRS

in court under the Religious Freedom Restoration Act (RFRA). Her case is the

first of its kind to test conscientious war tax resistance since the passage

of the RFRA in . Priscilla and her lawyer,

Peter Goldberger, will challenge two points covered by the act: the

government’s use of penalties against war tax resisters for their stands of

conscience; and the lack of a government accommodation for conscientious

objectors to paying for war (like a Peace Tax Fund). The RFRA states that in

conflicts between the government and religious freedom, the government must

show compelling state interest and then use the least restrictive means

necessary. In this case, Priscilla is challenging the government’s lack of

recognition of conscience in response to the

IRS

assessing her taxes and penalties. She and Peter are arguing that under RFRA,

the IRS

should waive penalties for religious war tax resisters as long as they

recognize other forms of reasonable cause for noncompliance with the tax law.

They also are stating that the RFRA requires the enactment of something like a

peace tax fund for religious war tax resisters who are willing to accept a

reasonable accommodation, such as earmarking tax monies for non-warlike

purposes in the federal government. The case has completed its earliest

procedural stages and will be heard in United States Tax Court. Though no

date has been set, lawyers expect a trial date

. Priscilla has participated in

several clearness committees and is receiving guidance and support from

Haddonfield Meeting, the National War Tax Resistance Coordinating Committee,

Philadelphia Yearly Meeting’s War Tax Concerns Support Committee, the

National Campaign for a Peace Tax Fund, and family and friends.

The issue gave an update:

Priscilla Adams… will appeal the court’s decision rejecting her right to

refuse to pay taxes. The case went before the Philadelphia Tax Court, where

Adams presented an extensive outline of Quaker history and beliefs related to

war tax objections. The court’s decision states, “Religious Freedom

Restoration Act of does not exempt Quaker

from federal income taxes, despite taxpayer’s religious opposition to

military expenditures.” , Rosa Packard of Purchase

(N.Y.) Meeting and

Gordon and Edith Browne of Plainfield

(Vt.) Meeting also have filed

complaints in federal district courts seeking to protect their conscientious

acts of war tax refusal.

The issue mentioned her appeal:

Tax resister Priscilla Lippincott Adams… faced the Federal Court of Appeals

on . Her case against the

IRS for

penalizing her for her religious objections to paying the military through

taxes was dismissed in … The court

had the choice of hearing oral arguments or making a decision based on the

written briefs. In a positive turn, the judges heard oral arguments. Adams

said her lawyer, Peter Goldberger, passionately presented her case, “just

like a lawyer on T.V.”

The three judges will now make a decision, a process that could take anywhere

from six weeks to six months.

From there, to the Supreme Court, according to a

press release that formed the

basis for a

Journal news brief:

Philadelphia Yearly Meeting has filed a friend-of-the-court brief with the

U.S. Supreme Court

in support of its member, Priscilla Adams… who petitioned the high court in

, following unsuccessful efforts

in lower courts to obtain government accommodation for her conscientious

objection to paying war taxes by allowing her to pay federal taxes without

paying for military expenditures. Her employer, Philadelphia Yearly Meeting,

supports religious witness by not forwarding the military portion of a

conscientious objector’s taxes to the

IRS. A

Peace Tax Fund, where tax dollars of conscientious objectors would be directed

exclusively to nonmilitary programs, is one possible solution to the dilemma

for adherents to nonviolence; a bill to establish a Peace Tax Fund has been

introduced in every Congress .

…Lower courts addressed the issue of accommodating war tax resistance only by

declaring that the government has a compelling interest in collecting taxes;

the courts have not dealt with the arguments that accommodation of

conscientious objection would be possible within the context of mandatory

participation in taxation. The Supreme Court has not heard any case that

raises these religious liberty questions under the

law.

By then it was too late, though. The issue noted that Adams’s Supreme Court appeal had been turned down:

On , the

U.S. Supreme Court

declined to hear appeals by Gordon and Edith Browne and Priscilla Lippincott

Adams to lower-court rulings that allowed the Internal Revenue Service to

impose late fees and interest for their conscientious refusal to pay the

military portion of their federal tax. The issue in this case was not paying

the tax when forced to do so by the

IRS,

but whether a “religious hardship” existed that should enable them to pay

without any penalties and interest. The lower-court rulings reaffirmed a

statement of the Supreme Court in that “The

tax system could not function if denominations were allowed to challenge [it]

because tax payments were spent in a manner that violates their religious

belief.” The Justice Department lawyers said that “Voluntary compliance with

the tax laws is the least restrictive means of furthering the government’s

compelling interest in collecting taxes.”… “We’re very disappointed that the

Supreme Court will not be taking the opportunity to reinforce religious

freedom and freedom of conscience,” said Marian Franz, executive director of

the National Campaign for a Peace Tax Fund. “Congress seems like the most

appropriate place where this human right can be protected.”

Adams wasn’t going to give up though. Whether or not the government was going

to deign to make her war tax resistance legal, she was going to resist, and

the Philadelphia Yearly Meeting was willing to help her. From the

issue:

The United States Department of Justice, Tax Division, is suing Philadelphia

Yearly Meeting for refusing to forward wages of an employee to the Internal

Revenue Service. The employee, Priscilla Adams, resists paying taxes for war

and the military on the basis of religious conscience. The lawsuit, filed in

, is a move to attain funds from

PYM

as recompense for taxes owed by Priscilla Adams, plus a 50-percent penalty

for not garnishing her wages as instructed by the

IRS in

. If the

IRS

succeeds,

PYM

would owe approximately $60,000.

On ,

PYM’s

Interim Meeting decided to respond to the lawsuit and defend its position in

court.

PYM

stated that to garnish Priscilla Adams’s wages would infringe upon her

religious beliefs, and

PYM

should not “be required to act as a collection agent for the government when

doing so will require it to violate key tenets of the Quaker faith.”

Thomas Jeavons,

PYM

general secretary, commented in the Philadelphia Inquirer, “About 50 percent

of our taxes pay for weapons and warfare… We have long sought the creation of

a Peace Tax Fund, a government fund for nonmilitary use, where taxes of

[those who regard paying for war as a violation of religious conscience]

could go. Legislation for this has been in Congress for many years. It should

be passed now.”

The issue spelled out the

Meeting’s legal argument:

On , Philadelphia Yearly

Meeting filed its answer to a Justice Department lawsuit that asks a $20,000

penalty to be imposed on them and seeks to make them the collection agent for

the government. The yearly meeting’s response makes dear its intention to

stand by its essential religious principles, and publicly defend the free

exercise of religion on all possible grounds, including constitutional and

statutory religious freedom defenses. The

IRS

contends that

PYM

must garnish the salary of one of its employees and members who refuses — in

keeping with longstanding Quaker convictions — to pay taxes that support war

and preparations for war. While the

IRS

could easily take other courses to collect the back taxes it claims are due,

instead the federal government is trying to force a church to collect these

funds for it, an action that would require this Quaker organization to

violate its own essential religious convictions regarding freedom of

conscience.

PYM

has refused to do so. The answer to the suit says that the government “asks

the court to assist it in violating the most fundamental religious principles

of an established church… Although those principles and the yearly meeting’s

reasons for its actions have been painstakingly explained to the [government]…

the complaint purports to set forth the history of this matter without even

mentioning

PYM’s

efforts at communication and conciliation. Further, the complaint labels the

Yearly Meeting’s religiously mandated actions as a ‘failure’ to submit to

government coercion, and brands the [Quaker] theological scruples as

‘unreasonable’ and deserving of harsh penalties.” The news release from

PYM

adds, “Quakers have long been known for their religious pacifism, opposition

to war, and support of religious freedom and freedom of conscience.

PYM

regrets that being true to its faith has now brought us into conflict with

the government. The Quaker organization sees itself as defending freedom of

religion and freedom of conscience — and not just for itself, but for all

those who desire to be both good citizens and people of faith. While

PYM

regrets the need to resort to legal action, it looks forward to a full airing

of the issues involved in a public forum where both the sound reasons and

religious principles that guide this Quaker organization’s actions may be

upheld.

PYM’s

defense will rest on the constitutional right to freedom of religion

generally, and particularly as upheld and restated in the Religious Freedom

Restoration Act of .”

The issue reported on how far

they’d gotten with that argument:

On , A federal judge ruled that

Philadelphia Yearly Meeting must comply with a levy on the wages of war tax

refuser Priscilla Adams, but rejected a 50 percent penalty desired by the

Internal Revenue Service.

U.S. District

Judge Stewart Dalzell agreed with the Quaker argument that complying with the

levy “substantially burdens its exercise of religion,” because, as

PYM

General Secretary Thomas Jeavons earlier testified, the organization

“considers it a sacred duty to support the conscientious actions of its

individual members, especially in such historic witnesses as the Peace

Testimony.” Judge Stewan Dalzell also agreed that the

PYM

defense “raised novel and important questions,” thus demonstrating in this

instance that the previous refusal of

PYM

to comply was not a frivolous activity. But he disagreed that the

IRS had

practical alternative means to collect taxes from Priscilla Adams. The

government should not be required “to engage in a time-consuming, and

possibly fruitless, scavenger hunt for other assets.” In

, the Third

U.S. Circuit Court

of Appeals had already rejected Priscilla Adams’s claim that the government

could devise a means for earmarking taxes for nonmilitary expenditures,

stating that there were “particularly difficult problems with administration

should exceptions on religious grounds be carved out by the courts.”

That issue also noted:

Film students from Brooklyn Friends School are directing and producing a

video documentary about Quaker peace activist Priscilla Adams. The students

came to Friends Center in Philadelphia to interview her about how her

religious beliefs led her to refuse payment of taxes in order to avoid

contributing to military funding. The students also interviewed George Lakey,

head of Training for Change, and Gene Hillman, adult religious education

coordinator for Philadelphia Yearly Meeting. This documentary film may be an

entry for Bridge Film Festival, which is open to middle and upper school

students at Quaker schools worldwide.

The issue noted that the film had

been made — a 16-minute short titled A Need to Witness. And hey, look — it’s on-line: