How you can resist funding the government →

about the IRS and U.S. tax law/policy →

how the government deals with tax resisters →

frivolous filing penalty

B. Frivolous tax submissions. The provision increases the penalty for filing frivolous tax returns or for filing frivolous tax submissions from $500 to $5,000 and expands the penalty to apply to all taxpayers and all types of Federal taxes.

This provision applies to submissions for collection due process, installment agreements, offers-in-compromise and taxpayer assistance orders.

This provision becomes effective for all submissions and issues raised after the date on which the Secretary first prescribes the required list of frivolous positions.

Raises $30 million over ten years.

C. Increased criminal fines and penalties.

The provision increases criminal fines and prison sentences for the three most common offenses: failure to file, filing a false or fraudulent return and tax evasion.

These proposed changes are substantially similar to increased criminal penalty provisions passed by the Senate in last year’s JOBS Act.

One notable change is the creation of a new aggravated failure to file offense.

While retaining the current misdemeanor penalty for non-filers needed to address simple violations, the new provision creates an aggravated offense to address more serious noncompliant behavior (“aggravated” means failing to file for 3 or more years with an aggregate tax liability of $100,000 or more).

Raises $5 million over ten years.

In ’s last-minute tax bill, the “frivolous filing” penalty was increased from $500 to $5,000 and expanded to apply not only to “frivolous” arguments made when filing a tax return, but to arguments made at other times, such as when requesting a collection due process hearing, an application for an installment agreement, an offer-in-compromise, or a Taxpayer Assistance Order.

Mostly this is of concern to people making the various constitutionalist tax protester arguments, which the IRS pretty much universally considers to be frivolous.

However, occasionally conscientious tax resisters get caught up in this as well.

A good policy to follow if you want to avoid this penalty is to keep your arguments about why you are not paying taxes or should not be required to pay all or some portion of your taxes separate from any official interaction with the IRS concerning your tax return or their attempt to collect from you.

In other words, if you do not want to risk getting hit with a penalty, do not write a note on your 1040 form explaining why you’re not including a check and do not request a collection due process hearing to discuss the Nuremberg Principles or anything of that sort.

If you are eager to explain to anyone at the IRS why it is that you’re resisting taxes, why it should be legal to do so, or why you think it is legal to do so, make your arguments separately from any official correspondence concerning your tax returns and make your arguments general ones so that the IRS will not interpret them as legal positions you are taking regarding your particular return.

That might not be enough to satisfy them, though, so be aware of the risks if you tilt at that particular windmill.

The IRS position, of course, is that conscientious tax resistance has no legal justification.

They spelled this out most explicitly in Revenue Ruling 2005-20.

The IRS is empowered to issue $5,000 fines to people who take what they call “frivolous” positions on their tax returns or in other filings with the agency or the tax court.

Occasionally, the IRS will send a frivolous filing warning to people who merely write them a letter laying out their conscientious objection to paying taxes.

According to the War Tax Boycott site:

These letters seem to be randomly sent to some (by no means all) war tax resisters who send the IRS a letter about their refusal to pay for war.…

Sometimes the IRS has sent this letter to people who have paid their taxes in full but enclosed a letter of protest paying for war.…

The site suggests that the IRS is using these letters to try to intimidate war tax resisters and people who let the government know of their conscientious objection.

The site also quotes from the tax code to show that a frivolous filing penalty can only legally be assessed in narrow cases, and can’t just be handed out to anyone who is uppity enough to say “I wish we didn’t have to pay for war.”

My own policy, thus far, has been not to bother communicating with the IRS much beyond what they require of me.

I don’t think their machines care what I think of them, and I’ve got better uses for my time than to correspond with them about how I think about things.

But for those tax resisters who want to explain themselves to the IRS, the advice I usually give goes something like this:

Don’t phrase what you say in a way that can be considered a legal argument.

It’s okay to say that your conscience forbids you to pay taxes.

But if you go on to say that you think some Constitutional Amendment or the Nuremberg Principles or something gives you legal authorization to take that stand, the IRS may interpret this as some sort of amateur pro se legal argument, and may declare your letter to be not just an expression of opinion but a “frivolous filing.”

I should say that this is just guesswork on my part.

It’s just as likely that the IRS sends out these “frivolous filing” notices more-or-less randomly and arbitrarily, based more on who’s stuffing envelopes on any particular day than on any articulable policies.

Tax resisters resist from many motives, sometimes more than one at once. For

instance, some war tax resisters resist as a form of conscientious objection — they’re unwilling to participate in war financing. Others resist as a form of

protest — they want to resist taxes as a way of emphasizing their opposition

to the government’s policies or to call their opposition to the attention of

the powers that be through civil disobedience. Many war tax resisters share

both of these motives.

For those that have protest as a motive, simply refusing to write a check to

the IRS

when they file their returns in April often doesn’t seem enough. How will the

government distinguish their refusal to pay as a protest from someone else’s

refusal to pay for other motives? For this reason, such war tax resisters will

often include a letter of explanation along with their tax filing that

explains their motives.

But lately, the

IRS has

been interpreting these letters of explanation as part of the tax filing

itself, and has been threatening resisters with a $5,000 penalty for

“asserting a frivolous position” in their filing.

,

Mike Palecek at

Pacific Free Press shares his experience with

one of these “frivolous filing penalty” threats. The last two years, he has

accompanied “crossed-out” tax returns with letters of explanation of the

following sort:

Hello. Enclosed is my tax form for this year.

It is crossed-out because I do not wish to cooperate with the government of

George W. Bush.

President Bush has chosen to spend our tax dollars on war and killing while

cutting spending on social programs.

As a Christian, I cannot go along with this.

I must protest.

Note that the letter is not taking any legal positions whatsoever — frivolous

or not. Palecek is merely saying that he is not paying because he does

not want to cooperate with the government, and indicating how the government

has lost his support.

Is that enough to trigger a frivolous filing penalty? Or, legally, should it

simply be a failure-to-file or failure-to-pay penalty? The

IRS sent

Palecek a letter saying they considered his filing to be frivolous, and

threatening him with a $5,000 penalty if he doesn’t refile properly.

The law that covers this is

Subtitle F, chapter 68, Subchapter B, part Ⅰ, section 6702

of the U.S. Tax

Code (the fine has been raised from $500 to $5,000 and some of the wording has

changed since the version of law that’s posted at the link above). It says

that the frivolous filing penalty can be assessed on someone who “files what

purports to be a [tax] return … but which — (A) does not contain information

on which the substantial correctness of the self-assessment may be judged, or

(B) contains information that on its face indicates that the self-assessment

is substantially incorrect; and [this]… — (A) is based on a position which

[is] frivolous…, or (B) reflects a desire to delay or impede the

administration of Federal income tax laws.”

The question then is whether a letter like Palecek’s can be reasonably

interpreted as a “claim that [he] may reduce [his] federal tax

liability based on [his] objections” or whether it is best understood simply

as an explanation of his decision to disobey the law without any intention of

making legal claims as to what he believes he may or may not do

within the law.

Practically a question like this one will be answered by some level of the

government bureaucracy, and so the rules of logic and language and such are at

best an imperfect guide. I could see it going either way.

There is, however, another section of this preamble that says “The penalty may

also be applied if the purported return… reflects a desire to delay or impede

the administration of Federal tax laws” — perhaps this would apply.

Myself, I think the best policy here is to simply refrain from poking the

hornets’ nest. If you resist your taxes and you feel the need to make some

noise about it, don’t make your noise in the direction of the

IRS, but

start a blog, or send a letter-to-the-editor, or write your congressperson, or

send an email to your friends and family.

If you do get a “frivolous filing” warning letter, don’t panic — according to

the letter, if you re-file in a non-frivolous fashion within 30 days of

getting the letter, they say they’ll forget all about it.

, I related

the story of Mike Palecek, who got hit

with a “frivolous filing penalty” warning letter when he enclosed a letter of

protest with his tax return.

His story

has since been picked up by the Des Moines Register.

It turns out that the adjective “frivolous” has a long history of being

applied to uncomfortable protest statements — critics of the U.S. Declaration of Independence called its complaints “false and frivolous.”

“both daunting and encouraging and well worth the considerable reading time… captures in one indexed volume many individual acts and campaigns of conscientious objection to war and of revenue refusal to tyrannical governments… sincere voices and challenging arguments.”

“167 intelligent and intense writings on the challenging question of whether people of conscience should pay for war…

People struggling with this moral issue today will be guided by the writings in this book and may find some wonderful language to use in their own statements of conscience… a straightforward and compelling book.”

Some notes on frivolous filing warnings, new tax laws, and IRS enforcement techniques.

Notes about tax resisters Bob Williams, Mike Palecek, and David Schenck, about the trial of two Los Alamos National Laboratory protesters, and about the upcoming New England Regional Gathering of War Tax Resisters and Supporters.

A story about long-time resister Thomas Wilson.

The state of Massachusetts suspended his dental license 21 years ago when he stopped cooperating with state tax laws because the state, in turn, was acting as a collection agency for the IRS.

Wilson kept practicing dentistry without a license, and was able to keep doing so until this year when he was forced to shut down after a competing dentist ratted him out to the state board of registration.

At 75 Tom is philosophical about closing the door on his professional life and has no regrets about his choices.

“In this present economy we’re getting a payback for what the government has been doing and what I haven’t been paying for and resisting all this time.

People ask if war tax resistance changes anything.

I can’t say that, but it’s helped me put up with what we have to put up with in this country.”

I’m fresh back from the NWTRCC national conference, which was held in Eugene, Oregon, and hosted by the enthusiastic and welcoming Eugene “Taxes for Peace Not War” group.

I’ve got a binder full of handouts and hastily-scratched notes that I took whenever I found a spare moment.

Today I’ll share some of my impressions of the gathering and of the current state of the war tax resistance movement.

Frivolity

Many of the attendees were concerned about the IRS being more aggressive in sending out notices of “frivolous filing” penalties to resisters who send letters of protest that explain their refusal to pay along with their tax returns.

One couple who were first-time resisters and had only refused to pay a token $50 last year were assessed “frivolous filing” penalties of $5,000 — each, even though they had filed a single return jointly — though they had filled out their return accurately and completely.

The IRS also insists that once they have assessed a “frivolous filing” penalty, you must pay that penalty before you can appeal it!

The law seems pretty clear that the “frivolous filing” penalty is only meant to apply if the tax return is incomplete or incorrect, but the IRS seems to be applying it haphazardly — not only to people who file complete and accurate returns but who refuse to pay some portion, but even to people who file and pay every cent but who merely inclose a letter registering their protest or disapproval!

Meanwhile, other resisters — including one who files a return every year with her social security number at the top but with none of the other required information, and with the 1040 form over-written with a protest message in red ink — have never been assessed a “frivolous filing” penalty or even received a “frivolous filing” warning letter.

The coordinating committee discusses the RFPTFA on morning

The “Religious Freedom Peace Tax Fund Act”

For a more in-depth examination of my misgivings about the RFPTFA, see:

One item on the agenda was a request by the National Campaign for a Peace Tax Fund that NWTRCC formally “recommit to the Religious Freedom Peace Tax Fund Bill and the efforts NCPTF is doing to get it passed in Congress.”

As I explained , I have serious misgivings about “peace tax fund” proposals in general, and think that the current incarnation of the Religious Freedom Peace Tax Fund Act in particular would do more harm than good.

However, NWTRCC had endorsed a different version of this legislation years ago, and so many people expected this new call for an endorsement to be a no-brainer.

Much debate ensued.

Robert Randall pointed out that NWTRCC’s “Statement of Purpose” includes “support of the US Peace Tax Fund Bill.”

He interpreted this as being a built-in endorsement of the latest act which would make the current debate moot.

However, no act by that name has been introduced recently — I think since — and in many important ways the current legislation does not resemble the version that NWTRCC endorsed back in the day.

I was a little worried that I would be the only one objecting to the endorsement and that this would put me outside of the general consensus of the group, but as it turns out there were many people present who expressed misgivings about peace tax fund legislation and who weren’t enthusiastic about endorsing it, and I heard more than one person express that this was a long-overdue debate.

Many of the Act’s supporters seem to have ideas of what the Act would accomplish that go way beyond the actual text of the legislation.

One said, for instance, that if the Act passed, it would effectively allow citizens to annually vote yea or nay on war or on whatever wars the government was engaged in at the time.

Some participants in the discussion were concerned that NWTRCC remain on good terms with NCPTF, in part so that we may be more influential as they recraft their strategy in the coming years.

One person said that because the Act is a long-shot to ever become law, it is best judged not by what its effects would be if it were enacted, but by what it symbolizes as a proposal that approximates the hopes of people who want legal recognition for conscientious objection to military taxation.

(Myself, I’m not sure I buy this argument, but in any case I think that the symbolism of the Act is ambiguous at best and may very well communicate a message that is, on the whole, harmful to the cause.)

The result of our discussion was that we decided to hold off on making a decision of whether or not to endorse until our meeting, at which time we will have more time to discuss the question and more time to study the points that are in debate.

A book of writings by and about Marian Franz and her work with the peace tax fund campaign is forthcoming, and will include a piece by Ruth Benn about the war tax resistance movement and its relationship with the peace tax fund campaign.

Election aftermath

There was varied reaction to the recent presidential election.

Many people were skeptical of the promise for meaningful change, and distrustful towards the Democratic party, and saw the election mostly in terms of whether it would anaesthetize progressive activists or whether it might be possible to reactivate the hopeful coalitions that helped to propel Obama into office once Hope turns to disappointment.

Others were very enthusiastic about the change and hoped that progressives and peace activists might finally be able to influence government policy.

One person went as far as to say that we’d “won” and would have to get used to being winners on the inside of the power structure instead of ignored pleaders outside of it.

Another hopefully imagined getting a group of progressive religious leaders to sit down with Obama and confront his faith with a challenge to go further than his public statements have so far suggested.

To me this all sounds like stuff of the same sort as gingerbread houses, flying carpets, and fairy godmothers, but I mention it here to show that some of the Hope bubble has infected even a skeptical group like NWTRCC.

There was much mention of “Camp Hope” — a vigil that will be held near Obama’s home in Chicago in up to inauguration day.

The goals of this vigil will be to encourage Obama to follow-through boldly on some of his more progressive campaign themes.

The demands of the vigil are meant to harmonize with, rather than to protest, the goals of the Obama campaigners, and will concentrate on actions that the new administration can take immediately via executive orders.

This is said to be partially based on a similar vigil that took place in the run-up to Jimmy Carter’s inauguration in that asked Carter to pardon Vietnam-era draft resisters and to cancel the B-1 bomber program, both of which Carter did.

A new war funding supplemental bill is expected to hit Congress in , and this will be an early test of what kind of Change we can expect from the new order, and what kind of power the current anti-war movement is capable of asserting.

The War Tax Boycott

’s war tax boycott campaign was well-received by some local war tax resistance groups, who found it a good focal point for their outreach efforts.

However, the number of people who participated in the boycott disappointed the hopes of those who initiated the campaign.

There was much discussion of whether we should continue the campaign into and if so in what fashion.

If we were to continue the campaign into — making the the climax of the campaign — this would give us little time to mount a serious outreach effort, and at the same time it would have to compete for attention with the actions of the opening months of the new Obama administration.

It might be hard to convince new resisters to join up if they’re still placing their hopes for peace with their rulers.

We eventually concluded that we would continue the campaign, but would concentrate this year on retrenching and consolidation rather than on a major outreach and publicity campaign, in preparation for a larger campaign when the inevitable Obama Disappointment sets in.

Meanwhile, local groups that find the campaign useful can continue to use it as before.

Rather than making April 15th the target date for beginning to resist, we may be better off doing what Code Pink did with its war tax resistance campaign and tell people that their resistance begins the moment they take their first affirmative step toward tax resistance, for instance by adjusting their W-4 withholding.

One person said that although she resisted taxes , she didn’t sign up for the boycott because she was only resisting a small amount and was redirecting that amount to local groups, and she had the impression that the boycott was mainly for people redirecting larger amounts to the two showcase charities highlighted by the boycott campaign.

Some people who did boycott outreach found that some folks were reluctant to sign on to the boycott for fear of the danger of being on some government list, and stressed that there should be a way for people to join the campaign anonymously.

Miscellany

Some local University of Oregon students dropped by the meeting and volunteered to create a redesigned mock-up of the nwtrcc.org web site that we could use if we’d like — a much-appreciated and spontaneous act of generosity.

NWTRCC will be trying to nurture a new regional gathering of war tax resisters — something along the lines of the New England Regional Gathering of War Tax Resisters and Supporters that is coming up later .

To this end, it will be inviting groups that are interested in hosting such a gathering to submit proposals, and will select one of these proposals to support with some seed money and other assistance.

NWTRCC decided to commit to revitalize the War Tax Resisters Penalty Fund, which seems to have run out of steam (appeals for funds go out very infrequently, and resisters are reimbursed only after long delay).

NWTRCC coordinator Ruth Benn is preparing a series of “Readings on Money.”

These include transcripts of some of the discussion on that subject at the Fall gathering in Las Vegas, Karen Marysdaughter’s essay on “The Influence of Money on Decisions to Engage in War Tax Resistance,” George Salzman’s “Inheritance and Social Responsibility,” a debate about the ethics of accepting interest on loans and bank deposits from Juanita Nelson and Bob Irwin, and a look at the intwined structure of government spending, national debt, the war machine, the federal reserve, and the income tax from Jay Sordean.

Kathy Kelly leads a workshop on “Honesty and Empathy: Questions for Collaborators”

Kathy Kelly led us through some role-playing exercises concerning collaboration and how to confront it, and shared some stories with us from her experiences with activism and humanitarian assistance.

Her public presentation at the University after the end of the NWTRCC conference session was well-appreciated by those who attended.

Kelly is an engaging speaker who relates interesting experiences vividly and well — with a great command of accents and the ability to invoke strong and varied emotions without making the audience feel like they’ve been strapped on a roller-coaster.

One of her themes: around the world, many people are forced to make great sacrifices because of the decisions our political leaders are making.

Meanwhile, what will raise us to make the sacrifices we need to make to make things right?

To those of us to whom much has been given, much will be expected in this regard.

We need to slow down and unflinchingly reassess our priorities.

“This is what grown-ups do.”

Mike Butler volunteered to bring NWTRCC into the MySpace / Facebook universe, so keep an eye out there.

Erica Weiland removes a pillar of militarism in Susan Quinlan’s workshop

Susan Quinlan demonstrated some of the techniques she uses in youth outreach to teach about the unbalanced government budget priorities and about how to build a better society by shifting your support from the pillars that support a system of injustice to the pillars that support the scaffolding of a better system.

I remember a couple of interesting stories of how people were introduced to war tax resistance.

One couple was working with Christian Peacemaker Teams in Colombia and met some war tax resisters there and then took up war tax resistance on their return home.

Another new resister had been working for an alternative newspaper that received a grant from a war tax resisters’ tax-redirection alternative fund, and learned about war tax resistance that way.

Conference attendees review part of Steev Hise’s rough cut for Death and Taxes

Steev Hise’s war tax resistance video project continues, with a projected completion date around .

Conference attendees saw a preview of a portion of the film and seemed enthusiastic about it.

The next national meeting will be held this coming Spring (early ) somewhere in the vicinity of Washington, D.C. — details to be hashed out in the coming months.

The next national will be in Cleveland, Ohio around .

And with all that, I’m still leaving a lot out.

But for now, that’ll have to do.

I mentioned in my wrap-up of ’s NWTRCC gathering in Eugene that “One couple who were first-time resisters and had only refused to pay a token $50 last year were assessed ‘frivolous filing’ penalties of $5,000 — each, even though they had filed a single return jointly — though they had filled out their return accurately and completely.”

I’m happy to report that this couple came home from Eugene to some good news:

…for those of you who heard of the couple who got slapped with $10,000 frivolous fine ($5,000 each) it was just lifted.

Apparently the Taxpayer Advocate Office helped.

For those of you who don’t know, this was a first-time resistance of a small amount of a larger tax bill.

Honest return filed with a protest letter and partial payment.

The filers were warned they might get a fine, so they re-filed and paid the amount refused a few months later and shortly after got a letter telling them they each owed $5,000 as a frivolous penalty.

They protested and finally heard this quite unjustly applied fine was released.

Whew.

We’ll try to add more on the NWTRCC website about this frivolous business as we learn it.

It appears to be applied very inconsistently and incorrectly.

Counseling notes including news about the new policy of allowing employers to give their employees tax-free bicycle commuting reimbursements, a reminder that if you’re given a summons to appear before the IRS you should ask for reimbursement of expenses, and a note about the “socially responsible” investment business Pax World Fund getting caught investing irresponsibly.

International News — an update on the case of Siân Cwper that I mentioned .

Apparently the British revenue department is playing some strange games with the members of the Peace Tax Seven.

(For more on the Peace Tax Seven, see this report on The Shrieking Violet.)

Ideas and Actions — including a report on tax resistance for same-sex marriage rights, a report from Ed Hedemann who spoke about war tax resistance with a class of seventh-graders, and a new NWTRCC-themed scarf (perfect for fundraising at winter demonstrations).

Notes about updated literature — including the booklet War Tax Resisters and the IRS which “gives a flow-chart style version of the risks of refusing to pay for war if the IRS notices.”

A call for fundraising help particularly to help promote Steev Hise’s upcoming war tax resistance documentary

Reflections and lessons learned by Becky Pierce — “I have been a war tax resister for the past 43 years, all of my adult working life…” This includes some useful information on IRS collection tactics, for instance how they go about hunting for assets to seize as the statute of limitations closes in and they start to get desperate.

The newsletter article about frivolous filing penalties mentioned that “in after the IRS instituted the ‘frivolous’ return penalty, Karl Meyer called for a ‘cabbage patch’ response, filing a form every day for a year to defy this new policy.

He was assessed $140,000 in penalties during , and in the IRS seized his station wagon in an attempt to collect on the fines.

It was sold for $1,020. Karl continues staunchly to refuse to pay for war.”

Here’s how the Chicago Sun-Times covered that story back in :

Tax resister mails a protest return every day

Every afternoon, Karl Meyer sits at his old cedar desk under a sign that declares “Your tax dollars arm the world!” and fills out a federal tax form.

Where the form calls for a Social Security number, he prints, “Refused — not to be used for social insecurity purposes.”

Where it instructs “Add line 1 and line 2,” he prints, “Military Spending” and adds a summary of the Pentagon’s budget.

And where it instructs “If line 8 is larger than line 9, subtract line 9 from line 8,” he prints, “I refuse to pay federal income taxes that sustain military violence in Central America and all over the world.”

Meyer, a 48-year-old Chicago carpenter, mails one such protest to the IRS each day.

He never includes a check.

He is one of about 76,000 Americans who will refuse this year to pay part or all of their federal income taxes.

Some say taxes are unconstitutional.

Some don’t have the money.

And some, like Meyer, believe federal tax dollars are doing more harm than good.

“If people want us to contribute to the common good by way of paying taxes, they’ll have to find some way we can contribute without paying for the military system,” he said.

Meyer’s words are not the self-serving rhetoric of a skinflint.

His 25-year history of regular jail terms for acts of civil disobedience attests to the strength of his convictions.

In , after graduating from the University of Chicago, he was arrested and jailed 38 days for passing out anti-tax leaflets.

Months later, he joined a 4,000-mile peace march to Moscow’s Red Square.

In , he tore up his draft card and mailed the pieces to then-U.S. Attorney Edward V. Hanrahan.

And in , he served nine months in federal prison for filing false tax returns to protest U.S. involvement in Vietnam.

Since , Meyer has filed more than 54 federal tax returns — one for each day’s average earnings of $38. The Internal Revenue Service has responded by fining him $6,000 for filing “frivolous” returns.

His wife, Kathy Kelly, a high school teacher in Chicago, also refuses to pay taxes.

Instead, he said, she accepts only $8,000 of her annual $18,000 salary and tells her employer to donate the rest to charity.

Meyer, who says he has earned between $13,000 and $18,000 annually , claims the IRS has managed to collect only $168 from him .

He has quit jobs and moved bank accounts to prevent further collections.

Michael McGrail, an IRS tax specialist, could not verify this claim, but confirmed that Meyer has been fined and jailed repeatedly for tax evasion.

Athens, Ohio — When Dr. Marjorie Nelson wrote “war tax deduction” on her federal income tax return to protest military spending, the Internal Revenue Service fined the 44-year-old Quaker $500 for filing a “frivolous tax return.”

Miss Nelson still hasn’t decided what to do with her tax forms, but says she’s willing to go to prison to uphold her religious beliefs if a court orders her to pay the fine.

At least a half dozen other Ohioans face a similar choice.

“This business of laboring with the IRS is not my career.

It’s just something that happened to me — I certainly find it strange,” said Miss Nelson, a teacher at Ohio University’s College of Osteopathic Medicine since .

In figuring a refund amount Miss Nelson believed was equal to her taxes that would go to support the military, she attached a letter explaining her religious objections.

She says the $500 fine is a ploy to limit free speech on the nuclear war issue.

“It seems to me the government’s main purpose should be to collect the taxes, not to stifle a statement of conscientiousness.

I get the feeling the government is trying to chill dissent, to intimidate people so they won’t speak up over issues of conscience.”

But the government attorney handling frivolous return cases in Ohio said efficient tax collection will be threatened if people aren’t stopped from filing inaccurate returns.

“It does not require great imagination to see that if all taxpayers were free to act as the plaintiff (Miss Nelson) acted here, our self-assessment system of taxation would be seriously jeopardized,” attorney Seth Heald said in documents filed in U.S. District Court at Columbus, where Miss Nelson’s case is pending.

Heald, of the U.S. Justice Department tax division, said incorrectly figuring a refund is just as wrong as falsifying income and causes just as much work for IRS clerks.

He said Congress passed the frivolous return law specifically to apply to war tax deductors and that waiting for a court to look at each return before judging it frivolous would let people ask for refunds “because the sky is blue.”

Since the frivolous return law took effect in , people across the country have challenged the fines in court.

Cases have been decided — all against the “war tax” deductors — in California and Massachusetts, but many people will fill out tax returns before their cases are decided.

If courts rule against them and they don’t pay the fines, Miss Nelson believes they could go to jail.

In court documents, Miss Nelson said the IRS doesn’t fine people who refuse to pay taxes without explaining their objection.

She said her dispute with the government is the only way people who have taxes deducted from paychecks can oppose military funding.

The self-employed can refuse to pay taxes, but most people can only ask for refunds of taxes they have already paid.

Bruce Campbell, the American Civil Liberties Union lawyer handling Miss Nelson’s case, said it’s unlikely she or anyone else would go to prison.

Where are they now, 26 years later?

Nelson is still resisting war taxes, I believe, or at least was as late as when she was interviewed for another article on war tax resisters for the Dispatch.

I think also that Seth Heald is still working the tax angle at the Justice Department, and Bruce Campbell is still filing briefs for the ACLU.

“Cabbage Patch Resistance” marks a true war-tax hero

by Stephen Brockmann

By April 15 of any year most of the people in this country who earn money

will have paid their taxes to the federal government. Some of them will

cheat, but most of them will be honest.

Many of the people who pay their taxes may do so reluctantly. They disagree

with the federal government about the way their money is spent but pay their

taxes anyway. That is the consensus on which the government’s ability to

operate is based.

Year after year a small proportion of people refuse to pay all or part of

their federal taxes. Some of these people are libertarians who radically

question the government’s right to assess taxes; others disagree with the

government on specific issues. Some of them have good arguments; some of them

don’t.

The case of one man who refused to pay his taxes this year strikes me as

particularly interesting and creative. The man’s name is Karl Meyer, and he

is part of a small but determined group of war-tax resisters who refuse to

pay their federal income tax because they do not want their money spent on

nuclear war.

A year ago the Internal Revenue Service started assessing $500 fines for what

it labels “frivolous” tax returns; in this case “frivolous” meant anything

from actually refusing to pay all or part of one’s tax to simply writing a

message of protest or using a phony name on the tax form.

It seems to me that the

IRS’

choice of “frivolous” is remarkably poor. The people against whom it is

levying $500 fines are the opposite of frivolous: They take the tax form and

their own actions with the utmost seriousness. Indeed, the

IRS

seems to be fining them because they are not frivolous.

Karl Meyer’s response to this “frivolous” fine was both clever and

thoughtful: He decided to call the government’s bluff and see how far it

would go with the frivolous $500 fine. Meyer published a statement in the

monthly peace-movement forum The Peacemaker,

announcing his intention of sending in a tax return for every day of the

year. The government might be able to collect $500 from him, but it would

have difficulty collecting 365 times that amount.

Meyer urged other people to follow his example or to come up with creative

ideas of their own. He called his project the “Cabbage Patch Resistance”

after the name of the popular doll: Like the dolls, each of his 365 tax

returns would be slightly different, each with a special anti-war message.

The government would have to test its frivolity in 365 cases.

One year later the

IRS

has called Meyer’s call of the

IRS

bluff: As of recently, Meyer had accumulated $135,000 in frivolous penalties

and interest for the income tax returns he filed

.

Meyer, who is 47 and married, has three children in high school and college.

A self-employed carpenter in Chicago, he has a long history of fighting with

the IRS.

In he spent nine months in prison for his

beliefs.

Meyer’s example has until now had only modest outward success: Six people

appear to be following it.

All this interests me because, like Meyer, I oppose this government’s

frivolous nuclear-war policy. I favor disarmament and believe that the

government is doing less than nothing to promote peace.

I believe in many of the things that Meyer believes in, and yet, unlike

Meyer, I am a conspicuously law-abiding person. I am not married, nor do I

have children, and so my failure to break the law has nothing to do with fear

for dependents. I am, quite simply, afraid for myself. Insanely, my fear of

immediate personal discomfort is more effective than the deeper fear of

ultimate nuclear destruction. In that sense, I suppose I am irresponsible and

frivolous.

Oh yes, I believe in taxes and government. I am neither an anarchist nor a

libertarian. Under normal circumstances I would have no qualms about paying

taxes, even for things that I don’t like.

Many of my friends are daring and admirable in their principled civil

disobedience, both to taxes and to weapons that taxes pay for, but I am not

a particularly courageous man.

I am not a criminal, and I am not a hero. I am a comfortable petty bourgeois

living in a time with plenty of criminals and a few heroes.

Which is why Karl Meyer makes me stop and think. A man willing to risk so

much to gain so much, and for such a good cause, is rare. Karl Meyer is my

hero.

Counseling Notes — how tax resisters can avoid getting preyed upon by “settle with the IRS for pennies on the dollar” companies; more “frivolous filing” overreach from the IRS; and increased use of IRS enforcement tactics isn’t leading to increased tax revenue

Many Thanks — to the generous donors who keep NWTRCC in business

Criminal Cases and Fear — Karl Meyer writes from the standpoint of decades of experience with war tax resistance about what factors increase the likelihood of criminal prosecution for war tax resistance. Larry Dansinger and Ruth Benn add two cents apiece.

War Tax Resisters in History — Ed Hedemann reviews some of his research into the U.S. government’s use of property seizures and criminal cases as tools against war tax resisters in the post-World War Ⅱ era

Resources — notes on the Death & Taxes DVD, the new “Thoreau and His Heirs: The History and the Legacy of Thoreau’s Civil Disobedience” study kit, and the NWTRCC fundraising scarves

NWTRCC News — a note on the upcoming national conference in Boston next month

What happened between the time when Peacemakers was leading the war tax resistance charge and , when the National War Tax Resistance Coordinating Committee was founded?

There was another group, simply called “National War Tax Resistance,” that took the reins during the Vietnam War.

was, as the CNVA Bulletin declared, “The Year of Vietnam.”

Picketing and sit-downs across the country marked the announcement of the first US bombing of North Vietnam on .

These continued throughout the month and much effort was expended gathering signatures for a new appeal, the Declaration of Conscience, circulated by radical pacifist groups, urging civil disobedience.

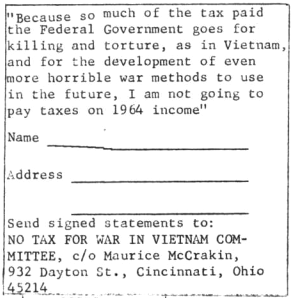

The Peacemakers group in Cincinnati organized a “No Tax for War in Vietnam Committee” calling for tax resistance.

In a separate group — War Tax Resistance, coordinated by Bob Calvert — was established and at the time included some 200 local tax resistance centers across the country.

Nonpayment of war taxes, practiced by Quakers and others, disappeared as a pacifist testimony soon after the Civil War and Thoreau’s famous stand against the U.S. foray in Mexico.

It first reappeared in World War Ⅱ when a few widely scattered individuals refused to pay federal taxes on the grounds that there was no way to prevent a significant part of their money from being used for military purposes.

One resister, Ernest Bromley, was prosecuted and imprisoned for his refusal.

Many others began to inform the Internal Revenue Service that payment violated their principles.

The enactment during World War Ⅱ of a measure which required employers to withhold taxes from their employees caused particular difficulties for pacifists and led to the formation of Peacemakers in .

A Peacemaker committee promoted tax refusal and provided research, literature, action suggestions, and publicity for those in the tax resistance movement.

Although many hundreds of people were refusing to pay income taxes during , the government prosecuted and imprisoned only six: James Otsuka of Indiana, Maurice McCrackin of Ohio, Eroseanna Robinson of Illinois, Walter Gormly of Iowa, Arthur Evans of Colorado, and Neil Haworth of Connecticut.

These imprisonments and the seizure of a few cars and houses by the IRS, served to highlight the tax refusal testimony and establish it as a major nonviolent principle and tactic.

Tax resistance, like other forms of opposition to the military, increased dramatically during the Vietnam War.

In the federal government levied an additional tax on every private telephone, and in a rare moment of candor, admitted that the money would help subsidize the war in Indochina.

Peacemakers, the War Resisters League, and other nonviolent groups urged refusal of this tax and in the following years countless thousands heeded their call.

Under the leadership of Bob and Angie Calvert, War Tax Resistance was formed in as a separate organization to investigate all aspects and ramifications of conscientious tax refusal.

During the war there were over 200 local war tax resistance centers, as well as a number of “alternative life funds” which rechanneled refused tax money back into the local community for constructive purposes.

Many of these continued after the end of the war.

The tactic of claiming enough dependents so that no income tax would be withheld became more widespread as the Vietnam war continued.

Often the tax refuser would make clear the moral grounds for the protest by listing, for example, “all the Vietnamese” as dependents.

Refusing to pay for war by claiming excessive exemptions brought particularly strong response from the government.

A number of people were prosecuted and imprisoned: Jim Shea, Karl Meyer, William Himmelbauer, Mark Riley, Ellis Rece, Carole Nelson, John Leininger, and Martha Tranquilli (a 64-year-old grandmother and nurse).

The tax resistance movement continued after the war and grew to include both pacifists and non-pacifists who could no longer in conscience support the military priorities of the government.

As more and more tax money was directed toward the [Reagan era] military buildup, many activists revived interest in war tax resistance.

Protests were organized each year, and individual resisters tried a variety of means to deny the government money for war.

In , demonstrations were held in Dallas, Atlanta, San Francisco, Los Angeles and other cities and 24 people were arrested at IRS offices in New York City.

The following year, the National War Tax Resistance Coordinating Committee was formed by the Center on Law and Pacifism, Conscience and Military Tax Campaign, WRL, Peacemakers and eighty local groups.

featured the largest show of war tax resistance actions in , including Ralph Dull, an Ohio farmer and tax resister , who drove a truckload of grain to the IRS office as payment for his taxes.

The IRS instituted a “frivolous returns” penalty to discourage the filing of returns with any but the requested information, and some resisters began an insurance fund, pooling their resources to pay fines and interest charges levied against fellow tax resisters.

It was e.e. cummings, I used to love this when I was an early teenager about a conscientious objector [“i sing of Olaf glad and big”].

There was one line, “there is some shit I will not eat,” that reverberated in my social conscience since probably age 12.

There comes a point when there is something out there that we have to reject ultimately, and we have to throw ourselves on the wheel to stop it — even if the wheel devours us.

The boycott of taxes is so strong, so potentially powerful, that I guess I am urging other people to go forward without fear.

We are right.

War is wrong.

We are approaching the totalitarian state.

Take from them their finances, and we take their strength.

Eliminate the nexus between corporate wealth and industry and politics.

In this era there is so much to protest against, and tax is a very salient part of that.

A note about “frivolous filing” notices.

The IRS has gotten in the habit of responding to taxpayer protests with $5,000 frivolous filing penalties — even if the protests accompany a tax return that has been filled out correctly and legally.

What’s worse is that by the IRS’s rules, in order to appeal such a fine, you have to first pay it.

Peace activists have a resource of financial support when they accrue penalties for resisting taxes, participating in civil disobedience or in nonviolent direct action.

Through the PSC, the cost of a person’s or family’s penalty can be defrayed by almost 100%.

This is possible because a community of almost one hundred people have come together and committed to help each other with their fines.

A new edition of More Than a Paycheck,

NWTRCC’s newsletter, is now on-line, and features the following:

A war tax resistance manifesto by Larry Rosenwald, and responses from Claire Schaeffer-Duffy, Karl Meyer, and Bill Glassmire.

(I’ll have more on this in a future Picket Line entry… stay tuned.)

Buyer Beware, a poem on military spending by Marge Piercy

The IRS has gotten in the habit of sending out “frivolous filing” notices to anyone who writes them a letter explaining their reasons for tax resistance (or even in response to letters from non-resisters who are just paying under protest). These notices are accompanied by a $5,000 fine — a fine that, by law, must be paid before it can be appealed. The IRS is only authorized to assess such fines in response to a tax filing that is incomplete, inaccurate, and that involves some frivolous legal stance, so it is pretty clearly overstepping its bounds here: but because a resister must pay the fine in order to appeal it, and most war tax resisters are unwilling to do so, this puts them in a bind. One resister, Steve Leeds, got such a frivolous filing notice and then, instead of paying the fine and formally appealing it, he complained to his congressional representatives about the IRS’s abuse of the law. One of his representatives then contacted the IRS, which then caved — sending Leeds an apology.

If the IRS attaches a levy to your salary, it will leave you some portion of your salary to live on while it sucks away the rest. How does it determine how much to take? Is it based on your base salary, or on what’s left over in your check after deductions for 401(k) contributions, insurance premiums, commuter checks, or what have you? Turns out the answer is the latter, but only if those deductions were already in effect at the time the levy was received by the employer.

A book review of The Green Zone by Clare Hanrahan — this book looks at the environmental impact of the U.S. military, which is exempt from laws and treaties designed to protect the environment, and, according to the author, is “the largest single polluter of any single agency or organization in the world.”

War tax resistance ideas and actions, featuring a penny poll in Oregon, a protest in Washington D.C., and the upcoming New England gathering of war tax resisters.

NWTRCC News — a behind the scenes look into operations at NWTRCC headquarters.

Boardman says that the agency is violating the First Amendment right to freedom of religion, and to the later Congressional bolstering of that right by the Religious Freedom Restoration Act of 1993, by labeling her war tax resistance “frivolous” and failing to provide a taxpaying method that accommodates her sincere religious beliefs forbidding her to pay for war (Boardman is a Quaker).

At a luncheon held to mark the filing of her Claim, actor Jeffrey Viguie, playing the part of 18th Century Quaker John Woolman, addressed the attendees, and read from the “Epistle of Tender Love and Caution” in which Woolman and others promoted war tax resistance to the Society of Friends in 1755.

The Internal Revenue Code permits the IRS to slap a $5,000 “frivolous filing penalty” on anyone who files a tax return that “(A) does not contain information on which the substantial correctness of the self-assessment may be judged, or (B) contains information that on its face indicates that the self-assessment is substantially incorrect, and … (A) is based on a position which the Secretary has identified as frivolous… or (B) reflects a desire to delay or impede the administration of Federal tax laws.”

The IRS has been abusing this authority to fine people who file full and correct tax returns but who also include with their returns letters of protest indicating why they are not paying the full amount or why they feel their taxes are being misspent.

The law pretty clearly says the penalty only applies to filings that both assert a legal position the IRS considers frivolous or designed to delay or impede tax collection and accompany a tax return that is incomplete or incorrect.

But the IRS has a trick up its sleeve: in order to challenge an unlawful fine like this, according to the IRS’s own rules on the subject, you must first pay the fine.

Tax resisters who are unwilling to give money to the IRS are thereby locked out of the appeal process, and the agency can fine them whether or not they have the legal authority to do so.

The agency seems determined to continue abusing its authority in this way.

The law students who have taken on Vickie Aldrich’s case plan to pursue this angle in their defense strategy.

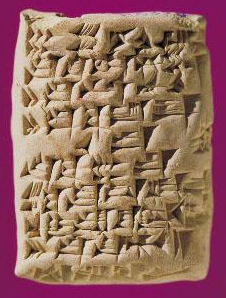

an early tax form, from when paperwork was fired in clay

Tax agencies live by bureaucracy and paperwork.

Many of the earliest examples of writing in the worlds’ museums are tax records.

But some mischievous tax resisters have discovered that this is a vulnerability that can be targeted.

For example, , a video blogger going by the name “StormCloudsGathering” considered the idea of “filling out thousands of random tax returns with nonexistent names and numbers… so suddenly they get flooded with a bunch of returns that don’t make sense…”:

What’s even more brilliant about [this] option is that even non-U.S. citizens — people living in other countries — could participate.

You could send in hundreds of tax returns even if you’re an Indonesian.

You know: Americans can live in Indonesia, and they’re required to file taxes… there’s no way for them to be sure, just because it’s coming from Indonesia, that it’s not a valid tax return.

They would have to do the investigation, and that costs resources.

He recommends filing in the name of particular, offensive, multinational corporations, but I think the average person would have a difficult time filing a sufficiently complex return to serve as a convincing decoy in such a case.

Another option would be to file corporate returns for nonexistent corporations, or individual returns for phantom (or dead) people.

War tax resister Ed Hedemann has already made plans for what he calls “zombie war tax resistance” — filling in years of tax returns ahead of time and putting them in pre-stamped envelopes so that his survivors can continue to file (but, of course, refuse to pay!) after he’s gone.

“Why give the government a break from having to deal with your resistance when you die?”

he asks.

Hedemann also makes a point of periodically filing Freedom of Information Act requests for any information the IRS and other government agencies have been collecting about his activities — hundreds of pages — and he’s put together a guide for other tax resisters to follow in making their own requests.

Currently in the U.S. there is an epidemic of tax fraud in which the fraudsters file for phony tax refunds in the names (and taxpayer identification numbers) of other, real people.

This often causes the tax collection bureaucracy to swing into action against the victims of the identity theft, which is both a waste of resources and a way of further alienating the population from the government and its tax bureaucracy — potentially a model that a tax resistance campaign could benefit from.

The IRS has made a big shift in recent years from processing paper income tax returns, filled out by hand, to electronic filing.

This is more efficient for the agency, as it no longer has to hire as many people to laboriously transcribe the numbers from paper returns into its computer databases.

The agency estimated that it cost about 35¢ on average for the agency to process an electronically-filed return, compared to an average of $2.87 for a paper return.

This suggests that one way to make a minor dent in the agency’s budget and efficiency is simply to file paper returns rather than file electronically (this is still a legal option for individual filers, even those who go to professional tax preparers).

But if this became a strategy of a mass-campaign it could even cripple the tax collecting bureaucracy.

George Jakabcin, IRS assistant deputy associate chief information officer for systems integration, said in that the agency “would be in a world of hurt” if even half of the people who had switched to electronic filing at that time decided to switch back.

“We no longer have the capability to process the additional 43 million returns manually.

We no longer have the facilities, we don’t have the IT infrastructure in place to support them, we don’t have the people, and some would argue that we are beginning to lose the expertise.”

The IRS has tried to crack down on people who send them paperwork just to waste their time.

They have come up with something called the “frivolous filing penalty” and can use this to ding you $5,000 each time you file any sort of paperwork with them that takes a position they consider to be “frivolous.”

They can do this immediately and on the whim of whichever bureaucrat is handling your forms, without going to court, and you are only allowed to appeal your fine before a judge if you pay it first!

War tax resister Karl Meyer wasn’t about to let the IRS think it could intimidate him with such tactics.

So in , when the “Cabbage Patch Kids” dolls (each one slightly different) had become ubiquitous, he invented when he called “cabbage patch resistance” — filing a different, blatantly “frivolous” tax return every day.

He was assessed $140,000 in penalties in alone (though the penalty was only $500 back then).

The IRS never collected the money though.

The best it could manage was to seize and sell his car, for a little over $1,000.

“Constitutionalist” and “sovereign citizen”-style tax protest groups in the U.S. are fond of harassing tax officials and other government employees with lawsuits, liens, bogus quasi-official court filings, and so forth.

In one example, Eddie Kahn’s “Guiding Light of God Ministries,” filed some 2,000 misconduct complaints against IRS agents.

A newspaper article about a subsequent legal case against the group noted that:

Some agents have said that their supervisors ordered them to back off from audits or collection efforts in the face of [such] threats, just to avoid investigations by the Treasury inspector general for tax administration.

Some paperwork tricks are more like “hacking” in that they treat the IRS as a system that processes input and produces output, and note that certain examples of pathological input can result in output unanticipated by the system designers.

For example, the IRS gave out $20 million dollars in the filing season when people figured out that if they substantially overpaid a tax return with a bad check, the IRS would cut them a hefty refund check before they noticed they’d been had.

Here are some more examples of paperwork hacks being used against the tax collecting bureaucracy:

South Carolina’s state government recently passed a law that required all organizations that “directly or indirectly advocate, advise, teach or practice the duty or necessity of controlling, seizing, or overthrowing the government of the United States, the state of South Carolina, or any political division thereof,” to register their activities with the South Carolina Secretary of State and pay a five-dollar filing fee.

A member of the Alliance of the Libertarian Left (which probably qualifies, at least in its more ambitious moments) decided to register, but with a twist:

When belligerence and inhumanity prevail, the peaceful and the humane must find honor in being categorized as the enemies of the prevailing order.

Please keep me updated as to the status of our registration.

I look forward to hearing back from you as to our official recognition as enemies of your state and its government.

… P.S. I am told that there is a processing fee in the amount of $5.00 for the registration of a subversive organization.

Our organization is in fact so dastardly that we have refused to remit the fee.

Prussian farmers in used the bureaucracy against itself.

A New York Times report noted:

[T]he big agrarians… are determined to resort to sabotage of all the tax laws…

[A correspondent in East Prussia says] “They have all filed protests and demanded that they be relieved from paying the tax until the protests are settled.

That means a delay of at least three years in collecting the taxes, and it is said that the Provincial Treasury is inclined to grant this request.

The big agrarians declared that they would do the same thing with all the tax laws.

In Berlin the people might decree what pleased them, they (the agrarians) would not pay the taxes or subscribe to the compulsory loans.

They want to sabotage the whole taxation system that they hate, and consequently they want to make so much work for the Treasury officers that the latter don’t know which way to turn.”

During the Beit Sahour tax strike against the Israeli occupation, Elias Rishmawi worked to get a suit challenging the legality of the tax accepted by Israel’s court system.

He remembers: “I had never had an illusion that the Israeli supreme court would give any justice to Palestinians.

… [T]he appeal formed the legal coverage by which I and others were able to continue resisting from one side not paying taxes, since there is a case in court and they cannot force me pay until the case is solved they cannot take any actions against us since we have this case, and we kept challenging the system through different means.… This was impossible to achieve without the legal coverage of the supreme court.

Because then, I and the others, would have been considered as inciters and then might be imprisoned for ten years.

That’s why we needed that coverage.”

An early form of resistance to Thatcher’s Poll Tax was called the “send it back” campaign.

The idea was that people would register for the tax, as required, but would accompany their registration with questions that would require further manual processing by the individual councils that were processing the tax:

Government regulations state: “…if for any reason you consider that you are not a ‘responsible person’ please let me know and return the form to me without completing it.”

Stop It wants people to take up this offer by writing to ask if they should be the “responsible person” and suggests they ask who will have access to the information supplied and why the authorities require exact dates of birth.

The implementation of the tax was dependent on an accurate register and the protest campaign could make the register “wildly inaccurate,”… Labour MP Brian Wilson, chairman of [the anti-poll tax campaign called] Stop It, said: “It is a campaign of obstruction within the law that does not lead people to incur the substantial penalties that are built into the legislation.”

The aim was to have the legislation amended or abandoned.

For this and other reasons, the councils were inundated with paperwork, for which they were unprepared.

“Councils sat under a mountain of paper.

Everything they did seemed to create more work,” wrote campaign historian Danny Burns.

He quotes from the Poll Tax Legal Group:

The paper-work involved with administering the charge is enormous — and likely to get worse.

Backlogs switch from one area of activity to another.

Indeed, local authorities cannot really do anything without generating more paper-work.

Kate Harvey, a tax resister for women’ suffrage in 1913, once wrote: “I have just received the first demand note for this year’s taxes.

I have torn it up, put it in the envelope in which it came, and re-posted it to the Tax Collector.

I suppose it is now reposing in his rubbish basket.”

The Association of Real Estate Taxpayers in Chicago during the Great Depression led tens of thousands of property owners to demand reassessments of their property, which effectively swamped the Board of Review and allowed the property owners to legally delay tax payment.

It may sound like a long shot, but have you considered trying to make friends with the tax collector?

It’s a strategy that’s so crazy it just might work!

Here are some examples of where tax resisters or their allies have tried it:

The Peacemakers were eventually successful in winning back war tax resisters Ernest and Marion Bromley’s home, which had been seized for back taxes.

In a retrospective, they claimed:

The Peacemakers were resolute that their confrontation with the government would be on their terms. Believing that the legal system is an instrument of oppression and exists to protect the state and the property of the powerful, they refused to take their case into the courts.

Instead they worked to make the truth known through personal meetings with IRS officials, through continuous leafletting, through appealing to their supporters country-wide to demand justice.… They put enormous energy into building relationships with IRS officials that would allow for honest dialogue.

And always, they challenged and responded to the bureaucracy in a highly personal manner.

Initially it appeared that IRS’ reversal had been an act of faith in the Peacemakers; that it had been touched by the group’s philosophy of truth and their consistent methods.

It wasn’t that complete a victory.

The Commissioner had been sufficiently impressed by these people to where he called for a special investigation — which verified the Peacemakers’ statement.

Dorothy Day wrote of this:

Chuck Matthei had told me the story of his interviews with the head of the Internal Revenue Service, the almost daily dialogue that went on between them, and the frank and “manly” admission, made finally by the IRS chief, that a mistake had been made, that the Peacemakers had Truth on their side.

I felt a great sense of joy and thanksgiving, a sense of hope too, that our officials in Washington D.C. could be approached in this way — with dignity and perseverance, with courtesy, with the recognition that we are all, each one of us, whether government official or radical (one who gets to the roots of things), children of God.

We do believe that we are all brothers and sisters.

We believe, too, that we can only show our love for God by our love for our brothers and sisters.

So we share our joy with you, our readers, and hope we all have a sense of renewed strength and energy to continue our opposition to all violence, to all wars.

Ernest and Marion Bromley pose in front of their home.

Quaker Thomas Watson was seized by the American army during the revolution, and condemned “to be stripped and ironed, and on the next afternoon to be publicly hanged” for refusing to take the continental currency that Congress was using to finance the war, his family was given little hope for him.

“You may go home,” one petitioner was told, “and rest assured your uncle will be hanged.”

But the wife of the prisoner had a warm friend in the landlady of the inn at Newtown; and when was woman’s kindness ever invoked for the relief of suffering, or woman’s tact required in vain?

She was advised not to apply in person for the release of her husband.

The landlady had learned Lord Sterling’s fondness for the creaturely comforts of life; and knew that wine had the effect to soften the severity of his temper.

To take advantage of this disposition, she invited him to a sumptuous dinner.

He did full justice to the delicacies of the table, and willingly partook of the generous old wine, which had been reserved for special occasions.

As the wine warmed the General’s good-nature and disposed him to kindlier feelings, she cautiously introduced the case of the condemned; pitied his condition, cold, and in irons; regarded his treatment as needlessly severe; and at length requested that his fetters might be removed and his clothes restored to him.

He could not resist this appeal of his hostess; and a note was sent to the guard in answer to her request.

The good woman continued her entreaties, and still plied the wine; when, at the proper moment, the wife was introduced.

She fell on her knees before him, burst into a flood of tears, and told him who she was, and, with all the earnestness, feeling, and eloquence of a loving wife pleading for the one she loved best on earth, begged him to spare her husband’s life.

Her entreaties were of a nature hard to be withstood.

He remained some time silent; then, raising her to her feet, he said, “Madam, you have conquered.

I must relent at the tears and supplications of so noble and so good a woman as you.

Your husband is saved.”

He immediately wrote a pardon for the prisoner, and ordered his discharge.

The happy pair now returned to their homes rejoicing.

Such friendly meetings do not always end well.

Quaker Henry Paxson found this out when he was visited by the tax collector some 300 years ago:

Paxson kindly treats [the tax collector] with best he had, and when he had filled his wem, and drank plentifully of good cider, he distrains the plates he had eaten on, and the tankard he so freely toped out of, but the wife begged the tankard, and bid him take something in lieu of it.

In , a delegation of Quakers met with the sheriff, his sub-lieutenants, a judge, magistrates, and a tax collector in their area of Pennsylvania.

They reported:

[We] had opportunity of laying before them the reasons and grounds of our refusal to comply with several requisitions, made for the support of, or that have near connection with, war; and to open our principles, and the consistency thereof with the doctrines of the Gospel, as set forth in the New Testament and pointed out by the prophets, and the inconsistency of Christians oppressing one another for conscience sake.

They generally appeared friendly, and to receive our visit kindly, some of them particularly so; and most of them acknowledged that the prophecies concerning the disuse of carnal weapons, pointed to the Gospel dispensation, and was much to be desired.

We had good satisfaction in the performance of this service, believing truth owned it, and that there is encouragement for Friends to use further endeavors of this kind.

The Rebecca Rioters could be cruel, or even deadly, to the keepers of the toll gates they were destroying.

More frequently, they would allow the keepers a few moments to collect their personal belongings and remove them from the building before they demolished it.

And on some occasions, the encounters were almost cordial:

The gate-keeper begged of them not to destroy the furniture, as it was his own; and his wife and child were in bed, but they might do as they liked with the gate and toll-house.

Rebecca went to the door, and ordered her [Rebecca’s] daughters not to touch anything but the gate and the roof of the toll-house, and not to break the ceiling for fear the rain would harm the woman and child in bed.

In their hurry, however, to unroof the house, one of them slipped between the rafters, and his foot got through the ceiling.

Rebecca expressed her sorrow at the accident, as it might cause inconvenience to the gate-keeper.

They behaved remarkably well to the gate-keeper, and frequently desired him and his wife not to be alarmed, as they would not injure them in the least; but at parting Rebecca desired him not to exact tolls at that gate any more.

There was no more persistent foe of the IRS than Vivien Kellems, but:

Miss Kellems stresses that she holds no animosity toward the officials who enforce the tax laws.

When IRS Commissioner Johnnie M. Walker took office earlier she sent him a note outlining their differences but congratulating him on his appointment.

“He sent back a nice thank you note,” she said.

During the tax resistance campaign for women’s suffrage in Britain, good relationships between the resisters and the auctioneers who were enlisted to sell off their goods for taxes allowed them to better use these auctions as rally and propaganda opportunities.

On one occasion:

…the auctioneer opened the proceedings by declaring himself a convinced Suffragist, which attitude of mind he attributed largely to a constant contact with women householders in his capacity as tax collector.

When Kate Raleigh’s property was seized by the tax collector:

Miss Raleigh naturally made use of the occasion for propaganda purposes, conversing with the tax collector for some time on the subject of Woman Suffrage, and presenting him with Suffrage literature, which he accepted.

Before taking his leave he expressed himself as, on the whole, in favour of women’s claims to enfranchisement.

The movement against Thatcher’s Poll Tax initially tried to reach out to the councils who were responsible for setting the budgets that implemented the tax, and to the labor union representing the tax collectors who would be enforcing it, to ask them not to cooperate.

However, this met with very little success.

War tax resister Robin Harper met with a tax auditor and a “frivolous tax coordinator” at an IRS office in .

He described how it went:

I quickly assured them that an accurate accounting should of course be established, but that in no way could I alter my refusal to deliver my tax dollars into the U.S. military machine.

Earlier I had described how my Conscientious Objection was rooted in our Quaker Peace Testimony and how I had performed two years of civilian alternative service with a self-help housing project during the Korean War.

With his defensive posture evaporating, Mr. Means [the “frivolous tax coordinator”] told us that his father fought in the Korean War and came home tormented by post traumatic stress disorder.

Thereafter he would have nothing more to do with guns, “because he had seen what guns can do.”

That gave my supporter, who had lived through World War Two in Germany, an opening.

Drawing a parallel with my war tax refusal, she pointed out how German income taxes funded the governmental atrocities of the Third Reich.

…

At one point, when I was describing how the International Center has been installing solar water purification units in Central American villages, Mr. Means broadened our discussion, noting that the scarcity of safe water is becoming a global problem.

In my followup letter to our interview, I sent him a copy of an eye-opening article from the Resist newsletter discussing this issue in depth.

Near the end I took the opportunity to unfurl the large chart which chronicles my war tax redirection these past forty-one years and to describe how I was first propelled into war tax protest by U.S. nuclear atmospheric bomb testing in Nevada and the Pacific.

After more than three hours (and well past normal lunchtime), the two finally closed the interview with smiles and friendly handshakes.

Mr. Means even admitted that his title of “Frivolous Tax Coordinator” was really a substitute for “Tax Protester Coordinator,” an internal administrative category which Congress had abolished in recent Taxpayer Bill of Rights legislation.

Despite their training to be suspicious (all taxpayers are trying to get away with something), IRS folk, like all human beings, can be positively affected by openness, honesty and sincerity.

Transparency can often trump suspicion.

I have learned how we all hunger for caring, person-to-person exchanges.

Look how a one hour audit stretched into more than three hours, much of which involved genuine sharing far beyond the scope of the audit!

As our discussion rose above tax details, Mr. Means, the tax protester “sheriff,” was led to cast aside some of his official person and let his personal feelings and thoughts come through.

He also became increasingly interested in discerning what makes war tax refusers tick.

I am sure he came to understand that our witness is anything but “frivolous.”

Some bits and pieces from here and there:

Peter J. Reilly, who has a blog at the Forbes website, writes about how the IRS labels conscientious objectors to military taxation “frivolous” as a way of discouraging dissent, and how war tax resister Elizabeth Boardman is challenging this in court.

Some developments in the “won’t pay” movement in Greece:

I wish I could read Greek or that mechanical translation were more sophisticated.

This page seems to be describing a tax resistance tactic that involves paying a single euro in road tax to the federal government, accompanied with a letter of protest about how road taxes & fees are being siphoned off by foreign creditors rather than being used to keep the roads in decent repair.

The government is trying to promote a new social norm in which people will be free to refuse to pay for goods and services they receive, unless they are presented with a printed receipt — this in an attempt to crack down on off-the-books transactions.

The government has signaled that it won’t prosecute people who steal from merchants in such circumstances.

The National Taxpayer Advocate (a sort of ombudsman within the IRS) issued her annual report recently.

One bit caught my eye: the Advocate estimates that U.S. taxpayers spend a combined 6,100,000,000 hours per year doing the recordkeeping and filing they have to do to be tax compliant.

Janet Novak, at Forbes, puts that in perspective:

If you file a U.S.

federal income tax return that is inaccurate or incomplete and you justify

this by taking explicit positions that the

IRS has

ruled to be legally “frivolous,” the agency can hit you with an instant $5,000

frivolous filing penalty.

So, for instance, if you were to take a “black tax credit” or “war tax

deduction” on your 1040 form, or if you were to submit a blank form along with

a letter claiming that you have a 5th Amendment right not to answer questions

about your finances, you might get hit with such a fine.

But several American war tax resisters found that they were getting fined in

this way even when they submitted complete and accurate tax returns, just

because they accompanied the returns with a letter explaining their reasons

for not paying the complete amount shown as due.

(Here is some background.)

This appeared to be overreaching on the part of the IRS, but it was difficult for war tax resisters to challenge this because the agency demands that you pay the fine before you can appeal it.