How you can resist funding the government →

about the IRS and U.S. tax law/policy →

IRS is not always forthcoming and accurate

The Transactional Records Access Clearinghouse has been a great source of independent information on how government agencies are doing their jobs — looking behind the self-serving spin in the agency reports and doing their own analyses of the data.

For example, every time the IRS puts out a press release about how it’s getting tougher, auditing more people, and isn’t gonna be taken for a sucker no more no how, TRAC crunches the numbers and puts out its own release saying that as far as they can see, the IRS is the same paper tiger it’s been for years.

(For example, see , and .)

The IRS, naturally, would like to figure out a way to get this pesky child to stop pointing out the nudity of the emperor.

They think they’ve finally found the solution in that universal solvent of transparency in government — the War on Terror:

The lawsuit is part of an ongoing effort by the Transactional Records Access Clearinghouse (TRAC) to obtain statistical information from the IRS about enforcement actions.

Reversing 30 years of policy, the IRS under the Bush administration has stonewalled requests for public disclosure of such information.

The IRS is having a rough go of it.

It’s new plan to use private debt collectors is being denounced as a boondoggle, its information technology infrastructure is crumbling in such a way as to have cost them over $300 million in fraudulent refunds it has been unable to retrieve, and it has been caught inflating the numbers of audits of the wealthy by making those audits automated and superficial (and easier to hide assets from).

Oh yeah, and their headquarters is closed due to flood damage.

Some short bits from here-and-there around the web:

The Get Rich Slowly blog recently highlighted Don Schrader, a low-income / simple-living war tax resister and Albuquerque-area local legend.

At last count, there were 56 comments from people evaluating Schrader’s eccentric and dedicated lifestyle and the principles behind them.

The Colorado Springs Independent covers the war on war tax, and includes quotes from Peter Haney and Esther Kisamore.

Expatriate satyagrahi tax resister Jeff Knaebel delivered a speech at the Gandhi Sixtieth Memorial in Pune .

The text of the speech has been reprinted at LewRockwell.com.

Excerpt:

Complete non-violence today would mean acquiescence in systematic destruction of the whole earth, and thus all of humanity with it.

Some situations demand that we defend our land, our right to livelihood, and our lives with violent defensive action.

Direct Action Today, I feel, however, is best expressed in self-restraint, in the quiet refusal to buy corporate products, in boycott, in self-reliance and in tax refusal, in refusal to report for combat in aggressive war, in refusal to accept corporate and government media propaganda as truth.

I know what “simplified” means in these contexts, and I’m highly aware of being a war tax resister who doesn’t try to live such a life, at least in some senses of “simplified,” and I’m wondering, Where exactly… is there room for me, a war tax resister , “sustainable for the long haul,” and with every expectation of continuing to do war tax resistance as long as I live?

“Simplicity” isn’t… being presented as something to deliberate over; it’s presented as something to “embrace.”

The Internal Revenue Service has serious issues with outdated financial management systems and insufficient information security that could affect the accuracy of its financial statements, according to a Government Accountability Office report released on Wednesday.

The report concluded that the agency’s internal controls were not effective and that it did not comply with legal requirements for federal financial management systems.

The IRS has something called the Federal Payment Levy Program, which is designed to intercept payments coming from the federal government to people who have tax debts.

According to this report, “the bulk of FPLP levy payments have historically been related to Social Security benefits.”

At one point there was a hardship income threshold under which the government would not seize social security benefits to reclaim taxes, but the government phased this out and finally eliminated it at the beginning of .

The Taxpayer Advocate noted that this was further impoverishing some people on fixed-incomes who were already below the poverty line, and proposed a new filter.

The IRS has agreed to implement a “low income filter” that “will exclude taxpayers from the FPLP if their estimated income (based on internal IRS data) is less than 250 percent of the poverty level.”

This change is due to begin in .

The “internal IRS data” the report speaks of here it tries to explain in a footnote:

To compute the taxpayer’s income, where the taxpayer has filed a tax return for the most recent year or two, the IRS will use the greater of the total positive income from that return, or income based on payor documents filed with IRS for that year.

Where no such return was filed, the IRS will use payor documents for the most recent tax year.

To determine family size, which is a component of the federal poverty level computation, the IRS will use the family unit size claimed on the taxpayer’s most recent return filed for the last two years, or if no such return is filed, the IRS will assume a family unit size of one.

Although people with low-incomes may be saved from having their social security seized via FPLP in this way, the IRS may still use other collection techniques.

For instance, they may seize the bank account your social security payment is deposited into, thus saving you from a partial levy only to hit you with a 100% seizure.

Or they may file a “paper levy” to attach 100% of future social security payments until the unpaid tax is collected.

For low-income tax resisters, this will require vigilance.

Still, the Advocate predicts that this change “will protect hundreds of thousands of taxpayers from economic damage and unnecessary interaction with the IRS.”

According to the Advocate, “many of the collection policies and practices in place today have little empirical justification even as they violate the spirit, if not the letter, of the IRS Restructuring and Reform Act of and result in unnecessary harm to taxpayers.

For example, despite the fact that IRS levies and Notice of Federal Tax Lien filings increased by approximately 590 percent and 475 percent, respectively, [see The Picket Line, ], overall inflation-adjusted collection revenue declined by approximately 7.4 percent over the same period.”

The IRS appears to be systematically exaggerating the effectiveness of its collection efforts by attributing any revenue collected during the collection process, even things like subsequent tax refunds being automatically intercepted before they’re sent, as being attributable to the activities of collections personnel.

Also, “[t]here is an astonishing lack of transparency as to what is included in the revenue figures and how they are computed.”

The hardship standards that the IRS uses to determine whether a tax debt is collectible (that is, is there anything to seize, and will seizing it effectively throw the taxpayer onto government assistance, thus robbing Peter to pay Peter) don’t take into account things like credit card debt, school loans, and medical bills.

In many cases, they’re trying to get blood from a stone.

The IRS tends to file official lien notices haphazardly, without much regard for whether they are effective.

Their policy seems to be: when an account reaches a certain threshold of unpaid balance, file a a notice of federal tax lien.

This even though very little collection revenue comes from liens and though a lien notice like this can make it more difficult for delinquent taxpayers to get back on their feet financially.

(These notices make the “secret lien” filed against all delinquent taxpayers part of the public record, available to potential creditors and employers and landlords and such, and put the lien into effect so that the IRS can skim money, for instance if the taxpayer sells property or has accounts receivable.)

Taxpatriatism appears to be rife.

According to the report, “[i]t is estimated that more than seven million American citizens reside abroad.

Although U.S. citizens are required to file U.S. income tax returns regardless of their residency status, IRS data show that only 462,340 taxpayers (or 6.6 percent) filed returns from a foreign address in tax year 2007.”

The “offer in compromise” program — in which people with large tax debts they can’t pay off can enter into an agreement with the government to pay a portion of their debt, comply fully with the tax laws for five years, and have the remainder of their debt forgiven — has become useless for most people.

Now, in order to use this program, you have to pay a fee and submit a substantial down-payment along with your application (which involves “more than 100 steps in a 44-page package”) — and then your application may still be declined.

Weirdly, the IRS processes our 1040 forms before it processes the W-2s and 1099s that substantiate the income we report.

This makes it easy for fraudsters to understate their income and get refunds before the government knows anything is wrong.

“The IRS is experiencing high levels of new individual taxpayer payment delinquencies in categories that could produce high levels of subsequent noncompliance.”

Music to my ears.

I’ve recently come upon an income tax question I didn’t know the answer to:

Let’s say you have the opportunity to rent one room of a two-bedroom house, one room of which is already being rented by someone else.

Maybe you are subletting, or in some other way cooperatively paying the rent on the house as a whole.

You have the opportunity, for an additional amount of rent, to rent an additional, smaller room in the house (one that would otherwise be common space) for exclusive use as an office for your business (you are a sole proprietor who uses Schedule C).

How do you calculate the business expense for this office space rent?

Do you take the full amount of the additional rent as a business expense?

Or, do you consider the extra room a “home office” since it’s in the same building as your residence, and somehow calculate how much of your combined rent can be attributed exclusively to the office — and, if so, how do you make this calculation, especially with another rent-paying housemate in the picture and a mixture of common and housemate-exclusive space in the building?

My first stop was irs.gov, which has some information on the home office deduction.

Unfortunately, nothing I found there seemed to unambiguously consider this particular case.

Their examples all seemed to assume that one person, the business-owner, is also the sole renter or owner of the house or apartment, and is paying a single amount for a single occupancy space, part of which is being converted to business use.

So then I called the IRS telephone assistance hotline.

Four times I called the IRS telephone assistance hotline.

Four times I pressed 1 then 2 then 2 then 3, or maybe 1 then 3 then 1 then 2 then 3.

Four times I talked with someone who heard my question and transferred me to the “small business department.”

And four times I was put on hold, only to be cut off or hung up on after ten, twenty, or thirty minutes of listening to tinny, repetitive muzak.

So I called up my local IRS office, as I’m lucky enough to have one a short bus ride away, and asked to make an appointment to talk with someone about my question.

Two days later they called back to tell me they couldn’t answer questions like mine — that it was “out of scope” for their office.

They recommended I call the IRS telephone assistance hotline.

I told them how that had gone and asked if they had any better ideas.

They had none.

Yesterday I tried to get sneaky and call the IRS “Telephone Assistance for Businesses” line in the hopes that this would get me at least one step closer in the queue.

No such luck.

This time I had to press 1 then 5 then 1, but then had to do the same dance of talking with someone who transferred me to the “small business department.”

A mechanical voice told me the expected on-hold time was “greater than thirty minutes,” but it turned out to be only about 25.

Unfortunately, the woman I eventually spoke with, “Jan” (#0843180), was having phone problems of some sort (or maybe I was), and she had difficulty hearing what I was saying, finally couldn’t hear me at all, then I could no longer hear her either, and after a couple of minutes of frustrating silence, I was cut off again.

All I got out of Jan was 1) that because Congress is still in session, they can’t tell anyone definitively what the law is going to look like when it comes time to file taxes, and 2) the IRS is unwilling to advise me on what the best thing to do would be in this circumstance (I protested that it wasn’t the “best” thing I was looking for, but the “correct” thing).

She had just begun walking me through what sounded like it would be a long, long flowchart (“Were you a U.S. citizen at the end of 2011?”) when our audio troubles became insurmountable.

So now I know what that process feels like.

It’s encouraging to me to know that people who try to deal person-to-person with the IRS are likely to come away from the experience frustrated, infuriated, and yet more cynical about their government and its bureaucracies.

I may try the Taxpayer Advocate Service to see how that process works.

It may be that in the same way that you don’t call up the Justice Department to find out what’s illegal this week, but you’re supposed to hire a lawyer if you’re confused, the correct thing for me to do with tax questions like mine is to consult a tax professional of some sort.

But the IRS seems loth to admit that they’re incapable of helping ordinary people with their ordinary tax questions (and mine doesn’t strike me as particularly out-of-the-ordinary).

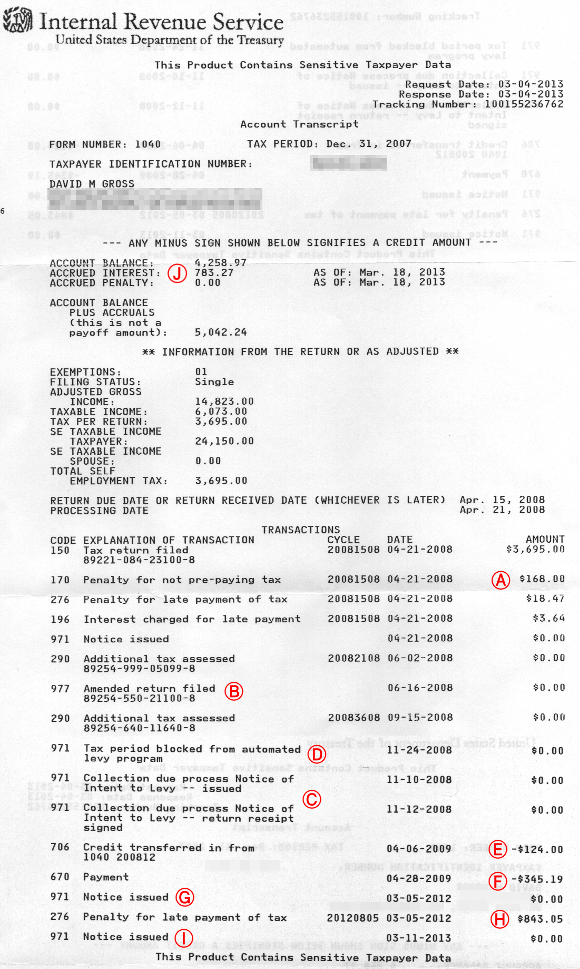

I got four letters from the IRS that purported to sum up my total unpaid taxes, along with interest & penalties, for , , , and .

Their numbers didn’t add up consistently even within their own printouts, though, so I thought I’d dig a little deeper.

I requested my “tax account transcripts” for those years from the IRS.

(This is easy to do: you can request your transcripts from the IRS website.)

They arrived on (in four separate envelopes, naturally, as the agency’s way of reminding me how respectfully it spends taxpayer dollars).

These are interesting artifacts, but in many ways they only add to my bewilderment.

I’ll show you one of the transcripts they sent me below, and add some comments and explanations.

The original transcript was two pages — I’ve pasted them together in this illustration.

I added the red circled letters for my annotations below:

First, a note: In there was

a weird glitch in which the

IRS

erased the “personal exemption” from my

return. Perhaps somebody tried to claim me as a dependent on their tax return,

or accidentally filled in my social security number for that of their actual

dependent, or maybe it was just a snafu — I

never did get an explanation. I simply filed an amended return reinstating

my personal exemption and left it at that. It didn’t effect the bottom line in

any case, so I didn’t give it much thought afterwards.

The transcript shows my initial tax assessment ($3,695.00), the penalty

immediately assessed on me for not having paid any of this in quarterly

installments ($168), the initial late payment penalty for not having enclosed

a check with my tax return ($18.47), and a small amount of interest that had

accumulated at the time of their first delinquency notice to me ($3.64). All

of that matches my records. (Ⓐ)

In June they erased my personal exemption, then took note of my amended return

in which I reinstated it (Ⓑ). I didn’t get

official word that they’d accepted my

amended return until . I think

their phrase for “we changed the numbers on your tax return” is “Additional

tax assessed” since it appears twice on the transcript around here, once to

omit the personal exemption and once to reinstate it, though neither of these

occasions actually resulted in an assessment of additional tax.

On I got an “Intent to Levy” letter from the

IRS for

the tax year. This also does not show up on

the transcript. That letter listed $166.28 in accumulated penalties and $98.46

in accumulated interest, and asserted that my original tax due was $3,885.11

(which actually is the amount of my original tax due, plus the failure to file

quarterly penalty, plus the initial late payment penalty, plus the first

amount of interest that accumulated).

On I got a “final notice of intent to levy” letter. This

is mentioned in the transcript: both the date it was issued, and the

date the

IRS

was notified that I signed for the letter (Ⓒ). By this time, the accumulated

penalties & interest on the original $3,695 tax bill had risen to a bit

over $572.

Here something peculiar shows up in the transcript: “Tax period blocked from

automated levy program” (Ⓓ). This, just two weeks after they’d issued me a

“final notice of intent to levy.” I’m not sure how to interpret this. (Note

also that this appears out of chronological order in the transcript, just from

perverseness I suspect.) There’s also one of these on my

transcript.

When I filed my return in (for the

tax year) I had so little income to report

that I actually was one of those “lucky duckies” who not only owed no taxes

but qualified for a refundable earned income tax credit: a whole $124. The

IRS

seized this refund and applied it to my unpaid

taxes. This shows up on the transcript (Ⓔ).

They also credit me for a “Payment” of $345.19 on

(Ⓕ). This was actually

a levy of a bank account of mine…

so apparently that “block” issued in

had been released or had expired

by then, or perhaps this levy was not one of the “automated” variety.

I got another letter from the

IRS in

complaining about

the unpaid balance, and then

another in

. These don’t show up in the

transcript either.

The

IRS

tried to seize another bank account , but I’d long since closed it. By then, the interest and

penalties had risen to $985.14. Neither an indication of the levy attempt,

nor any amounts of interest & penalties from this period show up on the

transcript.

The next thing that does show up in the transcript, after

, is

a “reminder of overdue taxes” that they

sent me (Ⓖ). This is

accompanied, in the transcript, with a late payment penalty of $843.05 (Ⓗ).

The transcript also notes

the letter it sent me

, though it gets the

date wrong (Ⓘ).

The transcript also has a summing-up section (Ⓙ), which just makes things

worse:

ACCOUNT BALANCE PLUS ACCRUALS

(this is not a payoff amount): 5,042.24

Why does the interest “accrue”, but the penalty just gets added to the account

balance? If they just are going to add the penalty to the account balance, why

do they bother to have an “accrued penalty” line on the transcript? Why, if

this is their policy, do I only have a zero accrued penalty amount on my

and

transcripts, while my and

transcripts do show accrued

penalties?

The account balance does seem to add up to my original tax owed plus

that original set of penalties and interest (Ⓐ), plus the $843.05 in penalties

(Ⓗ), minus what they managed to seize from me (Ⓔ) & (Ⓕ). I can’t tell you

how surprised I was to find some set of numbers on the page that added up to

another number on the page in a semi-intuitive way, though it took me a while

to develop the correct formula, and I couldn’t tell you why they stuff that

original interest amount in there.

I was a little puzzled at first as to why they stopped assessing penalties

, but I think by that point the

penalty had reached its legal maximum — 25% of the unpaid amount. From here on

out there will be no more penalties on my

taxes, though the interest will continue to accrue.

So you may have heard that the

IRS has

been caught targeting overreaching audits at

TEA Party

groups.

I’ll admit that when I first heard these groups complaining that they were

being targeted for their politics, I thought they were probably just being

paranoid and histrionic. Turns out they were right.

There’s somewhat less to the story than the headlines might lead you to

believe. There isn’t much solid evidence that anyone in the White House, or in

the IRS,

was on a “let’s nail the

TEA Party”

kick, exactly.

The IRS

did target groups for their politics, but they did so in the course of trying

to find groups who were illegally politicking while organized as 501(c)(4)

organizations. In other words, they were looking for political groups because

they had a reason to be looking for political groups.

501(c)(4) is a variety of tax-exempt non-profit organization. You cannot be

a 501(c)(4) if your purpose is to do electioneering and other such political

advocacy. But you can if your main purpose is to promote “social welfare,”

even if this occasionally includes political work. Naturally, this fuzziness

has led to a bunch of political groups trying to redefine themselves as social

welfare groups so they can qualify for the exemption. So

the IRS

has wanted to give extra scrutiny to applications from groups that are

attempting to organize under this section to make sure they’re not campaign

funds in disguise.

But the

IRS, as

I’ve been gleefully noting hereabouts, has been struggling with a shrinking

budget and workforce in recent years. During the run-up to the last election,

the agency got a bunch of applications for new 501(c)(4) groups, more than it

could handle, and so it tried to come up with a way of scrutinizing those that

seemed more likely than not to be improperly political groups.

One way they selected groups to scrutinize more closely — and the

IRS

claims that this decision was made by a rank-and-file employee of the

agency — was to see if they had words like “patriot” or

“TEA Party” in

their names. This had the effect of skewing

IRS

harassment toward right-wing critics of the status quo.

501(c)(4) groups also have the advantage (particularly when they are being

used as cover for electioneering) that they do not have to report who donates

money to them, the way political campaigns do. But during the

IRS

inquiries into these right-wing protest groups, the agency asked the groups to

provide a list of their donors, which it was not authorized to do. I haven’t

yet seen a good explanation for how that turn of events came about (a

TIGTA report on the scandal will be released soon, and may have some details).

When these groups initially raised the alarm and said they suspected they were

being targeted, asked inappropriately delving questions, and having their

applications delayed for partisan reasons, the

IRS

flatly denied it was doing anything of the sort. The recent revelations are an

embarrassing walk-back for the agency.