How you can resist funding the government →

about the IRS and U.S. tax law/policy →

IRS incompetence →

enforcement effort/results →

National Taxpayer Advocate reports on

The National Taxpayer Advocate’s office released its annual report to Congress .

There’s a wealth of interesting information in there (well, interesting if you’ve got some tax geek in you).

Some things that caught my eye:

“With regard to IRS’s stepped-up enforcement activity over the past few years, we are beginning to see signs that taxpayer rights are not being protected as well as they have been in recent years, particularly in the collection process.

Perhaps this is almost inevitable when enforcement is ramped up quickly and pressure is applied to program managers to show results, but we believe it is important to highlight our concerns and for the IRS to take our concerns seriously to avoid the risk that the enforcement over-zealousness which plagued the agency in will recur.”

“In , the IRS reported more delinquent tax dollars as ‘currently not collectible’ than it actually collected on active balance due accounts (TDAs), installment agreement accounts, and offers in compromise (OIC) combined.”

“IRS studies and external experts in collection confirm that collection cases 24 months past due generally yield less than 15 cents on the dollar and after three years are practically uncollectible.”

“Some aspects of the [private debt collection] plans reflect dramatic departures from IRS practice and impact taxpayer rights.

We would like to discuss some of the specifics in this report, but the IRS has advised us that much of the information in the PCA operational plans and calling scripts is designated as ‘proprietary information,’ and generally cannot be released without the consent of the PCAs.

The operational plans and calling scripts describe such things as belated Fair Debt Collection Practices Act (FDCPA) warnings and psychological techniques used to coax debtors into paying.”

(The report recommends that the private debt collection initiative be entirely scrapped.)

The IRS has been using an automated process of attaching 15% levies to federal payments to people with tax delinquencies.

Most typically, this is used to seize a portion of Social Security payments.

The IRS has used this power against people well below the poverty line, although for other sorts of levies and seizures it does take financial hardship into account.

IRS

Policy Statement 5-34 provides that, “Collection enforced through seizure and

sale of the assets occurs only after thorough consideration of all factors

and of alternative collection methods” and that “the official responsible for

making the decision to seize must be satisfied that other efforts have been

made to collect the delinquent taxes without seizing.… Seizure action is

usually the last option in the collection process.” Yet,

TAS

is now seeing in its cases an inclination toward seizure despite the

existence of viable alternative collection methods. In addition,

TAS

is witnessing apparent failures on the part of the

IRS

to follow various provisions of the

IRM

regarding the collecting process. For example,

TAS

has seen the

IRS

seek extensions of collection statute expiration dates

(CSEDs) in apparent contradiction to the

terms of

IRM

§5.14.2.1 (). In several

instances,

TAS

has also observed the imposition of a levy on assets in a taxpayer’s

retirement account even though the requisite “flagrant

conduct”* did not appear to be present.

* IRM §

5.11.6.2(5) () (stating that

funds in retirement accounts are not to be levied if the taxpayer has not

engaged in flagrant conduct and providing examples of flagrant conduct,

including taxpayers who make frivolous arguments, are convicted of tax

evasion, are assessed fraud penalties, and hide assets).

And…

The National Taxpayer Advocate is seeing cases in which delinquent tax

accounts have sat for five to ten years without meaningful

IRS

intervention only to be aggressively pursued as the

CSEDs

draw near. Such prolonged periods of

IRS

inactivity significantly exacerbate taxpayers’ delinquency problems due to

the accumulation of interest and penalties.

The IRM

states that seizure should be considered for taxpayers who “won’t pay” and

provides a number of examples of such taxpayers (including “taxpayers who

have the ability to remain current and/or resolve their delinquent taxes

through an alternative collection method but will not do so” and “taxpayers

who will not cooperate with the Service,

e.g., taxpayers that evade contact, will not

provide financial information, etc.”). These examples focus on taxpayers’

present conduct, not their past noncompliance. Yet,

TAS is

seeing a tendency to use the noncompliance that lead [sic.]

to taxpayers’ deficiencies and other past behavior, not the current level of

cooperation and willingness to find a way to resolve the liabilities, to

justify seizure.

The IRS has something called the Federal Payment Levy Program, which is designed to intercept payments coming from the federal government to people who have tax debts.

According to this report, “the bulk of FPLP levy payments have historically been related to Social Security benefits.”

At one point there was a hardship income threshold under which the government would not seize social security benefits to reclaim taxes, but the government phased this out and finally eliminated it at the beginning of .

The Taxpayer Advocate noted that this was further impoverishing some people on fixed-incomes who were already below the poverty line, and proposed a new filter.

The IRS has agreed to implement a “low income filter” that “will exclude taxpayers from the FPLP if their estimated income (based on internal IRS data) is less than 250 percent of the poverty level.”

This change is due to begin in .

The “internal IRS data” the report speaks of here it tries to explain in a footnote:

To compute the taxpayer’s income, where the taxpayer has filed a tax return for the most recent year or two, the IRS will use the greater of the total positive income from that return, or income based on payor documents filed with IRS for that year.

Where no such return was filed, the IRS will use payor documents for the most recent tax year.

To determine family size, which is a component of the federal poverty level computation, the IRS will use the family unit size claimed on the taxpayer’s most recent return filed for the last two years, or if no such return is filed, the IRS will assume a family unit size of one.

Although people with low-incomes may be saved from having their social security seized via FPLP in this way, the IRS may still use other collection techniques.

For instance, they may seize the bank account your social security payment is deposited into, thus saving you from a partial levy only to hit you with a 100% seizure.

Or they may file a “paper levy” to attach 100% of future social security payments until the unpaid tax is collected.

For low-income tax resisters, this will require vigilance.

Still, the Advocate predicts that this change “will protect hundreds of thousands of taxpayers from economic damage and unnecessary interaction with the IRS.”

According to the Advocate, “many of the collection policies and practices in place today have little empirical justification even as they violate the spirit, if not the letter, of the IRS Restructuring and Reform Act of and result in unnecessary harm to taxpayers.

For example, despite the fact that IRS levies and Notice of Federal Tax Lien filings increased by approximately 590 percent and 475 percent, respectively, [see The Picket Line, ], overall inflation-adjusted collection revenue declined by approximately 7.4 percent over the same period.”

The IRS appears to be systematically exaggerating the effectiveness of its collection efforts by attributing any revenue collected during the collection process, even things like subsequent tax refunds being automatically intercepted before they’re sent, as being attributable to the activities of collections personnel.

Also, “[t]here is an astonishing lack of transparency as to what is included in the revenue figures and how they are computed.”

The hardship standards that the IRS uses to determine whether a tax debt is collectible (that is, is there anything to seize, and will seizing it effectively throw the taxpayer onto government assistance, thus robbing Peter to pay Peter) don’t take into account things like credit card debt, school loans, and medical bills.

In many cases, they’re trying to get blood from a stone.

The IRS tends to file official lien notices haphazardly, without much regard for whether they are effective.

Their policy seems to be: when an account reaches a certain threshold of unpaid balance, file a a notice of federal tax lien.

This even though very little collection revenue comes from liens and though a lien notice like this can make it more difficult for delinquent taxpayers to get back on their feet financially.

(These notices make the “secret lien” filed against all delinquent taxpayers part of the public record, available to potential creditors and employers and landlords and such, and put the lien into effect so that the IRS can skim money, for instance if the taxpayer sells property or has accounts receivable.)

Taxpatriatism appears to be rife.

According to the report, “[i]t is estimated that more than seven million American citizens reside abroad.

Although U.S. citizens are required to file U.S. income tax returns regardless of their residency status, IRS data show that only 462,340 taxpayers (or 6.6 percent) filed returns from a foreign address in tax year 2007.”

The “offer in compromise” program — in which people with large tax debts they can’t pay off can enter into an agreement with the government to pay a portion of their debt, comply fully with the tax laws for five years, and have the remainder of their debt forgiven — has become useless for most people.

Now, in order to use this program, you have to pay a fee and submit a substantial down-payment along with your application (which involves “more than 100 steps in a 44-page package”) — and then your application may still be declined.

Weirdly, the IRS processes our 1040 forms before it processes the W-2s and 1099s that substantiate the income we report.

This makes it easy for fraudsters to understate their income and get refunds before the government knows anything is wrong.

“The IRS is experiencing high levels of new individual taxpayer payment delinquencies in categories that could produce high levels of subsequent noncompliance.”

Music to my ears.

A few more things of interest that passed through my RSS aggregator and email inbox while I was away:

George Monk and Molly Schaffnit went off-the-grid and back-to-the-land, motivated in part by their desire to live under the tax line on a lower income to avoid contributing to the U.S. military.

The Charleston Daily Mail tells their story. Also: they have a web site.

The “National Taxpayer Advocate” (a sort of IRS ombudsman position) released her annual report on .

As was the case in her report last year, she complained that the IRS is overusing its enforcement techniques of levies and liens in ways that are cruel and, even from the perspective of government revenue, counterproductive — , the number of liens the IRS has filed each year has increased by 550%, but the amount of revenue collected through such enforcement efforts has not increased at all.

“By filing a lien against a taxpayer with no money and no assets, the IRS often collects nothing, yet it inflicts long-term harm on the taxpayer by making it harder for him to get back on his feet when he does get a job,” Taxpayer Advocate Nina Olson said.

“Absent data that show liens make a meaningful contribution to revenue collection and especially in this economy, I find it unacceptable that the IRS continues to torment financially struggling taxpayers in this way.”

The government of Romania is threatening to tax the nation’s witches, astrologers, and fortune tellers.

Curse them!

A dozen witches will hurl the poisonous mandrake plant into the Danube to put a hex on government officials “so evil will befall them,” said a witch named Alisia.

She identified herself with one name — customary among Romania’s witches.

Queen witch Bratara Buzea, 63, who was imprisoned in for witchcraft under Ceausescu’s repressive regime, is furious about the new law.

Sitting cross-legged in her villa in the lake resort of Mogosoaia, just north of Bucharest, she said she planned to cast a spell using a particularly effective concoction of cat excrement and a dead dog, along with a chorus of witches.

“We do harm to those who harm us,” she said.

“They want to take the country out of this crisis using us?

They should get us out of the crisis because they brought us into it.”

The IRS says that it’s implementing new processes that ease up on the liens it files against people who haven’t paid their federal taxes.

This includes raising the tax-debt threshold at which the agency decides to file a lien, making it easier for newly-recompliant taxpayers to have their liens lifted, and making it easier to enter into installment agreements and “offers in compromise.”

This was partially in response to complaints from the Taxpayer Advocate’s office about the agency’s heavy-handed and counterproductive enforcement methods.

The National Taxpayer Advocate released its 2013 Annual Report to Congress today, in a flashier and more public-facing package than I remember it using in the past.

The report identifies how funding cuts, increased responsibility, and Congressional hostility to the agency have put the IRS in something of a crisis state:

Throughout the Most Serious Problems section of this report, we recount the ways in which chronic underfunding drives the agency to develop short-term solutions that merely patch over problems and impose unnecessary burden and even harm on taxpayers.

These short-term solutions also create more work for the IRS in the end…

Agency budget woes are a theme that runs through the document, and this is highlighted as its own “Most Serious Problem” — “The IRS Desperately Needs More Funding to Serve [sic] Taxpayers and Increase Voluntary [sic] Compliance.”

That problem statement describes the funding crunch this way: “Since , the IRS budget has been cut by nearly eight percent.

Over the same period, inflation has risen by about six percent, further eroding the IRS’s resources.”

Meanwhile: “the workload of the IRS has increased significantly.”

This has led the agency to cut way back in what it calls taxpayer service (responding to phone calls and letters, providing walk-in consultation, answering questions about tax laws and regulations).

It has reduced its staff by 8% in recent years (including 12% and 21% reductions in its number of Revenue Agents and Revenue Officers respectively), and slashed its training budget by 87%.

The Taxpayer Advocate notes that this is likely to lead to reduced tax collection, and that this will largely be not because a lack of enforcement personnel means that more tax evaders will get through the net, but because poor “customer service” and increasing IRS clumsiness will make the mass of compliant taxpayers more cynical about taxpaying and more likely to try to get away with something.

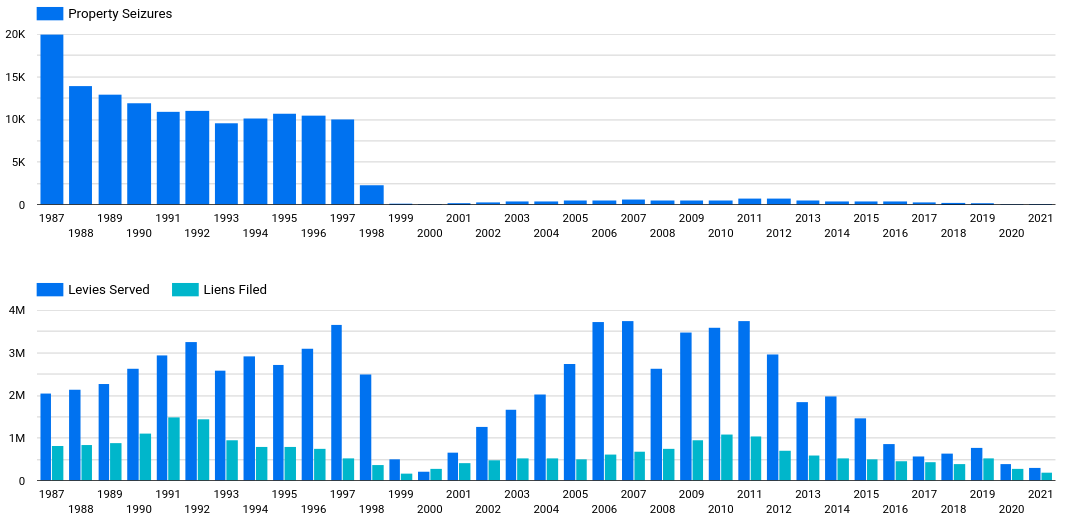

Some preliminary numbers on liens and levies are embedded in the report, so I can update my charts:

It tells of “a devastating erosion of taxpayer service,” and a “lack of effective administrative and congressional oversight” combined with “the failure to pass Taxpayer Rights legislation,” that “is reshaping U.S. tax administration in ways that are not positive for future tax compliance or for public trust in the fairness of the tax system,” and furthermore “we need fundamental tax reform, sooner rather than later, so the entire system does not implode.”

In other words: mostly good news this year.

The report is charmingly earnest, and imagines that it is addressing a Congress that has a genuine interest in improving the functioning of the U.S. government and the lives of its subjects, but has somehow lost its way.

As an example of this naïveté, one of the Taxpayer Advocate’s recent success stories, by its standards anyway, was when it convinced the IRS to issue a “Taxpayer Bill of Rights” — one which didn’t actually give taxpayers any rights, but just tried to list the ones it thought taxpayers ought to believe they have.

Since then, the actual experience of taxpayers has declined for just about every item in the Bill.

One thing the new report emphasizes is that the IRS’s inability to do its job is a problem that compounds with time — “the tax system goes into a downward spiral” as the report puts it.

When the agency is late responding to letters, or can’t be reached on the phone (the IRS projects it will answer fewer than half of incoming calls this year, and those only after on-hold waits exceeding half an hour, and even then it will refuse to answer any but the most basic questions), or doesn’t staff its walk-in sites, citizens get frustrated and either don’t bother to pay or file, or they make up their own answers to the questions they have — often incorrect or conveniently taxpayer-favorable ones.

Both scenarios create more work for the IRS and add to their backlog.

Furthermore:

The erosion of taxpayer trust is an even more serious matter than the erosion of taxpayer service, because with the provision of adequate funding, declines in taxpayer service can be reversed.

Not so with declines in trust — once lost, trust takes a very long time to be regained.

For a taxpayer whose trust has been shaken, each IRS failure to meet basic expectations (e.g., answer the phone…) confirms the belief that the IRS is not to be trusted.

In Congress told the State Department to deny passports to, and revoke passports from, people with large federal tax debts.

But I have yet to hear about anyone actually having their passport revoked or denied because of this.

Here’s an update on the policy, from the Taxpayer Advocate Service’s Annual Report to Congress, that explains why:

In , Congress passed the Fixing America’s Surface Transportation (FAST) Act, which requires the Department of State to deny an individual’s passport application and allows the Department of State to revoke or limit an individual’s passport if the IRS has certified the individual as having a seriously delinquent tax debt.

Although the IRS does not plan to implement the passport certification program until , the proposed IRS procedures and policies raise concerns about how the program will harm taxpayers and infringe upon their rights.

Currently, an estimated 270,000 taxpayers meet the criteria for a seriously delinquent tax debt and do not meet one of the statutory exceptions or discretionary exclusions to certification.

The IRS expects to certify 2,700 taxpayers when it initially implements the program in , and continue with certifications throughout the year in phases based on taxpayer response rates.

At this time, the IRS will not be sending recommendations or requests to the Department of State to revoke taxpayers’ passports; although, the Department of State will revoke passports in accordance with its longstanding procedures.

This suggests to me that if you have such a tax debt (defined as one in excess of $50,000 $51,000), you may want to file an expedited request to renew your passport as soon as possible.

They may renew your passport before the IRS gets around to sending in your name, and may not get around to filing a revocation recommendation any time soon.

If you wait, however, you may find it difficult to renew your passport when it expires.

The Taxpayer Advocate Service, by the way, is very critical of how the IRS is implementing the program.

It concludes:

Taxpayers have a constitutional right to travel, and the IRS risks abridging this right by declining to adopt additional taxpayer protections, such as stand-alone pre-certification notices that provide taxpayers with the right to challenge the IRS’s position and be heard.

(That italicized phrase comes from the Taxpayer Bill of Rights which the IRS adopted as a sort of aspirational or public-relations document in lieu of adopting actual policies to protect taxpayer rights.)

Some recent links of note:

NWTRCC kicked off this year’s federal tax filing season with a panel consisting of the experienced war tax resisters Kathy Kelly, Sam Yerger, Erica Leigh, Charlie Hurst, and Maria Smith, who explained their approaches to resistance and took questions from a live audience.

You can view a video of the panel and the Q&A here.

[S]uppose… that the governor of a state like Texas or Florida were to say: Citizens of this state should not pay federal taxes this year, and our state will indemnify its citizens against federal prosecution. In other words, the state would assume the federal tax bill for its own citizens, and declare it null and void.

Meanwhile, one of the more unhinged Trumperists decided it would be a good idea to publicly tweet an increasingly violent series of fantasies including threatening the life of a traffic cop, killing Nancy Pelosi, running over “a million people” in a speeding car, and… bombing the IRS headquarters.

That last bit got him indicted on federal charges.

TIGTA has released another report on the federal government’s use of private debt collection companies to pursue unpaid taxes.

The report says that the companies recovered a mere 1.79% of the unpaid taxes they were assigned, and that more than a third of the money collected went to cover costs and profit for the private companies, with the remainder going to the Treasury.

The National Taxpayer Advocate also released its report recently.

It highlights some of the many problems the IRS had to cope with and/or exacerbate during the year of pandemic shutdowns and greater-than-usual government dysfunction.

For example:

Taxpayers got misleading tax notices that included deadlines to respond that had already passed by the time the notice was sent.

People who tried to call the IRS were able to get through to an agency employee less than 25% of the time.

Taxpayer records are processed on “the oldest major IT systems in the federal government,” but Congress has appropriated only about 8¼% of the estimated cost of updating them.

Hey, what do you know?

Another tax strike is brewing in South Kivu.

This strike, which is scheduled to start in , is meant to pressure the government to repair roads and bridges in the region.

Democrats in Congress are having more trouble than expected getting everyone in and out of the clown car.

The upshot is that the painstakingly-negotiated “Build Back Better Act” is in jeopardy — along with the $80 billion in new IRS funding that was part of the bill.

was surely the most challenging year taxpayers and tax professionals have ever experienced — long processing and refund delays, difficulty reaching the IRS by phone, correspondence that went unprocessed for many months, collection notices issued while taxpayer correspondence was awaiting processing, limited or no information on the Where’s My Refund? tool for delayed returns, and — for full disclosure — difficulty obtaining timely assistance from TAS.

, examination coverage has decreased, enforcement efforts have been negatively impacted, and the Level of Service has continued to drop as the IRS’s workforce and budget have declined.

On the resources side, the IRS’s baseline budget has been reduced by about 20 percent on an inflation-adjusted basis , and its workforce has shrunk by about 17 percent.

There is no way to sugarcoat in tax administration: From the perspective of tens of millions of taxpayers, it was horrendous.

[T]he number of individual income tax returns the IRS receives — a reasonable approximation of its workload — has increased by 19 percent , while its baseline appropriation on an inflation-adjusted basis has decreased by nearly 20 percent.

This imbalance has left the IRS without enough resources to meet taxpayer needs, let alone to invest in additional personnel and technology.

The IRS has not finished processing millions of original and amended returns from , even though returns will soon arrive for processing.

According to the Department of the Treasury, the gross tax gap — the difference between taxes paid and taxes owed — is estimated to have totaled about $580 billion in , up from an estimated amount of nearly $440 billion in , and is expected to rise to about $7 trillion by if left unaddressed.

Processing a paper-filed return is significantly more expensive for the IRS than processing an e-filed return due to the costs associated with training, recruiting, and staffing for manual data transcription.

In fact, the cost to process a paper-filed Form 1040 in was $15.21, which is substantially higher than the $0.36 cost to process an e-filed return.

The report also included some totals for levies, liens, and seizures, so I can update these graphs:

More excitement from the human war on traffic ticket robot cameras, as fire, spray paint, and other sorts of sabotage knocked cameras out of commission in France, Germany, and Italy in recent weeks.

Some tabs that have slid through my browser in recent days:

At the NWTRCC blog, tax resister William E. Ruhaak shared his experience trying to get the government to acknowledge his carefully-drafted, personal “statement of conscience.”

He fought a determined pro se legal battle to get the U.S. Tax Court to admit his statement of conscience as evidence in his tax appeal.

He believes such a struggle is important in order to defend “The fundamental human right to publicly express an opinion or belief.

And also the right to have a written expression of that belief included in government documentation for future reference.”

The Court eventually gave in and added his statement as a piece of evidence, but seemingly only to humor him.

The ruling in his case reads in part:

We nevertheless admonish petitioner that instituting future proceedings before the Tax Court for the purpose of advancing frivolous arguments relating to his conscientious objection to the payment of Federal taxes is likely to result in the imposition of a significant section 6673 penalty against him.

We recognized four decades ago that “there has been a long and undeviating parade of cases in this and other courts” rejecting the arguments of conscientious objectors who sought to avoid paying “the part of their taxes which they estimated to be attributable to military expenditures and to which they objected because of their religious, moral, and ethical objections to war and because of their claimed ‘rights’ under various constitutional provisions, the Nuremberg Principles, international law, and numerous international agreements and treaties.”

Greenberg v. Commissioner, 73 T.C. 806, 810 ().

At this late date, the Court will not condone the continued assertion of similar frivolous positions in meritless litigation that wastes both its own limited resources and those of the IRS.

The War Resisters League has released its annual “Where Your Income Tax Money Really Goes” pie chart fliers, based on the Biden Administration’s proposed budget for .

As Pentagon spending continues to rise, and yet more millions are being spent to arm Ukraine, pie chart aficionados may be surprised to see that the military-spending slice of the pie chart seems to have noticibly shrunk this year.

Ed Hedemann and Ruth Benn, who do the research and composition for the pie chart, explain why.

In part, the reason is that they are operating on the proposed budget, not whatever budget (and supplementary appropriations) Congress will eventually, tardily enact.

The Biden Administration’s proposed budget is chockablock with a wish list of non-military spending that Congress will probably not enact.

The absolute amount of military spending has risen substantially, but relatively it looks smaller because of all that extra wish list spending.

The latest NWTRCC newsletter is out, with a preview of the upcoming tax filing season and other news from the American war tax resistance scene.

The only thing that comes close to the problems we’re seeing now at the Internal Revenue Service was in 1985, when the agency was rolling out some new technology—technology it’s still using today.

Back then, the processing centers got so behind on their work that employees started hiding tax returns in closets and putting them in bags in the trash.

Now it’s way worse, with the IRS, for the second year in a row, entering the filing season with a backlog of millions of not yet processed returns and pieces of correspondence.

The current National Taxpayer Advocate released an amusing blog post about how pathetic and outdated the IRS processes for handling tax returns are. Excerpts:

When I released my annual report in , I said that paper is the IRS’s Kryptonite and the IRS is buried in it.

The reason paper returns are so challenging is that the IRS still has not implemented technology to machine read them, so each digit on every paper return must be manually keystroked into IRS systems by an employee.

The IRS has announced that it plans to hire thousands of new workers to try to deal with its paperwork backlog.

But, in a tight labor market, and unable to offer competitive pay rates to compensate for the soul-crushing tedium ($15.61/hour anyone?), they’re finding it a challenge to turn those plans into personnel.

The Washington Post took a look at a recent job fair the agency held.

IRS employees don’t follow the rules on paid time-off, with a suspicious pattern of sick leave days allowing employees to make their own three-day weekends and extended holidays.

Catalan separatist group / government-in-exile Council for the Republic is promoting a tax redirection campaign in which Catalan citizens withhold the portion of their taxes that would go to the Spanish monarchy or to its repression apparatus, and give that money instead to Front Republicà d’Acció Solidària or some such group working for Catalan independence.

Doomed, quixotic, gonzo tax resister John McAfee is trying to get in the last word by means of a set of interviews he gave when he was on the run from the law.

In them, he explains why he stopped paying. Excerpts:

I’d just had enough.

I’d paid $50 million in income tax over the years.

I thought that was plenty.

I hadn’t paid tax since I went to Belize, but technically, as an American citizen, even if you’re not living in the country, using the services and driving on the roads, you still have to file and pay 30% of your income to the United States.

The only two countries in the world that enforce that rule are the United States and Eritrea!

How [frigging] bizarre is that?

Anyway, I just said, “I’m sorry.

This is insane.

I’m not doing this anymore.”

[I]n America, income tax is in fact unconstitutional anyway.

It was only ever created to fund the war effort in , but that edict, like many others, was never extinguished after the need for it ceased to exist.

I was telling people that I thought taxes were illegal, and if they also felt that they were illegal and/or unjust they should just stop paying, too.

Not just that, I was showing them how to do it without getting caught.

I stumbled somehow on the No Obligation Challenge website.

It looks like a U.K. version of the familiar U.S. tax protester song-and-dance (“Did you know there is no law obligating you to pay council tax?”) but I was impressed by the quality of the graphic design and layout of the website, which is head and shoulders above what I usually see from that segment of the fringe.

In the latest U.S. Taxpayer Advocate report to Congress, the Advocate crunches the numbers and says they simply do not support the claims of IRS brass that they’re on top of things and will have the tax return backlog whittled down by next year’s tax season.

Looking just at the 1040 (income tax) forms, she writes:

As of late , the IRS had a known backlog of 8.2 million paper Forms 1040, and it may end up receiving as many paper tax returns this year as it received last year (17 million).

Processing has been comparatively slow.

As of , the IRS had processed a weekly average of 242,000 paper Forms 1040 over .

As of , the IRS had processed a weekly average of 205,000 paper Forms 1040 over .

That represents a productivity decline of 15 percent from April to May.

If the IRS were to process paper Forms 1040 at its current rate of 205,000 per week over a 52-week year, it would only process 10.7 million returns in a full year.

To work through its current Form 1040 paper inventory and the additional Form 1040 paper returns it will receive as we approach the extended filing deadline of , the IRS would have to process far more than 10.7 million returns — and do it in less than half a year.

It likely would have to process well over 500,000 Forms 1040 per week to eliminate the backlog this year.

The math is daunting.

She notes that the agency does not expect to begin processing ’s paper-filed 1040 forms until , more than five months after those returns started to arrive.

Looking at paper returns in general:

For , the backlog of unprocessed paper tax returns stood at 20 million.

At , the backlog had increased to 21.3 million.

This photograph of the cafeteria of an IRS facility in Austin, Texas, shows some of this immense backlog of paper returns.