Tax resistance in the “Peace Churches” →

Quakers →

20th–21st century Quakers →

the American Friends Service Committee

War tax resistance in the Friends Journal in

By , though there was still no consensus in the Society of Friends about whether paying taxes was the right thing to do (and if not, how best to resist it), the issue had become impossible to avoid.

The issues of the Friends Journal published that year reflect this, with most of them including at least a mention of war tax resistance or of the dilemma for Quaker taxpayers.

War tax resistance was again on the agenda of the Philadelphia Yearly Meeting’s annual conference , but the Journal only includes the topic in a list of “special concerns” that were covered on , without giving any details of how the conversation went.

In the opening article in the issue, “Tithing for Peace” by Alan Strain, the author expresses his anguish over how much he has “tithed for war and instruments of war… several dollars each day to create a warfare state in which fear and violence have become ever more accepted and expected.”

However: “I cannot see how to disentangle myself from this madness… I cannot even see a way to end my involuntary tithing for war.”

Rather than resist the war tithe, he has decided to try to match it with a peace tithe: “giving this amount to private or public agencies working to remove the causes of war and to develop the conditions and institutions of peace.”

In that same issue, a note about the Canadian Friends Service Committee’s humanitarian efforts in Vietnam includes a parenthetical remark that some of the $60,000 donated to the cause came from “two U.S. churchmen who sent money normally used to pay income taxes.”

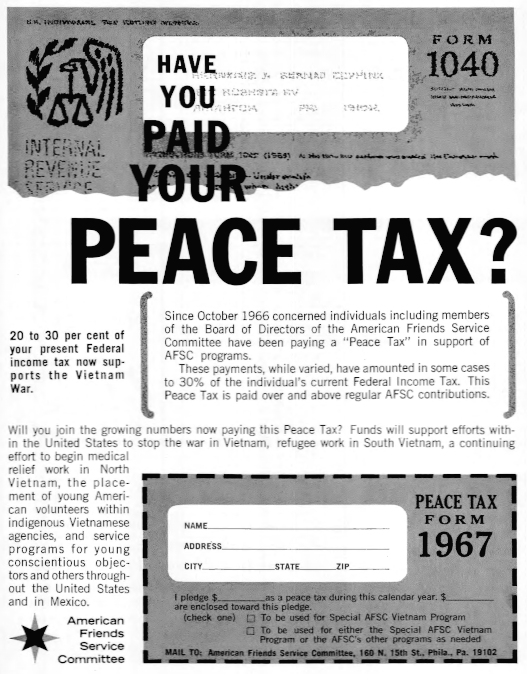

In the issue, the American Friends Service Committee tried to capitalize on the new craze with this ad:

In the Baltimore Yearly Meetings approved a minute “including refusal to pay the surtax for the war if such a tax is imposed.”

An article by Cynthia E. Kerman on “The Rationale of Protest” in the issue made note in passing of the communicative possibilities of war tax resistance: “Tax refusal, for instance, may be a means of speaking to people — not only of purifying our lives.”

In the issue, a letter from Lucy P. Carner picked up where Cynthia E. Kerman left off, asserting that there are “possibilities for witness inherent in tax refusal” that are not immediately obvious to people who are looking for a quick fix “to put a stop to war.”

Excerpts:

Tax refusal enables one to “speak truth to power.”

A letter to the Revenue Service protesting the tax, but paying it, is likely to get less attention than one explaining why one is not paying a portion of the tax.

In the latter case, the Revenue Service has to do something about it.

A representative of the service has to make a telephone call reminding the taxpayer of his delinquency.

Here is another opportunity to witness.

“You mean you do not intend to pay?” said the incredulous voice of the representative.

I explained to him what I had already written to his office.

“Yes, I know that you will eventually get the money from my bank.

That isn’t your fault and you have very courteously fulfilled your duty.

But this is my way of saying that I think the war is wrong.

Only for that reason would I break the law — I’m not accustomed to breaking laws.”

“Yes,” said he, rather helplessly, and hung up.

A few months later a bank official will send a letter saying how much the bank would regret allowing the tax collector to take money from my account and won’t I please pay up and avoid this embarrassment.

Here is another opportunity to write my objection to the war.

Refusal to pay the additional Federal tax on my telephone bill provides similar opportunity to make my voice heard.

Tax refusal, then, is a manner of speaking to government officials, to banks and business concerns.

It is a nonviolent way of reaching the hard-to-reach, for it has nuisance value.

It deserves wide consideration as one way of bearing witness to one’s conscientious objection to war.

The lead editorial in that same issue, by Ruth A. Miner, suggests that instead of resisting war taxes, Quakers should pay an additional tax — “the same amount (or a practicable fraction of it — or even more!)”

— to the United Nations.

This, she suggests, would be in the spirit of Jesus’s suggestion that “whoever compels you to go one mile, go with him two.”

That issue was also the first to feature the ad from “Southern California Business Service” (see ♇ 1 July 2013) that included the message: “A word about tax refusal: Since we limit our income to avoid paying income tax, our rates are low — and — in hiring our help we actively seek out C.O.s and/or tax refusers.”

Phone tax resistance

James B. Osgood, in a letter-to-the-editor in the issue, takes note of the American Friends Service Committee’s “stickers which one can attach to one’s phone bill to make payment of the war tax under protest” (see ♇ 13 July 2013).

This form of protest is better than nothing, but its practical effect is next to nothing.

No real witness is made; no war funds are withheld from the government; no one’s reputation is put on the line.

Those of us who have refused to pay the ten per cent tax hope that others joining us will make a great visible witness and will cause sufficient trouble to the government to give it pause for thought over both collection and prosecution of those who conscientiously refuse.

This, however, will require a real step forward, not a mere licking of a label.

Maris Cakars of the Committee for Nonviolent Action also wrote in, and his letter appeared in the following issue.

He believed that there were “hundreds” of telephone tax resisters who had not notified the Committee of their resistance, and hoped they would speak up so that the campaign could move on to its next phase: “placing advertisement in newspapers and holding press conferences.

For this phase to have maximum impact it is important for us to have as complete a list of tax refusers as possible.”

The issue announced that the Claremont (California) Meeting had decided to resist the telephone tax on its meetinghouse phone.

In the issue was a letter from a representative of 57th Street Meeting in Chicago, in which they noted that two other Meetings had contacted them about actions they had taken in response to their call for phone tax resistance, and said “we would be pleased to act as a clearinghouse on positions taken by Meetings on telephone-tax refusal…”

In the issue, George Lakey wrote an article about why he was joining the crew of the Phoenix to illegally (by U.S. law) bring humanitarian aid to North Vietnam.

He described the escalation of his activism, from letter-writing and congressman-lobbying to his current action.

Along the way, he says, “I stopped paying the telephone tax.”

War tax resistance internationally

The issue noted that Quakers in The Netherlands had formed a “Conscientious Objectors’ Committee Against Paying Taxes for Defense Purposes” which was trying to come up with some sort of government-approved “peace tax”-style plan.

I got a wry smile out of the closing sentence: “In The Netherlands it is not permitted to affix protest stickers on tax forms; instead one must use a written announcement of protest.”

The fourth Friends World Conference was held .

The “Protest and Direct Action group” there “called upon Friends in countries party to the [Vietnam] conflict to ‘go as far as conscience dictates in withholding support from their governments’ war-making machinery,’ first by direct communication with those against whom the protest is made, and then if necessary by public witness and individual action, including the possibility of refusal to pay taxes for war.”

“Corporate Witness and Individual Conscience”

The lead (guest) editorial in the issue was “Corporate Witness and Individual Conscience” by Lindsley H. Noble.

It cautioned Quaker corporate bodies (like Meetings) that were contemplating civil disobedience actions like phone tax resistance.

For one thing, he says, a Quaker group should make sure to have the consent of all of its members before it takes such a drastic step, something he thinks some groups have been careless about.

Secondly, even if every member of the group consents to civil disobedience, the group as a corporation has a different relationship to the state than individuals do.

While individuals and their consciences predate and arguably supersede the state, corporations are creatures of the state and are therefore necessarily subordinate to them.

Quakers incorporate their meetings in part in order to get government privileges associated with legal incorporation.

“In voluntarily putting ourselves under the law to receive these subsidies do we not morally forego corporately the right to refuse to obey other laws not to our liking?”

If Quakers, as a group, find a law so intolerable that they must disobey it as a group, he says, they should first legally detach themselves — “withdraw from our contract with the state and give up our subsidies before setting out on this path.”

This led to months of discussion in the letters-to-the-editor sections of future issues, in particular:

Victor Paschkis thought that Noble’s argument failed on both points.

First, his call for groups to reach consensus before taking a civilly disobedient stand should be understood for what it is — merely a preference for the law-abiding status quo.

After all, “inaction in a given situation may violate the conscience of some members just as action may violate the conscience of others.”

Secondly, a Quaker Meeting, whether or not it has incorporated under the laws of the state, still has a yet higher allegiance to God that must be taken into account.

Also, what’s the point of having Meetings if they do not have “corporate insight” greater than the sum of their parts?

Stephen G. Cary mirrored some of this: “There are times when inaction speaks to the world as clearly as action.

In these situations inaction does not leave us neutral, but committed by default.

Responsibility is not a one-way street, resting only on Friends who wish an action taken.

Those who oppose the action are committing the Meeting, too.

I do not suggest that the proponents’ views should necessarily prevail; I only want it recognized that responsibility to conscience cuts both ways and requires both sides to search their hearts.”

He is also suspect of the idea that corporate entities have no responsibility to disobey unjust laws: “Does the Nuremburg principle have no bearing on the institutions of society?

I prefer to regard the corporation as the creature of those who create and operate it, and the fact that the state charters it does not make the state its ultimate master.”

Marie S. Klooz also defended “corporate witness” as being not exactly “the witness of a corporation” but the collective witness of the corporation’s “component members.”

Such a thing is not only justifiable, but is particularly important to Quakers: “Each member is supposed to test his light by the corporate light.”

And: “If the light requires social action, it is our duty to labor lovingly with those whose light differs, not to refrain from action.”

It is no more necessary for a Meeting to divest itself of its corporate charter to be civilly disobedient, than it is necessary for an individual to first renounce his citizenship.

Pat Foreman found himself uncomfortable with the peace testimony “as interpreted by most Friends” and thinks Quakers like him “sometimes have the feeling that we are being shunned.”

He wants “to remind Friends that Quakerism is a religion and not a prodigious committee.”

Evan Howe thought that dissenters were asking too much if they were asking Quaker Meetings to give up their corporate privileges in order to engage in civilly disobedient actions under the direction of the “sense of the Meeting.”

Such a “surrender of subsidies, as I see it, while apparently a demand of conscience, is rather a surrender of conscience with the ultimate consequence of destroying the society.

I do not believe that dissent gives anyone that right.”

Norman J. Whitney stressed that “Meetings do have a responsibility for corporate witness if the integrity of our testimonies is to be maintained.

It is not enough to shift responsibility to ad hoc committees or special groups among us.”

Roy W. Moger suggested that Noble had hit on a truth when he suggested that legal incorporation was a sort of “trap” that the Religious Society of Friends had fallen into, “thereby placing our conscience in jeopardy.”:

I wonder if the Religious Society of Friends should not begin to unincorporate and remove itself from the trap into which it has fallen, so that Friends can once more seek dependence upon the Holy Spirit, act under guidance of that Spirit as a corporate body, and not have to say, “As a group we dare not take corporate action [and offend the state] because our corporate life depends upon the State, and we are obligated to obey.

The individual can alone take the risk and break the law of the State if he feels the law of the State breaks the law of God.”

Roger S. Lorenz said that because there is a good argument that the Vietnam war is itself illegal, both under international and under domestic law, what it means for a person (or a corporation) to remain within the law under our circumstances is no easy question to answer.

David Hartsough

Over the years, starting in , David Hartsough contributed several pieces to the Friends Journal touching on war tax resistance:

In the issue, he set out a simple, compelling case for war tax resistance — “is it not our responsibility to set the example and refuse to pay our taxes for the weapons and ammunition which inflict this suffering?”

He also suggested that if enough people were to refuse, the government would probably legalize some form of conscientious objection to military taxation.

In the issue, he paraphrased George Fox’s advice to William Penn: “Pay the military portion of thy tax as long as thou canst.”

He suggested that people begin now by resisting the phone tax, and then prepare to resist “the 69.2 percent of our income taxes which go for war” .

In the issue, he told the story of what happened when an IRS agent came to his office to try to collect his unpaid income taxes.

Excerpts:

We talked about the Nürnburg trials, in which the Americans told the Germans that they should obey their consciences rather than their state.

I told him I felt that when we are bombing and burning people and their homes in Vietnam, I cannot condone this action by paying other people to do it.

“I want to make it clear that I have no argument with you on your position about the war,” he said.

“I do not argue that you shouldn’t follow your conscience.

But it is my responsibility to get this money.”

…he gave me a financial statement to fill out.

I refused.

He reminded me: “It’s my job to get this money in any way I can.

I don’t like to do this, but we can take any property you have — your house, your car, or whatever.”

“I have a bicycle downstairs,” I said, “and the suit I’m wearing.”

“No, no, I wouldn’t take your bike or your suit.”

He also expressed concern about the dangers of the poorer neighborhood where I live — a concern beyond his responsibility.

“I guess I’ll have to do what I believe is right,” I said when he was leaving, “and, friend, you will have to do what you believe is right.”

He left without collecting the overdue tax or taking any of my property.

In the issue, he penned another exhortation: “Let us, like Friends through the years, blaze the trail and set the example for others, rather than wait until there are masses of people taking this action.”

He recommended redirecting taxes to the American Friends Service Committee or the Friends Committee on National Legislation, which “will do a much better job of putting our beliefs into action than does the Pentagon.”

David & Jan Hartsough returned to the Journal in with a letter expressing the same basic argument, and giving some details as to how their tax resistance technique had evolved: “Each year we write a check to the Department of Human Services (rather than the IRS) for the 50 percent of our taxes that we do pay.

Along with the check, we send our 1040 form to the IRS and ask them to spend all that money for healing and education, not for killing.

And the other 50 percent (the war portion), we refuse to pay.

Instead, we contribute those funds to organizations helping to feed the hungry, heal the sick, house the homeless, and work for justice and peace in the world.”

War tax resistance and the American Friends Service Committee in the Friends Journal

The American Friends Service Committee, since its founding in , has been one of the most prominent ways modern American Quakers have tried to put their peace testimony into practice.

But it could be a voice of relative hesitance and conservatism when many in the Society of Friends were adopting war tax resistance.

And I mentioned the AFSC’s weirdly toothless response to the extension of the federal excise tax on phone service to help pay for the Vietnam War effort — to make stickers that people could put on their phone bills reading “The Vietnam War Tax Included in This Bill Is Paid Only Under Protest.”

(See ♇ 13 July 2013.)

Finally, I noted that the AFSC had tried to capitalize on the emerging concern among Quakers about war tax payment, war tax resistance, and war tax redirection, with a full page ad that encouraged Quakers to pay a “Peace Tax” — by calculating some percentage of their federal income tax… not in order to resist or redirect it, but in order to determine an appropriately-sized donation to give to the AFSC.

I dunno about you, but to me all of this looks less like an honest effort to grapple with the issue of taxpayer complicity and more like an attempt to ride a trend as a marketing opportunity.

In , the group decided to confront the issue more directly, though they did it in a peculiar way.

ad from the Friends Journal

Two employees of the AFSC — Lorraine Cleveland and Leonard Cadwallader — asked

the Committee to stop withholding war taxes from their salaries. The AFSC

complied with their request, sort of.

The Committee did not withhold the taxes from the employees’ salaries but

instead “withdrew from its general funds enough to cover funds not withheld”

and sent this to the

IRS

instead. Of course, to the

IRS,

none of that accounting really mattered… the money was money, whether it came

from the AFSC payroll budget or its general fund.

But then the AFSC applied for a refund of this amount.

When the

IRS

denied the refund, the

AFSC filed a lawsuit, claiming that:

For employees “to be forced to pay their war taxes without even the symbolic

gesture of refusal and enforced collection by the Government,” according to

the brief, violates the clause of the First Amendment that guarantees the

free exercise of religion.

(These quotes come from an article in the issue of the Friends Journal.)

This all seems like a strangely convoluted path that tangles around the heart

of the matter without really getting there. I suspect that this weird

dance — refusing to withhold war taxes from their salaries, but then paying

these taxes after all out of a different fund, and then immediately applying

for a refund of the amount paid — was deemed necessary by the lawyers as a

means of establishing

legal standing

that would enable them to successfully file their suit.

Also bolstering their argument about standing, the Committee’s legal brief

explained:

American Friends Service Committee is further aggrieved, and threatened with

irreparable economic injury because valuable, esteemed and loyal employees

have threatened to resign from their employment because the operation of the

withholding taxes has interfered with the expression of their religious

conscientious objection to the support of war, and because contributors have

questioned the propriety of their donations to an organization which acts as

a collector of war taxes.

That’s all well and good, but the First Amendment argument… hoo boy… were they

really arguing that the government is obligated to allow religious people

unfettered access to a “symbolic gesture of refusal and enforced collection”?

Is that what war tax resistance and the Quaker peace testimony are

about? Is that what the First Amendment is about?

Civil disobedience is one thing this legal gambit pointedly wasn’t.

The AFSC

apparently felt a strong need to stay within the law wherever possible, perhaps

because of the sensitive and vulnerable nature of some of their activities, or

perhaps because they worried about alienating donors.

A letter-to-the-editor from Bill Samuel in the

edition of the

Journal expressed impatience with this caution.

Excerpts:

I have known several [people] who would not be a part of a Society so

comfortable and content with the evil ways of the larger society. They are

not impressed with our “Quaker” President [Nixon] who grossly violates Quaker

testimonies and has not once worshiped with Washington Friends.

Often, even worse than the meetings in complicity with evil, are the “social

action” agencies, the prime example of which is the AFSC.

My yearly meeting has seen the evil of investing in war, but not the AFSC.

My monthly meeting refuses to pay the war tax on telephone service, but the AFSC even forbids regions

[the AFSC is structured as a collection of semi-autonomous regional offices]

that wish to follow such leadings from doing so.

An excerpt from an AFSC

board meeting transcript, reprinted in the issue of the Journal, is an example of

the temptation for the otherwise very pragmatic, hands-on group to retreat into

abstractions and mumbo-jumbo when the issue of corporate war tax resistance

came up:

When I think of the Spirit I think of something which ought, in the best of

circumstances, to permeate each large and small action which we carry out

throughout all of our lives. Even at those moments such as the present, where

in terms of a particular issue such as taxes, we want to take some action

which is paramount or transcending, we should take the action in the light of

the whole sense of the destiny of the human spirit, which we perceive as

somehow distilled and clarified at one particular historical juncture or

through one particular individual or corporate action. If one thinks of the

Spirit as a kind of unity, as I do, one has a great deal of difficulty in

dealing with the tax question the way we have been doing… It seems to me that

dealing with such questions of beliefs, one at a time and serially, mocks the

Spirit of totality — it seems, rather, that all these things should somehow

be wrapped up together in the Light.

But meanwhile, the AFSC lawsuit

was making its slow progress through the legal system. According to the

issue of the

Journal:

Others [aside from Cleveland and Cadwallader] testifying for AFSC

were Frances Neely, lobbyist for Friends Committee on National Legislation,

from Washington,

D.C.;

Cushing Dolbeare, Philadelphia; Tom (John T.) Flower, San Antonio,

TX; Henry Cadbury,

Philadelphia, and Bronson Clark, executive secretary of AFSC.

The government presented no witnesses and no evidence.

The Judge ruled in favor of the AFSC.

(Before you get too excited, the Supreme Court ruled that all of the AFSC’s attention to standing issues was for naught, as “The Anti-Injunction Act… prohibits suits ‘for the purpose of restraining the assessment or collection of any tax,’ [and so] bars the relief granted…”

That court reversed the ruling that had been in favor of the AFSC.)

The issue of the Journal trumpeted the initial decision. Excerpts:

AFSC Tax Case:

Decision Supports Peace Testimony

In what may become a landmark case, a United States federal judge has found

it unconstitutional for two Quakers and their employer, the American Friends

Service Committee, to be compelled to support war through taxes withheld from

their income.

“We are of the opinion that the withholding method of collection of taxes

does foreclose plaintiffs’ ability to freely exercise that part of their

beliefs requiring them to refuse to participate in war in any form…” the

judge said. “The tax which is withheld is in fact a tax on their incomes

which means that the support of whichever war we happen to be engaged in is

coming out of their pockets. The ‘support of war’ also includes the payment

of taxes in time of ‘peace’ so long as those taxes are used to support the

military’s defense budget generally. Quakers make no distinction between an

offensive or a defensive war. Both are equally objectionable.”

The judge also ruled that the section of the Internal Revenue Code requiring

AFSC

to in effect act as employer-middleman-tax collector for the government was

in this case unconstitutional. Judge Newcomer ordered the government to

refund $574.09 which AFSC

had paid as taxes for the plaintiffs while the case was pending.

“Quakers have for many hundreds of years taken the position that they could

not engage in war or violence of any kind and could not take the life of

another human being,” the judge said in his 18-page opinion. “In more recent

years this view has come to be known as the ‘peace testimony.’ The peace

testimony is not a negative concept but is rather a positive idea requiring

Quakers generally to strive to make war and violence unnecessary…

“When the peace testimony of individual Quakers comes into conflict with a

governmental requirement, the first step usually taken is to petition the

government to change its position. Quakers worked out such a change and

compromise with respect to alternative service during World War Ⅰ and

thereafter. If such a compromise cannot be worked out then the individual

must re-examine his or her conscience to determine if it is possible to live

with the government’s requirement or if not, then to disobey the law so as

not to violate conscience.”

In commenting about the case, Lorraine Cleveland, who has been refusing to

pay war taxes and has been

raising her concern within the Service Committee even longer, said, “There

has never been any doubt in my mind that the Quaker peace testimony was

protected by the First Amendment, and the confirmation of this by the court

strengthens my conviction that it is improper for me to pay war taxes.”

In an earlier statement prepared for the case, Lorraine Cleveland said her

refusal to support war in any form “has contributed to my own integrity — my

sense of wholeness — by bringing my actions into harmony with my deeply held

beliefs and with the guidance of my conscience. It (also) has kept me

sensitive to my own direct responsibility in relation to war in a world in

which ‘everything is connected to everything else.’ ”

“It has been our position,” said Bronson Clark, executive secretary of

AFSC,

“that the First Amendment protects us as an organization because of our

basically religious character, from acting as a tax collector for the

government in this matter of war taxes. We also believe that we should not be

forced to act as the government’s agent in a middleman role that deprives our

employees of the right to confront the government individually on this issue.”

Cleveland also penned an op-ed about the case that I found in the

Palm Beach Post:

When on

Judge Clarence Newcomer of the federal District Court in Philadelphia ruled

in favor of me and one of my former co-workers and the American Friends

Service Committee in our suit against the United States government, it marked

a turning point in an effort my husband and I began .

Judge Newcomer declared unconstitutional the withholding-tax method of

collecting taxes used for military purposes when, by its operation, it

violated my religious beliefs. He also relieved my employer of any legal

burden of taking those taxes out of my paycheck in consideration of my

conscientious objection to paying such taxes.

This ruling has cleared the way for me now to confront the Internal Revenue

Service as an individual without my employer acting as a surrogate tax

collector for the

IRS

The historic significance of Judge Newcomer’s ruling, though this was not a

class action, is that it is the first judicial recognition of conscientious

objection where war taxes are involved.

Many factors entered into my decision to oppose the Internal Revenue Service’s

collection of war taxes from my paycheck. Perhaps the most momentous of those

was in , when our government

dropped atomic bombs on Japan. This seemed to be the most monstrous evil, and

made me feel that some new and more demanding commitment was required of me.

By I had joined the Society of Friends

(Quakers) and was serving with the American Friends Service Committee in

postwar relief work in Europe where I saw firsthand the devastating effects

of war. When it came time to pay our tax, we

sent with our tax return a check payable to the United States Children’s

Bureau in excess of the amount of tax due and requested that this contribution

be accepted in settlement of our tax liability.

I explained to the government that the dropping of the bombs on Japan has led

me to perceive that I could no longer voluntarily pay taxes for military

purposes. I was willing to make an equivalent payment on an ear-marked basis

to any nonmilitary government agencies that could accept such payments.

, I have resisted

paying war taxes and the

IRS has

attached either my bank account or my salary. In

the board of directors of the American

Friends Service Committee, sensitive to the concern of some of its staff

members, agreed to take action together with me and Leonard Cadwallader,

another Quaker employe, to sue the United States to remove the committee as

the withholder of taxes for military purposes. This led to our successful

lawsuit.

It has seemed to me that a government in a free society should be able to

work out an arrangement so that its departments do not violate the First

Amendment of the Constitution while performing their functions.

This might cause the

IRS

some additional inconvenience, but, as Judge Newcomer said in his opinion:

“The additional cost of collection, if any, is a small price to pay when

compared with the possible frustration of the religious practice of bearing

witness to one’s conscience, which practice has sought the aegis of the

First Amendment.”

The tragedy is that so many individuals and organizations are over-whelmed by

the complications of the governmental bureaucracy and see no way to make an

effective protest on matters of conscience.

There was a single dissenting vote in the Supreme Court decision that

overruled this temporary triumph — that of

Justice William

Douglas, whose dissent sounded remarkably (almost incredibly) sympathetic

to the AFSC argument — going

beyond dissenting on the issue of whether the case could be heard under the

Anti-Injunction Act, and agreeing that the Quaker employees should have been

permitted to resist their withheld taxes. Excerpts:

The sole question on the merits is whether the provision of the Internal

Revenue Code… which requires employers to deduct and withhold from wages

federal income taxes, is constitutional as applied to employees, who on

religious grounds object to the withholding taxes on their salaries which

represent that portion of the federal budget allocated to military

expenditures. They invoke the Free Exercise Clause of the First Amendment, as

they are Quakers who are opposed to participation in war in any form and who

claim that this method of collection directly forecloses their ability freely

to express that opposition, i.e., to bear witness to their

religious scruples.

There is no evidence that questions the sincerity of the employees’ religious

beliefs. Nor is there any issue raised as to whether that religious belief

would give the employees a defense against ultimate payment of the tax. The

District Court held that the withholding was unconstitutional as to the

employees… a conclusion with which I agree.

The withholding process forecloses the employees from bearing witness against

the use of these monthly deductions for military purposes. Under the opinion

of this Court, they are deprived of bearing witness to their opposition to

war — these withheld portions of their salaries pay the entire tax and they

therefore have “no alternative legal remedy.”…

Quakers with true religious scruples against participating in war may no more

be barred from protesting the payment of taxes to support war than they can

be forcibly inducted into the Armed Forces and required to carry a gun, and

yet be denied all opportunity to state their religious views against

participation.… The Court misses the entire point of the present controversy.

The employees are barred from protesting these monthly deductions under the

Court’s opinion.… Here the employees challenge the withholding law as

depriving them of their one and only chance of contesting the

constitutionality of the withholding of the tax as applied to them.…

The religious belief which the Government violates here is that the employees

must bear active witness to their objections to their support of war efforts.

Dr. Edwin Bronner, who qualified as an expert on the history of Quakerism,

gave testimony which… stated: “[M]ost Quakers have considered it an integral

part of their faith to bear witness to the beliefs which they hold. It has

always been the prevailing view that simple preaching of one’s beliefs is not

sufficient, and that one’s actions must accord with and give expression to

one’s beliefs. Many of the employees of the AFSC,

including particularly appellees’ Cleveland and Cadwallader, share this

belief, and for these employees, the operation of the withholding tax, which

leaves them no option as to the payment of the taxes which they

conscientiously question, operates as a direct abridgment of the expression

and implementation of deeply cherished religious beliefs.”

If we are faithful to the command of the First Amendment, we would honor that

religious belief. I have not bowed to the view of the majority that “some

compelling state interest” will warrant an infringement of the Free Exercise

Clause.…

…to construe the Act as the Court construes it does not avoid a

constitutional question but directly raises one. The Act, read as literally

as the Court reads it, plainly violates the First Amendment as applied to the

facts of this case, for “no law” prohibiting the free exercise of religion

includes every kind of law, including a law staying the hand of a judge who

enjoins a law for the collection of taxes that trespasses on the First

Amendment.

…when it comes to the First Amendment and the free exercise of

religion, the mandate is that “Congress shall make no law… prohibiting” it.

The Anti-Injunction Act is a “law”; and the Constitution gives no such

preference to tax laws as to permit them to override religious scruples. May

Congress enact a law that prohibits a minister from preaching if his taxes

are in arrears? Or that disallows the making of a protest to a tax assessment

even though the assessment and payment violate one’s religious scruples?

Until today, I would have thought not. The First Amendment, as applied to the

States by the Fourteenth, bars a tax on the conduct of a religious exercise

by a minority even though that religious exercise is obnoxious to the

majority.… Dicta to the effect that an allegation of unconstitutionality is

irrelevant under the Anti-Injunction Act… — which the Court today elevates to

a holding — were based on the premise that there was an alternative remedy to

the unconstitutional actions. Here, as demonstrated, there is no other

remedy. A refund suit is of no value, since the religious scruples which

these taxpayers invoke relate to their inability to protest the payment, not

to the use of the taxes themselves for military purposes.

A retrospective on the life of Henry J. Cadbury, published in the

issue of the

Journal, opened by recounting an episode from

Cadbury’s testimony in this case:

…Marvin Karpatkin, chief attorney for the plaintiffs, had invited to the

witness stand the man who had presided at the first meeting of the

AFSC, on .

Henry Joel Cadbury had always been a man of slight build. Now at the age of

89½, he appeared frail and wizened, his rather rumpled suit hanging on him,

his manner occasionally hesitant, as though a little confused. He wore a

hearing aid, but although it was turned up to full volume it was still

necessary for him to ask a speaker to repeat himself. Those in the courtroom

who did not know him might have wondered what value his testimony could have.

Speaking slowly and clearly, Marvin Karpatkin led Henry Cadbury through a

recitation of his educational background, including his Ph.D.

from Harvard — a teaching career which included 20 years as Hollis Professor

of Divinity at Harvard — his many published books and essays, his role in

translating a new revision of the New Testament, his six honorary degrees.

Henry Cadbury answered each question with careful modesty, but the onlookers

were impressed, and when he acknowledged, in response to further probing,

that he had met with presidents Wilson, Hoover, Roosevelt, Kennedy, and Nixon,

the lawyer for the defense rather plaintively objected to this line of

questioning. The judge, however, appeared interested and denied the motion.

Switching to peace, the lawyer asked Henry Cadbury to describe the Peace

Testimony, and to tell the court what was meant by the term “bearing witness.”

“Bearing witness means, primarily, I suppose, a vocal expression of your

belief in certain ideals, but beyond that in the consistent expression in

your actions of those ideals.”

“Could you say in a nutshell that it means practicing what you preach?” the

lawyer pressed.

Henry Cadbury’s eyes danced and his face lit up with a delightful,

mischievous twinkle. Those who knew him well realized he had something

amusing to say. “Yes, or only preaching what you practice,” he quipped.

Today, while the AFSC continues to decry the enormous amount of money American taxpayers spend on wars past, present, and future, it also continues to stop well short of recommending any direct action by taxpayers (or even, usually, acknowledging that as an option) — instead it engages in projects to “encourage Congress” and “urge our leaders” to do something about it.

At the upcoming national gathering of NWTRCC at Earlham College in Richmond, Indiana, I’m going to be presenting a summary of the history of war tax resistance in the Society of Friends (Quakers).

Today I’m going to try to coalesce some of the notes I’ve assembled about how the Quaker practice of war tax resistance began to reemerge after the Great Forgetting period.

The Thaw ()

In the Great Forgetting period, Quakers endeavored to overlook that war tax resistance had been an important part of putting the Quaker peace testimony into practice.

But during World War Ⅱ and the opening decade of the Cold War, a largely Christian pacifist war tax resistance movement began to coalesce, which included Quakers, but the most prominent members of which belonged to other denominations.

This movement set the stage for the coming renaissance of war tax resistance in the Society of Friends.

A few of the earliest tax resisters of this period were Quakers.

I’ve already mentioned Mary Stone McDowell, who carried on her resistance from the World War Ⅰ period (the only such example I’m aware of).

There was also Arthur Evans, who was resisting perhaps as early as 1943, making him one of the earliest adopters of war tax resistance in this Thaw period.

But institutionally, the Society of Friends still had little interest in the subject.

In the American Friends Service Committee, a major voice of the practical side of the Quaker peace testimony, put out an influential booklet: Speak Truth to Power: A Quaker Search for an Alternative to Violence.

It mentions war tax resistance only once, and in an 18th century historical overview context, not as an example of a contemporary method of speaking truth to power in search of alternatives to violence.

This is in spite of the fact that the committee that produced the booklet included among its members the war tax resisters A.J. Muste and Milton Mayer.

Instead, the leadership in advocating for war tax resistance and in organizing the fledgling modern war tax resistance movement largely came from outside the Society of Friends.

Some of the more prominent war tax resistance promoters in this important period were Dorothy Day (Catholic) & Ammon Hennacy (often Catholic), A.J. Muste (sometimes-Quaker, but bounced around a lot), Maurice McCrackin (Presbyterian), Ernest Bromley (Methodist, later a Quaker), Ralph DiGia (not religious as far as I could tell), and Milton Mayer (Jewish, later a Quaker).

The work of this emerging group of resisters helped to encourage the remaining Quaker war tax resisters and to remind Quakers that war tax resistance wasn’t only something of the legendary past but was an available testimony to them in the present.

The thaw in the Society of Friends had begun.

One of the first examples of this thaw was a particularly dramatic one.

When four Quaker conscientious objectors in the United States were put on trial for evading the Korean War draft, the judge told them:

“If you are not willing to defend this country, you should leave.”

They took that advice seriously, and began to look for an alternative.

They chose Costa Rica, a country that had abolished its standing army in .

“We wanted to be free of paying taxes in a war economy,” recalls Marvin Rockwell, one of the emigrants.

Seven Quaker families left the U.S. to found the community of Monteverde, Costa Rica, in .

Rockwell later told a Friends Journal reporter:

“I do not feel bad at all paying taxes in Costa Rica.

The largest item in the tax budget is for education.”

At the upcoming national gathering of NWTRCC at Earlham College in Richmond, Indiana, I’m going to be presenting a summary of the history of war tax resistance in the Society of Friends (Quakers).

Today I’m going to try to coalesce some of the notes I’ve assembled about the renaissance of Quaker war tax resistance during the Cold War.

Much of what I have assembled here comes from my close look at the archives of the Friends Journal, the only Quaker publication from this period I have reviewed thoroughly, and so whatever editorial biases that publication may have had may also bias my history of this phase.

There is a lot that happens in this short period of time, and in some places my narrative is going to be condensed into a bunch of bullet-point-like summaries of the rapid-fire events to try to keep up with it all.

The Renaissance ()

The modern war tax resistance movement began in the wake of World War Ⅱ in the United States.

There had been isolated war tax resisters here and there in other places in recent years, and there was a quiet war tax resistance tendency hiding under the surface of the Society of Friends, but things did not come out into the open in any organized and growing fashion until then.

Quakers were not in the forefront of this movement, but Quaker war tax resisters took courage from it, and it wasn’t long before they began trying to reestablish the war tax resistance traditions in the Society of Friends.

The earliest mention of this that I have found from this period concerns Franklin Zahn of the Pacific Yearly Meeting, who was distributing a leaflet on war tax resistance as early as .

A report on the Philadelphia Yearly Meeting that year noted that the subject of war taxes had come up and had led to what sounds like a long and earnest discussion:

Few present felt it right to refuse to pay, nor yet felt comfortable to pay.

Varied suggestions were presented: Send an accompanying letter expressing one’s feeling about war; live so simply that income is below tax level; make no report, but once a year send a check for nonmilitary purposes; engage in peace walks and other minority demonstrations; follow Jesus’ example of rendering unto Caesar the things that are Caesar’s; beware of taking for granted the evils deplored, such as riding on military planes; associate more closely with the Mennonites, who share Friends’ concerns; rise above one’s own shortcomings through personal devotion; work to unite with all Friends Yearly Meetings in refusal to pay taxes.

Nothing can be done unless there is a willingness to suffer unto death.[!]

The blinders put on during the Great Forgetting period were still evident.

An article in a issue of the Friends Journal described “refusal to pay taxes for support of war effort emerging as a new testimony” [my emphasis].

Another article from the same issue, titled “The Quaker Peace Testimony: Some Suggestions for Witness and Rededication” didn’t mention taxes at all.

By this time some Friends in Switzerland had been refusing to pay war taxes (I would guess, under the tutelage of Pierre Cérésole).

In some Quakers in the Pacific Yearly Meeting began to sketch out the initial drafts of a legislative “peace tax” proposal which they envisioned would be a way for conscientious objectors to pay their taxes into a fund that the government could only spend on non-military items.

The idea that there might be a legislative solution that could make tax-paying no longer an act of complicity with war would bob up throughout this period, until, by the end of it, the temptation of lobbying instead of committing to direct action would contribute to the eventual decline of war tax resistance in the Society of Friends.

also, the Yellow Springs Monthly Meeting issued a statement of support for war tax resisters, the first example of new institutional support for war tax resistance in the Society of Friends that I could find from the 20th century.

In there was a burst of excitement about war tax resistance in the Baltimore Yearly Meeting (yet a survey of 350 adults from that meeting found only two or three who were willing to consider actually becoming resisters; whereas almost half of those surveyed were totally unconcerned about their tax money going to the military).

A group of about twenty Quakers, organized by Clarence Pickett and Henry Cadbury, met at the Philadelphia Yearly Meeting to discuss war tax resistance, but they were unable to come up with a consensus statement.

Quaker war tax resister Arthur Evans was imprisoned for three months for his tax refusal.

In the Friends Journal ended what strikes me as a policy of editorial embarrassment about Quakers and war tax resistance by publishing its first article devoted to the practice, and one that also full-throatedly advocated it.

This started a debate in the letters-to-the-editor column and certainly caused more Quakers to confront the question, directly or indirectly.

By the tide was shifting rapidly.

Before this time, individual Quaker tax resisters are unusual enough to highlight individually as being on the cutting-edge; after this, Quaker war tax resistance becomes commonplace enough that individual resisters are exemplars of a larger trend.

In the New York Yearly Meeting promoted war tax resistance in an official statement, and promised financial assistance for any Quakers in the Meeting who might be forced to change jobs or to suffer other financial hardship for their stand.

The statement in part read:

We call upon Friends to examine their consciences concerning whether they cannot more fully dissociate themselves from the war machine by tax refusal or changing occupations.

That was the most concrete advocacy of war tax resistance by a Quaker institution in years.

Franklin Zahn wrote a booklet on Early Friends and War Taxes to reintroduce Quakers to their own history and to further banish the Great Forgetting.

The support from Quaker institutions and publications at this point is often noncommittal and is usually vague about exactly how to go about war tax resistance, which taxes to resist, and how to deal with government reprisals.

There is nothing like the specific, concrete discipline of earlier Quaker Meetings.

This means that Quaker war tax resisters from this period are largely making it up as they go along, conferring with each other informally and organizing, when they are organizing, in groups like Peacemakers, the War Resisters League, and the Committee for Non-Violent Action — that is to say, with non-Quaker groups.

(There was briefly something called the “Committee for Nonpayment of War Taxes” run out of Quaker war tax resister Margaret G. Bowman’s home in , but I have not found much about it.)

Quakers were using a broad variety of tax resistance tactics.

Arthur Evans and Neil Haworth refused to pay some or all of their income taxes or to cooperate with an IRS summons for their financial records.

Johan Eliot redirected twice the amount of his taxes to the United Nations to promote international federalism as a world peace strategy.

Clarissa & Samuel Cooper lowered their family income below the tax line.

John L.P. Maynard and Robert W. Eaton took pay cuts that reduced their incomes to the maximum allowable before federal income tax withholding was mandatory.

Lyle Snyder stopped withholding by declaring three million dependents on his W-4 forms.

Alfred & Connie Andersen stopped filing income tax returns.

Some Quakers fled to Canada as taxpatriates to join the draft evaders there.

Others deposited their taxes into escrow accounts and invited the IRS to seize the accounts while refusing to pay voluntarily.

Lloyd C. Shank advocated “the ‘sneaky’ way” of tax resistance — what many people would call tax evasion — saying “ ‘cheating’ is only an oppressive government’s name for a good man’s refusal to murder.”

Phone tax resistance was beginning to become widespread, and many Quaker meetings began resisting this tax on their office phones (one meeting was unable to reach consensus on resisting the phone tax and compromised by dropping its phone service entirely).

People too timid to resist, and meetings unable to reach consensus on resisting, might instead write their legislators to urge them to enact some form of legal conscientious objection to military taxation.

The most timid groups, like the American Friends Service Committee, urged people to pay taxes “under protest” or to match their war tax payments with additional payments to the AFSC.

Robert E. Dickinson had perhaps the most creative tactic of the bunch.

He designed and built a set of furniture for his home that was formed of interlocking sheets of plywood such that it could be quickly disassembled and hidden away.

He called this “my tax refusal furniture” and meant it to frustrate IRS attempts to seize furnishings from him for back taxes.

Two Quaker employees of two groups within the Philadelphia Yearly Meeting asked their employers to stop withholding income tax from their paychecks, and that Meeting tried to come up with a good policy to follow in such cases.

The fourth Friends World Conference was held in .

The “Protest and Direct Action group” there “called upon Friends in countries party to the [Vietnam] conflict to ‘go as far as conscience dictates in withholding support from their governments’ war-making machinery,’ first by direct communication with those against whom the protest is made, and then if necessary by public witness and individual action, including the possibility of refusal to pay taxes for war.”

U.S. President Johnson called for a 10% income tax surcharge explicitly to fund the Vietnam War.

This would be the first explicit “war tax” (other than, arguably, the phone tax) since World War Ⅱ, and its announcement prompted renewed interest in war tax resistance inside and outside the Society of Friends.

Quakers were, because of this tax, better-enabled to quote the discipline of early Quakers on refusal to pay explicit war taxes as a way of explaining their own stands.

In 203 delegates from “nineteen Yearly Meetings, eight Quaker colleges, fifteen Friends secondary schools, the American Friends Service Committee National Board and its twelve regional offices, and nine other peace or directly-related organizations” met in Richmond, Indiana, to draft a “Declaration on the Draft and Conscription.”

Part of this declaration mentioned the war tax concern:

We call on Friends everywhere to recognize the oppressive burden of militarism and conscription.

We acknowledge our complicity in these evils in ways sometimes silent and subtle, at times painfully apparent.

We are under obligation as children of God and members of the Religious Society of Friends to break the yoke of that complicity.

We also recognize that the problem of paying war taxes has intensified; this compels us to find realistic ways to refuse to pay these taxes.

After only of thaw, some seventy years of Great Forgetting have been melted away, and the Society of Friends has again reached a consensus that Quakers are compelled to refuse to pay war taxes.

President Johnson’s war surtax went into effect in , adding a 7.5% surtax to the income tax returns for , and 10% for (the tax would be extended at a reduced rate into and then abandoned).

Meetings all across the country were discussing and passing minutes on war tax resistance, though few would advocate it in specific and unreserved ways, most choosing instead to voice expressions of unspecified “approval and loving support” for Quakers who felt compelled to resist.

In , the Philadelphia Yearly Meeting passed a relatively strong minute stating:

Refusal to pay the military portion of taxes is an honorable testimony, fully in keeping with the history and practices of Friends…

We warmly approve of people following their conscience, and openly approve civil disobedience in this matter under Divine compulsion.

We ask all to consider carefully the implications of paying taxes that relate to war-making…

Specifically, we offer encouragement and support to people caught up in the problem of seizure, and of payment against their will.

The New York Yearly Meeting decided to begin resisting corporately by refusing to honor liens on the salaries of tax resisting employees (though it could not reach consensus on a refusal to withhold income tax from such employees), and, , by refusing to pay its own phone tax.

The American Friends Service Committee finally decided to do something concrete about the war tax question, but it was a little odd.

They withheld and paid taxes from a war tax resisting employee and then sued the government for a refund.

The strange structure of their process seems to have been a very deliberate way to structure a legal suit for maximum effectiveness, and it did (briefly) show some success.

A court ruled in , on First Amendment freedom-of-religion grounds, that the government could not force the organization to pay the taxes of an objecting employee — alas, the Supreme Court almost immediately, and overwhelmingly, overturned this.

Also in , Susumu Ishitani, a Japanese Quaker, formed a war tax resistance group in Japan — the first example I am aware of from Asia.

By , the Friends Journal’s coverage of war tax resistance is less occupied with advocacy, debate, and the presentation of individual exemplars, and is more concerned with the practical aspects of how Quakers are going about it.

The editorial stance shifts again, to one of more forthright advocacy.

It is assumed that Quakers want to avoid paying war taxes, and the question is how to do so well.

The ending of the U.S. war on Vietnam did not seem to slow the enthusiasm for war tax resistance.

In the Friends Journal devoted an issue to the subject for the first time.

In Robert Anthony began another attempt to get the courts to legalize conscientious objection to military taxation.

It went nowhere, but notably, in a letter to the court, his monthly meeting wrote:

We assert that the free exercise of the Quaker religion entails the avoidance of any participation in war or financial contribution to that part of the national budget used by the military.

If not exaggerated for effect, this statement would be among the strongest yet articulated by a Quaker institution in this renaissance period — not simply expressing support for war tax resisters, or encouraging Friends to consider resisting, but asserting that to practice the Quaker religion necessarily meant to refuse to pay war taxes.

In , Quakers met with their Brethren and Mennonite counterparts to draft a joint statement that encouraged war tax resistance — the “New Call to Peacemaking.”

The Philadelphia Yearly Meeting asked its ongoing representative meeting to draft some formal guidance for Quaker war tax resisters for how they should go about it, and to set up an alternative fund to hold and redirect resisted taxes.

(New England Yearly Meeting began its own alternative fund for resisted taxes .)

By this time war tax resistance is a core part of any discussion of the Quaker peace testimony, and there are increasing calls for Meetings to resist taxes as an institution.

In the Philadelphia Yearly Meeting approved a minute on war tax resistance that pulled its punches a bit:

Our strength and our security are derived from our belief in the reality of a loving God and the oneness of that of God in all people.

In order to say yes to this belief, we must seriously consider saying no to payment of war taxes.

This “seriously consider” compares poorly to discipline of times past (e.g. “a tax levied for the purchasing of drums, colors, or for other warlike uses, cannot be paid consistently with our Christian testimony” [Ohio Yearly Meeting, 1819]).

It also, some Quakers point out, sometimes pales next to the more direct and certain advice from some meetings that young Quaker men resist the draft.

As more Quakers and Meetings feel the pressure to take a stand on war taxes, the more timid ones are increasingly desperate to find ways to do so without actually having to resist.

Silly ideas, like writing “not for military spending” in the memo field of their tax payment checks, and “peace tax fund” ideas proliferate.

By , Quakers in Canada and Australia are floating their own peace tax fund legislation ideas.

Meanwhile, Quakers in England seem to have gotten the tax resisting bug.

The Friends World Committee for Consultation and London Yearly Meeting stopped withholding income taxes from twenty-five war tax resisting employees in , putting the money in escrow.

(This resistance was short-lived; after losing a legal appeal in , they went back to withholding.)

In war tax resistance, according to Friends Journal reports, was a “major preoccupation” of the London Yearly Meeting, and a “burning concern” at the Philadelphia Yearly Meeting (where “unity could not be achieved”).

Lake Erie Yearly Meeting encouraged its Monthly Meetings “to establish meetings for sufferings to aid war tax resisters.”

Pacific Yearly Meeting started an alternative fund.

Smaller Monthly and Quarterly meetings around the country were beginning to take even stronger stands.

The Minneapolis and Twin Cities Meetings approved a minute that asked “all members of our meetings to practice some form of war tax resistance”!

The Davis (California) meeting passed a similar minute.

Monthly Meetings are assembling “clearness committees” to help each other find responses to the war tax problem that are appropriate to their conscientious “leadings.”

also, the Friends General Conference promoted the idea of Quakers giving interest-free loans to them, a thinly-veiled (not explicitly stated) way of hiding assets from IRS:

…Friends loan money to F.G.C. at no interest, which F.G.C. invests to earn income which is used to support the varied programs of the Conference, such as publications, religious education curricula, and the ongoing nurture program.

These loans provide regular dependable monthly income to the Conference, and reduce the interest income on which the lender must pay federal income taxes, while providing the lender with protection against unforeseen financial reversals.

F.G.C. will repay the principal amount within 30 days after receiving a written request from the lender.

All principal amounts are kept in insured investments.

In the Friends Journal, now edited by a war tax resister, devoted another issue to the subject.

Non-resisting Quakers were now very much on the defensive.

One complained that at the Philadelphia Yearly Meeting , taxpaying Quakers like him “were compared to the Quaker slaveholders of , and not a dissenting voice was raised,” but even he had to acknowledge that war tax resistance was “in the mainstream of Quaker thought, and therefore entitled to support from Quaker bodies.”

The meeting itself though could only agree to issue another minute that would “not urge” Friends to resist, but would “give strong support” to those who did.

In , the Friends World Committee for Consultation held a war tax resistance conference in Washington, D.C., and formed a standing “Friends Committee on War Tax Concerns.”

, they held a conference for Quaker organizations that had war tax resisting employees.

The conference was attended by 35 people, including representatives from 21 such organizations.

They were united by an interest in supporting the war tax resistance of their employees in an open and honest fashion, in a way that included the redirection of the resisted taxes to beneficial causes, and that used the “clearness committee” process.

You definitely get the feeling that momentum is building and Quaker war tax resistance is having a vigorous revival.

Unfortunately, though, it seems to me that this is the high-water mark.

In surprisingly little time the tide will begin to recede.

But there is still some forward progress to be made.

In the London Yearly Meeting declared:

We are convinced by the Spirit of God to say without any hesitation whatsoever that we must support the right of conscientious objection to paying taxes for war purposes…

We ask Meeting for Sufferings to explore further and with urgency the role our religious society should corporately take in this concern and then to take such action as it sees necessary on our behalf.

The Friends United Meeting adopted a policy of not withholding taxes from resisting employees as well.

The Philadelphia Yearly Meeting soon followed suit, and refused to withhold federal taxes from three war tax resisters on the payroll (after a legal battle, they would pay “under duress” ).

The Baltimore Yearly Meeting also adopted such a policy, in .

In another conference for employers of tax resisting employees was held, this one expanded to include Mennonite and Church of the Brethren employers.

The Friends Journal got an IRS levy on the salary of its editor, and it devoted a third issue to the topic of war tax resistance.

Some Quakers begin using the tax resistance tactic in the service of other causes, such as opposition to capital punishment or nuclear power.

In an early sign of the receding of the war tax resistance tide, the Friends World Committee for Consultation retired its “Friends Committee on War Tax Concerns” in favor of a “Committee on Peace Concerns.”

From here, sadly, it’s pretty much all downhill.

In the next and final segment of this series on the history of Quaker war tax resistance, I’ll try to describe and explore the second “forgetting.”

Today, another item of interest I found in a back issue of Friends Bulletin, the journal of the Pacific Yearly Meeting of Quakers.

As I noted a few years back when I was looking through back issues of the Friends Journal, the American Friends Service Committee could be relatively conservative about war tax resistance, despite being so prominent in a lot of Quaker peace activism.

Here’s another data point that shows that there was some heartfelt seeking going on behind the scenes.

The American Friends Service Committee is currently considering some unprecedented action to respond to the terrible challenge of the war in Vietnam.

The National Board and other parts of the Service Committee are now weighing

what sacrificial financial effort they will ask themselves and other Friends

to make as individuals… They feel that they must find the way to say that we

must support young men who refuse war service in Vietnam, deny moral sanction

to U.S. military

intervention in Vietnam and encourage churches and other religious bodies to

do the same, support those who refuse their skills as scientists, engineers,

and administrators to produce instruments of death, encourage citizens and

soldiers to consider whether there are moral grounds for them to resist

policies or disobey orders that would require them to engage in what their

consciences clearly have told them are wrong, assist those who conscientiously

resort to civil disobedience on such things as payment of taxes for war

purposes, and so on.

The group asked me to say to Yearly Meeting that It [sic] is possible

to alter one’s way of life, to live more simply, to recognize that $600 of

every $1,000 of income tax we pay supports war expenditures and $200 of that

supports the war in Vietnam. They wanted me to say that the time has come for

us to look honestly at our own lives in the light of what is happening in

Vietnam.

They wanted me to say that we may want to tithe or tax ourselves for peace and

that if our situations are such that we cannot tithe or tax in money, we may

be free to rearrange our lives so that we can tithe our time for working as

volunteers.

This was followed by two “statements… presented by the Peace Committee and,

after consideration and revision, …approved by the Yearly Meeting” including

the following “Statement on Taxes”:

Many Friends feel a growing conflict between their testimony for peace and the

taxes they pay for war. Friends, individually and together, are encouraged to

examine their own economic involvement in creating conditions and institutions

of both war and peace.

In the Discipline of Pacific Yearly Meeting

(pp. 41, 42) “Friends are urged

to consider carefully the implications of paying those taxes a major portion

of which go for military purposes.” An increasing number of Friends and

like-minded people have been led by conscience to express their protest of

such taxes in such ways as the following:

By a letter of protest included with their tax payment, in which the

religious basis of their objection is explained.

By a letter of tax refusal in which the reasons for refusing to pay all or

part of the tax are set forth.

By a formal request for return of taxes paid under protest, or of taxes

and penalties which have been seized from the resources of tax

refusers.

By bringing suit against the government for recovery of such taxes when

such requests for return are denied. Technical information regarding this

is available from the Peace Committee.

By refusing to file an income tax form and sending a letter of

explanation.

By refusing to pay the 7% telephone tax recently added to monthly

telephone bills to help finance the budget deficit caused by Vietnam, and

sending a letter explaining this action.

By pledging not to buy automobiles and other items on which the increased

excise tax for Vietnam is levied.

By lowering their income below the taxable level and informing the

government that this is a protest against war taxes.

Whether or not Friends are moved to such acts of protest as these, they are

urged to take all possible deductions when filing income tax returns. Such

deductions not only reduce taxes paid for war, but make available additional

money which can be invested in Friends’ work for peace.

Believing that effective protest is grounded in the vision and enthusiasm of

affirmation and positive action, some Meetings are assisting their members in

sending a self-imposed tax of 1% of income each year to the United Nations.

Individual Friends have been moved to contribute each month to the United

Nations and the American Friends Service Committee a voluntary tax for peace

equal to the amount they now pay in taxes used for military purposes.

While it is recognized that such acts of protest or affirmation are ultimately

matters of individual conscience, Friends would encourage concerned

individuals among them in their efforts to act in harmony with the light of

conscience, and would support them in such acts as they are led by the Spirit

to take. To this end meetings are urged to make information about possible

courses of action available to concerned members and to counsel and assist

those members seeking to act on their concerns about payment of war taxes.

Freund gives a brief overview of the history of conscientious tax resistance

that seems to me to understate it, though it’s possible that in

less evidence was easily available.

[I]t was not until the Vietnam War that tax resistance became a significant form of Christian witness against war.

One of the early Vietnam-era tax resisters was William Faw, a minister of the Church of the Brethren, one of the historic peace churches.

Faw had not come to my attention before, but Freund tells his story as follows:

William Faw: “Here I Stand; I Cannot Do Other”

William Faw was born in in Nigeria where his parents were missionaries for the Brethren Church.

His father took a post teaching at Bethany Seminary, and the family moved to Chicago where Bill grew up.

He went to college in Indiana and then attended the seminary until his graduation in .

While at school Faw was compelled to confront the issue of the draft. “Both my

parents were pacifists so I had decided early on that I would either be a

resister or a conscientious objector; I could not accept a student or

ministerial deferment in good conscience,” explains Faw. Despite his religious

background it still required a two-year battle with the draft board to obtain

his CO

status. By the time he received

CO status

he had a family and was never required to perform alternative service.

He received his first assignment in at the Douglas Park Church of the Brethren, a poor, multiracial community on the West Side of Chicago.

It was during this period that Bill Faw became a tax resister.

Faw explains that decision, saying, “I was a self-employed pastor and my wife was not working so we had control over our tax payments.

Since my wife was also a pacifist, we felt that it was necessary to protest the Vietnam War.

The question was, ‘How can we do this together?’ We spoke with several other Brethren who had been refusing taxes and listened to political leaders who opposed the war.

By early we decided to refuse to pay our taxes in full knowledge that it could lead to criminal punishment.”

When the time came to file their income tax

return, the Faws sent the

IRS a

long letter explaining why there was no check enclosed. Other resisters had

engaged in resistance by refusing even to file a return, but Faw believed that

a religious witness should be made in an open and public manner. The Faws’

letter made clear the personal struggle which accompanied their decision:

We refuse to willingly contribute to a “war machine” which is engaged in the very brutal war in Vietnam… In the past we felt that the ambiguities of tax paying outweighed the war-tax issue.

That is, our government’s expenditures for foreign aid, law enforcement, programs in health, education, and welfare, agriculture, urban redevelopment, and poverty fighting are worthy of support… Events have occurred which lead us to reconsider our responsibilities as citizens.

We feel we can be true to our national citizenship only if we oppose a so-called “non-war” that has not been constitutionally declared.

We feel that we can be true to our international citizenship as spelled out at the Nuremberg Trials only if we disassociate ourselves from and actively protest our unjust, illegal, morally deplorable, aggressive offensive against human beings in Vietnam.

But most basically we feel that we can be true to our Christian discipleship

only if we oppose… the seizure of God’s prerogative by the United States in

attempting to become the philosophical, theological, executive, legislative,

judicial, and policing agency for the entire world; only if we oppose the

exploiting of American “racism” by

A-bombing, napalming,

scatterbombing Asians; only if we oppose the mode of “evangelistic effort”

our nation is making in Vietnam to show the Buddhists what being a

“Christian” nation means…

Thus we are led to withhold our income tax and to seek constructive alternative ways of sharing our income… In God’s name, and under his judgment, we pray that we might choose the best path to make our witness.

…As a result, they chose to donate the tax money to the Canadian Friends Service Committee for the relief of war victims.

They were well aware that some of those victims who would be helped by their money were North Vietnamese and Viet Cong; they believed this action to be consistent with Jesus’ command to “love your enemy.”

The Faws refused to pay their income taxes for the next five years, donating

the funds to various international relief agencies. The Internal Revenue

Service sent an agent to attempt to obtain the taxes directly. When this

failed the

IRS

placed a levy on the Faws’ bank account and was able to collect the back

taxes. The Faws were not threatened with criminal penalties.

Freund says the Faws were also resisting their phone tax, but returned to being taxpayers in the wake of the Paris Peace Accords.

However, as of the writing of the book, they were planning to become resisters again by refusing a percentage of their income tax:

The continuing military buildup, especially nuclear weapons, has led us to resume tax resistance… We are being lulled into accepting more and more.

Johnson tried to give us guns and butter, but Reagan’s policy of sacrificing butter for guns represents a barbaric reversal of priorities.

Freund asked about the practical effectiveness of individual tax resistance.

…Faw conceded that it would be far more powerful if institutions were to openly advocate and practice tax resistance. “If one church did it, even a small one like the Brethren, the Mennonites, or the Quakers, it would have a tremendous impact on some of the liberal mainline denominations,” Faw believes.

However, even the New Call To Peacemaking, a grassroots movement within the historic peace churches begun in , of which Faw was the local chairman for two years, has failed to adopt a position of total resistance to war taxes.

This has been a source of frustration for Bill Faw, but he nevertheless believes in the importance of individual witness, “I would still do it even if no one else did.

There comes a point, with Vietnam or the arms race, where you say, ‘I’m not going to participate in that, no matter what the cost.’ It’s kind of like Martin Luther saying, ‘Here I stand; I cannot do other.’ ”

Freund then briefly described “A Simple Methodology” for Christians who were considering war tax resistance, covering the options of 1) paying taxes under protest, 2) voluntary poverty, 3) refusal to pay.

He then tried to discern what sort of guidance might be found in the Bible, considering the difficult “Render unto Caesar” and “the powers that be are ordained of God” sections in particular.

Then he returns to the problem of the lack of institutional support for war tax

resistance among Christian churches:

War Taxes: Where the Churches Are