The statue of John Hampden, presented to the county of Buckinghamshire by Mr. James Griffiths, of Long Marston, in commemoration of the Coronation, was unveiled at Aylesbury on by Lord Rothschild.

There was a large gathering, representative of Buckinghamshire generally.

After some difficulty the Women’s Tax Resistance League received the assurance that they would be able to pay their last tribute to the great Tax Resister.

At the close of the unveiling ceremony a procession of members of the League crossed the market square to the statue, the crowd readily making way, while police lined the short route.

On behalf of the League, two delegates, Miss Gertrude Eaton and Miss Clemence Housman, laid a beautiful wreath at the foot of the statue.

It was made of white flowers, on which, in black letters, were the words, “From Women Tax Resisters.”

Within the circle of flowers was a ship in full sail with the name of John Hampden in gold letters on the streamers.

The ship was made of brown beech leaves (the beech is the tree most famous in Buckinghamshire) and white flowers.

Emblems were also laid at the base of the statue from the Irishwomen’s Franchise League [this was corrected in a later issue; it was actually from the Irish League for Women’s Suffrage] (a harp in Maréchal Niel roses), the Gymnastic Teachers’ S.S. (blue immortelles and silver leaves), and the London Graduates Union (a laurel wreath).

Among those present were Mrs. [Myra Eleanor] Sadd Brown, Mrs. [Mary] Sergeant Florence, Dr. Kate Haslam, Mrs. [Ethel] Ayres Purdie, Mrs. [Margaret] Kineton Parkes, Miss [Minnie?] Turner, M.A., Miss [Maud?] Roll, Mr. Lee and Mr. Sergeant.

Tax Resistance: The Situation at Bromley.

“My goods are not yet seized for non-payment of taxes. I am still barricaded.

“Outside the gate!

“A most uncomfortable position for the tax collector!

But, while offering sympathy, I feel the experience will be beneficial.

There is nothing so enlightening as a little ‘fellow-feeling.’

Nothing like going ‘there’ to learn the discomforts of being where the woman is, and should be, according to the gospel of the man at Westminster.

Bolts and bars are never pleasant things to deal with — from outside!

They are terribly, cruelly hard to remove when fixed by men driven by fear to protect an unjust wall of separation.

But walls must yield to pressure, and the women gather, intent on ‘breaking down’; content, if need be, to ‘be broken.’

While men, relying on their fastenings, ignore the trembling of foundations, women know the wall is doomed, and when it falls they will flock in to do the bidding of the “Anti” — to scrub and clean, to mind the babies, to stay in the home — the National Home.”

K[ate]. Harvey.

Meetings in the Market-square, Bromley.

Meetings are now being held every evening in the Market-square, Bromley, and are exciting wide interest.

Mrs. [Charlotte] Despard was the speaker at the first, and told the crowd why Mrs. Harvey was making this emphatic protest against taxation without representation.

Mrs. Despard’s own experiences aroused much interest.

The following evening Mrs. [Isabel] Tippett spoke, and still larger crowds gathered to hear her.

By news of these regular meetings had spread, and the audience was ready to receive the speakers.

The “Antis” are showing themselves — a sure sign of our success — but the chief argument they bring forward, in the form of questions, is that of physical force: because women do not fight they should not vote.

Mrs. Merivale Mayer, the speaker on , was able to show how beneficial the women’s vote had proved in Australia, and told of the surprise of Australian politicians that the Mother Country still refuses to give the women the chance to stand side by side with men in the fight against evil.

The police are exceedingly kind — and evidently interested.

More Tax Resisters.

On , at Redding, goods belonging to Professor Edith Morley were sold.

Speakers: Mrs. [Anne] Cobden Sanderson, Miss Gertrude Eaton.

Also goods belonging to Miss Manuelle, at Harding’s Auction Rooms, Victoria Station, W.

Speakers: Mrs. [Caroline] Louis Fagan, Mrs. Cobden Sanderson, Dr. [C.V.] Drysdale; and at Working, silver, the property of Mrs. Skipwith, was sold.

Speakers: Mrs. [Barbara] Ayrton Gould, Mrs. Kineton Parkes.

On , at Southend, silver belonging to Mrs. Douglas Hameton and Mrs. [Rosina] Sky was sold.

There was a procession with brass band prior to sale, and also a very successful protest meeting.

Speakers: Mrs. Cobden Sanderson, Mrs. Kineton Parkes, Mr. Warren.

The need for women to be on the watch is strikingly shown in the news of her experiences which has been sent us by Miss Clara Lee, of Thistledown, Letchworth, who points out how she forced an admission of error from the Inland Revenue Authorities.

She writes thus:—

As a tax resister, the following experiences prove the carelessness of Government officials.

Having refused to pay Inhabited House Duty (8s. 9d.) to the local collector, I was reported by him to the surveyor for this district, who sent a demand containing two inaccuracies.

I wrote to point that one ought not to have occurred, seeing that we had had compulsory education since ; the other, he would see did not agree with the original:—

Local Demand.

s.

d.

Schedule A

5

0

House Duty

8

9

Surveyor’s Demand.

£

s.

d.

Schedule A

0

5

0

Schedule B

1

1

5

House Duty

0

8

9

Schedule B, I found, applied to nurseries and market gardens.

So I wrote pointing out that the nearest connection I had to either, was that under the Lloyd George Insurance Act I was classed with agricultural labourers.

To this I received the following letter:—

4, Cardiff-road, Luton, .

Inland Revenue — Surveyor of Taxes.

Madam, — Referring to your letter of , I much regret that £1 1s. 5d. was included upon your demand note in error — the entry relating to the next person upon the collector’s return. — Yours faithfully,

(Signed) G.R. Simpson.

Is this the exactness of the work for which women, as well as men, pay so heavily?

How long would a commercial firm exist, if it allowed such errors?

How long would the public tolerate such mistakes by women workers in our hospitals and elsewhere?

The title of idiot, lunatic and criminal must revert to the people responsible for such a condition of things.

The 8s. 9d. Inhabited House Duty has now been deducted from my claim of return Income-tax; this seems an unusual proceeding.

I am still locked up!

A fellow “resister” has sent the following lines to cheer me:—

Good luck, my friend, I wish to thee, In thy brave fight ’gainst tyranny. Bracken Hill Siege will bring good cheer To those who hold our Freedom dear, And fight the good fight far and near.

And when oppression is out-done, And Liberty, at last, is won, When women civic rights possess, They’ll think, I hope, with thankfulness, Of those who bore the battle’s stress.

Those women who have heard or read of the impending arrest of Mr. Mark Wilks (the husband of Dr. Elizabeth Wilks) in consequence of his inability to pay income-tax on his wife’s earnings from her profession, will doubtless be interested to know why such a situation is possible, and what is the exact legal position of the husband and wife.

Long ago in the dark ages, or to speak more precisely, in , the Income Tax Act was passed, which regulates all income-tax procedure, even to the present day.

It is a most fearsome piece of composition.

Its language is archaic and tautological, it rises wholly superior to punctuation, and proceeds breathlessly through one hundred and ninety-four clauses.

Clause No. 45 provides that the “profits” of any married woman “shall be deemed to be the profits of her husband,” and are to be charged with income-tax in his name and not in hers.

In other words, he was to pay, and she was to be exempt, a perfectly fair arrangement in the bad old times when a man acquired his wife’s revenues or earnings on their marriage and she became thereby literally a “destitute” person.

The word “profits” denotes all revenue or income derived either from the wife’s capital or her labour.

So whether she receives her income from rents, interest, dividends, &c., from the exercise of a trade or profession, or from salary or wages paid for her services or labour, a demand for payment of income-tax thereon must be made to her husband, and to him only.

If he fails to comply with such demand, he can be thrown into prison (without any trial or other formalities) until he pays.

Such is the unfortunate and wholly absurd position to which man-made law has brought Mr. Mark Wilks — as well as numerous other husbands whom the Inland Revenue authorities are mostly unable to locate.

It will be seen that his arrest might involve a husband’s being imprisoned indefinitely, or even permanently, the period of detention being only determined by payment of the sum demanded, which in the present instance is £40. Most of the Press reports have rather distorted Mr. Wilks’ case by asserting that it is Mrs. Wilks who is refusing to pay.

Legally no married woman can even be asked to pay income-tax, and therefore a refusal on her part is quite out of the question.

I can hear someone saying, “Oh, but in we obtained a Married Woman’s Property Act.”

Quite true, but according to an official letter from Somerset House in my possession, “the Crown does not recognise this Act.”

The Crown authorities claim the right to maintain the position as it existed seventy years ago, and to over-ride the later and minor Act whenever it happens to suit their own ends.

It happens — for reasons which space compels me to omit — to suit them to the tune of two and a-half million pounds a year.

Mr. Lloyd George confessed quite frankly in the House of Commons recently, when it was suggested to him that it was high time the Government set an example of compliance with the law, instead of bare-faced defiance of it, that to recognise the Married Women’s Property Act would annually deplete the Treasury to this large amount.

Mr. Stuart Wortley boldly told the Government they were an unscrupulous and dishonest lot, who juggled with the laws of the country, and shaped their policy on £ s. d., instead of on even-handed justice.

And in the course of the debate it was stated that if mercantile firms conducted their business on this principle they would speedily find themselves in the dock.

Readers will probably be in thorough agreement with this declaration.

As a tax-resister on the ground that taxation and representation must go together, Miss Marie Lawson has made the following appeal to His Majesty the King:—

To the King’s Most Excellent Majesty, etc. The Humble Petition of Marie Lawson, of 5, Westbourne-square, London, showeth:—

That your petitioner, having been proceeded against by Your Majesty’s Attorney-General in the High Court of Justice with respect to the non-payment of Income Tax, humbly prays Your Majesty to stay the said proceedings in consideration of the circumstances hereunder set forth:—

That the imposition of such tax is wrong and unjust in that it is an infringement of the principle that taxation and representation must go together, a principle which has been long recognised in that rule which prohibits the House of Lords, and an unrepresentative assembly, from initiating or amending Money Bills; and it is respectfully submitted that the same principle should operate to prevent the House of Commons, an assembly equally unrepresentative with regard to Your Majesty’s female subjects, from initiating or enforcing financial legislation affecting such subjects.

That the redress of grievances has long been recognised as a condition to supplies, and that arbitrary taxation has been persistently and successfully resisted in the past, whether the arbitrary taxation levied by the King in his own person which in the Stuart period plunged this country into Civil War, or the arbitrary taxation levied by Parliament, in the name of the Crown, which caused the American revolution.

That Your Petitioner, in common with large numbers of other women, has been driven to resistance by the goad that is furnished by the continued refusal of your Majesty’s government to grant to the women of Great Britain that measure of justice already enjoyed by their sisters in Your Majesty’s dominions beyond the seas.

The morals of Somerset House [the offices of Inland Revenue] are like those of the much abused “heathen Chinee.”

The Department has a very simple and convenient maxim by which it regulates its conduct, and that is, Never be aware of anything unless it pays.

So long as money could be easily obtained by annexing Mrs. Wilks’ furniture and effects, the Inland Revenue authorities shut their eyes to the fact that she was Mrs. Wilks, living with Mr. Wilks, and therefore might be assumed by any intelligent person to be married.

Their excuse is that she never “told” them she was married until recently, and so they assumed she was not!

Presumably they thought Mr. Wilks was her father-in-law or her grandfather-in-law, or that she called herself Mrs. Wilks by way of a joke.

So soon as they found no more money would be obtainable from her, they conveniently realised that she had a husband, from whom they demand the tax.

“But a great many excuses must be made for a Department which has only become officially alive to woman’s existence during the current year,” writes Mrs. [Ethel] Ayres Purdie to us.

“Hitherto all official letters began with ‘Sir,’ regardless of the fact that women pay taxes, and pay for the official stationery and clerical work.

As I objected to having ‘Sir’ hurled at me every time I opened an official letter, I drew up a form letter, in which I observed that ‘business men’ were in the habit of addressing women clients or customers as ‘Madam,’ and I should be much obliged if they would remember this fact, and refrain from the solecism of addressing me as ‘Sir.’

Every public official from the humble clerk up to Departmental secretaries and arrogant Treasury clerks received one of these letters as regularly as clockwork every time they called me ‘Sir.’

At last they have learnt to address women as ‘Madam,’ and this year even the printed forms begin ‘Sir or Madam,’ for all the world like a respectable business firm.

That “the Law is a Hass” no one has ever seriously attempted to deny; but what one wants to know is what to say of the people who make it?

This is an aspect of the case that has been much neglected; but with a little goodwill and concentration, we hope to make up for lost time and direct attention to the real offenders.

It is a poor kind of wit or wisdom that breaks its shaft over the suffering head of the Law, and keeps silence on the subject of the Law-maker.

The gentlemen who draw salaries large and small, ranging from £10,000 to £400 a year for performing what one might describe as the most highly skilled work required by the country, and who perform that work in such a way as to create such situations as that leading to the arrest of Mr. Mark Wilks for non-payment of taxes not his own and due on an income over which he has no control and whose amount he can only guess at, are surely playing the biggest “bluff” ever put up, on their long-suffering fellow-men.

One’s mind wanders between the alternative possibilities, that those in office are knaves while the others are fools, or that they are all knaves together; or that they are “mostly fools,” both in office and out.

…

…Acts in conflict with each other, such as the Income Tax and Married Women’s Property Acts, the National Insurance and the Truck Acts, should be brought into harmony on some definite ruling; and some attempt should be made by future legislators so to simplify their language as to make their meaning plain without the superfluity of litigation which their unhappy ambiguity at present inflicts on the nation.

While waiting for this legislative millennium, we fill in the time by demonstrating on every possible occasion how poor is the workmanship for which we are called upon to pay such preposterous prices, and how entirely logical and correct a fashion of protesting our displeasure and disability is the Tax Resistance policy, of which Mr. Mark Wilks and Dr. Wilks are the latest exponents.

All Suffragists will thank them for their spirited action, which from the nature of the case must have been painful and unpleasant for them both.

We shall not readily forget such support as that given by Mr. Wilks; and the demonstration on by the W.F.L., the W.T.R.L., the Men’s League and the Men’s Federation, showed how forcible is such action.

The position was entirely appreciated by the large crowds which gathered round the Lions in Trafalgar Square; and in spite of a good deal of laughter and “chaff” which was never ill-natured, a large section of the “long-suffering” British public testified to its dissatisfaction with the present state of the law and its approval of the tactics of the Women Tax Resisters.

True “Queen’s weather” favoured the opening of our autumn campaign on , when the Freedom League, in conjunction with the Tax Resistance League, the Men’s League, the Free Church League, and the Men’s Federation for Women’s Suffrage met in the Trafalgar-square to demand the enfranchisement of women and to protest against the imprisonment of Mr. Mark Wilks for the non-payment of his wife’s taxes.

Mme. Mirovitch and Mr. Herbert Jacobs were among those who supported the speakers.

The large crowd, which gathered half an hour before the meeting began and remained throughout the two hours of its duration, showed the widespread interest in votes for women.

Both before and during the speeches members of the Tax Resistance League paraded the Square, carrying sandwich-boards bearing the words in bold letters, “We demand the immediate release of Mark Wilks.”

There were two platforms on the plinth, one presided over by Miss Anna Munro and the other by Mrs. [Isabel] Tippett.

At both of these the following resolution was put and carried by a large majority:— “That this meeting demands from the Government the political enfranchisement of women this Session, and the immediate release of Mr. Mark Wilks.”

Ridiculous Position of the Government.

Mrs. Tippett, in opening the meeting, pointed out the extraordinary and ridiculous position in which the Government has placed itself by the arrest of Mr. Wilks.

The crowd was intensely interested while she read a statement of Mr. Wilks with regard to his position.

Mr. Futvoye, of the Men’s Federation, in moving the resolution, said how glad he was to be on a common platform with so many suffrage societies.

The women’s movement had drawn together people of different parties, religions and sexes.

He emphasised the fact that women will be unable to get fair conditions of life and labour until they get the vote.

As long as they are unrepresented the Government will take no notice of their demand for a living wage.

Mrs. Merivale Mayer, seconding the resolution, said there was much talk about progress in these days, but when women talked of it it seemed to be thought that she required man’s permission to rise.

This was not progress.

Miss Boyle, in supporting the resolution, showed the ridiculous situation brought about by the incompatibility of the laws with regard to Income-tax and the Married Women’s Property Act.

Members of Parliament are the servants of the people, paid, whether they be ministers or ordinary members, out of the pockets of both men and women.

Though paid to make laws, they did their job so badly that other people then had to be paid to find out what the law meant.

Women wanted better value for their money, especially when it was taken from them under compulsion.

Suffragists had found that Tax Resistance was very effective; but though Government was spending public money in trying to put down the Suffrage movement, they would not succeed.

In being so blind as to the strength and significance of the movement, and in their treatment of the women of this country, they were obliged to look either fools or brutes, and as they were not afraid to look either they succeeded in looking both.

An Appeal to Business Men.

Mr. Simpson supported the resolution.

He appealed to the practical business men in the crowd, who had the vote because others had fought for it for them.

After long years of legislation of the people for the people by the people they wanted less of Party politics and more improvement in social conditions.

In the Labour market, what had been done to raise wages was neutralised by the cheap labour of women.

Votes for women was the only remedy for this.

Miss [Margaret] Kineton Parkes, of the Tax Resistance League, explained that Mrs. Wilks refused to pay her taxes because she realised that such a refusal was the most logical protest a woman could make against a Liberal Government whose cry had been that with taxation must go representation.

The Government was bound either to remove the burden of taxation, or give women the vote.

She thought men ought to make the protest, for the Government had imprisoned a man, while Mrs. [Charlotte] Despard, Mrs. Pankhurst, and many other women who had not paid taxes for years, were still at large.

Worse than Ancient Rome.

At the other platform, presided over by Miss Munro, the mover of the resolution was Mrs. [Margaret] Nevinson, who kept her audience in a ripple of laughter.

She thought it was high time to alter the laws of this country, which in some respects were worse than those of ancient Rome, when in the twentieth century a man could be put in prison for doing nothing.

She told several very amusing and yet pathetic stories of cases she had known before the passing of the Married Women’s Property Act, but said that the passing of that Act had brought about such anomalies as the present one, when a man could be arrested for not paying his wife’s taxes when he didn’t even know her income.

Mr. Lawrence Housman, in seconding the resolution, said that as a member of the Tax Resistance League he would like first to thank the Women’s Freedom League for allowing them to share in this meeting and to state a man’s grievance.

He found women always ready to help men, and felt that if men had been as ready to help women they would not be in the position they are to-day.

According to the Anti-Suffragists, the sending of a man to prison for his wife’s default is an example of the wife’s privileges under the law.

All honest women want to get rid of this privilege.

At the mention of Mrs. [Mary] Leigh’s release there was loud applause.

Mr. Housman said the Government dare not kill her because, whatever she had done, they knew she was fighting for a just cause.

Here was a case where physical force, so beloved by the Anti-Suffragists was defeated.

Man and Woman Standing Together.

Mrs. Despard, who was received with loud applause, said it gave her peculiar satisfaction to support the resolution, particularly the last part of it, for in the case of Mr. and Mrs. Wilks she saw coming true an old dream of hers, the dream of men and women standing together, not only in the family, but in that larger family — the State.

She was proud that these were her personal friends.

It was difficult to understand the actions of the Government with regard to tax resistance, for she had not paid taxes for two years, and the Government had done nothing but tell her that she should know their intentions.

In Ireland one weak woman had defied them; they had found it useless to coerce; the only possible course was to yield to the just demands of womanhood.

Poetic Justice.

Mrs. Tanner said that although everyone was indignant at the arrest of Mr. Wilks, there was some sort of poetic justice in a man having to suffer through the muddle made by men.

It showed how incapable men were of legislating by themselves.

Women asked for a share in the Government in order to try and prevent such muddles occurring in the future.

Mr. Kennedy supported the resolution as a member of the Men’s League.

He reminded his audience that the poet Whittier, in writing of Women’s Suffrage, had said that it was right because it was just, and although the consequences were not known, it was the safest thing, the truest expediency, to do right.…

Mrs. [Anne] Cobden Sanderson, of the Tax-Resistance League, also very briefly supported the resolution.

She begged for sympathy and support of Mr. Wilks and announced how this could be publicly shown.

…

Enthusiasm for Dr. Wilks.

At the end of the meeting Dr. Wilks spoke a few words from each platform.

She was received with great applause, which was redoubled when she announced that neither she nor her husband intended to pay the tax.

Mr. Mark Wilks, of 47, Upper Clapton-road, N.E., was arrested on while on his way to the school of which he is headmaster, and removed to Brixton Prison, for the non-payment of his wife’s Income-tax.

He is the husband of Dr. Elizabeth Wilks, suffragist and upholder of the principle “No vote, no tax.”

Her goods have been distrained upon on two occasions for non-payment of taxes.

In a “manifesto” he has issued Mr. Wilks says:—

In my wife claimed that such distraint was illegal, asserting that under the Income-tax Act she, as a married woman, was exempt from taxation.

The authorities then wavered in their claim, making it sometimes on her, sometimes on me, sometimes on us both conjointly, finally on me alone.

On my pointing out that her liability had already been established by forcible distraint upon her property, I was informed that for the future I should be held liable, as that by the Income-tax Act the “wife’s property for purposes of taxation is the husband’s,” although by the Married Women’s Property Act it is entirely out of his control.

Thus I am to be held liable for a tax on property which does not belong to me.

I am now told I am to be committed to prison until such time as I shall pay the “duty and costs” — over £37.

Dr. Wilks’s Statement.

Writing to the Standard (“Woman’s Platform”) Dr. Elizabeth Wilks states the case forcibly and clearly thus:—

Will you allow me a space in your columns to explain as clearly as I can the position my husband and I respectively take in regard to the non-payment of tax on my earned income?

The Press misrepresents the case when it speaks of Mr. Wilks’s refusal to pay the tax.

I refuse to pay any Imperial tax until the Parliamentary vote is granted to women on the same terms as to men.

He does not refuse to pay, but as an assistant-teacher under the London County Council he has not sufficient money to do more than pay the tax on his own income, which he has done.

While, however, married women are not recognised as taxable units the claim does not fall on the right person.

At present the Income-tax Act still holds a man liable for the tax on his wife’s income, in spite of the fact that a more recent Act, the Married Women’s Property Act, has taken from him all control over that income.

Yet we neither of us dreamed that this anachronism would be thus glaringly exposed by the imprisonment sine die of a husband earning a smaller income than his wife.

I am taunted with the fact that while asking for my rights I am unwilling to accept my liabilities.

This is untrue.

I am asking to be recognised as a person both as regards rights and liabilities.

If the State comes to recognise me as a person liable to taxation, but still denies me representation, I, as a voteless tax-resister, shall be in Holloway Prison instead of my husband, a voter and taxpayer, being in Brixton — perhaps a somewhat less absurd position than the present one.

In the meantime the law does indeed press hardly on my husband, and a very striking example is given of the tendency of present-day legislation to penalise those who desire to comply with the marriage laws of the country.

Had the tie between us been irregular my husband would have been practically exempt from Income-tax, and for years I could have claimed abatement.

Because we are legally married he has had to pay the tax on the whole of his salary.

There is one other point I should like to mention.

From the outset of my professional career the authorities have sent the claim on my earned income to me and not to my husband.

In , instead of paying, as I had previously done, I wrote across the form, “No vote, no tax.”

They then distrained on me for the amount.

In I questioned the legality of the threatened distraint, and the authorities then wavered in their claim, making it sometimes on me, sometimes on my husband, sometimes on us both conjointly, finally on him alone.

Now after two years’ intermittent correspondence he is in prison for inability to meet it.

Manifestly if he is liable I am not, and the distraints executed on my goods were illegal.

If I am liable his arrest was illegal and the distraints on me should have been continued.

Certainly it is open to suppose that my husband’s imprisonment is not only unjust but unlawful.

A remark made by Mr. Hobhouse in a debate on the Finance Act on , makes this supposition the more probable.

On this occasion (Parliamentary Debates, Vol. 20, No. 92) he said, speaking on Mr. Walter Guinness’s amendment: “It may be said by hon. gentlemen opposite, ‘Why don’t you send one of the demand forms to the wife?’

I am not at all sure if that course were taken that the Inland Revenue would not put themselves out of court subsequently in their demand from the husband.”

Have they not in this case so put themselves out of court?

Mr. Hobhouse was not sure at that time.

Have the officials become sure since?

Teachers Sign a Petition

A petition against the arrest of Mr. Mark Wilks, the Clapton headmaster, for the non-payment of his wife’s Income-tax, has been circulated among London County Council teachers.

On the first day a thousand signatures were received, and many others are rapidly being obtained.

Protest Meeting.

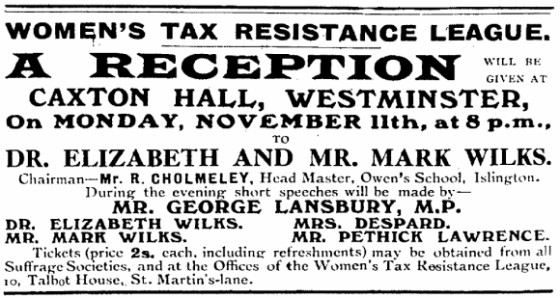

A public indignation meeting, to protest against the imprisonment of Mark Wilks, will be held on , at the Caxton Hall, Westminster.

The chair will be taken by the Hon. Sir John Cockburn, K.C.M.G., and the speakers will be Mr. H[enry].G[eorge].

Chancellor, M.P., Mr. Laurence Housman, Mr. Herbert Jacobs, Rev. Fleming Williams, and Mr. G[eorge].

Bernard Shaw.

Tickets: Reserved, 2s. 6d.; unreserved, 1s. To be had from The International Suffrage Shop, Adam-street, Strand; and from The Women’s Tax Resistance League, 10, Talbot House, St. Martin’s-lane, W.C.

…Mrs. [Marianne] Hyde and Miss Bennett addressed a meeting in Regent’s Park on , and a resolution was passed calling on the Inland Revenue authorities to release Mr. Mark Wilks, who is imprisoned in Brixton Gaol for the non-payment of his wife’s income-tax.

Great Protest Meeting Against the Imprisonment of Mr. Mark Wilks.

“No Government Can Stand Ridicule. The Position is Ridiculous!”

The great meeting of indignant protest against the imprisonment of Mr. Mark Wilks, held at the Caxton Hall on , under the auspices of the Women’s Tax Resistance League, will be not only memorable but epoch-making.

The fight for woman’s citizenship in “free England” has led to the imprisonment of a man for failing to do what was impossible.

Throughout the meeting the humor of the situation was frequently commented upon, but the serious aspect was most strongly emphasized.

Sir John Cockburn, who presided, struck a serious note at the outset; for anything, he said, that touched the liberty of the citizen was of the gravest importance.

He remarked that it was the first occasion on which he had attended a meeting to protest against the action of law.

The resolution of protest was proposed by Dr. Mansell Moullin, whose many and continued services to their Cause are warmly appreciated by all Suffragists, in a very able speech, and ran as follows:—

That this meeting indignantly protests against the imprisonment of Mr. Mark Wilks for his inability to pay the tax on his wife’s earned income, and demands his immediate release.

This meeting also calls for an amendment of the existing Income-tax law, which, contrary to the spirit of the Married Women’s Property Act, regards the wife’s income as one with that of her husband.

A Husband the Property of His Wife.

Dr. Moullin expressed his pleasure in supporting his colleague, Dr. Elizabeth Wilks, in the protest against the outrage on her husband.

The case, he said, was not a chapter out of “Alice in Wonderland,” but a plain proof that, although imprisonment for debt has been abolished in England, a man may be deprived of his liberty for non-payment of money which was not his, and which he could not touch.

The only argument that could be used was that Mr. Wilks was the property of his wife.

Twice distraint had been made on the furniture of Mrs. Wilks, the third time the authorities carried off her husband; it is the first occasion on which it has been proved that a husband is the property of his wife.

The law allows a man to put a halter round the neck of his wife, take her to the market-place and sell her, and this has been done within recent years; but there is no law which allows the Inland Revenue authorities to sell a husband for the benefit of his wife.

Governments, he added, can stand abuse, but cannot stand ridicule, and the position with regard to Dr. Wilks and her husband is both ridiculous and anomalous.

The serious question behind the whole matter was how far anyone is justified in resisting the law of the land.

The resister for conscience’ sake is the martyr of one generation and the saint of the next.

Dr. Moullin doubted whether the Hebrews or Romans of old would recognise what their laws had become; we are ashamed of the outrageous sentences for trivial offences passed by our forefathers; our children will be ashamed of the sentences passed to-day.

Everything in the law connected with women required reconstruction from the very foundation, declared Dr. Moullin.

Constitutional methods, like Royal Commissions, were an admirable device for postponing reform; all reformers were unconstitutional; they had to use unconstitutional methods or leave reform alone.

The self-sacrifice of an individual makes a nation great; that nation is dead when reformers are unwilling to sacrifice themselves.

No Man Safe.

Mr. George Bernard Shaw was the next speaker, and gave a characteristically witty and autobiographical address.

He said that this was the beginning of the revolt of his own unfortunate sex against the intolerable henpecking which had been brought upon them by the refusal of the Government to bring about a reform which everybody knew was going to come, and the delay of which was a mere piece of senseless stupidity.

From the unfortunate Prime Minister downwards no man was safe.

He never saw his wife reflecting in a corner without some fear that she was designing some method of putting him and his sex into a hopeless corner.

He never spoke at suffrage gatherings.

He steadily refused to join the ranks of ignominious and superfluous males who gave assistance which was altogether unnecessary to ladies who could well look after themselves.

“If my wife did that to me, the very moment I came out of prison I would get another wife.

It is indefensible.”

— George Bernard Shaw

Under the Married Women’s Property Act the husband retained the responsibility of the property and the woman had the property to herself.

Mr. Wilks was not the first victim.

The first victim was G.B.S. The Government put on a supertax.

That fell on his wife’s income and on his own.

The authorities said that he must pay his wife’s supertax.

He said, “I do not happen to know the extent of her income.”

When he got married he strongly recommended to his wife to have a separate banking account, and she took him at his word.

He had no knowledge of what his wife’s income was.

All he knew was that she had money at her command, and he frequently took advantage of that by borrowing it from her.

The authorities said that they would have to guess at the income; then the Government passed an Act, he forgot the official title of it, but the popular title was the Bernard Shaw Relief Act.

They passed an Act to allow women to pay their supertax.

In spite of this Act, ordinary taxpayers were still apparently under the old regime, and as Mrs. Wilks would not pay the tax on her own income Mr. Wilks went to gaol.

“If my wife did that to me,” said Mr. Shaw, “the very moment I came out of prison I would get another wife.

It is indefensible.”

Women, he added, had got completely beyond the law at the present time.

Mrs. [Mary] Leigh had been let out, but he presumed that after a brief interval for refreshments she would set fire to another theatre.

He got his living by the theatre, and very probably when she read the report of that speech she would set fire to a theatre where his plays were being performed.

The other day he practically challenged the Government to starve Mrs. Leigh, and in the course of the last fortnight he had received the most abusive letters which had ever reached him in his life.

The Government should put an end to the difficulty at once by giving women the vote.

As he resumed his seat Mr. Shaw said: “I feel glad I have been allowed to say the things I have here to-night without being lynched.”

Bullying Fails.

Mr. Laurence Housman laid stress on the fact that the Government was endeavouring to make Mrs. Wilks, through her affection, do something she did not consider right.

Liberty could only be enjoyed when laws were not an offence to the moral conscience of a people.

Laws were not broken in this country every day because they were not practicable.

Every man, according to law, must go to church on Sunday morning, or sit two hours in the stocks; it was unlawful to wheel perambulators on the pavement.

If the police were compelled to administer all the laws on the Statute Book, England would be a hell.

To imprison Mr. Wilks for something which he had not done and could not do was as sane as if a servant were sent to prison because her employer objected to lick stamps under the Insurance Act.

The Government had tried bullying, but women had shown that it did not pay.

Self-respecting people break down a law by demonstrating that it is too expensive to carry.

Question for the Solicitor to the Treasury.

The legal aspect was the point specially dealt with by Mr. Herbert Jacobs, chairman of the Men’s League for Women’s Suffrage.

He said that it was stupidity, not chivalry, which deprived the husband under the Married Women’s Property Act of of the right to his wife’s earnings, but did not relieve him of responsibility to pay for her.

Imprisonment for debt has been abolished; but if it could be shown that a man had the means to pay and refused to pay, he could be sent to prison for contempt of court.

Mr. Jacobs suggested that the Solicitor to the Treasury should be asked to reply to the following question: “What has Mr. Wilks done or omitted to do that he should be imprisoned for life?”

The law, he added, does not compel a man to do that which he cannot possibly perform.

The action of the Internal Revenue authorities may be illegal; it certainly is barbarous and ridiculous.

Bad Bungling

Mr. H[enry].G[eorge].

Chancellor pointed out that the Married Women’s Property Act was an endeavour by men to remove injustice to women, but because they did not realise the injustices from which women suffer and avoided the woman’s point of view, they bungled badly.

No one can respect a ridiculous law, and the means to be taken in the future to avoid making ridiculous laws, must be to give women the right to make their opinions effectively heard through the ballot-box.

Mr. Chancellor said that he had investigated 240 Bill[s] laid on the table of the House, and had found that 123 were as interesting to women as much as to men; twenty-one affected women almost exclusively; six had relation to the franchise.

“When we consider these Bills,” he added, “we rule out the whole experience and knowledge of women.

We must abolish sex privilege as it affects legislation.

I appeal to men who are Antis to consider the Wilks case, which is possible just so long as we perpetuate the huge wrong of the continued disenfranchisement of women.”

Refinement of Cruelty

In a moving speech Rev. Fleming Williams declared that the case of Dr. Wilks and her husband ought to appeal to men all over the country.

He spoke of the personal interviews he had had with Mr. Wilks in the presence of the warder, and of the effect of imprisonment upon him.

It was impossible to contemplate without horror the spectacle of the Government’s attempt to overcome the wife’s resistance by the spectacle of her husband’s sufferings.

If she added to his pain by humiliating surrender, it would lower the high ideal he cherishes of her principles.

“She dare not do it; she will not do it!” exclaimed Mr. Williams. He added that he had had an opportunity of waiting upon the Inland Revenue Board and tried to show them how their action appears to outside people.

He had suggested that, in order to bring the law into harmony with justice, representative public men in co-operation with the Board should approach the Treasury to secure an alteration in the law.

“But,” declared Mr. Williams, “if women are made responsible by law it will not bring the Government an inch nearer the solution of the difficulty.

They may imprison women for tax resistance, but married men would not stand it.

The only way is to say to Dr. Wilks, “We will give you the right to control the use we intend to make of your money.”

The resolution was passed unanimously with great enthusiasm, and thus ended a meeting that will be historic.

The Campaign.

A great campaign is being carried on for the release of Mr. Mark Wilks.

On , the Women’s Tax Resistance League held a meeting, followed by a procession in the neighborhood of the prison, and on Sunday there was a large and very sympathetic meeting in Hyde Park.

Mrs. Mustard took the chair.

Mrs. [Charlotte] Despard and Mrs. [Margaret] Parkes were the speakers.

The resolution demanding the release of Mr. Wilks was carried unanimously.

Nightly meetings are held in Brixton by the Men’s Federation for Women’s Suffrage.

A great demonstration will take place on , in Trafalgar-square.

Members of the Women’s Freedom League and all sympathisers are asked to come and to bring their friends.

There will be a large attendance of London County Council teachers — more than 3,000 of whom have signed a petition against the arrest of Mr. Wilks.

A deputation of Members of Parliament and other influential men is being arranged by Sir John Cockburn to wait upon Mr. Lloyd George and to see him personally about the case.

We hope earnestly that before this issue of our Vote appears, news of the release of Mark Wilks will be brought to us.

It seems to us impossible that the authorities of the country can persist in their foolish and cruel action.

But, in the meantime and in any case, it may be well for us seriously to consider the situation.

We are bound together, men and women, in a certain order.

For the maintenance of that order, it has been found necessary for communities and nations all over the world to impose laws upon themselves.

In countries that call themselves democratic, it is contended that the civil law is peculiarly binding, because the people not only consent, but, where they have sufficient understanding, demand that the laws which bind them shall, in certain contingencies, be made or changed or repealed according to their need, and because by their voice they place in seats of power the men whom they believe to be honest and wise enough to carry out their will.

That, at least, is the ideal of democracy.

For several generations the British nation has claimed the honour of being foremost in the road that leads to its achievement.

We (or rather the men of the country) boast of our free institutions, of our free speech, of the liberty of the individual within the law to which he has consented, of the right to fair trial and judgment by his peers when he is accused of offences against that law; above all — and now we have the difference between a democratically governed country and one under despotic rule — not to be liable to punishment for the omission of that which he is unable to perform.

It seems clear and simple enough — what any intelligent schoolboy knows; and yet our so-called Liberal Government, which flaunts in every direction the flag of democracy, which proclaims, here severely and there with dulcet persuasion, that liberty for all is their aim, and that “the will of the people shall prevail,” does not hesitate, when it is question of a reform movement which it dislikes and despises, to set itself in direct opposition to its own avowed principles.

For what do the arrest and imprisonment of Mark Wilks mean?

We are perfectly certain that it will not last long.

Stupid and inept as it has been, the Government, we are certain, will not risk the odium which would justly fall upon it if this outrage on liberty went on.

A Government which has much at stake and which lives by the breath of popular opinion cannot afford to ignore such strong and healthy protest as is being poured out on all sides.

To us, who are in the midst of it, that which seems most remarkable is the growth of public feeling.

In the streets where processions are nightly held, we were met at first by banter and rowdyism.

“A man in prison for the sake of Suffragettes!”

To the boy-mind of the metropolis, on the outskirts of many an earnest crowd, that seemed irresistibly funny; but thoughtfulness is spreading; into even the boy-mind, the light of truth is creeping.

If it had done nothing else, the imprisonment of Mark Wilks has certainly done this — it has educated the public mind.

It is not we, the Suffragists alone — it is women and men in hosts who are asking, What do these things mean?

On the part of these in our movement they mean courage, determination, skilful generalship — aye, and speedy triumph.

On the part of our opponents, perplexity and failure.

“This is defeat, fierce king, not victory,” said Shelly’s Prometheus, when from his rock of age-long pain he hurled heroic defiance at his tormentor.

The ills with which thou torturest gird my soul To fresh resistance till the day arrive When these shall be no types of things that are.

Woman, in this professedly liberty-loving country, may echo the hero’s words.

Defeat, in very truth, for what can the authorities do?

Their position is an extraordinary one.

In a lucid interval, politicians — not clearly, it may be, understanding the issues involved — passed the Married Women’s Property Act.

We believe there were no Antis then to guide and encourage woman-fearing man.

This may partly account for it.

In any case, the deed was done.

Married, no less than single women and widows, became owners of their own property and lords of their own labour.

It would have saved the country from much unnecessary trouble if, then, politicians had gone a step further, if they had recognised woman’s personal responsibility as mother, wage-earner or property-owner, and had dealt with her directly.

Love of compromise, unfortunately, weighs too deeply on the soul of the modern politician for him to be able to take so wise a course, and it is left for his successor to unravel the tangle.

What are the authorities to do?

While, with threats of violence and dark hints of disciplined, organised resistance, Ulster defies them, Suffragists by almost miraculous endurance are breaking open prison doors.

While brutal men, under the very eyes of a Minister of the Crown, are torturing and insulting women, in token, we presume, of their devotion to him, the story of the wrongs of women — not only these but others — is being noised abroad.

None of our recent publications has been bought so freely as “The White Slave Traffic.”

While well-known women tax-resisters are left at large, a man who has not resisted, but who respects women and will not coerce his wife, is arrested and locked up in prison without trial, and, since he cannot pay, for an indeterminate time.

A pretty mess indeed, which will take more than the subtlety of an Asquith, a Lloyd George or a McKenna to render palatable to the men on whose votes they depend for their continuance in power!

In a few days they will be faced with a further difficult problem.

Women are prepared to resist, not only the Income, but also the Insurance Tax.

Let us see what the alternatives are.

Mark Wilks may be let out as Miss [Clemence] Housman was; but that will not help the Government.

It is a poor satisfaction to a creditor of national importance to know that his debtor is or has been in prison.

He wants his money, and the example of one resister may be followed by many others.

If so, that big thing the Exchequer suffers.

The creditor may, when Parliament comes together, pleading urgency, pass an Act which will make married women responsible for their own liabilities.

That might result in a revolt of married women which would have serious consequences.

Men who live at ease with their children, shepherded by admirable wives, would find it, to say the least, inconvenient to be deprived periodically of their services.

And these men might be in the position of Mark Wilks.

They might not be able to pay, while their wives might have no goods on which distraint could be made.

Truly the position would be pitiable.

Over the Insurance Act the same difficulties will arise.

What is a distraught Government to do?

The answer is clear.

The one and only alternative that lies before our legislators is at once to take steps whereby women — workers, mothers, property-owners — shall become citizens.

That done, we will pay our taxes with alacrity; we will bring our quota of service to the State that needs our aid, and the unmannerly strife between man and woman will cease.

In the meantime, the law and the legislator are defeated ignominiously, and it is becoming more and more evident that, in a very near future, “the will of the people shall prevail.”

It would be very difficult, if not impossible, to devise a situation which would show more clearly than does the Wilks’ case, how absolutely incapable is the average man of grasping a woman’s point of view, or of realising her grievances and legal disabilities.

For seventy years men have been cooly appropriating the Income-tax refunded by the Inland Revenue on their wives incomes.

Did anybody ever hear of a man raising a protest against the state of the law which made it possible and legal for a husband to do this?

My own experience covers a good many years of Income-tax work, and the handling of some hundreds of cases, but the only complaints I have ever heard have come from the defrauded wives.

I have observed that the men always accepted the position with the utmost equanimity.

But now, when by the exercise of considerable ingenuity, women have contrived, for once in a way, to put the boot on the other leg, the Press and the public generally is filled with horror, and the air is rent with shrieks of protest from the male sex.

The Evening News sapiently remarks that women might have been expected to have more sense than to seek to show up a law which is “so obviously in their favour”!

And The Scotsman says: “One would imagine that the last thing the Wilks’ case would be used for is to illustrate the grievance which woman suffers under the law.

Here two laws combine to favour the wife and inflict wrong upon the husband.”

And it goes on to deride women and “their inherent illogicality.”

Here we see clearly manifest the absolute incapacity of man to realise the existence of any injustice until it touches himself or his fellow man.

Nothing could well be more logical than the holding of a man responsible for non-payment of his wife’s Income-tax, since it is the necessary and inevitable corollary of the theory that a wife’s income belongs to her husband, and that all refunds of Income-tax must be made to him, and to him only.

It is in accordance with logic and also with strict business principles that no person can claim the advantages of his legal position while repudiating its disadvantages.

Thus if a man dies leaving money, his son cannot claim to take that money and at the same time repudiate his father’s debts.

He must accept the one with the other.

And in exactly the same way, women are no longer going to allow men to claim their legal right to demand re-payment of their wives’ Income-tax, unless they also accept their legal responsibility for its non-payment.

The game of heads-I-win-tails-you-lose is played out, and the sooner men realise this fact the better it will be for everybody.

The “logic” of The Scotsman and its contemporaries is no longer good enough for women.

The law must be forced to take its course where men are concerned as it does where women are concerned.

As to the provisions of the Income-tax Act favouring the wife and wronging the husband, I can only say that Mr. Wilks’ case is the first in all my experience where these provisions acted adversely to the husband.

And even in this case they only so acted because women had laid their heads together to bring it about, and thus show how little men relish a law of their own making when it begins to act on the boomerang principle, and they find themselves “hoist with their own petard.”

A few actual instances, casually selected out of a large number, will show how wives have hitherto been “favoured.”

A man and his wife have £100 a year each, taxed (at 1s. 2d. in the £) by deduction before they receive it.

There are four children, on each of whom the husband is entitled to claim a rebate of £10 a year.

(The wife, it should be noted, can never claim any rebate whether she has a dozen or a score of children.

And if a widow, having children, re-marries, the rebate on these children goes to their step-father.)

Consequently the husband can, and does, reclaim not only the tax deducted from his own income, i.e. £5 16s. 8d., but also the £5 16s. 8d. deducted from his wife’s income.

So he really pays no tax at all, and gains £5 16s. 8d. while she loses a similar amount.

Thus the actual position is, that the wife is only worth £94 a year, while he is worth £106 a year, though nominally their incomes are the same.

If single, each could claim repayment of £5 16s. 8d., therefore marriage represents a loss to the wife, but a profit to her husband.

A member of the Women’s Freedom League was forced to leave her husband on account of his misconduct, and to bring up and educate her children without any financial aid from him.

But for a number of years he regularly drew the “repayment” of her Income-tax, until a merciful Providence removed him from this mundane sphere, by which time it was calculated that she had lost, and he had gained, about £200. At his death she, of course, ceased to be a legal “idiot,” and was allowed to claim her repayment for herself.

I may remark here that the Income-tax Act has a favourite method of classifying certain sections of the community, namely, as “idiots, married women, lunatics and insane persons.”

I don’t know precisely what the difference is between a “lunatic” and an “insane person,” but doubtless there is a difference, though unintelligent persons might think they were synonymous terms.

As regards the point of resemblance between the “idiot” and the “married woman,” it is rather obscure, but after intense mental application I have succeeded in locating it; and really when somebody illuminates it for you it becomes clear as daylight.

It is quite evident to me that our super-intelligent legislators are convinced that the woman who is capable of going and getting married is an utter “idiot,” and in fact next door to a “lunatic.”

Well, men ought to know their own sex, and if they say that the women who marry them are idiots, it must be true, I suppose.

We may therefore take it that a woman evinces her intelligence by remaining unmarried.

I ought humbly to explain that, being married myself, I am only one of the idiots, and therefore my ideas on any subject must not be taken to have the slightest value.

But to return to our instances of “favouritism,” another man has £230 a year and his wife £170 a year.

She pays Income-tax (deducted before receipt) to the tune of £9 18s. 4d., and he pays 2s. 6d..

It sounds impossible, perhaps; but when you know the rules it is quite simple.

To begin with, he gets an abatement of £160, which leaves him with £70. Then he gets a further abatement of £67 for insurance premiums, a great part of which premiums are paid by his wife on her own life.

This leaves him with a taxable income of slightly over £3, on which he pays 9d. in the £1., amounting to half-a-crown.

This couple have no children.

If they had any he would begin not only to pay no tax himself, but to have some of hers repaid to him.

She, however, under any circumstances, will always be mulcted of the £9 18s. 4d.; unless she becomes a widow, when she will be able to reclaim the whole amount.

(The official forms supplied to those reclaiming Income-tax read: “A woman must state whether spinster or widow.”)

If we reverse the financial position of this couple, and assume that she receives £230 and he only £170, she would then be paying £13 8s. 4d. Income-tax.

Contrast this with his payment of half-a-crown in the same circumstances, and observe how highly she is “favoured.”

He, however, would then pay nothing and would receive a “refund” of nearly £3 10s. a year.

A very enterprising and smart young fellow was able to treat himself to a really nice motor-cycle — not the sort that has a side-car for a lady — out of his wife’s “repaid” tax; repaid to him, I mean.

He can’t support himself, but depends on her, as she has just about enough for them both to rub along on, though she can’t afford luxuries for herself, and wouldn’t have paid for his.

But the Inland Revenue gave him her money quite cooly and without the slightest fuss.

The “Scotsman” will be pleased to hear that this poor husband manages to bear up quite bravely under his “wrongs,” and seems indeed to get a considerable amount of satisfaction out of them.

His wife, I am truly sorry to say, doesn’t properly appreciate the favour shown to her by the law.

But then men are naturally brave, and women are by nature a thoroughly ungrateful lot I expect, if they could only see themselves as The Scotsman and The Evening News see them.

In this connection it is interesting to note that three years ago two members of our Edinburgh Branch, the Misses N[annie]. and J[essie].

Brown, walked from Edinburgh to London, chatting of Woman Suffrage with the villagers all along the line of route southwards, many of whom had then not even heard about this question.

They started from Edinburgh in and reached London before .

A further point of interest is that the father of these ladies was the last political prisoner in Claton Gaol in .

Mr. Brown’s offence was his refusal to pay the Annuity Tax which he considered an iniquitous imposition.

He was imprisoned for one week, but received the treatment of a political prisoner; he had the satisfaction of knowing that his protest led to the repeal of the Annuity Tax.

The next people who committed a political offence in Edinburgh were two Suffragettes, who — fifty-two years later than Mr. Brown’s incarceration — were imprisoned, but were not treated as political prisoners.

Notwithstanding the showers a good crowd gathered on to hear Mrs. Despard, who spoke of the anomalies existing in our laws affecting women and taxation, and referred at length to the imprisonment of Mr. Mark Wilks for his inability to pay his wife’s taxes on her earned income.

A resolution expressing indignation at this and demanding Mr. Mark Wilks’ release was passed with only five dissentients.

The chair was taken by Mrs. Mustard, who told the audience of the indignation felt by the Clapton neighbours and friends of Mr. and Dr. Elizabeth Wilks over his imprisonment.

…On evening we had our usual open-air meeting.

Mr. Hawkins kindly chaired, and Mrs. Tanner spoke with her usual excellency, bringing in the “Wilks” case in her speech, as a specimen of anomaly in law in which the man suffers.

The crowd was sympathetic as regarded “poor old Wilks,” but was swayed otherwise by mistaken ideas of our aims and motives.…

The release of Mr. Mark Wilks, under precisely the same circumstances as the release of Miss [Clemence] Housman — that is to say, after a futile imprisonment, a series of defiant suffrage demonstrations, and with no sort of official explanation — is a triumph for the Women’s Tax Resistance League, the W.F.L., and the various men’s association[s] that helped to conduct the protest campaign.

It is more than a triumph; it is an object lesson in how not to do things.

To incarcerate a helpless and innocent man for his wife’s principles, knowing that that wife was one of a movement that never strikes its colours, was foolish on the face of it.

(That it was also unjust is a matter which we recognise to be of little consequence in the eyes of those who make and administer our law).

But to let him out without rhyme or reason seems foolishness of so low a degree that it is only to be described as past all understanding.

One is reminded of the genial duffer who protested that he might be an ass, but he was not a silly ass.

Our highest authorities are not so particular about their reputations as the stage idiot.

The Pity of It.

Yet we are all set wondering what is behind it all.

Is it a contempt so great for the intelligence of the public on which they batten which makes our rulers so unconcerned about even the appearance of wisdom or consistency?

Or is it sheer contempt for women which makes them bully, badger, and torture in turns, and then dismiss the matter as of not sufficient importance to pursue?

It is too easy and flattering a solution to determine that ministers have been impressed by the women’s resolute defiance.

It hardly accounts for the milk in the cocoanut.

Nothing, for instance, would have been easier than to give Mrs. [Mary] Leigh and Miss Evans first-class treatment, and keep them in durance for months and years!

The release of the latter lady at the same time as Mr. Wilks points, we sadly fear, not to an intelligent appreciation of the gathering forces of progress and humanity, but a cruel and callous disregard of wisdom, righteousness, and decency.

If this be “representative” government, it is a sorry testimonial to the worth of the [sic] those represented.

Terminological…?

No tale appears too farcical to present to the tax-payers on behalf of the Government.

One explanation that has been seriously offered, with a view to relieving the Chancellor of the Exchequer from any odium that may be incurred by those responsible for the Wilks imbroglio, is as follows: “The Chancellor knew nothing of the case.

His official correspondence followed him during his recent Welsh peregrinations, missing him everywhere, and only catching him up on his return to London, where he at once ordered a meeting of the Board of Inland Revenue, on whose report (unpublished) he acted promptly.”

Now this is a little too thin.

Wanted, a Good Lie.

The political and militant organiser of the W.F.L., who pens these lines, has to confess with emotion that during recent wanderings in the fastnesses of the Land of George, certain correspondence, re-addressed to divers and sundry humble cottages in mean streets, did indubitably go astray.

But the political and militant organiser is not a world-renowned personage who on occasion has been reduced to the Royal necessity of travelling incognito.

The more than Royal progress of the Carsons and the Georges does not lend itself to these subterfuges; and we feel inclined to give the Chancellor the advice addressed by a too intelligent master to a schoolboy of our acquaintance, whose effort at explanatory romance was not convincing: “No, no, George, my lad; that doesn’t sound likely.

Run away and think of something better.”

In consequence of the release of Mr. Mark Wilks, a sprightly account of which appeared in The Evening Standard, the proposed demonstration on Trafalgar-square was not held by the Women’s Tax-Resistance League .

The main issues which have been brought forward by this new phase of the struggle are:— “That the present irregular method of administering the Income-tax and Married Women’s Property Acts amount to a penalty on matrimony; that the relief afforded to persons of limited income is unjustly and illegally filched from them; and that the Tax Resistance campaign has for one of its objects the determination to secure to the public one million and a half of money which is at present improperly diverted from the pockets of the people to the Government coffers.

It took a woman expert — Mrs. [Ethel] Ayres Purdie — to fathom the real meaning of the law as it is administered to-day; and it is some considerable time since she expressed the opinion, and was laughed at by male legal experts for so doing, that the situation which actually arose was possible.

At Bolton.

A tax-resistance meeting was held at Bolton on , at which Mr. Isaac Edwards presided, the speakers being Miss Hicks and Mrs. Williamson-Forrestier.

The meeting was a public one, explaining the policy and principle of Tax Resistance, and was well attended.

The goods of Mrs. Fyffe, hon. treasurer of the Women’s Tax Resistance League, member of committee of the Horsham and South Kensington Branches of the National Union of Women’s Suffrage Societies, and hon. secretary of the London “Common Cause” Selling Corps, have been seized for tax resistance, and will be sold on , at Whiteley’s Auction Rooms, Westbourne-grove.

A procession will form up at Roxburghe Mansion, Kensington-court, at and start at going to the corner of Westbourne-grove and Chepstow-place, where a Protest Meeting will be held.

Mrs. [Anne] Cobden Sanderson, Mrs. [Caroline] Louis Fagan, Mrs. [Margaret] Kineton Parkes, and others will speak.

The procession will then go on to the sale.

It is hoped that as many members of the Freedom League and other Suffragists as can will support Mrs. Fyffe by walking in the procession and attending the sale.

Mrs. Fyffe, who is an ardent Tax Resister, was presiding at a meeting of the Kensington branch of the National Union (London Society) at her own house, when the bailiffs arrived to distrain on her goods.

It was a novel experience for the non-militant ladies!

Pleasant Amenities.

Mrs. Louis Fagan, summoned at West London Police-court for non-payment of taxes in respect of motor-car, man-servant, and armorial bearings, had quite a merry dialogue with the presiding genius, Mr. Fordham, who waxed — might one say waggish?

— during the encounter.

After refusing to discuss her “conscientious objections” — while in no way belittling them — he imposed a penalty of 20s. and 2s. costs in respect of the man-servant; £10 2s. costs in respect of the motor-car; and 2s. 6d. for the armorial bearings.

Mrs. Fagan represented that her conscientious objection included fines as well as taxes, and he expressed regret at having no alternative to offer save imprisonment.

“I shall sentence you to a month,” he said, “but you won’t do it, of course — you ladies never do.

If I really wanted you to have a month, I should have to call it five years!”

With such little pleasantries the affair passed off in the happiest manner; and Mr. Fordham was equally obliging in fixing the time for the distraint on Mrs. Fagan’s goods “at the earliest possible moment,” to suit the lady’s convenience.

The goods were seized on ; and all Women’s Freedom League members who know anything of the way in which the sister society organises these matters should attend the sale in the certainty of enjoying a really telling demonstration.

Mr. Lansbury’s Chivalry

At a meeting held in the Hackney Town Hall on to demand the release of Mr. Mark Wilks, Dr. Elizabeth Wilks and the Rev. Fleming Williams, who were received with enthusiasm, both addressed the audience, and a resolution of protest was carried unanimously.

The stirring speech given by Mr. [George] Lansbury contained valuable hints for Suffragists.

“Parliament,” he said, “did not do more for the cause of the women because the women did not make themselves felt sufficiently.

If, instead of remaining Liberal, Conservative, or Socialists, they went on strike against the politicians, they would get what they wanted.

“Many years ago, Mr. Lansbury continued, he had believed in the honesty of politicians, and in the sincerity of political warfare, but much water had flowed under the bridges since then, and many new ideas had gone through his head.

What was of most importance to the women of this country was not politics — whether Tory or Liberal — but the emancipation of their sex.

“The imprisonment of Mark Wilks, though it might be a laughing matter to the daily Press, was no laughing matter for the man imprisoned.

It was a jolly hard thing for Mr. Wilks.

He believed that if the working-class women of this country could be got to realise that his was no mere fight for a vote, but a fight for their complete emancipation, they would soon get this sort of thing altered.”

Resistance in Scotland

The Glasgow Herald tells us that:— “Dr. Grace Cadell, Leith, has, as a protest against the non-enfranchisement of women, refused to pay inhabited house duty on a property belonging to her in Edinburgh.

Several articles of her furniture have been poinded to meet the amount of the tax, about £2, but so far the authorities have not taken these away.”

We are also expecting news of the distraint on Miss Janet Bunten’s property for the same reason.

Miss Bunten, Hon. Sec. of the Glasgow Branch, has already lost goods in this manner, and has also been sentenced to imprisonment for refusal to pay dog license or fine in default.

The other day a woman, an utter stranger to me, came into the office to seek advice.

She was a pale, worried little creature, and had a little blind child.

Her trouble was that she had had to leave her husband on account of his brutality — he seemed to be a thoroughly bad lot — and had returned to her parents with the child.

She never saw her husband, nor received any money from him, but he was getting her Income-tax repaid to him.

Her income was very small, and she needed it all for herself and her child, and asked how this procedure could be stopped and the money obtained for her own wants.

I could only tell her that nothing could be done, as the law held that her income belonged to her husband, on hearing which, she broke down and sobbed bitterly, saying she had thought that women might be able to help her.

These are cases one hears of every week, but the Press remains conveniently silently about such, and reserves all its sympathies for the “wronged” husband.

These repayments often amount to quite respectable sums, perhaps as much as £40 or £50, for a three years claim.

I must say that personally it is terribly distasteful to me, when I have recovered tax deducted from a married woman’s income, to be obliged to draw the cheques in favour of her husband, though morally the money is hers.

Yet this is what I am forced to do for my own protection, as, if I handed the money to its real owner, I should still have to pay it to the husband in addition.

He could sue me in the County Court for it, or I might perhaps be charged with “feloniously misappropriating” his money, if I dared to hand it to the wife.

The isolated case of Mr. Wilks is a relatively small matter when compared with numerous cases of defrauded wives.

Mr. Wilks, being released, will have saved £40 by imprisonment, and lots of these wives would joyfully do a few weeks in Holloway, if thereby they could save their money.

What we want to do is to get the law altered, and the Married Women’s Property Act recognised by the Crown, so that marriage shall not involve the brand of “idiocy” and a financial penalty for a woman.

But there seems to be a general impression abroad that the only injustice lies in Mr. Wilks being imprisoned, and not in the law being as it is; and that as he has been got out, that will be the end of the whole thing, and nobody need trouble about it or make any further fuss, unless and until another husband finds himself held liable for tax on his wife’s income, and put in prison for not paying it.

Whether people are Suffragists or Anti’s or neutrals, it is equally to their interest to get the law brought up-to-date.

The Anti husband of an Anti wife might quite as easily find himself in Mr. Wilks’ position, and “tax-resistance” has nothing to do with it, because Income-tax on a wife’s income may be demanded from a husband quite without his wife’s knowledge.

There is a case going on at the present time where 2s. 8d. is being demanded from a man for Income-tax on some Consols which the authorities state are held by his wife.

She has never been asked to pay it, and is not even aware that it is being demanded from him.

He disputes paying it on the ground that he has no evidence that she possesses any Consols, as he has never asked her anything about her means and never intends to do so.

He has formally appealed against the charge, and at the hearing of the appeal his wife’s name was not mentioned, nor her existence even referred to, as the Consols in question are legally deemed to be in his possession.

This husband will doubtless be put in prison in due course.

He contends, quite logically, that if he is held liable for the tax on one of his wife’s investments, he ought to be held equally liable for the tax on all of her other investments, and while the whole position remains so unsatisfactory and anomalous he will pay nothing and do nothing, but will remain simply passive.

At the hearing of the appeal two highly-paid Special Commissioners, drawing, I believe, at least £1,000 a year each, sat to consider the matter.

There was also present a Surveyor of Taxes, who had come up on purpose from Brighton at the public expense, the appellant and his legal representative (myself).

This gentleman and I wasted our valuable time, and the three Revenue officials wasted their time (and the public’s money) for upwards of an hour, discussing a matter involving 2s. 8d., and the existence or non-existence of some Consols which none of the persons present knew anything about.

There were also one or two clerks who took everything down; and altogether it was a most amusing demonstration of the methods of the Circumlocution Office, and the sublime art of How Not To Do It.

Numbers of married women invest their money in order to escape from the anomalies of the Income-tax Act, so some day we may see an equal number of husbands being called upon to pay tax on these investments (which they know nothing about), and ultimately getting locked up sine die.

When men in considerable numbers begin to feel the shoe pinching, probably some serious effort will be made to amend the law.

In the course of a well-reasoned speech, Mrs. Cobden-Sanderson said: We live in revolutionary times.

The will of the people must prevail.

The Portuguese Royal Family fell because it did not consider this.

Berlin has also revolted, and the revolt there would have been more sanguinary had it not been for women, who placed themselves in the front — themselves and their children — and it takes much self-sacrifice to sacrifice your child.

Here the women are also in revolt against the social and economical condition of things, for similar grievances prevail here to those which prevail in Tariff Reform Germany.

Mr. Lloyd George will be attacked more severely.

Hitherto he has had some unpleasant moments; now we are going to attack his pocket.

We are going to have our say in the spending of twelve millions on Dreadnoughts, and also on the reform of Poor Law system.

I am a Poor Law guardian, but I am almost ashamed to own it, for I find the whole system of Poor Law administration is rotten to the core, and I work harder as such than in presenting petitions at Downing Street.

Our next move is to pay no taxes.

It is the most direct and unanswerable method.

If we are not good enough to vote, we are not good enough to pay.

No vote, no tax.

Those little income-tax forms, Form Ⅳ. or Ⅵ., or some other number, will be just thrown into the basket and not returned.

Everyone who perhaps has not an income to be taxed can have a dog, and then refuse to pay tax.