For , retired social worker and lifelong peace activist Esther Kisamore has received threatening phone calls and letters from the Internal Revenue Service because she refuses to pay federal income taxes and federal excise taxes on her telephone bills.

Lawyer Bill Durland and his wife, Genie, have appeared in tax court numerous times since and had their Social Security checks garnished by the IRS.

Psychologist Donna Johnson had two houses seized and eventually returned.

The Colorado Springs residents were aware of such possible consequences when they deliberately snubbed tax time — not to have extra money in their pockets and not because they don’t believe the government should tax citizens.

They don’t want their taxes used to fund military spending and war efforts.

“It is an individual act of moral conscience,” [Peter] Haney said.

“In Colorado Springs close to 50 percent of our primary employment comes from military bases and defense contractors, so we’re so reliant on the federal dole, yet many of us have a frontier mentality to be independent and self-reliant.”

Before Johnson reduced her income to below the taxable rate, she paid half of what she owed in federal income taxes.

Her first house was seized by the IRS for nonpayment of the phone excise tax, about $7. She eventually got the house and another one back, and the $200,000 she owed in taxes and liens on her property were released after a statute of limitations ran out.

“You just stand up and say ‘I’m not willing to pay even though you threaten me,’ ” Johnson said.

I regretted that Charles Purvis’s petition for a writ of certiorari in his

Supreme Court appeal was not available

on-line. It’s a good example of someone trying to get the

U.S. government to

take seriously what its prosecutor, Supreme Court Justice Robert Jackson, said

at the Nuremberg trial of German “war criminals”:

And let me make clear that while this law is first applied against German

aggressors, the law includes, and if it is to serve a useful purpose it must

condemn aggression by any other nations, including those which sit here now

in judgment. We are able to do away with domestic tyranny and violence and

aggression by those in power against the rights of their own people only when

we make all men answerable to the law. This trial represents mankind’s

desperate effort to apply the discipline of the law to statesmen who have

used their powers of state to attack the foundations of the world’s peace and

to commit aggressions against the rights of their neighbors.

Fat chance, but there’s something to be said for making the effort. Anyway,

here, on-line for the first time as far as I can tell, are excerpts from the

Purvis writ, as presented by his attorney William Durland (and as found in

Durland’s book People Pay

for Peace). Afterwards I’ll share some of my thoughts:

The decision below as it applies to Petitioner, a Quaker, and war tax

refuser, causes him to become a party or an accessory to a criminal act in

violation of international law, the United States Constitution, the criminal

statutes of the United States and his conscience.

To compel the petitioner to pay federal income tax deficiencies and additions

as war taxes makes him a party of an accessory to a criminal act in violation

of international law and Article Ⅵ of the United States Constitution.

International Law is Applicable to Cases Arising in

U.S. Courts

There can be no doubt that international law is relevant and applicable to

cases arising in United States Courts. Article Ⅵ , paragraph 2 of the United

States Constitution provides that:

All treaties made, or which shall be made, under the authority of the United

States, shall be the supreme law of the land, and the judges of every state

shall be bound thereby, anything in the Constitution or law of any state to

the contrary notwithstanding.

When a question arises concerning whether international law is relevant to a

domestic case, it is the duty of the domestic court to determine (1) whether

principles of international law are implicated in the case; if so (2) which

principles of international law are applicable and (3) whether application of

these principles to the case at bar overrides inferior municipal law thus

justifying otherwise allegedly illegal conduct.

In the

Paquete Habana, 175

U.S. 677, 700

(), the Supreme Court declared that:

International law is part of our law, and must be ascertained and

administered by the courts of justice of appropriate jurisdiction as often

as questions of right depending upon it are duly presented for their

determination.

Accord,Hilton v. Guyot.

See generally I Whitman International Law Section 11

(). International law is applicable to

domestic courts. The question is which aspects of international law become

“the supreme law” of the land. Treaties made by the President, “and with the

advice and consent of the Senate” are obviously included by express

provisions of Article Ⅱ, Section 2 of the United States Constitution. The

term “treaty”, though not defined in the Constitution, has generally been

determined to include “irrespective of their nomenclatures, such

international agreements as conventions, pacts, protocols and covenants.”

Introduction to

U.S. Treaties and

Other International Agreements, Cumulative Index, ⅹ

() (Hereafter,

U.S.T.).

What has been termed “customary international law” is also binding on

domestic courts.

Such customary International Law as is universally recognized or has at any

rate received the assent of the United States, and further all international

conventions ratified by the United States, are binding upon American courts,

even if in conflict with previous American statutory law…

Ⅱ Oppenheim,

International Law. 101

(6th

ed.

). “Offenses against the Law of Nations”

have been sustained in federal courts even if there were no statutes defining

the offense under Article Ⅰ, Section 8, Clause 10 of the

U.S. Constitution.

Therefore a substantial body of treaties, international agreements, and

offenses against the Law of Nations or customary international law are

binding on American courts. See Introduction to

U.S.T. Cumulative Index, supra, at ⅺ.

International Law Prohibits Aggressive Policies of “Defense”

There are many bases for determining that American nuclear weapons are in

violation of international law. (Petitioner will present his case against

nuclear planning here rather than the Vietnam War crimes because (1) the

brevity of the writ requires it; (2) the latter has terminated and

(3) the former continues to be a basis for the present refusal to pay war

taxes for past years. However, much of this argument also applies to the

former). Perhaps the most fundamental tenet of all international norms is

that a sovereign refrain from use of or threat of force in its relations with

other countries. This policy has been consistently expressed in various forms

as early as .

In the

Convention for the Pacific Settlement of International

Disputes, , 32

Stat.

1779, 1780, T.S.

392 the parties (including the United States) expressed “a strong desire to

concert for the maintenance of the general peace;” to extend “the empire of

law,” and to strengthen “the appreciation of international justice…”

Accord, Convention for the Pacific Settlement of International

Disputes, , 37

Stat.

2199, 2201, T.S.

536.

Similarly, Article Ⅰ of the Pan American Anti-war Treaty of Non-aggression and Conciliation,

, 49

Stat.

3363, 3375, T.S.

906, states that the parties “solemnly declare that they condemn wars of

aggression in their mutual relations or in those with other states…”

The Charter

of the United Nations, , 59

Stat.

1033, T.S. 993

(hereinafter

U.N.

Charter) is replete with references to the duty to use peaceful means

in international relations. The Preamble expresses a determination “to save

succeeding generations from the scourge of war…”; “to ensure, by the

acceptance of principles and the institution of methods, that armed force

shall not be used, save in the common interest…”

U.N.

Charter, 59

Stat.

1033, 1035. Chapter Ⅰ of the

U.N.

Charter sets forth the purposes of the United Nations. Because these

provisions provide a guiding light in the interpretation of international

law, it is important to develop a firm grasp of these basic principles.

Article Ⅰ provides that:

The Purposes of the United Nations are:

To maintain international peace and security, and to that end: to

take effective collective measures for the prevention and removal of

threats to the peace, and for the suppression of acts of aggression

or other breaches of the peace, and to bring about by peaceful means,

and in conformity with the principles of justice and international law,

adjustment or settlement of international disputes or situations

which might lead to a breach of the peace;

To develop friendly relations among nations based on respect for the

principle of equal rights and self-determination of peoples, and to take

other appropriate measures to strengthen universal peace;

[E]ncouraging respect for human rights and for fundamental freedoms for

all…

U.N.

Charter at 1037 (emphasis added).

In Article 2, the members agree to “fulfill in good faith the obligations

assumed by them” in the Charter; to “settle their international disputes by

peaceful means in such a manner that international peace and security, and

justice, are not endangered” to “refrain in their international relations

from the threat or use of force…” or to act “in any other manner inconsistent

with the purposes of the United Nations.”

U.N.

Charter at 1037.

International Law Prohibits Specific Planning for and Acts of

Aggression

The Hague

Convention Respecting the Laws and Customs of War on Land,

, 36

Stat.

2277, T.S. 403

(hereinafter, Hague Conventions), was “inspired by the desire to

diminish the evils of war…” 36

Stat.

at 2279. The Convention declares that where no specific international

regulation addresses a specific course of conduct, that the parties follow

“the principles of the law of nations, as they result from the usages

established among civilized peoples, from the laws of humanity, and the

dictates of the public conscience.” 36

Stat.

at 2280. Article 22 of the Convention provides that “[t]he right of

belligerents to adopt means of injuring the enemy are not unlimited.” 36

Stat.

at 2301. Most importantly, Article 23 provides:

In addition… it is especially forbidden:

To employ poison or poisoned weapons;

To kill or wound treacherously…

To employ arms, projectiles, or material calculated to cause unnecessary

suffering…

36

Stat.

at 2301–02.

Article 24 prohibits the bombardment of villages, towns, or cities which are

undefended. 36

Stat.

at 2302, while Article 27 declares that in sieges or bombardments all

necessary steps must be taken to spare buildings dedicated to religion, the

arts, science, or caring for the sick and wounded. 36

Stat.

at 2303.

The Charter of

the International Military Tribunal

, 59

Stat.

1544, E.A.S. 472 (“London Agreement

enunciating the Nuremberg Principles”) (Hereinafter, Nuremberg

Charter) outlined violations of international law for which even

individual citizens of belligerent nations could be held responsible. Article

6 provides that:

The following acts, or any of them are crimes… for which there shall be

individual responsibility:

Crimes Against Peace: namely, planning, preparation… of a war of

aggression or a war in violation of international treaties, agreements

or assurances, or participation in a common plan… for the

accomplishment of any of the foregoing.

War Crimes: namely, violations of the laws and customs of war.

Such violations shall include but not be limited to, murder,

ill-treatment… of civilian populations… plunder of public or private

property, wanton destruction of cities, towns or villages…

Crimes Against Humanity: namely, murder, extermination… and

other inhuman acts committed against any civilian population before or

during the war or persecutions on political, racial or religious

grounds in execution of or in connection with any crimes… whether or

not in violation of the domestic law of the country where

perpetrated.

Article 7 went on to provide that the “fact that the Defendant acted pursuant

to order of his [sic.] Government

or of a superior shall not free him from responsibility.”

Charter at 1548.

In the United States delegation to the

United Nations introduced a Resolution before the General Assembly affirming

“the Principles of International Law recognized by the Charter of the

Nuremberg Tribunal.”

G.A.

Res. 95(1),

U.N.

Doc.

A/64/Add. 1, at 188

(). The Resolution was unanimously adopted

by the General Assembly on . In the Nuremberg Principles

were restated by the International Law Commission. Finally, the United

Nations Security Council, by Resolution, condemned acts of “reprisals as

incompatible with the Purposes and Principles of the United Nations.”

G.A.

Res. 188, Session ⅩⅨ,

4/1/1964.

U.S. Policies

and Development of Nuclear Weapons are Inconsistent with International

Law

There can be no doubt that the actual aggressive use of atomic weapons

results in almost total destruction of everything within several miles of the

site of the explosion. See United States Department of Defense, The

Effects of Nuclear Weapons (). The

residual effects caused by radiation and radio-active fall-out create

long-term illness and death in a matter analogous to poisoning. See United

States Atomic Energy Commission, The Effects of Nuclear Weapons

(),

p. 473.

The indiscriminate and “wanton destruction of cities” which results from the

use of nuclear weapons is prima facie proof of war crimes,

as defined by Principle VI

of the Nuremberg Charter, and of crimes against humanity, as

defined by Principle VI(c)

of the Charter. Likewise, the poisonous effects of nuclear

radiation and fall-out are prima facie violations of the

United States’ obligations under Article 23(a) of the Hague

Conventions prohibiting the use of “poison or poisonous arms.”

Additionally, Article 23(a) of the Hague Conventions of

and ,

which prohibits the use of “arms, projectiles, or material of a nature of

cause superfluous injury”, and the

Declaration of St. Petersburg

of , which declares that “the only

legitimate object… [of] war is to weaken the military forces of the enemy”,

indicate a customary rule of international law prohibiting weapons of

indiscriminate destruction such as nuclear weapons.

Moreover, the aggressive use of atomic weapons would directly contradict the

express purposes of using best efforts to avoid a nuclear war and negotiate

an end to the nuclear arms race. See discussion,

infra.. And since the radiation-related after effects

of nuclear explosions cannot be controlled, the harm to persons and property

in neutral countries would constitute an act of aggression against third

states. G.A.

Res. 3314, Session ⅩⅩⅨ,

12/14/74.

The real question is whether current policies and weapons are in violation of

international law. To answer this question one must look to the history and

facts of nuclear weapons development.

On the basis that the “planning” or “preparation” for wars of aggression

violates Article 6(a) of the Nuremberg Charter, that “use of

threat of force” is in violation of several treaties including the

U.N.

Charter; that the

U.N.

Charter condemns “situations which might lead to a breach of the

peace,”

U.N.

Charter Art. 1, 59

Stat.

at 1037, and imposes a duty upon members “to practice tolerance and live

together in peace,”

U.N.

Charter, Preamble, at 1035; that the United States has declared an

intention “[t]o prevent the use of atomic energy for destructive purposes”

and to eliminate nuclear weapons from national arsenals,

e.g. Declaration on Atomic

Energy, 60

Stat.

at 1480. Nuclear Non-proliferation Treaty, 21

U.S.T. at 484–85; and that the United

States has promised to work for international peace and security “with the

least diversion for armaments of the world’s human and economic resources” 21

U.S.T. at 486;

U.N.

Charter Art. 26, 59

Stat.

at 1041, the possession of nuclear weapons for future “first strike” use is

violative of international law. The “official” nuclear policy of this country

is one of deterrence or second-strike capability. This concept is aptly

explained by Robert Aldridge who for sixteen years worked in Lockheed

Corporation’s engineering department, designing every submarine-launched

ballistic missile bought by the Navy. Aldridge explains:

Deterrence is the strategic policy under which most of us believe the

Pentagon is still operating. It is presented as a defensive measure, of

sorts, because it is based on a second-strike response — massive and

unacceptable retaliation — which theoretically deters the Soviet Union from

attacking us.

Aldridge, The Counterforce Syndrome () (hereinafter Counterforce)

Aldridge goes on to note that to be an effective deterrent, United States

retaliatory forces would have to survive the worst conceivable attack and

still wreck havoc in the Soviet Union. To this end, land-based ballistic

missiles are stored in underground silos. The fact is that since the late

1960s both the Soviet Union and the United States have possessed this

deterrent capability. Counterforce at 2. To maintain this

“balance” super-powers agreed in S.A.L.T. Ⅰ

(Strategic Arms Limitation Treaty) to refrain from developing elaborate

anti-ballistic missiles (ABMs).

There came a time, however, when actual

U.S. policy

shifted from deterrence to what Aldridge terms “counterforce”. In9

, Aldridge resigned after helping design

three generations of Polaris missiles, the multiple individually-targeted

reentry vehicles (MIRVs) for Poseidon, and

the beginnings of the Trident missile. The cause of Aldridge’s resignation

was his sense of a shift in nuclear policies:

At the onset of the Trident program, I discovered the Pentagon’s interest in

acquiring a precise “counterforce” weapon capable of destroying “hardened”

military emplacements such as missile silos. This was a profound shift from

a policy of retaliating only when fired upon, because it does not make sense

to attack empty silos (which is all that would be left following an enemy

first-strike attack on the United States).

Counterforce at ⅶ.

The S.A.L.T. Ⅰ agreement

froze the number of strategic arms, but did not freeze quality improvements — the area of primary

U.S. emphasis.

Counterforce at 60. The sheer explosive power of these weapons

is unimaginable. According to Senator George McGovern, the

U.S. presently

possesses 8,500 warheads, a combined explosive power of over three billion

tons of TNT, which calculates to about

1,500 pounds of explosive for every man, woman and child on the planet.

McGovern, “End of the World”, Playboy 124, 126

() (hereinafter,

McGovern). But the magnitude of explosive is not as important as

the accuracy of the explosion. Moreover,

S.A.L.T. Ⅰ

did not limit the numbers of strategic warheads (as opposed to strategic

missiles) and thus since

S.A.L.T. Ⅰ

the U.S. has

increased its nuclear warhead stockpile from 4,600 to 9,000 while the Soviet

Union has increased theirs from 2,000 to 4,000. “The

SALT Trap”. The Progressive, p. 9, ().

Additionally, S.A.L.T. Ⅰ placed no

restrictions on production of two weapon systems which have critically

affected the arms race: MIRVs and the cruise missile.

MIRVing missiles means two to fourteen additional independently

targeted warheads to a single missile, giving it the kill potential of many

missiles. The cruise missile is a mobile weapon which flies at altitudes

below the detective capabilities of radar and which can strike within thirty

feet of a target over 2,000 miles distant, according to the

Progressive Magazine.

The dangers in such policies are legion. For one thing, these developments

make it virtually impossible to verify compliance with an arms limitation

agreement. Although satellites can count missiles, submarines or airplanes,

they cannot determine how many warheads are on a given missile.

McGovern at 196.

The United States has retrofitted accuracy improvement systems and

MIRVs

to both land and submarine launched missiles. In

the

U.S. retrofitted

550 Minutemen Ⅲ missiles with the NS-20

guidance system which doubled the accuracy of the 1650

MIRV warheads.

This gave each warhead an even chance of landing within 600 feet of any Soviet

silo with a blast nine times greater than the Hiroshima bomb.

McGovern at 196. Each of the 1,650 Minuteman warheads now has

over an 80% chance of destroying any Soviet silo at which it is aimed.

Other weapons systems currently in development pose an even greater threat of

the risk of outbreak of nuclear war. Lockheed began work in

on a maneuvering re-entry vehicle

(MARV) which permits in-flight alterations

in navigation increasing ever-more the accuracy of the hit. In

, concept studies were initiated for the

Mark 500

MARV

for possible use on Trident missiles.

In the

ABM Treaty was modified to allow only

100 defensive interceptors for each country, thus making nonsense of the

Pentagon rationale that in-flight maneuverability is essential to evade enemy

defense systems.

In the Missile X program was initiated. The

actual implementation of the program began in

. Under this system five to

twenty-five mile trenches will be dug in the Western

U.S. Each trench

will conceal a missile which can be moved back and forth at random, the

assumption being that the Soviets would exhaust their

ICBMs

trying to “find” the missile. The problem is that the Pentagon scenario omits

to consider the fact “that a 20-megaton burst, such as that produced by a

Soviet SS-9 ICBM,

would leave a 75-foot high layer of dirt on the lid if it struck as far as

half a mile away. Missile-X would probably be entombed unless it were planned

as a first-strike weapon.” Counterforce at 27. Moreover, the

trench system once again creates insurmountable verification problems since

“there would be no way the Soviets would be certain that there was only one

missile in any given trench.” Counterforce at 27.

The Trident submarine launched missile system is a floating vessel of

destruction. The 560 foot long Trident carries twenty-four submarine launched

ballistic missiles (SLCMs) each with a

range of 4,000 nautical miles and each equipped with eight 100-kiloton

warheads. The proposed modifications of the Trident submarine, or Trident-2,

carries twenty-four Trident-2 missiles, each with a range of 6,000 nautical

miles, and each capable of “delivering seventeen super-accurate

MARV

warheads to within as few feet as many targets. Counterforce at

25, 26. As Aldridge describes it:

One Trident submarine will be able to destroy 408 cities or military

targets with a blast five times that which was unleashed over Hiroshima.

A fleet of thirty Trident submarines would be able to deliver an

unbelievable 12,240 nuclear warheads against an enemy’s territory — or 30

times the number originally thought sufficient for strategic deterrence.

Clearly, if Trident attains the accuracies the Navy seeks, it will

constitute the ultimate first-strike weapon. Counterstrike at

26.

Once each nation possesses weapons capable of a first-strike, then the risks

of a nuclear war escalate in a geometric progression. The dilemma is that (1)

since each is capable of a first-strike which would presumably cripple the

other’s ability to retaliate, (2) since only 100

ABMs are allowed per side, and (3) since

cruise missiles and other systems can penetrate enemy territory undetected by

radar, then each side will be vulnerable to a crippling first-strike attack

thus tempting each side to devastate the “enemy” before the “enemy”

devastates them. This scenario of mutual nuclear insecurity is only years

ahead. Although the United States is ahead of the Soviets in developing a

first-strike capability, Counterforce at 59, it is only a matter

of time before the Soviets possess an effective first-strike capability.

Perhaps, in anticipation of that day, President Carter announced a

U.S. first nuclear

strike doctrine in his address to the General Assembly of the

U.N. from the

rostrum of the General Assembly on .

…I hereby declare on behalf of the United States that we will not use

nuclear weapons except in self-defense; that is, in circumstances of an

actual nuclear or conventional attack on the United States, our territories

or armed forces, or such an attack on our allies.

New York Times, Transcript of President Carter’s

Address to United Nations General Assembly,

p. A12.

The doctrine is extremely far-reaching:

It announces that the

U.S.

“will” use nuclear weapons (he did not say, for example, “might”

or “reserves the right” or similar words);

Nuclear weapons would be used also in case of attack by “conventional”

weapons;

They would be used also in case of attack by conventional weapons on

U.S. forces

stationed, flying over, or on the high seas, anywhere in the world — for

example, in situations similar to

the Pueblo

incident.

Mr. Carter did not use the language of Article 51 of the

U.N. Charter,

which allows individual or collective self-defense only “if an armed

attack occurs”; the formulation “in circumstances of an

actual attack” is not used in any pertinent international instrument.

Implicit in the phrase is that the

U.S. might use

nuclear weapons also if no armed attack “has occurred”, so that it could

conceivably cover also preventive use of nuclear weapons.

Since the doctrine announces first use of nuclear weapons regardless of

the results (perhaps a

U.S. Air Force

plane was shot at, but not hit?) and, in any case, severity, duration,

and character of the “actual attack”, is not discussed, the doctrine

violates the general principle of proportionality.

The doctrine does not explicitly state that the nuclear weapons would be

used exclusively against the attacking state. Is that omission

deliberate? In other words, is it a revival of Secretary of State Dulles’

doctrine of “massive retaliation of our own choosing”, that is, against a

nation which did not attack but which the

U.S. would

unilaterally hold responsible for the attack?

The doctrine does not say that the attack, to which the

U.S. would

reply with nuclear weapons, was illegal (If a

U.S. bomber or

a bomber of any

U.S. ally

would penetrate the territory of another state, the latter would act

legally in shooting it down).

The doctrine does not refer to the obligation to seek peaceful

settlement before taking such enormous steps, which would be in

contravention of Article 33 of the

U.N.

Charter.

This coupled with the authority of the President under the

War Powers Act, who is therein allowed

to engage in hostilities without declaration of war for a period of 60 to

90 days, violates the Hague Convention

No. 3 of

.

The American nuclear firepower outlined above provides ample basis for

concluding that such systems are violations of international law. (This

analysis was formulated by

Prof. John H.E. Fried,

Former Special Legal Assistant,

U.S. War Crimes

Tribunal, Nuremberg). Dr.

Fried, in a recent paper presented to the Ⅺth Congress, International

Association of Democratic Jurists in Malta, concluded that a first nuclear

strike is forbidden by existing international law because nuclear war (1)

has no rational war aim — its aim is destruction, (2) would prevent obedience

to fundamental rules concerning the conduct of hostilities, (3) would prevent

the carrying out of post battle obligations of belligerents, (4) would make

it impossible to respect the rights of neutral states. The danger of

accidental unintended nuclear war is paramount, causing the dictates of

public conscience to prohibit a first nuclear strike before it takes

place. (See also Art. 18, 1,

Geneva Convention for the Protection of Civilians in Time of War

().)

International Law Imposes a Duty Upon Individual Citizens to Disassociate

Themselves from Violations of Such Law

Since the Nuremberg principles have become a part of international law, the

notion of individual responsibility for war crimes has achieved wide

acknowledgment. (See below). Under the Nuremberg Charter, it is

no defense to claim one was merely following orders. Nuremberg

Charter, supra,

Art. 7. Individual

responsibility attaches if “a moral choice was possible”.

Ex Parte Quirin 317

U.S. 1

(1942).

Professor Falk has found that case law developing during the War Crimes

Trials after World War Ⅱ “established that the zone of individual

responsibility for crimes against peace extended well beyond principal

policy-making and state leaders.” Falk, “The Nuremberg Defense in the

Pentagon Papers Case”, Crimes of War (Falk, Kolko and Liften,

eds.,

) 231. See,

e.g. “The Ministries Case,” Ⅻ–ⅩⅣ,

Trials of War Criminals (). In

the Flick Case, which involved prosecutions of German

industrialists, the War Crimes Tribunal stated:

[I]t is urged that individuals holding no public offices and not

representing the state, do not, and should not come within the class of

persons criminally responsible for a breach of international law. It is

asserted that international law is a matter wholly outside the work,

interest, and knowledge of private individuals. The distinction is unsound.

International law, as such, binds every citizen just as does ordinary

municipal law… The application of international law to individuals is no

novelty.

Quoted in Ⅱ The Law of War: A Documentary History 1283 (L.

Friedman ed.

) (hereinafter Friedman).

Furthermore, the Tokyo War Crimes Trial Decision, reprinted in

Friedman at 1029, suggests that anyone with knowledge of

illegal activity and an opportunity to do something about it is a potential

criminal under international law unless the person takes affirmative

measures to prevent the commission of the crimes. (emphasis added).

Under these considerations an individual American citizen is in violation of

international law if he or she consents to cooperate with any government

which produces, possesses or uses nuclear weapons. (Part of the material

included here is from Graber, “The International Law Defense”,

Pacificus Papers,

Vol. 2,

No. 5, Colorado Springs,

Center on Law and Pacifism, ).

The Applicability of International Law to Taxpayers is Proven

The payment of war taxes to the United States for the years

would have

constituted complicity in the commission of crimes against peace, crimes

against humanity, war crimes in Vietnam and in nuclear planning. A moral

choice to refuse to be in complicity with the commission of such crimes was

available to the Petitioner and he exercised that choice and refused to pay a

war tax. On the point of the nature and extent of individual responsibility,

the Nuremberg Judgment states: “The very essence of the charter

is that individuals have international duties which transcend the national

obligations of obedience imposed by the individual state.”

F.R.D.

69, 110 ().

Fundamental fairness requires that the Petitioner be permitted to rely on

any argument arising from his accountability under international law. That

such a policy extends to the Nuremberg Principles is confirmed by the former

Assistant General Counsel for International Affairs of the Department of

Defense, who acknowledged that “from an international criminal law point of

view… the Nuremberg norms are part of our municipal law and may be enforced

by our courts.” Quoted in Falk, A Global Approach to National

Policy, 112 (). However, Petitioner

has not been given an opportunity to present evidence concerning the

questions of fact contained in this Writ before any court.

Individual liability is determined on the basis of knowledge of war crimes

coupled with inaction. See “The Tokyo War Crimes Trial Decision,” Ⅱ The

Law of War: A Documentary History, 1029 (Friedmann

ed.

). It follows, then, that anyone with

knowledge of war crimes and the opportunity to do something about it is

potentially criminally liable unless that person takes steps to prevent

further commission of the crimes. Even if these principles do not impose an

affirmative duty to act, the imposition of criminal liability on persons

having knowledge of war crimes must create a right in persons to act in a

prudent manner in an effort to halt what they reasonably believe to be

international crimes.

In a due process sense, it is enough that the Petitioner reasonably believed

that the domestic law was superseded by international law. Because domestic

law must be construed in conformity with international law whenever such a

construction is possible, Borchard, “The Relation Between International Law

and Municipal Law,” 27 Va.

L.

Rev., 137

(), it violates due process to subject the

Petitioner to possible criminal liability for tax deficiency in the face of

the contradictory claims on his behavior posed by the domestic and

international law. Due process does not permit the imposition of criminal

liability for tax deficiency (which is possible under the Internal Revenue

Code) for an act intended to terminate complicity in war crimes and its

preparation when the act was justified under relevant principles of

international law.

In , at Nuremberg, Germany, the United

States participated in the prosecutions of persons under principles of

international law imposing criminal liability for deference to municipal law

when they knew, or should have known that their government was

committing violations of international law. It violates the most basic

principles of fundamental fairness and due process for the United States,

while continuing to participate in the punishment of persons convicted of

violating the Nuremberg Principles, to refuse to acknowledge the right of

taxpayer to refuse war taxes in violation of municipal law established by the

Nuremberg Military Tribunal [sic].

Arguments Invoked Against the Applicability of International Law are

Invalid

Usual rebuttals to the international law argument are stated as follows:

(1) “International law does not apply to American courts unless it concerns a

treaty not superseded by a statute.”

As presented aforesaid, this is not so and moreover in the instant case

insofar as the Nuremberg Charter is concerned it has been made part of

domestic law by its incorporation in 59

U.S.

Stat. 1544. (2) “The provisions of the Nuremberg Charter are strictly

limited. Crimes Against Peace only apply to ‘major’ war criminals, and War

Crimes and Crimes Against Humanity are limited to wartime.” In respect to

Crimes Against Peace, Petitioner argues that 18

U.S.C. 960

makes any person within the United States criminally liable. In

respect to War Crimes and Crimes Against Humanity, The Report of the

International Law Commission () at

Principle Ⅵ, paragraph 122 states that “The Tribunal did not, however,

exclude the possibility that crimes against humanity might be considered

before a war.” Finally, as to all three classes of Nuremberg crimes, the

limitation placed upon the jurisdiction of the then court by itself were

self-imposed flowing from its discretionary power due to a desire to strictly

construe the charges because of the initial use of the Charter, the

ex post facto charge against its use, giving the benefit of

the doubt to defendants for that reason. The literal words of the Charter do

not make such discretion mandatory upon future judges or interpretors as this

Court.

International law is progressive. See 2 Mueller, International Criminal

Law, () at 263. No such conditions

apply 35 years later and individuals such as business men and women, ordinary

soldiers or members of war organizations would have been of a sufficient

status then and now to be considered an accessory. See Ⅱ Whitman, Digest

of International Law 885–87, . The

last paragraph of Article 6 of the Nuremberg Charter concerns complicity and

states that “…accomplices participating in the formulation… of a common plan

to commit any of the foregoing crimes are responsible for all acts performed

by any persons in execution of such plan.” See also Mueller at

269. (3) The argument is tirelessly repeated that International Law prohibits

only the use and not the possession of nuclear arms. But the

aforesaid chronology of applicable international law provisions vitiates that

myth. “First Strike” planning puts the lie to that rebuttal forever. If the

law must wait on “use” in this type of case there will be no law or people

left to adjudicate. (4) Finally, these arguments are usually rebutted, if all

else fails, on the basis that they are political in nature and

non-justiciable. This rebuttal is spurious on its face for this Petitioner’s

plea is a plea much more than political. It is a plea for humanity and against

the super-powers of the

U.S. and

U.S.S.R., lest we find our planet destroyed for want of “legal standing”.

Thus the involvement of the United States in Vietnam war crimes and the

formulation of current plans for nuclear war violate international and

constitutional law, and will make Petitioner an accessory to both and

criminally liable if he is forced to pay war taxes for said plans and

preparations. Thus Purvis concludes his argument on international law.

Durland noted that Purvis also made an argument that a domestic statute that

said “Whoever within the United States knowingly begins or furnishes the money

for any military enterprise to be carried on from thence against a territory

or dominion of any foreign state or people with whom the United States is at

peace shall be imprisoned,” also applied to his case.

The law of war is so adorable.

I can’t help but shake my head, sigh, and give a bittersweet smile at the

well-intentioned ridiculousness of it all. I almost sympathize with the White

House torture lawyers who looked at international law and found it “obsolete

and quaint.” Apparently the cutting edge international law thinkers a century

ago seriously contemplated a scene in which officers would lead their troops

to battle with something like, “Okay everybody, to the trenches… but don’t

forget that it’s forbidden by law to kill or wound treacherously!”

And after the 20th century played itself out

anyway, we’re apparently still supposed to take the Hague Convention

seriously.

But there is still something satisfying in trying to hold the

U.S. government to

the principles it so pompously crafted as it was collecting scalps after World

War Ⅱ — watching those principles dissolve in a reductio ad

absurdum where the absurd part is expecting Uncle Sam to agree that what’s

good for his own goose is what was good for der Adler.

Durland complains that “The Supreme Court refused to hear

Purvis and probably will continue to refuse to

recognize the law because the court acts solely out of power when confronted

with morality.” While his conclusion may be valid, I think there may be more

to it than this.

Durland’s “writ” is strangely writ. It is hard for me to imagine Durland

expecting the Supreme Court justices to be impressed by his citations of a

Playboy interview with George McGovern or a

Progressive magazine estimate of the size of the

U.S. nuclear

arsenal. Much of the discussion of arms technology and arms control

difficulties seems not to have much to do with the legal argument and would be

more at home in a for-the-choir think tank article. There’s precious little

citation of legal precedents but plenty of quotation of books and essays and

law review articles and appeals to “the most basic principles of fundamental

fairness” and the like.

Perhaps it wasn’t really intended for the audience to which it was ostensibly

delivered, but then why go through such fuss? It seems to me if you’re going

to bother to try to take a legal argument up the court system, you ought to

try to craft it in a form that will be persuasive to judges. As it is, because

Purvis lost his case and was unable to get the courts to take his argument

seriously, the legal legacy of Purvis

v.

Commissioner is as a precedent for the idea that

…the act of paying taxes does not amount to complicity in any war crime

committed by the Government. [The Eleventh Circuit Court of Appeals citing

Purvis in its ruling against war tax resisters

Robert and Linda Randall in ]

The latest issue of More Than a Paycheck, NWTRCC’s newsletter, is now on-line.

It’s a special edition, commemorating the 30th anniversary of the founding of the committee.

current events in tax resistance including a Pacific Yearly Meeting fund to help tax resisting Quakers, innovations in tax resistance in Spain, and the implications of Mitt Romney’s infamous “47%” comment

ideas and actions including the Afghan Peace Volunteers group, a recent talk radio broadcast about war tax resistance, an on-line penny poll, and updates on a recent Plowshares action and on the Iran Pledge of Resistance

upcoming evens like the NWTRCC national gathering next month in Colorado, the New England regional gathering later this month in Massachusetts, the School of the Americas action in November, and next year’s international war tax resistance conference

Someone shot video at the recent NWTRCC national conference in Colorado Springs.

Some of the highlights include:

Bill Durland recalls the founding and early history of NWTRCC

Ruth Benn compares the work of NWTRCC today with the goals of its founders.

War tax resistance in the Friends Journal in

War tax resistance was a frequent topic in the issues of Friends Journal in , though there was still no consensus about how to go about it, and there was a lot of hesitance among Quaker institutions about how strongly to endorse it.

The issue was another special issue devoted to the peace testimony, which might as well have been a special issue on war tax resistance for how frequently it was mentioned.

Clearly by this time, there was no talking about peace work without talking about war tax resistance.

an illustration by Duncan Harp, from the issue of Friends Journal

Editor Ruth Kilpack opened the issue.

She noted:

I see the billions of dollars (including taxes from my own earnings) being poured into the “defense” budget.

I hear of vastly increased crime and see the wanton waste everywhere, much of it the direct legacy of our last war; I remember the lives still festering in military hospitals, the suffering from the wounds of war both here and across the world.

But now, there is a handful of people who are beginning to take a new view of war and war-making, realizing that it takes place not only when the bombing and shelling begin, but in the will of the people who make — or allow — it to happen.

War-making must be paid for.

As it is said elsewhere in this issue, “we pray for peace, but we pay for war.”

When we once understand that, great change will come about.

And especially, as war becomes more and more impersonal, with computerized strategic commands and weapons, more people are increasingly going to ask, “Who is waging this war?

Are we ourselves responsible, since we pay for it?”

(As the old saying goes, “Your checkbook shows where your heart is.”)

Take Richard Catlett, for example, a Friend who — as I write at this very moment in — is beginning his jail sentence of two months at the Kansas City Municipal Rehabilitation Institute (for first offenders) in Kansas City, Missouri.

That will be followed by three years of probation.

Richard Catlett has been an antiwar activist , refusing to file his income tax return .

In , his health food store was closed for non-payment of taxes (it is now under his wife’s ownership), and now, at sixty-nine years of age, Richard Catlett is treated as a criminal.

Clearly, he is being held up as an example of what can happen to a trouble-maker who dares to go against the tax law.… Richard Catlett’s age gives added emphasis to the warning to those no longer young and foolhardy.

(Besides, the pockets of those in his age bracket are usually better filled, and not to be overlooked by IRS.)

Catlett’s case was covered in more depth later on in the same issue by means of lengthy quotes from a Colombia Missourian article (see “Local war protester leaves for jail term” in ♇ 5 January 2013) and the following section from a Wall Street Journal article:

Tax Report

A protester got loads of publicity that drew criminal charges for nonfiling.

The IRS selects tax protesters for criminal prosecution based on the amount of publicity they get.

Usually protesters who don’t seek the spotlight are pursued by civil actions; criminal is reserved for the publicity hound.

Richard Ralston Catlett is a notorious war and tax protester.

The sixty-eight-year-old Columbia, Missouri, health food store owner argued that criminal charges of failing to file returns should be dropped because the IRS was guilty of “selective prosecution.”

The government is barred from selecting people to prosecute on grounds of race, religion or the exercise of free speech, or other “impermissible grounds.”

Catlett claimed that basing a criminal prosecution on publicity isn’t permitted.

But an appeals court disagreed.

His exercise of free speech wasn’t involved here, the court noted.

The IRS seeks criminal prosecution against publicized protesters to promote compliance with tax laws, the court observed.

“The government is entitled to select those cases for prosecution which it believes will promote compliance,” the court declared.

For some decades now we have been hearing the Church call on governments to take steps toward disarmament.

And it would be difficult to think of a thing more urgent or more appropriate for churches to say to governments.

It is hardly necessary here to give another recitation of the monstrous and unconscionable dimensions of the world arms race, culminating in the ever-growing stockpiles of nuclear weapons and the refinement of systems to deliver their carnage.

The Church has done part of its duty when it has said that this is wrong.

But the time has come to say that the good words of the Church have not been, and are not, enough.

The risks, the disciplines, the sacrifices, and the steps in good faith which the Church has asked of governments in the task of disarmament must now be asked of the Church in the obligation of war tax resistance.

It is, at the root, a simple question of integrity.

We are praying for peace and paying for war.

Setting euphemisms aside, the billions of dollars conscripted by governments for military spending are war taxes, and Christians are paying these taxes.

Our bluff has been called.

In all candor it must be suggested that the storm of objection which arises in the Church at this idea borrows its thunder and lightning from the premiers, the presidents, the ambassadors, and the generals who make their arguments against disarmament.

War tax resistance will be called irresponsible, anarchist, unrealistic, suicidal, masochistic, naive, futile, negative and crazy.

But when the dust has settled, it will stand as the deceptively simple and painfully obvious Christian response to the world arms race.

A score or a hundred other good responses may be added to it.

We in the Church may rightly be called upon to do more than this, but we should not be expected to do less.

Let the Church take upon itself the risks of war tax resistance. For church councils to take the position that the arms race is wrong for governments and not to commit themselves and call upon their members to cease and desist from paying for the arms race is patently inconsistent.

This is probably a fundamental reason why the Church’s pleas for disarmament have met with so little positive response.

Not even governments can have high regard for people who say one thing and do another.

If governments today are confronted with the question whether they will continue the arms race, churches are confronted with the question whether they will continue to pay for it.

As specialists in the matter of stewardship of the Earth’s resources they have contributed precious little to the most urgent stewardship issue of the twentieth century if they go on paying for the arms race.

How much longer can the.

Church continue quoting to the government its carefully researched figures on military expenditures and social needs and then, apparently without embarrassment, go on serving up the dollars that fund the berserk priorities?

The arms race would fall flat on its face tomorrow if all of the Christians who lament it would stop paying for it.

It is not, of course, simple to stop paying for the arms race as a citizen of the United States, or anywhere else for that matter.

If you refuse to pay the portion of your income tax attributable to military spending, the government levies your bank account or wages and extracts the money that way.

If your income tax is withheld by your employer, you must devise some means to reduce that withholding, such as claiming a war tax deduction or extra dependents.

If, as an employer, you do not withhold an employee’s war taxes, you will find yourself in court, as has recently happened to the Central Committee for Conscientious Objectors.

All of these actions are at some point punishable by fines or imprisonment, and none — in the final analysis — actually prevents the government from getting the money.

Nevertheless, it must be said that the Church has not tried tax resistance and found it ineffective; it has rather found it difficult and left it untried.

The Church has considered the risk too great.

Individuals fear social pressure, business losses, and government reprisals.

Congregations, synods, and church agencies equivocate over their role in collecting war taxes.

There is the risk of an undesirable response — contributions may drop off, tax-exempt status may be lost, officers may go to jail.

To oppose the vast power of the state by a deliberate act of civil disobedience is not a decision to be made lightly (an unnecessary observation, since there are no signs that Christians or the Church in the United States are about to do this lightly).

It would be inaccurate to give the impression that Christians, individually, and the Church, corporately, in the U.S. have done nothing about war tax resistance.

There have been notable, even heroic, exceptions to the general manifest lethargy.

The war tax resistance case of an individual Quaker was recently appealed on First Amendment grounds to the U.S. Supreme Court, but the court refused to consider it.

A North American conference of the Mennonite Church is grappling with the question of its role in withholding war taxes from the wages of employees.

Among Brethren, Friends and Mennonites — sometimes called the Historic Peace Churches — there is a rising tide of concern about war taxes.

The Catholic Worker Movement and other prophetic voices in various denominations have long advocated war tax resistance, but they have truly been voices crying in the wilderness.

For all our concern about the arms race, we in the churches have done very little to resist paying for it.

That has seemed too risky.

But then, of course, disarmament also involves risks.

Could there be a moral equivalent of disarmament that did not involve risk?

In this matter of the world arms race, it is not a question of who can guarantee the desired result, but of who will take the risk for peace.

Let the Church take upon itself the discipline of war tax resistance.

Discipline is not a popular word today, but it should be amenable to rehabilitation at least among Christians, who call themselves disciples of Jesus.

How quickly does the search for a way turn into the search for an easy way!

And how readily do we lay upon others those tasks which require a discipline we are not prepared to accept ourselves!

War tax resistance will involve the discipline of interpreting the Scripture and listening to the Spirit.

In a day when the Bible is most noteworthy for the extent to which it is ignored in the Church, it is an anomaly to see the pious rush to Scripture and the joining of ranks behind Romans 13, when the question of tax resistance is raised.

In a day when the authority of the Church is disobeyed everywhere with impunity, it is a curiosity to see Christians zealous for the authority of the state.

In a day when giving to the Church is the last consideration in family budgeting, and impulse rules over law, it is a shock to observe the fanaticism with which Christians insist that Caesar must be given every cent he wants.

As the Church has grown in its discernment of what the Bible teaches about slavery and the role of women, so it must grow in its discernment of what the Bible teaches about the place and authority of governments and the payment of taxes.

War tax resistance means accepting the discipline of submission to the Lordship of Jesus Christ in the nitty-gritty of history.

Call it civil disobedience if you wish, but recognize that in reality it is divine obedience.

It is a matter of yielding to a higher sovereignty.

Those who speak for a global world order to promote justice in today’s world invite nations to yield some of their sovereignty to the higher interests of the whole, and those persons know the obstinacy of nations toward that idea.

It may be that the greatest service the Church can do the world today is to raise a clear sign to nation-states that they are not sovereign.

War tax resistance might just be a cloud the size of a person’s hand announcing to the nations that the reign of God is coming near.

It is clear that Christians will not rise to this challenge without accepting difficult and largely unfamiliar disciplines.

But then, of course, disarmament also involves disciplines.

The idea that one nation can take initiatives to limit its war-making capacities is shocking.

To do so would represent a radical break with conventional wisdom.

How is it possible to do that without first convincing all the nations that it is a good idea?

Let the Church take upon itself the sacrifices of war tax resistance.

It is never altogether clear to me whether Christians who oppose war tax resistance find it too easy a course of action, or too difficult.

It is said that refusing to send the tax to IRS and allowing it to be collected by a bank levy is too easy — a convenient way of deceiving oneself into thinking that one has done something about the arms race.

And it is said that to refuse to pay the tax is too difficult.

It is to disobey the government and thereby to bring down upon one’s head the whole wrath of the state, society, family, business associates, and probably God as well.

Moreover, the same person will say both things.

Which does he or she believe?

In most cases, I think, the second.

The sacrifices involved in war tax resistance are fairly obvious.

They may be as small as accepting the scorn which is heaped upon one for using the term “war tax” when the government doesn’t identify any tax as a war tax, or as great as serving time in prison.

It may be the sacrifice of income or another method of removing oneself from income tax liability.

It can be said with some certainty that the sacrifices will increase as the number of war tax resisters increases, because the government will make reprisals against those who challenge its rush to Armageddon.

Yet, there is the possibility that the government will get the message and change its spending priorities or provide a legislative alternative for war tax objectors, or both.

In any case, for the foreseeable future, war tax resistance will be an action that is taken at some cost to the individual or the Church institution, with no assured compensation except the knowledge that it is the right thing to do.

But then, of course, disarmament also involves sacrifices.

The temporary loss of jobs, the fear of weakened defenses, and the scorn of the mighty are not easy hurdles to cross.

A moral equivalent will have to involve some sacrifices.

Let the Church take upon itself the action of war tax resistance.

The call of Christ is a call to action.

It is plain enough that the world cannot afford $400 billion per year for military expenditures, even if this were somehow morally defensible.

It is plain enough that the dollars which Christians give to the arms race are not available to do Christ’s work of peace and justice.

In these circumstances the first step in a positive direction is to withhold money from the military.

If we say that we must wait for this until everybody and (and particularly the government) thinks it is a good idea, then we shall wait forever.

Having withheld the money, the Church must apply it to the works of peace.

What this means is not altogether obvious at present, but there is reason to believe that a faithful Church can serve as steward for these resources as wisely as generals and presidents.

The dynamic interaction between individual Christians and the Church in its local and ecumenical forms will help to guide the use of resources withheld from the arms race.

This is a call to individual Christians and the Church corporately to make war tax resistance the fundamental expression of their condemnation of the world arms race.

Neither the individual nor the corporate body dare hide any longer behind the inaction of the other.

The stakes are too high and the choice is too clear for that, though we can have no illusions that this call will be readily embraced nor easily implemented by the Church.

But then, of course, we do not think that disarmament will be an easy step for governments to take either.

The Church has an obligation to act upon what it advocates, to deliver a moral equivalent of the disarmament it proposes.

If effectiveness is the criterion, it is certainly not obvious that talking about the macro accomplishes more than acting upon the micro.

A single action taken is worth more than a hundred merely discussed.

(When it comes to heating your home in winter, you will get more help from one friend who saws up a log than from a whole school of mathematicians who calculate the BTUs in a forest.)

To talk about a worthy goal is no more laudable than to take the first step toward it, and might be less so.

Michael Miller wrote an article for the same issue that noted that the National Guard is a U.S. military combat function that is largely paid for out of state budgets, not the federal budget.

He concluded:

I am now more fully aware how the military affects our daily lives and activities.

I also realize that not only is the objection to payment of war taxes a federal issue, but it is also a very real state issue.

State budgets contain rather large amounts in this respect.

As Friends, we must be constantly aware of the issues involved with our tax dollars.

The military has a great influence over our lives and our tax dollars, whether or not we recognize it.

We have a responsibility to make ourselves aware of the issues and how they influence our lives.

Alan Eccleston contributed an article on war tax resistance as a method of testifying for peace — aligning ones life with ones values.

This, he felt, could be done in a variety of ways:

We do not have to be prepared for jail to be a war tax resister.

We do not have to be ready, at this moment, to subject ourselves to harassment by the Internal Revenue Service.

We do, however, have to be truthful on our tax returns.

We do have to be clear about our belief in the peace testimony and our desire to align our lives with this belief.

And that is all!

If you are clear about that, you can withhold some amount of your tax.

It can be a token amount, if that is where you are, say five dollars or fifty dollars.

Or it can be the same percent of your tax as the military portion of the current budget, currently thirty-six percent excluding past debt and veterans benefits.

(An easy way to do this is to insert the amount under “Credits” as a “Quaker Peace Witness,” line forty-six.

Alternately, some people declare an extra deduction, but this is more complicated, since the deduction must be substantially larger than the amount you desire to withhold.)

It may bother you that three times or even ten times what you have chosen to withhold is going to be spent for war preparations.

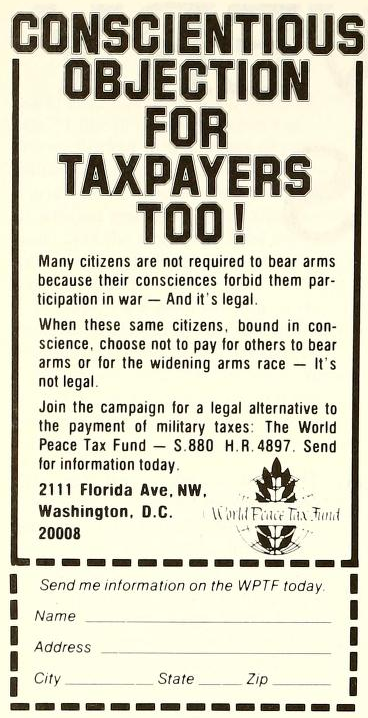

But far better to take this small step than to turn away from the witness. Write your congresspersons and tell them of your concern.

Urge them to pass the World Peace Tax Fund which would acknowledge your constitutional right to practice your religious beliefs without harassment and penalty.

Alternatively, if the government owes you money fill out the (very short) Form #843 “Request for Refund,” asking that they refund the amount you wish for peace witness.

One can also anticipate the withholding problem by filling out a W-4 Form at your place of employment declaring (truthfully) an allowance for expected deductions that includes the amount of your peace witness.

Then what?

You can expect a series of computer notices stating that you calculated your tax incorrectly and you owe the amount shown on the notice.

This may also include an addition of seven percent annual interest on the amount owed.

(Currently IRS seems not to be adding on penalty charges but that is a possibility.)

You have a choice: you can ignore the notice; you can write or call IRS and discuss it; or you can pay the tax.

Sooner or later you will receive a printout that says “Final Notice.”

If you again fail to pay the amount owed, you will probably receive a call from someone at IRS who will try to convince you that the whole process has gone far enough and that your purpose is better served by paying the government.

IRS wants to collect.

That is their job; when they have done it, they are through with you.

They cannot, by law, be harsh or punitive.

There is no debtors’ prison in this country.

If you declare the intent of your witness on your tax form and by letter to Congress, you cannot be convicted of fraud; therefore, you are not risking criminal penalties.

In other words, the tax resister controls the process.

One can witness to peace so long as it can be done lovingly and, if it is to be a meaningful witness of peace, that is the only way it can be done.

However, if one’s family obligations or other matters are too pressing, or if one’s spiritual resources are being unduly strained, it is time to lay down this particular witness.

One can carry on the witness and still bring the process to a conclusion by letting the payment be taken from a bank account or peace escrow fund.

Another round of letters to Congress and the president will testify to your continuing concern even after the pressure of collection has been relieved.

In your witness, no matter how small the amount withheld or how short the duration, you will gain strength and courage and insight.

This brings new resources to your next witness.

It gives you knowledge and resources to share with others, which in turn helps their witness.

In sharing, you both are strengthened.

Thus, a personal witness becomes a “community of witness,” and the “community of witness” gains strength, courage, and insight in its mutual sharing.

This witness and this sharing of Christian love becomes its own witness to the testimony of peace — the testimony of love for God, for ourselves, for humankind.

(A letter from Dorothy Ann Ware in a later issue credited the Eccleston article for spurring her to “make a token Quaker Peace Witness by withholding a very small portion of my income tax.

So Step One has been taken…”)

The same issue reprinted a Minute from the Philadelphia Yearly Meeting which encouraged Quakers “to give prayerful consideration… to the option of refusal of taxes for military purposes.”

Furthermore:

We reaffirm the Minute of the yearly meeting which states in part that “…Refusal to pay the military portion of taxes is an honorable testimony, fully in keeping with the history and practices of Friends… We warmly approve of people following their conscience, and openly approve civil disobedience in this matter under Divine compulsion.

We ask all to consider carefully the implications of paying taxes that relate to war-making… Specifically, we offer encouragement and support to people caught up in the problem of seizure, and of payment against their will.”

We request the Representative Meeting to arrange for the guidance of meetings and their members on the form of military tax resistance suitable for individuals in accordance with that degree of risk appropriate to individual circumstances, for advice on consequences, and for consideration of legal and support facilities that may be organized.

We also request Representative Meeting to provide for an Alternate Fund for sufferings, set up under the yearly meeting to receive tax payments refused, for those tax refusers who may wish to utilize this fund.

We recommend cooperation with the Historic Peace Churches and other religious groups in further consideration of non-payment on religious grounds of military taxes.

Following that, John E. Runnings wrote of his and his wife Louise’s war tax resistance, and decried the injustice of a “society that requires that Quakers, who renounce war and recognize no enemies, must pay as large a contribution to the support of the war machine as those who fully accept the malicious nature of other nationals and who are so frightened of their ill intent that no amount of extermination equipment is enough to assure security.”

The social reforms that we credit to George Fox’s influence did not come about by his waiting on the Spirit but rather by his responding to the Spirit.

If just one man could accomplish so much by responding to the Spirit, what would happen if several thousand modern Quakers were to respond to their spiritually-inspired revulsion to assisting in the building of the war machine?

If Quakers could be induced to discard their excuses for their financial support of the arms race and to withhold their Federal taxes, who knows how many thousands of like-minded people might be encouraged to follow suit?

And who knows but what this might bring a halt to the mad race to oblivion?

There was a brief update about Robert Anthony’s case.

Anthony hoped to use his Fifth Amendment right against self-incrimination (presumably in response to a government request for financial records or something of the sort).

The judge in the case asked if the government would grant Anthony immunity from prosecution for anything he disclosed, which would have cut off the Fifth Amendment avenue of resistance, but the government wasn’t prepared to do that, and that’s where the matter stood.

The issue included a notice that the Center on Law and Pacifism had “recently published a military tax refusal guide for radical religious pacifists entitled ‘People Pay for Peace’ ” but also noted that “the Center states that it is in ‘urgent and immediate need of operating funds.’ ”

A later issue gave some more information about the Center:

The Center was started after a former Washington constitutional lawyer and theologian, Bill Durland, met a handful of conscientious objectors who were appealing to the U.S. courts for their constitutional rights to deny income tax payments for the military.…

That was in .

The Center is now producing regular newsletters and has published a handbook on military tax refusal.

It has organized war-tax workshops for pacifists representing constituencies in the Northeast, South and Midwest.

One of its projects was the “People Pay for Peace” scheme, under which it was suggested that each individual deduct $2.40 from his/her income tax return to “spend for peace”: that sum being the per capita equivalent of the $193,000,000,000 which will be consumed in for war preparation in the United States.

This was a protest action against the fifty-three percent of the U.S. budget allocated to military purposes.

The Center on Law and Pacifism is a “do-it-yourself cooperative” which relies on both volunteer professional assistance and individual contributions.

Hmmm… my calculation for 53% of the federal budget in 1979 is more like $214,618,730,000… and per-capita (by U.S. population, anyway) that would be $953.63 per person.

If you use the $193 billion value, that’s still $857.57 per person.

Even if you use world population, you still get $44.08–$49.02 each.

Somebody’s confused… maybe it’s me.

Wendal Bull penned a letter-to-the-editor in the same issue about his experience as a war tax resister twenty years before.

Excerpt:

In I received a lump sum payment of an overdue debt.

This increased my income, which I normally keep below the taxable level, to a point quite some above that level.

I distributed the unexpected income to various anti-war organizations.

I anticipated pressure from IRS officers, so in the autumn, long before the tax would be due, I disposed of all my attachable properties.

This action, under the circumstances, I believe to be unlawful.

But it seemed to me a mere technicality, far outweighed by the sin of paying for war, or the sin of permitting collection of the tax for that purpose.

After disposing of all attachable properties, I wrote to IRS telling them I had taxable income in that year but chose not to calculate the amount of it because I had no intention of paying it.

In the same letter I explained my reasons for conscientious non-cooperation with Uncle Sam’s preparations for war in the name of “defense.”

My letter appeared in full or in generous excerpts in at least three daily papers and several other publications and I mailed copies to friends who might be interested.

I am not a publicity hound nor a notorious war resister.

The publicity did seem to effect a fairly prompt visit from the Revenue Boys.

They paid me three or four visits.

On one occasion two men came; one talked, the other may have had a concealed tape recorder, or was merely to witness and confirm the conversation.

After quizzing me for an hour or more they left courteously, whereupon I said I was sorry to be a bother to them.

At that the talker said, “You’re no trouble at all.

I brought a warrant for your arrest, but I’m not going to serve it.

It’s the guys who hire lawyers to fight us that give us trouble.”

If they had caught me in a lie, or giving inconsistent answers to their probing questions, I suspect the summons would have been served.

I was fully prepared to go to court and to be declared guilty of contempt for not producing records to show the sources of my income.

I had told the men I was in contempt of the entire war machine and all officers of the legal machinery who aimed to penalize citizens for non-cooperation with war preparations.

Later came two visits from a man who attempted to assess my income for that year, and the law required him to try to get my signature to his assessment.

I considered that a ridiculous waste of taxpayer’s money.

The man agreed with a smile.

Still later, there came several bills, one at a time, for the amount of the official assessment, plus interest, plus delinquency fee, plus warnings that the bill should be paid.

These I ignored, of course.

The head men knew I would not pay; and they knew they had not any intention of trying to force collection.

I have no idea who decided to quit sending me more bills.

I think the claim is still valid since the statute of limitations does not apply to federal taxes.

It is inconvenient to have no checking account, to own no real estate, to drive an old jalopy not worth attaching, and so on.

Some of us choose this alternative rather than to let the money be collected by distraint.

In the same issue, Keith Tingle shared his letter to the IRS, which he sent along with his tax return and a payment that was 33% short.

He stressed that he didn’t mind paying taxes — “a small price for the tremendous privilege of living in the United States with its heritage of freedom, equal protection, and toleration” — but that “I do not wish my labor and my money to finance either war or military preparedness.”

Stephen M. Gulick also wrote in.

“Because the military and the corporations need our money more than our bodies, war tax resistance becomes important — in all its forms from outright and total resistance to living on an income below the taxable level,” he wrote.

“Fundamentally, war tax resistance must lead us to look not only at warmaking and the preparation for war, but also at the economic, social, and political practices that, with the help of our money, nurture the roots of war.”

Colin Bell attended the Southern Appalachian Yearly Meeting:

“I think,” Colin said, “that as a Society we are standing at another moment like that, when our forebears took an absolutely unequivocal stance” and we don’t know what to do.

Are we looking for something easy, he wondered, suggesting that it probably should be tax resistance.

Accepting the title Historic Peace Church, he declared, makes it sound like a worthy option, rather than it being at the entire heart and core of Christendom.

A letter to the editor of the Peacemaker magazine from John Schuchardt is quoted in the issue:

I have recently received threatening letters from a terrorist group which asks that I contribute money for construction of dangerous weapons.

This group makes certain claims which in the past led me to send thousands of dollars to pay for its militaristic programs. The group claimed: 1) It was concerned with peace and freedom; 2) It would provide protection for me and my family; 3) It was my duty to make these payments; and 4) I was free from personal responsibility for how this money was spent in individual cases.

Last year, for the first time, I realized that these claims were fraudulent and I refused to make further payments…

That issue also noted that the Albany, New York, Meeting “joined the growing number of meetings which are calling on their members to ‘seriously consider’ war tax resistance…” That Meeting was also considering establishing its own alternative fund, and was hoping Congress would pass the World Peace Tax Fund bill.