It’s a long shot, but Jenkins hopes to take advantage of the Religious Freedom Restoration Act and of his painstaking research into the history of American government accommodation of religious scruples to make an argument that will succeed where others have failed.

Daniel Jenkins is trying again, with a new set of arguments that I’ll try to summarize here.

Take note: I’m not a lawyer, so I may be missing a lot of legal nuance.

Jenkins’s examination of early war tax resistance in America, “The Liberation of Nathan Swift,” can be found in the book We Won’t Pay!: A Tax Resistance Reader.

In , Jenkins withheld part of his federal income tax from the IRS, putting it instead in an escrow account and informing the IRS that he would surrender it to them on the condition that the money would only be used for non-military spending.

In , the IRS sent Jenkins one of their intent-to-levy letters and Jenkins filed a Collection Due Process request.

The IRS quickly denied relief, so Jenkins appealed to the Tax Court, which shot down the appeal in , adding a $5,000 “frivolous filing” penalty to boot.

Jenkins then appealed to the 2nd Circuit Court of Appeals. , that court upheld the Tax Court’s ruling, and Jenkins asked the Supreme Court to take his appeal.

The state of law and precedent is, as far as I can tell, something like this:

The First Amendment says, in part, that “Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof…” So people whose religious beliefs prohibit their participation in certain government programs have asked the courts to exempt them.

For instance, in Wisconsin v. Yoder (), the Supreme Court ruled that a state compulsory education law violated the freedom of religion of the Amish people who challenged the law, “for the Wisconsin law affirmatively compels them, under threat of criminal sanction, to perform acts undeniably at odds with fundamental tenets of their religious beliefs.”

A challenge to tax laws came a decade later.

In U.S. v. Lee (), the Supreme Court ruled that the Old Order Amish could not use the same argument to get out of paying Social Security taxes because:

While there is a conflict between the Amish faith and the obligations imposed by the social security system, not all burdens on religion are unconstitutional.

The state may justify a limitation on religious liberty by showing that it is essential to accomplish an overriding governmental interest.

And

The tax system could not function if denominations were allowed to challenge it because tax payments were spent in a manner that violates their religious belief.

Because the broad public interest in maintaining a sound tax system is of such a high order, religious belief in conflict with the payment of taxes affords no basis for resisting the tax.

I would have thought that even this would have blasted a big hole in the argument that the uniform application of the tax laws is “essential” and that “[t]he tax system could not function” without it.

After all, if the tax system survived the legislative exception Congress carved out for self-employed Old Order Amish, there’s no reason to expect that it would collapse under the burden of a court-carved exception for the non-self-employed variety.

But the Supreme Court thought otherwise.

And that seemed to pretty much shut the door.

But in Congress passed the Religious Freedom Restoration Act, which instructed the courts to apply “strict scrutiny” to cases “where free exercise of religion is substantially burdened” by the government.

So conscientious objectors to military taxation started trying again.

In , the 2nd and 3rd Circuit Courts of Appeal turned down appeals that recrafted the old conscientious objection to military taxation legal arguments to see if they could be slipped in under the new Religious Freedom Restoration Act standard.

Both circuits said “no dice,” and in the Supreme Court decided not to review these decisions.

And that’s where that stood.

In , the Supreme Court decided Gonzales v. O Centro Espírita Beneficente União do Vegetal.

União do Vegetal is a religious group that uses ayahuasca in their ceremonies, a hallucinogenic tea that contains dimethyltryptamine, a substance banned by federal law.

The group challenged the application of that law to the participants in their ceremonies, basing their challenge on the Religious Freedom Restoration Act.

The government responded that, as with the tax law in Lee, the uniform enforcement of the Controlled Substances Act was essential to an overriding governmental interest.

Last year the Supreme Court ruled, unanimously, that the government was wrong, and that the Religious Freedom Restoration Act requires the government to carve out an exception to the Controlled Substances Act to accommodate the religious practices of União do Vegetal because the government had failed to show that the uniform enforcement of the Act was sufficiently essential to a sufficiently compelling governmental interest.

So when Jenkins filed his 2nd Circuit appeal, he used the O Centro ruling to try and distinguish his 1st Amendment / Religious Freedom Restoration Act arguments from those that the same circuit rejected in .

One problem with this, that the court pointed out when it rejected Jenkins’s appeal, is that when the Supreme Court decided O Centro, it explicitly distinguished the case before it from the tax case Lee.

The Court said that in contrast to the current case, Lee showed “that the Government can demonstrate a compelling interest in uniform application of a particular program by offering evidence that granting the requested religious accommodations would seriously compromise its ability to administer the program” and that the tax code was such a program.

Jenkins hopes he can convince the Supreme Court to take another look at Lee, which was decided on Constitutional grounds, and see if its logic still holds up under the Religious Freedom Restoration Act’s standards.

He wants the court to view the question this way:

Does Lee, or the logic of the circuit courts that relied on Lee, give the IRS a blanket exemption from the Religious Freedom Restoration Act when the Act itself does not allow for such an exemption?

If not, then his case should be decided on the merits, which requires a closer look at the extent to which his religious beliefs are violated by the law, and the extent to which accommodating those beliefs would compromise the IRS’s ability to collect taxes.

He’s got another argument, too, that’s very interesting, but I’m on much shakier ground in trying to summarize it because it relies on the Ninth Amendment, where even lawyers and judges fear to tread.

This amendment reads:

The enumeration in the Constitution, of certain rights, shall not be construed to deny or disparage others retained by the people.

This could mean anything or nothing, depending on who you ask.

Jenkins hopes that there’s a majority on the Supreme Court who are ready to give the Ninth Amendment some teeth.

Appealing to the Court’s conservative majority, Jenkins, in his Supreme Court petition, encourages them to interpret this amendment as über-conservative jurist Robert Bork suggested:

Ninth Amendment scholars propose giving content to its promise to preserve unenumerated rights by looking to this country’s history and tradition.

For example, in The Tempting of America: The Political Seduction of the Law (The Free Press ), Robert Bork observes that “[t]he Ninth Amendment appears to serve a parallel function [to the Tenth Amendment’s guarantee of federalism] by guaranteeing that the rights of the people specified already in the state constitutions were not cast in doubt by the fact that only a limited set of rights was guaranteed by the federal charter.”

Jenkins then goes on to argue that “that the individual right of religious conscience not to be compelled to participate in or support military activity was well recognized at the founding of this nation.

For example, the New York State Constitution of , which predates and is independent of the United States Constitution and the Bill of Rights, expressly protects persons with ‘scruples of conscience’ from forced military service and requisition for armament.

The constitutions of other colonial states also contain liberty of conscience guarantees and religious exemptions from the ‘bearing of arms’.

This constitutional right of conscientious objection was preserved by the states at least until the formation of the first permanent national army.

It was also preserved and protected by the actions of the early Congress and by the Civil War Congress that instituted the first federal universal military service draft.”

Jenkins has done an impressive amount of research into the history of conscientious objection to military taxation in the United States (see, for instance, The Liberation of Nathan Smith).

With this, he hopes to prove that conscientious objection to military taxation was among the “rights… retained by the people” at the time the Constitution was ratified.

But for this to work as a legal argument, the Supreme Court not only has to find this evidence compelling, but has to accept Jenkins’s invitation to wade into the Ninth Amendment — something that Court has generally been averse to.

Pundit James J. “He’s Still Alive?” Kilpatrick comments on Dan Jenkins’s Supreme Court petition (in which he hopes to get the Court to recognize a 9th Amendment right to conscientious objection to military taxation).

I mention it, but can’t recommend it.

Having gone over the same territory , Kilpatrick’s op-ed strikes me as confused, superficial, and uninformative (though I more-or-less come to the same conclusion, which is that Jenkins’s argument is a long-shot).

, the U.S. Supreme Court declined to take up Daniel Jenkins’s appeal which asserted his claim of a Constitutional right to conscientious objection to military taxation.

(I covered this appeal in some depth .)

This effectively upholds the 2nd Circuit Court of Appeals ruling, which upheld the Tax Court ruling, which more-or-less said “no dice, and here’s a $5,000 frivolous filing penalty for making me say so.”

A new issue of NWTRCC’s newsletter — More Than a Paycheck — is out featuring an article I wrote about how to craft a persuasive and motivating tax resistance message.

(It’s a distillation of a Picket Line entry from .)

Also in the newsletter are some notes about IRS policy and foibles, an update on the ongoing attempts by war tax resister Daniel Jenkins to find a legal forum that will rule that conscientious objection to military taxation is a human right, and the latest on All Saints Church’s struggle to maintain its freedom of speech and its tax-exempt status at the same time.

“I suddenly woke up about five years ago and made a big sign that said ‘Does Our Lifestyle Demand War?’ and hung it on my door.”

Frances then proceeded to work at changing her lifestyle, starting by not using her car for two days a week.

As she walked more, she found she could use her car less and less — and liked walking more and more.

It became something of a meditation, with the added bonus of meeting people along the way.

She changed from a Friends Meeting that was some miles away to one within walking distance, and dropped her YMCA membership where they use so much heat and air conditioning.

She doesn’t want to fly anymore and takes the train instead.

She’s still working on many things, like buying food that is grown locally.

She’s really working to reduce her footprint on the planet, and at the same time redirecting taxes from war to funding real human needs like schools, peace and justice work, and rebuilding the new society in the shell of the old.

The IRS has released some preliminary data about tax year , and these show that the increasing “lucky ducky” trend — the percentage of Americans living under the income tax line — has pretty much levelled off.

, the percentage of those households who filed their tax returns but were below the income tax line was in the 18%–25% range.

, the numbers have gone way up.

for which I have stats look like this:

Tax Year

Number of Zero-Tax Filers

Zero-Tax Filers as a Percent of All Filers

2004

42,500,000

32.6%

2005

43,800,000

32.6%

2006

45,700,000

33.0%

Almost a third of American households who filed tax returns paid no federal income tax at all for — either they paid none to begin with, or all of what they paid was returned to them as a refund.

It’s in the United States — the deadline for filing our personal federal income tax returns.

In a few minutes, I’m going to head across the bay to meet up with Berkeley’s notorious squadron of Code Pink protesters at the Marine Corps recruiting center.

From there, the crew will march to the main Oakland post office to remind the last-minute filers what they’re paying for.

War tax resisters nationwide are having deductions taken from their fifteen minutes of fame , as the news media take advantage of the Tax Day angle to swing the lens their way.

Amy Goodman’s Democracy Now show is broadcasting from Portland, Oregon , and it features war tax resisters Pat & John Schwiebert, Portland locals who have been resisting taxes for .

(You can hear the show on-line — the Schwiebert segment starts at about 12:49.)

LoHud.com out of New York takes a look at war tax resisters there, including Ethan & Rima Vesely-Flad, Chad Murdock, Frederick Dettmer, Rosa Packard, Daniel Taylor Jenkins, and Hugh & Sirkka Barbour.

Tax resistance is the most direct way U.S. citizens can avoid being complicit in this war and other illegal activities and actions by government employees and agencies.

If all of us who have written our Congresspersons or taken to the streets also refuse to financially back the war and other illegal activities and actions of the government, the decision-makers in Washington have a much harder time ignoring our resistance.

There were about 60 people from 14 countries — about standard for these

conferences. Sadly I have to report that our efforts to get George Rishmawi

from Palestine to the conference ended in a refused visa, so that he could

not travel to the conference. The British organizers tried really hard to get

thru the red tape but to no avail. Two people from Ghana were refused visas

also.…

…As with most conferences (at least in my humble opinion) the time spent

talking with folks at meals and between the organized sessions is at least as

important as anything that comes up in the sessions. Quite a few of my

conversations were with individuals from other countries who are war tax

resisters, who refuse to pay at least some of taxes due to their respective

governments. Many combine their refusal with redirecting the money to some

kind of fund for nonviolent defense or peace-building funds.

As we have found in the past, it is more difficult to resist in most

countries because of the way taxes are pulled from paychecks. Those who

resist tend to be self-employed. In general, collection is much faster in

other countries than has been our experience in the

U.S. (at least up

to now), and many organizers at this conference make no effort to build

WTR, seeing

it as futile. The majority of people at the conference are working on

peace tax fund

campaigns or looking for ways to take their complaint of being forced to pay

for war through some court system or

U.N. body. I

think 5 of the Peace Tax Seven

were in attendance, and they are slowly making their way into the European

Court of Human Rights. Daniel Jenkins from the

U.S. reported on

the effort to bring a formal complaint to a

U.N. body. The

Germans have a resister or two in their circles, but are focusing on a new

effort of 10 people to take a complaint to a German high court based on the

budget being a violation of fundamental

rights because of the military spending. The Germans are trying to get away

from appealing through the tax system and instead trying this more direct

route to the government officials who create the budget. In Norway peace tax

fund campaigners are appealing to their local councils; if the council

accepts their complaint as an “initiative of national interest” then the

council can send a complaint up to the next level of the government system.

I attended two workshops that related more generally to organizing, with both

having some focus on how to widen our efforts. Groups and campaigns in every

country seem to face issues similar to our own. “How to bring in more young

people” was the topic of one workshop. While no group seemed to be doing any

better than many of us here in the

U.S., many are

looking for answers in the internet, such as getting into Facebook and other

networking sites, and upgrading our websites. The Danish peace tax fund

campaign has been working with the model

U.N. program in

high schools with some success at making “the right not to pay for war” a

topic in those discussions. One person noted that the activists groups that

seem to be most successful at drawing in young people are the ones that give

new members something to do immediately and regularly. There was also a good

deal of discussion of language, in particular the use of the word

“conscience,” and whether that is a word that resonates with young folks

today. Because the hosting group was Britain’s “Conscience: the peace tax

campaign,” it was the local folks who were having this discussion among

themselves and also bringing it to the conference. “Taxes for Peace Not War”

was a slogan that many people appreciated due to the positive spin.…

…There were small group sessions to talk about the common ground between war tax resisters and peace tax campaigns and develop ideas about how we can all work together more across international boundaries.

I don’t know if any of the groups came up with any brilliant insights on this.

My group did spend quite a bit of time comparing our tax systems and learning more precisely what each of our organizations do.

It’s hard to figure out how to work together without understanding more about each situation; there’s a lot of confusion about why there is such a “strong” war tax resistance movement in the U.S. as compared to other countries.

One person said rather emphatically — “I just don’t understand why anyone would be a war tax resister without also working for a peace tax fund.”

Others perceived that peace tax fund campaigns and WTR need each other, that you can’t have one without the other; I said that I could certainly resist without any connection to a peace tax fund campaign, but I began to see that many Europeans see the effort to actually redirect military taxes to a fund that is only for peace-building efforts or alternative defense is primary to their peace tax fund campaigns.

I think the U.S. efforts have never had this peace-building fund as an emphasis; the peace tax fund bill as it has been written in the U.S. redirects the taxes of conscientious objectors to the non-military spending in the U.S. budget, not to a specific peace-building effort.

I found that insight rather interesting as I never understood so clearly how many of the campaigns are writing their bills for this specific purpose.

In my small group and in general there was clearly interest in making Conscience and Peace Tax International more of an umbrella group for all of our work.

Due to technicalities of nonprofit status, NWTRCC has not been an official member of CPTI but has been a supporter.

CPTI was founded as more of a link for the peace tax fund campaigns than for WTRs, but we’ll see how things develop.

Many wanted to see more organizing successes and ideas posted on the CPTI website.

Right now it has links to the groups in each country and information on WTR court cases and conscientious objection rulings within the U.N.…

War tax resisters Frank Donnelly, Larry Dansinger, and Dan Jenkins were on WERU’s “Voices” show early .

Here’s a podcast:

I think I’m a little late to this party, but it only now showed up on my radar.

Conscience Studio is a Quaker-oriented group that focuses on living life conscientiously.

They have a service program centered on development and human rights issues in Indonesia, and a strong war tax resistance focus.

Among the war tax resistance-related pages on their site are:

A declaration you can sign to complain that, against our deeply-felt values, “we are all ultimately compelled to pay taxes used for military purposes, and that we have a continuing liability to do so in the future. We have thus been obliged, and are being obliged, in direct violation of our consciences, to be complicit in the funding and waging of war.”

Of which there is one, apparently: “Can I still write a statement of conscience while in the midst of the internal debate [over how far I’m willing to go]?”

The 15th international conference will likely be held in Geneva.

Rather than looking for a local group in Geneva to act as a host and sponsor, a committee of conferees will work together to plan the conference themselves.

Social Media

A number of the regional groups and campaigns reported that they were making attempts to experiment with social media outreach, but they largely felt out of their depth in this area.

Some groups noted that because of the demographics of their membership, social media (or even email) was ineffective for in-group outreach.

In one case, a group reported that three-quarters of its members do not use email at all, so for them a printed and snail-mailed newsletter is essential for keeping them informed and involved.

Bringing COMT/WTR to a New Audience

The Colombian antimilitarist movement is so urgently concerned with stopping batidas and protecting the rights of conscientious objectors to military service that the issue of war tax resistance has not been a priority.

This conference did a good job of putting that issue on the radar here among the people most likely to adopt it.

Statements of Conscience

Conferees, led by Dan Jenkins and Jens Braun, spent several hours over two days trying to better articulate the conscientious motives that lead them to conscientious objection and/or tax resistance.

It can be difficult to come up with a good “elevator pitch” to explain to people we meet why we resist (and why maybe they should too), and this is crucial to the growth and thriving of our movement.

If we can better articulate how we became war tax resisters, we can more clearly point out the path for other people to follow.

a conference participant reads from her distilled statement of conscience

What is conscience? What does it tell us?

What helps us to listen to conscience and follow its advice?

Can you sum up in one or two sentences your motivation for your resistance?

Speakers

We were treated to several speakers on a variety of topics related to conscience, the situation in Colombia, and the prospects for demilitarization.

Alan Vargas and Nicolás Navas gave us a status report on the state of conscientious objection in Colombia.

They are particularly concerned about the way the law puts a burden of proof on the objector to show that his objection is long-held and demonstrable in his past actions.

This prevents the law from recognizing an “objector via epiphany” and is particularly inappropriate since draftees are very young men, who rarely have any history of grappling with issues of conscience and nonviolence and who are likely to be in the process of forming their characters rather than having any fixed characters to demonstrate.

Alan Vargas and Nicolás Navas talk about legal strategies for expanding the rights of conscientious objection to military service in Colombia, and Ciro Roldán gives us the philosophical and historical background in which the concept of conscientious objection has evolved.

Philosophy professor Ciro Roldán recapitulated the philosophical history of conscientious objection, from Antigone to the protestant reformation to relatively new concept of “freedom of conscience” and through to the modern Hegelians.

He argued (as has Juan Carlos Rois in Spain) that rather than arguing that some people ought to have the freedom of conscience to object to military service, we really should be arguing that everybody has a right not to kill or be put in the line of fire against his will.

It’s not so much that conscientious people ought to be exempt from the draft, but that the government ought not to be in the drafting business at all.

Pursuing a right of conscientious objection puts the objectors on the defensive; instead, we should put the state on the defensive.

Clara López told us of her days as a Students for a Democratic Society radical at Radcliffe during the Vietnam war (she’s a politician today: former mayor of Bogotá and now a presidential candidate and head of a left coalition political party) and of her views about how addressing urban violence and resolving the drug war are essential to a genuine peace process.

Alberto Yepes, coordinator of the Human Rights Observatory, gave us the context and consequences of the militarization of Colombian society in recent decades, and how this is linked with inequality in Colombia, with corruption and theft of public resources, and with Colombia being seen as an important franchise of the U.S. military-industrial complex.

Professor Carlos Mario Perea spoke of how urban violence is the undernoted but exceptionally important counterpart of the guerrilla wars in Colombia, and how the two feed on one another and need a common resolution.

Former constitutional court justice and presidential candidate Carlos Gaviria advocated a peace process that would result in the eventual abolition of the Colombian military.

He thought that economic inequality and political reform must be part of the peace process, and that since any results of that process would necessarily be political in nature, the process ought to be transparent and open to participation by political representatives, and not just behind-closed-doors negotiations between the warring factions.

He was cynical about the current peace talks, but thought they might have symbolic value and could prompt the wider society to begin a crucial revolution of ethical values.

Ricardo Esquivia, who has been fighting for conscientious objection in Colombia for over two decades, spoke about conscience and memory.

His text was Romans 12:2 (“And be not conformed to this world: but be ye transformed by the renewing of your mind, that ye may prove what is that good, and acceptable, and perfect, will of God.”)

He highlighted how the many small ethical transgressions that have become commonplace have poisoned society and help to provide cover for larger horrors (he related a Colombian proverb about public works projects which is that you should always add in a little extra in your bid so that you have enough money left over after the bribes and kickbacks to do the job).

It’s not so much that we need to develop a “new ethics” as that we need to more seriously engage with the ethics we’re all familiar with.

Nonviolent activists, he says, because we do not have the discipline, practice, and professionalism of our military counterparts, are often overmatched — we need to take our activism more seriously and put our backs into it in the same way soldiers are expected to.

Why was there only one conscientious objector in prison in Colombia?

If there were five, ten, fifteen… that might be all it took for outrage and rebellion to begin.

Peter Newton is trying to revive the tradition of utopian world federalism that was so central to the peace movement 150 years or so ago.

That movement died out in the wake of the failures of the League of Nations and the horrors of utopian movements with world-spanning ambitions like totalitarian communism, but Newton believes its time has come again.

People are not naturally violent, he says, and governments are not necessarily corrupt:

We could come together to build large-scale political structures that make the world more peaceful and more free if we put aside our cynicism and got down to it.

War tax resistance in the Friends Journal in

The few mentions of war tax resistance in the Friends

Journal in were mostly looks at

war tax resisters from Quaker history, though there was some mention of

Daniel Jenkins’s ongoing attempt to get the courts to discover a Constitutional

right to conscientious objection to military taxation.

The issue contained a

letter-to-the-editor from Perry Treadwell in which he chided Friends for

letting their peace testimony slacken. Excerpts:

I received another of those

IRS

letters that I have been getting off and on for the past 35 years. They tell

me to pay back taxes, penalties, and interest. It still gives me that slight

kick in the stomach. I sent back another letter informing them again that as

a member of the Religious Society of Friends my belief dictates that I cannot

pay for killing.…

Where is the passion of the

Friends to witness our Peace Testimony?

Recently a member of Atlanta

(Ga.) Meeting defended his

paying income taxes by using the same argument that Stan Becker proposes in

his Viewpoint in the October issue, "How Can We Work More for Peace Than for

War?" [see ♇

]: using money and/or

time commitment for peace purposes. How many cluster bombs have been bought

with their tax money? Each day I weep seeing the list in the

New York Times of those killed in Iraq,

particularly the 18–20-year-olds. I cannot describe the impact the deaths of

hundreds of thousands of Iraqis we have slaughtered has on me.

What if 500 Friends withheld $10–$100 from their

tax returns? What if more did so

? Throw sand in the wheels of the

IRS.

Put our money where our collective mouths are when it comes to Peace Tax Fund

legislation. That might get Congressional attention.

What are we afraid of? War tax refusal is not to be feared. In fact, it has

opened up for me whole new opportunities for service and ministry.

The issue included Daniel Jenkins’s article “The Liberation of Nathan Swift,” which concerned the arrest of a Quaker in for his refusal to pay a militia exemption tax, and his subsequent release from jail when New York Governor William Seward intervened.

Seward later, in an address to the legislature, endorsed an amendment to the state Constitution that would release conscientious objectors from the militia exemption tax (Jenkins finds indications that a subsequent Constitutional Convention did in fact change the Constitution in this way).

Jenkins saw this story as inspiration for the movement advocating a Peace Tax Fund law, saying it showed that with persistent witness and lobbying, it is possible to get a government to make concessions to conscientious objectors to military taxes.

The author’s note mentioned that Jenkins had “taken a military tax objection case into the federal courts with the support of a clearness committee, financial assistance from Purchase Quarterly Meeting, and an amicus brief submitted by New York Yearly Meeting,” and that the article was a revised and expanded version of “an oral report presented by the Conscientious Objection to Military Taxation Sub-Committee of the Peace Concerns Committee at a yearly meeting session held in .”

A later update on Jenkins’s legal case noted that his appeal had been turned down by the Second Circuit Court of Appeals:

Jenkins… bore witness to the leading of his conscience that paying taxes for

war is wrong by withholding his payment of federal income tax and setting it

aside in escrow until the government agreed to use it only for nonmilitary

purposes. For this he had been penalized not only with the tax and ordinary

penalties and interest, but also with a $5,000 fine for bringing forth what

the government contended was a “frivolous” case. Lawyer Fred Dettmer, clerk

for the Witness Coordinating Committee of New York Yearly Meeting…, argued

the appeal.

Relying

on the First and Ninth Amendments to the

U.S. Constitution,

he argued that Jenkins wanted to pay his taxes but the government must

accommodate his conscientious insistence that his money not pay for military

expenditures. On , prior to

the argument of appeal, more than 30 Friends had gathered in the cafeteria of

the Federal Court House in Manhattan for a special meeting of worship. In

rejecting the appeal, Judge Jose A. Cabranes wrote that such religious

objections to military activity have previously been rejected and that

Jenkins’ appeal was no different, though it was “presented in unusual garb.”

The Witness Coordinating Committee is conferring on next steps, including

possibly appealing to the

U.S. Supreme Court.

(An update in the issue noted

that Jenkins was denied cert on his appeal to the Supreme Court on

. It said that Jenkins was

preparing an appeal to the Inter-American Commission on Human Rights.)

Jenkins’s article was mentioned in the issue’s introductory editorial, where

editor Susan Corson-Finnerty wrote that “[t]he willingness of Quakers in that

period to risk the loss of their property and their freedom and to go to jail,

as Nathan Swift did, for the sake of their belief in nonviolence and their

faithfulness to that leading was remarkable.”

A historical overview of Carolina Quakers in the

issue noted:

Carolina Quakers as a rule stuck hard by the Peace Testimony; their refusal

to bear arms was honored to some degree, at least during more peaceful times.

As tensions rose between colonists and the Crown over exploitation of

resources and taxes, Quakers and other peace church people in the

Carolinas — Mennonites, Brethren, and Moravians — suffered

disproportionately. For instance, in they

were assessed a threefold amount for requisition of supplies for the army.

The Advice issued by Western Quarterly Meeting was to refuse compliance, and

many did so; many property seizures ensued. Others suffered also, as many

agents of the Colonial government were corrupt and were pocketing much of

their collections; seized property was often sold for small sums to friends

and relatives of these agents.

War tax resistance in the Friends Journal in

After noting several years of dwindling coverage of war tax resistance in the Friends Journal, it was a pleasant surprise to see that the magazine devoted its issue to the topic.

Robert Dockhorn wrote the opening editorial.

Excerpt:

Historically, many Friends have refused to participate in armed forces, and occasionally Friends, in an organized way, have refused to pay taxes to finance military activity.

But mostly, especially in recent years, only a few individuals, acting on the basis of individual conscience, have refused to pay taxes that are “mixed” — i.e. where one cannot determine which monies are funding which functions of government.

These individual Friends have sometimes received endorsement from their meetings, and on occasion, meetings (including yearly meetings) have gone so far as to encourage individual Friends generally to think seriously about tax resistance.

In this issue of Friends Journal, we offer several

articles that address this subject. At the center of them is a moral dilemma:

how can those of us who are clear that our government is pursuing an immoral,

militarist course live with our consciences in the knowledge that we are

funding this activity? What is required of us? What are our

real choices? What is our most effective response? And, at

another level: are we required only to be faithful to our

consciences, and to leave the consequences in God’s hands?

For — my wife, Roma, and I refused to pay the military portion of our federal income tax, as calculated by Friends Committee on National Legislation.

We donated the refused amounts to various causes that we felt were appropriate.

During these years I was employed by Philadelphia Yearly Meeting.

Eventually, the IRS came to my employer and sought to levy my wages for the owed amounts.

Much searching resulted, and the yearly meeting, while declining to turn over the funds, placed them in a separate account and did not hide them.

Eventually, they were attached.

And in , Roma and I prayerfully considered our course, sensed that we were no longer led to this resistance, and settled with the IRS, paying a substantial amount of interest and penalties.

We followed a leading, and the leading changed for us.

In the entire process, we were supported and nurtured by my monthly and yearly meeting (I am a Friend, Roma is not) — but it was our leading, supported by meetings, not the meetings’ leading.

And that is part of the question in these articles. It is not just about what

individuals can do, and should do. It is also about what all

Friends can and should do — together. How are Friends led today?

The first war tax resistance article in the issue came from Nadine Hoover, who told the story of Dan Jenkins’s attempt to get the courts to recognize conscientious objection to military taxation as a right of individual conscience that American citizens had before the enactment of the U.S. Constitution and that they had deliberately not relinquished by means of that document (see ♇ ).

The courts weren’t buying it, and in fact found the argument so far-fetched

that they upheld a $5,000 fine against Jenkins for using legally-frivolous

arguments. Hoover thought the arguments were good enough to be worth

repeating in the Journal, however.

She noted that “nearly three dozen Quakers and other supporters” joined Jenkins when he was arguing his appeal, and she argued:

To pay war taxes or to purchase from or invest in corporate structures that profit on war or use military might in order to secure wealth, in violation of our religious conviction, plants a dis-ease among us.

Friends’ witness is letting our lives speak — not that we will be protected but that we are willing to make ourselves vulnerable — knowing our faith will sustain us, set us free, and give us joy.

I have experienced this joy when I live in accord with my conscience and faith, regardless of the apparent, temporal consequences.

She invited “Friends who will stand before the courts and proclaim our faith… [or] write their statements of conscience and share them with others… [or] make the commitment to represent and/or support any Friend who is called to this witness” to write a war tax resistance committee of the New York Yearly meeting.

She hoped that if enough Quakers began to resist, they might make a change in the country the way the women’s suffrage movement did.

The change Hoover was hoping this would bring about was that the government

would legally acknowledge conscientious objection to military spending by

passing the Religious Freedom Peace Tax Fund bill, or something along those

lines:

Quakers, Mennonites, Shakers, and others have maintained this testimony throughout U.S. history.

Still many people today, of a wide variety of faiths, do not pay taxes for military purposes because this action violates their essential religious beliefs and moral convictions of conscience.

Passage of this bill by Congress would facilitate the payment of all taxes owed by these principled people.

Perish the thought.

Hoover shared a minute from the New York Yearly Meeting, dated

:

The Living Spirit works in the world to give life, joy, peace and prosperity through love, integrity and compassionate justice among people.

We are united in this Power.

We acknowledge that paying for war violates our religious conviction.

We will seek ways to witness to this religious conviction in each of our communities.

Then she listed off some possible “ways to witness”:

encourage your congregation to write and deliver a statement of

conscientious objection to paying for war

write a statement of conscience to include with your tax return and to

send to various other people

redirect some or all of your taxes “to an escrow account to be held in

trust for the

U.S.

government”

file more lawsuits using Jenkins’s 9th

Amendment argument

live on a below-the-tax-line income

divest from “corporations that profit from war” and invest and spend more

responsibly

“Pursue local ordinances that deny corporations recognition as persons,

and that deny recognition of corporate charters as contracts”

It was a long, rambling, repetitive, sometimes vague and random-seeming (what did corporate charters have to do with any of this?) argument.

It represents one weird extreme of the Peace Tax Fund idea, which had come to be seen by some supporters as an end in itself, rather than a means to a more important end.

Why do we resist paying war taxes?

Because that might help us get the Religious Freedom Peace Tax Fund bill passed!

The following article, edited by Karen A. Reixach, tried to account for how

enthusiasm for conscientious objection to military taxation had taken hold in

the New York Yearly Meeting in recent years. It began by identifying a

“movement of conscience” in much the same way that voluntaryists describe

ideal noncoercive politics, with a quote from

Jim

Corbett:

Nonviolent civil initiative by covenant communities is… the way human beings preserve and develop society based on consent, in which the rule of law, as distinguished from the rule of commanders, is necessarily grounded… Civil initiative must be societal rather than organizational, nonviolent rather than injurious, truthful rather than deceitful, catholic rather than sectarian, dialogical rather than dogmatic, substantive rather than symbolic, volunteer-based rather than professionalized, and based on community powers rather than government powers.

The article hoped to describe how when individuals articulate and share their conscientious yearnings, by means of a “statement of conscience,” they can find like-minded souls to form a “movement of conscience” that can work together to “act on our collective beliefs of conscience,” using the recent activity in the New York Yearly Meeting as an example.

She described some of the minutes and reports from the Meeting that had touched

on peace and justice issues in recent years, and on the Meeting’s support for

Dan Jenkins in his court cases. Then:

In the yearly meeting’s Committee on Conscientious Objection to Paying for War sponsored a series of conferences in support of this growing movement of conscience.

The first conference was held at Purchase Meeting the weekend following the oral argument of Jenkins in the Second Circuit in .

The court hearing and the conference were attended by about 35 Friends and others from the metropolitan area and the northeast region.

Out of that conference arose two strands of action: exploring the possibility of group legal action, and expanding the movement of conscience [PDF illegible] step of writing a statement of conscience.

The second conference, in at

Rochester Meeting, featured a public forum on the failure of violence that

included Robert Holmes, professor of Philosophy at University of Rochester;

Derek Brett, of Conscience and Peace Tax International; and Frederick

Dettmer, the attorney representing Daniel Jenkins. During the following day

and a half, Friends continued to consider action steps individually and in

concert with others.

The third conference was held at Flushing Meeting in … It focused on international venues for raising freedom of conscience issues as they apply to paying taxes for war.

A fourth conference , is being planned; and as momentum builds, we envision more every few months, inviting ever-widening circles of participants.

I don’t see many details there about what, if any “action steps” the conferees decided on.

Jens Braun is quoted in the article as suggesting some possible next steps:

to develop a better theoretical understanding of pacifism and the failure

of violence, so as to share this vision more convincingly

to “explore, develop, and improve the many ways Friends can work towards

not paying for war” —

get the Religious Freedom Peace Tax Fund bill passed

try new court challenges along the lines of Dan Jenkins’s

develop and use workshops and other outreach material

to join with counterparts in other countries, for instance at international

conferences

The Yearly Meeting then issued this Minute:

To Conscientious Objectors to Paying for War Everywhere,

New York Yearly Meeting of the Religious Society of Friends invites you to

join us in acknowledging that paying for war violates our conviction in the

Power of the Living Spirit to give life, joy, peace and prosperity through

love, integrity and compassionate justice among people.

We call on all conscientious objectors to paying for war to state in writing 1) your belief against paying for war and the preparations for war, 2) major influences in forming your belief, 3) how it is demonstrated by the way you live, and 4) a request that our government recognize and accommodate our convictions.

We ask anyone who prepares such a statement to send it to

NYYM

Committee on Conscientious Objection to Paying for War… We ask Friends to

send your statement to your monthly, quarterly and yearly meetings to record

in the minutes having received your testimony.

The thing that unnerves me is that it’s possible to read the whole article without seeing a single reference to one of these newly enthused New York Yearly Meetingers actually refusing to pay their taxes (except for Jenkins himself, who put his taxes in escrow with a promise to pay them into a government “Peace Tax Fund” once one was established).

There’s lots of talk about writing statements of conscience and holding gatherings and planning legal strategies and contacting legislators and all that, but where is the actual not-paying-for-war part?

Of “the many ways Friends can work towards not paying for war,” you’d think some of them might involve not paying for war.

Hopefully this just went without saying, but I worry.

A sidebar from David R. Bassett and Karen Reixach concerned the status of the

Religious Freedom Peace Tax Fund bill, and where one could look on-line to

find information about it. Another, by John Little Randall, described his

work with the National Campaign for a Peace Tax Fund and with Conscience and

Peace Tax International.

The following article, by Jens and Spee Braun, wrote about war tax resistance as part of (and contributing to) a larger project of living a life of integrity, and how not-straightforward it all is.

It’s a good overview of what a typical modern American war tax resister is in for:

Are you frustrated thar the war goes on and on?

Has your conscience brought up with you the subject of not paying for war?

Be careful; your conscience can make you do things (albeit for a good cause) that can turn your life upside down!

You don’t really want to think of refusing to pay part of your taxes to the

government, do you? For starters, no matter how you calculate the percentage

to refuse, there will always be some frustrating other formula that makes

just as much sense. You can use the FCNL percentage of the budget

going towards war, but the War Resisters League has another calculation and

number. You can refuse to pay a token amount, or you can simply not pay the

estimated 50 percent or so of the tax burden that goes to war-making, past

war debts, the Department of Energy’s nuclear weapons work, and all that

spying we do. How to decide?

And then, to top it off, you have to figure what to do with the money not going to the government!

Give it to charity?

Put it in an escrow account?

Use it for peaceful and life-affirming purposes at home or overseas?

Of course this problem can be avoided by living under the taxable-income level — if you don’t mind life without all the great stuff we have nowadays.

After you make these decisions of how to go about not paying for war, have

fun telling your employer that you don’t want any funds withheld from your

paycheck and not to send any money directly to the government for you!

If you get really serious, you can take the government to court, try to change the laws, or try to change the lawmakers.

So many options!

And that is not all. Deciding to be a conscientious objector to paying for

war and setting up the mechanisms by which you put action into your

intentions is the easy part. Once you do that, you know your conscience will

have taken a few strides into your being. And with that foothold (not to

mention the knowledge and understanding you have been given for having taken

those steps), your conscience will begin to demand all manner of other

deviations from a normal daily way of living!

Here is where life gets really dicey.

The problem is integrity.

As your conscience integrates one part of your life with your belief structure (and who says they need to be integrated — people have believed one thing and done another for as long as there have been people!), the process can turn into a domino effect with all sorts of other areas likewise wanting to be integrated.

It becomes a terrible sacrifice.

And don’t believe those who say it is actually liberating! It is like putting

your house in order: once you start organizing the mess, you keep finding

other things to clean up that you didn’t even know were out of place. Take

finances. It turns out that we could all pay less in taxes,

i.e., buy fewer bombs, if we took all the deductions coming to

us. What? Well, for example, if you keep track of all that travel to Quaker

committee meetings and write down the mileage in a little book to document

the expenditure, it may be deductible.

Businesses deduct driving and lunches (and even golf games), but Quakers seldom do.

That is so because we Quakers generally are not hagglers; we want to pay our full share of taxes to support our government as it builds roads, keeps up national parks, and pays politicians’ salaries.

We just don’t like that uncomfortable part that goes to war.

In the house-in-order analogy we want to share our cake, but not have part of it be eaten by our neighbor the landmine manufacturer.

You might think about something as useful and simple as your credit cards.

Who really wants to question those little pieces of plastic that make renting

cars or buying great books over the Internet so easy? Even (especially) if

you pay off your bill in full every month, there can’t be anything wrong, you

think, in using a system that would collapse if everyone were responsible,

saved their money before making purchases, paid off debts promptly, and

weren’t willing to pay usurious interest charges. In particular, don’t think

about how, if you do pay off your bill each month, the credit company

tolerates your borrowing money free of charge only because others don’t pay

up and you might not in the future. See? If you get started, who knows what

trouble you will make for yourself Now you have to think about going inside

to pay cash and talking to the gas station attendant rather than swiping the

plastic card out at the pump!

Can we retain integrity in our relationship to money?

Forget it!

You know very well that money is not important enough to spend precious time keeping track of, even if some folks call it a representation of our life force.

Better to spend time on that street corner protesting the lousy war.

And heaven forbid the government would audit our finances, since we have been occupied with the real spiritual tasks of speaking truth to power in public places.

They say money talks, but not like we can!

We’ve been told that early Friends opened their financial books to their

meeting communities. We can’t do that anymore — it’s hard enough to talk

about sex, but to talk about our money? Who can trust others that far — well,

except if the others are insurance companies, brokerage firms, or retirement

planners? We sure can’t trust our spiritual community to have the power and

scale of resources to support us in need or relieve the fears of what would

happen to us without money!

Yes, money is scary, so don’t bother pondering the irony of why fear of getting out from under its control ends up being even scarier then being part of a war-based society where you can believe whatever you want, as long as you pay up.

It’s not worth it — and besides, a messy house is so much more comfortable!

The next article was by Elizabeth Boardman.

She laid out the problem this way:

Among Friends, there is not much debate about whether war taxes are problematic.

Depending upon the federal budget for the year and how you count the line items, about half of our income tax dollars will be used for the outrageous costs of war.

Thousands of our personally earned dollars will be used to enrich the military-industrial complex, to make killers of young men and women,. and to cause death and destruction in the world.

Letting our own money be used this way is not consistent with good stewardship, with right sharing, with Quaker testimonies, or with Christian teachings.

The question of whether and how we can resist is much more complex. Standing

up to Goliath is possible only for the most confident David.

She mentioned a different set of anxieties than the Brauns had covered in their piece: worries that tax resistance or protest might trigger an audit (and then worries that such an audit might uncover math mistakes, or worse, “convenient” errors)… worries that the accountant who helps her with her tax forms will disapprove of her stand and maybe drop her as a client… difficulty reconciling willingly racking up IRS penalties & interest with her otherwise frugal and practical economic practices… difficulty finding the time to research and plan her tax resistance strategy… reluctance to break the law (or to be known as a law-breaker).

In the face of things like this, Boardman recommends that prospective war tax

resisters start small: maybe with phone tax resistance, or some sort of

symbolic protest like withholding $10.40 from your taxes or supporting the

Peace Tax Fund.

She also recommended that people who resist quietly, by slipping below the taxable income line, start making some noise about what they’re doing — otherwise “we accomplish nothing but a sense of personal righteousness.”

Following this were an excerpt from John Woolman’s journals

(see Excerpts from the Journal of John

Woolman) and from the letter Woolman and twenty other Quakers sent

to their fellow-Friends in to explain why

they could not pay taxes being raised for war expenses

(see ♇ ).

The next article in the set was by Steve Leeds.

He described becoming a war tax resister in and then drifting away in discouragement after the IRS garnished his salary for the taxes, penalties, and interest.

Then:

Fifteen years later, through renewed spiritual commitment and membership in a Friends meeting, I was led to take action with other Quakers on war tax resistance.

It began among a few of us, and that’s all it takes.

, my meeting began cohosting

war tax resistance gatherings with Northern California War Tax Resistance. We

urged Friends in our meeting to engage in symbolic war tax

resistance — refusing federal phone taxes, paying under protest, withholding

symbolic amounts, or living below the tax line — and letting our legislators

know about it. We found that a number of households in the meeting partook in

some form of war tax resistance, symbolic or otherwise.

Philosophically, it’s a slam dunk.

No more war.

Not with my dollars.

Logistically, though, it’s easy to become fixated on the mechanics and legal

aspects of war tax resistance. There’s a lot to learn and consider. My

journey, through discernment, prayer, and the support of others, led me to

focus on complex social and financial issues. Mostly, I have been confronting

my fear of the

IRS and

the insecurity of not knowing where this will lead.

For I have held back $1,040 from the IRS (symbolic of the IRS 1040 form).

Living with multiple feelings — fear, joy, and liberation — makes life whole.

My faith as a Quaker, striving to be nonviolent and to oppose all wars, has led me down this path.

I am sustained by the knowledge that many Quakers throughout history have resisted paying taxes for war.

When I think that we as a faith community need to do more, I know that the we starts with me.

So!

Quite a bit of material and many perspectives there — and a great deal of contrast in approaches between the pursuit of legal accommodation from the New York Quakers and the cautious but deliberate war tax resistance of the California Quakers (Boardman and Leeds were both from the San Francisco Meeting).

It had been years since the Journal devoted that much attention to the topic, and they haven’t done so since.

The series of articles prompted a lot of discussion in the

letters-to-the-editor column of subsequent issues — some of it quite hostile

to war tax resistance.

Dennis P. Roberts noted that the Bible is full of stories of war, and that

it “establishes beyond any doubt that the performance of an army in the

field is directly correlative to the quality of the faith and spirit of

the society or nation that put it there” and that because “the heart,

faith, honor, and spirit of a nation” is best represented by “the fighting

soldier, the fighting sailor, the fighting marine, the fighting airman,”

he finds that “this nonpayment of war taxes can indeed be carried to

frivolous extremes.”

Lucinda Antrim thought that war tax resistance “contradicts the Testimony

of Community… We are, here in the

U.S., members

of the community of the United States.… I find myself agreeing, somewhat

to my surprise, with the judge’s imposition of a ‘frivolous” fine on Dan

Jenkins.” (Naomi Paz Greenberg responded that she could not understand how

this vague and unarticulated “Testimony of Community somehow nullifies our

historic Peace Testimony”.)

Perry Treadwell responded that he did not recognize the

U.S. government

as his “community.” “Thirty-six years ago I was led to refuse to pay war

taxes… I currently send the small amount that I calculate this warrior

nation wants to agencies that support the families of wounded military

personnel. I have followed Thoreau’s warning:

‘What I have to do is to see, at any

rate, that I do not lend myself to the wrong which I condemn.’”

David Zarembka wrote in to correct “the impression that the

IRS

is as omniscient as God, all seeing, all knowing, never making a mistake

in getting the last farthing out of the helpless tax resister. Nothing

could be further from the truth.” He recounted some

IRS

blunders in his own case, and said, “I have always made sure that the cost

of the

IRS

getting funds from me exceeded any penalties and interest that they might

charge. In my 37 years of war tax resistance I am certain that I (and all

the other active war tax resisters I know as a group) have withheld much

more funds for government war-making and given them to peace organizations

than the

IRS

has ever collected, including penalties and interest. I don’t think that

this excuse should be used by Quakers as a group as a cop-out for refusing

to pay for our wars. In fact, if all Quakers in the United States were war

tax resisters, the

IRS

couldn’t even cope with our collective resistance.”

George Levinger, who said he’d been a phone tax resister in the Vietnam

War era, had soured on war tax resistance, considering it ultimately

counterproductive largely because the government succeeded in seizing the

taxes from him with penalties and interest. He suggested channeling the

resources you might otherwise use in war tax resistance “to contribute to

various sorts of peace-promoting organizations” instead.

Ruth Hyde Paine wrote in to promote the “penny poll” idea.

Gary Shuler wrote in to sing jingo bells: “As a retired military man, I

take exception to anyone who wants to use the privileges of this country

and not help to foot the cost. Many of my forefathers and yours died for

this freedom and you don’t want to pay taxes to keep it? Move! Cuba is

nice!” (Isn’t it cute that in someone

was still using the idea of tyranny in Cuba as a contrast to the

U.S. rather

than an example of it?)

For Pamela Haines, the challenge presented by war taxes seemed largely to

be a challenge to come up with good excuses not to resist them. Excerpts:

I don’t think the problem is just lack of courage, at least I hope not!

Part of the difficulty, I believe, is the extent to which we are embedded and enmeshed in a deeply violent world.

It’s not just the portion of my tax dollars that goes to deadly warfare.

It’s my computer, the disposal of which poisons poor people in Africa and Asia.

It’s my everyday purchases from invisible corporations that destroy lives and habitats far from mine.

It’s my energy consumption that threatens the very viability of future generations.

If war tax resistance seems too hard for most of us, what do we do if

that’s just the tip of the iceberg? Some Friends are not deterred by the

seemingly impossible and set out to disentangle themselves from the

whole mess — living below taxable level, with only the bare necessity of

purchases and a minimal carbon footprint. This may be a true calling for

some, and certainly a courageous one, but I know it’s not mine. To me

the focused goal of living a life free from complicity with

institutional violence would involve participating in another sin, that

of separation from my neighbors.

Is it better not to do a right thing, if by doing a right thing you would

be being inconsistent in not doing all possible right things?

In the issue, Jamie K. Donaldson explained why she gave up on trying to change the United States and left it rather than continue to be part of its war machine.

She’d contemplated tax resistance at one point, but decided it wasn’t for her.

Here’s how she describes that decision:

I was haunted by the quote attributed to former Secretary of State Alexander Haig: “Let them march all they want as long as they pay their taxes.” Suddenly the television shots of millions of people in the streets protesting the start of war lost their inspiration for me, and I wallowed in our powerlessness to prevent it.

Haig’s cynical remark exemplified my inner struggle as well as a wrenching

and age-old moral dilemma for all Friends. Some bear it as a cross, enabling

them to continue the Lamb’s War on behalf of love, truth, and justice. Could

I, too? Alas, the contradiction of working for peace while paying for war, of

being complicit by mere participation in the

U.S. “system,”

became untenable and intolerable. I explored war tax resistance, but rejected

it because I hold the assets of my incapacitated mother and could not allow

the government to garnish money for her care to recuperate my taxes withheld.

An obituary notice for Stephanie Kennedy in the issue mentioned her work on war tax resistance.

An obituary notice for Charles Richard Johnson in the issue called him “a dedicated war tax resister.”

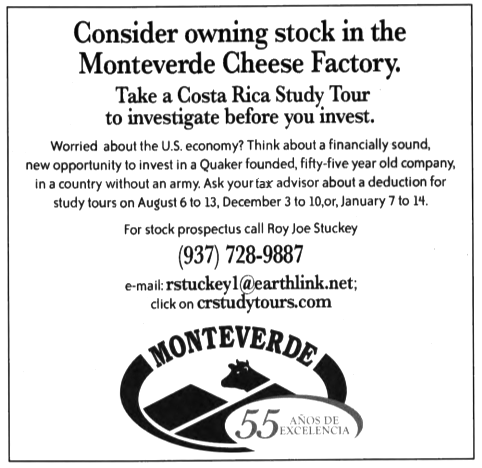

an ad from the Friends Journal in

pitches the Monteverde community in Costa

Rica, which was founded by American Quaker taxpatriates, as an ethical

investing opportunity and also a potentially attractive tax-break junket

War tax resistance in the Friends Journal in

There was a bit of an anti-war tax resistance backlash in the Friends Journal in .

In the issue, Peter Phillips came out against war tax resistance in a two-page article.

Here is a summary of his argument:

Friends’ advice against paying war taxes is sometimes incoherent.

The New York Yearly Meeting suggests that friends “examine… voluntary payment of war taxes” but taxes by definition aren’t voluntary.

The practice of some Quakers of refusing to pay but allowing the government to seize the amount by levy makes such war tax resistance “insignificant.”

What do people mean by “war taxes”?

If it’s the percentage of the revenue that goes to the Pentagon, even some of that money isn’t spent for war (for instance the Army Corps of Engineers work to rebuild hurricane-damaged New Orleans).

What about “reparations to Iraqis whose property is damaged” or “the Air Force’s remarkable mediation program that resolves employment and procurement disputes without litigation” — or, in the other direction, what about the Interstate Highway system, which was initially designed as a defense measure: is money raised for that, too, “war taxes”?

Is everyone on their own to decide what taxes are war taxes, or is there an authoritative answer, or is it okay to withhold symbolic amounts — what is the justification for withholding Elizabeth Boardman’s $10.40, an arbitrary amount that has nothing to do with war spending?

Withholding of taxes is not a good way of withholding funds from the war machine for the simple reason that the government won’t decide how to respond to a shortage of funds by respecting the reasons why the tax resister withheld them.

It is every bit as likely (perhaps more likely) to cut spending elsewhere.

“Should Head Start, research on solar energy, unemployment benefits, and support for healthcare all be underfunded in the exercise of our righteousness?

A consequence of my not joining the armed forces in was that someone else did who would not otherwise have had to.

People were hurt because I was not there to help.

This too is a consequence of conscientious objection.

Are those who advocate withholding part of their taxes prepared as well to live with the consequences of their actions?”

There is a Quaker ethic of trying to adapt to communal consensus that is expressed in many of its teachings, and the ethos of participating as equals in trying to probe a dilemma and adopt a communal consensus is one of the things Quakers have contributed to the American polis — war tax resistance turns its back on this with its ethos of individualism and rejection of the decisions of the community.

You will not be surprised to learn that Phillips’s article led to some exchanges in the letters-to-the-editor column in later issues.

Here is a summary of some of the back-and-forth:

Dennis P. Roberts thought the article was “the finest work on war taxes I have yet seen in the pages of your journal” and then told a half-remembered story about a terrible massacre in colonial Pennsylvania that could have been prevented but for the pacifism of the “strong Quaker elements within the settlement.”

— “I cannot say or recall with certainty whether this story is fact or fiction.

What does it matter?

Either way, an important lesson is drive home eloquently and powerfully: military preparations sometimes must be made.”

Robin Harper responded with some suggested guidelines for Quaker war tax resistance that he thought might meet some of Phillips’s criticisms (see ♇ for an excerpt from this letter).

David R. Bassett felt that Phillips had been too dismissive of war tax resistance in general after concentrating his criticism on a few specific arguments and methods he found to be weak or ineffective.

What about resisters who keep their income below the tax line?

Or people like Bassett who work in the judicial and legislative arenas to try to get something like conscientious objection to military taxation legalized?

Or folks who try to make sure their investments and purchases are clear of involvement in war?

Perry Treadwell compared Phillips’s “rationalizations” to “Friends’ historical resistance to confronting their complicity in enslavement,” and thought that just as a few Friends had to break from the pack and lead Quakers to an abolitionist stand, it will take Quakers speaking out against paying for war to make their “spiritual testimony” come to life.

Daniel Jenkins called Phillips’s argument “smooth and lawyerly” and “crafted… to lead to a foregone conclusion.”

He felt that Phillips gave short shrift to occasions when “conscience may sometimes transcend the constraints of conventionality and pressures of conformity.”

Naomi Paz Greenberg considered Phillips’s argument that by not serving or not paying taxes you are merely foisting the responsibility off on someone else to be flawed:

The moral consequence [of Phillips’s decision not to serve in the military] is not that other people were made to serve in his stead, as Phillips suggests.

The moral consequence of his not serving in war is simply that he did not violate his conscience by serving.

Others could have and did make their own choices, consulting conscience or not.

The moral consequences of not paying taxes for war are similarly direct.

She even suggested a more radical outlook toward taxes that I have rarely seen in Quaker circles:

Our taxes are compulsory, and in some sense they are the least desirable way to provide a constructive economic foundation for a compassionate society.

They presuppose that there is no Friendly nor Christian nor Jewish nor Hindu nor Muslim nor conscientious nor atheistic nor socialist love for one another and so we must be forced.

Paying taxes separates us from those with whom we might otherwise be in community, and with whom we might shake hands, share food, share laughter and tears.

Paying taxes for war separates us from many of them irrevocably.

Some Friends testify that we expect better of ourselves than that, because we know experimentally that God expects better of us.

Greenberg also felt that there was a big difference between the Quaker ethos of consensus and conformity when “recognizing the sense of the meeting” and trying to figure out how to confront “legislation written by lobbyists and summarized by Congressional interns in a process that has been compared to the making of sausage.”

An obituary notice for Kent Larrabee in the issue noted that “[f]or much of his life, Kent purposely lived below the poverty line in order to identify with the poor and to avoid payment of income taxes for war.”

In the issue, Arthur Waskow offered a reading of the “Render unto Caesar…” koan that puts it into a context of thousands of years of Rabbinical debate about the passage in Genesis that reads: “God created humankind in God’s own Image.”

He thought that Jesus had been intending to refer to this debate, and not intending to give any advice about taxes.

An obituary notice for Lillian Willoughby in the issue mentioned that “Lillian felt called to refuse to pay war taxes, and the IRS seized her car in .”

An obituary notice for Arthur Evans in the issue said that “[f]or 20 years, Arthur withheld the portion from his federal income tax that he believed went to war and weapons, and in , he was jailed for 90 days for refusing to turn over income records to the Internal Revenue Service.”

And an obituary notice for Merrill Hallowell Barnebey in the identified him as “a war tax resister.”

At the upcoming national gathering of NWTRCC at Earlham College in Richmond, Indiana, I’m going to be presenting a summary of the history of war tax resistance in the Society of Friends (Quakers).

Today I’m going to try to coalesce some of the notes I’ve assembled about the current period of Quaker war tax resistance — what I’m calling “the second forgetting.”

The Second Forgetting ()

After an enthusiasm for war tax resistance that had grown to a near-mania by there was an astonishing and swift drop in interest in the subject.

I can’t with any great confidence say why this might be, but here are some theories:

The collapse of the Soviet Union and the resulting end of the Cold War made people more optimistic about the chances of avoiding nuclear war and ushering in a more peaceful international order.

Even hawkish politicians were crowing about the “peace dividend” that would come from reduced military spending as a result.

War tax resistance may have slackened because peace work in general was seen as less urgent.

The “peace tax fund” idea had gained traction in Quaker circles.

Some Quakers who were concerned about their taxes paying for war may have chosen to refrain from taking action in the hopes that such a law would eventually give them an easy-out, or in the misapprehension that the absence of such a law made the Quaker taxpayer’s dilemma really a problem for the legislature and not for the Quaker.

It may have been simple demographics:

Those Quakers who were so confident in their war tax resistance stand that they were willing to start resisting when very few Friends were, and who as a result were the leaders and pioneers of the war tax resistance Renaissance, were reaching the ends of their lives at this point.

The younger resisters who joined up during the Renaissance may have been less self-sustaining, less confident, and less persuasive — following a trend more than they were following a compelling conscientious leading.

(This was a worry among Friends as far back as , when John Churchman wrote “Such build on a sandy foundation who refuse paying that which is called the provincial or king’s tax, only because some others scruple paying it whom they esteem.”)

In the Friends Journal, feeling it had reached the end of its legal appeals, threw in the towel and paid the IRS levy on the salary of its editor, Vint Deming.

Two German Quakers were prosecuted for war tax resistance, and their court hearing was attended by some forty Quakers.

Meanwhile in the U.S., the “peace tax fund” legislation got its first and only congressional hearing.

Several Quakers attended and a few testified in favor of the bill.

In a stage dramatization based on the IRS seizure of the home of war tax resisters Randy Kehler & Betsy Corner was part of the program at the Friends General Conference Gathering.

The Canada Yearly Meeting, after years of debate, adopted a policy of refusing to withhold taxes from the salary of war tax resisting employees.

In U.S. President Clinton signed the Religious Freedom Restoration Act, which seemed to offer some hope for a new court challenge against the government’s insistence on taxing religious conscientious objectors to pay for military spending.

In Quaker Priscilla Adams began a case using this argument; Quakers Rosa Packard and Edith & Gordon Brown filed similar suits soon after.

These suits didn’t make any headway.

In , Adams filed a final appeal to the Supreme Court, with the Philadelphia Yearly Meeting contributing a friend-of-the-court brief on her behalf, but the Court turned down the case.

By this time, sad to say, a superstitious, blinkered, panglossian take on the “peace tax fund” has become the norm, and on the rare occasions when war taxes are even discussed (for example, in the Friends Journal), it is taken for granted that should Congress pass such a law, American Quakers will finally be freed from having to worry about paying for war (and implied, in the spirit of the “forgetting,” is the sentiment “and until then, well, what can we do?”).

Statements from Quaker meetings about war tax resistance are increasingly endorsing the “peace tax fund” idea not in addition to supporting war tax resistance, but in lieu of it.

As dawns, most of the mentions of war tax resistance in the Friends Journal are found in the obituary column.

War tax resistance is presented as something that noble and honored Friends used to do; only rarely as something they are currently doing.

Nadine Hoover wrote an earnest plea for Quakers to adopt war tax resistance as a corporate testimony in , but it seems to have fallen with a thud and produced little effect or even debate.

In there were still some Quakers trying increasingly desperate legal arguments to try to get the courts to legalize conscientious objection to military taxation.

Dan Jenkins tried a Ninth Amendment argument, which is the constitutional equivalent of a hail mary pass (the court would not only reject the case, but found it so far-fetched that they also upheld a frivolous filing penalty).

That case is notable, though, for the amount of support he got from the New York Yearly Meeting.