Tax resistance in the “Peace Churches” →

Quakers →

20th–21st century Quakers →

Lorraine Ketchum Cleveland

War tax resistance and the American Friends Service Committee in the Friends Journal

The American Friends Service Committee, since its founding in , has been one of the most prominent ways modern American Quakers have tried to put their peace testimony into practice.

But it could be a voice of relative hesitance and conservatism when many in the Society of Friends were adopting war tax resistance.

And I mentioned the AFSC’s weirdly toothless response to the extension of the federal excise tax on phone service to help pay for the Vietnam War effort — to make stickers that people could put on their phone bills reading “The Vietnam War Tax Included in This Bill Is Paid Only Under Protest.”

(See ♇ 13 July 2013.)

Finally, I noted that the AFSC had tried to capitalize on the emerging concern among Quakers about war tax payment, war tax resistance, and war tax redirection, with a full page ad that encouraged Quakers to pay a “Peace Tax” — by calculating some percentage of their federal income tax… not in order to resist or redirect it, but in order to determine an appropriately-sized donation to give to the AFSC.

I dunno about you, but to me all of this looks less like an honest effort to grapple with the issue of taxpayer complicity and more like an attempt to ride a trend as a marketing opportunity.

In , the group decided to confront the issue more directly, though they did it in a peculiar way.

ad from the Friends Journal

Two employees of the AFSC — Lorraine Cleveland and Leonard Cadwallader — asked

the Committee to stop withholding war taxes from their salaries. The AFSC

complied with their request, sort of.

The Committee did not withhold the taxes from the employees’ salaries but

instead “withdrew from its general funds enough to cover funds not withheld”

and sent this to the

IRS

instead. Of course, to the

IRS,

none of that accounting really mattered… the money was money, whether it came

from the AFSC payroll budget or its general fund.

But then the AFSC applied for a refund of this amount.

When the

IRS

denied the refund, the

AFSC filed a lawsuit, claiming that:

For employees “to be forced to pay their war taxes without even the symbolic

gesture of refusal and enforced collection by the Government,” according to

the brief, violates the clause of the First Amendment that guarantees the

free exercise of religion.

(These quotes come from an article in the issue of the Friends Journal.)

This all seems like a strangely convoluted path that tangles around the heart

of the matter without really getting there. I suspect that this weird

dance — refusing to withhold war taxes from their salaries, but then paying

these taxes after all out of a different fund, and then immediately applying

for a refund of the amount paid — was deemed necessary by the lawyers as a

means of establishing

legal standing

that would enable them to successfully file their suit.

Also bolstering their argument about standing, the Committee’s legal brief

explained:

American Friends Service Committee is further aggrieved, and threatened with

irreparable economic injury because valuable, esteemed and loyal employees

have threatened to resign from their employment because the operation of the

withholding taxes has interfered with the expression of their religious

conscientious objection to the support of war, and because contributors have

questioned the propriety of their donations to an organization which acts as

a collector of war taxes.

That’s all well and good, but the First Amendment argument… hoo boy… were they

really arguing that the government is obligated to allow religious people

unfettered access to a “symbolic gesture of refusal and enforced collection”?

Is that what war tax resistance and the Quaker peace testimony are

about? Is that what the First Amendment is about?

Civil disobedience is one thing this legal gambit pointedly wasn’t.

The AFSC

apparently felt a strong need to stay within the law wherever possible, perhaps

because of the sensitive and vulnerable nature of some of their activities, or

perhaps because they worried about alienating donors.

A letter-to-the-editor from Bill Samuel in the

edition of the

Journal expressed impatience with this caution.

Excerpts:

I have known several [people] who would not be a part of a Society so

comfortable and content with the evil ways of the larger society. They are

not impressed with our “Quaker” President [Nixon] who grossly violates Quaker

testimonies and has not once worshiped with Washington Friends.

Often, even worse than the meetings in complicity with evil, are the “social

action” agencies, the prime example of which is the AFSC.

My yearly meeting has seen the evil of investing in war, but not the AFSC.

My monthly meeting refuses to pay the war tax on telephone service, but the AFSC even forbids regions

[the AFSC is structured as a collection of semi-autonomous regional offices]

that wish to follow such leadings from doing so.

An excerpt from an AFSC

board meeting transcript, reprinted in the issue of the Journal, is an example of

the temptation for the otherwise very pragmatic, hands-on group to retreat into

abstractions and mumbo-jumbo when the issue of corporate war tax resistance

came up:

When I think of the Spirit I think of something which ought, in the best of

circumstances, to permeate each large and small action which we carry out

throughout all of our lives. Even at those moments such as the present, where

in terms of a particular issue such as taxes, we want to take some action

which is paramount or transcending, we should take the action in the light of

the whole sense of the destiny of the human spirit, which we perceive as

somehow distilled and clarified at one particular historical juncture or

through one particular individual or corporate action. If one thinks of the

Spirit as a kind of unity, as I do, one has a great deal of difficulty in

dealing with the tax question the way we have been doing… It seems to me that

dealing with such questions of beliefs, one at a time and serially, mocks the

Spirit of totality — it seems, rather, that all these things should somehow

be wrapped up together in the Light.

But meanwhile, the AFSC lawsuit

was making its slow progress through the legal system. According to the

issue of the

Journal:

Others [aside from Cleveland and Cadwallader] testifying for AFSC

were Frances Neely, lobbyist for Friends Committee on National Legislation,

from Washington,

D.C.;

Cushing Dolbeare, Philadelphia; Tom (John T.) Flower, San Antonio,

TX; Henry Cadbury,

Philadelphia, and Bronson Clark, executive secretary of AFSC.

The government presented no witnesses and no evidence.

The Judge ruled in favor of the AFSC.

(Before you get too excited, the Supreme Court ruled that all of the AFSC’s attention to standing issues was for naught, as “The Anti-Injunction Act… prohibits suits ‘for the purpose of restraining the assessment or collection of any tax,’ [and so] bars the relief granted…”

That court reversed the ruling that had been in favor of the AFSC.)

The issue of the Journal trumpeted the initial decision. Excerpts:

AFSC Tax Case:

Decision Supports Peace Testimony

In what may become a landmark case, a United States federal judge has found

it unconstitutional for two Quakers and their employer, the American Friends

Service Committee, to be compelled to support war through taxes withheld from

their income.

“We are of the opinion that the withholding method of collection of taxes

does foreclose plaintiffs’ ability to freely exercise that part of their

beliefs requiring them to refuse to participate in war in any form…” the

judge said. “The tax which is withheld is in fact a tax on their incomes

which means that the support of whichever war we happen to be engaged in is

coming out of their pockets. The ‘support of war’ also includes the payment

of taxes in time of ‘peace’ so long as those taxes are used to support the

military’s defense budget generally. Quakers make no distinction between an

offensive or a defensive war. Both are equally objectionable.”

The judge also ruled that the section of the Internal Revenue Code requiring

AFSC

to in effect act as employer-middleman-tax collector for the government was

in this case unconstitutional. Judge Newcomer ordered the government to

refund $574.09 which AFSC

had paid as taxes for the plaintiffs while the case was pending.

“Quakers have for many hundreds of years taken the position that they could

not engage in war or violence of any kind and could not take the life of

another human being,” the judge said in his 18-page opinion. “In more recent

years this view has come to be known as the ‘peace testimony.’ The peace

testimony is not a negative concept but is rather a positive idea requiring

Quakers generally to strive to make war and violence unnecessary…

“When the peace testimony of individual Quakers comes into conflict with a

governmental requirement, the first step usually taken is to petition the

government to change its position. Quakers worked out such a change and

compromise with respect to alternative service during World War Ⅰ and

thereafter. If such a compromise cannot be worked out then the individual

must re-examine his or her conscience to determine if it is possible to live

with the government’s requirement or if not, then to disobey the law so as

not to violate conscience.”

In commenting about the case, Lorraine Cleveland, who has been refusing to

pay war taxes and has been

raising her concern within the Service Committee even longer, said, “There

has never been any doubt in my mind that the Quaker peace testimony was

protected by the First Amendment, and the confirmation of this by the court

strengthens my conviction that it is improper for me to pay war taxes.”

In an earlier statement prepared for the case, Lorraine Cleveland said her

refusal to support war in any form “has contributed to my own integrity — my

sense of wholeness — by bringing my actions into harmony with my deeply held

beliefs and with the guidance of my conscience. It (also) has kept me

sensitive to my own direct responsibility in relation to war in a world in

which ‘everything is connected to everything else.’ ”

“It has been our position,” said Bronson Clark, executive secretary of

AFSC,

“that the First Amendment protects us as an organization because of our

basically religious character, from acting as a tax collector for the

government in this matter of war taxes. We also believe that we should not be

forced to act as the government’s agent in a middleman role that deprives our

employees of the right to confront the government individually on this issue.”

Cleveland also penned an op-ed about the case that I found in the

Palm Beach Post:

When on

Judge Clarence Newcomer of the federal District Court in Philadelphia ruled

in favor of me and one of my former co-workers and the American Friends

Service Committee in our suit against the United States government, it marked

a turning point in an effort my husband and I began .

Judge Newcomer declared unconstitutional the withholding-tax method of

collecting taxes used for military purposes when, by its operation, it

violated my religious beliefs. He also relieved my employer of any legal

burden of taking those taxes out of my paycheck in consideration of my

conscientious objection to paying such taxes.

This ruling has cleared the way for me now to confront the Internal Revenue

Service as an individual without my employer acting as a surrogate tax

collector for the

IRS

The historic significance of Judge Newcomer’s ruling, though this was not a

class action, is that it is the first judicial recognition of conscientious

objection where war taxes are involved.

Many factors entered into my decision to oppose the Internal Revenue Service’s

collection of war taxes from my paycheck. Perhaps the most momentous of those

was in , when our government

dropped atomic bombs on Japan. This seemed to be the most monstrous evil, and

made me feel that some new and more demanding commitment was required of me.

By I had joined the Society of Friends

(Quakers) and was serving with the American Friends Service Committee in

postwar relief work in Europe where I saw firsthand the devastating effects

of war. When it came time to pay our tax, we

sent with our tax return a check payable to the United States Children’s

Bureau in excess of the amount of tax due and requested that this contribution

be accepted in settlement of our tax liability.

I explained to the government that the dropping of the bombs on Japan has led

me to perceive that I could no longer voluntarily pay taxes for military

purposes. I was willing to make an equivalent payment on an ear-marked basis

to any nonmilitary government agencies that could accept such payments.

, I have resisted

paying war taxes and the

IRS has

attached either my bank account or my salary. In

the board of directors of the American

Friends Service Committee, sensitive to the concern of some of its staff

members, agreed to take action together with me and Leonard Cadwallader,

another Quaker employe, to sue the United States to remove the committee as

the withholder of taxes for military purposes. This led to our successful

lawsuit.

It has seemed to me that a government in a free society should be able to

work out an arrangement so that its departments do not violate the First

Amendment of the Constitution while performing their functions.

This might cause the

IRS

some additional inconvenience, but, as Judge Newcomer said in his opinion:

“The additional cost of collection, if any, is a small price to pay when

compared with the possible frustration of the religious practice of bearing

witness to one’s conscience, which practice has sought the aegis of the

First Amendment.”

The tragedy is that so many individuals and organizations are over-whelmed by

the complications of the governmental bureaucracy and see no way to make an

effective protest on matters of conscience.

There was a single dissenting vote in the Supreme Court decision that

overruled this temporary triumph — that of

Justice William

Douglas, whose dissent sounded remarkably (almost incredibly) sympathetic

to the AFSC argument — going

beyond dissenting on the issue of whether the case could be heard under the

Anti-Injunction Act, and agreeing that the Quaker employees should have been

permitted to resist their withheld taxes. Excerpts:

The sole question on the merits is whether the provision of the Internal

Revenue Code… which requires employers to deduct and withhold from wages

federal income taxes, is constitutional as applied to employees, who on

religious grounds object to the withholding taxes on their salaries which

represent that portion of the federal budget allocated to military

expenditures. They invoke the Free Exercise Clause of the First Amendment, as

they are Quakers who are opposed to participation in war in any form and who

claim that this method of collection directly forecloses their ability freely

to express that opposition, i.e., to bear witness to their

religious scruples.

There is no evidence that questions the sincerity of the employees’ religious

beliefs. Nor is there any issue raised as to whether that religious belief

would give the employees a defense against ultimate payment of the tax. The

District Court held that the withholding was unconstitutional as to the

employees… a conclusion with which I agree.

The withholding process forecloses the employees from bearing witness against

the use of these monthly deductions for military purposes. Under the opinion

of this Court, they are deprived of bearing witness to their opposition to

war — these withheld portions of their salaries pay the entire tax and they

therefore have “no alternative legal remedy.”…

Quakers with true religious scruples against participating in war may no more

be barred from protesting the payment of taxes to support war than they can

be forcibly inducted into the Armed Forces and required to carry a gun, and

yet be denied all opportunity to state their religious views against

participation.… The Court misses the entire point of the present controversy.

The employees are barred from protesting these monthly deductions under the

Court’s opinion.… Here the employees challenge the withholding law as

depriving them of their one and only chance of contesting the

constitutionality of the withholding of the tax as applied to them.…

The religious belief which the Government violates here is that the employees

must bear active witness to their objections to their support of war efforts.

Dr. Edwin Bronner, who qualified as an expert on the history of Quakerism,

gave testimony which… stated: “[M]ost Quakers have considered it an integral

part of their faith to bear witness to the beliefs which they hold. It has

always been the prevailing view that simple preaching of one’s beliefs is not

sufficient, and that one’s actions must accord with and give expression to

one’s beliefs. Many of the employees of the AFSC,

including particularly appellees’ Cleveland and Cadwallader, share this

belief, and for these employees, the operation of the withholding tax, which

leaves them no option as to the payment of the taxes which they

conscientiously question, operates as a direct abridgment of the expression

and implementation of deeply cherished religious beliefs.”

If we are faithful to the command of the First Amendment, we would honor that

religious belief. I have not bowed to the view of the majority that “some

compelling state interest” will warrant an infringement of the Free Exercise

Clause.…

…to construe the Act as the Court construes it does not avoid a

constitutional question but directly raises one. The Act, read as literally

as the Court reads it, plainly violates the First Amendment as applied to the

facts of this case, for “no law” prohibiting the free exercise of religion

includes every kind of law, including a law staying the hand of a judge who

enjoins a law for the collection of taxes that trespasses on the First

Amendment.

…when it comes to the First Amendment and the free exercise of

religion, the mandate is that “Congress shall make no law… prohibiting” it.

The Anti-Injunction Act is a “law”; and the Constitution gives no such

preference to tax laws as to permit them to override religious scruples. May

Congress enact a law that prohibits a minister from preaching if his taxes

are in arrears? Or that disallows the making of a protest to a tax assessment

even though the assessment and payment violate one’s religious scruples?

Until today, I would have thought not. The First Amendment, as applied to the

States by the Fourteenth, bars a tax on the conduct of a religious exercise

by a minority even though that religious exercise is obnoxious to the

majority.… Dicta to the effect that an allegation of unconstitutionality is

irrelevant under the Anti-Injunction Act… — which the Court today elevates to

a holding — were based on the premise that there was an alternative remedy to

the unconstitutional actions. Here, as demonstrated, there is no other

remedy. A refund suit is of no value, since the religious scruples which

these taxpayers invoke relate to their inability to protest the payment, not

to the use of the taxes themselves for military purposes.

A retrospective on the life of Henry J. Cadbury, published in the

issue of the

Journal, opened by recounting an episode from

Cadbury’s testimony in this case:

…Marvin Karpatkin, chief attorney for the plaintiffs, had invited to the

witness stand the man who had presided at the first meeting of the

AFSC, on .

Henry Joel Cadbury had always been a man of slight build. Now at the age of

89½, he appeared frail and wizened, his rather rumpled suit hanging on him,

his manner occasionally hesitant, as though a little confused. He wore a

hearing aid, but although it was turned up to full volume it was still

necessary for him to ask a speaker to repeat himself. Those in the courtroom

who did not know him might have wondered what value his testimony could have.

Speaking slowly and clearly, Marvin Karpatkin led Henry Cadbury through a

recitation of his educational background, including his Ph.D.

from Harvard — a teaching career which included 20 years as Hollis Professor

of Divinity at Harvard — his many published books and essays, his role in

translating a new revision of the New Testament, his six honorary degrees.

Henry Cadbury answered each question with careful modesty, but the onlookers

were impressed, and when he acknowledged, in response to further probing,

that he had met with presidents Wilson, Hoover, Roosevelt, Kennedy, and Nixon,

the lawyer for the defense rather plaintively objected to this line of

questioning. The judge, however, appeared interested and denied the motion.

Switching to peace, the lawyer asked Henry Cadbury to describe the Peace

Testimony, and to tell the court what was meant by the term “bearing witness.”

“Bearing witness means, primarily, I suppose, a vocal expression of your

belief in certain ideals, but beyond that in the consistent expression in

your actions of those ideals.”

“Could you say in a nutshell that it means practicing what you preach?” the

lawyer pressed.

Henry Cadbury’s eyes danced and his face lit up with a delightful,

mischievous twinkle. Those who knew him well realized he had something

amusing to say. “Yes, or only preaching what you practice,” he quipped.

Today, while the AFSC continues to decry the enormous amount of money American taxpayers spend on wars past, present, and future, it also continues to stop well short of recommending any direct action by taxpayers (or even, usually, acknowledging that as an option) — instead it engages in projects to “encourage Congress” and “urge our leaders” to do something about it.

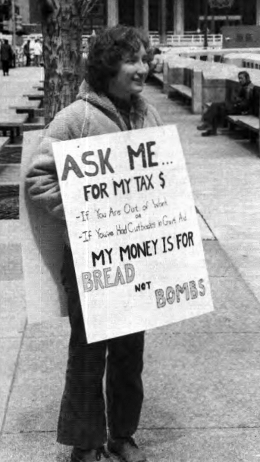

War tax resistance in the Friends Journal in

War tax resistance was a frequent topic of discussion in the pages of the

Friends Journal in ,

with an increasing emphasis on how Meetings as a body could engage in war tax

resistance, and with at least one Meeting taking the step of recommending that

all of its members begin resisting war taxes.

“A tax resister at a vigil in Philadelphia,

”

The issue noted that “a growing

number of Friends bodies” were organizing demonstrations against war taxes around the country:

New Call to Peacemaking approved the idea in one of its workshops in

. The idea of a Good Friday witness was

the subject of an “Epistle to All Friends in America” in

from North Carolina Yearly Meeting

(Conservative). In , Baltimore Yearly

Meeting endorsed the idea and suggested it be broadened to include members of

other churches. Friends Coordinating Committee on Peace endorsed the idea at

its annual meeting in .

The form of witness can be decided independently in each local area.

Participants might gather together for worship followed by public witness.

This could include an offering of letters from individuals, an appeal for

support of the World Peace Tax Fund bill, a vigil at the local

IRS

office, collection of withheld funds from tax refusers to be presented to a

local organization,

etc.

Also:

An effort is underway to collect signatures and funds for an ad in several

newspapers and magazines opposing the payment of military taxes. For a copy

of the proposed ad send SASE to Don Groersma…

A later issue reproduced this “Epistle to All Friends in America” from the

North Carolina Yearly Meeting:

Dear Friends:

Recognizing the potential effectiveness of simultaneous corporate action in

speaking truth to power, North Carolina Conservative Friends urge all Friends

everywhere to join with members of the several yearly meetings, and of the

Mennonites and the Church of the Brethren — persons who, together with

Friends comprise the historic peace churches — in making a witness to

Internal Revenue Service on .

It is urged that all Friends everywhere who are called upon to remit income

taxes to the U.S.

Government, and who are prepared to file an income tax return, do so on that

date and incorporate with their tax returns any one of several forms of

protest. Some examples of such protest include, but are not limited to, the

following:

Enclosing a letter stating Friends’ beliefs about the making of war, and

expressing concern that a large proportion of one’s taxes will be so used

as to violate those beliefs.

Withholding a small, symbolic amount of money deemed by Internal Revenue

Service to be owed as a tax payment, as a gesture of protest of the

war-making portion of our national budget.

Withholding that proportion of the taxes one is called upon to pay which

would otherwise go toward the making of war and war preparations.

Making a public witness, singly or together with others, giving

expression in deed as well as word that Friends stand prepared as a body

of Bible-believing Christians to still take seriously our call to

peacemaking in our increasingly troubled and militarized world.

We commend this epistle to you in the name of our Saviour, who continues to

set before us his standard, and who calls us to be faithful even unto death,

as he was faithful even unto death upon the cross.

Yet more impressively, on , the

Minneapolis and Twin Cities Meetings approved a minute that asked “all members

of our meetings to practice some form of war tax resistance”! That minute was

excerpted in the issue:

…We are called to nonviolent protest in response to preparations for war. We

recognize lovingly that individuals must conscientiously weigh their own

commitment to these traditions in the light of their own personal situations

and obligations. Yet we are asking all members of our meetings to practice

some form of war tax resistance:

To withhold all or a portion of our federal income taxes that go to pay

for war, shifting these resources from preparation for war to the meeting

of human needs;

To aid and support others who refuse to pay war taxes for conscience

sake;

To make every effort to reduce our federal tax liability through

contributions to peace-oriented and life-affirming endeavors;

To reduce our affluence through less than full-time occupations or by

other means to diminish income to or below the level of tax liability,

releasing thereby also time and energy to devote to endeavors related to

domestic and international justice and peace, living simply so that

others in the world may simply live;

To support and seek passage in Congress of the legislation which would

establish the alternative World Peace Tax Fund for receipt of funds from

citizens who cannot in conscience aid in the preparations for modern

warfare; and

To include letters of protest with our income tax statements as well as

to inform the president and our senators and representatives that we can

no longer in conscience share complicity for the current preparations for

war.

Our government and others seem prepared to bring catastrophe to humanity and

nature through the use of devastating weaponry. We recognize that those who

for religious reasons refuse to pay taxes for war are committing acts of

civil disobedience. We, members of the Twin Cities and Minneapolis Friends

Meetings, affirm civil disobedience through war tax resistance to be one

appropriate witness to our religious precepts and to be an expression of deep

concern for our country’s future.

We ask all citizens of other faiths to consider carefully these conclusions

to which we have come and to act in the light of their own consciences.

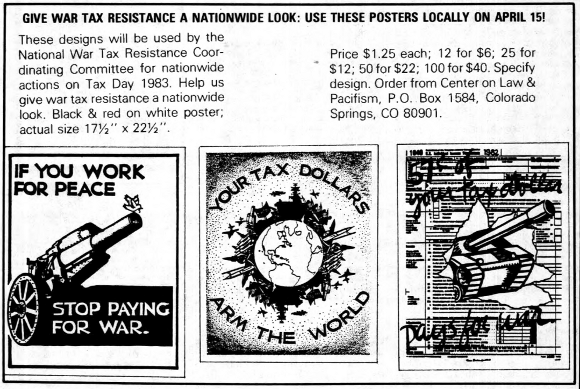

an ad from the issue of

Friends Journal

David Zarembka, identified as the treasurer of the recently-formed National

War Tax Resistance Coordinating Committee, had an article in the

about the American cultural norm

in favor of violence and the lack of strong taboos against homicide in our

culture. He concluded:

Like the prophets of the Old Testament, we must realize that our whole world

view, the whole intent of our society, is based on a divine misordering of

our lives and society. We must stop. Each individual must stop joining the

military, must stop working for the military in any fashion, must stop owning

stock in corporations that profit from military contracts, and must stop

paying military taxes.

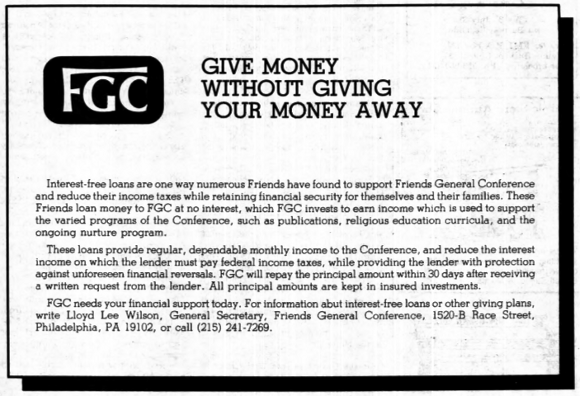

a Friends General Conference ad in the issue of Friends Journal promoted

interest-free loans to the Conference as a way to to keep assets secure

without gaining taxable interest income

One of three “burning concerns” addressed in Saturday sessions at the

Philadelphia Yearly Meeting in

was “The Draft and War Tax Concerns: Toward a Corporate Testimony” — but a

report on the sessions in the issue

noted that “unity could not be achieved” on that point.

The General Board of Friends United Meeting endorsed the World Peace Tax Fund

legislation, according to a note in the issue. The Meeting “calls upon its members to take action in

support of the bill before Congress… The World Peace Tax Fund,

FUM notes,

would provide a legal way for individuals to redirect their taxes ‘to

nonmilitary, peaceful purposes.’ ”

That issue also mentioned that Rahway and Plainfield (New Jersey) Monthly

Meeting had sent out a war tax resistance information packet to all the

monthly meetings in the New York Yearly Meeting.

“Bill Strong, member of the War Tax Concerns Support Committee of

Philadelphia Yearly Meeting, donates war tax resisters’ money to

St. John’s Hospice of Men,

.”

War tax resistance came up at the London (England) Yearly Meeting in

, and some delegates from

Philadelphia noted that the debate seemed very similar to the one Philadelphia

Friends were having. Norma Jacob wrote:

One major preoccupation this year, both in Philadelphia and in London, is the

withholding of taxes. In both places serious reservations were expressed

about the wisdom or the expediency of this particular form of protest against

war, and the arguments are the same. There are, perhaps, some differences in

the law, which may alter the degree to which the employer, in this case

London Yearly Meeting, is to be held civilly responsible. But there was no

reluctance to give support to the Friends House staff members who object to

supporting the military through taxes, even among those who might find

themselves in serious legal trouble as a result of a stand of which they

personally might not approve.

The issue noted that Lorraine

Cleveland had redirected $400 of her taxes to her Meeting so that it could

purchase a copy of the film The Hundredth Monkey

which she hoped could be used to demonstrate that “we have the creativity and

power to change both ourselves and this world.”

At the Lake Erie Yearly Meeting in ,

among the minutes they approved was one “encouraging monthly meetings to

establish meetings for sufferings to aid war tax resisters.” The North Pacific

Yearly Meeting met at

and also took up the issue, though the description given in the

Journal is vague about what they actually decided to

do about it:

During sessions set aside for seasoned concerns, a minute on war tax

resistance was presented by University Friends Meeting

(Wash.). The minute was

introduced and accepted in the context of Friends tradition and the need for

a supportive statement as expressed by the many tax resisters in attendance.

When Friends Journal editor-manager Olcutt Sanders

died in , Vinton Deming took his place.

Deming was a war tax resister, and would later try to get the

Journal to support his resistance by not cooperating

with the

IRS’s

attempts to tax his salary.

The Pacific Yearly Meeting met in

and, among other things, “established a peace tax fund.” The Ohio Valley

Yearly Meeting met

and “approved minutes in support of the World Peace Tax Fund and of

conscientious war resisters.”

The issue included this note:

A War Tax Resistance Minute by Davis

(Calif.) Meeting states,

in part, “We, the members of Davis Friends Meeting, affirm civil disobedience

through war tax resistance to be one appropriate witness to our religious

precepts and to be an expression of deep concern for our country’s future… We

are asking all members of our meeting to practice at least one of the

following forms of tax resistance”: to aid and support others who refuse to

pay war taxes for conscience’s sake; to support the World Peace Tax Fund

legislation; to include letters of protest with our income tax returns as

well as to inform our legislators that we can no longer share complicity in

the current preparations for war; to reduce our affluence and diminish our

income to or below the level of tax liability by living simply; to contribute

to peace-oriented or life-affirming endeavors; and to withhold a portion of

our federal income taxes that go to pay for war, shifting these resources

from preparations for war to the meeting of human needs.

That issue also reprinted a minute from the Washington,

D.C.

Friends Meeting concerning the phone tax:

The U.S. excise

tax on telephones has always been associated with war. Throughout the period

of American military involvement in Indochina, congressional proponents of

this tax said that it was needed to pay for the costs of war.

After the withdrawal of American troops from Indochina, the excise was to be

eliminated. Over the years it was steadily decreased from ten percent to one

percent. In this tax was increased to three

percent.

Friends have a long-standing testimony against participation in war and

preparations for war. At present, the Congress has ignored the popular

mandate for a freeze on the deployment and testing of nuclear weapons, and

has continued to appropriate funds for new weapons systems. Our president has

ignored public opinion polls which show that the majority of people oppose

U.S. military

intervention in Central America, and has proceeded with plans to commit

U.S. forces in

that region. Registration for the draft has been reinstituted.

We strongly urge Friends to consider whether it is appropriate to continue

payment of this war tax on telephones.

In the same issue, Tim Deniger had a letter-to-the-editor about the World

Peace Tax Fund legislation. Although he acknowledged that the proposed law

“does not address the problem of spending for defense versus social welfare;

it is simply a bookkeeping proposition which would ease the consciences of

pacifists” he had written a letter to a senator (Alfonse D’Amato of New York)

to urge him to support it. D’Amato wrote back to explain why he wouldn’t be,

saying in part:

[W]ithholding of tax dollars from the Department of Defense would simply be

an accounting illusion. Total defense spending would not decline. A larger

proportion of the tax dollars of other Americans would merely be used for

military programs. Most likely, it is the non-defense programs which would

end up being underfunded. Thus, despite its lofty intentions, the burden of

S. 880 would fall

most heavily upon the needy receiving benefits from a multiple of federal

social programs.

At the meeting of the Friends

World Committee for Consultation, Section of the Americas, “[r]epresentatives

approved a document outlining the implementation of a War Tax Resistance

Minute that the annual meeting approved [see

♇ 30 July 2013]. Positive responses and

cautionary notes from yearly meetings were considered when the war tax

subcommittee established policy for this FWCC corporate witness.”

The issue had a note about

Quaker Mark Judkins’s war tax protest:

…Mark brought $300 worth of food to the

IRS

center to pay for $78 worth of taxes. The food was not accepted as legal

tender. Police officers prevented the protesters from bringing the food into

the office. Mark announced that he would donate the food to the Milwaukee

Hunger Task Force’s food bank.

And the same issue noted:

War tax resisters in Ann Arbor,

Mich., are planning to run

ads in local and national newspapers and magazines listing the names and

addresses of signers of a statement setting forth their reasons for living in

volunteer poverty (below taxable income level) or refusing to pay some or all

income taxes or the federal excise tax on phones. Friends wishing to become

part of this project should write to War Tax Resistance National Ad Campaign…

War tax resistance in the Friends Journal in

In mentions of war tax resistance in the Friends Journal were few and far between.

In the issue, Cliff Marrs (a British Quaker) gave his interpretation of the “Render Unto Caesar…” koan from the Bible, and in particular what guidance it offers to those war tax resisters who take advice from scripture.

His point-of-view:

The idea that Jesus was circumscribing a political realm that was Caesar’s domain, and a sacred realm that belonged to God, is anachronistic.

Jesus, and his Jewish listeners, “regarded God as the Creator, and the whole universe as God’s domain — including politics — and would not have distinguished between the political and the religious.”

The tax in question “functioned as a kind of rent that assumed that all land belonged ultimately to the Roman Empire,” while core Jewish scripture makes it clear that Israel belongs to God.

The fact that Jesus had to ask someone else for a coin to use to illustrate his point may be significant — perhaps he did not carry such a coin because its use of a graven image that represented a member of the Roman ruling class as a divinity was idolatrous, or perhaps he had rejected Roman money and so (by the logic of his epigram) its taxes as well.

Maybe he was suggesting that it’s not sufficient to refuse to pay Roman taxes, but you ought to reject Roman money as well: give it back to Caesar and be done with it.

Would Jesus, who cared for the poor, really promote a regressive poll tax?

Paul’s unmistakable pay-your-taxes command in Romans 13 isn’t necessarily an interpretation of Jesus’s instructions, or even good advice in general, but was just a pragmatic, common-sense instruction to Christians living in Rome.

Since Jesus was ultimately charged with promoting resistance to Roman taxes prior to his execution, this seems to indicate that at least some of his listeners interpreted his message that way.

In short, biblically-oriented tax resisters should not be frightened off by the “Render Unto Caesar…” episode, as its interpretation is not so simple as its vulgar usage may suggest.

An obituary notice for Edith Carlton Browne in the same issue noted that “[s]he and [her husband] Gordon became military tax resisters in , and she continued that witness throughout her life.”

Another obituary, for Lorraine Ketchum Cleveland, said that “[i]n she became a war-tax refuser in a case that eventually went to the Supreme Court (Cleveland, Cadwallader, and the AFSC vs. U.S.A.).

Lorraine continued throughout her life to deduct from her federal taxes that portion that would be used for war, and sent it to a worthy cause.”

The issue mentioned the tax resistance of Robert Purvis, who refused to pay his Pennsylvania state taxes in protest against the state’s denial of equal voting rights to black citizens around , and then refused to pay “that portion of his property tax that went to support the schools” in when his children were refused admission to the whites-only classrooms. Purvis wrote:

I have borne this outrage ever since the innovation upon the usual practice of admitting all the children of the township into the public schools, and at considerable expense, have been obliged to obtain the services of private teachers to instruct my children, while my school tax is greater, with a single exception, than that of any other citizen of the township.

It is true, (and the outrage is made but the more glaring and insulting): I was informed by a pious Quaker director, with sanctifying grace, imparting, doubtless, an unctuous glow to his saintly prejudices, that a school in the village of Mechanicsville was appropriated for “thine.”

The miserable shanty, with all its appurtenances, on the very line of the township, to which this benighted follower of George Fox alluded, is, as you know, the most flimsy and ridiculous sham which any tool of a skin-hating aristocracy have resorted to, to cover or protect his servility.

An article in the issue mentioned in passing that “Quakers withdrew almost as a single body from the Pennsylvania legislature in rather than vote taxes for war.”

An obituary notice for Wally Nelson (not, I believe, a Quaker, but the obituary says he “demonstrated the values and commitment of a Friend; by his loving manner and unwavering integrity, he shaped an ideal for Friends to aspire to”) mentions his war tax resistance activities:

In , he cofounded Peacemakers, a national organization dedicated to active nonviolence as a way of life.

In , he and his wife, Juanita Nelson, began their lifelong practice of refusing to pay taxes used for armaments and killing.… During , the couple was among the founders of the Valley Community Land Trust, Pioneer Valley War Tax Resisters, and the Greenfield Farmers Market.

He was well known as a regular market vendor in downtown Greenfield and as a participant in the annual war tax protest in front of the Greenfield Post Office on tax day.

The issue noted that the Northern Yearly Meeting had “approved a minute expressing support for the Religious Freedom Peace Tax Fund Bill and for those who are conscientiously opposed to war taxes.”

At this point, those Quakers who cannot pay for military and weapons are subject to great sacrifice.

Some have refused employment that would result in a taxable level of income.

Others have exposed themselves to confiscation of their homes and other possessions.

We seek a legal mechanism whereby we may pay taxes and be responsible citizens without funding human death and suffering.

We view adoption of [the Bill] as providing religious freedom to many of our Society currently suffering for their faithfulness to their Quaker beliefs.

Add that all up and we get:

one abstract discussion of whether war tax resistance conflicts with Jesus’s teachings

three mentions of American war tax resisters recently deceased

one mention of a tax resister from

one mention of American Quaker war tax resistance from

one contemporary American Quaker Meeting advocating the latest Peace Tax Fund scheme and alluding to the acts of contemporary Quaker war tax resisters

Which is to say: next to nothing about actual real-life American Quakers doing actual, honest-to-goodness war tax resistance in .

From the edition of Tempo, a magazine of the National Council of Churches, comes this article by Margaret H. Bacon (who was information director of the AFSC at the time):

Must Pacifists Pay for War?

As the war in Indochina drags wearily on, more and more Americans are seeking ways to protest their unwilling complicity in a struggle which they regard as immoral.

There are more conscientious objectors in relation to draft age Americans than ever before in our history, more draft resisters, more protesters within the army.

And a small but growing band of war weary citizens are turning to another method of protest: refusal to pay that portion of Federal income taxes which supports the war.

“Why should I send my dollars to war when I myself refuse to fight?” the war resister asks.

“How can I prove the sincerity of my protest if I am too old for the draft, or the wrong sex, unless I am willing to take this simple positive step?”

Tax resistance is not new in this country.

First the Quakers and then the Mennonites brought the notion with them when they came as settlers.

In Pennsylvania, Quakers in the government agonized for years over raising war taxes at the request of the British crown, while private citizens often refused to pay either militia fees or war taxes.

Many Friends Meetings kept records of Sufferings which were largely accounts of property seized by the militia from members for non-payment of such taxes.

Other New Englanders seized upon the idea of civil disobedience.

William Lloyd Garrison made non-resistance a part of his abolitionist campaign.

Women suffragettes took up the theme.

In one famous case, Abbey Kelley Foster and her husband, Stephen S. Foster, refused to pay taxes on their farm because Abbey did not have the right to vote.

Modern Tax Resisters

Tax refusal, however, remained the act of a mere handful until after World War Ⅱ, when a few hundred pacifists decided to band together to reinforce each other’s determination not to pay taxes, to urge others to join with them, and to work for conscientious objector status for their tax dollars.

In , the Internal Revenue Service announced that 848 individuals had refused to pay a portion of their taxes on their income.

The figures will undoubtedly be much higher, since a spirited campaign was launched to increase tax resistance as part of the anti-war demonstrations of .

One roadblock in the way of the individual who wants to refuse to pay a portion of this income tax has been the withholding tax.

Many men and women find when April 15 rolls around that they do not owe the Government any money; their tax has already been collected by their employer.

In fact, the Government may owe them a refund.

A few individuals have tried to surmount this problem recently by claiming a large number of mythical dependents — in one case, all the wounded children in Vietnam — and informing IRS of this.

Others have pressed the organization for which they work to stop playing the role of tax collector.

Since Federal law compels organizations to withhold taxes from their employees, most employers have felt unable to comply with this request.

Even churches and service organizations dedicated to peace — even the strictly pacifist groups — have regretfully continued to serve as tax collectors.

Because of the obvious dilemma faced by a pacifist employer in demanding that his pacifist employee pay war taxes, such organizations have been seeking with increasing vigor for a way out of the double bind.

A possible source of relief to this situation appeared on the national scene when the American Friends Service Committee, a well-known Quaker organization, filed a complaint against the U.S. government for the return of AFSC funds which were paid to the government in lieu of Federal income taxes collected from employees conscientiously opposed to war.

The suit, which was entered in the United States District Court of Eastern Pennsylvania, may reach the Supreme Court because of the constitutional issue raised.

The Service Committee had long been under pressure to take this step from employees who were opposed to paying war taxes.

In its complaint to the government it stated that individual employees had threatened to resign and contributors had questioned the propriety of their donations while the AFSC continued to play the tax collector role.

The AFSC was in fact eager to find a way out, but it took several years of committee meetings and conferences with lawyers to formulate the case now before the courts.

The AFSC Claim

During , the AFSC began to honor the requests of several employees that it cease to collect from their salaries that percentage of their Federal income tax which goes for war purposes.

(51.6 percent according to the Friends Committee on National Legislation as of .)

When it came time to make quarterly payments to the IRS for withheld taxes, the AFSC took from its own general funds the sum of $574.09 to make up the deficit.

It is for the recovery of these funds that the claim is made.

Two AFSC employees are also serving as plaintiffs in the case.

They are Lorraine Cleveland, 60, Director of the Family Planning Program of the AFSC, and Leonard Cadwallader, 27, Director of Youth Affairs.

Mrs. Cleveland, who has been with the Quaker organization , has been a tax resister .

Every year she and her husband refused to pay and the Government took the money from their bank account.

Cadwallader, who is married and has a young baby is making his first income tax protest , though he and his wife had previously refused to pay the Federal war tax on their use of the telephone.

In Boston, two additional employees are planning to enter a similar suit, enjoining the AFSC to cease serving as the Government’s tax collector.

It is hoped that between these two suits the constitutional question involved will be brought to public attention.

At issue, the AFSC feels, is the right of the Government to compel an organization founded on conscience to violate the conscience of its employees.

“The Federal withholding tax which compels the AFSC to collect military taxes as hereinbefore defined from those of its employees who are by reason of religious training and belief conscientiously opposed to participation in war in any form, is in direct violation of the religious liberty guaranteed by the First Amendment to the United States Constitution,” the Quaker claim states.

If the AFSC wins its suit, the implications for all religious organizations are immense.

Even if it loses, the issue of conscientious objector status for tax dollars will have been brought more widely into public debate.

In , the colony of Rhode Island in consideration of its Quaker citizens wrote the first exemption for those of “tender conscience” to participation in warfare:

Be it therefore enacted, and hereby it is enacted by his Majesty’s authority, that no person (within this Collony) that is or hereafter shall be persuaded in his conscience that he cannot or ought not to trayne, to learn to fight, nor to war, nor to kill any person or persons, shall at any time be compelled against his judgment and conscience to trayne, arm, or fight, to kill any person or persons by reason of or at the command of any officer of this Collony, civil or military, nor by reason of any by-law here past or formerly enacted, nor shall suffer any punishment, fine, distraint, penalty, nor imprisonment, who cannot in conscience trayne, fight or kill any person, or persons for the aforesaid reasons.

Perhaps in tender conscience in regard to warring tax dollars will win equal recognition.

You can find out more about the AFSC lawsuit, which briefly succeeded but ultimately fizzled, in an earlier Picket Line entry.