How you can resist funding the government →

about the IRS and U.S. tax law/policy →

IRS incompetence →

enforcement effort/results →

levies, liens, and seizures

In war tax resistance circles, there have been whispers of a recent increase in the speed and number of IRS enforcement actions such as liens and levies.

The bottom line for our enforcement efforts shows that dollars collected rose again last year.

There’s a strong trend line going up.

was a watershed year for us, with a number of big initiatives that helped push enforcement revenues up 10% to $47.3 billion.

In , enforcement revenues — the monies we get from our collection, examination, and document matching activities — increased to a record $48.7 billion.

The press release breaks down the numbers a little more thoroughly.

For instance, sure enough:

In our collection activities, levies and liens continue to top their levels.

Levies increased by 36% to 3,742,276. Liens rose nearly 20% to 629,813.

These numbers are data but the IRS seems over-eager to jump from that to conclusions about the underlying situation.

Are increased enforcement efforts leading to more enforcement revenue, or is there just more tax money in general lying around for audits to discover — either because improving financial markets have caused people and corporations to owe more than in recent years or because they are more likely to be trying to illegally evade their taxes?

Hard to say.

I’m even more skeptical of the IRS’s own spin on the numbers when I learn how resistant the agency is to providing the raw data to groups like Transactional Records Access Clearinghouse so that they can do independent analyses.

(TRAC characterizes it as “continuing intransigence and unwillingness to providing public access to detailed statistics about many agency activities, along with a closed-door policy on releasing any meaningful results from taxpayer-financed studies on how our tax system is functioning.”)

Today, for instance, TRAC released its own analysis of IRS audit numbers for big corporations (which “controlled 90% of all corporate assets and received 87% of all the corporate income”).

TRAC finds that “the annual audit rate for these corporations, all with assets of $250 million or more, while increasing in has now receded to about the level it was in and is much lower than levels that prevailed a decade or more ago.”

In addition, the number of hours that the IRS spends on each of these audits has declined.

In , it spent 1,210 hours per audit of such corporations; in , it spent 958. But perhaps it is just being more efficient and effective and doesn’t need to spend as much time as it used to?

TRAC’s opinion:

Some economists and tax experts believe that other explanations are possible, namely that a massive surge in non-compliance is believed to have swept through corporate America.

Although government enforcement activities can be measured, accurately tracking the number individuals or corporations who secretly decide to break the law is extremely difficult.

In recent years, however, [IRS] Commissioner Everson, his immediate predecessor and many others have argued that case-by-case evidence strongly suggests more and more corporations are skirting the law.

The bottom line: a real increase in the number of non-compliant taxpayers may explain the increase in enforcement revenues.

Therefore, while it is true that enforcement dollars are up, particularly for recommended audit adjustments among the largest corporations, the reason remains unclear.

In the face of lowered coverage and audit hours, this increase could be due to a more effective IRS audit program.

However, if corporate noncompliance is up, it could be that the dollars require less effort to find.

Step right up folks — you won’t want to miss this exciting new attraction — direct to your computer screen from the wilds of deepest Washington, D.C. — it’s the Internal Revenue Service Data Book !

<frog class="kermit"> Yaaaaaaaay! </frog>

I’m going to try to find something interesting in its 84 pages of statistics.

Here goes:

Each year, people like myself file their tax returns but don’t include enough payment to cover the assessed tax, penalties, and interest.

Here’s how much overdue tax, penalties, and interest have been assessed in each of the past few years (this doesn’t include the interest and penalties that continue to accrue on past-due accounts):

year

amount

$46,738,194,000

$50,680,546,000

$57,594,901,000

$69,555,590,000

The IRS collected almost $41 billion (59%) of this (but this amount does include accrued interest and penalties, so there’s an apples and oranges aspect to this comparison) — $1.7 billion of this through their new program of outsourcing some cases to private debt collection agencies.

Of the total that was collected, taxpayers sent in $15 billion (37%) in response to the first nastygram from the IRS, and another $13 billion (33%) in response to the second nastygram.

The last $12 billion (30%) was recovered through “taxpayer delinquent accounts and additional actions.”

Liens, levies and seizures are all up over recent years:

year

liens

levies

seizures

544,316

1,680,844

399

534,392

2,029,613

440

522,887

2,743,577

512

629,813

3,742,276

590

Oh, there’s more… but I’ve got my boredom threshold too.

The IRS has just released its audit figures for .

Audits are up across-the-board.

This in spite of not having significantly more enforcement personnel or budget.

In the past, a closer look at the numbers has shown that they’ve accomplished this miracle by emphasizing “correspondence” audits over “field” audits.

It looks like this is again the case.

While about three-quarters of the total audits the IRS conducts are correspondence audits, more than 90% of the increase in audits this year comes from correspondence audits.

The agency also seems to be backing off on audits of large corporations.

These have the potential to be big-bucks items, but they also take a lot of time and a lot of personnel — both of which can be redeployed to increase the numbers elsewhere.

Indeed, the larger the large corporation, the stronger the drop-off in enforcement in recent years.

Corporations in the $50–100 million asset range have seen their likelihood of an audit drop from 16.4% to 11.4%; those in the $100–250 million range have gone from 17.5% to 12.1%; those above $250 million have dropped from 44.1% to 27.2%.

The strategy may be a wise one.

“Overall, enforcement revenue reached $59.2 billion, up from $48.7 billion in and nearly $34.1 billion in .”

On the other hand, this increase could reflect increased tax evasion rather than more effective enforcement — the same sized slice but of a larger pie.

Levies, liens, and seizures are all up over last year’s numbers.

After last year’s leap over the previous year from 2,743,577 levies to 3,742,276, this year’s increase is much more modest: to 3,757,190.

The IRS Data Book is out.

It includes information on IRS enforcement activity.

In the charts below I’ve combined the numbers from this Data Book with those from an earlier edition to give a longer-term picture (I wasn’t able to find earlier figures for non-filers).

The number of people who file but who don’t include a check for what they “owe” has been increasing:

And the IRS’s backlog of these delinquent accounts has been going up as well:

The number of people who fail to file their returns when they’re supposed to also seems to be going up:

The IRS is responding with increased enforcement activity, including levies…

…liens…

…and, much more rarely, seizures.

, I took a look at the IRS enforcement numbers over the last several years.

TIGTA has now released its own analysis.

They note increased levies, liens, and seizures during the past several years, leading to an increase in the total revenue collected.

But they also say that “the total dollar amount of uncollected liabilities increased to the 10‑year high of $290 billion.

In addition, the gap between new delinquent account receipts and closures had widened by almost 63 percent by the end of .

[T]he number of taxpayers (866,777) and the amount owed ($34.9 billion) on accounts in the Queue were each at a 10‑year high.

One reason for the increase in the Queue this year is a rise in the number of compliance assessments.

While the Queue is a source of work for Collection function employees, a significant number of accounts in the Queue might never be worked.

In addition, in , the IRS removed almost 7.6 million accounts with balance-due amounts totaling almost $31.2 billion from Collection function inventory.

These accounts might never be worked.

Here are their numbers (which are mostly the same as the numbers I found, except that they go back a couple of years more):

Another choice quote:

More TDAs were received than closed, and the gap between TDA receipts and TDA closures had widened by almost 63 percent (to 1,914,508 accounts) as of .

This is the largest year-end gap in the 10‑year period.

… The Collection function is unable to work all of the existing accounts in the Queue with current staffing, and the number of TDA receipts is outpacing closures.

IRS

Policy Statement 5-34 provides that, “Collection enforced through seizure and

sale of the assets occurs only after thorough consideration of all factors

and of alternative collection methods” and that “the official responsible for

making the decision to seize must be satisfied that other efforts have been

made to collect the delinquent taxes without seizing.… Seizure action is

usually the last option in the collection process.” Yet,

TAS

is now seeing in its cases an inclination toward seizure despite the

existence of viable alternative collection methods. In addition,

TAS

is witnessing apparent failures on the part of the

IRS

to follow various provisions of the

IRM

regarding the collecting process. For example,

TAS

has seen the

IRS

seek extensions of collection statute expiration dates

(CSEDs) in apparent contradiction to the

terms of

IRM

§5.14.2.1 (). In several

instances,

TAS

has also observed the imposition of a levy on assets in a taxpayer’s

retirement account even though the requisite “flagrant

conduct”* did not appear to be present.

* IRM §

5.11.6.2(5) () (stating that

funds in retirement accounts are not to be levied if the taxpayer has not

engaged in flagrant conduct and providing examples of flagrant conduct,

including taxpayers who make frivolous arguments, are convicted of tax

evasion, are assessed fraud penalties, and hide assets).

And…

The National Taxpayer Advocate is seeing cases in which delinquent tax

accounts have sat for five to ten years without meaningful

IRS

intervention only to be aggressively pursued as the

CSEDs

draw near. Such prolonged periods of

IRS

inactivity significantly exacerbate taxpayers’ delinquency problems due to

the accumulation of interest and penalties.

The IRM

states that seizure should be considered for taxpayers who “won’t pay” and

provides a number of examples of such taxpayers (including “taxpayers who

have the ability to remain current and/or resolve their delinquent taxes

through an alternative collection method but will not do so” and “taxpayers

who will not cooperate with the Service,

e.g., taxpayers that evade contact, will not

provide financial information, etc.”). These examples focus on taxpayers’

present conduct, not their past noncompliance. Yet,

TAS is

seeing a tendency to use the noncompliance that lead [sic.]

to taxpayers’ deficiencies and other past behavior, not the current level of

cooperation and willingness to find a way to resolve the liabilities, to

justify seizure.

Senators Max Baucus and Chuck Grassley, the top Democrat and Republican on the Senate Finance Committee, issued a press release to convey their outrage or what-have-you.

Grassley summarized the new report this way:

For , while collections increased by $10 billion, unpaid debts

increased by the same amount. During this same time, the

IRS

wrote off from 31 percent to 46 percent of unpaid debts because it

essentially ran out of time to collect these debts. For

, the

IRS

classified only $100 billion out of $290 billion of unpaid tax debts as

collectible. Of the $100 billion potentially collectible debt, the

IRS is

actively pursuing only $25 billion with $2.5 billion being shelved because

of a claimed lack of resources. The longer a debt is outstanding, the less

likely it will be collected. Any business person can tell you that. Knowing

that the

IRS

isn’t going to collect the debt also gives tax cheats additional

incentives not to pay.

The senators conclude: “When all is said and done, over half of the tax debt

inventory that the

IRS

resolves will come from writing off the tax or being prevented from collecting

it under the 10 year statute of limitations.” The numbers in the report

specify this a little more precisely: 20–28% of these tax debts were “abated…

which may have been appropriate” and 31–46% were “written off due to statutory

limits on how long

IRS

could pursue the debt.” Only between 34–41% of the tax debts that were

“resolved” involved the

IRS

actually getting its hands on the money.

Expect the next Congress to try to come up with some ways to squeeze a little

more blood from that stone.

The report has some interesting background details on the

IRS

collection process, and a nice flowchart (see page 7 of the report) of how tax

debts get routed around (and sometimes stall) in the process.

Here, for instance, is the initial phase of the process for people who do not

file, spelled out nicely:

IRS

first is to send a “30-day letter” that includes a proposed assessment of

tax, penalty, and interest. The letter is to instruct the taxpayer on

possible ways to respond, such as by accepting the proposed assessment;

filing an original return; providing evidence that there is no filing

requirement; or appealing the proposed assessment to

IRS’s

Office of Appeals. If no response is received to the 30-day letter within the

allotted time,

IRS is

to send a 90-day statutory notice. The statutory notice is to contain

information similar to the 30-day letter and information on the taxpayer’s

right to petition the Tax Court. If

IRS

does not receive a response within the allotted time, the tax, penalty, and

interest on the return are to be assessed.

IRS’s

practice is to send up to four balance-due notices at 5-week intervals for

the amount owed. Six weeks after the fourth balance-due notice,

IRS is

to forward any unpaid accounts to

IRS

staff who are to try to collect the unpaid amounts through other phases of

the collection process — the telephone or in-person contact phases.

There were also some nuggets of information about new

IRS

enforcement-related projects. A few caught my eye:

Electronic Lien — to process over a million liens each year

Streamline and expedite lien filing, reduce lost lien reports, and ensure

prompt payment of lien filing fees by making process electronic.

Reduce costs for lost lien research and analysis by 15 percent in

and 40 percent in

. Similar savings in these 2 years in

lien filing fees. Collect additional revenue by raising

IRS’s priority against other creditors.

Bulk Electronic Levy

Automate the process for delivering levy notices to and processing

responses and remittances from financial institutions and large

employers, including the posting of levy payments to taxpayer

accounts.

Reduce the cycle time for sending levies. Reduce mailing costs. Expedite

posting of payments to taxpayers’ accounts.

Camera cell phones

Improve (1) productivity of revenue officers in determining asset

valuation, (2) communication between

IRS

and taxpayers, and (3) employee safety on field visits.

Increased employee and taxpayer satisfaction.

I assume that last bit means that when the

IRS

comes a-callin’, they’ll be whipping out their phone cameras to snap a quick

picture inside your doorway or outside your driveway so they can look at the

photos later and see if anything is worth stealing.

The new IRS Data Book is out, so I can update the numbers.

Breaking with recent trends, both seizures and levies were down , though there was another big jump in liens filed:

On the “delinquent” side, the number of people who didn’t pay their taxes

when they were due held steady, and the number of people who didn’t file on

time (or at all) dropped, but the

IRS

continued to to be overwhelmed by the backlog of delinquent cases and so the

total unresolved delinquent accounts continued to rise:

The IRS wasted a lot of time and energy rolling out its private debt collection scheme, and now they’re going to have to waste a lot more time and energy unrolling it now that it’s been abolished.

They lost enforcement manpower in the course of that experiment, too.

They say they plan to beef up in that area, but this will take time and the rookies will need training, so I think we can expect them to continue to have problems with their enforcement backlog for a while.

Some links that have caught my eye recently:

The Green Zone: How a Greening Culture Cannot Ignore the Military.

The elephant in the room during the debate over the environment and climate change and what-have-you is U.S. militarism.

If “the largest source of pollution in the world is the military, particularly the military at war” then maybe environmentalists have something better to do than encourage people to change their lightbulbs.

Tax resistance by American fiscal conservatives against taxpayer-funded bailouts and deficit spending continues to be an idea that has yet to come, though a lot of folks are meekly hoping somebody else will get the ball rolling.

The latest of these ideas goes by the name “Operation Dep 9” and encourages folks to re-file their W-4 forms, claiming 9 allowances so as to reduce or eliminate federal income tax withholding (this is the same technique that many war tax resisters use).

China’s official Xinhua news agency said the local government’s plan to more strictly enforce payment of taxes from the furniture makers and dealers has been suspended in the face of the opposition.

China’s furniture industry has suffered in the global economic downturn from a decline in demand from export markets.

Thousands of similar protests over taxes, land disputes or corruption are reported in China each year.

The IRS has something called the Federal Payment Levy Program, which is designed to intercept payments coming from the federal government to people who have tax debts.

According to this report, “the bulk of FPLP levy payments have historically been related to Social Security benefits.”

At one point there was a hardship income threshold under which the government would not seize social security benefits to reclaim taxes, but the government phased this out and finally eliminated it at the beginning of .

The Taxpayer Advocate noted that this was further impoverishing some people on fixed-incomes who were already below the poverty line, and proposed a new filter.

The IRS has agreed to implement a “low income filter” that “will exclude taxpayers from the FPLP if their estimated income (based on internal IRS data) is less than 250 percent of the poverty level.”

This change is due to begin in .

The “internal IRS data” the report speaks of here it tries to explain in a footnote:

To compute the taxpayer’s income, where the taxpayer has filed a tax return for the most recent year or two, the IRS will use the greater of the total positive income from that return, or income based on payor documents filed with IRS for that year.

Where no such return was filed, the IRS will use payor documents for the most recent tax year.

To determine family size, which is a component of the federal poverty level computation, the IRS will use the family unit size claimed on the taxpayer’s most recent return filed for the last two years, or if no such return is filed, the IRS will assume a family unit size of one.

Although people with low-incomes may be saved from having their social security seized via FPLP in this way, the IRS may still use other collection techniques.

For instance, they may seize the bank account your social security payment is deposited into, thus saving you from a partial levy only to hit you with a 100% seizure.

Or they may file a “paper levy” to attach 100% of future social security payments until the unpaid tax is collected.

For low-income tax resisters, this will require vigilance.

Still, the Advocate predicts that this change “will protect hundreds of thousands of taxpayers from economic damage and unnecessary interaction with the IRS.”

According to the Advocate, “many of the collection policies and practices in place today have little empirical justification even as they violate the spirit, if not the letter, of the IRS Restructuring and Reform Act of and result in unnecessary harm to taxpayers.

For example, despite the fact that IRS levies and Notice of Federal Tax Lien filings increased by approximately 590 percent and 475 percent, respectively, [see The Picket Line, ], overall inflation-adjusted collection revenue declined by approximately 7.4 percent over the same period.”

The IRS appears to be systematically exaggerating the effectiveness of its collection efforts by attributing any revenue collected during the collection process, even things like subsequent tax refunds being automatically intercepted before they’re sent, as being attributable to the activities of collections personnel.

Also, “[t]here is an astonishing lack of transparency as to what is included in the revenue figures and how they are computed.”

The hardship standards that the IRS uses to determine whether a tax debt is collectible (that is, is there anything to seize, and will seizing it effectively throw the taxpayer onto government assistance, thus robbing Peter to pay Peter) don’t take into account things like credit card debt, school loans, and medical bills.

In many cases, they’re trying to get blood from a stone.

The IRS tends to file official lien notices haphazardly, without much regard for whether they are effective.

Their policy seems to be: when an account reaches a certain threshold of unpaid balance, file a a notice of federal tax lien.

This even though very little collection revenue comes from liens and though a lien notice like this can make it more difficult for delinquent taxpayers to get back on their feet financially.

(These notices make the “secret lien” filed against all delinquent taxpayers part of the public record, available to potential creditors and employers and landlords and such, and put the lien into effect so that the IRS can skim money, for instance if the taxpayer sells property or has accounts receivable.)

Taxpatriatism appears to be rife.

According to the report, “[i]t is estimated that more than seven million American citizens reside abroad.

Although U.S. citizens are required to file U.S. income tax returns regardless of their residency status, IRS data show that only 462,340 taxpayers (or 6.6 percent) filed returns from a foreign address in tax year 2007.”

The “offer in compromise” program — in which people with large tax debts they can’t pay off can enter into an agreement with the government to pay a portion of their debt, comply fully with the tax laws for five years, and have the remainder of their debt forgiven — has become useless for most people.

Now, in order to use this program, you have to pay a fee and submit a substantial down-payment along with your application (which involves “more than 100 steps in a 44-page package”) — and then your application may still be declined.

Weirdly, the IRS processes our 1040 forms before it processes the W-2s and 1099s that substantiate the income we report.

This makes it easy for fraudsters to understate their income and get refunds before the government knows anything is wrong.

“The IRS is experiencing high levels of new individual taxpayer payment delinquencies in categories that could produce high levels of subsequent noncompliance.”

Music to my ears.

The new IRS Data Book is out, so I can update the numbers.

The number of levies and seizures are down from their peaks, but the use of liens continue to rise:

On the “delinquent” side, the number of people who didn’t pay their taxes

when they were due and the number of people who didn’t file on time (or at all)

are both off from their peaks, but the

IRS

continued to to be overwhelmed by the backlog of delinquent cases and so the

total unresolved delinquent accounts continued to rise:

A few more things of interest that passed through my RSS aggregator and email inbox while I was away:

George Monk and Molly Schaffnit went off-the-grid and back-to-the-land, motivated in part by their desire to live under the tax line on a lower income to avoid contributing to the U.S. military.

The Charleston Daily Mail tells their story. Also: they have a web site.

Counseling Notes — how tax resisters can avoid getting preyed upon by “settle with the IRS for pennies on the dollar” companies; more “frivolous filing” overreach from the IRS; and increased use of IRS enforcement tactics isn’t leading to increased tax revenue

Many Thanks — to the generous donors who keep NWTRCC in business

Criminal Cases and Fear — Karl Meyer writes from the standpoint of decades of experience with war tax resistance about what factors increase the likelihood of criminal prosecution for war tax resistance. Larry Dansinger and Ruth Benn add two cents apiece.

War Tax Resisters in History — Ed Hedemann reviews some of his research into the U.S. government’s use of property seizures and criminal cases as tools against war tax resisters in the post-World War Ⅱ era

Resources — notes on the Death & Taxes DVD, the new “Thoreau and His Heirs: The History and the Legacy of Thoreau’s Civil Disobedience” study kit, and the NWTRCC fundraising scarves

NWTRCC News — a note on the upcoming national conference in Boston next month

The “National Taxpayer Advocate” (a sort of IRS ombudsman position) released her annual report on .

As was the case in her report last year, she complained that the IRS is overusing its enforcement techniques of levies and liens in ways that are cruel and, even from the perspective of government revenue, counterproductive — , the number of liens the IRS has filed each year has increased by 550%, but the amount of revenue collected through such enforcement efforts has not increased at all.

“By filing a lien against a taxpayer with no money and no assets, the IRS often collects nothing, yet it inflicts long-term harm on the taxpayer by making it harder for him to get back on his feet when he does get a job,” Taxpayer Advocate Nina Olson said.

“Absent data that show liens make a meaningful contribution to revenue collection and especially in this economy, I find it unacceptable that the IRS continues to torment financially struggling taxpayers in this way.”

The government of Romania is threatening to tax the nation’s witches, astrologers, and fortune tellers.

Curse them!

A dozen witches will hurl the poisonous mandrake plant into the Danube to put a hex on government officials “so evil will befall them,” said a witch named Alisia.

She identified herself with one name — customary among Romania’s witches.

Queen witch Bratara Buzea, 63, who was imprisoned in for witchcraft under Ceausescu’s repressive regime, is furious about the new law.

Sitting cross-legged in her villa in the lake resort of Mogosoaia, just north of Bucharest, she said she planned to cast a spell using a particularly effective concoction of cat excrement and a dead dog, along with a chorus of witches.

“We do harm to those who harm us,” she said.

“They want to take the country out of this crisis using us?

They should get us out of the crisis because they brought us into it.”

The IRS says that it’s implementing new processes that ease up on the liens it files against people who haven’t paid their federal taxes.

This includes raising the tax-debt threshold at which the agency decides to file a lien, making it easier for newly-recompliant taxpayers to have their liens lifted, and making it easier to enter into installment agreements and “offers in compromise.”

This was partially in response to complaints from the Taxpayer Advocate’s office about the agency’s heavy-handed and counterproductive enforcement methods.

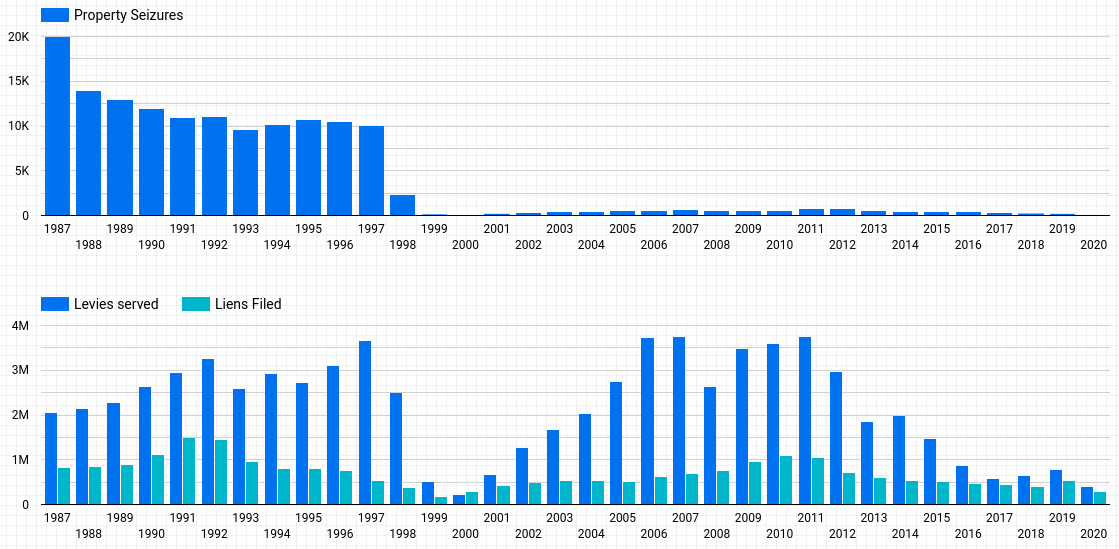

For I’ve been posting some charts that show how IRS enforcement activity is changing over time and also some charts showing how “delinquent” taxpayer activity was changing over time.

The new IRS Data Book is out, so I can update the numbers.

The number of levies and seizures are down from their peaks, but the use of liens continue to rise:

On the “delinquent” side, the number of people who didn’t pay their taxes when they were due reached a new recent-years high, though the number of people who didn’t file on time (or at all) is off from its recent peak.

The IRS continued to to be overwhelmed by the backlog of delinquent cases and so the total unresolved delinquent accounts continued to rise:

For I’ve been posting some charts that show how IRS enforcement activity is changing over time and also some charts showing how “delinquent” taxpayer activity was changing over time.

The IRS has just put out some numbers on its enforcement activity for , so I can update the numbers.

The number of levies and liens remain high, though off their peaks, while the number of seizures has risen to a recent high, though also much lower than in the bad old days:

The “delinquent” taxpayer activity charts will have to wait for their update until the IRS releases its “Data Book” later this year.

Here is how they looked as of the numbers:

The new IRS Data Book is out, with information on IRS enforcement activities in , so it’s time to update my graphs:

Here are some items of note that have come to my attention in recent weeks:

I wondered if this might happen: One of the weirder aspects of Obamacare is that the individual health insurance mandate is to be enforced by adding a penalty to the income tax of any individual who fails to get health insurance — but for public relations reasons the IRS is forbidden to use its usual methods of liens, levies, seizures, and the like to chase down this penalty if the taxpayer refuses to pay it.

So now, Obamacare foes are starting to whisper about this cheap-and-easy civil disobedience opportunity.

Though “whisper” isn’t really the right word when you’re talking about Rush Limbaugh.

Are Cryptocurrencies [like Bitcoin] “Super” Tax Havens? asks Omri Y. Marian of the University of Florida.

Marian concludes: “Significantly, cryptocurrencies possess all the traditional characteristics that tax havens do; Earnings are not subject to taxation, and taxpayers’ anonymity is maintained.… Thus, cryptocurrencies have the potential of defeating the recent successes of governments in battling offshore tax evasion.… while governments have paid some attention to this issue, they have so far failed to identify the acuteness of the potential problem.”

Among the things the so-called government “shutdown” brought us was a halt in almost all IRS levies and liens for the duration.

The agency had plenty on its plate before the shutdown, and now it’s already behind in regearing for tax season.

France enacted a populist measure to throw a 75% marginal tax on incomes above €1 million.

Professional soccer teams, whose players may earn large annual incomes but usually over a short viable career, have decided to protest by going on temporary strike, effectively eliminating a round of matches this year — the first time teams have done anything of this sort .

The National Taxpayer Advocate released its 2013 Annual Report to Congress today, in a flashier and more public-facing package than I remember it using in the past.

The report identifies how funding cuts, increased responsibility, and Congressional hostility to the agency have put the IRS in something of a crisis state:

Throughout the Most Serious Problems section of this report, we recount the ways in which chronic underfunding drives the agency to develop short-term solutions that merely patch over problems and impose unnecessary burden and even harm on taxpayers.

These short-term solutions also create more work for the IRS in the end…

Agency budget woes are a theme that runs through the document, and this is highlighted as its own “Most Serious Problem” — “The IRS Desperately Needs More Funding to Serve [sic] Taxpayers and Increase Voluntary [sic] Compliance.”

That problem statement describes the funding crunch this way: “Since , the IRS budget has been cut by nearly eight percent.

Over the same period, inflation has risen by about six percent, further eroding the IRS’s resources.”

Meanwhile: “the workload of the IRS has increased significantly.”

This has led the agency to cut way back in what it calls taxpayer service (responding to phone calls and letters, providing walk-in consultation, answering questions about tax laws and regulations).

It has reduced its staff by 8% in recent years (including 12% and 21% reductions in its number of Revenue Agents and Revenue Officers respectively), and slashed its training budget by 87%.

The Taxpayer Advocate notes that this is likely to lead to reduced tax collection, and that this will largely be not because a lack of enforcement personnel means that more tax evaders will get through the net, but because poor “customer service” and increasing IRS clumsiness will make the mass of compliant taxpayers more cynical about taxpaying and more likely to try to get away with something.

Some preliminary numbers on liens and levies are embedded in the report, so I can update my charts:

The IRS released its Enforcement and “Service” Results, which have more and more-precise numbers than those I noted .

Here are the charts on property seizures, levies, and liens:

There’s a new IRS DataBook out, so I’ve updated my charts with numbers for :

There’s a new IRS DataBook out, so I’ve updated my charts with numbers for :

If the IRS is after you for back taxes and they haven’t been able to convince you to write them a check, the next thing they’ll do is to try to find easy-to-seize assets: bank accounts and things of that sort.

Social Security benefits are one easy-to-seize asset. After all, the government

is writing the check in the first place.

There are two ways the government goes about seizing Social Security benefits: via the Federal Payment Levy Program (FPLP) and by Field Collection.

FPLP

is more automated, but also more limited. Through this program, the

IRS can

seize no more than 15% of your Social Security benefits continuously until your

back taxes are paid off. However, by policy, the agency will not levy your

Social Security benefits by means of the

FPLP

if your estimated income is below 250% of the poverty line.

Field Collection is less-limited.

If your case is turned over to Field Collection, the agent assigned to your case may seize however much they think is appropriate — as much as 100%.

However, Field Collection is also less-automated: It requires a revenue officer to examine your case and your circumstances and make a judgment call.

The IRS’s budget has been reduced in recent years, which has affected the number of cases it can work.

In an press article, an IRS manager stated that, due to resource constraints, revenue officers are only assigned very high-dollar balance due accounts.

While the IRS later clarified that its collection actions are not limited to high dollar accounts because it has a variety of collection tools available, it did not clarify that revenue officers continue to work a full range of balance due cases.

That quote comes from a new TIGTA report on Social Security levies.

The Washington Post article it refers to quoted an IRS Field Collection supervisor as saying that only if a person’s back taxes exceeded $1 million would a revenue officer be assigned to the case.

It also quoted the IRS’s non-denial denial of this. (In TIGTA’s own investigation of a random sample of 136 cases where Social Security benefits were levied by Field Collection, however, it found the median balance due to be $83,226, with a back taxes range from hundreds to millions of dollars.)

Anecdotal reports from within the American war tax resistance community

suggest that Social Security levies are done inconsistently and haphazardly,

and the TIGTA report

bears that out, noting that different Field Collection group managers had very

different policies, and different ideas of what the goals of Social Security

benefits seizures were. Some indicated that they had set policies that, on

further inspection, were not actually being carried out by the revenue officers

in their groups.

Field Collection agents were sometimes assigned cases that were already being collected via FPLP, and in most of these cases, they canceled the FPLP and issued a manual levy for a higher amount.

Sometimes they did this even though they had reason to believe that this would cause economic hardship.

They also felt no reason to respect the 250%-of-poverty-line cut-off that the FPLP program uses.

Although Field Collection agents can decide they want to take as much as 100%

of your Social Security benefits to pay back taxes, you have the right to a

partial exemption, based on

your age, filing status, number of dependents, and other sources of income,

so that they leave you enough to live on. In practice, the audit found, the

IRS was

frequently failing to give people these exemptions they were entitled to, or

to let them know they were entitled to them.

My take-away from this is that if you find that your Social Security benefits are being seized for back taxes, it may well be worth your while to research the laws and policies the IRS is supposed to be following in such cases and then to raise a fuss if they are screwing up.

If you have a low income, mostly from Social Security, you can likely get most of it exempted from the levy, but the agent on your case may not know this or may be hoping you don’t figure it out.

There’s a new IRS DataBook out, so I’ve updated my charts with numbers for :

There’s a new IRS DataBook out, so I’ve updated my charts of IRS enforcement activity with numbers for :

There’s also a new IRS Data Book out, so I can update these numbers on enforcement activity:

In other news:

One of the tools the

IRS

uses against tax scofflaws like myself is to file a federal tax lien in the

local court system of the scofflaw. This puts creditors and the local legal

system on notice that the

IRS

intends to step in and assert its rights to seize money. This can make it

difficult to get credit, and also makes it easier for the feds to seize

anything awarded by the courts in lawsuits, probate resolution,

etc. However

(and this is where it gets interesting and newsworthy), filing a lien costs

money. And the

IRS

thinks several California counties are charging them too much, and so they

have started to refuse to pay. In response, some counties are refusing to

process the

IRS

liens. Alas, this filing fee, and the standoff between the bureaucracies,

also applies to paperwork to release a previously-filed lien. So

this doesn’t always work in the scofflaw’s favor. Here’s some news

coverage:

War tax resister Larry Bassett was interviewed on the Parallax Views podcast.

Bassett is the subject of the recent documentary film

The Pacifist and is responsible for the largest

known individual act of war tax resistance, in terms of the amount of

dollars resisted at once.

Another Treasury Inspector General for Tax Administration report points out

that reduced IRS

resources means collapsing tax enforcement capability.

“As more taxpayers experience little to no consequences for non-filing, the

long-term impacts may include potential erosion of the voluntary compliance

rate.”

The IRS

issued an update to its estimate of the “tax gap” (the difference between how much tax people are supposed to pay and how much they do pay).

The upshot is that they think little has changed: people pay about 84% of

what the agency believes they owe. However, the last time I looked at the

details of one of these “tax gap”

reports, I noticed a lot of hand-waving, guesswork, and extrapolation, and

only a little empirical data collection, so I would recommend taking these

numbers with a grain of salt.

More attacks on traffic ticket issuing radar cameras — in France & Italy; Mexico, Germany, and France; and France again.

Revenue from the cameras is only half of what the government had hoped for

and budgeted for in France this year, and the government has had to divert

some of that money to installing more heavily-fortified cameras.

The National War Tax Resistance Coordinating Committee is holding a national conference and committee meeting in Oregon.

This meeting will include a special focus on cooperation between the war tax resistance movement and climate/environmental activism.

He put in a kind word for war tax resisters:

“If a cellphone, burger, or cup of coffee isn’t worth the price to me, I can choose not to buy it.

Were you ever given an ‘unsubscribe’ option from American Empire?

If I want to stop paying to subsidize the brutal Saudi war in Yemen for instance I have very few options.

There is of course a noble tradition of war tax resistance in the United States, with Henry David Thoreau refusing to pay poll taxes that he believed funded the Mexican-American War and Noam Chomsky and others resisting taxes during the Vietnam War, but tax resisters face repression, they risk incarceration, they risk garnishing of their wages, they risk having their property seized, and even moving out of the United States isn’t enough to avoid paying for American Empire:

When you criticize U.S. foreign policy you might get told ‘hey if you don’t like it you can leave’ — well even if you leave you still are seen as owing taxes to the U.S. government unless you go through a costly process of renouncing your citizenship.

And that’s ignoring that there are also funds gained through inflation, through the printing of money, that’s a tax on everyone who holds U.S. dollars…”

I noticed a campaign calling itself “Tax Resistance” suddenly appear on-line.

It has appropriated photos from the U.S. war tax resistance movement, but it seems to be directed at potential war tax resisters in the U.K.

Its Twitter account was suspended before I could even take a look at it.

Its Facebook page is spare and generic.

There’s no indication who’s behind it.

I’ve got a suspicious eyebrow raised, but will keep my eyes on it.

Attacks by motorists on traffic ticket machines continue worldwide.

Some recent examples:

Remember Ed & Elaine Brown?

The “show me the law”-style tax protesters who became causes célèbres in constitutionalist/sovereign-citizen circles?

They were arrested after a long siege of their New Hampshire home about a decade ago and given lengthy — essentially life — prison terms.

But one of the major charges against them was based on a law that was declared to be unconstitutionally vague in an unrelated Supreme Court case, and so now the Browns will be resentenced and may soon be released as a result.

The government of Ontario is protesting the Canadian federal government’s carbon taxes by mandating that gas stations put stickers on the pumps that point out how carbon taxes are rising and contributing to the price of gasoline.

Ontario is also spending millions of dollars on legal battles opposing the tax.

There’s a new IRS Data Book out, so I can update these numbers on enforcement activity:

ProPublica looks at the numbers this year — including $6.7 billion in tax debt that the IRS let the ten-year statute of limitations expire on without collecting — and asks “Has the IRS Hit Rock Bottom?”

I’m guessing not.

I’m really looking forward to seeing next year’s numbers.

Some recent links of note:

The IRS has announced that not only will it issue stimulus payments and Paycheck Protection Program loans to people and businesses even if those people or businesses are behind on their taxes, but also that the agency will not levy bank accounts into which those payments are deposited — for 24 weeks in the case of PPP loans, or 8 weeks in the case of stimulus payments.

Current IRS policy says that agents should contact taxpayers before issuing a levy to ask whether the account in question recently received such a payment.

If so, they are supposed to refrain from levying until the proper number of weeks have passed.

If the IRS tries to levy a bank account in which you have recently deposited such a check, you can protest this and the IRS is supposed to release the levy.

In either case, this should give you plenty of time to empty out the account so that a future levy attempt will fail.

I fear that waiting out the ten year statute of limitations on collections is becoming a reasonable strategy and that many “taxpayers” have caught on and that the IRS, when it comes to collection, is to a significant degree bluffing.

My overall takeaway from the [recent Treasury Inspector General for Tax Administration] report is that the IRS has a lot of outstanding receivables that it does nothing about.

That made me want to look more closely at the numbers.

Working with the spreadsheets is a little frustrating.

They don’t answer all the questions I would like answered, but it does give a pretty clear idea that the IRS is something of a shadow of its former self.

At , the balance of assessed tax, penalties and interest (ATPI) was $114.2 billion spread among 10.4 million accounts.

In that year IRS filed 1,096,376 notices of federal tax lien and requested 3,606,818 levies on third party.

IRS wrote off $14.6 billion that had expired due to the ten year statute.

At ATPI was $125.8 billion spread among 11.2 million accounts.

There were 543,604 liens and 782,735 levies.

$34.2 billion expired due to the ten year statute.

It is important to remember that when we are talking about collections, we are talking about tax that has already been assessed.

This has nothing to do with people who have not filed or who underreported income and have not gotten caught.

That is an entirely different kettle of fish.

Through my decades of tax practice, the notion of flat out not paying assessed tax was not something that was in my bag of tricks.

It has slowly dawned on me that this is a thing.

A tax strike by restaurants and bars in Italy has begun.

The strike is being organized by Movimento Imprese Ospitalità, which is a project of the tourist industry branch of the General Confederation of Italian Industry.

It is protesting continued tax collection at a time of collapsing business during the Covid pandemic.

I’ve seen a few more articles that give some additional details about the latest tax strike in South Kivu:

The campaigns have been organized and led by what are vaguely referred to as “la société civile” (civil society).

This refers to some sort of preexisting groups, but I don’t really understand what they are.

They seem to be non-governmental organizations that sometimes behave as parallel governments or service providers, other times as sorts of citizens’ unions or chambers of commerce.

Guillermo Incer Medina, in Confidencial, evaluates the tactics used by the protesters in Nicaragua who have been struggling with the Ortega regime.

He concludes that the best high-impact, low-risk action would be tax resistance from a small number of large-scale taxpayers.

Excerpt:

In Nicaragua, 94% of the total tax collection comes from large taxpayers (a large taxpayer is a company that has large volumes of transactions and, therefore, that collects taxes such as VAT, IR — and others– in large amounts.

Examples of these could be supermarket chains, large importers, large commercial establishments, or large agro-industrial consortia).

In our country, the sectors with the largest taxpayers are industry, commerce, finance, transportation, and services.

In these sectors, large taxpayers collect more than 90% of the total taxes of their respective sector (which is to say that of every 100 córdobas that is collected from taxes in each sector, 90 córdobas are contributed by large taxpayers and only 10 córdobas by mid-sized and small ones).

Furthermore, in areas such as liquors, beers, soft drinks, and fuel, the large taxpayers collect 100% of the total taxes.

Why is this important?

Because the dictatorship needs taxes to maintain its repressive apparatus and its patronage politics.

If you take the oxygen out of their horror machine and purchase of consciences, you take away their room for maneuver.

“Let’s do a consumer strike!” said COSEP and AMCHAM representatives every time we demanded a national strike.

This is a mistake for two reasons: 1) for a consumer strike to have a real and not symbolic effect, requires that millions of unorganized Nicaraguans, including pro-government people, decide to deprive themselves of consuming goods that are difficult for them to obtain due to the precarious living conditions in which we live, 2) it is useless for us to stop consuming (not paying VAT) if companies still pay the State taxes such as IR and others (one must keep in mind that those who directly “deliver” taxes to the State are not we the consumers, but they are the collectors — the companies).

What can one do then?

The action that could have the greatest impact at the lowest cost and in the shortest term is tax resistance from the large taxpayers, which is nothing more than the large companies stopping payment of taxes to the dictatorship for a period long enough to oblige them to make concessions for his departure.

“They are going to close us down!”, the big businesses say immediately.

But it is not likely that the government will close large companies due to how this would look to foreign investment, and due to the political cost of sending thousands of people into the streets.

Furthermore, if they close large companies, this would in practice have the same effect as tax resistance, since they would stop receiving their taxes.

“We are exposing thousands to unemployment!”, they also say… more jobs are being jeopardized by letting this political and humanitarian crisis drag on and by the coming interruption of CAFTA and ADA, if the dictatorship continues to do what it wants and stays five more years.

“It’s too risky!”

It is more risky to put your body on the line in a march or a roadblock, or to go on a hunger strike in a church and get shot, cut off your services, and imprison those who want to help you.

There is no large, medium, or small company that is worth more than a human life.

Tax resistance is more feasible than other actions of high-risk and low-impact (such as a chain of express pickets or coordinated sit-ins) because it does not require the coordination of thousands of unorganized people.

To promote tax resistance, it is enough that a few of the largest companies, which are already organized in chambers, agree, stand firm, and coordinate among themselves.

Gig workers in Serbia used to be more or less income-tax free, apparently.

Not any more. A new law not only makes them liable for income tax, but requires them to cough up taxes for the last five years.

Marchers in Belgrade protested the new tax law.

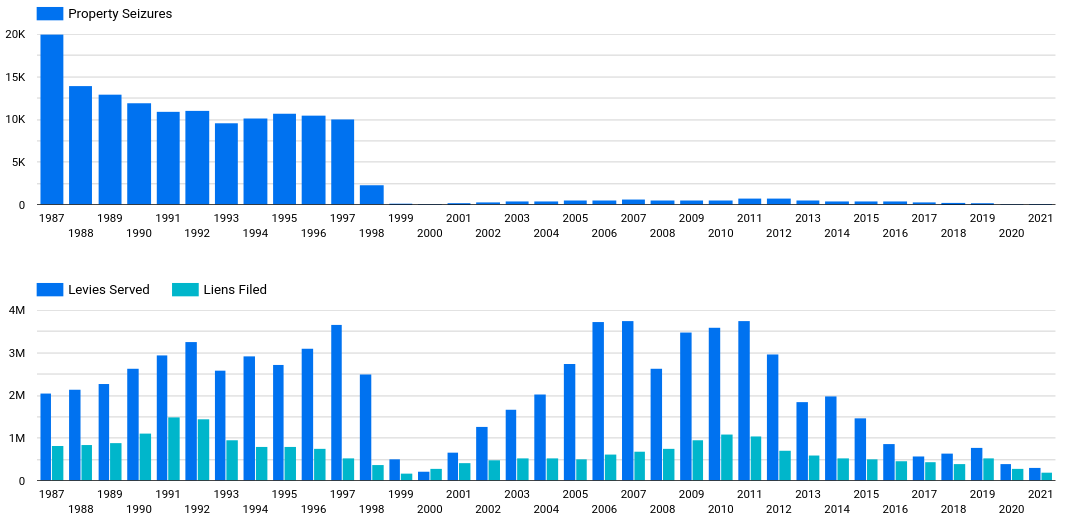

The IRS just released its latest Data Book, which gives us some statistics about another tax season.

This means I can update my charts of how IRS enforcement activity — specifically liens, levies, and property seizures — has been changing over the years.

In short, all three are at twenty-year lows:

In recent years, something in the neighborhood of 40–45% of American households have not owed any federal income tax.

This is due to a combination of factors including progressive tax rates and tax deductions & credits that shield a certain amount of income from tax.

Although fabulously wealthy people who do not pay income tax are certainly a thing, most of this group of “lucky duckies” come from the bottom half of the income scale.

In , with its pandemic-related economic disruption and the stimulus payments that took the form of refundable tax credits, the numbers jumped: the Tax Policy Center estimates that 61% of U.S. households paid no federal income tax .

Under a newish law the U.S. government will be issuing advance “Child Tax Credits” to qualifying families with children as checks periodically throughout the year.

These checks take the place of the refundable tax credit that such families would have used to offset their federal taxes at annual tax filing time in past years.

Interestingly, the IRS has directed its enforcement personnel to avoid seizing money from bank accounts in which these Child Tax Credits have been direct-deposited and to refund any inadvertently seized Child Tax Credits.

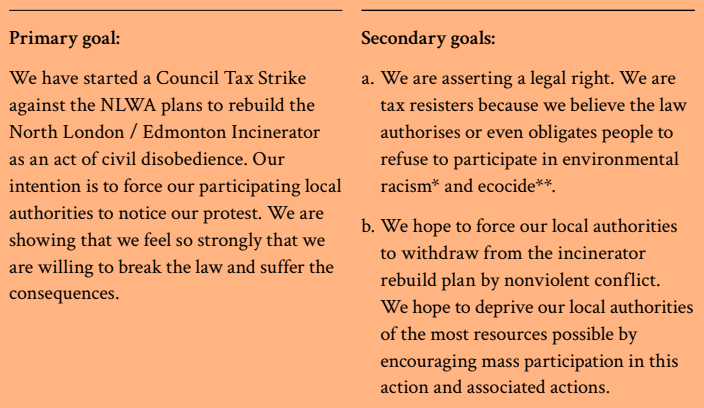

“Council Tax Strike” is a subproject of the Extinction Rebellion movement in the U.K. They claim: “There are people all over the U.K. withholding their council tax and demanding action on the things that matter to them.”

The National Catholic Reporter looks back on the nuclear disarmament activism of Archbishop Raymond Hunthausen:

“ ‘I think the teaching of Jesus tells us to render to a nuclear-armed Caesar what that Caesar deserves — tax resistance.

And to begin to render to God alone that complete trust which we now give, through our tax dollars, to a demonic form of power,’ he said in his ‘Faith and Disarmament’ speech.

‘Some would call what I am urging “civil disobedience.”

I prefer to see it as obedience to God.’ ”

IRS Circumvents “Statute of Limitations” by Ruth Benn.

Normally, the IRS has ten years to collect unpaid taxes from you before they have to give up.

Also, normally, if you decide to voluntarily pay your taxes, you can also decide for which tax year you are paying them, and by IRS policy, they’ll respect that.

Ruth Benn’s tax resistance takes the form of refusing to pay her income tax, but voluntarily paying her self-employment tax.

As the ten year statute of limitations approached on one of her unpaid years of income tax, the IRS tried to pull a fast one and used some sleight-of-hand to apply the money Benn was paying for the current year’s self-employment tax to the expiring year’s income tax amount.

She is hoping to get the agency to change its mind and to respect its own policy, and promises to keep us up to date on how the red tape tangles.

Counseling Notes.

Including a reminder that Social Security levies can continue past the ten-year statute of limitations date because the levy is considered “continuous” when it is first applied (not reapplied with each new Social Security check).

Democrats are keen to force banks to report how much their customers have put into and taken out of their accounts each year.

They hope this will bring to the surface some of the money in the underground economy that the government has been frustrated when trying to tax.

This proposal has gotten a lot of pushback, and has been an on-again / off-again part of the budget package currently oozing through Congress.

The latest guesswork suggests that the Democrats may reactivate the proposal but restrict it to accounts with $10,000 or more in them.

There’s a nice website that’s been established by the caretakers of The Nelson Homestead — the modest home of war tax resisters Juanita & Wally Nelson in Deerfield, Massachusetts.

It has good recaps of the lives and activism of the Nelsons, including photos.

The Biafra Nations League, which is trying to establish a break-away nation more representative of the Igbo people, has issued an ultimatum to oil firms in the area, ordering them to stop paying taxes to Cameroon and Nigeria, which currently claim sovereignty over the region.

Argentina legalized abortion .

Now a group of Argentine legislators have proposed a law that would permit a sort of conscientious objection to taxpayer-involvement in abortion, of a similar sort to what is proposed in the “Religious Freedom Peace Tax Fund Act” in the U.S.

The human war on traffic ticket robots continues, with robots taken out of service by human rebels in the U.S., Italy, France, and Germany & France in recent weeks.

Democrats in Congress are having more trouble than expected getting everyone in and out of the clown car.

The upshot is that the painstakingly-negotiated “Build Back Better Act” is in jeopardy — along with the $80 billion in new IRS funding that was part of the bill.

was surely the most challenging year taxpayers and tax professionals have ever experienced — long processing and refund delays, difficulty reaching the IRS by phone, correspondence that went unprocessed for many months, collection notices issued while taxpayer correspondence was awaiting processing, limited or no information on the Where’s My Refund? tool for delayed returns, and — for full disclosure — difficulty obtaining timely assistance from TAS.

, examination coverage has decreased, enforcement efforts have been negatively impacted, and the Level of Service has continued to drop as the IRS’s workforce and budget have declined.

On the resources side, the IRS’s baseline budget has been reduced by about 20 percent on an inflation-adjusted basis , and its workforce has shrunk by about 17 percent.

There is no way to sugarcoat in tax administration: From the perspective of tens of millions of taxpayers, it was horrendous.

[T]he number of individual income tax returns the IRS receives — a reasonable approximation of its workload — has increased by 19 percent , while its baseline appropriation on an inflation-adjusted basis has decreased by nearly 20 percent.

This imbalance has left the IRS without enough resources to meet taxpayer needs, let alone to invest in additional personnel and technology.

The IRS has not finished processing millions of original and amended returns from , even though returns will soon arrive for processing.

According to the Department of the Treasury, the gross tax gap — the difference between taxes paid and taxes owed — is estimated to have totaled about $580 billion in , up from an estimated amount of nearly $440 billion in , and is expected to rise to about $7 trillion by if left unaddressed.

Processing a paper-filed return is significantly more expensive for the IRS than processing an e-filed return due to the costs associated with training, recruiting, and staffing for manual data transcription.

In fact, the cost to process a paper-filed Form 1040 in was $15.21, which is substantially higher than the $0.36 cost to process an e-filed return.

The report also included some totals for levies, liens, and seizures, so I can update these graphs:

More excitement from the human war on traffic ticket robot cameras, as fire, spray paint, and other sorts of sabotage knocked cameras out of commission in France, Germany, and Italy in recent weeks.

There’s a new IRS Data Book out, so I can update these numbers on enforcement activity: