Tax resistance in the “Peace Churches” →

A New Call to Peacemaking

Here’s an AP dispatch

that I found in the

Free Lance-Star of Fredericksburg, Virginia:

Protestant groups eye war-tax resistance

New York (AP) —

Three Protestant denominations opposed to war are considering a new kind of

tax resistance — refusal to pay taxes that go for arms and equipment for

war.

Following a year-long series of joint regional conferences under the banner

of a “New Call to Peacemaking,” the three historic “peace” churches have set

a national conference about it

in Greenlake, Wis.

The meeting is to consider regional proposals for some form of tax protest

against spending for armaments and munitions of war.

The denominations, whose hallmark for centuries has been conscientious

objection to participation in violence and war, are all relatively small. But

they’ve had an influential impact on Christianity at large and on American

thought.

They are the Society of Friends, involving about 100,000 Quakers; the Church

of the Brethren, a Midwest-based denomination with about 180,000 members,

and the Menonites, totaling about 130,000

Although many of them have protested war in the past by refusing to accept

military service, the nature of modern war has turned “from manpower to

money for technology and automated weapons,” the churches said.

In a joint statement, they said members of the movement now are “poised

for stronger action.”

“The time has come for all Christians and people of all faiths to renounce

war on religious and moral grounds,” the new cooperative coalition of peace

churches said in its new call.

Regional meetings at 26 locations have been held in the last year about the

issue, with more than 1,500 persons taking part, citing war and violence as

“denials of the life and teachings of Jesus Christ.”

At one of the conferences at Old Chatham,

N.Y.,

, it raised this question: “Are we

going to pray for peace, and pay for war?” Another in Wichita,

Kan., declared that 50 percent

of funds collected from income taxes are used for military-related purposes

and for manufacture of destructive weapons. The meeting encouraged

“individuals who feel called to resist the payment of the military portion of

their federal taxes.”

A meeting in North Manchester,

Ind., proposed making use of

the current tax revolt highlighted by California’s Proposition 13 and the

distress at the national debt and inflation to further the peace cause.

The Indiana meeting suggested “legislative approaches that attract”

the concerns of millions. The meeting urged an annual 5 percent decrease in

military spending until it is cut 25 percent.

“The supposition that arms provide security is an illusion,” say the

planners of the October conference in their letter of invitation.

“We call for a world based on peaceful order rather than the ‘balance

of terror’ fueled by nuclear arsenals and the spreading arms sales.”

I shared an Associated Press dispatch from

about a then-upcoming meeting of Quakers,

Brethren, and Mennonites who were planning to coordinate war tax resistance.

Today, an article reporting on how the conference went, from the

Milwaukee Sentinel:

Sects Urge Tax Protest for Peace

Green Lake,

Wis. — A national

meeting of “historic peace churches” — Quakers, Mennonites and Brethren — agreed to support those who refuse

to pay “the military portion” of their federal taxes.

The possibly illegal “war tax resistance” position is a giant step for many

in the churches from the passive refusal to bear arms and turning the other

cheek.

Statements such as “we are praying for peace but paying for war” prodded the

more than 300 delegates at a New Call to Peacemaking conference to back what

advocates called an economic moral equivalent to military conscientious

objection.

The lengthy statement also urged total disarmament after arms reduction,

formation of a peace church delegation to President Carter, establishment

of a world peace tax fund and simpler lifestyles.

It is not binding on the 350,000 members of the churches in the

US or the nearly

one million members worldwide.

The four day conference at the American Baptist Assembly here followed 26

regional meetings with participation by more than 1,500 Quakers, Mennonites

and Brethren.

The joint meetings in themselves were a new ecumenical venture in breaking

stereotypes. It was the first time in recent years representatives of the

churches had met in such a conference.

The national conference challenged congregations and church agencies to

consider refusing to pay the military portion of their federal taxes,

generally thought to be about half, as a response to Christ’s call to

radical discipleship.

It also asked them to “uphold war tax resistors with spiritual, emotional,

legal and material support,” and to consider requests of employees who ask

that their taxes not be withheld.

The 8 August 1981 Nashua Telegraph carried an article by Associated Press “Religion Writer” George W. Cornell.

Some excerpts:

A-bomb anniversary brings peaceful fight

New York (AP) —

In a time of military buildup, the “peace” people are marching, praying, fasting and signing petitions.

Several denominations have made “peacemaking” a current priority.

And some church leaders, including a bold bishop, have advised refusing to pay the portion of taxes that goes for arms.

[A]dvocacy of withholding so-called “war taxes” — the share of federal income taxes that go for military equipment — came not just from traditional “peace” denominations, but from a Roman Catholic archbishop.

Archbishop Raymond G. Hunthausen of Seattle, in a speech that has since evoked wide and varying reactions, suggested Christians refuse to pay the half of their federal income taxes going for armament.

“We have to refuse to give our incense — in our day, tax dollars — to the nuclear idol,” he said.

“I think the teaching of Jesus tells us to render to a nuclear-arms Caesar what Caesar deserves — tax resistance.

“Some would call what I am urging ‘civil disobedience.’

I prefer to see it as obedience to God.”

Similar suggestions have come from some other Christians, most solidly from leaders of three relatively small, but historic “peace” denominations — The Church of the Brethren, the Friends and Mennonites.

A joint meeting of them under the banner of “New Call to Peacemaking” said paying for war is wrong and asked members to “consider refusal to pay the military portion of their federal taxes, as a response to Christ’s call to radical discipleship.”

In separate denominational actions, the Church of the Brethren has supported “open, massive withholding of war taxes” and the Mennonites general conference is fighting in court against being required to withhold taxes partly used for military purposes from employes’ income.

The New York-based War Resisters League estimates 2,000 to 10,000 Americans annually hold back part of their taxes, some eventually being forced to pay but continuing to repeat the protest.

War tax resistance in the Friends Journal in

There was hardly an issue of the Friends Journal in that did not at least mention war tax resistance, and some issues covered the topic in depth.

In the issue was an article by Scott Benarde about the Quaker community of Monteverde in Costa Rica.

Excerpts:

In , a year after the sentencing [of Marvin Rockwell for draft resistance], Rockwell and the small Quaker community of Fairhope made national news.

In a short article, Time magazine mentioned that “for the first time in history a group of Quakers were planning to leave the U.S. because of their peace-loving convictions.”

Seven Quaker families — including Marvin Rockwell and his parents — twenty-five or thirty people in all, had decided to move to the Central American Republic of Costa Rica.

, Marvin Rockwell recounts why he left the U.S. and what has happened to him since settling 5,000 feet up in the steep, rugged mountains of Costa Rica.

“We had a growing dissatisfaction with what we in Fairhope thought was a military build-up, a wartime economy.

We wanted to be free of paying taxes in a war economy,” Rockwell says in a soft, yet deliberate, voice.

“When the judge sentenced us he said, ‘If you’re not willing to defend your country, you should get out.’

So we began to think seriously of that possibility.”

That issue also brought the news that Quaker Richard Catlett “has been indicted on criminal charges of willful failure to pay income tax for three years” (the indictment was actually for failure to file).

The issue — under the theme “Can the Government Cancel Conscience?”

— had many mentions of war tax resistance.

The opening article, by Ruth Kilpack, began:

Ten years ago, at the height of the Vietnam War, a Friend spoke directly to my condition at Philadelphia Yearly Meeting when he said, “Many of us support our sons’ conscientious objection to serving in the armed forces.

But what about ourselves?

Do those of us who are beyond draft age, or not otherwise subject to the draft, conscientiously object to giving our money for war?”

For me, this struck deep, as did the words, “Two things are needed to fight a war: warm bodies and cold cash.”

For the first, the full flush of youth is required for combat.

For the second, there is no age limit for those who must pay tax funds, over half of which are channeled directly into wars, past, present, and future.

Everyone is involved.

By the payment of taxes, all are required to support the “national defense,” or whatever the current euphemism is.

Kilpack’s article concerned the legal case of Robert Anthony, who was appealing his tax case on religious freedom grounds.

What Bob Anthony’s case was about that day was an effort to break the longstanding precedent set by the case of A.J. Muste, the great peace activist, who in had challenged the U.S. government in the matter of paying taxes for war.

The court had then ruled that the income tax does not interfere with religious practice.

Whatever attempts have been made since that time to break that precedent-and there have been many-have been thwarted, federal judges repeatedly refusing to examine the deep issues involved: the issues of rights of conscience and the First Amendment’s protection of religious belief.

As it turned out, according to Anthony, “the court came up with a complete backing of the government’s right to cancel conscience for the sake of the taxing system.”

The same issue reprinted excerpts from a letter that Media Monthly Meeting had sent to the court that was hearing the Anthony case, in which it said:

As a Meeting, we have consistently backed and encouraged [Anthony’s] position on military taxes.

We believe that any citizen who on the basis of religion or conscience is opposed to paying for armaments or war should not be compelled by the tax laws to pay taxes for these purposes.

Refusal to participate in any way in killing and warfare is a basic principle of the Quaker faith.

…Robert Anthony’s refusal of military taxes constitutes an essential and consistent implementation of Quaker religious principles.… We assert that the free exercise of the Quaker religion entails the avoidance of any participation in war or financial contribution to that part of the national budget used by the military.

In the same issue, Bruce & Ruth Graves wrote of how their war tax resistance had grown out of their conscientious objection to the draft.

[O]ur early married years were largely those of family and professions, years in which we were no longer pressured by government to form external written attestations of belief to satisfy the draft board.

After all, we had done that.

What else could just we two do to alter this evil?

The pacifist ideas could safely rest — or could they?

In retrospect, those beliefs that had been yanked forth from us by society, perhaps too early in our lives, needed more time to mature, to become integrated into our very beings.

Perhaps ten years of integration preceded our realization that a different and subtler written attestation of belief was being required of us by our society.

This attestation was made not once, but every year and it was an attestation of beliefs we did not believe.

It was a lie.

It was our income tax return.

We signed it every year, and thus gave money, without objection, to buy the tools of war, even though we did not believe in killing.

It was subtle because it was money and did not look like death.

But when you put them together, it is a contract.

…All of this occurred during a time when militarism increasingly permeated national policy.

Here, then, we finally reached a point where the idea of our financing the arms race became unbearable.

After all, warfare was becoming more automated, thus relying far more on the expenditure of tax money than on the conscription of lives.

In fact, it now appears that conscientious objection itself may be tending toward irrelevance, unless the concept is expanded beyond the confines of the Selective Service system — especially for those over draft age.

At this point we changed our tax returns into something we could in conscience sign and our remittance checks into contracts for the Internal Revenue Service.

Each year, the item “Foreign Tax Credit” and about fifty percent of our normal tax “due” was entered.

Carrying that credit over to the first page as instructed, we showed each year on our signed returns a credit balance due us from the IRS.

To reduce IRS profit from interest and penalty, we still paid tax “owed” as calculated normally, but our check required the IRS to promise to refund the war tax we claimed by their endorsement because of a restrictive clause we placed on the back of the check.

Rather than our refund, the IRS has usually sent a notice for us to sign, correcting our return.

We have never signed these, because that means agreeing to the original war tax.

Yet the IRS seems to need our agreement to resolve each case legally — that is, unless it should decide to initiate proceedings against us in U.S. Tax Court.

That, in fact, happened to us in for tax year .

From here, the Graveses write about their frustrations with the legal system, which seems eager to latch onto superficial technicalities to avoid having to face head-on the issue of whether the government can force people to violate such core tenets of conscience as “thou shalt not kill” via the tax system.

They also express the need they feel for a stronger and more sustaining national war tax resistance organization:

At present, the community of war tax resistance appears to us to be a loosely-structured communications network of interpersonal contacts, newsletters, and small organizations perhaps not always widely known.

Entrance to this network, we presume, is often gained through need for help by individuals who then grow, gain experience, and are later able to help other newcomers in their various situations.

Whether they do help others or just gradually fade out of the network, however, is crucial to the power of the community.

If we, ourselves, were to fade out as our own tax problems become less immediate, for example, the experience and knowledge we will have gained (even though far from complete) would be lost to the others.

It would seem to be a sad waste to have this process repeated over and again for each member passing through the community.

There are a few organizations emphasizing war tax resistance (e.g., WTR, Peacemakers, etc.), from which a range of handbooks and information is available for individual action.

Some may provide counseling: for example, we have recently learned that CCCO is in liaison currently with the Philadelphia Office of War Tax Resistance (WTR), thus affording the wider range of counseling needed by this more recent form of conscientious objection.

They added:

There are other courses of individual action besides variations on how to fill out a tax return.

One such course is to reduce one’s income to a level of lower — or no — taxation.

For some, this would mean a change in profession, or else a donation of one’s professional services to his or her current employer.

If it is not desirable to put that kind of commitment into that particular employer’s pockets, one can give away up to fifty percent of taxable income to tax deductible organizations, thereby reaching three simultaneous objectives: a) continue one’s profession, b) support human interests of choice, and c) decrease war tax payments.

Tax liability on interest income can also be reduced by buying tax-exempt bonds or shares in exempt bond funds.

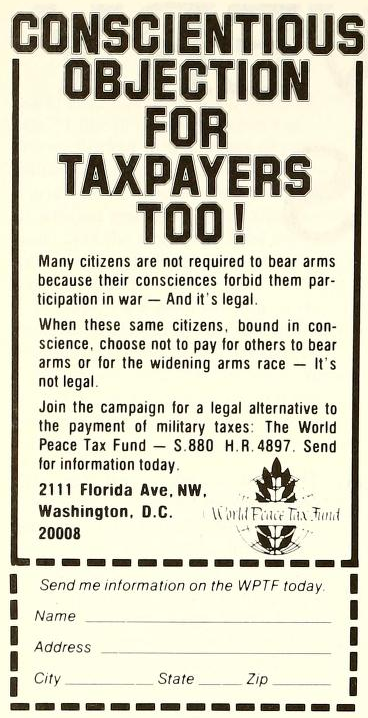

Both Individual Retirement Accounts and Deferred Tax Annuities (sometimes available through the employer) enable the postponement of income to retirement years, when, hopefully, the World Peace Tax Fund Act will have become law.

This provides a reasonable chance for legally claiming the exemption on a part of current income, the exempted funds then being redirected to the WPTF Trust Fund for uses more closely aligned with human values.

Also in that issue was an update on the Richard Catlett case, in which he was charged with “willfully and knowingly failing to file income tax returns for ” — he in fact hadn’t filed .

The Brandywine Peace Community wrote in with “some fundamental questions of reality and responsibility” for Quaker taxpayers.

The community ran an alternative fund “comprised of refused war taxes, personal savings, and group deposits, [that] makes interest-free loans to groups working for social change or providing change-oriented services.

Thus, the alternative fund is a small-scale act of beating swords into plowshares and initiating our own peace conversion program.”

Also:

In past January–April tax seasons, the Brandywine group and its supporters have been present at local IRS offices, presenting the option of war tax resistance, and posing the question, “H-bombs or Bread?” with peace tax counseling available.

The issue shared the story of John and Louise Runnings, who…

…have withheld payment of their income taxes in order, as they state, “to resolve the conflict between the spirit that dwells within and the violence implicit in surrendering our substance to the building of the war machine.”

They have submitted a brief to this effect to the Ninth Circuit Court of Appeals.

The Runnings feel that since their action makes them answerable to “those Quakers whose light allows them to pay the federal tax,” they must plead their case before the Society of Friends as well as before the Federal Court.

In doing so, they stress the fact that they share Friends’ testimonies against war but feel that these testimonies will be muted if they are not supported by actions which speak louder than words.

They question how we can “speak truth to power” when so large a part of our income supports that power.

They invite Friends to join them “in taking those uncomfortable actions which put us in conflict with the government rather than with the Spirit.”

That issue also brought the update that Robert Anthony’s appeal to the U.S. Third Circuit Court of Appeals had been rejected.

It also noted that, according to the Albuquerque Monthly Meeting’s newsletter, the Philadelphia Yearly Meeting and the AFSC were contributing to the legal expenses in the case.

At the Philadelphia Yearly Meeting, according to the Journal, “[a] minute on nonpayment of taxes for military purposes was adopted” — but not one that required much explanation, apparently.

A letter from Austin Wattles appeared in the issue in which he encouraged the Journal to continue to cover war tax resistance, saying that to him, “[t]he movement seems to be growing.”

He told of the support he had received from Meetings in his area — specifically the Old Chatham (New York) Monthly Meeting and Worcester (Massachusetts) Meeting.

He concluded:

[T]ax resistance can have its penalties.

You don’t have money to send your kids to college if you change your profession in a way not to pay withholding tax.

I think certainly one reason so few Friends have considered this witness is it can hurt one’s profession so seriously.

It’s not only losing the wages, but Friends enjoy doing a good job where they are working and don’t know how else they can live.

I like Quakers very much.

I’ve always been an active Friend.

But I feel our being part of the world to the degree we are prevents us from following Christ if the price is too high.

Molly Arrison also had a letter in that issue, but she thought war tax resistance “to be a most unrealistic and disrupting idea” because it would lead to a slippery slope of every citizen withholding taxes for whatever items of government spending they disapproved of, leading to “50 million contingencies” that would overwhelm the government’s revenue system.

She recommended that Quakers instead “orchestrate consistent barrages of phone calls, letters, and lectures until the general public has more influence than the Pentagon.”

David Scull considered this same argument in a letter in the issue:

We wish not to pay taxes for what we so strongly disapprove of.

But there are those who equally strongly feel that government contributions to the United Nations, or government money to pay for abortions, violate their principles.

It would not be difficult to compile a long list of purposes objected to; of course we say that our cause is a matter of high principle, but one person’s principle is another’s foible.

Is there some guideline which would make it easier to distinguish between two paramount obligations when they seem to be in conflict, one to support those purposes which our society has determined (no matter how imperfectly) to be for the common good, and the other to obey our consciences?

It seems to me that this can best be judged by our willingness to make some tangible sacrifices on behalf of conscience.

Scull went on to say that this made him skeptical of the World Peace Tax Fund plan: “[I]f I understand it correctly, there is no personal sacrifice involved.

It is just too easy to say to the government, ‘Please send my money where I want it to go instead of where you want it to go.’ ” He suggested improving the World Peace Tax Fund idea by “add[ing] the principle of personal sacrifice”:

Suppose I say, “Instead of $1000 which you say I owe you, here is $1100 as evidence of my sincerity; now will you allocate it in these ways?

That is how much extra I am willing to pay for the privilege of having my money not go to pay for machines of war.”

The inclusion of such a sacrificial element in the WPTF program would make a great deal of difference in my own ability to argue for it, and I think it would make a very convincing argument as we work toward its widespread acceptability.

…When we ask to relieve our consciences because of the way our money is spent, we should be… willing to put a price tag on the privilege.

A letter-to-the-editor in response to Scull’s argument, from Bill Samuel, thought that while the personal-sacrifice angle “has some surface attractiveness…”

Put another way, the proposal amounts to a government tax on conscience, which is quite a different matter from a voluntary personal sacrifice.

Not only is it morally questionable for the government “to put a price tag on” conscience, but some legal authorities believe it would constitute unconstitutional discrimination as well.

The World Peace Tax Fund bill would not be a special privilege.

Rather, the WPTF bill is a practical means of implementing the rights of conscience guaranteed by the First Amendment to the U.S. Constitution.

Like women, blacks and homosexuals, pacifists should take the position that we need not earn our rights but that they should be respected as a matter of course in a free and pluralistic society.

There is, of course, nothing wrong with the concept of people of conscience making a sacrifice for their deeply held beliefs.

Rather than impose a ten percent tax on conscience, concerned Friends might send an amount equal to ten percent of their tax payment to the National Council for a World Peace Tax Fund…

Corporately, Friends can also act to support those working to secure the right of pacifists not to pay for war.

One yearly meeting recently agreed to give $1,500 to the NCWPTF and several monthly meetings include the NCWPTF in their budgets.

Mennonites and Brethren each give a full time volunteer service worker to the NCWPTF.

While Friends do not have the kind of organized volunteer service effort that the other historic peace churches have, meetings can do their part by together contributing enough to support a full-time salaried worker.

Ross Roby also had some words to say about Scull’s argument against the World Peace Tax Fund plan.

He first begged for “immediate self-sacrificial labor and giving, on behalf of passage of a WPTF bill” and then wrote:

I would like to remind those who, like David Scull, have “difficulty with the World Peace Tax Fund as presently offered,” that there is nothing sacred and immutable about the present wording.

We can be quite certain that, when Congress takes a serious scrutiny of provisions for an alternative fund for C.O.s, much rewriting will be done.

The final bill. when passed, may look very different from the WPTF bill as now published.

He suggested that conscientious objectors to military spending should “soft pedal” the arguments amongst themselves over the details of the WPTF plan and instead concentrate on trying to convince the government to enact “a change in the income tax laws that will allow ‘free exercise of religion’ and give us the opportunity to build institutions for nonviolent solutions to international conflict with our present war tax dollars.”

His advice seems to have been followed, and the current campaign for “peace tax fund” legislation seems to have become so unwilling to use critical judgment and so eager to pass legislation of any sort that it has ended up backing a bill that would do nothing to help people with genuine conscientious objection to supporting military spending, nothing to reduce the military budget, and indeed nothing to increase spending on nonviolent conflict resolution — and yet even this bill has gone nowhere in Congress.

Such is the cost of “soft pedaling” internal debate.

an ad in the issue of Friends Journal

John J. Runnings confronted Molly Arrison’s argument more head-on in the letters-to-the-editor column of the issue.

Excerpt:

Our actions are determined by the degree of urgency we feel.

When our house is on fire we may exit by way of an upstairs window rather than by the conventional route via the stairs.

Many of us see the arms race as a fire out of control, and we are so adverse to feeding the flames that we are prepared to suffer considerable discomfort rather than do so.

So we break the law and are prepared to suffer the penalty.…

To break the law openly and expose oneself to the wrath of the power structure is to witness to the urgency and depth of one’s convictions.…

The early Quakers started at the places that Molly suggests, in the heart and in the community, but they went further.

They broke the law.

And they got themselves hanged and imprisoned; and they were heard above the contending clamors of their day.

And when the Constitution was written it contained provisions for freedom of religion and freedom of speech.

Modern Quakers continue, as of old, to work from the heart and in the community, but if we are to outshout the Pentagon we will have to use a louder and more urgent voice than we have used heretofore.

Perhaps more and more and more of us will have to break the law.

Franklin Zahn also responded to Arrison’s slippery-slope argument: “In practice, the portion of federal income tax for the military is far greater than for any other item.

Currently thirty-six percent goes for present costs and another estimated seventeen percent for past wars.

Objectors to smaller items would not find withholding worth the bother… [W]ords alone eventually lose all effect if no one ever acts.

But if a few other than war objectors choose to refuse, I see no objection to their doing so.”

Sally Primm interviewed Lucy Perkins Carner for the issue.

Among other topics, Carner addressed her war tax resistance:

[Q:] “Did you ever consider not paying part of your tax?”

[A:] “Oh yes, for years I’ve taken out of my income tax payment a portion that the Friends Committee on National Legislation says is equal to what the Pentagon gets.

Then I write a letter to the income tax people.

It’s good propaganda.

I send copies to my representatives in Congress and the President.

“I know my failure to pay isn’t going to impoverish the Pentagon, but it’s good propaganda.

They go to your bank and get the money.

I send them a copy of the letter, too.

Some people have refused to give them the information and go to jail as a result, but I’m not heroic.

They get it out of my bank every year.

“The bank has a right to charge for that, a service charge.

Well, in the last few years, believe it or not, I’ve received a letter from the bank saying they won’t make the charge any more.[”]

[Q:] “Why did they say that?”

[A:] “Well, that just shows you what good propaganda will do.

They know why I’m doing it.”

[Q:] “And how long have you done this?”

[A:] “I don’t know; when I became a pacifist, whenever that was [around the end of World War Ⅰ, according to another part of the article —♇].

I don’t even know when the income tax started.”

The issue covered the “New Call to Peacemaking” in which representatives from the three historic “peace churches” (Quakers, Mennonites, and Brethren) got together to try to put some oomph behind their peacebuilding efforts.

There was actually less about war tax resistance in this article than in much of the mainstream media coverage of the Call — perhaps because the civil disobedience angle was thought to be more newsworthy or attention-catching.

Here is where taxes were mentioned in the Friends Journal coverage:

The Friends Committee on National Legislation points out that all the federal income taxes withheld from your paycheck from January 1 to June 23 go for military purposes.

Not until June 24 do you begin to support any other part of the budget.

Especially in recent years — in light of increasing military budgets and the trend toward fewer soldiers and more expensive weapons systems — many conscientious objectors have chosen to witness against war by refusal to pay voluntarily those federal taxes that will be used to fund present, past, and future wars.

Some have done this by lowering their income below the taxable level; others who owe taxes have refused to pay the portion that would go for the military.

In the same issue, Robert C. Johansen wrote about the challenge of putting forward a pacifist alternative to mainstream political thinking.

In the course of that, he wrote:

Even though their goals are radical in the sense of seeking fundamental system change, political moderates will feel most comfortable using conventional means of education, consciousness-raising, lobbying, campaigning, organizing, and personal witness.

Those people who have tried such means and found them weak and insufficiently penetrating politically will search for other actions, such as tax resistance and civil disobedience, that convey a seriousness and urgency more equivalent to the threat of planetary militarization.

Maynard Shelly gave the Mennonite perspective in the wake of the New Call conference, and claimed that “[r]esistance to the payment of war taxes is becoming the witness of choice for a growing number of Mennonites.”

Charles C. Walker wrote in to the issue to suggest a token $1 resistance to the Pennsylvania state income tax as a way of protesting against its anticipated adoption of capital punishment.

The issue noted in its calendar that the Media Pennsylvania Friends Meetinghouse would be hosting a “National Military Tax Resistance Workshop” that would be “[i]ntroducing the program and services of the newly organized Center on Law and Pacifism.”

War tax resistance in the Friends Journal in

War tax resistance was a frequent topic in the issues of Friends Journal in , though there was still no consensus about how to go about it, and there was a lot of hesitance among Quaker institutions about how strongly to endorse it.

The issue was another special issue devoted to the peace testimony, which might as well have been a special issue on war tax resistance for how frequently it was mentioned.

Clearly by this time, there was no talking about peace work without talking about war tax resistance.

an illustration by Duncan Harp, from the issue of Friends Journal

Editor Ruth Kilpack opened the issue.

She noted:

I see the billions of dollars (including taxes from my own earnings) being poured into the “defense” budget.

I hear of vastly increased crime and see the wanton waste everywhere, much of it the direct legacy of our last war; I remember the lives still festering in military hospitals, the suffering from the wounds of war both here and across the world.

But now, there is a handful of people who are beginning to take a new view of war and war-making, realizing that it takes place not only when the bombing and shelling begin, but in the will of the people who make — or allow — it to happen.

War-making must be paid for.

As it is said elsewhere in this issue, “we pray for peace, but we pay for war.”

When we once understand that, great change will come about.

And especially, as war becomes more and more impersonal, with computerized strategic commands and weapons, more people are increasingly going to ask, “Who is waging this war?

Are we ourselves responsible, since we pay for it?”

(As the old saying goes, “Your checkbook shows where your heart is.”)

Take Richard Catlett, for example, a Friend who — as I write at this very moment in — is beginning his jail sentence of two months at the Kansas City Municipal Rehabilitation Institute (for first offenders) in Kansas City, Missouri.

That will be followed by three years of probation.

Richard Catlett has been an antiwar activist , refusing to file his income tax return .

In , his health food store was closed for non-payment of taxes (it is now under his wife’s ownership), and now, at sixty-nine years of age, Richard Catlett is treated as a criminal.

Clearly, he is being held up as an example of what can happen to a trouble-maker who dares to go against the tax law.… Richard Catlett’s age gives added emphasis to the warning to those no longer young and foolhardy.

(Besides, the pockets of those in his age bracket are usually better filled, and not to be overlooked by IRS.)

Catlett’s case was covered in more depth later on in the same issue by means of lengthy quotes from a Colombia Missourian article (see “Local war protester leaves for jail term” in ♇ 5 January 2013) and the following section from a Wall Street Journal article:

Tax Report

A protester got loads of publicity that drew criminal charges for nonfiling.

The IRS selects tax protesters for criminal prosecution based on the amount of publicity they get.

Usually protesters who don’t seek the spotlight are pursued by civil actions; criminal is reserved for the publicity hound.

Richard Ralston Catlett is a notorious war and tax protester.

The sixty-eight-year-old Columbia, Missouri, health food store owner argued that criminal charges of failing to file returns should be dropped because the IRS was guilty of “selective prosecution.”

The government is barred from selecting people to prosecute on grounds of race, religion or the exercise of free speech, or other “impermissible grounds.”

Catlett claimed that basing a criminal prosecution on publicity isn’t permitted.

But an appeals court disagreed.

His exercise of free speech wasn’t involved here, the court noted.

The IRS seeks criminal prosecution against publicized protesters to promote compliance with tax laws, the court observed.

“The government is entitled to select those cases for prosecution which it believes will promote compliance,” the court declared.

For some decades now we have been hearing the Church call on governments to take steps toward disarmament.

And it would be difficult to think of a thing more urgent or more appropriate for churches to say to governments.

It is hardly necessary here to give another recitation of the monstrous and unconscionable dimensions of the world arms race, culminating in the ever-growing stockpiles of nuclear weapons and the refinement of systems to deliver their carnage.

The Church has done part of its duty when it has said that this is wrong.

But the time has come to say that the good words of the Church have not been, and are not, enough.

The risks, the disciplines, the sacrifices, and the steps in good faith which the Church has asked of governments in the task of disarmament must now be asked of the Church in the obligation of war tax resistance.

It is, at the root, a simple question of integrity.

We are praying for peace and paying for war.

Setting euphemisms aside, the billions of dollars conscripted by governments for military spending are war taxes, and Christians are paying these taxes.

Our bluff has been called.

In all candor it must be suggested that the storm of objection which arises in the Church at this idea borrows its thunder and lightning from the premiers, the presidents, the ambassadors, and the generals who make their arguments against disarmament.

War tax resistance will be called irresponsible, anarchist, unrealistic, suicidal, masochistic, naive, futile, negative and crazy.

But when the dust has settled, it will stand as the deceptively simple and painfully obvious Christian response to the world arms race.

A score or a hundred other good responses may be added to it.

We in the Church may rightly be called upon to do more than this, but we should not be expected to do less.

Let the Church take upon itself the risks of war tax resistance. For church councils to take the position that the arms race is wrong for governments and not to commit themselves and call upon their members to cease and desist from paying for the arms race is patently inconsistent.

This is probably a fundamental reason why the Church’s pleas for disarmament have met with so little positive response.

Not even governments can have high regard for people who say one thing and do another.

If governments today are confronted with the question whether they will continue the arms race, churches are confronted with the question whether they will continue to pay for it.

As specialists in the matter of stewardship of the Earth’s resources they have contributed precious little to the most urgent stewardship issue of the twentieth century if they go on paying for the arms race.

How much longer can the.

Church continue quoting to the government its carefully researched figures on military expenditures and social needs and then, apparently without embarrassment, go on serving up the dollars that fund the berserk priorities?

The arms race would fall flat on its face tomorrow if all of the Christians who lament it would stop paying for it.

It is not, of course, simple to stop paying for the arms race as a citizen of the United States, or anywhere else for that matter.

If you refuse to pay the portion of your income tax attributable to military spending, the government levies your bank account or wages and extracts the money that way.

If your income tax is withheld by your employer, you must devise some means to reduce that withholding, such as claiming a war tax deduction or extra dependents.

If, as an employer, you do not withhold an employee’s war taxes, you will find yourself in court, as has recently happened to the Central Committee for Conscientious Objectors.

All of these actions are at some point punishable by fines or imprisonment, and none — in the final analysis — actually prevents the government from getting the money.

Nevertheless, it must be said that the Church has not tried tax resistance and found it ineffective; it has rather found it difficult and left it untried.

The Church has considered the risk too great.

Individuals fear social pressure, business losses, and government reprisals.

Congregations, synods, and church agencies equivocate over their role in collecting war taxes.

There is the risk of an undesirable response — contributions may drop off, tax-exempt status may be lost, officers may go to jail.

To oppose the vast power of the state by a deliberate act of civil disobedience is not a decision to be made lightly (an unnecessary observation, since there are no signs that Christians or the Church in the United States are about to do this lightly).

It would be inaccurate to give the impression that Christians, individually, and the Church, corporately, in the U.S. have done nothing about war tax resistance.

There have been notable, even heroic, exceptions to the general manifest lethargy.

The war tax resistance case of an individual Quaker was recently appealed on First Amendment grounds to the U.S. Supreme Court, but the court refused to consider it.

A North American conference of the Mennonite Church is grappling with the question of its role in withholding war taxes from the wages of employees.

Among Brethren, Friends and Mennonites — sometimes called the Historic Peace Churches — there is a rising tide of concern about war taxes.

The Catholic Worker Movement and other prophetic voices in various denominations have long advocated war tax resistance, but they have truly been voices crying in the wilderness.

For all our concern about the arms race, we in the churches have done very little to resist paying for it.

That has seemed too risky.

But then, of course, disarmament also involves risks.

Could there be a moral equivalent of disarmament that did not involve risk?

In this matter of the world arms race, it is not a question of who can guarantee the desired result, but of who will take the risk for peace.

Let the Church take upon itself the discipline of war tax resistance.

Discipline is not a popular word today, but it should be amenable to rehabilitation at least among Christians, who call themselves disciples of Jesus.

How quickly does the search for a way turn into the search for an easy way!

And how readily do we lay upon others those tasks which require a discipline we are not prepared to accept ourselves!

War tax resistance will involve the discipline of interpreting the Scripture and listening to the Spirit.

In a day when the Bible is most noteworthy for the extent to which it is ignored in the Church, it is an anomaly to see the pious rush to Scripture and the joining of ranks behind Romans 13, when the question of tax resistance is raised.

In a day when the authority of the Church is disobeyed everywhere with impunity, it is a curiosity to see Christians zealous for the authority of the state.

In a day when giving to the Church is the last consideration in family budgeting, and impulse rules over law, it is a shock to observe the fanaticism with which Christians insist that Caesar must be given every cent he wants.

As the Church has grown in its discernment of what the Bible teaches about slavery and the role of women, so it must grow in its discernment of what the Bible teaches about the place and authority of governments and the payment of taxes.

War tax resistance means accepting the discipline of submission to the Lordship of Jesus Christ in the nitty-gritty of history.

Call it civil disobedience if you wish, but recognize that in reality it is divine obedience.

It is a matter of yielding to a higher sovereignty.

Those who speak for a global world order to promote justice in today’s world invite nations to yield some of their sovereignty to the higher interests of the whole, and those persons know the obstinacy of nations toward that idea.

It may be that the greatest service the Church can do the world today is to raise a clear sign to nation-states that they are not sovereign.

War tax resistance might just be a cloud the size of a person’s hand announcing to the nations that the reign of God is coming near.

It is clear that Christians will not rise to this challenge without accepting difficult and largely unfamiliar disciplines.

But then, of course, disarmament also involves disciplines.

The idea that one nation can take initiatives to limit its war-making capacities is shocking.

To do so would represent a radical break with conventional wisdom.

How is it possible to do that without first convincing all the nations that it is a good idea?

Let the Church take upon itself the sacrifices of war tax resistance.

It is never altogether clear to me whether Christians who oppose war tax resistance find it too easy a course of action, or too difficult.

It is said that refusing to send the tax to IRS and allowing it to be collected by a bank levy is too easy — a convenient way of deceiving oneself into thinking that one has done something about the arms race.

And it is said that to refuse to pay the tax is too difficult.

It is to disobey the government and thereby to bring down upon one’s head the whole wrath of the state, society, family, business associates, and probably God as well.

Moreover, the same person will say both things.

Which does he or she believe?

In most cases, I think, the second.

The sacrifices involved in war tax resistance are fairly obvious.

They may be as small as accepting the scorn which is heaped upon one for using the term “war tax” when the government doesn’t identify any tax as a war tax, or as great as serving time in prison.

It may be the sacrifice of income or another method of removing oneself from income tax liability.

It can be said with some certainty that the sacrifices will increase as the number of war tax resisters increases, because the government will make reprisals against those who challenge its rush to Armageddon.

Yet, there is the possibility that the government will get the message and change its spending priorities or provide a legislative alternative for war tax objectors, or both.

In any case, for the foreseeable future, war tax resistance will be an action that is taken at some cost to the individual or the Church institution, with no assured compensation except the knowledge that it is the right thing to do.

But then, of course, disarmament also involves sacrifices.

The temporary loss of jobs, the fear of weakened defenses, and the scorn of the mighty are not easy hurdles to cross.

A moral equivalent will have to involve some sacrifices.

Let the Church take upon itself the action of war tax resistance.

The call of Christ is a call to action.

It is plain enough that the world cannot afford $400 billion per year for military expenditures, even if this were somehow morally defensible.

It is plain enough that the dollars which Christians give to the arms race are not available to do Christ’s work of peace and justice.

In these circumstances the first step in a positive direction is to withhold money from the military.

If we say that we must wait for this until everybody and (and particularly the government) thinks it is a good idea, then we shall wait forever.

Having withheld the money, the Church must apply it to the works of peace.

What this means is not altogether obvious at present, but there is reason to believe that a faithful Church can serve as steward for these resources as wisely as generals and presidents.

The dynamic interaction between individual Christians and the Church in its local and ecumenical forms will help to guide the use of resources withheld from the arms race.

This is a call to individual Christians and the Church corporately to make war tax resistance the fundamental expression of their condemnation of the world arms race.

Neither the individual nor the corporate body dare hide any longer behind the inaction of the other.

The stakes are too high and the choice is too clear for that, though we can have no illusions that this call will be readily embraced nor easily implemented by the Church.

But then, of course, we do not think that disarmament will be an easy step for governments to take either.

The Church has an obligation to act upon what it advocates, to deliver a moral equivalent of the disarmament it proposes.

If effectiveness is the criterion, it is certainly not obvious that talking about the macro accomplishes more than acting upon the micro.

A single action taken is worth more than a hundred merely discussed.

(When it comes to heating your home in winter, you will get more help from one friend who saws up a log than from a whole school of mathematicians who calculate the BTUs in a forest.)

To talk about a worthy goal is no more laudable than to take the first step toward it, and might be less so.

Michael Miller wrote an article for the same issue that noted that the National Guard is a U.S. military combat function that is largely paid for out of state budgets, not the federal budget.

He concluded:

I am now more fully aware how the military affects our daily lives and activities.

I also realize that not only is the objection to payment of war taxes a federal issue, but it is also a very real state issue.

State budgets contain rather large amounts in this respect.

As Friends, we must be constantly aware of the issues involved with our tax dollars.

The military has a great influence over our lives and our tax dollars, whether or not we recognize it.

We have a responsibility to make ourselves aware of the issues and how they influence our lives.

Alan Eccleston contributed an article on war tax resistance as a method of testifying for peace — aligning ones life with ones values.

This, he felt, could be done in a variety of ways:

We do not have to be prepared for jail to be a war tax resister.

We do not have to be ready, at this moment, to subject ourselves to harassment by the Internal Revenue Service.

We do, however, have to be truthful on our tax returns.

We do have to be clear about our belief in the peace testimony and our desire to align our lives with this belief.

And that is all!

If you are clear about that, you can withhold some amount of your tax.

It can be a token amount, if that is where you are, say five dollars or fifty dollars.

Or it can be the same percent of your tax as the military portion of the current budget, currently thirty-six percent excluding past debt and veterans benefits.

(An easy way to do this is to insert the amount under “Credits” as a “Quaker Peace Witness,” line forty-six.

Alternately, some people declare an extra deduction, but this is more complicated, since the deduction must be substantially larger than the amount you desire to withhold.)

It may bother you that three times or even ten times what you have chosen to withhold is going to be spent for war preparations.

But far better to take this small step than to turn away from the witness. Write your congresspersons and tell them of your concern.

Urge them to pass the World Peace Tax Fund which would acknowledge your constitutional right to practice your religious beliefs without harassment and penalty.

Alternatively, if the government owes you money fill out the (very short) Form #843 “Request for Refund,” asking that they refund the amount you wish for peace witness.

One can also anticipate the withholding problem by filling out a W-4 Form at your place of employment declaring (truthfully) an allowance for expected deductions that includes the amount of your peace witness.

Then what?

You can expect a series of computer notices stating that you calculated your tax incorrectly and you owe the amount shown on the notice.

This may also include an addition of seven percent annual interest on the amount owed.

(Currently IRS seems not to be adding on penalty charges but that is a possibility.)

You have a choice: you can ignore the notice; you can write or call IRS and discuss it; or you can pay the tax.

Sooner or later you will receive a printout that says “Final Notice.”

If you again fail to pay the amount owed, you will probably receive a call from someone at IRS who will try to convince you that the whole process has gone far enough and that your purpose is better served by paying the government.

IRS wants to collect.

That is their job; when they have done it, they are through with you.

They cannot, by law, be harsh or punitive.

There is no debtors’ prison in this country.

If you declare the intent of your witness on your tax form and by letter to Congress, you cannot be convicted of fraud; therefore, you are not risking criminal penalties.

In other words, the tax resister controls the process.

One can witness to peace so long as it can be done lovingly and, if it is to be a meaningful witness of peace, that is the only way it can be done.

However, if one’s family obligations or other matters are too pressing, or if one’s spiritual resources are being unduly strained, it is time to lay down this particular witness.

One can carry on the witness and still bring the process to a conclusion by letting the payment be taken from a bank account or peace escrow fund.

Another round of letters to Congress and the president will testify to your continuing concern even after the pressure of collection has been relieved.

In your witness, no matter how small the amount withheld or how short the duration, you will gain strength and courage and insight.

This brings new resources to your next witness.

It gives you knowledge and resources to share with others, which in turn helps their witness.

In sharing, you both are strengthened.

Thus, a personal witness becomes a “community of witness,” and the “community of witness” gains strength, courage, and insight in its mutual sharing.

This witness and this sharing of Christian love becomes its own witness to the testimony of peace — the testimony of love for God, for ourselves, for humankind.

(A letter from Dorothy Ann Ware in a later issue credited the Eccleston article for spurring her to “make a token Quaker Peace Witness by withholding a very small portion of my income tax.

So Step One has been taken…”)

The same issue reprinted a Minute from the Philadelphia Yearly Meeting which encouraged Quakers “to give prayerful consideration… to the option of refusal of taxes for military purposes.”

Furthermore:

We reaffirm the Minute of the yearly meeting which states in part that “…Refusal to pay the military portion of taxes is an honorable testimony, fully in keeping with the history and practices of Friends… We warmly approve of people following their conscience, and openly approve civil disobedience in this matter under Divine compulsion.

We ask all to consider carefully the implications of paying taxes that relate to war-making… Specifically, we offer encouragement and support to people caught up in the problem of seizure, and of payment against their will.”

We request the Representative Meeting to arrange for the guidance of meetings and their members on the form of military tax resistance suitable for individuals in accordance with that degree of risk appropriate to individual circumstances, for advice on consequences, and for consideration of legal and support facilities that may be organized.

We also request Representative Meeting to provide for an Alternate Fund for sufferings, set up under the yearly meeting to receive tax payments refused, for those tax refusers who may wish to utilize this fund.

We recommend cooperation with the Historic Peace Churches and other religious groups in further consideration of non-payment on religious grounds of military taxes.

Following that, John E. Runnings wrote of his and his wife Louise’s war tax resistance, and decried the injustice of a “society that requires that Quakers, who renounce war and recognize no enemies, must pay as large a contribution to the support of the war machine as those who fully accept the malicious nature of other nationals and who are so frightened of their ill intent that no amount of extermination equipment is enough to assure security.”

The social reforms that we credit to George Fox’s influence did not come about by his waiting on the Spirit but rather by his responding to the Spirit.

If just one man could accomplish so much by responding to the Spirit, what would happen if several thousand modern Quakers were to respond to their spiritually-inspired revulsion to assisting in the building of the war machine?

If Quakers could be induced to discard their excuses for their financial support of the arms race and to withhold their Federal taxes, who knows how many thousands of like-minded people might be encouraged to follow suit?

And who knows but what this might bring a halt to the mad race to oblivion?

There was a brief update about Robert Anthony’s case.

Anthony hoped to use his Fifth Amendment right against self-incrimination (presumably in response to a government request for financial records or something of the sort).

The judge in the case asked if the government would grant Anthony immunity from prosecution for anything he disclosed, which would have cut off the Fifth Amendment avenue of resistance, but the government wasn’t prepared to do that, and that’s where the matter stood.

The issue included a notice that the Center on Law and Pacifism had “recently published a military tax refusal guide for radical religious pacifists entitled ‘People Pay for Peace’ ” but also noted that “the Center states that it is in ‘urgent and immediate need of operating funds.’ ”

A later issue gave some more information about the Center:

The Center was started after a former Washington constitutional lawyer and theologian, Bill Durland, met a handful of conscientious objectors who were appealing to the U.S. courts for their constitutional rights to deny income tax payments for the military.…

That was in .

The Center is now producing regular newsletters and has published a handbook on military tax refusal.

It has organized war-tax workshops for pacifists representing constituencies in the Northeast, South and Midwest.

One of its projects was the “People Pay for Peace” scheme, under which it was suggested that each individual deduct $2.40 from his/her income tax return to “spend for peace”: that sum being the per capita equivalent of the $193,000,000,000 which will be consumed in for war preparation in the United States.

This was a protest action against the fifty-three percent of the U.S. budget allocated to military purposes.

The Center on Law and Pacifism is a “do-it-yourself cooperative” which relies on both volunteer professional assistance and individual contributions.

Hmmm… my calculation for 53% of the federal budget in 1979 is more like $214,618,730,000… and per-capita (by U.S. population, anyway) that would be $953.63 per person.

If you use the $193 billion value, that’s still $857.57 per person.

Even if you use world population, you still get $44.08–$49.02 each.

Somebody’s confused… maybe it’s me.

Wendal Bull penned a letter-to-the-editor in the same issue about his experience as a war tax resister twenty years before.

Excerpt:

In I received a lump sum payment of an overdue debt.

This increased my income, which I normally keep below the taxable level, to a point quite some above that level.

I distributed the unexpected income to various anti-war organizations.

I anticipated pressure from IRS officers, so in the autumn, long before the tax would be due, I disposed of all my attachable properties.

This action, under the circumstances, I believe to be unlawful.

But it seemed to me a mere technicality, far outweighed by the sin of paying for war, or the sin of permitting collection of the tax for that purpose.

After disposing of all attachable properties, I wrote to IRS telling them I had taxable income in that year but chose not to calculate the amount of it because I had no intention of paying it.

In the same letter I explained my reasons for conscientious non-cooperation with Uncle Sam’s preparations for war in the name of “defense.”

My letter appeared in full or in generous excerpts in at least three daily papers and several other publications and I mailed copies to friends who might be interested.

I am not a publicity hound nor a notorious war resister.

The publicity did seem to effect a fairly prompt visit from the Revenue Boys.

They paid me three or four visits.

On one occasion two men came; one talked, the other may have had a concealed tape recorder, or was merely to witness and confirm the conversation.

After quizzing me for an hour or more they left courteously, whereupon I said I was sorry to be a bother to them.

At that the talker said, “You’re no trouble at all.

I brought a warrant for your arrest, but I’m not going to serve it.

It’s the guys who hire lawyers to fight us that give us trouble.”

If they had caught me in a lie, or giving inconsistent answers to their probing questions, I suspect the summons would have been served.

I was fully prepared to go to court and to be declared guilty of contempt for not producing records to show the sources of my income.

I had told the men I was in contempt of the entire war machine and all officers of the legal machinery who aimed to penalize citizens for non-cooperation with war preparations.

Later came two visits from a man who attempted to assess my income for that year, and the law required him to try to get my signature to his assessment.

I considered that a ridiculous waste of taxpayer’s money.

The man agreed with a smile.

Still later, there came several bills, one at a time, for the amount of the official assessment, plus interest, plus delinquency fee, plus warnings that the bill should be paid.

These I ignored, of course.

The head men knew I would not pay; and they knew they had not any intention of trying to force collection.

I have no idea who decided to quit sending me more bills.

I think the claim is still valid since the statute of limitations does not apply to federal taxes.

It is inconvenient to have no checking account, to own no real estate, to drive an old jalopy not worth attaching, and so on.

Some of us choose this alternative rather than to let the money be collected by distraint.

In the same issue, Keith Tingle shared his letter to the IRS, which he sent along with his tax return and a payment that was 33% short.

He stressed that he didn’t mind paying taxes — “a small price for the tremendous privilege of living in the United States with its heritage of freedom, equal protection, and toleration” — but that “I do not wish my labor and my money to finance either war or military preparedness.”

Stephen M. Gulick also wrote in.

“Because the military and the corporations need our money more than our bodies, war tax resistance becomes important — in all its forms from outright and total resistance to living on an income below the taxable level,” he wrote.

“Fundamentally, war tax resistance must lead us to look not only at warmaking and the preparation for war, but also at the economic, social, and political practices that, with the help of our money, nurture the roots of war.”

Colin Bell attended the Southern Appalachian Yearly Meeting:

“I think,” Colin said, “that as a Society we are standing at another moment like that, when our forebears took an absolutely unequivocal stance” and we don’t know what to do.

Are we looking for something easy, he wondered, suggesting that it probably should be tax resistance.

Accepting the title Historic Peace Church, he declared, makes it sound like a worthy option, rather than it being at the entire heart and core of Christendom.

A letter to the editor of the Peacemaker magazine from John Schuchardt is quoted in the issue:

I have recently received threatening letters from a terrorist group which asks that I contribute money for construction of dangerous weapons.

This group makes certain claims which in the past led me to send thousands of dollars to pay for its militaristic programs. The group claimed: 1) It was concerned with peace and freedom; 2) It would provide protection for me and my family; 3) It was my duty to make these payments; and 4) I was free from personal responsibility for how this money was spent in individual cases.

Last year, for the first time, I realized that these claims were fraudulent and I refused to make further payments…

That issue also noted that the Albany, New York, Meeting “joined the growing number of meetings which are calling on their members to ‘seriously consider’ war tax resistance…” That Meeting was also considering establishing its own alternative fund, and was hoping Congress would pass the World Peace Tax Fund bill.

This “seriously consider” language, along with the Philadelphia Yearly Meeting’s earlier-mentioned call for Quakers “to give prayerful consideration” to war tax resistance, is a far cry from the sort of bold leadership John K. Stoner was calling for.

But then again, Quaker Meetings were no longer the sorts of institutions to bandy about Books of Discipline and threaten “disorderly walkers” with disownment, or even to give them “tender dealing and advice in order to their convincement.”

Meetings had in general become much more humble about what sort of direction they should provide and what sort of obedience they could expect.

It is hard to imagine a Meeting from this period adopting a commandment along the lines of the Ohio Yearly Meeting’s discipline — “a tax levied for the purchasing of drums, colors, or for other warlike uses, cannot be paid consistently with our Christian testimony.”

The issue included a review of Donald Kaufman’s The Tax Dilemma: Praying For Peace, Paying for War, a book that defends war tax resistance from a Christian and Biblical perspective.

“What is the individual’s responsibility in the face of biblical teachings and the history of tax resistance since the early Christian centuries?

Some biblical passages have been used to justify the payment of any and all taxes.

But Kaufman warns us to consider these passages in their historical context and in the light of the primary New Testament message: love for God, oneself, one’s neighbor, and one’s enemy.”

That issue also included an obituary notice for Ashton Bryan Jones that noted “[h]is courage in the face of the harsh treatment that he endured in the struggle for social justice and against war taxes…”

The issue reported on the New England Yearly Meeting, which held a workshop on war tax resistance, and also agreed to establish a “New England Yearly Meeting Peace Tax Fund.”

Recognizing that each of us must find our own way in this matter, the new fund is seen not as a general call to Friends to resist paying war taxes but specifically to help and to hold in the Light those Friends who are moved to do so.

The fund will be administered by the Committee on Sufferings, which came into being last year to support Friends who are devoting a major portion of their time and energies to work for peace.

New Call to Peacemaking

The “New Call to Peacemaking” brought together representatives of the Mennonites, Brethren, and Quakers in , and to try to strengthen their respective churches’ anti-war stands.

It continued to ripple through the pages of the Journal in .

Barbara Reynolds covered the Green Lake conference that drafted the New Call statement in the issue.

Among her observations:

In my own small group, I saw social action Friends struggling with Biblical language and coming to accept many scriptural passages as valid expressions of their own convictions.

And I saw a respected Mennonite, a longtime exponent of total Biblical nonresistance, courageously re-examining his position and corning out strongly in favor of a group statement encouraging non-payment of war taxes.

Elaine J. Crauder gave another report on the project in the issue.

Excerpts:

Quakers, Mennonites and Brethren are known as the Historic Peace Churches.

How do they witness against evil and do good?

Where does God fit into their witnessing?

Are they responding to the urgency of the present-day world situation, or are they truly “historic” peace churches, with no relevance to today’s complex world?

The New Call to Peacemaking (NCP) developed out of exactly these concerns: Where is the relevance and what is the source of our witnessing?

The answers were clear.

To seek God’s truth and to witness, in a loving way, by doing good (through peace education, cooperation in personal and professional relationships, living simply and investing only in clearly life-enhancing endeavors) and by resisting evil (working for disarmament and peace conversion, resisting war taxes and military conscription).

Crauder says she first started thinking about her support of war through her taxes in :

The 1040 Income Tax form didn’t have a space for war tax resisters.

Either I would have to lie about having dependents, or my taxes would be withheld. l didn’t feel that I had a choice.

It did not occur to me to claim a dependent and then support that person with the funds that thus wouldn’t go for war.

So, I did what was easiest — nothing — and paid my war taxes.

In , she says:

I started to think about my taxes again.

Maybe I could lie on my form.

It was definitely not right to work for peace and pay for the war machine.

I even went to one meeting of the war tax concerns committee.

But there were enough meetings that I had to go to, so I managed not to find the time to struggle with my war taxes.

Words of John Woolman seemed to fit my condition:

They had little or no share in civil government, and many of them declared they were through the power of God separated from the spirit in which wars were; and being afflicted by the rulers on account of their testimony, there was less likelihood of uniting in spirit with them in things inconsistent with the purity of Truth.

Woolman was referring to the early Quakers when he said it was less likely that they would be influenced by the civil government in questions of the truth.

It seemed to me that in Woolman’s time it was also easier to be clear about the truth — we are so much more dependent and tied to the government than they were.

Perhaps it is always easier to have a clear witness in hindsight.

I think Crauder has it a little backwards here.

Woolman was speaking of early Friends in England, who were being actively repressed by the government and banned from much of any exercise of political power, and contrasting them to the Quakers in Woolman’s own time and place (colonial Pennsylvania), where Quakers held political power, and were by far the dominant party in the colonial Assembly.

In Woolman’s time the government and the Society of Friends were as tightly linked as they ever have been.

Historical notes

In the issue, Walter Ludwig shared an interesting anecdote about Susan B. Anthony’s father, Daniel Anthony:

During the Mexican War he made the quasi tax-resisting gesture of tossing his purse on the table when the collector appeared, remarking, “I shall not voluntarily pay these taxes; if thee wants to rifle my pocketbook thee can do so.”

I hunted around for a source for this anecdote, and found one in Ida Husted Harper’s The Life and Work of Susan B. Anthony (1898), where she put it this way:

In early life he had steadfastly refused to pay the United States taxes because he would not give tribute to a government which believed in war.

When the collector came he would lay down his purse, saying, “I shall not voluntarily pay these taxes; if thee wants to rifle my pocket-book, thee can do so.”

But he lived to do all in his power to support the Union in its struggle for the abolition of slavery and, although too old to go to the front himself, his two sons enlisted at the very beginning of the war.

John Woolman was invoked in the issue as someone who “took as clear a stand on payment of taxes for military ends as he did on slavery.”

He was quoted as saying:

I all along believed that there were some upright-hearted men who paid such taxes but could not see that their example was a sufficient reason for me to do so, while I believed that the spirit of Truth required of me as an individual to suffer patiently the distress of goods rather than pay actively.

Bruce & Ruth Graves

The issue brought an update on the case of Bruce and Ruth Graves, who were pursuing a Supreme Court appeal in the hopes of legally validating their approach of claiming a “war tax credit” on their federal income tax returns.

They were trying to get people to write letters to the Supreme Court justices, in the hopes that they would find influential the opinions of laymen on such points as these:

1) petitioners right to First Amendment free exercise of religion and freedom of expression, 2) paramount interests of government not endangered by refusal of petitioners to pay tax, 3) petitioners should be able to re-channel war taxes into peace taxes (via World Peace Tax Fund Act, etc.), 4) IRS regulations should not take precedence over Constitutional rights of individuals, 5) threat of nuclear war must be stopped by exercise of Constitutional rights, 6) other pertinent points at the option of correspondent.

There was a further note on that case in the issue — largely a plea for support, without any otherwise significant news.

Included with this was a message from the Graveses with this plea: “How can Friends maintain the secular impact of the peace testimony expressed through conscientious objection when technology has replaced the soldier’s body with a war machine?

Does it not follow that technology then shifts the emphasis of conscientious objection toward reduction of armaments by resisting payment of war taxes?”

The issue brought the news that the Supreme Court had turned down the Graveses’ appeal.

“[W]hen asked whether the frustrations of losing the long court battle had ‘generated any thoughts of quitting,’ Ruth Graves replied, ‘Never.

If I were going to let myself be stopped by seemingly hopeless causes, I’d just die right now.”

World Peace Tax Fund

A note in the issue reported that some people who had “sent in cards or letters expressing support for the [World Peace Tax Fund] bill” had reported that they had “been subjected to IRS audits and other harassment.”

A letter from Judith F. Monroe in the issue expressed some concern about the World Peace Tax Fund plan.

Excerpts:

I fear the World Peace Tax could become a device to appease the consciences of those of us who are not willing to face the consequences of civil disobedience.…

…One important purpose of the tax is to shake the complacent into a realization of the madness of our current armaments race.

I don’t believe the casual matter of checking a block on a tax form will ever cause extensive introspection on the part of most people.

How will peace tax funds be handled?

Will such a tax require more complex tax laws, IRS investigators, and tax accountants?

How can we believe in the government’s ability to use such funds constructively?

I can envision the Department of Defense receiving peace grants.

After all, they’re the boys who fight for peace.

This may be an exaggeration.

The point is I do not feel we can trust any large bureaucracy with the task of peacemaking.

If the majority or at least a sizable minority do not opt for the peace tax, all that will happen is a larger percentage of their taxes will go to armaments to compensate for the monies diverted by the few who chose a peace tax.

Under such circumstances, the peace tax would accomplish little.

Evidence of some critical appraisal of the “peace tax” idea is also found in a note in the issue, which summarizes an address by Stanley Keeble to the June General Meeting in Glasgow, Scotland:

If this were permitted, would not government simply raise military estimates to compensate for expected shortfall?

Would not people not conscientiously opposed to military “defense,” take advantage of such legislation?

Would the procedure be destructive of democracy and majority rule?

Should not individuals rather reduce their earnings to a non-taxable level, or would that deprive useful projects of legitimate funds?

Other such questions were raised, relating to possible effects on national “defense” policy.