Tax resistance in the “Peace Churches” →

Brethren →

Charles E. & Cleda P. Zunkel

This is the eighth in a series of posts about war tax resistance as it was reported in back issues of Gospel Herald, journal of the (Old) Mennonite Church.

Up until now, war tax resistance has either been treated as unscriptural and therefore unthinkable, or as a curious practice that a few particularly conscientious people from other Christian sects were experimenting with.

But in something snapped, and the Gospel Herald began to consider it as a possible Mennonite response.

The issue noted that the closely-related Anabaptist cousins, the Church of the Brethren had turned the payment of taxes for military purposes into a problem that Christians needed to solve or work around:

Church of the Brethren leaders will approach government agencies in the interest of finding a “positive alternative” to the payment of taxes for military purposes.

The Brotherhood Board voted to make explorations “with the appropriate agencies of government to the end that an acceptable constructive alternative be provided for all those persons who by reason of religious training and belief conscientiously object to the payment of that portion of income taxes going for military defense.”

Several members of the Board pointed out that this matter would be much more complicated than arrangements already in effect for alternatives to military service, but the Board felt all possible explorations should be made.

The Mennonite Central Committee put this on the agenda at its Executive Committee meeting :

[The MCC Executive Committee actions included] Referring to Peace Section the invitation from the Church of the Brethren to study whether there might be a positive alternative provided by the U.S. government for persons conscientiously opposed to paying that portion of income taxes going for military defense.

Harold S. Bender did not address this tax problem directly, in his essay “When May Christians Disobey the Government?”

This may be meaningful because this was a time when war tax resistance was clearly in the air and because when Bender had been given the opportunity in the 1930s and 1940s, he had said unequivocally that Christians pay their taxes period.

Bender did, though, take a very conservative line on civil disobedience in general:

Jesus taught His disciples to “Render therefore unto Caesar the things which are Caesar’s; and unto God the things that are God’s” (Matt. 22:21), thus stating a principle which goes far beyond the question of tax payment which was immediately at issue.

The Christian owes allegiance and obedience to two sovereignties, both in good conscience.

He must decide in all conscientiousness and earnestness when his allegiance to God requires disobedience to regularly constituted governmental authority and cheerfully take the consequences.

Opinion that a law or a requirement of the state is unwise or undesirable cannot be a ground of disobedience.

There may be wide divergence as to whether legislation is good or bad or whether governmental policies are helpful or harmful to the general welfare.

The Christian’s overriding obligation is to obey, even while he may seek to persuade or convince the authorities to change the law.

What then are the conditions requiring disobedience?

Certainly the Christian must disobey (1) when he is required to perform an act which is clearly forbidden in Scripture or is a dear implication from such a prohibition (military training or service would be a case in point), and (2) when he is forbidden to do what the Scripture or the clear implications of it require.

In other words, the subject matter of an act required by the state must clearly be an evil in itself, which then becomes a sin when performed.

We must consider it a sin to disobey the government (in the light of the above-cited N.T. teachings) unless a sinful act is required.

The Christian is not at liberty to disobey the government for his own ulterior purposes, no matter how good these purposes may be in themselves…

Nonresistant Christians cannot justify disobedience to law merely because they have good ends in view.

In the light of the above, it would appear that the desire to witness to the truth or against an evil cannot be a ground to disobey the requirements of the state which in themselves are not wrong.

Nor may the supposed relative effectiveness of several kinds of witness be a ground for employing the type of witness that involves disobedience, rather than a type that is free of such disobedience.

For example, Bender wrote, in the case of conscription, it is not sinful to accept conscription into civilian service, so Christians must accept this if it is demanded.

Registration is also not sinful, so Christians must register.

If forced into military service, though, the Christian must refuse to obey.

Refusal to register is a form of witness against the military, not a proper example of Christian refusal to commit a sinful act, and so it’s not an appropriate occasion for disobedience.

This distinction is worth keeping in mind as we move forward, as some Mennonite war tax resisters will come to defend their resistance as a form of witness against an over-militarized state, while others will defend theirs as a form of conscientious objection against (indirect) military service.

When the Mennonite Central Committee issued its Annual Report, the “Peace Witness” section made note of the growing concern among Mennonites about the propriety of paying for the military by means of taxes:

Emerging throughout our constituency is a growing uneasiness concerning our witness against such problems as discrimination, militarism, and war, in view of the frightful consequences these might have today.

Concern is evident in discussions about possible participation in various protest actions and about the propriety of paying income taxes that are used so largely for war purposes, as well as the suggestion that perhaps nonregistration would be a clearer testimony against conscription and militarism.

Serious discussion on the question of whether the nonresistant Christian can in good conscience pay income taxes which go so heavily for war purposes has continued.

Some decided the time had come to press the point.

“A Concerned Member” had this to say in the issue:

Would you believe that Mennonites are giving many times more for military purposes than for missions?

Sixty per cent of your income tax money each year goes for defense and yet per member we give only about $20 each year for missions.

A.J. Muste, well-known pacifist leader, has lost a court battle in his refusal to pay income tax because some portion might go toward the nation’s military establishment.

United States Tax Court has ruled that Mr. Muste must pay back taxes plus a variety of penalties.

The opinion stressed that Congress has specifically provided military service exemption for conscientious objectors, but has taken no similar action in the income tax field.

Andrew R. Shelley was among the first Gospel Herald writers to try to provide a solution for concerned Mennonites.

He proposed using legal deductions for charitable donations (which were apparently more generous then than they are today) to reduce or eliminate income tax liability ():

Practically all thinking people are disturbed about the arms race in our world.

This does not mean there is common agreement as to exactly what should be done about it.

In the United States many people of various denominations, and some who do not claim to be Christians, are very much concerned over the proportion of the national budget which goes for military purposes.

There have been those who have felt that Christian people should withhold the portion of the tax which goes for military purposes.

These people reason that to pay the tax is a violation of conscience.

Our government has been petitioned numbers of times to provide an alternative to paying tax for military purposes.

During World War Ⅱ the Canadian government did provide what was called a “Sticker Bond.”

This meant that a conscientious objector, if he desired that his money be used for other than war purposes, could request that a sticker be attached to his bond which would indicate that the money was to be used for nonmilitary purposes of government.

While this eased the conscience of the conscientious objector, it was purely a bookkeeping matter as far as the government was concerned, because it provided for essential phases of the work of the government.

Recently in various periodicals there have appeared letters and articles regarding the paying of the portion of tax that goes for military purposes.

It has appeared to me that one phase of the solution of the problem has been overlooked in almost all of the letters and articles which I have read.

In our desire to find a full solution to the problems involved we should not be unmindful of that which we do have in our power to do.

The government of the United States is the most liberal government in the world in regard to giving recognition for giving to charitable purposes.

Our government allows a tax deduction of 30 per cent for charitable giving.

(The last 10 per cent must be given to certain phases of charity which fall into the category of the general giving of Christian people.)

All of us are aware of the unnatural and unwholesome nature of American living.

Yet, most Christian people choose to go along with this way of life which even many non-Christian leaders say is unwholesome.

It is possible for Christian people to sharply reduce the amount of tax which they pay for military purposes through the simple and legal expedient of charitable giving.

Here, our government gives us the marvelous opportunity to choose that phase of charitable giving to which we desire our money to go.

While it is certainly true that not all Christian families can give 30 per cent of their income to charitable purposes, certainly those in average circumstances can do so.

(Those in higher income brackets can go far beyond this.)

It is at once evident that we need not go along with some of the extremely wasteful practices of the American public.

For every hundred dollars more that the Christian family gives to the work of the church, they can save twenty dollars’ tax and approximately fifteen dollars which would go into the general category of military spending (on the basis of 20 per cent taxation).

Consequently, it would seem that those directly concerned with the problem of taxation for military purposes would go the very limit in reducing the amount of money which they give to military purposes through taxation.

For those who are concerned about this matter, I would urge that careful records be kept of every phase of living having to do with taxes.

Thus it will be seen that through careful expenditure of the money God has entrusted to us, it is astounding how much we can give to the work of the Lord.

Think of the prospects; the positive aspect of our modern America is the privilege of living full lives and yet giving largely to the work of the Lord.

I would like to clearly state that this is not the highest motivation for giving.

We give fundamentally not because we want to pay less tax, but primarily because we love the Lord and we want His work to go forward.

It is startling and it is wonderful that at this juncture of the history of the world, when the needs are great and the opportunities are beyond description, the Lord has granted us the greatest resources in the history of mankind.

We can send forth the Gospel of our Lord Jesus Christ.

Certainly without Him there can be no peace.

Without the saving grace of salvation which has been brought through the shed blood of Christ, there can be no lasting peace.

Among the various things that might be said, we must realize that the primary consideration is the sending forth of the Gospel.

While this approach does not answer the total problem with which we began this letter, it does mean that we are beginning at a point where we have control.

And from this point, which takes no more time than any other approach that we might use, we can do what we feel led to do further.

But let us begin at this point and I am sure whatever else we do will be observed with greater sympathy than if we do not start at this point of personal involvement.

All of us believe it is right and proper that we should support many phases of our government.

Whatever our differences may be on the attitude toward taxation in relation to the military part of our budget, certainly we recognize the need for government.

We recognize our responsibilities. Rom. 13.

Consequently, we gladly participate in that part of our government’s program which is essential for the welfare of our people.

A civilly disobedient war tax resister from the Church of the Brethren — Charles E. Zunkel — hit the pages of Gospel Herald on :

Charles E. Zunkel of Port Republic, Va., former moderator of the Church of the Brethren, wrote to President Kennedy and to the director of Internal Revenue that he and his wife would no longer pay a major portion of their federal income tax because 75 per cent of it goes for military purposes.

He wrote that they would continue filing their income taxes, but would pay only 25 per cent of the amount.

The remainder would be given to the church in quarterly payments, in addition to the 15 per cent or more which they already give.

He writes that they hope some alternative tax plan may be worked out whereby conscientious objectors may give their tax money to peaceable pursuits just as young men serve in alternative service in lieu of the military service.

Finally, a poem by Rachel Horst, found in the edition, and titled “Render to Caesar” suggested that the Render Unto Caesar quotation was being abused by people who prefer Caesar to Christ:

He spoke the words, Himself, not long ago

While looking at a craven face upon the coin.

We paid our tax with hatred to a hated man

And waved palms for a King of love,

Whose throng we hoped to join.

We shout the words from raucous throats today

While looking at a regal face upon the cross.

We acclaim the kingship of a loathsome man

As we renounce the Sovereign

Without a thought of loss.

There was a bit of a gap in coverage of war tax resistance issues for the rest of the year that coincided with John Drescher taking over the editorship from Paul Erb in (I don’t know if there’s any connection).

But then things heated up, as a genuine Mennonite declared himself a civilly disobedient war tax resister in .

Tune in tomorrow!

In , suddenly Brethren couldn’t stop talking about war tax resistance.

By war tax resistance had gone from heresy to something that was considered one possible appropriate Christian response to runaway militarism.

Take, for example, this mention in passing from Ralph E.

Smeltzer’s long essay on “The Church and the World” in the issue of Gospel Messenger:

When the Christian conscience and the demands of the state conflict, as many feel in the case of military service, taxes for military purposes, and defense jobs, the Christian must follow his conscience.

A lengthy war tax resistance letter-to-the-editor on war tax resistance led off that column in the issue (source).

The page scan (here and elsewhere in this volume) is difficult to read in parts, but I’ll try to restore it as best I can:

Taxes for War Purposes

The three of us, two ministers and a layman, have come to the conclusion that we can no longer pay Federal income tax for war.

This may seem an astonishing stand; but much more astonishing is our general Brethren complacency about paying income tax.

In colonial times and during the Revolutionary War there was much tax refusal by Quakers, Mennonites, and Brethren.

An irate critic of the Church of the Brethren charged,

“They not only refused to take up arms to repel the savage marauders and prevent the inhuman slaughter of women and children, but they refused in the most positive manner to pay a dollar to support those who were willing to take up arms to defend their homes and their firesides, until wrung from them by the stern mandates of the law.

They did the same when the Revolution broke out. They might at least have furnished money.

But no; not a dollar!”

It is not certain whether this writer referred to taxes or only to the substitutionary sum paid in lieu of the militia draft.

In either case the Brethren then had an alert ethical sensitivity about turning over their money for war.

In the belief that many Brethren are becoming troubled about paying income tax, we submit for fraternal consideration the following statement on income tax refusal.

Because the per capita U.S. military expenditure rose from less than $8 in to $268 in ,

Because approximately 75% of the Federal budget for the past several years has been annually appropriated for military purposes,

Because the government has been spending less than one million dollars yearly on the problems of disarmament, in contrast to $47 billion on arms, a ratio of one to forty-seven thousand,

Because there is so little national conscience about what nuclear war would mean for man, what it would be under God,

We find ourselves constrained by the love of Christ to refuse paying Federal income tax and instead are giving a corresponding amount, plus no less than 20%, to UN or other peacemaking programs.

We reject, as blasphemy against Christ, the prevailing readiness to exterminate hundreds of millions, or even all mankind, in order to “defend our values, our faith.”

Since modern technological warfare is much more dependent on huge amounts of money than on manpower, we believe that refusal to turn over our bodies is not enough; we can no longer turn over our dollars for the present rush t[o our] mass annihilation. Let West an[d East] really take total disarmament a[s our] goal, and not merely toy with it [under] the pressure of world public o[pinion] as till now.

We do not discount the cons[tructive] aspects of Federal activity, a[nd we] welcome governmental endeavo[rs that] do make for peace. But with t[he best] prospects for disarmament fadi[ng fast] and the population of East and [West] mostly unaware of the imminen[ce of] and the certainty of disaster if [these] policies continue, we are impe[lled to] income tax refusal as a way of [calling] others to hear God’s warning:

[“I have] set before you this day life and [good, and] death and evil. Therefore choo[se life,] that you and your descendant[s may] live, loving the Lord your God, [obey]ing his voice, and cleaving to [Him.”]

Those interested in discussi[ng this] difficult issue should write Dal[e] [Auk]erman, Bechlinghoven bei [?] Glueckstrasse 3, Germany. [Dale] Aukerman, John Forbes, and [Jerry] Royer.

That letter got an enthusiastic reply from Dale Rummel in the issue (source):

Church Should Take a Stand

I read the letter on “Taxes for War Purposes,” by Dale Aukerman, John Forbes, and Jerry Royer in [the] Gospel Messenger for [.

I] feel that they are trying, const[ruc]tively, to reach the answer [to the] problem that has been plaguing Christians since the two world wars.

I would like to see Annual Conference take action along the line[s of] their statement.

Our government can crush individuals when they take a stand which is “illegal.”

But if an organization like our whole Brotherhood took this stand and backed up [the] individuals who carried it out, [there] is much more chance for its [doing] some lasting good. I believe, [also] that if we take this stand [other] denominations will join us in it[.]

This is no time for the Brethren to become fearful and cowardly [and] be afraid to step forward and [go] where we know it is right to [go].

Let us, with God’s guidance, go [for]ward, regardless of the phy[sical] consequences, in what we know [is] right.

A note in the issue (source) said that the Michigan district conference had asked the Annual conference to “study the possibilities of making the pacifist movement a political force in our country” by, among other means:

Attempting to work out a proposal for an alternative tax arrangement, so that the taxes of those who object to war on conscientious grounds may be used for peaceful and constructive goals of government.

In the issue, J.

Robert Boyer encouraged his readers to take more courageous stands for their faith, and not like Peter deny Christ three times before the cock crows.

One example he gives of when one might take a stand: “Will you send your tax money to Cape Canaveral, where missiles are launched to kill the enemy?”

The following letter from Charles E. and Cleda P. Zunkel appeared in the issue (source):

No Tax for War Purposes

In keeping with our pronouncements concerning war, the last of which was made at the Annual Conference at Richmond, Va., we Brethren have encouraged our young men to seek alternative service, in lieu of military service.

Our young men, who have followed our teaching, have borne most of the brunt of this course of action.

Have we, their parents, kept faith with them, as we have continued to pay our income tax money, 75% of which has gone for the support of military preparedness and war? I think we have not.

Some of our young men have challenged us to action, by appealing to us to cease paying the 75% of our income tax which goes to military purposes.

It seems high time that we oldsters make our witness for peace, as we have asked our youth to make theirs.

My wife and I have been spurred to action by this appeal of our youth, and by the recent appeal of our President for $2 billion more to be added to an already staggering sum for military might.

The accompanying letter was sent to the Internal Revenue Service and to our President to clarify our position.

It seems to us that we are called upon to make clear our faith and our action, in keeping with our historic understanding of the life and teachings of our Lord.

Director of Internal Revenue,

Richmond, Virginia.

President John F. Kennedy

White House

Washington, D.C.

Dear Sirs:

Since the late 1920’s we have been conscientious objectors to war, in the settlement of international disputes.

We believe in the historic faith of our church, The Church of the Brethren, that “all war is sin.

We, therefore, cannot encourage, engage in, or willingly profit from armed conflict at home or abroad.

We cannot in the event of war accept military service or support the military machine in any capacity.”

Believing as we have, we have had guilty consciences as we have seen our nation increase its military preparedness.

We have been aware that approximately 75% of all our income tax money has been spent for war, preparation for war, or mainten[ance] of military might. In 1938 the [total] military expenditure was $8 [per] capita; in 1958 it had risen to [$268] per capita.

From time to time, as we [have] filed our income tax returns, we [have] in letters to the government, [pro]tested this use of our money. [We] suggested that there be some [pro]vision whereby these funds now [used] for military expenditures be used [for] peaceful pursuits, such as the fee[ding] of the hungry of the world [and] the aid to underprivileged [people] through technical assistance.

Thus far, our protests have [not] been regarded. On , our local newspaper carried the notice that you, President Kennedy, were asking for $2 [billion] more than the amount already [pro]posed for military defense, ma[king] a total asking of $43,794,300,000[.]

Recently, we learned that two [nu]clear scientists warned the Nat[ional] Education Association in its co[nven]tion that we in the United States already have enough manufact[ured] fissionable material to blot ou[t all] life from the face of the entire [earth] and leave it pock-marked and vo[id like] the face of the moon.

In all good conscience, we ca[n no] longer give 75% of our income [tax] money for the support of mil[itary] might.

We are not opposed to pa[ying] tax, but rather, to paying tax for [that] purpose.

We feel as guilty as if [we] were giving our lives in the pro[gram] of the military method of settling international disputes.

Therefore, we are filing our income tax report as usual, paying [the] full tax for , but paying [only] 25% of the tax due for the first [quarter] of 1961.

The other 75% of our [income] tax will be given in quarterly [install]ments to the church, in addition [to] the 15% or more we already [give.]

We hope the time may [speedily] come when such vast military expenditures may cease, and the [money] so spent may be used to relieve [the] suffering and need in our world.

[We] hope, further, that in the [mean] time some alternative tax plan [may] be worked out whereby conscientious objectors may give their [tax] money to peaceful pursuits, just [as] young men may serve in alternative service in lieu of the military service.

The Gospel Messenger editor, Kenneth Morse, endorsed peace protest in general in his editorial, and war tax resistance as one possible protest: “Consider also the personal decision of the moderator of Annual Conference and his wife with regard to taxation for war purposes… It is always easy to criticize the stand that others take. But please note that some have at least taken a stand.”

A response from Jack Kline, however, in the issue, took issue with tax resistance on the usual render-unto-Cæsar grounds (source): “I think it well to protest the high military expenditure.

But the type of letter that was written to Mr.

Kennedy and to the Internal Revenue Department I think does not show good grace.

I am a bit embarrassed that leaders in our own church would write that type of letter and refuse to pay taxes which our Lord distinctly told the Jews, under a military occupation, they should pay.”

There was another dissent, from John L.

Mohler, in the issue (source).

His objection was more on the grounds of democratic political theory: “[B]y participating on the economic life of our national community and accepting our incomes from it, we obligate ourselves to payment of the tax which, by democratic procedures, a majority of our citizens have imposed upon us.” Mohler felt that if you were going to conscientiously object to the taxes on your income, you should do so by refusing the income in the first place: “It seems to me that, in the case of refusal to pay taxes, the removal [of the dissenter from the democratically-chosen endeavors] should precede and prevent acceptance of the income on which the tax is paid.” But he didn’t think that was such a great idea either.

He felt that the tax resister’s quest to morally isolate himself from the decisions of the democratic polis was futile, and that he should instead accept his share of guilt for those decisions and begin from there.

On the other hand, Virgil Rose, in a letter in the issue (source) “was moved with deep spiritual elation” by the news of Brethren war tax resisters.

Rose tried to contradict some of the arguments against war tax resistance.

For example, the individual contribution to the modern war budget, he says, dwarfs the tiny head tax in Judea that Jesus spoke of, and so they cannot be directly compared; and the idea that he straightforwardly counseled the payment of a tax to Rome contradicts the whole point of the render-unto-Cæsar parable.

Rose also wasn’t impressed with Mohler’s democratic theory, though as I interpret it, it seems they were talking past each other on this point (Mohler responded in the issue).

His conclusion:

Let us not shrug off the pricks of conscience that disturb us as we witness the courageous decisions these Brethren are marking.

What defense have we before God if knowingly and without protest we supply money to buy instruments for the destruction of our fellow men?

Russ Montgomery also chimed in, in the issue (source). “I would like to congratulate [Charles Zunkel] on the courage to take such a stand.

When such bold action is taken by leaders it seems to make them worthy of the name.”

The issue brought an update about Maurice McCrackin (source):

Presbytery Suspends Minister Who Refused to Pay Income Tax

The Rev. Maurice F.

McCrackin, pacifist Presbyterian minister who for some twelve years has refused to pay a major portion of his income taxes, has been suspended indefinitely by the Cincinnati Presbytery from his ministry.

Mr.

McCrackin has been pastor of the West Cincinnati-St. Barnabas church, a racially integrated mission congregation supported jointly by the Cincinnati Presbytery and the Protestant Episcopal Diocese of Southern Ohio.

A spokesman for the Presbytery explained that Mr. McCrackin was suspended not for his stand on income taxes but for disobeying the law by ignoring a summons from the Internal Revenue Service, an offense for which he served a six-month prison sentence.

Many of the minister’s parishioners were reported sympathetic with his refusal to pay most of his income taxes on the ground that they were used for military purposes and that war is a sin.

The lead editorial in the issue (Morse again) again promoted conscientious tax resistance:

Just about the time that Valentine Byler, an Amish farmer in Pennsylvania, was ready to start his spring plowing, the Interal Revenue Service seized his three work horses and sold them at auction.

The reason was that Byler, who is conscientiously opposed to Social Security, had refused to pay a self-employment tax for that purpose.

Many members of the Amish sect regard Social Security as a form of insurance, and they are opposed to it. They have consistently refused to accept its benefits and do not take a Social Security number. While agreeing to the normal taxes on their property, they object to paying the Social Security tax required of farmers.

Thus we have another of those ironical situations in which the government finds itself [ba]nishing some of its most thrifty and self-reliant citizens.

Fortunately, as a result of the Byler case, several bills have now been introduced in Congress which would allow persons who are conscientiously opposed to Social Security to be excused from participating either in its support or its benefits.

We hope that some legal provision can be made for the benefit of those independent persons who have such scruples.

Many of us who would argue in favor of Social Security and even urge that it become available to more people still recognize the rights of conscience.

We respect the integrity of citizens who, like the Amish, may have some unique ideas as to how they contribute to the general welfare.

At the same time, is it not just as reasonable for the federal government to give some consideration to the scruples of citizens who are conscientiously opposed to paying taxes for war purposes?

A friend who is employed in the Treasury Department tells us it should not be too difficult for Congress to set up a general fund for nonmilitary purposes to which the tax payments of peace-minded citizens could be directed.

This would not satisfy all the concerns raised by taxprotesters, but it might at least provide an alternative more acceptable than the present arrangement.

A wise government should be able to find some way of conserving the conscientious contributions of citizens who cannot conform to policies they regard as wrong but who still desire to serve in constructive ways.

In the issue, an S.

Mohler (no idea if there’s any relation to the John Mohler referred to above) wrote in (source).

This letter began by saying that “in recent years I have read about a few Brethren suffering imprisonment for refusing to pay income taxes, because of the government’s military use of them.” I think this cannot be factually correct, as there were not very many Brethren war tax resisters at this point, and I don’t know of any who had yet been imprisoned for it.

Be that as it may, Mohler continues by saying that such “imprisonment for nonpayment of income taxes can be honorably and approvedly avoided” by increasing tax-deductible charitable contributions to the point where you do not owe taxes.

Mohler suggests that this is the method he or she has been using for “the past ten or fifteen years.”

Andrew R. Shelly, of the Board of Missions in the General Conference Mennonite Church, wrote in to second that suggestion, in the issue (source).

“Why should we not adjust our lives so that we can give very much more and at the same time materially reduce that which we pay directly to the war effort?”

(See ♇ 5 September and 9 September 2018 for Shelly’s contributions on this theme to the Mennonite Gospel Herald.)

The Brethren Evangelist was much more restrained in its coverage.

They did publish this wire service piece about Maurice McCrackin in the issue (source):

Presbytery Suspends Minister Who Wouldn’t Pay Income Taxes

Cincinnati, O. (EP)—

A pacifist Presbyterian minister who for some 12 years has refused to pay a major portion of his income taxes, has now been suspended indefinitely by the Cincinnati Presbytery.

The move not only halts his ministry but prevents his receiving communion in the church.

The Rev. Maurice F. McCrackin has been pastor of the West Cincinnati-St. Barnabas Church, a racially integrated mission congregation supported jointly by the Cincinnati Presbytery and the Protestant Episcopal Diocese of Southern Ohio.

An Episcopal diocese spokesman explained that although the mission is a co-operative project in its religious program, disciplinary jurisdiction rests with the Presbytery since Mr. McCrackin is an ordained Presbyterian clergyman.

A spokesman for the Presbytery said that Mr. McCrackin has appealed this suspension to the Presbyterian Synod of Ohio, but it was reported unofficially that his only hope for reinstatement would be a formal declaration to the Presbytery that he would pay his income taxes in the future.

It was explained that Mr. McCrackin was suspended not for his stand on income taxes, but for disobeying the law by ignoring a summons from the Internal Revenue Service, an offense for which he served a six-month prison sentence.

Presbytery has been studying the case for nearly a year.

I did not notice any mentions of war tax or war bond refusal in The Etownian, The Pilgrim, the Brethren Missionary Herald, or Bible Monitor in .

The war tax resistance debate raged in the letters-to-the-editor column of the Gospel Messenger in (though other Brethren periodicals ignored the issue entirely so far as I could see).

In one of the letters from that I noted yesterday, an S. Mohler had recommended that people who had conscientious scruples about contributing their taxes to military spending should increase their charitable giving to the point where they no longer owe taxes.

In the issue, Rollin E. Pepper threw some cold water on that suggestion (source), noting that the law limits the amount of charitable deductions that a taxpayer can claim.

The debate continued in the letters column of the issue, in which Charles W. Wampler said “it would be impossible to run a government allowing such action [tax resistance] by its citizens” (source).

I expect that if the government would allow people to pay tax only for the things that they approve the majority of the people would pay much less tax.

Some might even find excuses not to pay any tax.

Certainly no good Brethren would want to follow a course that would destroy our government even though it is not perfect.

A editorial from editor Kenneth Morse tried to put the critics of tax resistance on the defensive:

[Regarding] the stand taken several months ago by a Brethren minister who refuses to pay taxes to be used for war purposes.

Several of our readers were quick to disagree with him, but hardly any one came forth with a more constructive way of witnessing against the use of tax money for destruction.

You say you do not like the idea of tax refusal, mass demonstrations, or such public protests against the drift toward annihilation?

Then show us a better way to witness.

O.E. Gibson wrote in to the issue to promote civil disobedience against military taxation as a way of pressuring the government to accommodate such conscientious objection (source):

One Way God Works

May I sum up my thinking about one’s refusal to pay tax money to our government for the support of the big military build-up (one half to three fourths of the total of one’s income taxes assessed)?

Men bearing arms were the essential part of a war machine in all history up to within a few years ago.

But recently money has become the essential in plans using guided missiles, etc.

The government came to recognize the consciences of men who were unwilling to bear arms to take life only after some fearless ones were willing to defy the government and accept imprisonment to prove their convictions.

These men caused our laws to be changed.

What had been considered wrong came to be recognized as right.

For similar reasons it can hardly be expected that our government will change its laws to exempt money (allow it to be held back) without being morally forced to do so by conscientious objectors being willing to bear the consequences — probably imprisonment.

History, both Biblical and secular, has borne out this general principle — at critical times governments must be disobeyed if truth is to be vindicated and right standards more generally accepted.

This is one way that God works in history.

In the issue, a reader (whose name is unfortunately obscured in the page scan) wrote in to recommend that conscientious objectors to military taxation try voluntary simplicity instead (source).

Excerpts:

I believe those who wish to withhold income tax would admit that their “way of life,” materially speaking, is supported by the military economy.

I think a more constructive way, and the only consistent practice of withholding such money, is to reduce the standard of living, individually and voluntarily, to more of a subsistence level.

This would mean such a drastic reduction in salary that there would be no income tax due.

It would also mean revising our standards of living, materially speaking, such as mode of travel and home conveniences to what would be necessary if the military preparations and expenditures were suddenly and drastically curtailed.

The writer said that he himself lived economically, but he did not personally practice nor actually advocate this living-below-the-tax-line procedure.

He merely put it forward as being in his opinion more consistent than war tax resistance.

The debate continued to rage.

In the issue, [Jeanne?] Lee Jacoby wrote (source):

On Tax Refusal

I am a firm believer in the refusal to pay war taxes or, more appropriately, the percentage of income taxes which is used for war.

How many Brethren can conscientiously sit back and look at the missiles going up, wasting millions of our hard-earned dollars when there are so many other worthwhile projects for which we ought to be putting our money?

For example, why couldn’t the government use our percentage of the tax for the Peace Corps?

To me this is a wonderful experiment which I hope will continue for a long time.

Also, there are millions of tons of surplus food stored in our warehouses going to waste, and all that is needed is the money to send it to the starving people of the world.

Besides, if America needs allies so badly, there is no better way of obtaining them.…

How great is our concern?

Should we stand for something we know is wrong?

We refuse to bear arms.

Ought we consent to doing something like this which may prove to be even more destructive?

The General Brotherhood Board put forward a report on “the church’s historic peace position” in (source).

It tiptoed around the war tax resistance issue this way:

During the last few years, several voluntary agencies have been exploring with the government the possibility of an alternative tax arrangement.

The Brethren Service Commission has been working with the Friends and the Mennonites in the preparation of such a proposal.

We urge the Brethren Service Commission to continue its efforts to develop an acceptable proposal for an alternative tax arrangement.

Ralph Detrick announced his resistance in a letter published in the issue (source):

Caesar’s Due Portion

Following are excerpts from a recent letter I sent to President Kennedy, Senator William Proxmire, and the Internal Revenue Service.

I did not pay the $7.20 balance due on my income tax this year.… I protest the payment of a tax which supports the military machine and its false security.

There is nothing positive about the level of military involvement to which our country has devoted itself.

It is time to reverse this trend.

I take my stand in opposition to the direction our country is going and instead give my support to a peace-making organization.

I am sending $9.00 to the World Health Organization of the United Nations.… My voice may be small, but it is only when many such voices respond openly to the higher loyalty of God’s supreme law of love, that we as a nation may become a leader in peace rather than in weapons of war.

I often question the wisdom of this action.

I am ignorant of the long-range implications of this witness.

But where does the Christian draw the line at compromise?

Christians compromise out of necessity, and in some cases perhaps the ends justify the means.

Yet, there is also a great need for the person who tries to hold compromise at a minimum on certain issues in order that the plumb line of Christ may bring these issues into focus and reveal their evils.

When the federal budget is pitted against this plumb line, its evils — nuclear testing, the “military-industrial complex,” the waste created by Pentagon pressure — are revealed, creating an issue with which I do not wish to compromise.

Should the day arrive when Caesar’s budget becomes more in tune with God’s law of love, I shall be more than happy to render him his due portion.

A report on the annual conference, from the issue, reported (source):

William Smith, a representative on Standing Committee from Pennsylvania, expressed disappointment that the [General Brotherhood] board had not offered more help to persons who were disturbed by some of the issues involved in paying taxes to be used for war purposes.

Yet with one amendment, largely editorial in nature, the original statement [see above] was adopted by the delegate body.

In the issue, Charles Zunkel wrote in with an update on his family’s war tax resistance, and how they had backed out of it into more of a mild symbolic protest:

Witness by Designation

A little over a year ago, my wife and I decided we should refuse to pay the 75% of our federal income tax which was used for purposes of war.

We so announced to the Internal Revenue Department, the President of the U.S., and to our church through the Gospel Messenger. [see yesterday’s Picket Line]

Following that announcement, we had communication from the U.S. Treasury and the Department of Internal Revenue, and much with members of our own church and some other denominations.

All of the communications from the federal government were most considerate and courteous, a thing we did not always experience with our own Brethren.

The Department of Internal Revenue carefully acknowledged our conscientious scruples but reminded us that Mr. A.J. Muste had lost his case of conscientious tax refusal in the federal tax court, and urged us to pay ours.

In continuing correspondence we reaffirmed that we were not opposed to the payment of tax, but rather to the use to which it was put.

We asked if we might designate it for United Nations, Peace Corps, or Food for Relief, all of which are in the federal budget.

We were told that Internal Revenue did not have authority for the use of the tax money, but rather for its collection.

In discussing the matter with many friends and members of our families, we decided to test out the Internal Revenue on the designation of the tax money.

Accordingly, in paying our third quarter’s payment, we made one check for the 25% undesignated and for the 75% for three quarters, designated in the lower left-hand corner of the check — “For Peaceful purposes: U.N., Peace Corps, etc.”

The checks were cashed without any communication or question.

Since that, we have continued to write two checks, each quarter, designating the one in the fashion indicated.

We took this course of procedure, realizing that eventually the tax would be collected and with an additional 6% penalty.

The federal government will withdraw the tax due from the checking account, if funds are sufficient, or will confiscate property and sell it to secure the amount due.

Rather than make more money available for war purposes by confiscation and penalty, we decided to witness our protest by designated check.

Thus far, we have not tried to probe to discover whether the designated money was channeled as designated for United Nations, Peace Corps, etc. That we may still do at a later date.

We believe the witness can made by designation, at least until we can find some more effective way.

The issue reported on the General Assembly of the United Presbyterian Church in the U.S.A., including its decision to uphold the suspension of war tax resisting minister Maurice McCrackin (source).

I. Wayne Keller wrote in to the edition to decry the lawlessness of war tax resistance, and the Messenger’s “tacit, if not expressed approval” of it (source).

He wasn’t too fond of protests either:

“Carrying placards and walking in a public place are the methods of radicals, pressure groups, rioters, and anarchists.

Because they are, the Christian should not use them.”

Keller was joined by L. Wade Bollinger in the , who said that in a democracy “we the people are indeed ‘Caesar’ ” and so we should not be resisting our taxes but exercising our democratic franchise to help direct them (source).

Robert Fritter penned a lengthy rebuttal to these points of view in the issue (source).

Excerpt:

So aware were the early Christians of their primary loyalty to the laws of God rather than man’s laws when the two conflicted that for 300 years they were persecuted for disobeying the laws of the land.

They would not worship the emperor, nor would they take part in war.

They would not bow down to the military state because they knew that it was a stupendous and terrifying god of destruction which froze men into fearsome obedience while proclaiming to be their only salvation.

Those who refuse to pay income tax which feeds the insatiable hunger of this false god of 20th century America also refuse to pay homage to the same god.

A brief report on the Mennonite World Conference from the same issue (source) noted:

A Mennonite professor closed the conference with a speech in which he suggested that Christians who oppose the world power struggle and nuclear weapons might consider withholding payment of taxes which would be spent for military purposes. Dr. Edward G. Kaufman, professor of religion and philosophy at Bethel College in Kansas, said this would be an effective means of preventing nuclear war, but he conceded most people would not adopt his plan.

Harley J. Utter, in the issue, thought that war tax resisters were disregarding all of the nice non-military things the government spends our taxes on.

He also wasn’t a fan of protests: “show-off demonstrations are wrong, that is walks for peace and the like.” (source)

John Forbes wrote in to the same issue, saying in part:

“Thanks be to Bro. Charles Zunkel, whose witness against paying taxes for military purposes should inspire all of us to go and do likewise.”

After something of a lull in the mid-1960s, in the war tax resistance debate filled the pages of the Church of the Brethren’s Messenger magazine.

(Other Brethren periodicals were silent on the issue that year so far as I could tell.)

In the General Brotherhood Board decided it was time to polish up the peace witness of the Church of the Brethren.

And in preparation for this, it produced “a paper clarifying various stances on the payment of taxes for military uses… [which] cited various options now open and urged efforts to seek a further alternative for those who, because of conscience, oppose supporting war causes.” (source)

This included “urging the government to adopt a provision by which persons conscientiously opposed to paying taxes for military purposes may be granted some alternative, much as conscientious objection is permitted in draft legislation.”

On the matter of alternatives in the payment of federal income tax for war uses, a study committee report was presented and adopted by the General Brotherhood Board.

The report was prompted by various inquiries by Brethren, the most recent from the Pacific Southwest Conference board of administration.

The report enumerated as present options (1) paying the taxes, (2) attaching to the payment a statement of protest on the portion used for war purposes, (3) holding one’s income to a level not subject to taxation, and (4) refusing to pay all taxes or the portion of taxes used militarily, as a witness and a protest.

While not endorsing one alternative above another, the paper, like the proposed revision in the Annual Conference Statement on War, did recommend that efforts be made to secure tax laws permitting a constructive alternative to the payment of income taxes for war.

The board statement also proposed that publicity be given to such steps as the withholding of the federal telephone tax levied in support of the war in Vietnam.

Towards implementation, the board asked the administrative committee of the Brotherhood staff to study the implications of the paper and to bring subsequent proposals in .

One type of question raised by board members in discussion was whether the board itself, in its own operations, might withhold payment on the telephone tax.

A Brethren Peace Fellowship began to congeal, and in one of its early regional meetings: “At several points discussion centered on the possibilities for tax refusal and draft resistance and on proposing an Annual Conference statement on civil disobedience” (source).

The Annual Conference did end up putting out a statement based on the General Brotherhood Board’s recommendation (source):

Another new section deals with taxes for war purposes.

The statement on this point was amended in discussion on the floor of Conference to include a preliminary sentence indicating that although Brethren accept the need for paying taxes for constructive purposes, the church opposes the use of taxes by the government for war purposes and military expenditures.

Specific suggestions dealing with approaches to paying war taxes on the part of members were put in a permissive form, leaving the action to the conscience of the individual.

At the same time, churches and church-related institutions were urged to study the problem of paying taxes for war purposes and even to make a careful review of funds that they might possibly have invested in bonds that would support war.

The approach of civil disobedience is alive in our day.

Knowing that the telephone tax we pay finances the Vietnam war, some individuals do not include money in their payments for the federal tax.

They write across their bills, “No money for war,” or some similar statement.

A new surtax requiring ten percent additional tax money earmarked for Vietnam has been demanded by our government.

Some who believe that war is contrary to the will of God will question themselves, “Is it right to ask our young men to refuse to bear arms even if for some this may mean jail, if we as adults are willing to finance the devastation?”

The edition included an article that discussed the recent progress of the discussion about war tax resistance, and the search for a legal alternative, in the Church of the Brethren:

For the Christian pacifist, where is the conflict of loyalty to God and to the state felt more pervasively than in taxation?

And as the nation’s military expenditures skyrocket, persons of peace persuasion are moved to ask: If alternatives are allowable when it comes to putting one’s time and body on the military line, ought not a similar provision pertain to putting one’s taxes there?

The answer, as called for by a variety of concerned spokesmen, is for a legal, constructive, alternative tax arrangement for persons conscientiously opposed to paying taxes for war and military purposes.

The appeal for such a plan has been heard off and on for a quarter of a century.

For the Church of the Brethren, the matter came more sharply into focus when Annual Conference inserted in its Statement on War a section on taxes for war purposes.

Alternative use: “While the Church of the Brethren recognizes the responsibility of all citizens to pay taxes for the constructive purposes of government, we oppose the use of taxes by the government for war purposes and military expenditures,” the new section declared.

“For those who are conscientiously opposed to paying taxes for war purposes, the church seeks government provision for an alternative use of such money for peaceful, non-military purposes.”

The statement, recognizing that members will differ in their responses, cited four positions on the payment of federal taxes for war purposes which are evident:

to pay taxes willingly.

to pay the taxes but to express a protest to the government.

to refuse to pay all or part of the taxes as a witness and a protest.

to limit voluntarily one’s income or use of taxable services to a low enough level so as not to be subject to taxation.

To implement the concern, the Conference statement urged all members, congregations, institutions, and boards to pursue the matter with serious study and to act “in response to their study, to the leading of conscience, and to their understanding of the Christian faith.”

Dilemma: The appeal for study and action was prompted by concern over the “ever-growing portion” of the federal budget going for military purposes, according to a statement on “Taxes for War Purposes” adopted by the Brethren Service Commission .

The commission paper pointed up the dilemma which this escalation of war funds poses for “peace-minded people and conscientious objectors to war who put their trust in the power of love, non-violence, and international cooperation rather than military might.”

Sparked by a request from the Pacific Southwest Conference Board of Administration for a study of federal income tax alternatives, the Brethren Service study committee asserted that the church’s stance historically has been to oppose participation in war; at the same time it has taught responsible citizenship.

“The Christian should appreciate and support the worthy functions which government performs.

He should willingly obey the state in matters on which he has no contrary moral conviction.

On the other hand, he should be alert to occasions when government neglects or misuses its trust from God.

When he is profoundly convinced that God forbids what the state demands, it is his responsibility to express his convictions.

Such expression may include disobedience of the state,” the commission paper quoted from the Annual Conference statement on “Church, State, and Christian Citizenship.”

Pre-Vietnam: In its own background study the Brethren Service committee noted that while the nonpayment of taxes on conscientious grounds has been a movement of the past 25 years, the concern has “a long and honorable history.

Early Christians refused to pay taxes to Caesar’s pagan temple in Rome; many historic peace church members refused to pay taxes during the French and Indian wars, the Revolutionary War, and the Civil War; strugglers for independence in India, under Gandhi’s influence, refused to pay taxes to the British Empire.”

The study committee recounted a series of efforts which the Brethren Service Commission has made in seeking tax alternatives.

The General Brotherhood Board had urged explorations with government “to the end that an acceptable constructive alternative be provided for all those persons who, by reason of religious training and belief, conscientiously object to the payment of that portion of income taxes going for military defense.”

At Brethren Service’s initiative, representatives of eight peace agencies, each genuinely interested in seeking a suitable tax alternative, met in in Washington, D.C., for a strategy session.

The consensus was that there was little likelihood of the government’s providing a tax alternative until tax protestors and objectors created sufficient administrative difficulties that the government would decide it would be less vexing to provide a tax alternative.

Subsequent efforts by a follow-up committee and other efforts in liaison with the Mennonites and the Friends proved to no avail.

Legislators who had introduced measures calling for tax credits for contributions to the United Nations, which had been looked upon as possibly one alternative designation of tax funds, received little support from the public or from Congress for their proposals.

In a response to a related query the Annual Conference urged Brethren Service to continue efforts to develop an acceptable proposal for an alternative tax arrangement.

According to the study committee, all efforts to date have failed to find or gain sufficient support for a tax law provision or administrative formula that would satisfy Congress, the Bureau of Internal Revenue, and conscientious objectors.

Wider forum: For the next step, the appeal of Annual Conference and of the Brethren Service Commission is for the question on the payment of taxes for war purposes to receive a wider airing among members and congregations.

Copies of two major resource items, “Statement on War” and “Taxes for War Purposes,” were mailed in to pastors and to Witness and Brethren Service chairmen.

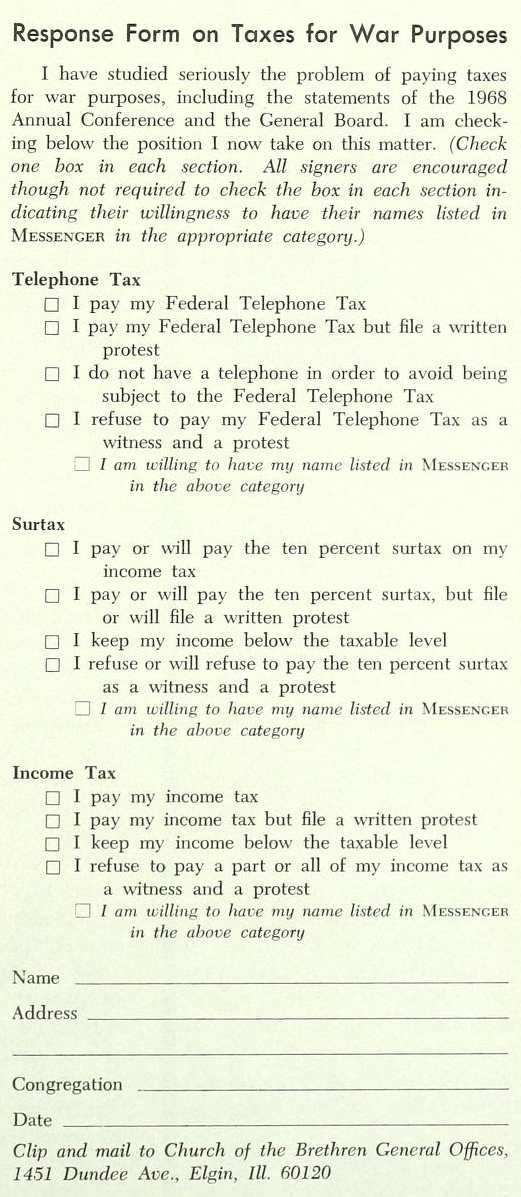

The issue of Messenger [see below] will feature a symposium with spokesmen for each of the four stances on the handling of tax payments.

A response coupon in the same issue will enable readers to report their own stand on the payment of three taxes used heavily for war use, the federal excise tax on telephone service, the recent ten percent surtax on income tax, and the income tax itself.

The names of persons willing to have their positions identified may be published.

Readers also are invited to submit letters to Readers Write to share testimonies and viewpoints on the matter.

Institutions and boards are likewise asked to study the payment of war taxes.

The General Board, through its Administrative Committee is examining the implications at the denominational level.

Ralph E. Smeltzer, who is coordinating the study emphasis, stressed the hope “that individuals, classes, study groups church boards, congregations, and all church institutions and related boards will come to their own thought-out positions.”

Accompanying that article was this sidebar, taken from the statement on “Taxes for War Purposes”:

Paying war taxes

Present positions

Four Positions on the payment of federal taxes for war purposes are evident:

Payment of taxes.

Persons who favor the government’s war and military policies willingly pay their taxes for these purposes.

Other taxpayers judge the constructive functions of government to outweigh the unacceptable activities.

Others feel that responsible citizenship requires the payment of all taxes.

Some who oppose the use of taxes for war feel that the risks and efforts involved in opposing such use of taxes are not worth the negligible results.

Payment of taxes under protest.

Persons who follow this alternative usually file a letter with appropriate government officials protesting the use of any of their tax money for war purposes or military expenditures.

Frequently they urge the government to use their tax money only for peaceful and constructive purposes…

Sometimes such persons ask government leaders to amend the nation’s tax laws, especially the income tax law, to provide an alternative opportunity… to designate the use of their tax dollars for peaceful and constructive purposes either through United States government functions or United Nations operations.

Limitation of income or use of service to nontaxable level.

Some persons are led by their consciences to limit voluntarily their income to such a low level that it will not be subject to federal taxation for war purposes.

Likewise they may not install a telephone or use other services which are subject to similar federal taxation.

They may endeavor to avoid participating in all those aspects of economic life which contribute to or support war and military operations…

Nonpayment of taxes or portions thereof.

Persons who follow this alternative refuse to pay all or part of the taxes asked by the government.

They engage in this form of civil disobedience because they conscientiously object to the use of their money by the government for war or military purposes and because they want to make a more vigorous protest against the government’s war policy and military policy.

Sometimes these persons contribute an equal amount to the United Nations or a private peace agency as a positive witness to their position.

The Federal Income Tax and the Federal Telephone Tax are presently the taxes most frequently refused by conscientious objectors.

Refusal to pay such taxes might possibly be considered a violation of Internal Revenue Code, Section 7203, which would be a misdemeanor subject to a fine up to $10,000 and jail up to one year.

However, the experiences of conscientious objectors to federal taxes for war purposes during the past several years indicate that the government is not interested in pressing possible criminal charges but in trying to collect the taxes here or there with interest.

The Internal Revenue Service usually attaches the salary or bank account of the nonpayer and collects the tax plus six percent interest from the date the tax was due.

The nonpayment of the Federal Income Tax or portion thereof is carried out by those who have payment control over all or part of their income tax return and who refuses to pay all or a portion of the money owed.

The nonpayment of the Federal Telephone Tax or a portion thereof is carried out by refusing to pay that part of one's monthly telephone bill and sending with each remittance a written explanation of why that portion is not included.

Telephone companies have indicated that refusal to pay this tax will not result in interruption of telephone service.

Telephone companies turn over to the Internal Revenue Sendee the responsibility for collecting such unpaid taxes.

The phone company treats refusal as a matter between the customer and the government.

Some companies continue to carry the refused tax on the telephone bill as an “unpaid balance,” others do not.

The issue asked four authors to each give his perspective on the war tax issue (“Debaters of the war tax question include Russell V. Bollinger, dean of students at Manchester College in Indiana; Charles E. Zunkel, pastor of the Crest Manor church, South Bend, Indiana; David B. Rittenhouse, pastor of several congregations in West Virginia; and William Faw, pastor of the Douglas Park church in Chicago”) and included a survey readers could fill out and send in to the Messenger in which they could say which action they were taking:

In recent actions of Annual Conference and of the General Board, members of the church have been urged to study seriously the problem of paying taxes used for war purposes and to act in response to their study.

The church recognizes that its members will believe and act differently in regard to the payment of taxes when a significant percentage goes for war purposes and military expenditures.

Four major positions on the payment of federal taxes for war purposes are evident:

Some will pay the taxes willingly; some will pay the taxes but express a protest to the government; some will voluntarily limit their incomes or use of taxable services to a low enough level so that they are not subject to federal taxation; and some will refuse to pay all or part of the taxes as a witness and a protest.

As an aid to discussion and action Messenger has invited four spokesmen to comment on these alternative positions.

There is also a response form that may be used individually or by groups to indicate how readers stand on this controversial topic. ―Editor

Why I Pay Taxes Used for War Purposes

by Russell V. Bollinger

Though I write in defense of the first position, namely, that the Christian ought to pay his taxes willingly, it should be clear that I have no objection to the second, which adds only some form of verbal or written protest against the defense budget.

Those who take the third position seem to me to be evading the issue.

They resolve their personal dilemma by abdicating their responsibility to society.

The fourth position constitutes an abdication of personal responsibility in an attempt to correct a social evil.

It should be very clear that I share and have always supported the Brethren peace position, which can be amply documented from the New Testament.

Under debate here are particular forms of protest or obstruction against war.

Such forms of protest, like all actions of Christians and of the church, must be tested against what Jesus both said and did.

In order to identify and to underscore some basic considerations affecting this discussion, it seems to me necessary to examine an assumption on which many such actions as tax withholding have been proposed and some implemented.

Considerable promotion has been given, for example, to the slogan, “Government Is the Christian’s Business.”

I have always objected strenuously to this concept, especially to its adoption as a slogan.

At best, the statement is misleading; at its worst it grossly distorts the Christian’s concept of his central task.

Government is the citizen’s business, whether he be Christian, Jew, or pagan.

To be sure, the Christian’s citizenship will be exercised in the light of his faith — but never as the central or major focus of his activity as a Christian.

He has accepted an enormously more urgent and significant “business” — to order his own life after Jesus’ teaching and example and to strive to win others to the same commitment.

Whatever the Christian’s proper role in government, it must always be secondary among his priorities.

Otherwise, it must seem strange that Jesus and Paul so clearly advised subjection to civil government, at least in all ordinary circumstances, and do not appear to have spent time or energy attempting to reform or even influence a very corrupt government at Rome.

I propose, under the foregoing assumptions, two considerations which for me justify willing payment of taxes, even if portions of the tax budget go for objectionable purposes.

First, it is a matter of reasonable doubt whether any government could long operate under a system by which tax paying is made subject to the range of possible “conscientious” objections to selected government activities.

Let us suppose that such groups as the Amish were to withhold that portion of their taxes which goes to support all education beyond the common school.

They declare opposition to secondary and higher education on grounds of conscience.

Suppose all Christian Scientists were to withhold a percentage of their taxes allotted to medical research and facilities.

Suppose we Brethren were to withhold taxes because welfare funds are sometimes so administered as to endanger or destroy normal family life or because Department of Agriculture funds are paid to large-scale farmers for nonproduction of food and fiber.

These and many more may with equal logic be considered matters of conscientious objection.

Happily, under our system of government, we have ample opportunity to present and defend other points of view, but the democratic social theory neither contemplates nor condones obstructionism.

There is reason to question whether Brethren leaders can support tax withholding with integrity while at the same time they discourage “designated giving” to the Brotherhood budget.

If churchmen be urged to support the total church budget, without discrimination, but citizens be exhorted to support only such governmental budget items as they can approve in good conscience, we may ask whether tax withholding is supported in principle or only opportunistically, as a strategy.

It is surely axiomatic that all forms of human association are possible only because of some surrender of personal freedoms and preferences.

Since in our society we have adequate legal, educational, and constitutional avenues for expressing our views to government, to withhold taxes for what we happen to disapprove (and who can differentiate between “conscientious,” philosophical, emotional, and mystical disapproval?) comes perilously close to asking for the benefits of government while shirking its responsibilities.

In short, the proposal to withhold all or a part of one’s tax obligations for reasons of individual or corporate conscience must be conceded to contribute to a fragmentation of society that tends toward anarchy.

Second, tax withholding on whatever grounds with the purpose of preventing selected government activity is essentially a method of force which Brethren in particular should reject.

All attempts to change the behavior, attitudes, or values of mature, responsible persons by force are degrading and destructive of personhood.

There seems to be no point in arguing that the purpose of such withholding is simply a symbolic form of protest.

Kant’s categorical imperative in ethics tests a proposed act in terms of whether it could be universalized.

Since tax withholding quite obviously cannot be universalized without destroying government, it clearly suffers by such an ethical criterion.

No thoughtful observer of the contemporary scene can deny a trend toward the substitution of force for persuasion, of compulsion for rational debate, to bring about social change.

The civil rights movement, the student protests, the Poor Peoples’ Campaign in some of its expressions and slogans are illustrations.

The church seems in imminent danger of succumbing to this trend, although it is both unworthy and out of character for Christians.

The ultimate indictment of the method of force is of course that it cannot succeed except in appearance.

An attack on the war system ought to proceed by using available means to demonstrate its futility, its ineffectiveness, and its immorality — none of which ends tax withholding can serve.

At most it seems a crude and primitive way of attracting attention to one’s cause.

From time to time the Christian, as a citizen, may properly make representation to government concerning his views, his desires, and his concerns.

Our impatience to reconstruct the world after our own particular blueprint must not lead us into betraying noble ends by the use of unworthy means.

Why I Pay the War Tax Under Protest

by Charles E. Zunkel

In order to be consistent the conscientious objector to war must face the whole range of his involvement with war.

In addition to participation in the military is certainly his concern for the use of his tax money for military purposes.

This is especially true now that so much of one’s income tax is being used for war.

When my wife and I came clearly to this conviction in and decided that we must do something about it, I wrote the Department of Internal Revenue, sharing copies of my letter with the President and declaring our concern and our intention to refuse payment of the percentage of our income tax which would be used for war [see ♇ 31 May 2020].

I made it quite clear that we were not unwilling to pay the tax, but we were objecting to its being used for war.

We wanted it used for constructive, peaceful purposes.

I received a very courteous reply, reiterating my words, but advising us and urging us to pay the tax.

I then wrote, asking if we could pay this percentage for the United Nations, Food for Relief, or Peace Corps, programs of the federal government which we considered peaceful and worthy.

Internal Revenue replied that it was not in their province to disperse the funds, only to collect them.

In the meantime, I conferred with one who had refused to pay the income tax and learned that, if we did not pay, the tax would be collected by taking it from our bank or savings account or by confiscation and selling personal property.

An additional penalty of five percent would be imposed.

We decided we did not want to provide the extra five percent for war to carry out our refusal, when the tax would eventually be collected anyway.

Instead, we decided to write two checks each time, one designated for “peaceful purposes: United Nations, Food for Relief, Peace Corps,” in the percentage amount of the federal taxes for war.

The other for the remaining percentage amount we marked “undesignated.”

Since the federal government has the power to use the tax money as it wishes, not as we may designate, the checks were cashed and no comment was or ever has been given.

Periodically to accompany the checks I have written letters voicing our concern and protest to the President and the Secretary of State.

While this method does not keep our money from supporting war, it seems to us the only viable way for us to protest, since we earn enough to have to pay the tax and since we do not want the added five percent penalty to provide more funds for war.

If enough persons or families used this method and the process became publicized, it would be an educational program which might build conscience in others and eventually lead to the provision for tax exemption of the sort we now have for military service.

Legislative bills have been prepared for this purpose but have not been introduced because the lack of public support would assure their defeat.

In the meantime, we would hope that the Brethren, Mennonites, Friends, and others concerned might send to the President a delegation asking for tax alternatives, as was done to secure an alternative to military service.

Regarding the surtax or the telephone excise tax, we believe that, because these are small enough amounts of one’s total tax and that they are clearly all for war purposes, they can and should be refused, even though the five percent penalty will be added and they will be collected.

Education could win sufficient popular support for objectors to war tax payment and make possible the passage of legislation that will provide alternatives for the worthy use of tax money which would otherwise be spent to support war.

Keep Income Below the Taxable Level

by David Rittenhouse

While serving in BVS 1-W Program, Merle Grouse, a fellow BVSer, and I were traveling by train from Turkey to Germany.

During an all-night ride through Yugoslavia, we talked with a young Yugoslavian who said that he had been taught that capitalism could not exist without war.

In all innocence we strongly disagreed.

During , the Church of the Brethren sponsored a work camp in Altoona, Pennsylvania, for the unemployed after the railroad shops changed from steam to diesel.

There, at the end of a hot summer day, a group of men sat on the steps talking about their hope for a job.

One remarked, “I guess we will have to wait for another war before we get work.”

So it is that with the event of the Vietnam War and the resulting defense contracts, we are forced to admit that which some had suspected.

Though I do not believe that this war economy is the inevitable result of capitalism, the war is definitely with us, even if not by design.

It is high time that vocal Brethren pacifists be called to attention by our consciences about our direct involvement in war through taxes.

It has been a natural temptation, when Christian ethics are frustrated by the real world in which we live, to turn inward in an attempt at individual purification and character refinement as a goal that is within reach.

I do not in any sense want to encourage this type of denial of the implications of Christ’s teachings, for we must accept the fact that we cannot disassociate ourselves from the economy in which we live.

In all our expressions of protest there must still be the humble recognition that the curse of Habakkuk is there: “Woe unto him who builds a city on blood.”

But there are ways in which individual citizens can exercise freedom of belief as persons.

Living on a limited income is one of these forms of witness.

Voluntarily limiting one’s income requires us to reevaluate our standard of values.

We are encouraged to find satisfaction in meaningful activity instead of in possession of things.

It is in keeping with the Christian concept that persons and beliefs are more important than property.