How you can resist funding the government →

a survey of tactics of historical tax resistance campaigns →

manufacture & sell alternatives to taxed goods →

underground economy →

size of, impact on tax gap

P.S. There’s a good article that was posted to AlterNet called “War Tax Resistance Made Simple.” It talks about the various forms of tax resistance — from going on strike like I’m doing, to filing “zero returns” or blank forms, to symbolic withholding of some portion of what is demanded, to resisting a particular excise tax (for instance the federal phone bill tax).

I also found an older AlterNet article today on “The ‘New’ Economy” that is an interesting look at the underground, or “shadow” economy:

The National Center for Policy Analysis points out: “Economists estimate that as many as 25 million Americans earn a large part of their income from underground activities.”

While economists have long estimated that the U.S. underground economy equals about 10 percent of the gross domestic product (GDP), there are reasons to believe the number may be larger.

According to a recent International Monetary Fund survey of 21 countries, the shadow economy has been growing for 30 years — the fastest in — doubling from less than 10 percent of the GDP in to 20 percent or more by .

“In the United States, for example, the shadow economy doubled from 4 percent of GDP in to 9 percent in ,” according to IMF.

But the Internal Revenue Service is taking a dim view.

The IRS recently estimated that the federal government is losing $195 billion per year in revenue due to underground activity — both legal and illegal.

In addition, it estimates the underground economy is anywhere from 3 to 40 percent of the above ground economy.

Once a quaint way to spend Saturday afternoon, flea-marketing has found its place in an emerging “social economy” that is supporting those on the lower rungs of the American economy, say experts.

These days, 1 in 7 Americans relies on this informal economy…

¶

The growth of that “informal economy” has increased the amount of cash in circulation per American from $1,105 in to $2,455 in — and untaxed goods account for some 10 percent of the gross national product…

The National Taxpayer Advocate reports to Congress each year on the state of the tax system and the burden on the taxpayer.

The latest report, released today, includes some tidbits about the underground economy, sources of the tax gap, and unkind enforcement follies like this one:

Criminal Investigation Refund Freezes.

The IRS Criminal Investigation function (CI), through its Questionable Refund Program (QRP), places a “freeze” on hundreds of thousands of refund claims each year that it believes may contain indicia of fraud.

CI personnel currently review the refund claims and “determine” whether they are fraudulent — without notifying taxpayers that their claims are under review and without giving taxpayers an opportunity to present documentation supporting their positions.

, the Taxpayer Advocate Service (TAS) received more than 28,000 requests for assistance from taxpayers whose refunds had been frozen.

TAS studied a randomly selected sample of nearly 500 cases to determine the ultimate disposition of these cases.

When TAS assisted the taxpayers, CI ultimately agreed to issue the full amount of the refund claimed (or more) in 66 percent of the decided cases and to issue a partial refund in an additional 14 percent of the decided cases.

Thus, taxpayers received a full or partial refund in 80 percent of frozen-refund cases brought to TAS.

The median Adjusted Gross Income (AGI) of these taxpayers was $13,330, and the median refund was $3,519. Thus, the refund constituted, on average, more than 26 percent of the claimant’s AGI for the year, and the taxpayers were required to wait, on average, more than 8½ months to receive their refunds.

The National Taxpayer Advocate believes that the QRP is an important program to protect against tax fraud, but the IRS must implement procedures to notify taxpayers that their refunds have been frozen, provide taxpayers with an opportunity to submit documentation, and bring cases to a quicker resolution.

This certainly affects those of us using the DON Method of tax resistance — particularly those of us who rely on getting our refunds before April 15th so we can make an IRA deposit in time to declare it on the previous year’s return.

The report also notes:

The Cash Economy.

Underreported income (and related self-employment tax) from the so-called “cash economy” is probably the single largest component of the “tax gap.”

It may exceed $100 billion per year.

Because income from the cash economy is not subject to information reporting, many of the IRS’s traditional means of enforcement are unlikely to be effective in addressing it.

The IRS has a number of initiatives that could be effective if coordinated and pursued more aggressively.

However, no single function coordinates research, outreach, and compliance initiatives aimed at improving reporting compliance among cash economy participants.

Nor does the IRS give these initiatives the same level of attention as other initiatives, such as those addressing tax shelters or the Earned Income Tax Credit (EITC).

The IRS must develop a comprehensive strategy for addressing the cash economy if it is to significantly reduce the tax gap.

Expanding on this summary, the full report says:

According to the IRS, taxpayers report:

99 percent of the income subject to withholding (e.g., wages),

96 percent of the income subject to third-party information reporting (e.g., interest), and

68 percent of the income not subject to withholding or information reporting (e.g., inventory sales proceeds).

This percentage drops to 20 percent for income earned by certain sole proprietors (called “informal suppliers”) who operate “off the books” on a cash basis in areas such as street vending, door-to-door sales or moonlighting in a trade or profession.…

The IRS has no direct estimate of the portion of the tax gap attributable to the so called “cash economy.”

However, according to IRS estimates:

More than 60 percent of the tax gap is attributable to self-employed individuals.

Eighty percent of the tax gap is attributable to underreporting of tax.

About 43 percent of the tax gap, $134 billion to $155 billion, is attributable to underreporting by self-employed individuals.

Over 80 percent of all individual underreporting is attributable to understated income rather than overstated deductions.

These estimates suggest that self-employed taxpayers who file returns but underreport their income (or self-employment taxes) represent the single largest component of the tax gap, accounting for more than a third of the gap and over $100 billion per year.

Further, the IRS’s estimates may understate the portions of the tax gap attributable to the cash economy because such noncompliance is inherently difficult to detect.

Taxpayers, including the self-employed, primarily underreport income that is not subject to third-party information reporting, i.e., income earned in the cash economy.

Practitioners confirm that the IRS is frequently unable to deter or detect underreporting among cash economy participants.

Research suggests that the cash economy is growing.

According to one estimate the “underground economy,” which includes both the cash economy and illegal activities, increased from four percent of the U.S. Gross National Product in to nine percent in .

A recent study suggests that between nine and 29 percent of the workers in Los Angeles County California are paid in cash and do not have federal or state payroll taxes withheld.

The cash economy may grow even faster as cash transactions move to the Internet.

To address some of this, the Advocate’s office suggests:

Measures to Reduce Noncompliance in the Cash Economy.

The IRS estimates that the annual federal tax gap for was between $257 billion and $298 billion.

The IRS receives about 130 million income tax returns each year.

Thus, every taxpayer is forced to pay an average $2,000 “surtax” each year to subsidize noncompliance.

IRS data show that the highest rate of noncompliance by far is attributable to transactions that are not reported to the IRS on a Form W-2, Form 1099, Schedule K-1, or similar form.

These unreported transactions occur largely in the so-called “cash economy.”

To reduce the tax burden on compliant taxpayers, we recommend that Congress (1) create a three-pronged reporting and payment system that encourages compliance in certain cash economy transactions by (a) instituting backup withholding on payments to taxpayers who have demonstrated “substantial noncompliance”; (b) releasing backup withholding on payments to “substantially noncompliant” taxpayers who have demonstrated “substantial compliance” and agree to schedule and make future estimated tax payments through the IRS Electronic Funds Transfer Payment System (EFTPS); and (c) providing that payors will not be required to institute backup withholding on payments to independent contractors that present payors with a valid IRS “compliance certificate”; (2) require the IRS to promote the making of estimated tax payments through EFTPS; (3) authorize voluntary withholding agreements between independent contractors and service recipients; and (4) require third-party information reporting for certain payments to corporations with 50 or fewer shareholders.

Probably easier said than done, but I wouldn’t be at all surprised to see some moves in this direction.

Another tax-gap source mentioned in the report is misreporting capital gains and losses on the sale of stocks and mutual funds.

Apparently there is no reliable reporting mechanism for the price at which an investor buys such a thing (the “basis”), so when the taxpayer reports the difference between the sale price and the purchase price, the IRS has to either take it on faith or perform a full-scale audit to force the taxpayer to cough up documentation:

Many financial institutions through which investors own stocks and mutual funds (“brokers”) do not currently keep track of an investor’s basis in the stocks or mutual funds, and no brokers report basis information to both taxpayers and the IRS on a Form 1099-B.

The absence of information reporting creates serious problems for many taxpayers and the government alike.

For taxpayers, tracking basis can be extraordinarily complex and many taxpayers seeking to comply with the law find that they simply cannot do so with accuracy, leaving them exposed if audited.

From the government’s perspective, the absence of information reporting enables underreporting by taxpayers who deliberately overstate their basis (thereby reducing their gain or even generating a loss), because they know the IRS generally cannot detect errors in basis reporting in the absence of an audit.

One recent estimate puts the revenue loss to the government from such underreporting at $250 billion over the next 10 years.

Sudhir Alladi Venkatesh explores the underground economy of Chicago’s South Side, in The Boston Globe’s Field Notes from the Underground:

Most of us could probably identify hidden economic activity in our own communities and indeed in our own homes.

Inner cities have their crack dealers, but the shady economy can also include kids selling lemonade, bars that host poker games, carpenters who work under the table, neighbors who offer day care.

In fact, trying to uncover each and every unregulated exchange would seem implausible.

Academics and policymakers continue to try, however, in large part because the costs of unregulated and hidden economies are so high.

The tax coffers are depleted when income is not reported.

Many underground workers are working for less than minimum wage, and most are failing to report their income.

And when we throw in drugs, sex work, and guns, we are of course forced to consider even greater social problems.

How big is the underground economy?

The General Accounting Office and the Internal Revenue Service produce estimates every few years that differ widely, but one government study calculated that $500 billion in income fails to be reported each year.

Another estimate, based on consumer behavior, suggests that 4 out of 5 Americans turn to the unregulated world for goods and services which would raise the $500 billion figure appreciably.

But the underground economy is more than just a set of cash transactions.

Cash, as it turns out, isn’t necessarily the preferred medium of exchange: on Chicago’s South Side, barter is just as common.

I interviewed the owner of an auto body shop who threw out his cash register because customers were paying their bills in kind.

They offered him cellphones, microwaves, furniture, and IOUs. He, in turn, started selling these goods from the back of the store, and now auto repair constitutes only a fraction of his income.

Venkatesh, author of Off the Books: The Underground Economy of the Urban Poor, observes how these oases of underground economy interact with the above-ground economy and the government that is parasitic on it and jealous of its competitors.

“Watching how these communities self-regulate,” for instance through real-life mutually-acceptable private mediators of the sort often found in theoretical anarchist literature, “I witnessed sophistication and creativity not usually associated with neighborhoods of concentrated poverty.”

The “tax gap” — the difference between what the law requires taxpayers to pay and what they actually fork over — is usually reported as being about $300 billion.

This number is based on a study, which in turn extrapolates from the results of earlier surveys.

The numbers are stale, and weren’t all that good to begin with, but they’re about all we have.

A new report from the IRS shows how they plan to address this gap and to obtain fresher figures.

One thing I noted while skimming through the report is that although the tax gap estimate does include taxes due on income from the “underground economy,” it apparently does not include income from that part of the underground economy that is itself illegal (such as the drug trade):

…IRS estimates of the tax gap are associated with the legal sector of the economy only.

Although tax is due on income from whatever source derived, legal or illegal, the tax attributable to income earned from illegal activities is extremely difficult to estimate.

The gist of his argument is that the various informal social norms and standards by which people come to arrangements — without having to draw up contracts or seek mediation by authorities — are quite valuable things.

Because they are valuable things, when people rely on them in social situations, they are exchanging things of value without reporting this to the tax authorities and thus the State is missing out on lots of money.

One example of this shady underground economy of social norms is the one that is reported to exist in rural Shasta County.

Don’t read this before bedtime if you’re prone to nightmares:

[Shasta County’s] farmers and ranchers build their relationships not by reference to their legal rights and obligations, but by relying on longstanding and pervasive norms of neighborliness.

Neighbors help neighbors build, inspect, and repair fences, retrieve stray cattle, maintain the water supply, execute controlled burns, staff volunteer fire departments, and so on.

They do not ask each other for payments, they do not enter into contracts, and they reject out of hand the idea of calling lawyers every time they do not like something their neighbors have done.

Shasta County’s system of social control is built on shared understandings that are always unwritten, almost always unstated, and frequently unsupported by (or even contrary to) the relevant legal rules.

The world is clearly an uglier place than anybody knew, but Alex Raskolnikov has opened our eyes.

Worse: “Shasta County is anything but unique.

Researchers studying everyday commercial interactions have found similar informal practices everywhere they looked.”

…Shasta County inhabitants routinely engage in all sorts of commercial transactions that, if formalized, would produce tax consequences for one or both parties.

Neighbors borrow (“rent,” in tax speak) each other’s equipment.

They help each other with chores such as fence building and maintenance; that is, they provide services to each other.

Occasionally, one neighbor supplies the other with building materials for a joint project.

For tax purposes, this transfer may be characterized as a sale, depending on the circumstances.

Even this cursory analysis suggests that in the world of neighbors helping neighbors, one thing they may help each other do is reduce their tax liabilities.

In conclusion:

Social welfare would be improved if the government could cheaply identify these norms and start treating them as legally binding contractual terms for tax purposes.

How would this improve social welfare?

Norm-based transactions allow taxpayers to reduce their tax burden, in effect shifting it to other taxpayers.

The new law [one that would treat all of these norms as though they were formal contractual agreements, and tax them as such] will reduce these undesirable effects, that is, it will diminish the cost of norms.

In other words, by taxing the norms, you diminish their cost (you know, to society).

For various reasons, though, it would be impractical and possibly even undesirable for the government to identify and formalize all such norms.

For this reason, Raskolnikov suggests that the government use some heuristics to identify a subset of those norms that is likely to mask economic transactions with the potential for a big tax bite.

So the informal norms in Shasta County are safe… for now.

“To be sure, these dealings sometimes allow inhabitants to reduce their tax liabilities, but there are good reasons to accept this cost and move on.”

How’s that IRS private debt collection agency program going?

Let’s ask the National Taxpayer Advocate:

It is not meeting revenue projections.

It is not more successful than the IRS at finding hard-to-locate taxpayers.

It is significantly less successful than IRS employees at fully resolving taxpayer past due accounts.

And:

The I.R.S. had expected private companies to collect $88 million but has now lowered that to as little as $23 million.

The collectors are paid almost a fourth of the money they bring in.

When the costs of government oversight are added in, [National Taxpayer Advocate Nina E. Olson] said, the program may even lose money.

Indeed:

Significantly, and contrary to projections made as recently as in , the expenses of the program to date exceed the revenue the program has generated.

“The cash economy is growing.

The percentage of all income subject to third party information reporting fell from 91.3 percent in to 81.6 percent in .

Moreover, the IRS expects the number of individual returns from small business or self-employed taxpayers to grow by about 33 percent , while the number of individual returns from other taxpayers is expected to decline by about 2 percent over the same period.”

, the IRS assessed $10 million in penalties against professional tax preparers for various forms of preparer misconduct.

But the agency only managed to collect $2 million of this $10 million.

It seems that tax preparers know the difference between a dog bark and a dog bite.

For tax year , the IRS identified more than 1.2 million cases in which someone failed to file a tax return even though they had taxable income.

In cases like these, the IRS creates a substitute tax return for the person, which (usually) results in a “default assessment.”

But, “the IRS collected just under two percent of the taxes assessed through the automated process, a sign that this method is not increasing filing and payment compliance.”

The IRS responds: “We… do not agree with the suggestion that dollars collected is the best measure of the effectiveness of these assessments.

Each assessment abated or adjusted reflects the submission of a return or other response by the taxpayer after the ASFR default assessment has been made — a clear indication <voice="darth vader">the taxpayer has been successfully brought into compliance</voice>.”

“A disregarded entity is a single member Limited Liability Company (LLC) that has not elected to be classified as a corporation.

It is called a disregarded entity because the owner reports business activity as if the entity did not exist.

For example, if the single member is an individual taxpayer, (LLC transactions are reported on the owner’s Form 1040 as if it is a sole proprietorship.

The compliance detection issue results from the owner of a disregarded entity using the tax identification number of an entity that does not have a filing requirement.

The IRS document matching program cannot match the disregarded entity income with the true owner and the income may go unreported.)”

“The earnings of an S corporation are taxed as ordinary income to its shareholders.

Unlike partnership or sole proprietor earnings, however, S corporation earnings are not subject to self-employment tax.

This difference in treatment gave rise to a tax planning strategy that treats shareholder compensation payments as distributions of profit to avoid payroll taxes.

Under this approach, officer/shareholders take no salary or a nominal salary and receive the remaining compensation as tax-free distributions.

The corporation saves payroll taxes and the shareholder ultimately pays only income taxes on his or her share of the corporate profits and avoids paying Social Security and Medicare taxes.”

However… “the IRS has repeatedly challenged and won the shareholder wage issue in court, [but] it is still used as a tax planning strategy.”

The IRS reported 18% more “Taxpayer Delinquent Accounts” in than in .

81% of these accounts involved tax years before , and many are “inactive.”

The Taxpayer Advocate purports to believe the following:

The United States tax system is based on a social contract between the government and its taxpayers — taxpayers agree to report and pay the taxes they owe and the government agrees to provide the service and oversight necessary to ensure that taxpayers can and will do so.

Without that unspoken agreement, tax administration in a modern democratic society could not function.

Thus, the government’s ability to raise revenue through voluntary tax compliance — the most efficient and economical form of tax compliance — rests on taxpayers’ belief that the government will honor its end of the social contract.

This “unspoken agreement,” says the Taxpayer Advocate, is overdue to be spoken — in the form of “a formal Taxpayer Bill of Rights” (which, since “a tax system that embeds rights also expects its taxpayers to conduct themselves in such a manner as to ensure those rights are not abused,” will also be “a statement of taxpayer obligations.”)

Naturally, this articulation of the unspoken agreement is not going to take the form of an actual negotiation or agreement.

It’s to be a top-down declaration emitted by Congress or the IRS for our benefit.

Jeffrey Tucker has a good article up at LewRockwell.com about the underground economy.

According to Winchester’s article that I referenced above, self-employed folks report fewer than half of the transactions that aren’t otherwise automatically reported to the government.

In other words, if someone pays them in cash, there’s less than a 50% chance the government will find out about it.

Tucker’s article is about these cash transactions, and how you can frequently get a better deal on goods and services by paying in cash because those you pay know that cash transactions (on which they can evade taxes) are more valuable than transactions that leave a paper trail (and which then get whittled down by the government).

With coming up, tax-related stories are making my RSS feeds look like the Nile in flood season.

Here are some that have caught my eye:

Emma Ross-Thomas at Bloomburg News reports that “Tax dodgers multiply as underground economy cushions job cuts.”

According to the article, in times of economic distress, the proportion of the economy that goes underground expands: businesses go off the books, workers take informal economy jobs, and so forth.

The article focuses on the idea that this makes the economy look worse than it is, as the official statistics are only counting the above-ground economy.

But I prefer to look at it as people getting good practice in untaxed economic activity.

One silver lining to the recent economic cloud is that with people earning less income, there’s less to tax, and governments are bringing in less money.

Here’s a news piece that quantifies some of this:

In the report, CBO projects that the Social Security trust funds will collect just $3 billion more in cash receipts than they will pay out in benefits in the 2010 budget year that starts in .

A year ago, before the economy slipped into recession, the CBO projected an $86 billion cash surplus for the same year.

The IRS last tried to figure out the “tax gap” — its name for the difference between how much tax the law obligates people to pay and what the government successfully squeezes out of them — based on data from the tax year.

It has occasionally released reports on the tax gap since then, but these have just been statistical extrapolations of the data from the 2001 survey.

But the IRS has been working on a new study of the tax gap, based on tax year , the results of which they released this afternoon — Friday afternoon, which is usually the time chosen by government agencies to release reports they hope the news media will ignore.

This is probably a sign that the report isn’t good news for the IRS, so let’s take a closer look.

First, though, look at this summary graphic that purports to show where the gap comes from — which taxes, and which varieties of collection failures (nonfiling, underreporting, and underpayment).

Note that only for the “underpayment” category does the IRS claim to provide “actual amounts” — this is only about 1½% of the total tax, and 10% of the estimated gross tax gap.

The rest of the gap is based on estimates (some based on data last collected as far back as 1984!), although in some cases the agency could not even provide estimates.

This was also true of the numbers.

The agency reports little change between and in the rate of taxpayer noncompliance.

The rate is slightly higher in (with 16.9% of taxes not voluntarily paid on-time, and 14.5% remaining uncollected after IRS enforcement activity), but within the margin of error of the earlier estimates.

The total amount of “underpayment” (that is, amounts that people or corporations declared that they owed, by filing forms or what-have-you, but failed to actually remit by the deadline) — the only part of the new estimates that the IRS had the capability to directly measure rather than estimate — rose in from $33 billion to $46 billion, a 39% increase.

This, while the estimated total tax liability only rose 26%, from $2,112 billion to $2,660 billion.

What I take away from glancing at this report is 1) the IRS didn’t make any headway on tax compliance , and may have lost ground if you think there is reason to suspect that they have been generous in keeping their extrapolated estimates flat while their actually-measured numbers took a leap; and 2) that the government doesn’t really have a very good idea of how big the tax gap is or where its biggest problems are.

These are the best numbers it has, and they are so loosely guesstimated as to inspire little confidence in their accuracy.

Some bits and pieces from here and there:

First off, you may have heard some talk in the news about cuts to the Pentagon budget. You should be aware that it’s hooey. What the talk is really about is proposed reductions to the budget increases that the Pentagon had been hopefully anticipating. The Pentagon budget is still going up in both real and nominal dollars. This talk of “cuts” is like a sign in a store reading “25% Off our recently-doubled price!”

Richard Cebula and Edgar L. Feige have attempted to estimate the size of the underground economy in the United States. They estimate that 18–19% of legally-reportable income in the U.S. stays under-the-table, which translates to about half a trillion dollars in taxes each year that the IRS fails to collect. The IRS itself hasn’t attempted to measure this underground economy since .

The Greek “We Won’t Pay” movement, which is resisting the stealth tax the Greek government imposed in the form of sharply hiked utility rates, has notched up a victory in court, winning an injunction preventing the utility company from shutting off power to resisters who have refused to pay the extra amount in their bills.

Jerry DePyper has beefed up his Pro-life Strike Manifesto — which advocates tax resistance in the service of anti-abortion activism — since I last visited his site. It has a good overview of the whys and hows of tax resistance, with many parallels to the war tax resistance movement.

Some bits and pieces from here and there:

There’s “something fishy” in the latest economic statistics.

Paychecks are down (thanks to a boost in the payroll tax), incomes haven’t been rising in other ways to make up for it, bank account savings aren’t rising, and people aren’t charging more on their credit cards or taking out more loans… and yet, consumer spending is doing just fine, as if somehow the money was materializing anyway.

What’s the trick?

Bernard Baumohl of the Economic Outlook Group thinks it’s the underground economy:

While the IRS tries in vain to convince Congress not to cut its budget (after all, they whine, we’re the part of the government that brings in money for y’all to spend!), members of Congress are enjoying one of their favorite sports: pretending they’re on the side of the little guy against the wasteful government bureaucrats in the tax office.

Lately this has taken the form of House Ways and Means Oversight Subcommittee chairman Charles Boustany, Jr., demanding that the IRS turn over for the subcommittee’s investigation copies of training videos the agency produced in its own presumably extravagant production studio — “a Star Trek parody and a skit based on the television sitcom Gilligan’s Island.”

Hostility towards the IRS can provoke auto-immune complications that are as disruptive as overt threats.

Case in point: In Bloomington, Illinois, an IRS distribution center was cordoned off while a bomb squad of state and Department of Homeland Security specialists navigated a robot through the parking lot to retrieve and inspect two suspicious packages.

The process took five hours, and eventually revealed that the suspicious packages contained… tax forms.

You may have heard that the island nation of Cyprus is the latest nation whose government has resorted to drastic measures to try to raise money from a reluctant population to pay off international creditors.

That government took the odd step of proposing the simple and arbitrary step of shaving a percentage off of every bank account in the nation and using that money to pay for the bailout.

Cypriots reacted by storming the ATMs to try to withdraw their money.

Some bits and pieces from here and there:

NWTRCC is collecting a list of protest actions that will be going on around the U.S. this year.

The “necessity defense”: yes, your honor, I broke the law, but I had to

do it to prevent a greater harm — American activists have tried to use it

to defend their civil disobedience against the militarist government and

its stockpile of weapons of mass destruction, but rarely do the courts

even permit such an argument to be made

(activists in other countries have had

more success). But in the trial of the Transform Now Plowshares

activists in federal court ,

former U.S. Attorney General Ramsey Clark testified for the defense on the subject.

The activists — Greg Boertje-Obed, Megan Rice and Michael Walli — broke

into the Y-12 nuclear weapons plant , held a Christian ceremony with a bible and candles, splashed

some human blood about, and spray-painted messages like “woe to the empire

of blood” and “the fruit of justice is peace” on the walls. The empire,

not amused, and embarrassed that an 82-year-old nun made a fool of its

nuclear weapons security, has thrown the book at them.

Ramsey Clark is an interesting case. You can’t get much more

establishment than being the United States Attorney General (under Lyndon

Johnson). At that time, he was prosecuting anti-war activists (his office

successfully prosecuted Dr. Benjamin Spock for conspiracy to aid and abet

draft resistance, for instance). But since then he has become an

enthusiastic critic of the American empire — even to the extent of

defending, legally and otherwise, such unsavory American enemies as

Slobodan Milošević, Lyndon Larouche, Omar Abdel-Rahman, and Saddam

Hussein.

Clark testified that the use of nuclear weapons represents an

imminent — “omnipresent” was his word — threat. The judge was skeptical:

“Excuse me,” the Judge said. “Are you saying the President intends to

use nuclear weapons? Are you in a position to know that? Are you tied

in with the President? … does the President have his finger on the

button?”

“Well,” said Clark, “he walks around with

it by his

side.”

Then there was this examination of Clark by the defense attorney:

Quigley: Is it reasonable to believe that

what is being refurbished at Y12 are weapons of mass destruction?

Clark: It’s an established fact.

Quigley: And reasonable to believe they

violate international law?

Clark: Reasonable. Under the NPT we agreed to eliminate them.

Quigley: And I believe I just heard today

or yesterday that the Boston bomber was indicted for use of a weapon of

mass destruction — that is part of our criminal code…

The Judge stepped in. “A weapon in the

hands of a terrorist or a citizen is different than a weapon in the

hands of the government. A machine gun, or a tank—is that a fair

statement?”

Clark: It’s fair if you limit it to machine

guns or rifles, but weapons of mass destruction — the

U.S. is in

violation of the intent of the most important treaty we ever signed.

Quigley: Do you believe the continuing

threat of the use of Y12 weapons constitutes a war crime?

Clark: It is a reasonable and fair

statement of belief.

Quigley: And a soldier can commit war

crimes?

Clark: Yes.

Quigley: And using, or preparing to use

weapons of mass destruction is a war crime.

Clark: That is reasonable to believe.

Quigley: The defendants believe the work at

Y12 is preparation for genocide, could be carried out by civilians or

armed services. But they believe the weapons activities at Y12 are in

preparation for genocide and a violation of international law.

Clark: That is reasonable. Because of the

magnitude of the program at this time. One sub, one sub can carry one

hundred warheads. Eight submarines, on alert at all times, eight

hundred warheads in a position to strike. Think of maps. Eight hundred

places in Europe… or on the continent of the Americas. It is criminally

insane.

Quigley: Not homicidal, but omnicidal.

Clark: The life of the planet is at risk

from this one plant here in Tennessee.

The prosecutor tried to pin Clark down: “A minute ago, you testified

that the activities at the Y12 site were unlawful. Are the people who

work there criminals?”

Clark: They are engaged in a criminal

enterprise.

It was interesting to hear of arguments like these being explicitly

aired in court. I don’t really expect the judge to address them

forthrightly and at their worth, but there is some satisfaction in

imagining His Honor trying to figure out just how he’ll sidestep the

issue.

On I mentioned the chill I felt when I noticed that two Google execs’ new book on the future of the internet had gotten glowing prepublication reviews from folks like Tony Blair, Bill Clinton, Henry Kissinger, and a handful of other national security state celebs.

Here is an op-ed the book’s authors wrote for the Wall Street Journal.

It largely strikes a nonconfrontational freedom-is-good tyranny-is-bad tone, though I thought I saw a little saliva appear at the corners of the authors’ mouths when they wrote this:

The world’s autocrats will have to spend a great deal of money to build systems capable of monitoring and containing dissident energy.

They will need cell towers and servers, large data centers, specialized software, legions of trained personnel and reliable supplies of basic resources like electricity and Internet connectivity.

Once such an infrastructure is in place, repressive regimes then will need supercomputers to manage the glut of information.

The authors look at movements like the Arab Spring, and conclude that they petered out because their grassroots, leaderless, decentralized beginnings never matured:

“some sort of centralized authority must emerge if a democratic movement is to have any direction.”

Indeed, these grassroots, leaderless, decentralized movements constitute a threat:

a “mad consensus” that will require “a great leader” to defy, according to Henry Kissinger, whom they approvingly quote.

Over at Slate, Mya Frazier suggests that

Google has aspirations of statehood.

The internet is just such a grassroots, leaderless, decentralized

dystopia… a mad consensus in need of a great leader… and Google knows just

the company for the job.

At The New Yorker, James Surowiecki offers

a meditation on the American underground economy. “Ordinary Americans have gone underground, and, as the recovery continues to limp along, they seem to be doing it more and more.”

I’m not sure it makes much sense to spend time worrying about Obama’s

proposed budget. It’s part wish-list, part advertisement, but not policy.

But one of the things it includes is a 94% bump in the federal excise tax on cigarettes.

Every pack of cigarettes purchased would have a $1.95 federal excise tax

attached to it. While on the one hand, this would be one more reason to

quit smoking and to discourage others from taking up the habit, on the

other hand it would make tax resistance via smuggling that much more

attractive. State cigarette excise tax increases in New York, for example,

have grown to the extent that the majority of cigarettes smoked there are

smuggled in. As marijuana legalization spreads, expect the smuggling

networks that have so successfully supported the marijuana trade over the

years to find a new use in combating the cigarette tax.

The book is a sort of evil twin of my own 99 Tactics of Successful Tax Resistance Campaigns.

Such books can be useful to review because they often, in a sort of sideways-fashion, give tips on how one might erode taxpayer compliance.

The book begins by noting that “Governments in the developing world are striving more than ever to mobilise greater tax revenues,” and, under the unquestioned assumption that this “domestic resource mobilisation” is a splendid aspiration, proceeds to review some of the methods they’ve tried.

The process of “foster[ing] an overall culture of tax compliance… can begin with schoolchildren of primary and secondary level, which [sic.] are at a key moment in their socialisation and tax awareness process.”

This need not be as dull as it sounds:

“With theatre, video games, television shows, and interactive play space, taxpayer education can also be a truly entertaining experience.”

Here is one example: “Costa Rica has created a ‘Tribute to My Country’ space for children at the Museo de los Niños de San José, a former penitentiary.”

Some of the features of this exhibit:

“The Ministry of Finance” includes a video game entitled “Tax Statements” which involves completing a tax income statement in a user-friendly format, entering basic details.

The aim is for children to become familiar with tax payments and the taxation cycle.

This space represents the electronic service points located at tax administrations.

“La Facturita” (The Little Invoice Shop) teaches about the general tax levied on sales.

By pretending to buy and sell, children learn how this tax works: how to distinguish which payment receipts are valid and which are not.

They are also encouraged to get used to requesting an invoice.

A European Union program helped Costa Rica convert its penitentiary space into a space for teaching tax compliance to children (and, along with the United States Agency for International Development, helped start a similar program in El Salvador) by bringing in advisors from Argentina, which had pioneered this approach.

Many of the projects described in this book had financial backing and other support from international agencies like these.

It’s interesting to me the extent to which propagandizing the world’s children in order to imbue them with “an enhanced sense of moral obligation to pay taxes voluntarily” is a global project of the West’s superpowers.

Some other bits I found interesting:

“While there is no universally accepted definition or measure of the informal sector, it is the norm in low- and most middle-income countries, estimated to account for nearly two-thirds of the global working population (even more in developing countries).”

The report uses the phrase “bringing them into the tax net” to describe attempts to lure people out of the informal economy, which I thought was refreshingly honest in its predatory implications.

Many of the programs described target children at the grade-school level, and seem to both have a long-term focus on shaping the attitudes of the upcoming generation (and, as one description put it, breaking the cycle of bad attitudes about taxation passed from generation to generation), and a short-term focus on creating what one program calls “tax ‘ambassadors’ ” who will spread these ideas to their elders.

Implied in some of the programs was the idea that the children would also become informers who would rat out tax evaders or people in the informal economy.

The Inland Revenue Board of Malaysia, for example, subjects a few hundred children there to its annual “educational three-day camp” that “aims to instill a sense of responsibility for paying taxes among the younger generation.”

Sounds fun.

Some of the national tax agencies had partnered with Kidzania, a playground-style role playing area where schoolchildren pretend to take on roles in an adult employee/consumer-oriented economy.

The children perform tasks in adult-styled professions to earn “Kidzos” which they can then spend at mini businesses (all with real-world names, exposed to the children as part of Kidzania’s “immersive and interactive brand experience”).

With guidance from the tax agencies, Kidzania now withholds a certain amount from these Kidzo-paychecks, and tax elements of the economy are also part of this experience.

A common argument against tax resistance goes something like this: The government will add penalties and interest and such to the amount you refuse to pay, and when they eventually wring the money out of you, in the end you’ll have given even more financial support to the government than you would have if you’d just paid up in the first place.

Today I’ll show you some evidence that I hope will convince you that this is not a very good argument.

Lots of people don’t pay the IRS what the agency thinks they should.

The IRS has tried to figure out where this missing money is hiding, but their methodology isn’t all that great, and it’s not an easy mystery to solve.

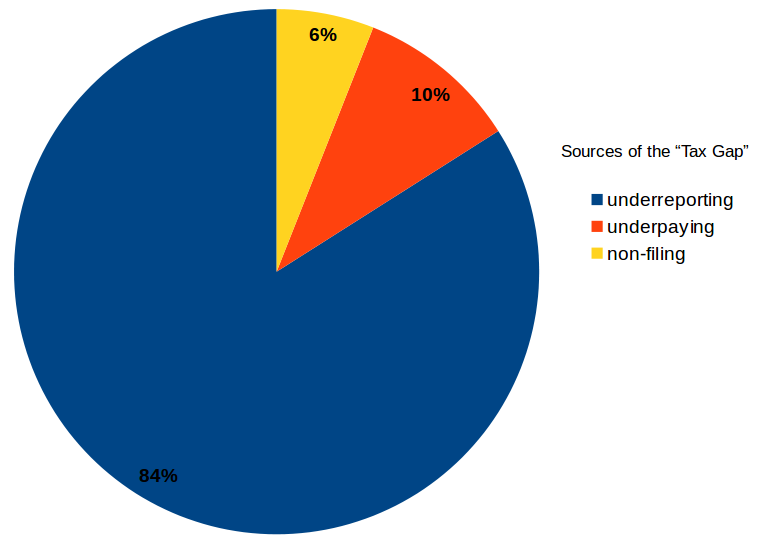

Their best guess is that the vast majority of missing taxes comes from “underreporting” — that is, taxable activities that the IRS never becomes aware of.

For example: if you placed a bet with a friend on the outcome of the Super Bowl, the winner of that bet should have added the amount won to their income and should have paid taxes on it, according to the IRS anyway.

Most people don’t go out of their way to report taxable transactions like these that the IRS wouldn’t learn about on its own, and so a lot of these transactions never get taxed and they stay in the “underground economy.”

An estimated 84% of the “tax gap” comes from unreported taxable activities like these.

Another 6% comes from taxable activities the IRS does learn about, but for which the responsible party never bothers to file a tax return.

The remaining 10% comes from people whose tax debt is registered on paper according to Hoyle, but who never get around to forking over the money.

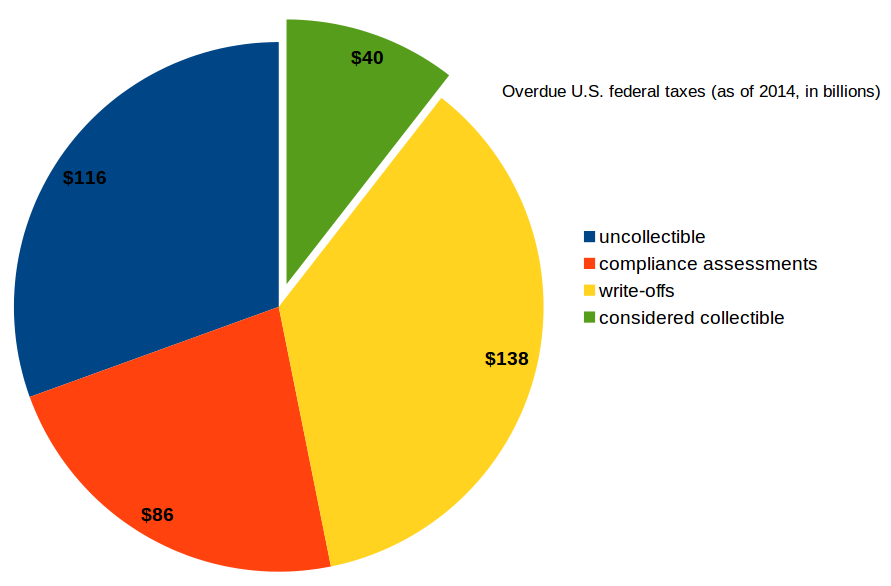

According to IRS financial statements for , there were at that time about $380 billion in outstanding unpaid taxes that it knew about.

This includes about $205 billion in interest & penalties added to the originally-due taxes, but it does not count any taxes that people have thus far successfully evaded by keeping out of the IRS’s view — that is, all the stuff in the 84% blue area above.

It also doesn’t include amounts that the agency can no longer pursue because the statute of limitations has expired.

Of that $380 billion, the agency considers $116 billion to be “currently uncollectible” (“primarily because of the economic situations of the taxpayers”).

Another $86 billion is something called “compliance assessments” — which I think means the IRS tells a taxpayer who hasn’t filed a return (or a fully-revealing one) what the agency suspects the taxpayer would have owed if they had filed accurately, but the taxpayer isn’t going along with it and the controversy is still in limbo.

The agency doesn’t have much confidence in collecting this money either.

There is also a category called “write-offs” that totals $138 billion.

This is tax debt that is hopelessly uncollectible because the taxpayer is bankrupt, insolvent, dead, vanished into thin air, or something of that sort.

That only leaves about ten percent of the total that the IRS considers to be collectible and includes as a potential asset on its financial statements.

So to $175 billion in unpaid taxes, the IRS has added $205 billion in interest & penalties, but it only expects to collect $40 billion of the total (in recent years it has actually collected closer to $46–49 billion per year by means of its enforcement arm, so it may somewhat exceed its expectations).

This I think shows conclusively that people who don’t pay their taxes do not, in the aggregate, ironically end up paying more to the government.

of the $380 billion owed to the IRS in back taxes, the agency only hopes to collect the $40 billion green slice of the pie

For tax resisters — who are typically alive, solvent, and often have seizable assets and income streams — the news isn’t quite as good as this chart would suggest.

But even from juicy targets like us, the IRS fails to seize enough money in penalties and interest from some of us to make up for the money it fails to seize from those of us it lets slip through its clutches.

An informal survey of war tax resisters a few years back, for example, found that the IRS had successfully seized only about 25% of what those resisters had refused to pay.

In addition, it is costly for the agency to deploy its collection apparatus: sending out all of those letters, filing liens & levies, managing the associated bureaucracy — all of that costs money.

The IRS spends about $5 billion dollars on enforcement (including investigations, audits, and collection), and so resisters contribute to this additional cost of the government conscripting our support.

So if you are hesitating to refuse to pay taxes because you worry that by doing so you may inadvertently swell government coffers… I hope this has reassured you that in the aggregate, tax resisters do indeed cost the government money.

The U.S. Government Accountability Office has issued its latest financial audit of the IRS.

The report reiterates what we already knew — that most of what people fail to hand over to the government voluntarily, and the interest & penalties that the IRS adds to those amounts, the government never collects and never really expects to:

Analysis of Unpaid Assessments — Most Unpaid Assessments Are Not Receivables and Are Largely Uncollectible

The unpaid assessment balance includes amounts owed by taxpayers who file returns without sufficient payment as well as amounts assessed through the IRS enforcement programs. As reflected in the supplemental information to the IRS Financial Statements, the unpaid assessment balance was $398 billion… Of the total unpaid assessments balance, $215 billion (54 percent) consists of interest and penalties.

Also, 45 percent of the total outstanding balance of IRS unpaid assessments is largely uncollectible because it is composed of compliance assessments and write-offs.… Write-offs are assessments considered to have no future collection potential.

A table further on in the report details this:

(In Billions)

2018

2017

Federal taxes receivable, net

$58

$52

Total unpaid assessments

$398

$382

Compliance assessments

(65)

(74)

Write-offs

(115)

(111)

Gross federal taxes receivables

218

197

Allowance for uncollectible taxes receivable

(160)

(145)

The report also offered the latest estimate of the “tax gap”:

The gross tax gap is the amount of true tax liability for a given tax year not paid voluntarily and/or timely.

The most recent estimate of the gross tax gap is $458 billion.…

There are three primary sources of noncompliance:

nonfiling tax gap (the tax not paid on time by those who do not file required returns on time;

underreporting tax gap (the net understatement of tax on timely filed returns); and

underpayment tax gap (the amount of tax reported on timely filed returns not paid on time).

The estimated noncompliance of each of these components is $32 billion for nonfiling, $387 billion for underreporting, and $39 billion for underpayments.

Additionaly, the gross tax gap can be grouped by type of tax, as follows:

$319 billion for individual income tax,

$44 billion for corporation income tax,

$91 billion for employment tax, and

$4 billion for combined estate and excise tax.

The net tax gap is the gross tax gap less tax subsequently collected for a tax year either voluntarily or from IRS administrative and enforcement activities.

As a result, the net tax gap is the portion of the gross tax gap that will not be paid.

The portion of gross tax gap to eventually be collected is estimated to be $52 billion, resulting in a net tax gap of $406 billion.

The estimated net tax gap by type of tax is:

{kind=link}