When Ruth Benn of Brooklyn filed her federal income taxes , she left out an important element: the check.

“In good conscience I cannot pay this money to the US government,” Ms. Benn wrote in a letter to the IRS that accompanied a completed, but unpaid, 1040 form.

“I do not want my tax dollars to be used for killing and war.”

Jim Allen, a retired Army social worker now teaching at St. Louis University, knows he is breaking the law by withholding some of his income taxes.

But he and his wife, Jan, became fed up with the billions of dollars spent to fund the war in Iraq and decided to take a moral stand.

“I am not opposed to paying taxes, but I am when such a large percent is going to pay for war,” says Mr. Allen, who served in the Army for 20 years.

Becky Pierce of Boston says she evades the IRS by not filing at all.

Each April she fills out a 1040 form to determine how much she’ll donate to charity, then puts the income tax form in her filing cabinet.

Ms. Pierce says she is part of a long American tradition of tax resistance, reaching back to when revolutionaries tossed tea into Boston Harbor.

But to follow in the footsteps of American protesters such as Henry David Thoreau — who went to jail for withholding taxes during the Mexican-American War — Pierce says she must live on a Walden Pond level of thrift.

“You need to have control of your money,” she says.

“I’m a self-employed carpenter.

No one is reporting what I make.

That’s why I can go unnoticed.”

But Jim Stockwell of Micaville, N.C., refuses to take a vow of poverty for what he considers “a simple act of conscience.”

He laughs about how he never paid income taxes while working as a vitamin supplement salesman in Maine and a Home Depot employee in North Carolina.

“I made bundles and bundles of money and gave bundles away [to charity],” Mr. Stockwell says.

“I arranged my life my own way and the IRS never caught up with me.”

Like most Americans, Peter Smith and his wife, Ellyn Stecker, sit down each year to fill out a federal tax form.

Then they write a check to the U.S. Treasury for half the sum in the “amount you owe” box.

They are among thousands of Americans who refuse to pay part or all of their federal taxes as a protest against war and military spending.

“It takes two things to fight a war: people and money,” says Smith, 67, a retired math and computer science teacher.

“I can’t refuse anymore to go, but I certainly can refuse to send the money.”

Smith and Stecker donate their withheld tax money to charities, such as Oxfam America, which fights global poverty and hunger, and a local shelter for battered women.

Stecker, 60, a physician, wishes the government would spend tax dollars on those sorts of programs instead of war.

“You look at what your money is being spent for, and you say, ‘No, I will not give my money for that,’ ” she says.

But the IRS eventually gets its share.

The couple know the routine: By July, they get a letter from the IRS asking them to pay the rest of what they owe.

They respond with a note explaining their reasons for not paying the full amount.

Then there’s a final notice.

The IRS says in 30 days it will extract the money from paychecks, bank accounts or retirement funds.

And the agency does just that.

The couple figure that over the years, the IRS has collected about $75,000 in back taxes, penalties and interest from them.

, thanks to withholding and charitable giving, they owe nothing to the federal government.

Want your anti-war protest to get noticed? Don’t pay your taxes.

Susan Quinlan’s been doing it for , and she’s attracted plenty of attention from the Internal Revenue Service, which showed up at her front door demanding she pay a portion of her earnings or face imprisonment.

Quinlan refused to cooperate, the IRS slunk away and, , she’s dodging federal tax laws as gamely as ever.

Quinlan, a Berkeley resident, has retooled her life to keep negative consequences to a minimum.

She doesn’t own property or maintain much cash in bank accounts and she declines jobs that require she withhold money from her paycheck.

“My approach was, I don’t want to pay any taxes at all, which means adapting my lifestyle to make that possible,” Quinlan said.

As a full-time volunteer peace advocate, Quinlan falls beneath the tax line and need not pay a dime.

In the past, though, when she’s owed money, she’s had to navigate thorny legal territory to ensure her earnings steer clear of federal war coffers.

One problem facing many aspiring resisters is that taxes are typically taken out of paychecks automatically, thwarting the opportunity to resist.

Solutions include self-employment, contract work, or loading up on W-4 allowances that minimize per-paycheck deductions.

When April 15 rolls around, many resisters either submit a 1040 then refuse to pay their taxes or eschew filing altogether.

Quinlan opts for the latter.

She hadn’t filed a federal income tax return , when the IRS came after her wages from a job she held at a nonprofit Latina employment agency.

Rather than pay up, she quit, and would do it again, she said.

“I loved that job, but my commitment to not pay for war came first,” she said.

Does that mean she pockets the money and heads for the outlets?

Definitely not, she said.

Like many resisters, Quinlan redirects those tax dollars to local charities and community groups.

“I always calculated what taxes would be owed because I do feel it’s important that I contribute to the community,” she said.

“I just don’t want it to go to illegal, immoral, imperialistic wars.”

I’m back from the NWTRCC National Gathering in Harrisonburg, Virginia.

I’ll share some of my impressions and go into more detail in the coming days.

I flew into Charlottesville and was picked up by one of our hosts — who’d be shuttling incoming conferencers all weekend and who did a fantastic job of making sure we all got collected, assembled, fed, and then given a comfortable place to lay our heads at the end of the day.

We passed the new America tombstone on the way back to Harrisonburg where we were holding the sessions of our meeting at the Community Mennonite Church.

After the administrative committee met on morning and afternoon to grease the wheels for the larger coordinating committee meetings, night was devoted to introductions, a viewing of a video on corrupt and insufficiently-monitored government spending on the Afghanistan War, and reports from local groups about how their Tax Day actions went and what they’ve been up to.

Clare Hanrahan shared some stories from the tour she and Coleman Smith have been conducting through Tennessee, Alabama, Georgia and South Carolina to meet with peace & justice activists in that area, forge alliances between them, and learn about the state of the regional movement.

They’ve been blogging their adventures on the War Resisters League Asheville site.

Lots of people reported that their tax day protests had been upstaged by the Tea Party demonstrations this year, though a few groups took the “if you can’t beat ’em, join ’em” approach and partied along with the rest of them.

One person noted that with more people e-filing their tax returns, the phenomenon of the last-minute post office rush has diminished, and there’s less media attention and less of an audience for leafletting and such.

Ruth Benn reported on how in New York they held a viewing of tax resistance related excerpts from Boston Legal and Stranger Than Fiction as a discussion-prompter.

Robert Randall reported that an attempt to focus messaging around the single issue of opposition to the Iraq War had seemed promising at first, as the war became more unpopular even in his red state of Georgia, but that it hadn’t seemed to lead to any noticeable uptick in interest in war tax resistance or in new resisters.

Many people noted the increasing challenge of developing interest in our message in a time when the anti-war movement is suffering from a post-election tranquilization.

Ray Gingerich reflected on the difficulty he is having in trying to reinvigorate the war tax resistance tradition in the Mennonite church.

On tax day, he sends his letter of protest to his church.

He also recalled for us that their local war tax resistance group used to be much more active and at one time they had a mutual aid fund that they used to defray the costs of penalties, interest, and frivolous filing fines incurred by individual members.

morning

After breakfast morning, we discussed what we thought of a rough cut of an upcoming war tax resistance film project, and talked about what we thought would be the best use of the available footage.

Then Bill Ramsey gave us an update on the War Tax Boycott project, and we discussed options for modifying the campaign going forward.

Here are some of the comments from my notes (these are all paraphrased and on-the-fly, so may not represent what these folks actually said or meant to say):

David Waters

I love the palm cards.

Pam Allee

It would be good to keep the campaign going on a low simmer during the sleepy times so that we would be ready to jump in with a flashier campaign when the moment is right.

Bill Ramsey

I recommend a scaled-down campaign in which we keep the website updated but reduce the budget.

Robert Randall

How can we hold on to the new resisters whom we learn about for the first time when they sign up for the boycott?

Ray Gingerich

I’m confused as to whether the boycott is meant only for first-timers or if it’s for everyone; to me it seemed gimmicky and not particularly appealing.

Susan Balzer

Some people might not want to sign on to the boycott because they don’t want to be “on a list” and they might be more comfortable if there’s a way to remain anonymous.

Jim Stockwell

I think maybe “boycott” is a threatening or discouraging word to some people.

Clare Hanrahan

The hard copy boycott sign-on sheets weren’t at all popular when we were tabling.

Daniel Woodham

We should make the palm cards less likely to go stale by removing the year and references to specific wars/issues.

Geov Parrish

The value of the campaign is mainly as a vehicle for publicizing war tax resistance as an option, not so much in getting people to sign on.

Erica Weiland

I wonder if by framing the campaign as a one-year thing we prompt people to make their resistance temporary.

Clare Hanrahan

I do low-income resistance and I redirect unwaged labor, not money.

I think the war tax resistance movement should honor that and recognize that option for boycott participants (not assume everyone has a dollar amount to redirect).

Tim Godshall (and others)

We need to have better follow-up with the people who sign on — by phone is better than by email.

Robert Randall

Maybe we could parcel out some of the following-up to people in our network list.

Next came a discussion of our finances and a report from the fundraising committee, and then we broke for lunch.

afternoon

First thing on afternoon we had a panel presentation and group discussion about the Religious Freedom Peace Tax Fund Act and about NWTRCC’s relationship with the National Campaign for a Peace Tax Fund.

This was the most contentious item on the agenda, and I’m going to leave you all in suspense about it by writing it up in a future blog post all its own rather than putting it here.

After this, we broke up into smaller group sessions.

In mine, a group of maybe twenty resisters just shared some of their recent experiences with resistance and with the IRS.

Sharing our war stories like this is one of the best parts of these meetings, and is also a great way of keeping our fingers on the pulse of how IRS enforcement trends are changing.

I didn’t take notes during that session since it seemed to be a more-intimate sharing of personal information than the general meeting.

I did write down one quote though that was too good to miss, from Clare Hanrahan:

“I used to say that they could boil me in oil before I’d pay any war taxes, but now that I know that they could actually do that…”

One idea I came away with was that it would be nice to have some tips from war tax resistance veterans about how to deal with “mixed marriages” in which one partner is a resister and the other one is not.

There are some tricky questions, especially when finances get tangled up together.

I’m hoping, next time I have some free time, to put some time into collecting some of these stories and tips.

The next full-group session was about “organizing strategies and outreach ideas in the Obama era.”

I didn’t take notes here either as I was facilitating and had to devote all of my attention to that.

What I mostly recall from the discussion is that people were less interested in talking about strategies, techniques, and outreach ideas and more interested in talking about what sort of messaging we should and shouldn’t use.

Before dinner was another set of small-group breakout sessions.

I joined the web team, discussing the nitty-gritty of web site maintenance and design, none of which is really worth relating here.

was our business meeting, in which decisions that require consensus approval of the coordinating committee are made, folks are rotated onto and off of the administrative committee (Erica Weiland is joining us this time), we review the budget and priorities and how the coordinator is doing, check in on the progress of ongoing projects, and plan for the next gathering.

The first half of the meeting was largely taken up by Peace Tax Fund-related discussion, which I’m holding off reporting on until a future post.

For the second half, I was the facilitator and so took no notes.

So you’ll just have to wait until Ruth Benn posts her meeting minutes for a full picture of what took place.

This issue had come up at our last meeting in Eugene because the National Campaign for a Peace Tax Fund had asked us to formally endorse this legislation.

We were unable to reach consensus on the endorsement at that meeting and didn’t allot enough time to really discuss the matter in detail, so we planned to readdress the issue and devote more time to discussion this time around.

One of the arguments in favor of us endorsing the bill was that in the NWTRCC “Statement of Purpose” is a section that many people interpreted as a built-in endorsement of the bill.

That section reads:

NWTRCC’s goal is to maintain and build a national movement of conscientious objectors to military taxes by supporting, coordinating and publicizing the WTR actions of groups and individuals.

These actions include: war tax resistance, protest, and refusal; the redirection of military taxes to meet human needs; support of the US Peace Tax Fund Bill; and adjustment of lifestyle to avoid tax liability.

I’ve heard many perspectives about whether this section endorses the bill or merely indicates that support for it is one of many war tax resistance related activities that our affiliate groups engage in.

But in any case, the “US Peace Tax Fund Bill” doesn’t exist as an active piece of legislation anymore.

The currently-proposed legislation is substantially different in content and has a new name.

So this time around, in addition to debating the endorsement question, we were also trying to come up with a satisfactory way to remove or replace the anachronistic language from our statement of purpose.

On , we had a panel presentation on the bill followed by an open discussion.

Bethany Criss, the executive director of the National Campaign for a Peace Tax Fund, presented the case for why we should endorse.

Ray Gingerich and I each gave statements opposing the endorsement.

Ruth Benn shared some of her insights from being exposed to the variety of international peace tax fund campaigns (some of which are promoting legislation that differs in important ways from the U.S. bill) and also recounted some of the history of the close working relationship of NWTRCC and NCPTF.

After these brief remarks from the panel, other attendees addressed the issue.

The following summary is based on notes I was taking at the time, so is only as good as my attention and note-taking were — caveat emptor:

Bethany Criss started out by noting the similarity between legalized conscientious objection to military service and conscientious objection to military taxation.

She also tried to assuage concerns that the “Religious Freedom” part of the bill’s title meant that the provisions of the bill would not be available to non-religious objectors.

She said that she felt confident that Congress would not raid the peace tax fund to pay for military expenses because the RFPTFA would represent a contract between us and Congress and that we could hold them accountable if they were to violate it.

She acknowledged that the bill was imperfect and would not accomplish as much as many people would like, but hoped that we would see it as an initial step in an incremental process.

I went next.

Here’s more-or-less the argument I gave against endorsement:

War Tax Resisters and Peace Tax Fund advocates agree that the belligerent militarism of the United States is a grave problem, that individuals must act to oppose it, and that our tax dollars are an important way in which we can move from complicity to opposition.

Because of this, we’re natural allies and have much in common.

The RFPTFA currently being pushed by the NCPTF has some significant problems. So much so that although our groups have much in common in our outlook and our interests, I think it would be a mistake for NWTRCC to endorse the RFPTFA.

Indeed, the problems with the bill are so significant that if the bill ever looked as though it might pass, we would be wiser to actively oppose the bill than to endorse it.

The main problems with the bill are two: 1) it’s no good, and 2) it’s bad.

That is, not only would it not deliver any meaningful benefits, but it would have harmful effects that would be damaging to the war tax resistance movement and dangerous to individual war tax resisters.

The reason why I say the bill is no good is this.

If the bill passes, it would give Congress more taxpayer money to spend and would allow Congress to spend as much money as it likes on war and armaments.

Every dollar paid into the “Peace Tax Fund” would increase taxpayer spending on the military.

This sounds like exactly the opposite of what the NCPTF intends, which may be true.

But sometimes good intentions lead to counterproductive laws and policies.

If you read the NCPTF literature, you’ll see that they admit that the bill would increase government revenue without decreasing how much Congress could spend on war:

So Congress would have more taxpayer money than before and could spend as much as it wants on war.

Why on earth would we want this?

Well, we’re supposed to want this because at least our money wouldn’t be spent on war.

But this is just an illusion.

The basic problem has to do with displacement.

If you pay into the Peace Tax Fund and Congress can only spend “your” money on something nice like the National Park Service, Congress can just take some other money that it had been planning to spend on the Park Service and divert it to the Pentagon.

So Congress spends just like it always has, with a little more taxpayer money than it would have had otherwise, but the people who pay into the Peace Tax Fund falsely believe that they aren’t responsible for the results of that increased spending.

It would be as though I were to pour a cup of sand into a mug full of hot coffee and then claim that I wasn’t responsible for the spillover since my sand sank to the bottom of the mug and it was only someone else’s coffee that spilled over the top.

So that’s why the RFPTFA isn’t any good.

Now here’s why it’s bad.

First: it constructs an illusion through which people can be induced to pay for war and militarism while believing that they are not.

The war tax resistance movement should be working hard to tear down illusions like this, not build up new ones.

Second: it would divide the war tax resistance movement between those people who maintain their testimony against paying for war and those who take advantage of the false moral cover of the RFPTFA.

This would also give the IRS fewer targets to pursue, and make the remaining war tax resisters more likely to be targeted by enforcement actions.

If the war tax resistance movement ever does become a powerful force for social change, you can bet that the government will consider passing such a bill — not as a concession to our movement but as a divide-and-conquer technique against it.

Third: it would give a persuasive rhetorical tool to people who oppose war tax resisters.

They would say that war tax resisters should just pay into the Peace Tax Fund like good, law-abiding, conscientious people.

Imagine what the IRS would say to resisters: “We gave you the ‘Peace Tax Fund’ you wanted — now you’ve got no more excuses not to pay up.”

Those three things are harmful effects the bill would have if it ever became law.

I don’t think this is likely, but there’s a fourth reason not to endorse the bill that doesn’t depend on whether or not it is successful in becoming law: advocacy of such a bill sends the message that the war tax resistance movement is naïve and that our conscientious scruples are superficial.

It tells people that war tax resisters:

are not particularly conscientious at all, but can be easily bought-off by symbolic concessions and simple sleight-of-hand

are conscientious enough to check a box on a form, but not conscientious enough to follow through on the ramifications of our actions

are willing enough to fund war if you can give us a way to deny that we’re doing it

would rather have a certificate from the government recognizing our officially certified conscientiousness than to actually be conscientious

These flaws have been pointed out before, and frequently PTF promoters have responded with an argument along these lines: Sure the RFPTFA won’t reduce military spending and it has at best an ambiguous effect on taxpayer complicity, but it has strong symbolic power: it’s a way to get conscientious objection to military taxation officially recognized, to get a foot in the door, to be able to take a census of conscientious objectors every April 15th, to propagandize for peace with every 1040 booklet, and so forth.

These benefits are not very convincing to me, for a number of reasons, but even if you were to acknowledge them — are they sufficient to justify putting any more energy into a 38-year-old campaign that has gone nowhere at all, currently in support of a piece of legislation that, even as watered down as it is, hasn’t had as much as a committee hearing in over a decade?

I feel strongly about this, and I have not pulled my punches.

Some of you may think I’m being uncharitable and unfair.

I’ll end on this note: I think the advocates of the RFPTFA have their hearts in the right place.

They are temperamentally our allies and I hope they continue to think of themselves that way.

I think that to the extent that we agree, we should continue to work closely and warmly together, and to the extent that we disagree we can agree to disagree.

After me, Ray Gingerich spoke, giving what I interpreted as a Thoreauvian argument against the peace tax fund idea: we shouldn’t wait to act conscientiously until the government gives us its permission to do so.

In addition, he feels from his work in trying to reintroduce war tax resistance into the Mennonite churches that the peace tax fund is an obstacle to this — it creates an excuse that people use: they say they’ll resist taxes but only when there’s a peace tax fund that allows them to do it legally.

After these prepared remarks from the panel, and Ruth’s discussion which I mentioned above, we heard from the other attendees.

Before Eugene, I thought of myself as a real outlier in my skepticism about the peace tax fund bill.

Most of what I heard about the bill in war tax resistance circles was positive, and the way people spoke about it made it seem like NWTRCC enthusiasm for the peace tax fund was a foregone conclusion if not a tautological one.

In Eugene I was pleasantly surprised to see that a few other people shared my misgivings about the bill, though I still felt like we were the minority.

In Harrisonburg last Saturday, though, it was clear that the tide had shifted dramatically.

Even with the executive director of the NCPTF there to pitch the bill, most people had little praise for it, and even the ones who were peace tax fund supporters in the abstract expressed that we probably shouldn’t endorse this version.

Gary Erb noted that most of those present probably wouldn’t qualify as conscientious objectors under the bill’s restrictive language, and so wouldn’t be able to legally avail themselves of the RFPTFA even if they cared to.

He also felt the bill would have a divide-and-conquer effect against the WTR movement, and recommended against endorsement.

Geov Parrish felt that the RFPTFA hadn’t a chance of becoming law, so it should be best seen as an educational vehicle.

That being the case, it was a poor idea to have watered it down so much in an attempt to make it palatable enough to pass through Congress.

Also, he noted that he feels excluded from the RFPTFA and its promotional materials because he is not a Christian.

Joffre Stewart said that as an anarchist resister, begging the state for exemptions and favors isn’t his style.

He thinks that conscientious objection to military service was mostly enacted for the state’s benefit, not for the benefit of the COs, and he thinks the same would be true of legalized conscientious objection to military taxation.

From this, he draws the conclusion that the reason we don’t have legal conscientious objection to military taxation is that war tax resisters have not yet become sufficiently inconvenient to the government.

Daniel Woodham thought that though the RFPTFA wasn’t perfect, it might make for a good first step, and once it was enacted we could work to amend it or correct its faults over time.

Bethany Criss said that in her view the “laundry list” of items in the section (§3b) of the bill that defines spending that falls under the “military purpose” category shouldn’t be seen as excluding other spending from that category, but only as examples of spending that fall under that category.

In her view, once the bill passes, a next step will be to ensure that the “military purpose” definition is interpreted inclusively so that it covers all the stuff we’re worried about.

Greg Reagle gave us some perspective on the reasoning behind watering down the bill to permit Congress to spend the money in the RFPTF on anything in the budget other than things in the military purpose category (previous incarnations of the bill had specified more precisely where that money would go).

He said that potential supporters in Congress had balked at having their spending decisions micromanaged by legislation, and so the changes had been made to mollify them.

Erica Weiland wanted to emphasize the positive working relationship between NWTRCC and NCPTF, though she too was opposed to endorsing the bill.

As an anarchist she doesn’t much favor trying to solve problems via legislation, but as an activist she tries to inspire well-intentioned people to be more active in ways that seem most appropriate to them, so she wants to encourage PTF promoters to keep doing their thing.

Robert Randall said he was impressed at the high plane on which the discussion was taking place.

He thought that the results of passing the RFPTFA might not be all that important, but that there might be some benefits to be had from the campaign to pass the bill anyway.

Pam Allee felt that the bill would help to emphasize that “we are the government” and so we can take control of the budget and change spending priorities so as to emphasize things like education, seat belt law enforcement, and other liberal priorities.

She was concerned that the RFPTFA seemed to lack grassroots support.

Larry Bassett paused to wonder whether it was really appropriate to the mission of a group like NWTRCC to be endorsing legislation or the individual projects of the affiliate groups.

Jim Stockwell felt that there might be a contradiction in that for many WTRs, the fact that tax resistance is illegal civil disobedience is an essential part of their WTR, and so legal conscientious objection would not be helpful to them.

He hoped our two groups would continue to work together.

Hiro (whose last name I didn’t catch, and whose first name I may be misspelling) encouraged us to patiently work at incremental approaches and not reject RFPTFA just because it wasn’t everything we wanted.

That said, she also worried that the government would spend the “peace” tax fund on things based on its warped definition of peacemaking work.

She envisioned Blackwater contractors doing their institution-building mopping-up exercises in Iraq (where she is from) and calling it “peacemaking” activities deserving of RFPTFA funding.

Tim Godshall tried to give us some perspective, noting that WTRs are one of the best arguments for the PTF (that is, the existence of WTRs demonstrates that many citizens have a strong conscientious objection that their government needs to accommodate), and also that although the RFPTFA might not have any effect on the military budget, the same could be said of WTRs. He believes that the RFPTFA is one part of a larger campaign to pressure the government to change its spending priorities.

Peter Smith disagreed with the suggestion that if the RFPTFA were to pass it would divide the WTR movement.

He agreed that we should not endorse the legislation, but hoped we would continue to support the PTF campaigners.

Ray Gingerich responded to a comment from Joffre Stewart by insisting that he was not an anarchist and indeed believed that a strong, active government (for example, one capable of implementing single-payer universal health care) was not incompatible with pacifism.

He plugged nonviolent conflict resolution strategies of the The Unconquerable World / A Force More Powerful school.

He also suggested that Marian Franz (the long-time National Campaign for a Peace Tax Fund executive director) had been used by people and institutions who wanted to delay their confrontation with taxpayer complicity by putting it off until some distant future in which conscientious objection to military taxation was a legalized option.

Joffre Stewart noted that the U.S. government had no qualms about raiding the Social Security “trust fund” to pay for its military spending, and that it had stacked its “U.S. Institute of Peace” with CIA folk committed to the government’s violent foreign policy.

He therefore sees no reason to trust the government to administer a “peace tax fund.”

Bethany Criss told us that not only is she committed to seeing the RFPTFA enacted into law, but that she is also a war tax resister and has been since .

She said that although there is an associated “Peace Tax Foundation” with an educational mission, there should be no doubt that the Campaign’s goal is to get the legislation passed into law.

She thinks that the bill will be beneficial to war tax resisters and the war tax resistance movement by making WTR more visible.

She says that if the bill were enacted, it would not take away the opportunity to resist or say no; that resisters could continue to resist as before if they wished.

The goal is to bring more people in to a war tax resistance mindset.

She notes that part of the reason the bill was watered down is that their campaign doesn’t yet have enough supporters to bring enough pressure to bear on the legislators; this is another reason why she’d like our support.

Finally, Bill Ramsey felt that we might be better off not concentrating on the (unlikely) endorsement and instead trying to work on ways the two groups can work better together.

was an open-ended discussion without any decisions to be made on either the endorsement or the statement of purpose wording; on , our “business meeting,” we addressed those decisions.

A number of people who could not come to the meeting sent along their opinions about the RFPTFA, and printouts of these were made available to attendees of the business meeting before we took up the issue.

These were on the whole much more positive about the Act and more in favor of endorsement than the attendees had been, with one person recommending endorsement, another recommending “NWTRCC continuing its endorsement” of the bill (though we had a hard time determining which if any version of the bill our group had originally endorsed), and another conveying the results of a discussion about the issue held by Sonoma County Taxes for Peace which led to that group deciding to strongly support NWTRCC endorsing the bill.

Predictably, we did not reach consensus at the business meeting on to endorse the RFPTFA.

I counted about a half-dozen people in favor of endorsement, maybe half again as many against it.

Unfortunately, although a non-endorsement was pretty clearly the inevitable conclusion, it took a while to get there, and we weren’t able to devote as much time as we needed to the stickier question of the Statement of Purpose and its anachronistic reference to the “US Peace Tax Fund Bill.”

The upshot of that discussion was that there were two replacement phrases with a large amount of support:

“…support of peace tax fund legislation…”

“…support of legislation that would legalize conscientious objection to military taxation…”

While there was broad support for both, neither was able to rally a consensus around it.

My proposal to simply scrap the old anachronistic wording for now and perhaps come up with a replacement at a later date also failed to attract consensus support — with many people feeling that by rejecting the endorsement and also eliminating mention of the PTF from our Statement of Purpose it would look too much like we’d conducted a wholesale purge of PTF sympathy from the group.

So when it came down to it, the Statement of Purpose ended up the same way it began in this area: it continues to pledge our support for supporters of the long-gone “US Peace Tax Fund Bill.”

This is a little ridiculous, but seems mostly harmless.

was .

I got here early to do some preliminary work as part of NWTRCC’s Administrative Committee.

While the last meeting was contentious, with the controversial issue of a possible Peace Tax Fund endorsement on the agenda, this meeting looks to be comparatively placid.

NWTRCC regulars were joined by curious locals like Tom Quinn of EcoWatch and Michael Patterson from Dennis Kucinich’s office (our meeting place is in Kucinich’s House district and he was curious enough to send an aide to take notes).

A few things jumped out at me during the opening introductory go-’round:

Jim Stockwell of North Carolina mentioned that after some initial mutual

suspicion there was surprising synergy between the traditional Tax Day

protest his war tax resistance group held

and the Tea Party protests going on

at .

Many of the local groups reported diminishing numbers and less-frequent

activity in the past months, mirroring a general doldrums in the peace

movement.

Bill Ramsey noted that it has become harder to set up alternative funds

in the post-9/11 financial paperwork era.

Ramsey also reported on an interesting and creative tax day protest in his

neck of the woods. A group grabbed hundreds of 1040 forms from public

places where such things are found (libraries, post offices, and the

like), then printed ghostly images of coffins and of children wounded in

war over the forms, and then replaced them where they had originally found

them.

Ginny Sсhnеider noted that in New Hampshire, the notoriety

of the Ed

and Elaine Brown tax protester stand-off fiasco has made it difficult

for her to do outreach in the progressive community. People hear “tax

resistance” and immediately their minds conjure up images of nuts holing

up with their arsenals and their conspiracy theories until the government

locks them up for life.

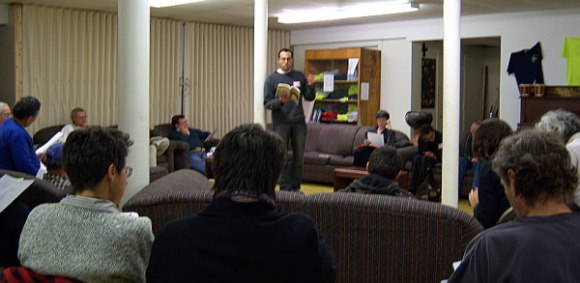

We watched a near-final cut of a film

NWTRCC is producing about war tax resistance and resisters:

Death and Taxes. It met with great acclaim (and

plenty of suggestions for last-minute edits). Last I heard, it’s due for

release .

Attendees watch a cut of Death and Taxes, an introductory war tax resistance film due to be released next month

Later, Phil Althouse, an election observer in El Salvador, updated us on conditions there, and Mike Ferner of Veterans for Peace talked about how to move from activism to organizing and build bonds between disparate parts of the broader anti-war coalition.

Mike Ferner and Phil Althouse address the gathering

While coalition building always sounds great in the abstract, when it comes

down to actually doing it, it runs into the practical difficulty of finding a

common ground and deciding where to compromise and where no compromise is

possible. Ferner thought that organizing around the larger vision of

real democracy was the way to go. Other folks were skeptical. It can

be difficult to find anything approaching an ideological common ground even in

a small group like

NWTRCC

with an inherently common, specialized and political interest.

In members of

NWTRCC

there’s often a tension between avowed nonviolent principles and promotion of

progressive projects (like universal health care and publicly-financed

elections for instance) that fundamentally rely on a coercive, violent state

to carry them out. The avowedly nonviolent progressives either don’t see the

violent ramifications inherent in such projects or I have failed to understand

the ingenious way they have squared this circle. I usually avoid the

temptation to press the point, but sometimes give in.

Anyway, after this we split up into two groups: a War Tax Resistance 101

discussion group that I moderated, and a larger group that discussed issues of

interest to more experienced resisters. There were other groups that met over

the course of the afternoon as well, but by then I found it hard to be in even

one place at once.

In the evening we heard more in-depth stories of the tax resistance from our hosts, Maria Smith and Charlie Hurst, and from Juanita Nelson and Erica Weiland.

Juanita Nelson told the story of her arrest-in-a-Sears-bathrobe that she also tells in A Matter of Freedom.

Erica described her transformation from a young Dean Democrat to a tax resisting anarchist (a salvation narrative in which, to my delight, The Picket Line plays a role).

Arthur Harvey, then an organic farmer from Hartford, Maine, was profiled in Samuel Fromartz’s book Organic, Inc. because of his legal battle to make sellers who use the “organic” buzzword adhere to the genuine standards of that variety of food production.

In the course of this, Formartz also mentions Harvey’s war tax resistance:

It was not the first time Harvey had gone up against the federal government.

As a tax resister opposed to military spending, “especially nuclear weapons, and the export of arms and military forces to many places around the world,” Harvey had refused to file or pay federal income taxes since .

His wife, Elizabeth Gravalos, hadn’t paid federal taxes since .

Instead, they donated time and money to social service and environmental organizations.

The IRS had come knocking at their door a couple of times, then seized the family’s property in and demanded $62,000 in back taxes and penalties — about three times the annual income of the farm.

When they did not pay, the IRS took the rare step of auctioning off the property at a town office across the street from their house, with protesters outside.

They initially lost the blueberry field to a bidder, though luckily no one bid on the house, perhaps because it had only rudimentary plumbing and no electricity.

Eventually, Gravalos’s mother bought the house, and the couple’s daughter successfully bid on another parcel of the land, which she later swapped for the blueberry field.

They were back in business.

Harvey, an affable and intelligent man with a wiry physique, perhaps owing to his vegetarian diet, said the lesson he learned from that fight was not to stop being a tax resister, but to avoid owning property in his own name that could be seized by the government.

“We own a couple of cars, so I guess they could go after those, but they aren’t worth much,” he told me.

Aaron Falbel wrote about the blueberry-growing couple for the War Resisters League’s magazine in :

Arthur Harvey has not filed a federal tax return or paid income tax .

His partner, Elizabeth Gravalos hasn’t filed or paid .

Until recently, the Internal Revenue Service gave them little trouble.

“They visited us twice, once around and again around , back when we lived in New Hampshire,” Harvey says.

“Probably they concluded we had nothing much worth taking and perhaps were not subject to much tax anyway,” he adds.

But after the Gravalos/Harvey family moved to Maine ten years ago, earned a bit more money, acquired a house, two wood lots and a blueberry field and started paying state taxes (New Hampshire has no state income tax, but Maine does), the IRS began to take notice.

, the IRS seized their properties in lieu of tax payments assessed at $62,000 (including interest and penalties) for an astonishing figure, considering the family’s annual income from their blueberry and flower business averages about $16,000.

Going Once…

The IRS held an auction at the town office across the street from the Gravalos/Harvey home.

“I might have cried if I were alone,” Gravalos admitted.

But she was far from alone.

About 75 supporters gathered outside the building and spoke of their solidarity with Elizabeth and Arthur.

To demonstrate the power and the good that can come out of war tax redirection, Harvey, Gravalos and their family and friends raised over $3,000 to pay off the local property tax liens of seven Hartford residents.

The auction didn’t last long.

When Gravalos and her family emerged stoically from the town office, she announced, “The good news is that no one bid on the house.”

Emily Harvey, Arthur and Elizabeth’s daughter and a sophomore at Wellesley College, bid on (and won) the small half-acre wood lot on behalf of her younger brother Max.

(Max, at age 16, was legally too young to enter a bid.)

The town selectman and town clerk teamed up to buy the larger 21-acre wood lot, and another Hartford resident bought the blueberry field.

Harvey speculated that the reason no one bid on the house was that the minimum bid was too high: $21,000 for a house with no electricity or indoor plumbing.

At the conclusion of the auction, the IRS declared that they would reevaluate the minimum bid and hold another auction .

Going Twice…

The minimum was eventually set at $7,900. Gravalos and Harvey had originally discouraged friendly bids on their house, feeling that the price was too high.

“We really did not want the IRS to get that much money,” Harvey said.

But for the second auction, with a lower minimum bid, they didn’t discourage people who would buy the house back for them, even though that meant surrendering money to the IRS.

Harvey explained that what matters most for him is making a strong public statement, bearing witness to the government’s violence: “Our reason for non-cooperating with the IRS is a reluctance to support war preparations, especially nuclear weapons, and the export of arms and military forces to many places around the world.

Others have gone a lot further in their war tax resistance than we have, and we honor and respect those people.

For [them], the most important thing is to withhold money from the IRS at all costs.”

That, he acknowledged, is not his style of war tax resistance.

“There are and there have been war tax resisters who have gone that far.

My friend Ammon Hennacy [the legendary pacifist connected with the Catholic Worker movement] was one.

Our approach is more complicated to describe and more flexible in practice.”

He scoffed at a news article that described him as “unwilling to pay one penny to the IRS.”

“We have three cars,” he noted, referring to the federal tax on gasoline that he pays every time he fills up at the pump.

About 35 supporters turned up for the second auction, this time held at the IRS office in Lewiston, Maine.

Demonstrators read excerpts from letters to IRS officials and to President Clinton urging them to call off the auction.

(As at the first auction, money was given away, this time to groups doing the kind of work tax dollars could fund: $500 to the local Abused Women’s Advocacy Project and $500 to a local chapter of Habitat for Humanity.)

Still Here

In the end, Elizabeth’s mother entered the winning bid for the house at $15,633. The town clerk and town selectman, who bid at the first auction, entered the only other bid of $8,000. The latter two were clearly miffed at having lost such a “bargain.”

(One war tax resister described them as “a picture of greed thwarted.”)

The clerk, clearly irate, asked, “Why was it okay for her [Elizabeth’s] mother to bid, but not for me?”

A week later, Arthur Harvey reflected on the clerk’s comment, questioning in turn the propriety of the town officials’ taking advantage of a family in a weakened financial position.

“That does not seem to me to be a proper thing for a town official to do,” he said.

Elizabeth Gravalos thinks the answer to the town clerk’s question is obvious: “The two of them were trying to take our house from under us, whereas my mother was trying to help us out, to help us continue our way of life here.”

Though Gravalos had dissuaded her mother from bidding at the first auction, she did not try to stop her at the second.

“It was harder to lose the blueberry field [at the first auction] than I thought.

I just didn’t feel I was ready to lose the house,” she admitted.

Harvey and Gravalos calculated that the house was worth somewhere between $10,000 and $15,000 and suggested that $13,000 would be a reasonable bid.

Max and Emily were in favor of a friendly bid; Max especially did not want to have to move.

“The alternative,” Arthur noted, “would be to go the Randy and Betsy route and not countenance a friendly bid and then risk eviction.

We, as a family, decided not to go that route.”

(He was referring to Randy Kehler and Betsy Corner, war tax resisters from Colrain, MA, whose supporters maintained an 18-month-long occupation/vigil after Kehler was arrested in and his and Corner’s house was auctioned off by the IRS.)

In the end, Arthur admitted, the auction “was something of a letdown.”

The IRS got a fair amount of money, $39,460 in all more money, he speculated, than it would have gotten if the family had filed and paid taxes all along.

Gravalos reflected, “Betsy and Randy did a better job at resisting the IRS than we did.

But each family has to draw its own line.

I really did not want to stage an occupation [as they did].”

So what does it mean for war tax resistance when the IRS manages to walk away with such a considerable sum?

Interestingly, Gravalos and Harvey do not think of themselves as having failed.

Along the spectrum of war tax civil disobedience, they are tax resisters rather than tax refusers.

(War tax resisters do not willfully hand over money to the Pentagon, but if the government nonetheless forcibly seizes money from them, they take those lumps, as it were; war tax refusers tend to put up more of a fight and are unwilling to let the government collect any money or assets whatsoever.)

But they believe both resisters and refusers provide witness to the backward priorities of the federal government.

“When it comes to war tax resistance,” Gravalos adds, “anything is better than nothing.”

Their 51 years (between them) of resistance to military spending and the redirection through the years of those war tax dollars is not to be scoffed at.

And what of the future?

Gravalos and Harvey do not hesitate when they are asked whether or not they will continue their war tax resistance.

Says Arthur, “We will continue our stand of non-cooperation, but we will certainly make sure not to find ourselves in such a position where we own so much property.”

And Elizabeth adds, “I do feel that the risks of paying taxes are greater than the risks of refusing to pay them.”

“He almost failed to graduate from high school after refusing to sign a loyalty oath to the laws and constitution of the United States.

‘I could support the Constitution,’ he said, ‘but I certainly wasn’t going to support all the laws.

They told me I was failing the rest of the students in my home room.

But I didn’t have much loyalty to my home room.’

Eventually the school gave him his diploma anyway.”

“In Michigan, a man who had recently returned from India lent him a book by Gandhi.

He was immediately struck by Gandhi’s arguments in favor of self-reliance and against excessive consumption.

In the late 1950s, Harvey spent six months in prison in Sandstone, Minnesota, for invading a missile base in Nebraska with a group of fellow peace activists.

‘Prison was a blast.

I was in there with one of my very best friends [Ammon Hennacy] and we played horseshoes and Scrabble and spent lots of time in the library.’

His tenure as library clerk ended when he refused to compile a list for the prison authorities of the books each prisoner was borrowing.”

A newspaper article

on educational outreach efforts by the pacifist non-violent action group Peacemakers, quoted Harvey on the nature of the group: “We are a radical pacifist organization.

We are against war preparation and against use of income tax for war purposes.

Our members also oppose mandatory registration for the draft.

However, we are not communists.

We believe the best defense is a strong spiritual one, in the tradition of the Indian leader Gandhi.”

The Sun-Journal of Lewiston, Maine, covered the tax auction in a pair of articles:

“Hands off our homes”

Couple protests on day before auction

by Mary Lou Wendell Sun-Journal Staff Writer

Auburn — The message on one of the placards held by many of the 50 or so protesters marching down Center Street morning was simple: “Honor family values.

Hands off homes.”

Accomplishing their goal for the day was not going to be so simple, however.

They were on their way to Lewiston to convince the Internal Revenue Service to halt the sale of property seized for nonpayment of taxes.

Arthur Harvey, who, before it was taken, owned the house and land in Hartford Center together with his wife Elizabeth Gravalos, led the march.

In his pants pocket was a letter the group eventually hand-delivered to the Lewiston IRS office on Main Street after walking there from the Auburn Mall, which took about two-and-a-half hours.

The note detailed the couple’s reasons for not paying federal taxes.

Funds collected by the federal government will “support war preparation of all kinds,” the typewritten letter read.

“This is not acceptable to our moral and religious beliefs.”

In , IRS agents served Harvey and Gravalos with a seizure notice for their property, which includes a small home and out-buildings, a 13-acre blueberry field, and 21 acres of two combined woodlots.

Selling blueberries and pansies, which is how the couple earns their living, brings in a total of $18,000 a year, Harvey said.

Based on those earnings, the government calculated Harvey and Gravalos owe $62,000 in unpaid taxes and penalties for , according to the couple.

A spokeswoman for the IRS in Boston said she would not confirm the amount owed because of disclosure and privacy laws.

Furthermore, the couple wrote in their letter to the IRS, “it is inconceivable that a family could be subject to a 49 percent tax rate, especially a low-income family including two children.”

Harvey and Gravalos have a daughter in college and a teen-age son, Max, who also marched on .

IRS

spokeswoman Peggy Riley did say the sealed-bid auction will go on as scheduled at at the town office in Hartford Center.

And if minimum bids were offered, the house and property will be sold, she said.

The minimum bid for the single family home was $20,476.98, Riley said.

The total minimum bid for everything else, which is divided into three properties, is roughly $16,000.

Against a backdrop of car dealerships, retail outlets and quick-change oil places, the protesters, who came from as far away as Chicago, walked in groups of three and four down Center Street.

Some came from New Hampshire and Vermont.

Most were from Maine.

Many of the protesters were also war-tax resistors and friends with Harvey and Gravalos.

Some had never met the couple but were marching to support their cause.

Sheila Dormody, a member of the 800-member organization, Peace Action Maine, pays her taxes, she said.

But she had sympathy for Harvey and Gravalos because she opposes disproportionate military spending, she said.

As the group hiked along, making their way across the Longley Bridge and around downtown Lewiston, Dormody passed out red fliers decrying the practice of “bloating the Pentagon… starving our communities.”

“This year Congress will give the Pentagon $7 billion more than requested,” the filer stated.

Education, mass transit, housing programs, job training and environmental spending are all the things that will be cut in order to pay for increased military spending, it said.

If the property is indeed sold , “we’ll have to find some place we can rent,” Gravalos said as she walked.

“I have a friend in Buckfield who has offered land so I can plant my pansies.”

Her husband thought it was a mistake to buy land, Gravalos said, adding he may have been right.

In hindsight, Harvey said, he would have preferred renting over owning property, which can be taken away.

But, while he and his wife have always paid their state and local taxes, he’s not sorry for not paying federal taxes, he said.

“We both understood the risk and we accepted it,” Harvey said.

It’s a matter of “personal responsibility.”

Withholding federal taxes is “a job that we can do,” he said.

Home survives IRS sale

Some of tax protesters’ Hartford property sold

by Judith Meyer Special to the Sun-Journal

Hartford — As sealed bids were opened morning, Arthur Harvey and Elizabeth Gravalos heard an Internal Revenue Service employee award three pieces of their property to others, but their home was spared, at least temporarily.

The couple, who are vocal about their resistance to paying federal taxes to a government that they say is spending irresponsibly, were served a notice of seizure on their property in .

That property was offered at a public sale in a sealed bid process inside the Town Office while a large crowd of supporters from throughout New England and reporters waited outside on the lawn morning.

Harvey and Gravalos, who say they earn about $18,000 a year growing blueberries and pansies, owe the IRS $48,555 in unpaid taxes .

Their properties were seized to satisfy that debt.

Attending the bid opening were dozens of other tax resisters, including one couple who carried a large painted poster proclaiming their nonpayment of federal taxes since .

The properties offered for sale included the couple’s home, which is not equipped with running water or electricity and which uses an organic compost septic system, a small house lot, a 21-acre wood lot and a 13-acre blueberry field.

No bids were submitted for the house, and a second sealed bid opening has been scheduled for at the IRS office in Lewiston.

If the property is not sold at that time, said IRS agent Diane Santoro, who conducted the sale, the federal agency will re-evaluate the $20,476 minimum bid established for the property.

Bids were opened inside the Town Office, which was restricted to bidders, the property owners, town and federal officials and five media representatives chosen by Capt. James Miclon of the Oxford County Sheriff’s Department from a pool of reporters standing in the side yard.

The couple’s children, Emily and Max Harvey, purchased the small house lot for $727, using money 16-year-old Max had earned raking blueberries, beating out a $600 bid from the town of Hartford.

Gravalos was visibly upset that the town bid on the property.

The Town Office stands directly across the street from Gravalos’ house on Route 140, and the piece of property the town bid on was being considered as a new Town Office site.

The couple’s wood lot was sold for $10,000 to Kathleen Hutchins and Linda Rowe, both of Hartford, beating out a $9,560 bid for the land.

Hutchins is the town’s tax collector, clerk, treasurer and administrative assistant, and Rowe is a selectman, but both women said they bought the land as private citizens.

The third piece of property, the blueberry field that has been cultivated for the past eight years by Harvey and Gravalos, was sold to Alan Noyes of Hartford.

Noyes, who left immediately after the bid opening, indicated that he liked the view at the property and would be willing to talk to Harvey and Gravalos about some kind of arrangement to continue farming the land.

Harvey said after the sale, which lasted less than 10 minutes, that he and his family intended to remain in Hartford, would continue to live in their home and would continue farming blueberries on fields they planned to lease from other property owners.

“The good news is that nobody bid on our house,” Gravalos told the crowd after the sale was finished, and Harvey expressed his pleasure at seeing so many people supporting their cause.

“This is not a victory or defeat for anyone,” Harvey said.

“It’s just a part of life.”

That observation drew a large round of applause from the crowd.

And although the IRS seizure is nearly complete, Harvey said his views on tax resistance haven’t changed and he has no plans to pay any money to the federal government.

Harvey has not paid federal taxes , and Gravalos hasn’t paid .

Supporter Jim Stockwell of Albion said, “I think (Harvey and Gravalos are) very proud of what they’re doing.”

Stockwell praised their resolve to stand firm for their beliefs against increased military spending and decreased spending for education and health care.

Lee Holman, a supporter and neighbor of Harvey and Gravalos, said the couple’s commitment to paying local and state taxes and resisting paying federal taxes comes from their desire to “redirect tax dollars to build real security in this town instead of investing in a false sense of security” with the federal government.

The couple can redeem their properties in the next 180 days if they pay the bid price, plus another 20 percent, and any costs associated with the sale to the IRS.

IRS

agent Santoro declined to talk to reporters before or after the sale.

Along with that second article was this sidebar:

Anti-tax group pays off liens of five families

Hartford — The tax resisters who demonstrated in support of Arthur Harvey and Elizabeth Gravalos say they are not against America’s tax system in itself and support payment of local and state taxes to help their own communities.

What they protest is the federal government’s use of the tax money, a use that they claim they have no control over.

In an effort to show support for the local property tax system, the group of resisters, who are calling themselves Spears into Pruning Hooks, walked into the Hartford Town Office just before the public sale of the Harvey/Gravalos property and paid off outstanding tax liens for five local families.

Harvey said the group paid nearly $2,200, choosing the liens to be paid off based on whether the property owner had children and actually lived in Hartford, rather than being a part-time resident.

The tax resisters did not have contact with the property owners; the payoffs were arranged through the Town Office.

The group originally offered to pay seven liens, but only five were paid because two of the families declined the group’s offer.

Tax Collector Kathleen Hutchins said the payment retired tax liens for property owners Joseph Bedard, Ann Carro, Penny Stubbs, Matthew Piantone and James Guilmet.

According to Hutchins, the property owners who declined the resisters’ offer of payment said they did not agree with Harvey and Gravalos’ stand on tax resistance.

Hutchins, who said the town has never seized any property for nonpayment of property taxes, indicated that there are others in Hartford who oppose the stand taken by the Harvey-Gravalos family.

Speaking for the group, which still has $800 in an account reserved for payment of other tax liens, Harvey said Spears into Pruning Hooks plans to continue raising funds and making goodwill gestures for struggling local taxpayers.

Harvey and Gravalos were still at it :

Federal income tax

Resisters keep incomes below filing threshold

by Kelly Morgan StaffWriter

Hartford — While many people across the country will be rushing to meet today’s deadline for filing federal income taxes, Arthur Harvey will more likely be home binding books or working on the mowers he’ll soon use to cut his blueberry fields.

It’s not that the 72-year-old organic farmer, inspector and book seller has filed early this year.

Instead, Harvey, who lives with his family across from the town office on Main Street, has not paid federal income taxes .

He won’t pay because he is opposed to where his dollars would be spent.

“My fundamental objection is to nuclear weapons,” he said Thursday while seated at a small table off his kitchen, surrounded by copies of the collected works of Mahatma Gandhi.

“And also to sending U.S. military forces to other countries.”

Harvey and his wife, Elizabeth Gravalos, 61, have joined as many as 200 Mainers and 10,000 people nationally who refuse to pay their federal income taxes in protest of military spending.

“We say about 8,000 to 10,000 people,” said Ruth Benn of the Brookly, N.Y.-based National War Tax Resistance Coordinating Committee on , “but it’s really hard to count.”

Benn said many, like Harvey and Gravalos, keep their incomes low so they won’t have to pay.

Many others protest by refusing to pay federal taxes on their phone bills, another action that’s difficult to track.

According to information from IRS spokeswoman Peggy Riley, who’s based in Boston, the federal government faces what it calls a “gross tax gap” of $300 billion a year.

The gap, Riley explained, “is the difference between what taxpayers should pay and what they actually pay.”

Riley said the IRS does not track those who refuse to pay on the grounds of opposing military spending.

Personal property seizures and deductions from paychecks are tools the IRS uses to collect unpaid tax dollars.

In , Harvey and Gravalos nearly lost their home and 13 acres of blueberry fields they farm in Hartford.

At an auction after the properties were seized, Gravalos’ mother bought back the house.

Their daughter Emily later received back the blueberry fields in a trade after the man who had purchased them found farming difficult, Harvey said, laughing.

Harvey, Gravalos and their son Max continue to farm the fields today.

They use wood heat and kerosene lamps and drive old Volvos.

Harvey sells books on the teachings of Gandhi, which he purchases from India, through the on-line marketplace Amazon.com.

The only electricity in the house comes from a small solar panel that runs a laptop computer and, on sunny days, a copier in a back room.

Because Gravalos now works as a part-time massage therapist, she does pay Social Security taxes, Harvey said.

But she hasn’t paid income taxes .

The two file separately, each having to earn less than $3,100 in order to fall below federal tax filing requirements.

Harvey and Gravalos have taken part in efforts of the War Tax Resistance Resource Center of Maine.

People affiliated with the organization often hand out fliers at IRS centers on tax deadline day.

Larry Dansinger, a Monroe-based representative of the group, said that people are expected to be handing out fliers from Portland to Ellsworth

He himself doesn’t pay federal phone taxes.

“In our calculations, about 50 percent of every (federal income) tax dollar that people pay is going either directly or indirectly for military purposes,” he said.

Not paying, he added, “is not a nice, easy thing to do.”

We have reached the end of the NWTRCC national gathering, held this time at the Earlham School of Religion in Richmond, Indiana.

The bulk of ’s portion of the conference was largely a series of workshops on subjects like:

basic war tax resistance (what we call informally “WTR101”)

the peace tax fund campaign

military counter-recruitment and support for conscientious objectors

advanced war tax resistance

the history of Quaker war tax resistance

“economic disobedience”

the militarization of U.S. foreign policy and its alternatives: a case study in East Africa

war tax resistance questions & answers

conscientious objection to the military and taxes for the military

Some of these sessions ran at the same time, and for a couple of them (the WTR101 and history of Quaker war tax resistance) I was one of the presenters, so I only was able to take notes on one of the two “economic disobedience” sessions.

In that session, Erica Weiland began by summarizing my report on the Spanish “desobediencia integral” movement and then she brought us up to date with new developments.

These include the fair.coop “Earth cooperative for a fair economy” and its alternative currency, the “FairCoin,” which is somewhat Bitcoin-like but is explicitly designed to promote a certain sort of economic model.

(I’ve looked at some of the FairCoin outreach material, but whether from translation difficulties or my amateur economics knowledge, I can’t quite figure out what makes it tick.)

The war tax resistance movement in the United States has made some contact with this Spanish movement and we’ve started to explore situating our work in the terminology and framework of this “comprehensive disobedience” movement, which helps to connect our work with the emerging sharing economy movement, Occupy, the modern environmentalist movement, and things of that sort.

Erica was joined by Jim Stockwell, who gave us a more historical perspective of how this sort of thinking weaves into a long thread connecting decentralism, Georgism, cooperative villages, the thought of Ralph Borsodi, and other related ideas.

Erica added some insight from her research into the cooperative movement among African-Americans in the Reconstruction and post-Reconstruction periods.

Erica then introduced us to some of what the Strike Debt group have been doing lately.

This group grew out of Occupy and the Rolling Jubilee project.

One of the actions associated with this group was the purchase and retirement of a large amount of medical debt.

They then purchased and retired some student debt in the same way.

Debts like these are packaged into groups based on how likely the debts are to be recovered.

Those debts that are very unlikely to be recovered, often because the debtor is too poor to pay, can be purchased for pennies on the dollar.

By retiring these debts, the project can reduce the stress of collection agency harassment on such people.

They are also trying to unionize students who have debt to particularly exploitative colleges to encourage them to strike collectively for debt relief.

The Strike Debt Operations Manual was republished a while back with a new chapter on tax resistance, which was largely based on NWTRCC literature.

We brainstormed some ideas for trying to connect the U.S. war tax resistance movement with a movement for a larger grassroots economic transformation.

Some ideas we tossed around included:

the use of community development loan funds (such as Equity Trust) as investments for our alternative funds or as ways of shielding assets from the IRS in less-visible zero-interest loans

encouraging the various regional alternative funds to coordinate their grants so as to support projects that build new economic models in a more systematic and well-publicized way

creating an alternative fund that uses a different granting model — rather than giving grants annually at a particular time, give grants at irregular intervals in reaction to acute needs.

War tax resistance legal advisor Peter Goldberger

Yesterday, attorney Peter Goldberger, who has worked closely with the war tax resistance community for many years, brought us up to date on how the climate for pressing for the legal recognition of conscientious objection to military taxation in the courts has changed in recent years, particularly in the wake of the recent “Hobby Lobby” case.

When I read the “Hobby Lobby” ruling, I didn’t see much that seemed encouraging.

There were some hopeful-sounding parts of it, like this bit from the majority opinion’s summary:

The belief of the Hahns and Greens implicates a difficult and important question of religion and moral philosophy, namely, the circumstances under which it is immoral for a person to perform an act that is innocent in itself but that has the effect of enabling or facilitating the commission of an immoral act by another.

It is not for this Court to say that the religious beliefs of the plaintiffs are mistaken or unreasonable.

But the justices were careful to remind war tax resisters that we’re out of luck if we think we can use the Religious Freedom Restoration Act to assert the legal validity of our beliefs:

United States v. Lee, 455 U.S. 252, which upheld the payment of Social Security taxes despite an employer’s religious objection, is not analogous.

It turned primarily on the special problems associated with a national system of taxation; and if Lee were a RFRA case, the fundamental point would still be that there is no less restrictive alternative to the categorical requirement to pay taxes.

The “Hobby Lobby” opinion itself expands on this a bit:

Lee was a free-exercise, not a RFRA, case, but if the issue in Lee were analyzed under the RFRA framework, the fundamental point would be that there simply is no less restrictive alternative to the categorical requirement to pay taxes.

Because of the enormous variety of government expenditures funded by tax dollars, allowing tax-payers to withhold a portion of their tax obligations on religious ground would lead to chaos.

Recognizing exemptions from the contraceptive mandate is very different…

The “Hobby Lobby” dissent goes so far as to describe the opinion as one that grants new powers of legal conscientious objection to just about everybody except tax resisters:

In a decision of startling breadth, the Court holds that commercial enterprises, including corporations, along with partnerships and sole proprietorships, can opt out of any law (saving only tax laws) they judge incompatible with their sincerely held religious beliefs.

If you hoped the dissenters might be more sympathetic to the use of the RFRA in war tax resistance cases, you won’t find much support for your hopes here.

The dissenters for the most part seemed inclined to generally weaken the reach of the RFRA.

But again, this was all just my first impression, and I’m not a lawyer.

Peter Goldberger is, and he’s worked in the area of conscientious objection and the free exercise clause for a long time, and he gave the “Hobby Lobby” decision a lot of thought and found some interesting angles.

For one thing, when the Supreme Court used conscientious objection to military taxation as a reductio in Lee and Hobby Lobby, it did so in cases that themselves did not concern conscientious objection to military taxation.

They assumed that the government could not accommodate the beliefs of such resisters without “chaos” breaking out — that it would be too onerous for the government to accommodate such objectors.

But there was nobody there to argue the objectors’ side and to present evidence that this was not necessarily true.

Perhaps in a more direct case, objectors might be able to present evidence that would convince the court to revise its point of view.

The Hobby Lobby case also seems like it might usefully expand the right of conscientious objectors to military service.

Previously the court had ruled that there was no constitutional right to conscientious objection, and so objectors enjoyed only those rights that Congress had chosen to grant them by statute.

The language of Hobby Lobby seems to suggest that now, the government will have to prove a fairly strictly-defined compelling government interest if it wants to restrict the rights of draftees or military personnel who are or who become conscientious objectors for religious reasons.

For example, Goldberger suggests, Congress has defined legal conscientious objection to military service so that it only applies to pacifists — that is, to people who object to all war.

It does not apply to religious objectors, for instance Catholics, who belong to a “just war” tradition which asks them to evaluate war by certain criteria and conscientiously object only to a subset of them.

Goldberger suggests that the new RFRA standard, as elaborated in Hobby Lobby, could invalidate this and force the government to accommodate more varieties of religious conscientious objection.

Goldberger thinks this might also be a good time for a challenge from someone of the variety of war tax resisters who resists by putting the amount of the tax into an escrow account and telling the IRS that it may seize the money if it wants to, but that the resister is unwilling to pay it voluntarily.

Since the IRS could accommodate the resister’s religiously-based conscientious objection, without undue difficulty for the government and without unleashing “chaos,” by simply seizing the money, perhaps the objector has a legal right not to be further penalized or subject to legal sanctions of other sorts for such a stand.

Finally, since Hobby Lobby (somewhat notoriously) decided that corporations can, under some circumstances, have some rights of their own under the RFRA, this may be a way to ask the Court to revisit a case similar to the Priscilla Adams case that it turned down on procedural grounds back in the day.

Adams was a Philadelphia Yearly Meeting (a Quaker corporation) employee and a war tax resister.

Her employer went to court to try to gain the right not to have to withhold taxes from her salary as this would force them to participate in violating her conscience.

Myself, I don’t see a lot of use in looking to the legal system for help, but I think this sort of thing is interesting and kind of fun to explore.