This is the thirtieth in a series of posts about war tax resistance as it was reported in back issues of The Mennonite. Today we continue to work through the early 1980s.

War tax resisters’ hour comes round at last in Bethlehem

In the General Board of the General Conference Mennonite Church met.

On the ongoing issue of tax withholding, GB agreed to submit a resolution to delegates at Bethlehem to “authorize the officers [of the conference] to test the constitutionality of [the tax withholding] requirement… by refusing to serve as tax collectors in cases where individual employees have asked that their federal income taxes not be withheld from their wages, in order that they may conscientiously refuse to pay for war.”

Peter J. Ediger contributed another of his prophecy-poems to the issue, saying in part:

The church which seeks to save her security by following only “legal, legislative and judicial avenues” to salve its war tax conscience will lose her life; the church willing to lose her security in supporting non-registrants for the sake of Christ will find life.

A special edition prepared for the triennial conference summarized the progress of the Conference task force on the war tax issue:

At the triennial sessions, the conference authorized the General Board to initiate a judicial action seeking exemption for the General Conference Mennonite Church from withholding taxes from the income of its employees. James Gingerich, Duane Heffelbower, Larry Voth, Robert Hull, and Vern Preheim were appointed as a judicial action committee to implement the resolution. William Ball was engaged as legal counsel. In , Ball advised the conference that the general climate in the United States, the attitude of the present government administration, and the attitude of the Supreme Court as evidenced by some recent decisions dealing with religious conviction or conscience and taxes were such that the likelihood of the General Conference accomplishing its objectives through a judicial action was virtually nil. The committee recommended and the General Board concurred to put the judicial action on hold and to bring the matter once again to the conference for further discernment and decision. A more detailed report and a recommendation from the General Board to the conference that we honor the requests of employees to not withhold taxes on their wages will be sent to the congregations in advance of the triennial sessions.

Throughout , while pursuing judicial action, we also continued to encourage the enactment of World Peace Tax Fund legislation.

An editorial in the edition described the upcoming decision thusly:

At a special midtriennium conference in Minneapolis in , GC delegates voted 1,218 to 134 in favor of urging their General Board to “use all legal, legislative and administrative avenues for achieving a conscientious objector exemption from the legal requirement that the conference withhold income taxes from the wages of its employees.” If no solution could be found within three years, the GB was to bring the matter back for further action. At Estes Park in , a judicial test case on the issue was okayed by a vote of 1,156 to 353.

Bethlehem will bring GC delegates face to face with the fact that all three avenues, at present, look like dead ends. As a result, the GB is proposing that the conference stop withholding taxes from salaries of employees who request such action in order to “assert the higher claim of Christ’s law of love.”

If approved, the resolution would take the conference one small but significant step into the sphere of divine obedience/civil disobedience. It could become the most formidable — and challenging — business item for GCs, despite the fact that several other organizations have already taken the same action.

In advance of the Bethlehem gathering, the text of the proposed resolution was released in the pages of The Mennonite:

Bethlehem resolutions (1): tax withholding

Among the resolutions for consideration by delegates at the General Conference Mennonite Church Triennial Sessions… is a formal action authorizing conference officers to stop withholding taxes from the salaries of its employees as required by U.S. law. It also encourages Canadian Mennonites to obtain relief from the same requirement by Revenue Canada.

The conference’s General Board… will bring the "Resolution on Faithful Action Toward Tax Withholding" to Bethlehem delegates as their recommendation for resolving the moral dilemma which church officials feel they are facing. If approved, the resolution could take the conference into divine obedience/civil disobedience.

The following is the text of the resolution:

As Mennonite Christians we seek to be biblically obedient, submitting to such injunctions as Romans 13:7, “Pay taxes to whom taxes are due,” but also Romans 13:8, 10, “Owe no one anything except to love one another… love does no wrong to a neighbor; therefore love is the fulfilling of the law.” We accept our subordination to government and our obligation to pay taxes. However, we must witness to governments our conviction that war and preparation for war do wrong to our neighbors and are contrary to the will of God as revealed in the teachings of Jesus Christ and his death, resurrection and ascension to lordship.

Thus we urge our governments to sharply reduce military spending and use our resources for life-affirming purposes. Furthermore, just as conscientious objectors have received exemption from military service, we also seek legislation exempting conscientious objectors from paying taxes for military purposes. Thus we continue to work in the United States for passage for the World Peace Tax Fund Act and in Canada for the Peace Tax Fund, which would allow individuals to designate all of their federal taxes for peaceful purposes.

Both the U.S. Internal Revenue Service and Revenue Canada require the General Conference Mennonite Church to violate the consciences of its employees who are conscientious objectors to paying taxes for military purposes.

In the United States, we have thoroughly explored all legislative, administrative and judicial avenues for obtaining a conscientious objector exemption to these withholding requirements, as we resolved at the Minneapolis midtriennium conference. Our explorations have convinced us there is no likelihood of relief in the near future for conscientious objectors to military taxes. The time has come when, like Peter and the apostles, “We must obey God rather than men” (Acts 5:29).

In Canada, equally thorough explorations of similar avenues for seeking a conscientious objection from withholding requirements have not yet been accomplished. We commend the “Resolution on Security and Disarmament” of the Canadian Mennonite Conference in and the work of the Canadian Tax Task Force under the sponsorship of MCC Canada Peace and Social Concerns. We encourage Canadian congregations to continue study of materials made available on the issue of military taxes.

As delegates to the triennial sessions of the General Conference Mennonite Church, we therefore:

- Authorize the conference officers to test the constitutionality of the withholding requirements in the United States and to assert the higher claim of Christ’s law of love by refusing to serve as tax collectors in cases where individual employees have asked that their federal income taxes not be withheld from their wages in order that they may conscientiously refuse to pay for war preparations. These employees will be treated similarly to the way General Conference treats ordained ministers, i.e. as self-employed persons, in that their earnings will be reported to the U.S. Internal Revenue Service, but no federal income tax withheld.

- We request that the Conference of Mennonites in Canada consider means to obtain relief from Revenue Canada withholding requirements as these apply to General Conference Mennonite Church employees.

- We shall inform the U.S. government of this act of conscientious objection to their withholding requirements. We shall again urge them to provide exemption from these requirements and exemption for people of peacemaking conscience from military use of their tax money.

At this moment of decision we commit ourselves to surround with our prayers the General Conference staff and government officials who will be involved in this action and all those individuals who refuse in conscience to pay taxes for war preparations, however costly their witness may be.

A more extensive report on the triennial put it this way:

Jim Gingerich of Moundridge, Kan., chairperson of the conference’s judicial action committee, reported that the suit against the IRS approved at Estes Park was, in the opinion of constitutional lawyer William Ball, almost certain to fail. Little progress was being made on the legislative or administrative fronts either. In light of this, the General Board was recommending that the conference honor the consciences of its employees who request that their full salaries be paid to them, allowing the employees themselves to remit to the IRS what their consciences would allow.

After Robert Hull, secretary for peace and justice, had reviewed the experiences of other groups which had attempted similar actions, Duane Heffelbower of Reedley, Calif., outlined the points of the resolution in detail and spoke of their possible ramifications. “We could scarcely devise a softer velvet glove to cast at the feet of the IRS,” he said. “But the action does show our corporate willingness to stand beside our employees. What will the government do? We don’t know.”

What followed was probably the most vigorous interchange of viewpoints by GC delegates of the entire week. Nearly two dozen speakers took their turns at the mikes before the vote was called for. Viewpoints on the resolution ran the gamut from disassociation with it to praising God for it.

“We believe that the Bible says we ought to pay our taxes. We want to be separated from and not have any part of this action,” said Paul Goossen, Wayland, Iowa.

“This resolution is creating an impossible situation for our government,” added John Voth of Meno, Okla. “We have emphasized that we love our enemy. I wonder whether the government has become our enemy. Have we adopted the same big-stick approach that we so often have criticized?”

Others, however, urged the conference to push ahead with the proposed action. “Mennonites took a stand against slavery even though it was unpopular,” said Mark Winslow, Allentown, Pa. “Today, the nuclear arms race is the primary social sin of our day. We should take a stand regardless of the fact that it may be unpopular.”

Lois Barrett, Wichita, Kan., observed that “in the U.S., disobeying the law is the time-honored way of changing the law,” noting that the cause of civil rights in was advanced primarily through civil disobedience.

H.A. Fast of North Newton, Kan., prompted the only round of applause during the lengthy discussion. “We refuse our selves in service, but we say nothing about our taxes,” Fast said. “I have said to the government, ‘You can’t take my body to fight a war.’ I have said, ‘You can’t take my son.’ And now I am saying, ‘You can’t take my money, either.’ ”

When it was over and the ballots counted, the resolution passed by a 70 percent majority. [1,128 to 457]

One of the characteristic features of the discussion on tax withholding, as well as other debates during the week, was the sensitivity and willingness to listen with which delegates approached the microphones. Several told of how they had come to the convention ready to vote one way, but were now moved to vote another. Phrases such as “I want to respect your point of view…” or “I’m willing to learn more…” preceded many of the speeches. And the tough debates of Bethlehem, during which emotions ran high and convictions deep, never seemed to overshadow the determination by participants to celebrate their common identity, their peoplehood, their unity. After the convention, many attributed that prevailing unity to the moving of the Spirit.

Delegates at the conference were treated to a performance of The Plow and the Sword, a musical about American Mennonites during the Revolutionary War who disputed whether or not it was proper to pay taxes to the rebellious Continental Congress. “The play’s content was powerfully pertinent to the delegates meeting at Bethlehem who discussed present-day responses to war taxes.”

The Conference’s test cases began in :

Non-withholding tax action begins, seven make request

Acting on the basis of a resolution adopted by General Conference delegates at Bethlehem , conference treasurer Ted W. Stuckey on issued the first paychecks on which federal income taxes were not withheld.

Seven employees of the denomination’s central offices made the request that the taxes not be withheld, so that they can remit to the IRS personally the amount of federal taxes their consciences will allow, given the U.S. government’s high rate of military spending.

Those making the request were Robert Hull, secretary for peace and justice; Lynn Keenan, Mennonite Voluntary Service associate director; Paula Diller Lehman, secretary for youth education; Fred Loganbill, assistant for peace and justice; John Sommer, overseas personnel secretary; Meribeth Sprunger, secretary for mission communications; and Elizabeth Yoder, general editor. Several others have indicated that they may be willing to take part in the action at a later date.

Stuckey said that, beginning with the paychecks, the seven will have state and social security taxes deducted but be treated like self-employed persons as far as federal income taxes are concerned. Under such a classification, they would be required to submit quarterly estimated tax payments to the IRS.

The seven plan to make a portion of those quarterly payments but put the balance — the amount they feel they cannot voluntarily pay because of high U.S. military spending — into a special account at General Conference central offices.

Stuckey and general secretary Vern Preheim informed Commissioner Roscoe L. Egger, Jr., at IRS headquarters in Washington by letter of the conference’s action, the motivation of employees for requesting the procedure, the reasons for the church’s granting the requests, the identities of the seven employees and the location of the account to which the IRS may initiate collection procedures. “We’re trying to be completely open and above board with them about this matter,” he said. Copies of the letter were also sent to IRS offices in Wichita, Kan., and Austin, Texas, as well as to state and federal legislators.

The pay period is the first opportunity for the conference to implement the “Resolution on Faithful Action Toward Tax Withholding” adopted by delegates to a churchwide convention in Bethlehem, Pa., on . There, conferees voted 1,128 to 457 to “authorize the conference officers to test the constitutionality of the withholding requirements in the United States and to assert the higher claim of Christ’s law of love, by refusing to serve as tax collectors in cases where individual employees have asked that their federal income taxes not be withheld from their wages, in order that they may conscientiously refuse to pay for war preparations.[”]

Miscellany

A note in the edition mentioned that the Historic Peace Church Task Force on Taxes had decided to go all-in on the World Peace Tax Fund bill, promoting “dunamis groups which approach congresspersons in a spirit of compassion rather than confrontation… to obtain a dozen more co-sponsors for the WPTF bill in the coming year.”

The edition noted that “MCC U.S. Peace Section has put together a War Tax Packet, designed to equip individuals and groups with a variety of resources for study on the question of paying taxes for war. Cost is $2.”

The edition included a profile of Cornelia “Nellie” Lehn, whose war tax resistance became the focus for much of the debate that overtook the General Conference Mennonite Church. It summarized this as follows:

Nellie was… dealing personally with the perplexing issue of war taxes. She liked to read Bible verses that say to pay your taxes, but began to wonder why she did not concentrate equally on those saying to love your enemies and put your sword away.

Finally she felt she could not pay that part of her taxes going to war purposes and asked the General Conference office not to withhold any of her salary for taxes. “The time comes when you have to cut through all the complexity and be obedient,” she says, reminiscent of her stand earlier in life.

At the triennium she stated her views. The conference continues to work on this issue even today.

I’m surprised I haven’t come across this amusing example of war tax resistance outreach before:

Mennonites in Harrisonburg, Va., gathered on to attach over $300 to about 75 helium-filled balloons. Each balloon, in addition to a five- or ten-dollar bill, carried a note from a participant explaining why he or she had withheld the money from current income taxes. “Because we are Christians who are trying to follow the peaceful way of Jesus, we cannot support this country’s military build-up,” said many of the notes. “Instead, we have chosen to ‘waste’ our money in a more constructive way.” Participants read Scripture, sang, danced, prayed, confessed their sins, and clowns passed out jelly beans as the balloons rose.

The shift of focus to “Peace Tax Fund” legislation would aggravate a decline in interest in real war tax resistance in the General Conference Mennonite Church that continues to the present day. Clearly, some Mennonites perceived this danger, as Robert Hull wrote an article to defend the push for such a law:

Is “peace tax” just a diversion of energies?

An argument by some war tax resisters is that any peace tax fund is a means for conscientious objectors to salve their conscience with regard to diverting their own taxes, and that this provision then will encourage such COs to be quiet and passively accept the warmaking of governments which will continue more efficiently without their dissent.

When I have explored this argument, I almost invariably discover that the war tax resister speaking is drawing upon an analogy made with the 20th-century U.S./Canadian history of conscientious objection to military service.

The Civilian Public Service camps of World War Ⅱ by and large had this “quietistic” effect. However, it should be noted that the provision for COs in World War Ⅱ came about because the government remembered the difficulties it had encountered with historic peace church resisters in World War Ⅰ. Similar spokespersons on the eve of World War Ⅱ stated their convictions to “draw the line” again if acceptable provisions were not made.

But even during World War Ⅱ, the legal criteria for CO classification in the United States were broadened by the Supreme Court to include all religious objectors, then during the Vietnam War to include people holding a belief equivalent to that in a Supreme Being (Seeger, ), and later to all people morally, ethically or religiously opposed to all war (Welsh, ). In the draft registration debate in , projections by the Selective Service of future CO claimants extended to 40 percent of all registrants. It seems reasonable to conclude that at least one cause for this large increase in the potential CO population is a result of the public visibility of thousands of young men performing alternative service during the Vietnam War.

The recent response of the U.S. Selective Service to its own projections has been to develop plans for CO alternative service which seek to once more “contain” the CO visibility by centralizing the program under direct Selective Service administration in order to meet military mobilization priorities. This policy is in turn quite likely to produce non-cooperators who will have registered but then find that such an alternative service program is unacceptable to their conscience. A significant number of such non-cooperators would increase the already more than 500,000 draft-eligible young men who have not registered.

Twentieth-century CO history has lodged anomalous laws within the government structures. That is, if these laws are interpreted by relatively tolerant regulations, the CO population may grow uncontrollably large; if the laws are interpreted by repressive regulations, the number of non-cooperators may grow uncontrollably.

Now let’s pursue this analogy with regard to peace tax legislation and war tax resistance. I am convinced that Parliament or Congress will never enact peace tax legislation until the war tax resistance movement grows so large that such laws come to be viewed as an expedient accommodation, as Civilian Public Service was viewed on the eve of World War Ⅱ.

But several differences between the two are significant. Bear in mind that peace tax legislation provides for the taxpayer to claim he or she is a CO and that the burden of the challenge and rebuttal lies upon the government. Additionally, peace tax legislation’s provision for income tax forms and information materials to describe the military proportion of the federal budget in some detail will ensure that a far greater percentage of the taxpayers become aware of the peace tax alternative than the percentage of draft-age men who were made aware by the government of the CO alternative from World War Ⅱ through Vietnam. Finally, the peace tax legislation provides for the diversion of CO taxpayers’ “military taxes” into a trust fund. This is intended to result in a direct drain out of the general treasury available for war preparations.

Thus the peace tax legislation further raises people’s consciousness. If peace trust funds in the United States and Canada are administered as the legislation intends, many millions of people will choose to support peacemaking alternatives to conflict rather than supporting warmaking preparations, and a “democracy of defense” may develop: those who rely on military weapons can pay for them without coercing the contributions of those who place their reliance upon other alternatives.

If the CO eligibility criteria are interpreted too restrictively, or inaccurate portrayals of the military proportion of the federal budget are published, or CO taxpayers’ funds are demonstrably rechanneled into the warmaking treasury, then increased numbers of informed citizens may respond with direct tax resistance.

The government will thus have on its hands another significant anomalous law, one by which millions of citizens can measure the government’s tendency to override their democratic rights in its clearing of the path toward war.

This then is the educational strategy behind the peace tax effort as I see it. The legislation will reach millions of people with the message that there are alternatives to paying for the war system. It will provide a step which millions of citizens can take, and whose aggregate pressure for peacemaking will be enormous, without overwhelming risk to the individual taxpayer. After all, it is at least in part the risk involved in war tax refusal which keeps it an infinitesimally small protest movement in the total population.

I hope that thousands of active peacemakers will heed the call to war tax refusal and that the pressure for peace upon the warmaking tendencies of government will grow. As it does, I believe it will prove disastrous if the peacemaking community has no legislative proposal to put forward which will secure as much of the “democracy of defense” goal as possible, and to which the government can turn as an accommodation.

The edition reported on the annual conference of the Church of the Brethren (Anabaptist cousins of the Mennonites). Among the notes:

The Church of the Brethren has long supported members who conscientiously object to the payment of war taxes. Some members wish to refuse to pay taxes but are unable to because the taxes are withheld by their employers. The delegates approved a paper that gives guidance to church institutions whose employees request, for reason of conscience, that their taxes not be withheld. The annual conference recommended that all legal possibilities be explored first but affirmed civil disobedience for both individuals and institutions when it is a matter of conscience.

This news comes from the edition:

A United Methodist congregation in New Haven, Conn., backing their pastor’s right to refuse paying federal taxes for military use, has declined to turn over his salary to the Internal Revenue Service. Carl Lundbord [sic], pastor of First and Summerfield United Methodist Church, has withheld federal income taxes in both and , telling the IRS his “obligations as a Christian and as a citizen are no longer reconcilable. The 50 percent of my taxes that support the military I cannot pay.” IRS ordered the church to withhold the pastor’s salary until the amount was paid. But church members voted on to reject IRS’s demand.

An article in the edition:

“War tax” dilemma continues for many U.S. taxpayers

Our ancestors migrated to the United States so that they would not be forced to participate in European wars. Eventually this government respected their deeply held beliefs about peacemaking and granted them the right to register as conscientious objectors.

Today we find ourselves in a technological age in which our money is more useful to the military than our bodies. So we are being forced by law to participate financially in the preparation for war, which violates the biblical command to love our neighbors as ourselves. When Caesar’s demands conflict with God’s, we cannot blindly obey our government.

These words from John S. and Sara L. Wengerd’s letter to the Internal Revenue Service echo the convictions of nearly 60 individuals and families who chose to contribute to Mennonite Central Committee U.S. Peace Section in lieu of paying a portion of their income taxes that would have been used for military purposes.

For some, the contribution was a symbolic amount, such as $7.77. For others, it equaled the 36 to 54 percent of their tax dollars that would have financed military activity. That portion is commonly referred to as a “military tax” or a “war tax.” In another case, a couple’s taxes had already been withheld by the Internal Revenue Service, so they donated an amount equal to their military taxes, which they had already paid.

In all cases, these individuals felt that silent compliance with the tax collection process would be a violation of their consciences and religious convictions against killing and participating in war in any way. Many noted that their dilemma of conscience could be ameliorated by passage of the World Peace Tax Fund (WPTF) Act…

Meanwhile, the federal government is attempting to crack down on various types of tax protests. People who object to paying taxes for military purposes may face stiff penalties designed to deter those trying to evade tax collection or destroy the tax system.

The Tax Equity and Fiscal Responsibility Act of instituted an automatic $500 penalty for individuals filing “frivolous” tax returns. The penalty can apply to people who take unallowable deductions, credits or exemptions or give incomplete information on their tax returns.

Those taking “war tax” deductions or credits or claiming an excessive number of exemptions to reduce their tax liability could be subject to the new fine. Several conscientious military tax resisters have received notices from the Internal Revenue Service that the penalty has been imposed, according to the May–June issue of Center Peace, the news journal of the Center on Law and Pacifism.

Robert Hull, peace and justice secretary for the General Conference Mennonite Church, suggests that conscientious objectors to military taxation take steps to distinguish their non-payment of military taxes from secular tax protests and evasion schemes. If taxpayers correctly compute and report the amount owed and indicate in an attached letter that they cannot with a clear conscience pay the military-related portion, their tax returns will go directly to the Internal Revenue Service Collection Division instead of to the overloaded Audit Division.

Hull suggests that this action be accompanied with letters to legislators to communicate the religious and moral grounds for such action, and to demonstrate the need for remedial legislation such as the World Peace Tax Fund.

Bill Samuel, member of the WPTF steering committee, suggests that taxpayers write a contract on the back of their check to IRS stating that deposit of the check constitutes a legally binding agreement (contract) that the money will not be used for military purposes. Courts have held that contractual checks involving private parties are legally binding, but it is uncertain whether or not IRS would abide by the contract.

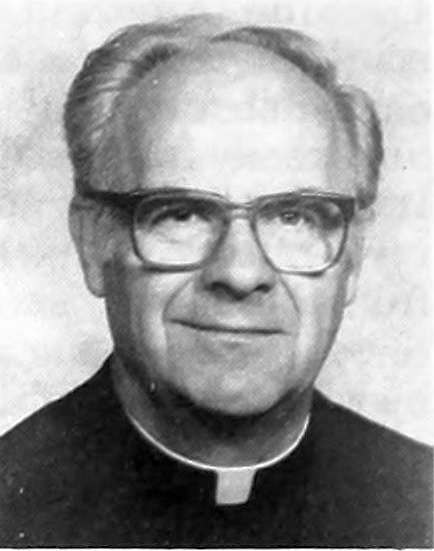

John R. Dyck

A article profiled Canadian war tax resister John R. Dyck. Excerpts:

Tax withholding is also a Canadian issue

All his life, John R. Dyck of Rosthern, Sask., has been a law-abiding citizen. He’s never been to court. But he expects that to change when Revenue Canada catches up with him for non-payment of taxes.

Dyck is one of a small but growing band of Canadians who are refusing to pay the portion of their income taxes they feel is designated for the military. Instead, they are calling for an alternative “peace tax fund” which would use their tax money for peaceful purposes.

Since that alternative does not exist and Dyck withheld 10.5 percent of his taxes for and for , he expects a court order to arrive eventually.

John R. Dyck is not a young radical defying authority. Officially he is retired (though not willingly or inactively) and has given the better part of the past two decades to service with the Mennonite Central Committee, Mennonite Foundation and the MCC Food Bank. A sudden stroke forced him to slow down over a year ago, but he has recovered and calls it “a real miracle.” Now he can go on serving, and he places military tax resistance in that category.

The decision did not come easily or hastily. “I don’t know where it (a conviction) began,” he commented during an interview at this year’s annual meeting of MCC Canada in Saskatoon. He had come to listen to the discussion and spend time with his brother and fellow peace-seeker, Peter J. He remembers that “Cornelia Lehn made us sit up and think” in .

John began with his tax return, filed while the Dycks were in Jordan under MCC and able to observe firsthand the effects of military exploitation. He sent two checks to Revenue Canada, asking that the smaller one be used only for peaceful development work. He heard nothing further and assumed that both checks flowed into government coffers.

Along with his tax return he sent only a letter of concern. But with his return he again enclosed two checks, one for Revenue Canada and a second made out to the Peace Tax Fund. Revenue Canada replied that such a fund did not exist (legally) and demanded payment in full. Dyck then sent the check to the Victoria, B.C.-based Peace Tax Fund and began correspondence with government officials to explain why. “I want to do things correctly and openly,” he says.

Now Dyck is expecting a day in court. It is bound to come, since Revenue Canada wants his money and must obtain a court order before garnisheeing his account at the Rosthern Credit Union. The sooner the better, he adds, since it may help establish a right of conscience that would allow other people to divert their hard-earned tax money from bombs to working for peace. He also hopes to find a sympathetic lawyer to handle the case.

“I think a lot of people would rather not talk to me about it,” he says, summing up the reaction to his protest. So far, any criticism has been muted, though one friend told him, “I admire you for it, but you’re wrong.” Paula, his wife, is supportive, but most fellow members at Rosthern Mennonite Church are either uninformed or indifferent.

John R. Dyck firmly believes, “We don’t need the military.” The threat of nuclear war hanging over the world means Christians must resist militarism with renewed vigor. “I see this (nuclear holocaust) coming and we’re accountable. The handwriting is on the wall.”

Dyck adds that there is a growing network of people asking about the peace tax fund, though the actual number withholding taxes is still small. (Ernie Hildebrand, a teacher at the Swift Current (Sask.) Bible Institute, is another Mennonite who is doing so.) “But people must think this through carefully,” Dyck concludes. “You can’t legislate a thing like this… I’m glad the Lord led us to this position.”

As the General Conference pushed ahead with its support of war tax resisting employees, with the blessing of the majority of conferees, the U.S. “Peace Section” seemed more reluctant to take a stand, at its meeting. From the edition:

While agreeing that the church has an important role to play in saying no to preparations for [nuclear war], the members struggled with the place of military tax resistance as a method of saying no.

Several members observed that the constituency is “not of one mind on this matter,” while Darrel Brubaker of Philadelphia, Brethren in Christ representative, urged that “here is one place we need to be leaders more than representatives.”

After the matter was tabled overnight for further reflection, the group affirmed a recommendation commending the General Conference for the serious attention it has given the issue and urging churches to work more diligently at the process of prayerful discernment of their response to this issue.

The resolution also strongly encouraged constituents to initiate further action in support of the World Peace Tax Fund bill, which would provide a legal alternative to the payment of taxes for military purposes.

War tax resister Don Schrader wrote in on to insist that Mennonites can best criticize revolutionary and other violence if they are careful not to support violence with their taxes:

Until our nonviolence becomes revolutionary, revolutions will be violent.

[A]s long as well-fed U.S. pacifists pay war taxes to support the imminent nuclear terror and mass murder of our planet and the dictatorial repression of Central America, what integrity do we have in questioning or condemning those peasants’ use of violence for survival.

To be peacemakers in this perilous age, we must refuse to pay war taxes, we must renounce all materialism which breeds militarism, and we must denounce foreign policy regardless of the risks for our community standing and employment.

Over four years ago I confronted the question “How can I speak for peace and pay for war,” and I became a war tax resister.