How you can resist funding the government →

about the IRS and U.S. tax law/policy →

IRS incompetence →

enforcement effort/results →

Government Accountability Office reports on

Every year, the Government Accountability Office puts out a “High Risk” list of those government activities that have “greater vulnerabilities to fraud, waste, abuse, and mismanagement.”

This year, the IRS makes the list twice — once for its doomed efforts to modernize its databases (I’ve blogged about this before, see and for instance), and once for its lagging ability to go after tax evaders and resisters:

In recent years, the resources IRS has been able to dedicate to enforcing the tax laws have declined, while IRS’s enforcement workload measured by the number of taxpayer returns filed has continually increased.

Accordingly, nearly every indicator of IRS’s coverage of its enforcement workload has declined in recent years.

Although in some cases workload coverage has increased, overall IRS’s coverage of known workload is considerably lower than it was just a few years ago.

Although many suspect that these trends have eroded taxpayers’ willingness to voluntarily comply and survey evidence suggests this may be true the cumulative effect of these trends is unknown because new research into the level of taxpayer compliance is only now being completed by IRS after a long hiatus.

Further, IRS’s workload has grown ever more complex as the tax code has grown more complex.

Complexity creates a fertile ground for those intentionally seeking to evade taxes and often trips others into inadvertent noncompliance.

IRS is challenged to administer and explain each new provision, thus absorbing resources that otherwise might be used to enforce the tax laws.

Concurrently, other areas of particularly serious noncompliance have gained the attention of IRS and the Congress such as abusive tax shelters and schemes employed by businesses and wealthy individuals that often involve complex transactions that may span national boundaries.

Given the broad declines in IRS’s enforcement workforce, IRS’s decreased ability to follow up on suspected noncompliance, the emergence of sophisticated evasion concerns, and the unknown effect of these trends on voluntary compliance, IRS is challenged on virtually all fronts in attempting to ensure that taxpayers fulfill their obligations.

IRS’s success in overcoming these challenges becomes ever more important in light of the nation’s large and growing fiscal pressures.

Accordingly, we believe the focus of concern on the enforcement of tax laws is not confined to any one segment of the taxpaying population or any single tax provision.

Our designation of the enforcement of tax laws as a high-risk area embodies this broad concern.

Furthermore…

The Commissioner of Internal Revenue has made strengthening enforcement a high priority, but IRS has not yet materially reversed enforcement declines, in large part because unbudgeted expenses and demands for improved taxpayer service have confounded IRS’s intentions.

Enforcement staffing decreased over 21 percent , and individual audit rates are below the levels of , even after recent increases.

IRS lacks current data on the effects of these declines on compliance.

For example, IRS’s estimate of the gross tax gap the difference between taxes owed and taxes paid (over $300 billion) was largely based on extrapolations from data.

Without current information on noncompliance, IRS cannot effectively target its enforcement resources, risks wasting resources by auditing compliant taxpayers, and is impeded in identifying changes to laws or regulations that could reduce noncompliance.

Senators Max Baucus and Chuck Grassley, the top Democrat and Republican on the Senate Finance Committee, issued a press release to convey their outrage or what-have-you.

Grassley summarized the new report this way:

For , while collections increased by $10 billion, unpaid debts

increased by the same amount. During this same time, the

IRS

wrote off from 31 percent to 46 percent of unpaid debts because it

essentially ran out of time to collect these debts. For

, the

IRS

classified only $100 billion out of $290 billion of unpaid tax debts as

collectible. Of the $100 billion potentially collectible debt, the

IRS is

actively pursuing only $25 billion with $2.5 billion being shelved because

of a claimed lack of resources. The longer a debt is outstanding, the less

likely it will be collected. Any business person can tell you that. Knowing

that the

IRS

isn’t going to collect the debt also gives tax cheats additional

incentives not to pay.

The senators conclude: “When all is said and done, over half of the tax debt

inventory that the

IRS

resolves will come from writing off the tax or being prevented from collecting

it under the 10 year statute of limitations.” The numbers in the report

specify this a little more precisely: 20–28% of these tax debts were “abated…

which may have been appropriate” and 31–46% were “written off due to statutory

limits on how long

IRS

could pursue the debt.” Only between 34–41% of the tax debts that were

“resolved” involved the

IRS

actually getting its hands on the money.

Expect the next Congress to try to come up with some ways to squeeze a little

more blood from that stone.

The report has some interesting background details on the

IRS

collection process, and a nice flowchart (see page 7 of the report) of how tax

debts get routed around (and sometimes stall) in the process.

Here, for instance, is the initial phase of the process for people who do not

file, spelled out nicely:

IRS

first is to send a “30-day letter” that includes a proposed assessment of

tax, penalty, and interest. The letter is to instruct the taxpayer on

possible ways to respond, such as by accepting the proposed assessment;

filing an original return; providing evidence that there is no filing

requirement; or appealing the proposed assessment to

IRS’s

Office of Appeals. If no response is received to the 30-day letter within the

allotted time,

IRS is

to send a 90-day statutory notice. The statutory notice is to contain

information similar to the 30-day letter and information on the taxpayer’s

right to petition the Tax Court. If

IRS

does not receive a response within the allotted time, the tax, penalty, and

interest on the return are to be assessed.

IRS’s

practice is to send up to four balance-due notices at 5-week intervals for

the amount owed. Six weeks after the fourth balance-due notice,

IRS is

to forward any unpaid accounts to

IRS

staff who are to try to collect the unpaid amounts through other phases of

the collection process — the telephone or in-person contact phases.

There were also some nuggets of information about new

IRS

enforcement-related projects. A few caught my eye:

Electronic Lien — to process over a million liens each year

Streamline and expedite lien filing, reduce lost lien reports, and ensure

prompt payment of lien filing fees by making process electronic.

Reduce costs for lost lien research and analysis by 15 percent in

and 40 percent in

. Similar savings in these 2 years in

lien filing fees. Collect additional revenue by raising

IRS’s priority against other creditors.

Bulk Electronic Levy

Automate the process for delivering levy notices to and processing

responses and remittances from financial institutions and large

employers, including the posting of levy payments to taxpayer

accounts.

Reduce the cycle time for sending levies. Reduce mailing costs. Expedite

posting of payments to taxpayers’ accounts.

Camera cell phones

Improve (1) productivity of revenue officers in determining asset

valuation, (2) communication between

IRS

and taxpayers, and (3) employee safety on field visits.

Increased employee and taxpayer satisfaction.

I assume that last bit means that when the

IRS

comes a-callin’, they’ll be whipping out their phone cameras to snap a quick

picture inside your doorway or outside your driveway so they can look at the

photos later and see if anything is worth stealing.

Auditors reviewed the records of 213 former employees brought back onboard in the Covington, Ky., office and found 96 had separated from the agency while being investigated.

Of those, 19 had potential tax code violations, 4 had accessed taxpayer accounts without authorization, 13 had falsified forms, 2 had misused email or equipment, and 6 had been accused of misconduct such as absences without leave, workplace disruption or failure to follow instructions.

Remember the myRA? No?

Well, it wasn’t very memorable.

It was a way to try to get more people to start up retirement accounts by making it cheaper and easier and less risky.

President Obama launched the program in .

Here’s what I had to say about it then.

In short, I wasn’t impressed.

The accounts would ultimately be invested in government bonds, and so would constitute a loan to the government.

It seems, though, that very few people were interested in participating in the program.

It’s now been scrapped.

“Nearly half of

IRS’s

Senior Executive Service (SES) is eligible to retire” (along with 21.3% of

the rest of the employees).

“IRS

exit survey results found 32 percent of separating employees indicated poor

office morale strongly influenced their decision to leave.”

Reductions in staff from 2011 to 2017 “have been most significant within

IRS

Enforcement, where staffing declined by 27 percent.”

“IRS

officials told us that, unlike other areas where the agency is legally

required to perform certain functions, the agency has flexibility to

curtail many enforcement activities when attrition rates increase. Auditing

tax returns, for example, is a critical part of

IRS’s

strategy to ensure tax compliance and address the tax gap, or the

difference between taxes owed and those paid on time. Our analysis of

IRS

data shows the number of individual returns audited has declined each year

between fiscal years 2011 through 2017, a 40 percent decline.” Audits of

large corporation have fallen even more dramatically.

Revenue Officers are the

IRS

employees who handle individual cases of tax noncompliance, including

meeting face-to-face with such scofflaws and initiating enforcement actions

like filing liens and seizing property. “[T]he total number of

revenue officers at

IRS

declined by nearly 40 percent from fiscal years 2011 through 2017, and

entry-level revenue officers declined by 86 percent during that same

period.”

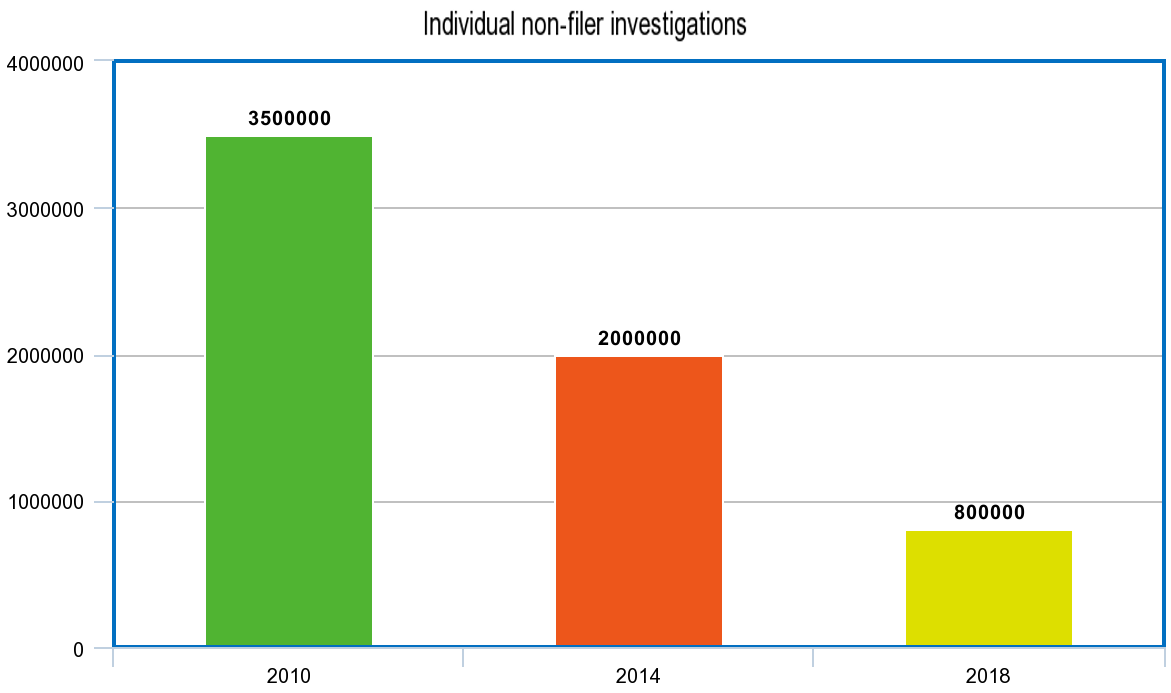

“IRS

decided to scale back nonfiler investigations in light of declining

staffing, according to

IRS

officials. We reported in tax year 2010 that

IRS

started 3.5 million individual nonfiler cases and 4.3 million business

nonfiler cases. In tax year 2014, nonfiler cases dropped to 2 million for

individuals and 1.8 million for businesses, a reduction of 43 percent and

58 percent, respectively. More recently in fiscal year 2018,

IRS

data show nonfiler investigations declined to 0.8 million for individuals

and 0.4 million for businesses.”