Tax resistance in the “Peace Churches” →

Quakers →

20th–21st century Quakers →

Mary Bye

the American Revolution was portrayed as the culmination of a tax revolt in this educational cartoon short that aired frequently between Saturday morning cartoons in the United States in

War tax resistance in the Friends Journal in

your humble editor and his little brother in

I was a little too young to be much of an observer of the political scene, but I remember as being something of an orgy of innocent patriotism.

America was sick of being cynical and wanted to go back to being stupid — besides, the Vietnam War was mostly over, at least for most Americans, and we’d given Nixon the heave-ho — and so there were plenty of red-white-and-blue commemorations of the bicentennial of the signing of the Declaration of Independence.

The Friends Journal wasn’t quite so willing to get with the star-spangled program.

In particular, it intensified its coverage of war tax resistance during the bicentennial year.

The issue was the Friends Journal’s first special issue devoted to war tax resistance.

It starts off with a couple of inspiring quotes on the subject from A.J. Muste and David Dellinger, then opens with a piece by Jennifer S. Tiffany on how she met the challenge of deciding whether to pay or to resist.

Excerpts:

This fall was a time when I was grappling a great deal with the question of war tax resistance.

To start with, I knew and had known for a long time that I could not be clear in paying taxes to any state which would use them to pay for war-making.

Particularly, I could not contribute to the nuclear death race between this nation and the Soviet Union.

Perhaps it goes back to the civil defense tests and simulated nuclear air-raids which had terrified and confused me when I was a child.

Anyway, the imperative, the need to keep clear of war (to use Bruce Baechler’s words), had always been strong.

I had been acting on it, in small ways, for a long while-avoiding earnings beyond the taxable minimum, for example, and claiming six “peace dependents” on my W-4 form when my income did exceed this minimum.

I also corresponded with the IRS concerning my views and actions.

However, a disclarity still existed regarding full resistance, with all the possible ramifications on my life and lifestyle.

The question was, to me, was I strong enough and centered enough to maintain a taxable income level, restructure my life in such a way as to prevent eventual government levies, and go on with my resistance?

Could I face creatively the possibility of putting a good deal of energy into court cases with the eventuality of prison?

I came into meeting for worship one morning at the height of these grapplings.

As I settled in, I was astounded.

Somehow the fears and conflicting leadings within me changed.

They did not fade or diminish, but grew into context.

The spirit of the meeting, the presence of loving Friends, who loved whether or not they agreed with one another’s approach, literally overwhelmed me.

The presence of God wholly covered the gathering, and finally clearness came.

Our God, the Presence in our worship and acts of witness, is a gentle, healing, loving, empowering God, one who speaks strongly and softly from within us.

At the same moment as making demands on our lives, this Presence says, “You need not fear; if you act on this I will sustain and strengthen you throughout the whole process.

I am…” This was a moment of resolution for me.

I was no longer entangled in a negative refusal to pay taxes, but was healed and sustained and led to a positive witness.

I could go on.

It is in this context that tax resistance has its roots and life.

War tax resistance, any resistance to war and to those authorities which bring about war, is not a negative presence: every no implies a yes, and this no to killing and death can be a yes to healing and life.

Within tax resistance dwell seeds which can help a whole new order to grow — seeds which deny fear and powerlessness in the face of death; seeds which lead us to the creation of healing alternatives to structures which sustain death.

As John Woolman puts it, “to turn all we possess into the channel of universal love becomes the whole business of our lives.”

I can speak only of my moment of resolution, the clearness and joy which is liberated in my life through a tax witness.

As I see it, this issue of Friends Journal is not a coercive tool, saying “you must for these reasons refuse to pay your taxes or I will no longer judge you to be a good Friend.”

The point of this issue is not to define terms for judgment, to draw lines of inclusion and exclusion.

Our faith is an experiential one, and your experience of real clarity is as right and valid for you as mine is for me.

The point is to lay ourselves open to what speaks truthfully in us, to really open ourselves to the spirit which utterly denies war, to really grapple with the questions this raises and the demands it makes on our lives.

One of those questions has to do with tax resistance.

This is an invitation to grapple with it, and a reaching out which says there is a great company of people, past and present, who have done so.

There is a process of empowerment, growth and the birth of community among people which can take root through tax resistance.

First comes the knowledge that the authorities of death are not all-powerful, that the laws and structures which sustain any war machine are in fact quite weak.

As Marion Bromley says in her article, “What can they take away that is of real value?”

Second dawns the realization that alternatives are possible: through the flaws in the death order, we glimpse the order of life.

And, although such consequences as possible imprisonment or loss of property, and the inward struggle with fear, are largely borne alone, the vision is shared by a growing company of sisters and brothers.

Isolation is hard to feel when so many glimpse the possibility of a new order — an order beyond war.

Finally and especially, tax resistance often grows as an act of ministry, an act of obedience to the loving and healing spirit.

War tax resistance is one aspect of a community set on fire with the presence of a gentle, empowering God.

Bruce Baechler thought the question of whether Quakers should resist war taxes was a no-brainer.

He wrote in from prison (where he was doing time for draft resistance) with this defense of war tax resistance.

Excerpts:

Do Friends support war?

At one time this could be answered with a “not at all.”

These days, though, it seems to depend on how one defines support.

Friends, generally, denounce war in the strongest terms. Indeed that’s all many people know about us.

But for the most part Friends can no longer claim to renounce, or “utterly deny” war.

Friends today are not compelled to bear arms… instead of fighting with outward weapons ourselves, we are merely asked to buy the weapons through taxation, and leave the dirty work to others.

And most of us do.

Yet we cling to our traditional peace testimony, often expressed as early Friends did in the Declaration of :

We utterly deny all outward wars and strife, and fightings with outward weapons, for any end, or under any pretense whatsoever; this is our testimony to the whole world.

This is strong language.

One cannot, without being hypocritical, utterly deny something and still give it material support.

But most Friends do.

There are many reasons given for paying taxes.

Most of these are quite valid, if one thinks of tax resistance as a protest.

But I see a difference between various types of protests, such as vigils and letters to Congress, and nonsupport, or remaining clear of war, as by tax resistance.

In protesting, one makes her/his views known, but leaves it up to someone else (the government) to make the decision.

Governments are not noted for their receptivity to the pacifist message, and it is unlikely they will be in the near future.

I am not deriding protest — much has been accomplished through it.

I am just saying that it is not enough.

Nonsupport, on the other hand, emphasizes individual responsibility.

To refuse to pay one’s taxes is to accept responsibility for the way they would be spent, and to refuse to allow them to be spent for immoral purposes.

Tax resistance should not mean just withholding taxes from the government.

An integral part of tax resistance is to redirect the money normally spent for taxes into life supporting channels.

In many places this is done through Alternative Funds, where the resisters in a community band together to make most effective use of the money.

Thus not only is money diverted from warmaking, but at the same time it is made available as a resource for peaceful activities.

Perhaps the biggest problem most Friends have with not paying for war is that it is illegal.

One faces the prospect of prison for it, and this alone is enough to make most people give it only superficial consideration.

Hopefully the World Peace Tax Fund, if established by Congress, will alleviate some of this problem in much the same way that the Conscientious Objector provisions in the draft laws gave a legal alternative to the army.

But in the meantime the problem remains.

Friends have often suffered for their beliefs.

Throughout our history large numbers of Friends have been imprisoned, tortured, and killed for preaching and practicing the message of the Inward Light.

Would you stay away from a Meeting for Worship if to go meant certain arrest?

Would you attend but not speak when moved, if that would be dangerous (a situation facing Korean Friends today)?

Would you join the army to avoid prison?

Kill to avoid being killed?

The question is where to draw the line.

When, to you, does the personal suffering involved in a course of action outweigh the reasons for taking that course?

Each person must decide for her/himself.

Another response to the problem of imprisonment is that if any substantial number of Friends did engage in tax resistance, the likelihood of their being imprisoned would be small, and some provision in the law would probably be made for them, thus eliminating the problem and encouraging more people to resist.

Jack Cady shared his long, meandering letter to the Director of the IRS.

Excerpts:

[O]ur first confrontation… will be the examination of my tax return.

I expect the examination is prompted by my refusal last year to pay half of my income tax.

I will refuse. to pay half of the tax again this year, although because of withholding, your agency already has most of the money.

I refuse to pay half of the tax on various grounds, some of which are moral, some of which are legal.

The refusal is prompted by the expenditure by our government of over fifty percent of tax monies on the maintenance and purchase and use of armies and weapons.

Through its agency, Internal Revenue Service, the United States Government seeks my complicity in the violation of twenty centuries of moral teaching.

The government is in further violation of the Constitution of the United States.

It is also in violation of various international treaties and agreements, and is, in fact, engaged in crimes against peace and crimes against humanity.

In requiring that I pay taxes for the support of war, planning for war, offensive weapons and the maintenance of a standing armed force sufficient to engage combat on a worldwide scale, the U.S. Government through its agent IRS is in violation of the First Amendment to the Constitution, which guarantees my religious freedom.

I am a member of the Port Townsend meeting for worship of the Society of Friends (Quaker).

The Quaker belief and effective detachment from war dates from the beginnings of the Society in .

The precedent of refusal to pay war taxes in America dates from when John Woolman, John Churchman, and Anthony Benezet refused to pay for the French and Indian wars.

Nonviolence and refusal to pay or endorse either side in a combat dates in U.S. history from the revolution when Quakers who refused to kill were stoned or beaten under the brand of Tory.

I claim my devout belief in God and the injunction that we may not kill as sufficient reason to refuse this tax.

I would expect that opposition to this view would also have to overcome three hundred years of Quaker nonviolence and two hundred years of U.S. acceptance of Quaker attitudes that insist on nonviolence.

[I]n asking taxes, the U.S.A. through its agent IRS seeks my complicity in crimes against peace and crimes against humanity as defined by the Nuremberg Principles.

These principles hold that citizens of a nation are guilty of crimes committed by that nation if they acquiesce to those crimes when, in fact. a moral choice is open to them.

In requiring that I pay taxes to support a war industry and armed forces capable of contending on a worldwide scale, the U.S. Government is threatening both my moral and my physical existence.

I am not being protected, because the U.S. builds atomic weapons, B-1 bombers, atomic submarines, poison gas, lasers, rocketry, napalm and all of the other expensive paraphernalia of war.

These do not protect me.

They invoke the suspicion and fear of other nations, and they provoke among other nations the building and stockpiling of similar weapons.

[T]he U.S. now gives every indication that it is, in fact, not a nation of laws but a nation of men and corporations.

This, despite the resignation from office of Richard Nixon and Spiro Agnew.

I charge that the freedom of the citizen is largely illusory, and that the payment of taxes, the keeping of tax records, the invasion of privacy by IRS and other agencies of government, the making of rules by agencies (rules that have the force and effect of law but which are not to be challenged in courts), the maintenance of records or files on the political, religious, economic and moral statements and actions of the individual, the power to levy fines and licenses by agency rule, and the presumption by government that citizens are guilty of any agency charge and must therefore bear the burden of proof of their innocence; all of these show the citizens of the U.S. are no longer free.

I have two main intentions in this tax refusal.

The first is quite clear.

I do not intend to pay for the destruction of other human beings, nor endorse by word or deed the crimes of the United States.

The second intent is a little more nebulous but it is just as strong.

It is strong because I love my country.

In this refusal I intend that the United States will display by its action whether or not a citizen, raised to believe in U.S. principles of freedom, equality, protection under the laws; raised, in fact, under statements like, “With a proper regard for the opinions of mankind,” can indeed trust and believe in the way he has been raised.

Either the Constitution is sound or it is not.

The U.S. will either honor its national and international commitments or it will not.

The courts will either face issues or the courts will duck them.

…If the rules of IRS are bigger than the Constitution, the UN Charter, the Nuremberg Principles and the Christian teaching of two thousand years, then I believe it is time that the U.S. acknowledge this…

The next article came from Marion Bromley.

Excerpts:

Ernest and I began a tax refusers’ newsletter soon after our marriage in .

In all the time since, only a tiny proportion of Friends and other pacifists have become tax refusers, and we sometimes try to understand why.

It has been, for us, more a personal imperative than a carefully reasoned political position, though we have done what we could to expound on all aspects of refusing to allow one’s labor to be taxed for war and weaponry.

Most people, whether they are pacifists or not, seem to respect our “right” to refuse taxes when we have a chance to explain how we feel about it.

In turn we have to accept the “right” of others to continue to pay large sums in taxes, even though the U.S. budget continues to be overwhelmingly devoted to war and the war system.

Before 1800 taxes were levied largely for specific things such as bridges, schools, highways.

A levy for war was as separate as the others.

Quakers, Mennonites and a few others who had strong scruples against paying for the militia or for gunpowder refused to pay and sometimes suffered distraint of goods or imprisonment for their stand.

When all these items began to be lumped together into one, general tax, it was no longer so simple an issue.

Some, with a considerable feeling of relief, began to pay; others paid more out of frustration.

And one of the most potent testimonies against war during became lost.

Now, in , probably no reasonable person believes that the billions to be spent for weapons research, deployment of armies and nuclear weapons, nuclear submarines prowling the ocean floor, planes carrying nuclear bombs, and intercontinental ballistic missiles will be in any sense a “defense” for anyone.

Since such policies and practices will probably lead to a nuclear holocaust at some future time, maybe distant, maybe near, paying for these weapons comes close to being an evil act.

It may be that the reason most Friends do not see it in that light is that they are conscientiously committed to liberalism — to the direction the federal government began in and from which there is now no retreat.

The federal government, in order to ease suffering and to maintain control over its own populace, began to assume some social responsibility.

Possibly most Friends are in the same position as those who began paying the “mixed” taxes in .

But in the whole world has witnessed the kind of horror that a powerful military state can unleash even without resort to the ultimate weapon.

…In an individual such behavior would be deemed madness.

Would a mad individual be permitted to continue such activities because that individual was also performing some useful services?

Another aspect of liberalism that has probably influenced Friends greatly in the past fifty years is the commitment to law.

I cannot explain why most Friends think it is almost a religious principle to honor the law and the courts, while I feel it is very low on my list of loyalties.

My religious instincts are insulted when I observe a judge in the robes of a priest, high above others in the courtroom, the witnesses and observers in pews and the bailiff enforcing a hushed silence.

My view is that this holy-appearing scene is for the purpose of defending the property and the power of the people who have those commodities.

It is the same in a socialist or a capitalist state.

It is certainly an acceptable arrangement for people to agree on certain codes or laws, agreements about property.

I would not disobey laws for frivolous reasons.

But I have no qualms about disobeying laws which would force me to pay for murder and other crimes related to the war system.

Civil disobedience which requires long-term adherence, such as arranging to make one’s living without the withholding system, perhaps is considered impossibly difficult by many conscientious people.

For many Friends, commitment to a service type vocation seems to require “fitting in” with a professional life style.

The scale has not been invented which could balance service that is beneficial to others with the negative effects of supporting warmaking and possibly silencing one’s conscientious stirrings.

The only contribution I can make to such considerations is my testimony that refusing to pay income taxes has proved to be a blessing in many ways.

For one thing, it resulted in our “backing into” a simple life style, consuming less than we otherwise would.

Friends who have valued simplicity know of its blessings — the simple life is more healthful, more joyful, more blessed in every way.

A new friend we met following seizure of Gano Peacemakers’ property, our home for 25 years, wrote us after moving from Cincinnati that he supposed we were having a very sad summer at Gano this year, knowing that we would be evicted in the fall.

This notion was quite contrary to the way we felt.

We were enjoying the time here more than ever before.

The growing season seemed more productive than ever, and the surroundings more beautiful.

We were working very hard, preparing leaflets, signs and press releases, corresponding, thinking of new ways to tell everyone who would listen that the IRS claims were fraudulent and politically motivated.

We expected to be evicted but never had the feeling that we would “lose” in the struggle.

(The following paragraph, concerning the eventual IRS surrender in the Gano Peacemakers case, is largely obscured in the PDF.)

One of the pleasant feelings we have about the reversal of the sale (besides knowing that we can continue to live on these two acres) is that many people have told us they got a real lift when they heard that some “little people” had prevailed in the struggle with the IRS.

We had the feeling that our daily leafleting and constant public statements during the seven months’ campaign had, at the least, the effect of showing that people need not fear this government agency.

People do fear the IRS and that is an unworthy attitude.

What can they take away that is of real value?

Jack Powelson struck a dissenting note, listing war tax resistance among a number of popular Quaker positions that he felt to be sentimentally motivated and economically naive.

Excerpt:

Friends are concerned about paying taxes to a government that allocates a high proportion of its budget to the military.

But we also know that if enough Friends refused to pay taxes so that the government was seriously impeded in its operations, the first items to be cut would be welfare and education, and the poor would suffer.

The Journal then quoted John A. Reiber on his vision for “a cultural revolution with political implications, not a political revolution with cultural implications.”

Excerpt:

The most effective social changes are not going to come from within the system, but without it.

We must realize that the vast, impersonal and powerful institutions are not intrinsic to our survival and well-being, but, in fact, extrinsic and harmful.

What we must do to achieve a cultural (r)evolution is to, first of all, withdraw our support of our unendurable, tyrannical and inefficient institution of the government.

One way of doing this is through tax resistance.

But tax resistance, by itself, is only a part of the solution.

Money, time and energy should be channelled into alternatives to our technological mass consumption/ mass waste society, our irrelevant and oppressive educational institutions and our mass media which don’t meet our informational needs.

Craig Simpson next gave a report on war tax resistance as it was practiced internationally.

Excerpts:

During the Peace Research and Peace Activists Conference in Holland in , I met Susumu Ishitani, a member of the Japanese Conscientious Objectors to War Taxes Movement (COMIT).

The group is the first of its kind in Japanese history and was started in .

It is made up of Christian pacifists — Mennonites, FOR members and Quakers — as well as non-church pacifists.

The group apparently has been growing rather quickly.

They have meetings all over Japan, print articles in newspapers, and hold press conferences.

Their emphasis is on the refusal of the 6.5% of their taxes which goes for the so-called “Self-Defense Forces.”

They have even written a “Song of 6.5% or 6.5% for a Peaceful World” protesting war taxes and expressing the need for money to stop death and the pollution of our environment.

Susumu is a wonderful and gentle member of the group.

Outside of his job as a university professor he is active as a member of the local Friends Meeting in Minato-ku (Tokyo).

He also trains students in nonviolence and works to raise consciousness about the Japanese government’s involvement with the repressive South Korean government.

He clearly sees the importance of not sending his money to the government for destructive purposes.

COMIT was still in operation at least as late as , but I haven’t been able to find much about them on-line.

France… has a long tradition of resistance to war and the military.

The tax refusal movement began in its present state in during the first French atomic tests in the South Pacific when a number of people decided to refuse the 20% of their taxes which would go to the war department.

This money was redistributed to organizations working for peace and developing social alternatives.

Groups soon were organizing in Orleans, Paris, Mulhouse, Lyon, and Tours and by were working in cooperation with one another.

They then made a decision to broaden the movement by asking people to refuse only 3% of their income tax.

They felt this way they would be able to attract more people because of the minimum of risk.

Many of these people decided to redistribute their money to the peasant-worker struggle in Larzac.

Larzac is a plain in Southern France where a group of peasants, farmers and shepherds have been resisting the expansion of an army training base onto land where they have lived and worked for centuries.

The Larzac struggle has become extremely important in France.

It receives broad support from leftists, environmentalists, workers and antimilitarists.

The peasants, who have come to believe strongly in nonviolent struggle, have used some very creative tactics to draw attention to their plight.

For example, they drove their tractors from Southern France onto the streets of Paris.

On the way, they were met in Orleans by 113 tax refusers who gave their tax money to the peasant struggle instead of to the military.

This link between the peasant struggle against the military and the people who refused taxes solidified the movement and both benefited.…

By , 400 French people had become tax refusers and at latest count as many as 4,000 are giving their money to Larzac instead of the government.

Many farmers, workers and pacifists are involved now in the refusal of taxes to support the Larzac struggle.

Most recently in France, pacifists are discussing and organizing for 100% refusal of their taxes as their non-cooperation with the military becomes more consistent with their lifestyles.

the issue also had a list of resources interested Quakers could use to find out more about war tax resistance

There were also several letters to the editor on the subject:

Mary Bye wrote in to explain the rationale behind her tax resistance.

“I believe that my tax dollars go to support a system which perpetuates misery and suffering in large parts of the world.

Here at home we have set up a monstrous military budget while the programs for the poor, the minorities, the disadvantaged and the defenseless are being cut.

I believe that the first step to moral health is to realize the callous role of oppressor we, as a nation, play abroad and at home.

The second step is to act.”

She said tax resistance works for her because “I know of no other way to introduce this concern into the courts, and… I want to commit my money to help meet human needs neglected by the government.

I give voluntarily an amount equal to that computed by IRS regulations to help build a community of caring.”

Ross Roby wrote in to promote the World Peace Tax Fund Act.

“Essentially, this bill would provide conscientious objectors to war (male and female, young and old) an alternative to having their Federal tax payments used to finance government agencies that wage war and those that contribute to the waging of war by our government and by other governments of this world.”

He complained that the proposal hadn’t gotten much Quaker support: “Are we unable to recognize a friendly hand when it does not come in Quaker garb?

Or, has vocal pacifism fallen so irrevocably into the hands of radical resistants that a congressional bill which proposes accommodating conscientious objection to the realities of the Internal Revenue Service (and vice versa) is automatically dismissed?”

He described the mechanism of the Act this way: “It sets up a Fund for Peace to which we, conscientious objectors to war, would automatically contribute as we paid our usual federal income tax.

If the federal budget were determined, by an impartial authority, to contain sixty per cent for military purposes, then sixty cents of each dollar we pay would enhance the treasury of a fund that builds peace…”

Jim Forest wrote about his decision to stop tax withholding from his paycheck by filing a new W-4 form.

“We will be using these moneys for human needs that aren’t being adequately met in the present world: hunger, housing, resistance to militarism, various efforts for impoverished people, etc. We receive fund appeals each day which, had we the means, we would respond to, or respond to more generously.

Now we will.”

Donald Hultgren gave a report of Robin Harper’s talk about war tax resistance and charitable redirection at the Quaker Meeting in Cornwall, New York.

Harold R. Regier, the Peace and Social Concerns secretary of the General Conference Mennonite church, wrote to thank the Journal for its “encouragement in our efforts to work at war tax payment/resistance issues.”

Harold R. Regier, the last letter writer I mentioned, said that: “One of our efforts along this line was to convene a war tax conference to look particularly at the theological and heritage bases for war tax resistance.”

The Journal article that followed concerned this conference.

A note at the top of that article said that “[o]ne hundred twenty persons registered” for a Mennonite/Brethren in Christ sponsored conference to seek theological and practical discernment on war tax issues.”

That conference issued a summary statement, which the Journal reprinted.

Excerpts:

After considering the New Testament texts which speak about the Christian’s payment of taxes, most of us are agreed that we do not have a clear word on the subject of paying taxes used for war.

The New Testament statements on paying taxes (Mark 12:17, Romans 13:6–7) contain either ambiguity in meaning or qualifications on the texts that call the discerning community to decide in light of the life and teachings of Jesus.

Although those in the Anabaptist tradition were generally consistent in their historical stand against individual participation in war, they were not of one mind regarding the payment of taxes for war.

Evidence suggests that most Anabaptists did pay all of their taxes willingly; however, there is the early case of the Hutterite Anabaptists, a sizable minority in the Anabaptist movement, who refused to pay war taxes.

In the later stages of Anabaptist history there is no clear-cut precedent on the question of war taxes.

During the American Revolution most Mennonites did object to paying war taxes, yet in a joint statement with the Brethren they agreed to pay taxes in general to the colonial powers “that we may not offend them.”

The record continued to be mixed until the present day.

Only a small minority chose to demonstrate their allegiance to Christ through a tax witness.

So far most discernment on the war tax issue has been done on an individual level as opposed to a church or congregational level.

Although individuals struggling with the issue have been supported by similarly concerned brothers and sisters, wider church support has been lacking.

While recognizing the need for a growing consensus in these matters, we know that not all in the Mennonite/Brethren in Christ fellowship are agreed on an understanding of scriptural teaching and a faithful response regarding war taxes.

We are ready to acknowledge this disagreement and seek to continue discerning God’s will in this.

But as a church community, we feel we should be conscious of the convictions and struggles of our sisters and brothers and supportive of the steps they have taken and are considering.

And all that’s just from one issue!

The issue included an article by Robin Harper about the Brandywine Alternative Fund, one of “a series of experiments [that] go by various names: fund for humanity, people’s life fund, life priorities fund, war tax resistance alternative fund.”

Excerpts:

As many as forty sprang into existence in as the country’s agony over Vietnam reached a crescendo.

Though each is organized and operated a bit differently, the basic concept is to pool federal war taxes (both telephone and income) conscientiously withheld from the IRS and redistribute them, by loans or grants, to community groups working for peace, social justice, and other areas of social change.

…the Brandywine Alternative Fund serves Delaware and Chester Counties just west of Philadelphia.

Although the greater part of the Brandywine fund comes from “reallocated” federal taxes, we also encourage deposits of personal savings.

This policy has not only enlarged the fund but has also broadened participation to include persons eager to help “reorder our nation’s priorities away from the military” who don’t choose to use the particular method of principled tax resistance.

In addition, seven monthly meetings, churches and civic groups have made deposits or contributions to the alternative fund, following the precedent of London Grove Friends Meeting.

This development of religious and other community groups investing in Brandywine is, I believe, a rather new departure for the alternative fund movement and offers an opportunity for sensitizing even larger numbers of people to issues of war preparations, civilian priorities and tax accountability.

Through the growth of our alternative fund, we have begun to take our central concern to the people of the communities in which we live; we are seeking creative ways to support financially some of those groups which are addressing a range of social and economic problems largely neglected by government; and we have undertaken the task of stripping the mask off one of our most powerful institutions — the IRS — as we portray its grim role in the betrayal of our society’s and world’s ultimate security.

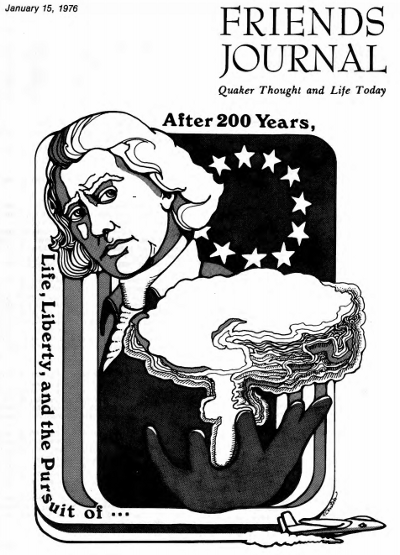

World Peace Tax Fund promoters tried to jump on the bicentennial bandwagon with a bizarre logo they promoted in the issue

The issue had some Revolutionary War-era history lessons.

Nonviolence theorist Gene Sharp wrote an article on “The Power of Nonviolent Action” in which he pointed out (among other things) the usefulness of tax resistance in the struggle for American independence:

During the Townshend resistance, in … for example, a London newspaper reported that because of the refusal of taxes and the refusal to import British goods, only 3,500 pounds sterling of revenue had been produced in the colonies.

The American non-importation and non-consumption campaign was estimated by the same newspaper at that point to have cost British business not a mere 3,500 pounds but 7,250,000 pounds in lost income.

Those figures may not have been accurate, but they are significant of the perceptions of the time.

The attempt to collect the tax against that kind of opposition was not worth the effort, and the futility of trying eventually became apparent.

Finally, Lyle Tatum examined the Philadelphia Yearly Meeting’s activity around .

Excerpts:

Although the Yearly Meeting was clear that members should not participate in military activities or pay direct war taxes, some areas were more difficult to decide.

Bills of credit, a form of negotiable instrument sanctioned by the colonies, were controversial.

The use of them stood in a similar position to the payment of taxes today.

To those Friends who were trying to get other Friends to stop using bills of credit, the Yearly Meeting minuted a bit of advice:

…we affectionately exhort those who have this religious Scruple, that they do not admit, nor indulge and Censure in their Minds against their Brethren who have not the same, carefully manifesting by the whole tenor of their Conduct, that nothing is done through Strife, or Contention, but by their Meekness, Humility and patient Suffering, that they are the Followers of the Prince of Peace.

Philadelphia Yearly Meeting of met in , just a little more than two months after .

As we have seen, pressure on the peaceable testimony had been growing over the previous few years.

In the face of this, the Yearly Meeting minuted:

…we cannot consistent with our Christian peaceable Testimony… be concerned in the promoting of War or Warlike Measures of any kind, we are united in Judgment that such who make religious Profession with us, & do either openly, or by Connivance, pay any Fine, Penalty, or Tax, in lieu of their personal Services for carrying on the War under the prevailing Commotions, or do consent to, and allow their Children, Apprentices, or Servants to act therein do thereby violate our Christian Testimony, and by so doing manifest that they are not in Religious Fellowship with us…

In spite of their many hardships, Friends were holding firm.

Loyalty oaths were going strong in .

It was minuted:

…in some places Fines or Taxes are and have been imposed on those who from Conscientious Scruples, refuse or decline making such declaration of Allegiance and Abjuration, it is the united Sense and Judgment of this Meeting, that no Friend should pay any such Fine or Tax…

War tax resistance in the Friends Journal in

There was plenty about war tax resistance in the Friends Journal in , but it seemed to involve tax resisting Mennonites as least as often as tax resisting Quakers.

The issue announced that the Center on Law and Pacifism was organizing a critical mass style tax resistance action:

The Center… has prepared and has available a “Conscience and Military Tax Resolution,” which may be signed by any conscientious objector to military taxes, witnessed (not necessarily notarized), returned to the Center.

When officially notified by the Center that there are 100,000 such resolutions on file, the signer may carry out his or her resolve to withhold the military portion of the federal income tax.

Alternatively, he or she may deposit the withheld taxes in an escrow account for the World Peace Tax Fund, pending passage by Congress of the WPTF Bill, deposit them in an alternative fund or donate them to some other peace purpose.

The issue was all about anti-war work, and it opened with an article on the history of Quaker war tax resistance by editor Ruth Kilpack.

Excerpts:

[W]e should not suppose that this is a new concern among Friends and members of other Peace Churches, who, by the very nature of our faith, have a conscience tender to such questionings.

For Friends, the searching extends back to the seventeenth century, when Robert Barclay, the English Quaker apologist, wrote in :

We have suffered much in qur country because we neither ourselves could bear arms, nor send others in our place, nor give our money for the buying of drums, standards, and other military attire.

This was the so-called “Trophy Money,” that could be distinguished as such.

But common or “mixed” taxes could not so readily be dealt with, since most Quakers believed it was their duty to pay taxes, and the part allocated to the military could not be separated out from the whole.

Today, like those earlier Quakers, we find ourselves in the same dilemma.

Law-abiding citizens, we continue to find ourselves troubled by the demand that we pay taxes for purposes we cannot in conscience condone.

We cannot pretend that we accept war as a legitimate function of the civil government which we support, and, just as some of our members have refused to serve in the armed services, many are beginning to question the contribution of our money for purposes we eschew for moral, humane, and religious reasons.

Quakers struggled with all these same questionings in the mid-eighteenth century and the period prior to the American Revolution.

One of the most articulate on the subject of war taxes was Samuel Allinson, a young Friend from Burlington, New Jersey, who in wrote “Reasons against war, and paying taxes for its support.”

The Samuel Allinson essay “Reasons against war, and paying taxes for its support” can be found in the book American Quaker War Tax Resistance.

Thus, in words written , he deals with the question of “a remnant who desire to be clear of a business so dark and destructive, that we should avoid the furtherance of it in any and every form.”

He describes it as a “stumbling block to others, [which] ought carefully to be avoided,” and sees such avoidance as advancing the Kingdom of the Messiah, that “his will be done on earth as it is done on heaven; a state possible, I presume, or he would not have taught us to pray for it.”

Further, says Samuel Allinson,

We have never entered into any contract expressed or implied for the paym[en]t of Taxes for War, nor the performance of any thing contrary to our Relig[ious] duties, and therefore cannot be looked upon as disaffected or Rebellious to any Gov[ernment] for these refusals, if this be our Testimony under all, which many believe it will hereafter be.

And finally, Samuel Allinson points out that even though earlier Friends paid their taxes (including that going to the military), that is no good reason for our continuing to do so.

It is not to be wondered at, or an argument drawn against a reformation in the refusal of Taxes for War at this Day, that our Brethren formerly paid them; knowledge is progressive, every reform[atio]n had its beginning, even the disciples were for some time ignorant of many religious Truths, tho’ they had the Company and precepts of our Savior…

Friends, we find ourselves in the very position of the Friends being addressed by Samuel Allinson two centuries ago.

For myself, I cannot think it is by sheer accident that I have stumbled upon his words now.

Neither is it by accident that a growing “remnant” of Friends are awakening to the ambivalence we feel in what we profess and what we practice regarding our involvement in the awesome “stumbling block” of nuclear warfare in our own age.

Friends in the past responded to the threats of the age in which they lived according to the light they had.

We of our generation have been given even greater light, and we must respond accordingly.

Given our heritage, if we don’t respond, who will?

In the meantime, I ask you to think on these things and, to paraphrase George Fox’s advice to William Penn, “Pay thy tax as long as thou canst.”

In the issue, Keith Tingle told readers that they should know “how easy it is to do” war tax resistance… at least in his experience:

My own experience in military tax resistance has been rewarding thus far.

By claiming a tax credit for conscientious objection to war on my income tax form, I was refunded $260 from my taxes.

Now that the IRS has discovered its mistake, I am resisting through federal tax court the recollection of this money.

My appearance in tax court has been reported favorably in three local newspapers, providing an opportunity to publicize the Quaker peace testimony, the history of war tax resistance, the economic impact of military spending, the pacifist position on the military draft, the concept of the World Peace Tax Fund, and the legal assistance offered by the Center on Law and Pacifism.

This has been accomplished with a total expense of about $30 and about thirty hours of time.

I have enjoyed the dedicated support of the Committee on War Tax Concerns of Friends Peace Committee and the legal guidance of lawyer Bill Durland at the Center on Law and Pacifism…

The issue noted that conscientious objection to military taxation was on the agenda at the Kent General Meeting in Canterbury, England — though from the sound of it, this was mostly in a theoretical way: presenting the argument that such a thing was a logical and practical counterpart of conscientious objection to military service.

That issue also reported on the case of Cornelia Lehn, an employee of the General Conference Mennonite Church who was trying to convince her employer to stop withholding federal income tax from her salary:

There was a “neither yes nor no” vote on this request by the 500 delegates present.

Those who favored a strong tax resistance program did not Nor did those who wanted members to unquestioningly pay taxes as a Christian duty.

There was a feeling, however, that neither side really lost.

Thirty percent of the delegates were ready for the conference to take action in “some sort of civil disobedience and tax resistance” and it was hoped the number will grow.

I’m struck by this last phrase — “it was hoped the number will grow” — which makes a pretty clear editorial statement of sympathy for those who favored corporate resistance by the Conference and antipathy for “those who wanted members to unquestioningly pay taxes as a Christian duty.”

At this time, few if any Quaker Meetings or organizations were willing to go out on that limb, in spite of strong urgings from Quaker war tax resisters that they do so.

But I don’t remember the Journal betraying an editorial bias when it reported on this debate in Quaker institutions.

One case in point is a report on the New England Yearly Meeting in which the lukewarm statement is made that “We approved a minute asking New England Friends to give prayerful consideration to non-payment of war taxes.”

The New York Yearly Meeting went so far as to “discuss” a “minute on Refusal of Taxes for Military Purposes” and to note that it “was to be commended for consideration by all monthly meetings and individuals.”

The issue had a followup in which the General Conference of the Mennonite Church was proposing launching a lawsuit in which it would seek a judicial ruling to legalize conscientious objection to military taxation, while at the same time it would increase its efforts to pass the “World Peace Tax Fund” legislation.

Maurice McCracken had a piece of autobiography in the issue.

Naturally, it touched on his tax resistance:

I had decided that I would never register again for the draft nor would I consent to being conscripted by the government in any other capacity.

In contradiction to this position, each year on April 15 I was letting the government conscript my money.

Thus I was voluntarily helping the government do what I vigorously declared was wrong.…

Realizing this inconsistency, I decided that in good conscience I could no longer make full payment of my federal taxes.

At the same time, I did not want to stop supporting civilian services supported by the government.

So, in my tax returns I continued to pay the small percentage allocated for civilian use.

The amount that I formerly had given for war purposes I hoped now to give to such causes as the American Friends Service Committee and to support other works of mercy and reconciliation which help remove the roots of violence and war.

As time went on I realized, however, that this was not accomplishing what had been my hope; for year after year the IRS ordered my bank to release money from my account to pay the money I had held back.

I then closed my bank account, and at this point it came to me with complete clarity that by so much as filing tax returns I was giving the IRS assistance in the violation of my own conscience, because the very information I was giving on my tax forms was being used in finally making the collection.

There is something else that those who withhold a portion of their tax on conscientious grounds should realize.

The IRS does not practice line budgeting.

All that it collects goes where the government wants it to go, which in ever-increasing proportion goes to finance wars, past, present and future.

I have not filed any tax returns, nor have I paid any federal income tax.

On , on charges growing out of my refusal to pay this tax, I was given a six-month sentence, which I spent at Allenwood, Pennsylvania, which is run by the Lewisburg penitentiary.

Some two years my release from Allenwood, in , the Presbytery of Cincinnati, on charges quite unrelated to the real issues, suspended me as a minister.

In , this action was upheld by the General Assembly, the highest court of the denomination.

In the presbytery declared my ordination to the ministry no longer valid, making a highly questionable presumption that they could cancel out whatever spiritual grace the Holy Spirit had bestowed on me when I was ordained at a meeting of Chicago Presbytery back in .

For nearly eighteen years our congregation has been a member of the National Council of Community Churches.

I have been accepted as a minister in full standing, and whatever validity my ordination had back in , is, for them, still valid.

A note in the issue recognized 86-year-old Pearl Ewald’s persistent activism: “Pearl Ewald continued her activities for peace, civil rights and war tax resistance, despite a recurring heart condition.

She has been arrested and jailed more than once for stubbornly refusing to discontinue her witness.

On one occasion, although desperately in need of medical attention, she refused to be admitted to a hospital, because it was a segregated institution.”

That same issue mentioned the case of Mennonite war tax resister Bruce Chrisman, “who was convicted of failure to file an income tax return in , was sentenced to one year in Mennonite Voluntary Service,” to which I can only think: “Please don’t throw me in the briar patch, Your Honor!”

“I’m amazed,” said Chrisman.

“I feel very good about the sentence.

The alternative service is probably the first sentence of its kind for a tax case.

I think it reflects the testimony in the trial and its influence on the judge.”

Chrisman could have been sentenced to one year in prison and a $10,000 fine.

A letter from Mildred Thierman in the same issue challenged Friends:

Could we now unite this year in sending a flood of personal declarations to President Carter and our government, saying that we can no longer, in conscience, allow part of our taxes to be used for the purchase of annihilating weapons?

Can we back this up by joining together in significant numbers to withhold whatever portion of our income tax fits our circumstances, in order to make our protest noticed?

A review of Conscience in Crisis: Mennonites and Other Peace Churches in America, , Interpretation and Documents in the issue, summarized its version of the history of Quaker war tax resistance this way:

Testimony against participation in the military and refusal to pay Trophy Money — the English tax to raise money for military regalia (arms were, by law, furnished by the individual soldiers) — were traditional Friends’ observances by the beginning of the period covered by Conscience in Crisis.…

…Friends and other Peace Church members were, by and large, loyal subjects.

They paid taxes “for the King’s use” — including the royal decision to make war.

Friends began to question payment of taxes more broadly.

The essential issue, according to the authors, was that “the individual is responsible for the actions of his government in a free society.”

Israel Pemberton, John Pemberton, John Churchman, John Woolman, and nineteen other Friends petitioned the Assembly on the issue of taxes in :

…Yet as the raising Sums of Money, and putting them into the Hands of Committees, who may apply them to Purposes inconsistent with the peaceable Testimony we profess, and have borne to the World, appears to us in its Consequences to be destructive of our religious Liberties, we apprehend many among us will be under the Necessity of suffering rather than consenting thereto by the Payment of a Tax for such Purposes…

By the time of the Philadelphia Yearly Meeting sessions, Friends decided not to discuss the issue of “mixed” taxes because of a significant lack of consensus.

Yet, Friends were increasingly beginning to question less direct forms of support for war not traditionally inconsistent with the peace testimony.

an illustration from the issue of Friends Journal

In the issue, Alan Eccleston wrote of his calling as a peacemaker, and how that manifested for him.

Excerpts:

For me personally, the witness to peace has led to war tax resistance.

Over the past six years of this witness I have been — and still am — strengthened by others who are not, themselves, war tax resisters.

The witness of war tax resistance is one that raises fear.

We have been conditioned to fear the Internal Revenue Service as something nearly equivalent to a ruthless secret police, in its imagined power to terrorize.

Most of us, unwilling to admit, even to ourselves, that fear alone would block us from a spiritual witness, find other reasons for willingly paying to produce weapons that can annihilate all humankind.

Based on my own experience, I would say fear imagined is greater in most people than fear actually experienced, and that this is by a factor of ten, at least — maybe 100. Fortunately, borrowing from each other’s experience and knowing others will be there to help us, we can find the courage to move ahead.

Then comes the surprise.

With dread and foreboding we make our stand.

Then, gradually, we become aware that a great weight has been lifted from us.

That nagging, cumbersome burden of blocking from consciousness our own complicity with this evil has fallen away.

We are lighter, more open, more truthful.

We are free, at last, to speak truth to power.

When this affirmation is truly clear in our lives, it will be seen and felt by the president and by Congress.

As in , when C.O. status was incorporated in the Selective Service Act, the tax laws will then be amended to create C.O. status for taxpayers and a “World Peace Tax Fund.”

That legislation, approved by the world’s leading arms supplier, will move the world one step closer to peace.

That portion of our population (approximately four percent during the Vietnam War) which is pacifist would then contribute to peace, not war, and these contributions would total in excess of $2.3 billion every single year — year after year.

For the first time in history, peace programs would have a significant budget.

The funds could be used to support: a National Academy of Peace and Conflict Resolution; research to develop and evaluate non-military, nonviolent solutions to international conflict; disarmament; retaining workers displaced by conversion from military production; international exchanges for peaceful purposes; improvement of international health, education and welfare; and education of the public about the above activities.

The Friends General Conference in drafted “A Statement of Conscience by Quakers Concerned” and collected signatures.

The statement said, in part:

We advocate conscientious refusal to register for the draft and wish young men of draft age throughout the United States to know that if, after thoughtfully considering the reasons and consequences, they refuse to register, we will give them practical and moral support in every way we can, even though our willingness to do so may result in our prosecution, fines and possible imprisonment for disobeying a man-made law that leads us in the direction of war.

Mary Bye wrote in response that although she signed the statement, it felt to her to be something “like a hollow gesture.”

[M]aybe we [adults] should make sure about the beam in our adult eyes before we concentrate on the motes in those bright young eyes of the nineteen- and twenty-year-olds.

“[W]hat would be our reaction to young Quakers pointing out that since it takes money as well as men to fight a war, they encourage Friends beyond draft age to refuse war taxes?

Finally, the issue presented the case of Ruth Larson Hatcher.

Excerpt:

Not wishing to contribute tax money for war-making purposes, she managed for years to have an income just sufficient for survival but not large enough to require payment of taxes.

Then in a friend persuaded her to accept the management and bookkeeping of a children’s art center.

Conscientious and religious beliefs caused her to oppose acceptance of insurance benefits under Social Security, as well as the payment of taxes for war.

Her claims for exemption under various sections of the Internal Revenue code of as well as under the First and Fifth Amendments were routinely rejected, until a Supreme Court judge approved her use of Form No. 4361. It seems that this form (and another previously ignored by the authorities) had been used by an Amish sect to avoid the taxes (and payments) of the social security system.

Although the Court of Appeals handed down the opinion that exemptions were enacted to accommodate individuals commanded by their conscience or their religion to oppose acceptance of insurance benefits, it refused to accept that this was the exact status of petitioner Ruth Hatcher.

It’s a little unclear what took place here, but it sounds like this is saying that the courts left an opening for people who were not members of sects that qualified for an exemption from the social security system but who held similar beliefs to gain the same exemption.

Interesting if true.

I was able to find the appeals court decision that ruled against Hatcher, and the earlier Tax Court decision to the same effect, and the District Court decision that affirmed the Tax Court decision.

I was not able to find any record of Supreme Court action on the case, but I did find some other cases that cited the Appeals Court decision as precedent, which seems to suggest that the Supreme Court didn’t overturn it (as the above excerpt implies).

War tax resistance in the Friends Journal in

The third of Friends Journal’s special issues on war tax resistance came in , and the topic came up in several other issues besides.

An article by Mary Bye in the issue showed how the arguments for war tax resistance were starting to break the bounds of the tax arena and take hold elsewhere.

Excerpts:

In a letter from the collection department of Philadelphia Electric Company demanded payment for a backlog of refused rate hikes.

I had withheld the 13.7 percent imposed to cover the construction costs of the Salem and Limerick nuclear reactors.

Why did I take this stand?

Looking back over the years for the source of my action, I could see it springing from a long-time insistence upon justice, a small but growing willingness to risk, a perennial sense of grief for suffering, and a blossoming love of the Earth.

These are the qualities of the spirit which began to unfold into action during the early days of the Vietnam War.

Somewhere along the line, I refused to pay the war tax portion of my federal income tax.

Later the Vietnam War ground to a halt when legislation ended financial support for it.

Was it just a coincidence that our war tax resistance preceded this legislation?

Or did citizens modeling the denial of monies not only support the growing disaffection with the war, but also provide a clue to a way to end it?

We had perhaps unwittingly slipped into an old Christian strategy of living as if the Kingdom were here now, and, behold, it manifested a brave, new world, or at least the beginning of one.

War tax resistance seemed an appropriate base upon which to build a new witness of caring for the whole Earth.…

…With crystalline clarity I selected my own utility, Philadelphia Electric, and refused the rate hike for Salem and Limerick.

After 1½ years of refusal, accompanied by monthly explanations, I received a warning letter from the collection department, threatening an end of service.

The initial fright yielded to a decision to continue resisting and move as swiftly as possible to establish my independence from nuclear power forever.

I faced a new, expensive, complicated simplicity: photovoltaic cells, which produce electrical current when exposed to light, and which could free me from bondage not only to nuclear generators but also fossil fuel-fired reactors.

As war tax resistance led me to a lower income, so rate hike refusal was pointing the way to lower energy demands.

My living standard may drop, but the quality of my life soars.

Meanwhile I have discovered that Philadelphia Electric is experimenting with photovoltaics in anticipation of the coming solar age.

If the price is right, I could purchase them there.

After all, nuclear power is the enemy, not the electric company.

This is the vision, but it is a dream deferred or rather only partially realized.

Philadelphia Electric Company and Solarex, which manufactures photovoltaic cells, want to establish a demonstration project at my home that would provide between one-fourth and one-third of the daily demand here for electricity.

The stumbling block is the cost, which would possibly necessitate a 35-year pay-back period.

So I am circling the photovoltaic issue in a holding pattern like a plane above an airport.

I am searching for answers to hard questions: such as what is the equitable balance between the cost of photovoltaics and the wattage generated?

What is a reasonable payback time?

If the cost is rock bottom right now, how do we gather funds?

How do we secure state and government support?

Are churches and meetinghouses able to model this kind of caring for God’s creation?

How do we dream this dream into reality?

I would welcome your suggestions.

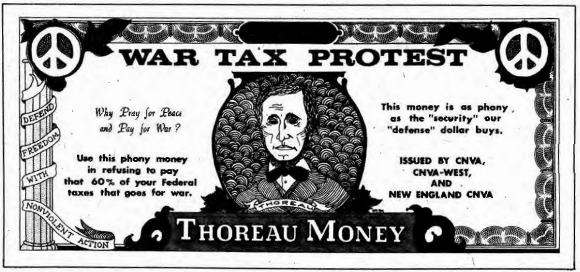

an ad in the issue of Friends Journal

That issue also announced a “Conference for Quaker, Mennonite, and Brethren employers, airing ways to deal with war tax resistance by employees.

Sponsored by Friends Committee on War Tax Concerns and New Call to Peacemaking.”

That conference was covered in the issue in an article by Paul Schrag.

Excerpts:

The question of how church organizations can help their employees follow their consciences — and how to deal with the risks involved for both employees and employers — were the issues that 36 Mennonites, Brethren, and Quakers struggled with at the meeting.

The church leaders, organizational representatives and lawyers affirmed their support for individual military tax resisters and for efforts to seek a legislative solution by working toward passage of the U.S. Peace Tax Fund bill in Congress.

They agreed to organize a peace church leadership group to go to Washington, D.C., to support the peace tax bill and to express concerns about tax withholding.

They also agreed to help each other by filing friend-of-the-court briefs if tax resisters are prosecuted and by sharing the cost of tax resistance penalties, if necessary.

People from churches that refuse to withhold federal taxes for employees who oppose paying military taxes shared their experiences with people from churches considering adopting such a policy.

The General Conference Mennonite Church and two Quaker groups are in the first category.

The Mennonite Church is in the second.

The meeting, held at Quaker Hill Conference Center, took place in an atmosphere of excitement generated by a gathering of people from different traditions who share a vision.

One conference participant said it was frustrating that many members of historic peace churches are unwilling to witness against financial participation in preparing for war, although they are opposed to physical participation in war.

Some said it was disappointing that so many people are unwilling to follow their consciences until the government, through the Peace Tax Fund, might allow them to do so legally.

One quoted Gandhi: “We have stooped so low that we fancy it our duty to do whatever the law requires.”

When a church or organization decides to honor employees’ requests not to withhold their federal income tax, it assumes serious risks.

Theoretically, a person in a responsible position who willfully fails to withhold an employee’s taxes can be punished with a prison sentence and a $250,000 fine.

An organization can be fined $500,000.

But such penalties have never been imposed on legitimate religious organizations, nor are they likely to be, said two lawyers at the meeting.

The usual Internal Revenue Service response to war tax resistance is to take the amount of tax owed, plus a 5 percent penalty and interest, from the employee’s bank account.

However, the IRS has not taken even this action against General Conference Mennonite Church employees who are not having their taxes withheld.

They pay the nonmilitary portion of their taxes themselves and deposit the 53 percent that would have gone to the military in a designated account.

The IRS has not touched that account after church delegates approved the policy in .

All church personnel who could be subject to penalties have agreed to accept the risk.

Friends World Committee for Consultation, which has had a nonwithholding policy , has had tax money seized, plus interest and penalties, from its resisters’ bank accounts.

Friends United Meeting adopted a non withholding policy .

Philadelphia Yearly Meeting of the Society of Friends is considering such a policy.

A representative of the Church of the Brethren said he would use input from the meeting to work toward developing a denominational policy on tax resistance.

Lobbying continues for the Peace Tax Fund bill…

The bill would allow people opposed to war taxes to put the portion normally given to the military in a separate fund for peaceful purposes.

The rest of that person’s tax money also would be designated for nonmilitary use…

Whether or not military tax resistance is effective, participants agreed that people’s moral imperative to follow their consciences must be respected.

“No conscientious objector ever stopped a conflict,” said William Strong, a Quaker representative [and treasurer of the Friends Journal Board of Directors].

“But they had to explain what they did, and the vision was kept alive, and those ripples, you don’t know where they stop.”

A postscript noted: “ ‘A Manual on Military Tax Withholding for Religious Employers,’ written by Robert Hull, Linda Coffin, Peter Goldberger, and J.E. McNeil, will be available .”

from the cover to the issue of Friends Journal

The issue was the third special issue on war taxes from the Friends Journal.

It was prompted in part by the fact that the Journal itself had received IRS levies on the salary of its editor, Vinton Deming, who had been refusing to pay income tax .

The Treasurer of the Journal, William D. Strong, explained what was going on in the lead editorial:

The Friends Journal Board of Managers has twice been unable to honor the levy against the wages of our editor, Vint Deming, for unpaid federal taxes.

In our most recent reply to the Internal Revenue Service we stated that:

It is not possible for us as a board to separate our faith and our practice: we must live out our faith.

Our earlier letter… refers to our 300-year-old Peace Testimony.

To more fully describe that part of our beliefs we enclose copies of two sections of Faith and Practice, the book of spiritual discipline of Philadelphia Yearly Meeting.

[“The Peace Testimony” and “The Individual and the State,” pp. 34–38, were shared.]

Our position of noncompliance to the requests of the Internal Revenue Service is not an easy one.

We do not question the laws of the land lightly, but do so under the weight of a genuine religious and moral concern.

We know as well that other religious groups — Mennonites, Brethren, and others — are facing this same difficult dilemma.

For this reason, many of us support the proposed Peace Tax Fund bill in Congress.

The board agreed at our meeting in to make known this continuing witness, both individual and corporate, to you, our readers.

The dilemma is clearly not the Journal’s alone.

Many Quaker institutions in the United States, Canada, and England have faced this challenge.

Beyond the historic peace churches are Catholics, Methodists, and others who are considering the whole question of taxes and militarism.

In February representatives of some 70 institutions came together at the Quaker Hill Conference Center in Richmond, Indiana, for a New Call to Peacemaking consultation on “Employers and War Taxes.”

This followed a Quaker conference at Pendle Hill considering the same concern.

The Journal board has worked at and reached unity in this matter.

We will continue to seek the light in the months and years ahead.

For now, however, we would welcome the support and reactions of our subscribers and readers.

If you’d like to share in this witness with your moral support, let us know.

If you’d like to add practical support, we would welcome it, as we are establishing a Conscience Fund.

We don’t plan extensive legal undertakings at this time, but we know that there can readily be some fees and costs ahead, as well as possible penalties resulting from our refusal to honor the levies from the IRS.

We look forward to the response of our readers. We feel that we cannot host writings in the issues of the Journal on peace and justice, on our testimonies and faith and practice, without, as an employer, living them out to the best of our God-given abilities.

Another article in the special issue was an extract from J. William Frost’s Tax Court testimony in the Deming case, in which he explained the Quaker war tax resistance practice:

The peace testimony has been a basic part of Quaker religious belief .

The testimony has not been static; it has evolved over time as Friends thought out the implications of what it meant to be a bringer of peace.

Some of the most creative actions of members of the Society of Friends have come from the peace testimony.

For example, Friends’ primary contribution to world history is that they began and carried through the antislavery testimony.

Friends became antislavery advocates in , when they realized that the only way one could obtain a black slave was to take him or her captive in war.

Pennsylvania was founded by William Penn for religious liberty.

Penn believed, and so did the early settlers, that to create a Quaker colony meant there would be no militia, no war taxes and no oaths.

These were conceived to be part of religious freedom, and in the early years of Pennsylvania, there was no militia, and there were no war taxes and no oaths.

At first, the Pennsylvania Assembly refused to levy any taxes for the direct carrying on of war.

Instead, after when the British government requested money because it was already beginning its long series of wars with France, the Crown and the Pennsylvania Assembly worked out a series of arrangements.

Those arrangements provided that the Assembly (then composed primarily of Quakers) would provide money for the king’s use or the queen’s use, but the laws also stipulated that that money would not be directly used for military purposes; i.e., there would be almost a noncombat status for Quaker money.

It could be used to provide foodstuffs to be used to feed the Indians, or it could purchase grain or relieve sufferings.

It would not be used to provide guns and gunpowder.

This policy of no direct war taxes, no militia, and no oaths, was followed in Pennsylvania .

In , a group of members of Philadelphia Yearly Meeting began the debate on whether Quakers should pay taxes in time of war.

At this time, some of the most devout Quakers refused to pay a war tax levied by the Pennsylvania Assembly.

And finally the yearly meeting agreed that those whose consciences would not allow them to pay the taxes, should not.

So the heritage of Pennsylvania was that government accommodated the religion.

The Federal Constitution allows for an affirmation, because certain religious rights are antecedent to the establishment of the government, and the government can and will accommodate itself to religious scruples of those people who are conscientious good citizens.

there was less opportunity for tax resistance because there was no direct federal taxation.

The federal government was financed by tariffs, and the tariffs were used to carry out the full operations of government.

(The major exception came during the Civil War, and here the main issues were military service and Quakers’ refusal to pay a substitution tax.)

The main Quaker response to World War Ⅰ was the creation of the American Friends Service Committee.

This organization was designed to allow those young men who did not wish to fight (conscientious objectors) to have an opportunity for constructive service (i.e., to provide relief and reconstruction in the war zone).

Friends conducted relief activities in France, and then later in Germany, Serbia, Poland, and in Russia.

The War Department accommodated itself to Friends.

There was no specific provision in the draft law in World War Ⅰ for conscientious objectors.

The War Department allowed those Friends who wished to serve in the American Friends Service Committee to be furloughed so that they could go abroad to participate in relief activities.

A second way in which the authorities accommodated Friends at that time was in relief money raised by the Red Cross for Bonds.

Much of the Red Cross effort was for military hospitals, and Friends did not wish to support that effort.

Therefore in Philadelphia an agreement was worked out whereby Friends contributed money or bonds which would be earmarked for the American Friends Service Committee or for relief activity rather than for direct war activity.

There were instances in World War Ⅱ of individual Friends refusing to pay war taxes, and the Philadelphia Yearly Meeting officially protested against certain war taxes, but the main movement against war taxes has occurred .

During the Cold War and particularly during Vietnam, war tax resistance has become a major theme in Philadelphia Yearly Meeting.

The Philadelphia Yearly Meeting, , has regularly put a discussion of war taxes on its agenda.

In many ways the Philadelphia Yearly Meeting position on war taxes is like its position was on antislavery before the Civil War: before , virtually all Friends opposed slavery.

, virtually all Friends oppose military taxation.

The difficulty in and in is that Friends are searching for a way to make their religious witness effective.

What Friends want to do is somehow change the focus of a policy which they see as destructive of what is basic to their value system.

In summary, the position of Friends is that religious freedoms preceded and are incorporated into the federal government.

Pennsylvania was founded for religious freedom, and religious freedom meant no taxes for war, no militia service, and the right of affirmation.

Friends think that the federal government incorporated part of that understanding in the affirmation clause in the constitution, in the first amendment, and in the religion clauses in the Pennsylvania Constitution.

Friends think that the government has in good faith tried to accommodate us in our position on military service, and what Friends are wanting from the government now is a like accommodation on a subject which is the same to us as conscientious objection: the paying of taxes which will be used to create weapons to threaten and to kill.

Deming represented himself next, in an article describing his “journey toward war tax resistance.”

Excerpts:

During a difficult moment [in the discussion over the Philadelpha Yearly Meeting’s response to the Vietnam War] a young Friend stood and spoke with deep emotion; and his words went straight to my heart.

It didn’t matter, he said, what older Friends might say in support of him and his generation (though support was needed and appreciated, for sure); what really mattered to him was that Friends look personally at their own lives to see how they were connected to warmaking.

If they were too old to be drafted (and most of us were) perhaps they could find other ways to resist the war.

About 20 years have gone by and I don’t even remember the name of the young Friend who spoke in meeting that day, but his words had a profound impact on me.

As a result of his ministry I decided to begin to seek ways to resist the payment of taxes for warmaking (what another Friend, Colin Bell, would term the “drafting of our tax dollars” for the military).

I should say that there was another motivating force at work on me as well.

My work for Friends in the city of Chester was bringing me into daily contact with poor and black people.

I was learning firsthand about a community — a microcosm of other urban areas across the country — that suffered the debilitating effects of chronic poverty, high unemployment, deteriorating housing, inadequate health care, and inferior public schools.

I was witnessing the insufficient funding of a so-called War on Poverty in Chester while millions of dollars and human lives were being expended in a war against other poor people in Southeast Asia.