Peters was back from Hebron, where he’d been working with Christian Peacemaker Teams, and he shared photos and observations about his time there.

Peters says his tax resistance has become more confrontational in recent years, moving from a mostly-symbolic refusal to pay the phone tax to “what Gene Sharp would call ‘withdrawal of consent.’ ”

Today Peters has adopted complete non-cooperation with the IRS — he refuses to file, and instead sends letters explaining his reasons.

“We’re entering an era of ‘spiritual warfare,’ ” Peters says, “the political process is bankrupt.”

I arrived a little late and so I missed the first part of Wright’s talk, but here are some items from the notes I took:

Wright was impressed with the Conscience UK group, which he thought was the most “slick” of the groups represented at the conference, and the one that had the broadest focus in terms of war tax resistance in general.

Most other groups had a more narrow focus on Peace Tax Funds or other forms of official accommodation for conscientious objectors, although most of the peace tax campaigners were also war tax resisters.

Peace Tax Fund advocates acknowledge that there are objections to their program within the war tax resistance movement, however Wright found that at this conference there was near-unanimity about the value of a Peace Tax Fund-like program.

It is seen as a winnable battle, and potentially a valuable tool that war tax resisters can use.

The most high-profile peace tax campaign going on these days is that of the Peace Tax Seven in the UK.

Some Italian war tax resisters have had success in pursuing the conscientious objector argument in the courts, and apparently are paying a portion of their taxes to non-governmental organizations with the blessing of some judges.

These cases haven’t yet been brought to higher courts, however.

Some people who are lobbying the government or international bodies (including multiple UN human rights bodies and overlapping multi-nation European meta-governments) to try to enact some official accommodation for conscientious objectors to military taxation feel that they are unable to become war tax resisters because such “lawless” actions would hurt their credibility with those they are lobbying.

The Quaker Council for European Affairs is trying to push for an acknowledgment of conscientious objection to military taxation as a human right in the Council of Europe (which is a larger body than the European Union and is apparently more amenable to such an argument).

The Peace Tax Fund bill being considered by the U.S. Congress has a similarly tight definition of “conscientious objector” as that used to categorize people for military service by draft boards — that is, to qualify as a “conscientious objector” a taxpayer must be “opposed to participation in war in any form based upon the taxpayer’s deeply held moral, ethical, or religious beliefs or training.”

Non-pacifists who nonetheless conscientiously object to the way their money is being spent on wasteful, reckless belligerence would not qualify.

Best slogan from the discussion: “War Tax Resistance — it’s a direct action you do every day.”

Over the holidays, I read Lest Innocent Blood Be Shed.

The book tells the story of the French village of Le Chambon, which sheltered Jewish refugees during the Nazi/Vichy occupation.

It’s a good and inspiring story, but I’m only mentioning it today to go off on a self-indulgent tangent.

There’s an aside in the book that jumped out at me.

It reads:

The word scruples comes from the Latin word for “pebble.”

Scruples, like sharp stones in a shoe, can hinder a retreat from danger.

An on-line etymological dictionary agrees, adding that the word scrupus was “used figuratively by Cicero for a cause of uneasiness or anxiety, probably from the notion of having a pebble in one’s shoe.”

I mention this because I remembered that when I was first starting off on this experiment in tax resistance, before I was familiar with the tax resistance movement or the literature and history of tax resistance, I tried to come up with some evocative way of explaining how my conscience was bothering me about taxpaying.

The phrase I chose was:

I am absolutely unable to give any moral support to the U.S. government, and that I have been a source of financial support to that government has been a stone in my shoe.

I suppose I may have picked up the etymology subconsciously, or I may have read about it and forgotten it, but the way I remember it I was just reaching for a metaphor for how I was feeling, then I stumbled on one that felt right, and ran with it.

Eerie.

That’s part of why I’ve become a little obsessed with the history of tax resistance.

Lots of people have been down this road before, and it pays to listen to the stories they’ve told, for one day I may be walking in their footsteps.

FSK’s Guide to Reality thinks I’ve become “overly obsessed with Quaker justifications for war tax resistance” lately.

Guilty as charged.

In my defense, I’m assembling a book on the subject as a companion-volume to We Won’t Pay.

I apologize to folks for whom this has all been like a dull late-summer day in History class.

I’ll try to mix it up with other stuff from time-to-time.

And I’m getting to the end of my material — we’re already up to the middle of the Civil War, and I don’t get much further than that war in my research.

FSK’s got another point, though: “If you use Quakers as your model for tax resistance, you’re thinking in the wrong terms. All taxation is theft, and not just taxes that is used for war.

A policeman who confiscates my property is committing an act of war as much as a soldier.”

I agree with this understanding of the nature of taxation and the state, but I would disagree that this means the Quaker variety of war tax resistance isn’t worth study.

Indeed, one of the things I’m finding is that critics of Quaker war tax resistance often used this very argument — that all government rests ultimately on violence, and so there is no way to distinguish war taxes from other taxes.

And Quaker war tax resisters had to come up with rhetorical strategies to meet this argument.

Some responded by further distancing themselves from government — not voting, refusing to file lawsuits, that sort of thing.

Most, though, took the sophist approach and tried to draw a line between “civil government,” which good Quakers could (indeed, must) support, and “military government,” which they had to avoid supporting.

Here’s “Philalethes” complaining, in , that Quakers in Philadelphia were inevitably compromising their religious principles by taking positions in the legislature — that to take part in the government (the “court”), you implicitly approve of the military that props the government up (the “camp”):

I have often told our church doctors they have no more to do in Cæsar’s court than in his camp; the last they decline in conceit.

But doesn’t the court maintain the camp?

Doesn’t the camp defend the court?

Then where’s the difference?

Later, James Logan, who disapproved of Quaker pacifism and Quaker war tax resistance, used the same argument to try to encourage war-squeamish Quakers to quit the Assembly so that it could make war requisitions.

(Quaker Assembly members did eventually resign their seats so that the legislature could prepare for war without their assistance, which marked the end of the political control of Pennsylvania by the Society of Friends.)

On another occasion, Moses Brown complained to Anthony Benezet that “I understand some Friends have fallen in with or been overpowered by the common argument that civil government is upheld by the sword, and therefore they decline paying to its support…”

Samuel Cox, who opposed the Quakers, tried to show that the arguments for Quaker war tax resistance were really arguments for anarchism — “Friends say, we cannot pay militia fines; nor do any thing to uphold the military power.

Ah! truly: — and why do you ever become adjuncts and allies and officers of such a civic dynasty? or vote for the ministers of such a power?

What are you doing at the polls, but upholding that very power?

What moral right have you there? to vote or be voted for?

And yet all of you (generally) exercise the right of suffrage.

And you virtually appeal to the sword, whenever you sue a man, and invoke the armed interference of the law to coerce him to his duty!”

Later, a non-Quaker peace movement journal took up the same argument: “we may well doubt whether we can consistently recognize civil government, as Quakers themselves do, by voting, and paying general taxes.

The right to use at will the force necessary for the execution of its laws, lies at the bottom of all government as indispensable to its existence and effective power; and this right we as truly recognize by voting, or by paying ordinary taxes, as we should by the payment of military fines.

Do not nine-tenths of our taxes confessedly go to pay war-expenses?

Is not our national debt all for this end?

Everybody knows it is; but shall peace men refuse on this ground to pay their taxes?”

These same sorts of arguments come up today.

“Peace tax fund” advocates and statist war tax resisters try to draw a line between good taxes and bad taxes, and good government violence and bad government violence.

The Christians among them are still burdened by Romans 13 and 1 Peter 2.

And those of us who think we’ve got a better idea can become more persuasive if we learn from the experiences of those who have made these arguments before us.

FSK’s Guide to Reality again takes me to task for my “bizarre fetish about Quakers and war tax resistance.”

He finds war tax resistance to be incoherent, seeing as the state is an inherently violent and aggressive institution, and so anyone who objects to war enough to resist war taxes ought logically to resist all taxes.

While I tend to agree with him in his conclusions, I think there are some

coherent (though precariously-balanced) positions that allow for objecting to

war without objecting to all coercive government. For the Quakers, though,

there wasn’t much room for staking out nuanced positions in this regard

because they were boxed in by scriptural demands to respect the authority of

the state — up to certain boundaries. Given that, the only question was where

the boundaries should be.

But to address FSK’s criticisms, I would

just say this: to the extent that the Quaker position on war taxes was

incoherent, I think much of the modern war tax resistance movement and

especially its “peace tax fund” contingent is equally or more incoherent. And

a large part of the reason for this is that its proponents do not carefully

consider their positions and the positions of those who disagree with them.

I’m eager not to make the same mistake, and so I’m taking some care to study a

variety of arguments about taxpaying, including those that I think are not

particularly wise or good.

And I think the Quaker arguments have serious flaws. But, that said, there

remains a lot we can learn from them. And I’m most impressed by the fact that

those Quakers who did develop arguments for one form of tax resistance or

another actually put those arguments into practice, which cannot be

said for a lot of the more ideologically pure intellectually libertarian tax

complainers we have about us today.

Some war tax resisters resist in this way:

They calculate how much federal income tax they owe, then they determine what percentage of income tax revenue the federal government spends on war, and then they hold back that percentage of their income tax while paying the rest.

This is a variety of protest that relies on symbolism and on the emphatic value of civil disobedience.

But sometimes these resisters claim that what they are doing is not merely a protest but is a variety of conscientious objection — an attempt to practically withdraw support from immoral government policies, or to evade complicity with those policies.

Looked at in that way, the tactic they’ve chosen seems disconnected from the ends they claim to be pursuing.

If they withhold 50% of their income tax, for instance, because they believe that that is the percentage of income tax revenue the federal government spends on the military, the remaining 50% that they do pay isn’t any less likely to be spent on the military or to expose the payer to any less complicity.

The separation of the bad money they’ve held back from the good money they’ve sent in is only in their mind.

It’d be like using half a can of orange paint to paint one chair, and half of it to paint another chair, and expecting to end up with a red chair and a yellow chair.

The people who practice this variety of war tax resistance aren’t idiots — they know that the government isn’t doling out each individual taxpayer’s tax dollars one-by-one with the Defense Department last in the queue (“sorry, General, but it looks like we’ve run out!”).

And they’ll acknowledge this if you ask directly.

But from time to time, many seem to forget that they’re engaged in a symbolic protest, and they deploy the rhetoric of conscientious objection to explain their position.

This was a particularly difficult problem with the Quaker war tax resisters I’ve been studying.

The most typical Quaker war tax resistance position went something like this:

We must refuse to pay any tax that is levied for the purpose of supporting war or the military, but we must cheerfully pay taxes for the support of civil government even when that government uses some of that tax money to fund a budget that includes military and war spending.

Or, as “Philalethes” put it: “we ought not to ask Cæsar what he does with his dues or tribute, but pay it freely.

But if he tells me it is for no other use but war and destruction, I’ll beg his pardon and say ‘my Master forbids it.’ ”

When resisters would deploy their most daunting rhetoric of conscience and pacifism to defend the first prong of this forked position, their critics would respond by wondering why such passionate reasoning wouldn’t apply equally well to the second.

Attempts to answer this objection by asserting the harmlessness or blamelessness of paying a mixed tax would then threaten to undermine the force of the conscientious objection argument, which seemed to rely on a heartfelt refusal to be involved even indirectly in bloodshed.

As one critic put it:

Why might they not as well resist the payment of a tax which goes to the support of the army or navy of the United States?

If they have any conscientious scruples at all upon the subject, they must be carried out or they are good for nothing.

What difference is there, in principle, between killing a fellow man in war and paying another man to kill him?

And, again, do not the Friends pay one man to kill another when they pay their share of the general tax towards the support of the government and the means of national defense?

There came to be a hotly disputed science of discerning the difference between war taxes and “mixed” taxes, the former being ones that would trouble a good Quaker conscience to the extent of civil disobedience, but the latter being ordained and blessed by Jesus and the Apostles.

The problem was that the nature of the difference between these taxes was difficult to pin down.

If the government raised taxes across the board as it was going to war and raising military spending to match, was this a war tax, or since it was just going into the general budget as before (although a higher percentage of this budget was being spent on war than usual) was it no less objectionable now than it had been before?

What if the government, in the course of raising taxes, had explicitly said that the latest tax hike was for the war?

Would that matter, and if so, how is it that your conscientious objection might be triggered by something of so little weight as a legislative preamble?

In many cases it was indeed the case that the words uttered while money changed hands were thought to be more important than the actual, practical transaction.

Thus, for instance, the Pennsylvania Assembly would not fulfill requests of money for fortifications or other war expenses, but would respond to these requests by granting money “for the King/Queen’s use.”

In this way, although the practical, real-world effect was the same, the Quaker consciences were spared.

“We did not see it,” one said, “to be inconsistent with our principles to give the Queen money notwithstanding any use she might put it to, that not being our part but hers.”

But what of those militia exemption fines that Quakers so regularly refused to pay?

These were fines that conscientious objectors (or, often, anyone with enough money and better ideas of how to spend his time) could pay in lieu of otherwise mandatory military service.

Most of the writings about Quaker war tax resistance that I’ve collected are about resistance to these fines.

But if the fines went into the general fund just like any other tax, as they sometimes did, on what ground could a Quaker object to the one and not the other?

In fact, the evolution of Quaker resistance to militia exemption taxes underwent an interesting shift over time from conscientious objection to a more confrontational civil disobedience.

At first, Quakers justified their resistance to these taxes by saying that they could neither bear arms nor pay a substitute to bear arms in their place, or that they could not pay a tax that was specifically designated for war purposes as this would mean actively participating in war.

But over time, this justification underwent a shift (one that was subtle enough that I have found no records that try explicitly to justify it).

Quakers came to object to militia exemption taxes even when these taxes went into the government’s general fund, or even if they were specifically designated for humanitarian purposes that Quakers would not otherwise object to.

They objected to these taxes, not because the taxes would make them participants in war but because, as the Meeting for Sufferings of the Philadelphia Yearly Meeting put it in :

Believing that liberty of conscience is the gift of the Creator to man, Friends have ever refused to purchase the free exercise of it by the payment of any pecuniary or other commutation to any human authority.

This is a much more radical position. No longer was resistance to militia exemption taxes just a refusal to participate in the wars and fightings of the powers of the world; instead, it became a notice that those powers had overstepped their bounds when they pretended to regulate and tax conscientious scruples.

People trying to extract war money from Quakers occasionally tried to “hack” this odd protocol by which they could approve of “mixed” taxes in most circumstances.

For instance, in when Benjamin Fletcher tried to get the Pennsylvania Assembly to cough up some money to fight the French & Indians, he wrote:

[I]f there be any amongst you that scruple the giving of money to support war, there are a great many other charges in that government, for the support thereof, as officers salaries and other charges, that amount to a considerable sum:

Your money shall be converted to these uses, and shall not be dipped in blood.

You’ll recognize this as the same sort of promise held out by today’s proponents of the Peace Tax Fund Act:

Give the government your money and in return the government pledges it will spend your money only on the good stuff and will spend someone else’s money on the stuff you don’t like.

It took some fortitude to look at mixed taxes and to say that the mixture of taxes for war with taxes for civil government didn’t wash the blood off the former but further bloodied the latter.

The “epistle” of John Woolman and others to their fellow Friends introduced this position:

[T]hough some part of the money to be raised by the said Act is said to be for such benevolent purposes as supporting our friendship with our Indian neighbors and relieving the distresses of our fellow subjects… and we could most cheerfully contribute to those purposes if they were not so mixed that we cannot in the manner proposed show our hearty concurrence therewith without at the same time assenting to, or allowing ourselves in, practices which we apprehend contrary to the testimony which the Lord has given us to bear for his name and Truth’s sake.

Job Scott “believed a time would come, when Christians would not so far contribute to the encouragement and support of war and fightings as voluntarily to pay taxes that were mainly, or even in considerable proportion, for defraying the expenses thereof.”

And Moses Brown worried that this might mean completely unraveling the distinction that allowed Quakers to think of themselves as both conscientiously objecting to supporting war, but also obeying the Biblical instructions to “render unto Caesar” and “pay ye tribute”:

[S]ome Friends refuse all taxes, even those for civil uses as well as those clear for war and others that are mixed, and thereby dropping our testimony of supporting civil government by readily contributing thereto, it has been a fear whether this variety of conduct won’t mar rather than promote the work.

Could we be more united in the ground of our testimony and in our practice in it, I should have more hopes of its speedy obtaining in society.

A time will doubtless come when a smaller proportion will be for war than at present when the greater part being for civil uses, friends may pay as there is and ought to be according to the apostle, a conscientiousness in paying to the support of civil government as well as refuse that for war…

Then he anticipates the “Peace Tax Fund” idea, or something like it:

…to refuse the payment of such when even a lesser part be mixed for war before we applied to the authority to separate them would not at present be my place, but probably before that time come when the lesser part will be for war friends may be agreed to ask a separation which, if it should be refused, we might be united in refusing even those the greater part of which may be for civil uses.

Joshua Maule sparred with other Friends about this issue.

When the government added a war surtax to the regular tax bill, many Quakers were untroubled by paying it: although it bore the name of a war tax, it was collected in the same way as the general tax they’d been paying all along, and like that tax, it was deposited in the general fund and spent at the whim of the legislature.

But Maule felt that by calling it a war surtax, the government had brought it into inevitable conflict with the Quaker conscience, and he lashed out at more accommodating Friends.

“[T]hat [tax] for the war and bounty was not mixed with any other,” he wrote, “until those who paid it voluntarily mixed it themselves and thereby made it their own act to pay the price for men to go forth to the field of human slaughter.”

The way Maule figured it:

[I]f I owe a just debt, I must pay it; if the person receiving the money uses it for a bad purpose, the accountability is with him; but if he demand money of me avowedly to be used in any way to the plundering of my neighbor, destroying his property, or taking his life, then if I furnish money thus demanded I become an accomplice in the evil work and accountable for the sin.

I consider our civil taxes a just debt that should be promptly paid, but I am satisfied that no human authority has either a moral or a religious right to demand of me money or means of any kind to aid in destroying the lives and property of my fellow-men.

But note that Maule only refused to pay the surtax — that portion of his total tax that was “avowedly” being raised for war.

Certainly, though, the government was “avowing,” with every budget, that it was going to be spending some portion of both the surtax and the regular tax on the very same things.

And so those who disagreed with Maule shot back that he was playing plenty of money “to aid in destroying the lives and property of [his] fellow-men” and he knew it, so won’t he please give it a rest.

Nathan Hall put it well when he wrote to Maule:

[W]hether we pay less or more of that tax, a certain proportion of it goes for military or war purposes; and it avails nothing to say: “We did not pay it for that purpose, and if wicked and bad men so apply it, it is their lookout, not ours.”

We can say that of all the tax as well as a part.

If the law had said so many dollars to be raised for war purposes, instead of such a portion of each and every dollar, it would have been plain and not a mixed tax.

Such is not the case; it is all collected together and thrown into one general treasury, where it remains till it is apportioned out for the different purposes designated by the law.

There might be as many different classes of objectors or withholders of tax as there are purposes for which it is appropriated, and the officers of government know nothing of the nature or cause of any of them; they would only know there was a deficiency, and apply that on hand in due proportions for their different purposes, and the deficiency, when collected, in like manner.

To illustrate it more fully I will suppose a case which I believe is strictly parallel, thus:

We both have a testimony against the use of ardent spirits, but are, being very thirsty, placed in a situation where we can get no water except some that has a small portion of whiskey in it.

Being under the necessity of taking something, you may, by inquiry and calculation, find what proportion of the objectionable article is contained in it, and leave just that much in your bowl; while my understanding will be that in partaking I partake of both good and bad, and in refusing refuse both.

So that with me the question is and has been, not what portion I should pay so much as whether any at all.

When I was speaking at the Abundance League a while back about my tax resistance, one horrified liberal — alarmed at the enthusiasm those around her were showing for the stand I’d taken — launched into a defense of government spending on things like roads and general infrastructure.

I thought what a shame it was that such valuable things as these had to be bought at such high prices from their monopoly supplier so as to support their “one Iraq war free with purchase” promotion deal.

An important ancestor to American Quaker war tax resistance that helped to give it its shape and its rhetorical justification was the Quaker refusal to pay tithes to the established church in England (and some places in colonial America).

These sorts of payments were also referred to in Quaker writings as “church rates” or “priests’ rates” or payment for “a hireling ministry.”

The way Barry Reay’s study “Quaker Opposition to Tithes” () tells the story, in the mid 17th century, there were a number of movements, including the Levellers, Diggers, and Seekers who opposed the tithes, and the Quakers obtained a number of converts from these movements perhaps to a large extent because of their own opposition to tithes.

Reay points out many examples of people who first became anti-tithe activists of one sort or another, and only later became Quakers.

Although the Quakers did have scriptural and theological arguments against tithe-paying, Reay believes that their opposition was really based on more down-to-earth concerns: that the tithes were unfairly shouldered by poor, rural people; that they discouraged agriculture (by taxing gross production, not net profit); that corrupt, idle, and greedy tithe-farmers were parasitic on the productive members of society.

It wasn’t just the clergy.

Often, people outside of the clergy would obtain rights to a percentage of the tithes.

About a third of the tithes collected in England ended up in the hands of such people.

“In some regions,” Reay writes, “the figure was as high as 60 per cent, a regular and inflation-proof income.”

Because of this, there were strong vested interests in favor of the tithing system both inside and outside the church, with good reason to oppose this popular insurrection.

They accused the anti-tithe forces of being objectively pro-Papist (indeed, they labeled the Quakers “disguised Jesuits”!) and claimed that the tithe system was not only Biblically sanctioned but based on an ancient social contract which everyone was bound to honor.

Furthermore, they claimed that tithes were only the first target in a larger battle, and if the government were to give in to their demands here, pretty soon the Quakers would be demanding to be free of paying rent to the landlords as well.

As Quakers were not followers of the established church, another reason why they opposed tithes was because the tithes supported a church that they felt was spreading incorrect doctrine.

They argued for a separation of church and state and for government respect of freedom of conscience in matters of religion.

Churches and their ministers, they believed, ought to be maintained by the voluntary support of their parishioners or by their own labors, and not by mandatory, government-enforced tithes.

The Quakers tried to use the existing political process to have tithes abolished — petitioning parliament and supporting sympathetic candidates for election — but they also engaged in and incited civil disobedience.

Reay writes: “The catalogues of Quaker sufferings for tithes conjure up a picture of chaos in many parts of the country, as goods were seized from recalcitrant Friends.”

The rhetoric of Quaker war tax resistance, which was a later development, borrows from the rhetoric of resistance to tithes, though because the issues are different, sometimes this mapping is awkward.

In Samuel Allinson’s “Reasons against War, and paying Taxes for its support” he went so far as to equate paying war taxes with paying tithes:

It is thought to be wrong for Friends to pay taxes for war, a hireling ministry being thereby supported, which is not allowed by us to be consonant with Christ’s doctrine…

In other words, by paying war taxes, you are paying tithes to a ministry that is ministering the doctrine of war.

Interesting, but a bit of a stretch.

I’m getting down to the final stages of my American Quaker

War Tax Resistance book. Here’s a peek at the index. The page numbers

won’t mean much to you except to give you an idea of how much print is devoted

to any particular topic.

A

abolitionism 104, 162, 210, 391

An Account of the Gospel Labours and Christian Experiences, of that Faithful Minister of Christ, John Churchman 70–72, 92

An Account of the Life of that Ancient Servant of Jesus Christ, John Richardson 62–63

An Account of the Sufferings of Friends of North Carolina Yearly Meeting (Spencer) 390–396

Adams, Peter 427

An Address to Protestants (Penn) 33, 39

An Address to the People Called Quakers (Taber) 174, 185–196

The Advocate of Peace 428

Alexander, William 152–153

Allen, John 115

Allen, William 56, 114

Allinson, Samuel 154–171

Amish 265, 311

Amon, James 311

anarchy 192

Andrews, Samuel 8

Anne of England 16, 46

Anthony, Henry B. 423–426

The Apology for the True Christian Divinity (Barclay) 30

Archdale, John 100

Arkansas 357

Armistead, Wilson 20–22

Armitt, John 79

Assembly see parliaments

Autobiography (Franklin) 55–61

Autobiography of Benjamin Hallowell 227–228

B

Babcock, Samuel 122

Baker, Jeremiah 172

Banks, Ephraim 263, 307–310

Barclay, Robert 26, 30–32, 128, 130–132, 193

Barker, Cyrus 383, 395

Barker, Nathan 383, 395

Barnard, Richard 150, 184

Barratt, Thomas 9

Bartram, James 79

Bates, Benjamin 197, 358–359

Beavers, Joseph 114

Bell, Thomas S. 273–280, 289, 301, 339–342

Benezet, Anthony 73, 79, 95–96, 138–139, 154, 173–174, 176, 178–179

Thomas Hazard son of Robert called College Tom (Hazard) 121–123

Thomas, George 50, 53, 55, 59

Thusstone, John 2

Tilton, John 8

tithes, see church rates

Transactions and Changes in the Society of Friends, and Incidents in the Life and Experience of Joshua Maule 362–365, 369–378, 386–390, 396–404, 439–445

trials 13–15, 152, 222

Tribute to Cæsar (Philalethes) 23–42

Trimble, Ann 145

Trotter, Benjamin 79

Tryon, William 6–7

Turnpenny, Jos. C. 448

Tuscarora Indian War 2

U

Underhill, John 8

V

Van Opdam, Heer 261

Vance, Zebulon B. 408, 414

Venable, C.S. 414–415

Vermont 279, 411, 413

Vestal, Tilghman 414–415, 427

Views of the Society of Friends in Relation to Civil Government (Howland) 351–352

Virginia 1, 3–7, 63–64, 76–77, 96–100, 197–198, 365, 383

My new book, American Quaker War Tax Resistance, is now available (you can order it either directly from the publisher at CreateSpace or from Amazon.com).

I get a bigger cut if you order from CreateSpace, but I think it’s probably a better deal for you if you order from Amazon, since that way the shipping is free.

The book gathers together in one place documents from dozens of sources that

show how war tax resistance developed in the Society of Friends in America.

These documents illuminate the Quaker positions on war tax resistance from

many angles — highlighting the search for truth within the Society of Friends

as well as the interest, concern, or aggravation of those outside of the

Society who, in one way or another, found themselves trying to understand or

navigate the Quaker point of view.

This 500-page collection draws on a variety of sources, including:

histories of the Society of Friends, or of particular Meetings or

regions

contemporary records of sufferings and minutes kept by Meetings

rules of discipline published by Meetings

commentaries published in Quaker-oriented periodicals

a novelization of the experiences of Quaker conscientious objectors

government records, and transcripts of legislative debates

published journals by individual Quakers

writings about pacifism and conscientious objection

writings by non-Quakers that relate episodes of Quaker war tax

resistance

writings by people trying to refute or denounce Quakerism or Quaker war

tax resistance

letters in which Quaker war tax resistance was discussed

pamphlets published by people taking one side or another in the debate

over Quaker war tax resistance

petitions sent by individuals or Meetings to people in government

writings from non-Quaker peace movement groups that discussed Quaker

conscientious objection

The collection is indexed, so that it’s easy to find all mentions of, for

example, the “Render unto Caesar…” Bible verse, William Penn, “tax collectors:

encounters with,” excise taxes, “social contract theory,” Mennonites,

“offensive vs. defensive war,” or particular Meetings.

Some of the highlights of the collection include:

Philalethes’ “Tribute to Cæsar, How paid by the Best Christians, And to

what Purpose; With Some Remarks on the late vigorous Expedition against

Canada.…” — a hard-to-find pamphlet and one of the earliest and most

strongly-worded arguments for war tax resistance.

Samuel Allinson’s “Reasons Against War, and Paying Taxes for Its Support” — This was only circulated in manuscript form during Allinson’s life, and

is difficult to find, but was praised by such readers as Moses Brown and

Anthony Benezet.

James Logan’s “Letter to the Society of Friends” — Logan was a Quaker who

disapproved of pacifism and war tax resistance, and he put forth his

reasons methodically and clearly in this letter.

A number of excerpts from the journal and writings of John Woolman on

the subject of war tax resistance.

Timothy Davis’s “Letter from a Friend” in which he puts forward the “Free

Quaker” case for paying taxes to the Continental Congress. Also Isaac

Grey’s and Joseph Taber’s pamphlets of protest against the disowning of

Davis for his pro-tax stance.

Excerpts from Joshua Maule’s journal and “A Testimony for the Truth” in

which he tries to convince Quakers to return to a more firm war tax

resistance.

When I was researching and assembling American Quaker War Tax Resistance, what I originally had in mind was a small spin-off book based on the research I did for We Won’t Pay! — one that was more focused and, being smaller, would be more affordable.

That didn’t work out as planned.

The more I researched, the more interesting material I found, and by the time I finished the project, American Quaker War Tax Resistance was almost as big as We Won’t Pay! and priced to match.

This book is a slim, pocket-sized 94 pages, and includes fifteen excerpts from American Quaker War Tax Resistance of those works that are the most sustained and considered arguments in favor of Quaker war tax resistance.

And I’ve managed to price it under $8, so it’ll be easier on the budget.

It’s getting closer!

I haven’t been wasting my yearly sabbatical, but have been expanding American Quaker War Tax Resistance into a snazzier and beefier edition.

I just sent off for a proof copy to review yesterday:

More than half of the 350+ documents in this collection are new to the second edition.

With some typographical fine-tuning and a little editing, though, I’ve managed to keep the page count (and thereby the price) down; the new edition is only about 15% thicker than edition 1.

Of course, everything is thoroughly indexed and cross-referenced, which is

the big advantage of the book over trying to hunt through the individual

documents here at The Picket Line or elsewhere

on-line. A good, human-tuned subject-matter index is a marvelous thing, and

a Google-like search for words or phrases is really no substitute.

I’ve also dated each document in the collection, based on the date or dates of the episodes it covers, and I’ve included these dates in the page headers and organized the documents chronologically, so it’s easier to flip to a particular period of time if you are hunting for, say, resistance at the time of the War of 1812.

I’ve also expanded my introduction, which gives you some context and shows you

some of the themes that run through many of the documents in the collection.

The new cover art is a tribute to the quote from the journal of Joshua Evans: “I found it best for me to refuse paying demands… which went to pay the expenses of war: and although my part might appear but as a drop in the ocean, yet the ocean, I considered, was made up of many drops.”

It’s not ready to be ordered yet. If past experience is any guide, I’ll

discover at least one glaring flaw while looking over the printed proof that

escaped me in the PDF or layout software

versions and I’ll need to cycle through the proof process again. But it won’t

be long now.

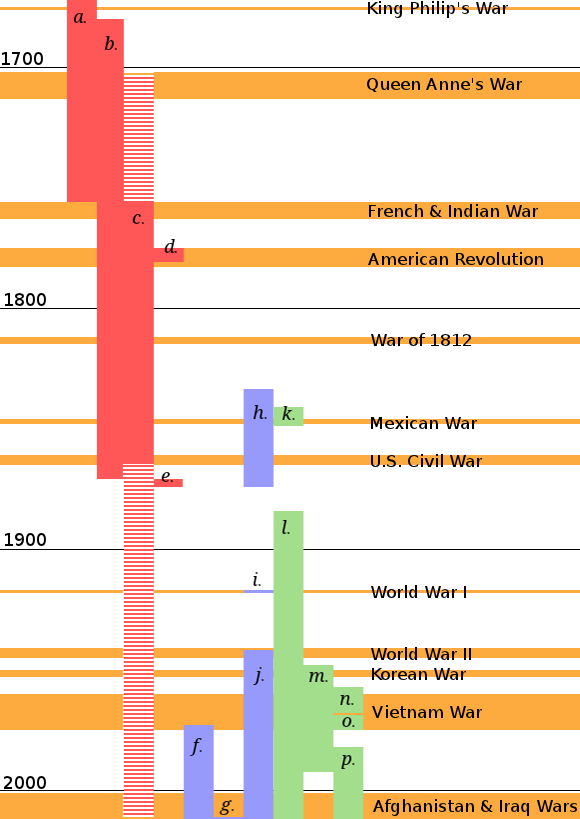

I got the itch the other day to get a birds’-eye historical overview of the war tax resistance movements in America.

Here is what I came up with:

resistance by Quaker-dominated colonial assemblies to requisitions for fortifications and military supplies

resistance by individual Quakers to militia exemption taxes or bounty taxes

resistance by individual Quakers to war taxes, including mixed taxes with a military component

resistance to use of the Continental currency

Rogerene Quaker resistance of militia taxes

Restored Israel of Yahweh sect

the “new monastic” movement

19th century non-sectarian Christian pacifists

World War Ⅰ “bond shirkers” (included Mennonites, political radicals, pacifists, and others)

the Catholic Worker movement

the Concord circle (Alcott, Lane, Thoreau)

Secular anarchist and other “lone wolf” war tax resisters

Peacemakers

the Committee for Non-Violent Action

National War Tax Resistance

the National War Tax Resistance Coordinating Committee

Here is the same diagram with some additional information about the major wars that were at issue in some of these campaigns:

Whenever the authorities arrested, prosecuted, imprisoned, or seized property

from Quaker war tax resisters, whatever Meeting that Quaker belonged to was

sure to make note of it in their book of “Sufferings.” These ordeals “for

conscience sake” were marks of honor and proofs of faith and these books were

in turn the evidence of martyrdom that sanctified the Meeting.

“Friends were always careful to put their sufferings on record,” wrote Stephen

B. Weeks, in Southern Quakers and Slavery. “Whatever

else the Quaker might suffer, he could not bear for the shade of oblivion to

come over the record of his testimonies.”

It was easier for a Quaker to exhibit fortitude in the face of government

reprisal if he or she knew that this would be remembered respectfully.

Monthly Meetings press their cases

It was a common practice for Monthly Meetings to pass their records of

sufferings along to be recorded also at the Quarterly Meeting level, and

then finally at the Yearly Meeting.

After the American Revolution, some American Monthly Meetings used this to

press for more respect for war tax resistance in the Yearly Meeting.

Officially, only Quakers whose tax resistance was due to militia exemption

taxes and other taxes that were explicitly and exclusively destined for war

spending were to have their sufferings recorded. But some Monthly Meetings

recorded sufferings for Quakers who were resisting general taxes, the bulk

of which went to pay off war debt.

In , David Cooper wrote of the Rhode Island

Yearly Meeting:

By a previous rule, such who paid any tax wholly for the support of war

should be dealt with as offenders, but Friends were allowed to pay mixed

taxes a part whereof was for civil purposes and part for war, nor were

sufferings of those who declined to pay these taxes received or recorded.

This subject now occasioned much debate, which resulted in a minute

directing such sufferings to be recorded as their testimony against

war.

In another case around the same time, the monthly meeting in Evesham, New

Jersey tried to forward the sufferings of its members who had refused to pay

war taxes, but their Quarterly Meeting in Salem balked at recording them and

forwarding them further. This led to a great deal of debate in the Quarterly

Meeting and kept war tax resistance on the front burner there — and also in

the Yearly Meeting, which appointed a committee of 36 Friends who unanimously

recommended that these sufferings be accepted and recorded.

Badges awarded by the Women’s Tax Resistance League

As I mentioned

the British

women’s suffrage movement awarded badges to women who had been imprisoned

for the cause, which is a different way of making note of and commemorating

such things.

Poll Tax resisters in the United Kingdom

When local council governments in the United Kingdom tried to shame tax

resisters by publishing their names in the newspapers during the Poll Tax

rebellion of the Thatcher era, the newspapers who published the lists of

“shame” found themselves on the receiving end of letters to the editor from

resisters who were outraged that they had not made the list — and demanding

that their names be included too!

If you can convince an organization to endorse tax resistance, or to recommend it to its members, this can strengthen your campaign and bring in new resisters.

Tax resistance in the women’s suffrage movement started with individual women who saw the logic (and the rhetorical power) of the “no taxation without representation” stand.

But it was an uphill climb to get suffrage organizations to endorse the tactic.

Here are some examples from the U.S.:

Both Susan B. Anthony and E. Oakes Smith offered resolutions advocating tax resistance at the Syracuse Women’s Rights Convention in , but the records of the convention do not indicate whether these resolutions were taken up or voted on.

In the newly-formed Congressional Union for Woman Suffrage announced that while it did not plan to organize a tax resistance campaign, it “would have every sympathy with such action.”

This came in the wake of a call to tax resistance by Anna Howard Shaw, president of National American Woman Suffrage Association.

and from the United Kingdom:

In , the Women’s Freedom League, which had advocated tax resistance since , was joined by the older Women’s Social and Political Union.

“It is to be hoped,” wrote a League member in their newsletter, “that the Women’s Tax Resistance League will succeed in persuading all the other Suffrage Societies to unite on this logical policy of refusing supplies until our grievance is redressed.”

In , the Federated Council of Suffrage Societies “unanimously and enthusiastically” endorsed tax resistance and “recommended its adoption as a means of supporting their demands for a Government measure of Woman Suffrage.”

The classic example of a group adopting tax resistance is that of the Society of Friends, or Quakers.

Since the founding of the Society, it had a policy of instructing members to refuse to pay tithes to rival churches, and this soon expanded to teaching Quakers not to pay taxes for “drums, colors, or for other warlike uses” or fines assessed for refusal to participate in the military.

These policies would be codified in a book of “discipline,” and Quakers who deviated from them would be subject to a process of correction, or, if they continued to defy the policy, “disowning.”

The extent of the policy could change over time, and from meeting to meeting, and there could be heated argument about how strict a standard of tax resistance Quakers should be held to.

Miners’ lodges in western Australia met and voted to instruct the Coal and Shale Employees’ Federation to launch a tax strike in it and other employees’ unions and to back it up with a general strike if the government took action against resisters, in .

In , three American “peace” churches — representing Quakers, Brethren, and Mennonites — issued a joint statement that called for war tax resistance among the 350,000 church members there.

The United Ireland Party — known as the “Blue Shirts” — passed a tax resistance resolution at its annual conference in .

In , the Landlords Association, a group of Jewish property owners in Palestine, adopted a policy of refusing to pay taxes to the British occupation government in protest against its “White Paper” policy.

After the passage of the Education Act which gave taxpayer money to sectarian schools, the Leeds Free Church Council voted 89 to one in favor of promoting tax resistance.

The New York Automobile Club met in and decided to advise its members not to pay a new license fee that it considered to be illegal.

The Moslem League instructed its members to refuse to pay a punitive tax to the United Provinces of British India in .

is the deadline for filing

U.S. federal income

tax returns — “Tax Day” — which is also a traditional day of action and

publicity for American war tax resisters. Here is an overview of some from this

year:

The War Tax Resisters Penalty Fund sent out its Spring Report.

The fund distributed $9,988 to war tax resisters last year to reimburse them for any penalties and interest the IRS had managed to seize from them.