How you can resist funding the government →

about the IRS and U.S. tax law/policy →

how the government deals with tax resisters

I finished my tax returns for .

I ended up owing no income tax, as I had planned, but $770 in additional self-employment tax.

I’ve decided to stop paying my self-employment tax, although I’ll continue to file accurate 1040 forms each year showing how much the IRS thinks I should pay them.

This has been a difficult decision to make.

I have been able to find no legal way of earning enough income to get by without owing self-employment tax (or its cousin FICA), so I’ve been left with the choice of paying that tax and learning to live with it, or resisting it illegally and accepting the consequences of taking that path.

I don’t expect that the consequences are going to be threatening or frightening, just annoying and frustrating.

I figure the way this will probably play out is that the IRS will send me a series of letters that eventually climax in one that informs me that they’ve put a tap on my bank account and seized the money directly, probably with interest and penalties added.

That will be annoying, and may have consequences like bounced checks or difficulty in withdrawing money from an ATM when I need it or some red asterisk on my credit report or some such.

That I can deal with.

What I’d have a harder time accepting would be if the government ended up coming out ahead on the deal — if the interest and penalties were significant enough that I felt that my efforts had been counterproductive.

This is a lot of what led me to choose my legal method of income tax resistance in the first place — by never owing the money, I don’t run the risk of having to pay it involuntarily.

Now I’m augmenting this with an illegal method of tax resistance that doesn’t have that same benefit.

I don’t think it is likely that the government will come out ahead if it decides to pursue my assets.

First off, I don’t owe much — because my income is fairly modest, my self-employment tax is too.

In a typical year, I’ll owe something like $3,000.

This isn’t something the IRS is likely to bring out their big guns for (unless, I suppose, The Picket Line becomes suddenly influential and they feel like they need to make an example of me).

And there is friction in the machine, which is to say that for the IRS to start the process of seizing money costs them money.

As I noted last month, the IRS is planning to outsource its simplest collection cases (a category into which my case may well fall) to private companies.

To cover their costs and give them a profit motive, these companies will swallow about a quarter of what they collect.

That gives some idea of how much the process is expected to cost — but the IRS will also rack up some additional expenses just getting to the point where they decide to turn a case over to these vultures.

I have some control over this — I can, if I choose, take additional steps to hide my assets and make it harder (and more expensive) for them to collect from me.

I don’t know much about this sort of thing, or how difficult it will be.

I may decide it’s not worth the bother.

This does blur the focus of The Picket Line somewhat.

I’ve been able to give a good, simple soundbite about my tax resistance:

“I’m avoiding paying any federal income tax, honestly and legally, by taking legitimate deductions and credits — and you can too!”

Now I don’t have a sound-bite anymore.

I have to explain that I’m resisting the income tax in a legal way, the self-employment tax illegally, (and then there’s excise taxes…).

That’s harder to sell because it takes longer to explain and it’s easy to get into glazed-eyes territory, and it seems more frightening and sketchy to people who might be sympathetic with tax resistance but who get weak-kneed at the thought of getting a stern letter from an IRS computer.

I’ll try to keep good records and “do the math” so I can demonstrate whether or not this really is a practical method of keeping money out of the government’s hands.

What happens if you don’t file your tax return, or if you do file but don’t pay what your return says you owe?

You know there are consequences, but if you’re like most people, you haven’t much more than a vague idea of what they are or how they come about.

Here’s a war tax resistance flashback from North Country Catholic:

Archbishop to withhold tax to protest arms race

Seattle — Archbishop Raymond G. Hunthausen of Seattle has announced that he will withhold 50 percent of his federal income taxes as “a means of protesting our nation’s continuing involvement in the race for nuclear arms supremacy.”

The archbishop’s announcement, first in a local television interview and then in a pastoral letter, came seven months after he suggested to delegates to the Pacific Northwest Synod Convocation of the Lutheran Church in America that one possible non-violent form of Christian resistance to “nuclear murder and suicide” would be to refuse to pay 50 percent of one’s income taxes.

In his letter, dated and released in the issue of his archdiocesan newspaper, the Catholic Northwest Progress, the archbishop stated that he is “aware that this action will provoke a variety of responses,” but urged all persons to “continue to discuss this nuclear arms issue in a spirit of mutual openness and charity.”

He also said that he was not suggesting that all who agree with his peace and disarmament views should imitate his action of income tax withholding.

“I recognize,” he said, “that some who agree with me in their hearts find it practically impossible to run the risk of withholding taxes because of their obligations to those personally dependent upon them.

Moreover, I see little value in imitating what I am doing simply because I am doing it.

I prefer that each individual come to his or her own decision on what should be done to meet the nuclear arms challenge.”

Citing a previous pastoral letter he wrote on the subject, Archbishop Hunthausen stated that certain laws may he peacefully disobeyed under serious conditions, and that there may be times “when disobedience may be an obligation of conscience.”

“I believe,” he said, “that the present issue is as serious as any the world has faced.

The very existence of humanity is at stake.”

What he hopes his words and actions will do, the archbishop continued, is “to awaken those who have come to accept without thinking the continuation of the arms race, to stir even those who disagree with me to find a better path than the one we now follow, to encourage all to put in first place not the production of arms but the production of peace.”

The federal income tax which he withholds, the archbishop said, will be deposited in a fund to be used for charitable purposes.

When Archbishop Hunthausen called for unilateral nuclear disarmament by the United States in an address to the Lutheran synod meeting and suggested nuclear tax resistance as one possible response to nuclear arms spending, his comments received national news coverage.

His speech led Catholic and non-Catholic church leaders in the state of Washington to begin programs of prayer, study and discussion on war and peace issues in their churches.

Archbishop Hunthausen, 60, did not reveal the amount of federal taxes he usually pays or how much one half of his taxes would be.

His chancellor, Father Michael Ryan, said he did not think the archbishop would publicize the amount because it was the symbol of the action that was important rather than the amount of money involved.

Father Ryan also said the archbishop “realizes he’s responsible for facing the consequences” of civil disobedience, but “I don’t think he’d want to speculate on” the penalties he may face (See accompanying article).

An “accompanying article” follows:

Hunthausen could face prison, fine for tax evasion, according to IRS

Washington — If Archbishop Ray mond Hunthausen of Seattle holds back half of his federal income tax in protest over U.S. nuclear arms policy, as he has said he will, the Internal Revenue Service could prosecute him.

In addition to having his assets attached to pay the taxes and interest or penalties on them, the archbishop could face up to five years in prison and $10,000 in fines for each year that he refuses to pay.

“We’ve got to administer the law regardless of the political or philosophical persuasion of the taxpayer,” said Larry Batdorf, an official of IRS’s national media relations office in Washington.

Archbishop Hunthausen said in a TV interview in Seattle that he planned to withhold 50 percent of his federal income taxes to protest U.S. involvement in the nuclear arms race.

In a pastoral letter to his archdiocese a few days later he stated his position more fully and explained it.

Batdorf, following IRS policy, declined to comment specifically on Archbishop Hunthausen’s action or how the IRS would respond, but he outlined the general IRS position and policy regarding those who try to resist or evade their taxes.

He cited the court case of Autenreith v. Cullan, in which a tax resister was trying to withhold part of his taxes in protest over the Vietnam War, as a key legal precedent for IRS policy in such cases.

Batdorf quoted the pertinent part of the judge’s ruling: “The fact that some persons may object on religious grounds to some of the things that the government does is not a basis upon which they can claim a constitutional right not to pay a part of the tax.”

“We feel that the court has ruled very clearly” on that type of protest of conscience, said Batdorf.

He said that during the Vietnam War one popular form of tax protest was to refuse to pay the excise tax on one’s telephone bill.

The IRS assessed and collected the taxes from “about 700 to 800 a year” who engaged in that protest, he said.

He said in most cases the procedure is to try for a civil settlement first.

If the person refuses to file a return or files a low return, the IRS computes the tax, informs the person of its findings, and notifies the person that he has 90 days to make corrections or petition the findings in court.

If the person does not petition, said Batdorf, the tax is presumed correct.

After the court decides in favor of the IRS or the person fails to go to court, the IRS is free to collect the money and can use various means to do so, including attachment of wages or assets.

If the case goes to criminal prosecution, he said, the maximum penalty upon conviction for tax evasion, which is a felony, is five years in prison and a $10,000 fine.

The actual penalties in each case are determined by the courts, not by the IRS, he said.

When a Las Vegas newspaper ran an article about the upcoming tax evasion trial of local resident Robert Kahre, the piece drew dozens of comments from apparent sympathizers.

“IRS forcing a Federal Income Tax on a man’s wages is illegal,” wrote one.

“I have not filed in over 30 years,” another boasted.

A third suggested that people should “organize protests at the courthouse.”

Now, a federal grand jury has subpoenaed the names, phone numbers, IP addresses and other identifying information about every person who commented on the original article, which appeared in the edition of the Las Vegas Review-Journal.

News of the subpoena was first reported last week by one of the paper’s columnists, Thomas Mitchell.

“There was no indication what they were looking for or what crime, if any, was being investigated, just a blanket subpoena for voluminous and detailed records on every private citizen who dared to speak about a federal tax case,” Mitchell wrote.

Some bits and pieces from here and there:

I posted an update about the ongoing IRS software modernization fiasco.

They seem to have more or less thrown in the towel, after years of missing deadlines and busting budgets and burning through contractors.

The latest news goes into some more detail about how they started playing fast and loose with their budget and their milestones as the project started taking on water faster than they could bail.

Basically, when they would miss a milestone and run out of money, they would steal money budgeted for a future milestone and apply it to the work on the one they’d failed to complete under budget.

Clarence Lee Swartz’s book What is Mutualism? () is now on-line.

It includes a section on “passive resistance,” including tax resistance, from which I take this excerpt:

Many of the less important laws are openly and guilelessly ignored or violated every day, to say nothing of the constant and consistent evasion of taxes by rich and poor, pious and pagan, without the least sense of wrong-doing; but the citation of the foregoing is sufficient to point the way to the ultimate refusal of everyone to support or recognize any authority which denies equality of liberty or which fails to give an equivalent in services for every cent demanded for them.…

Until a majority of the people can be brought to see the need for the legislative repeal of certain laws, passive resistance suggests itself as the best means for securing relief from the oppression of such statutes.

This is a method that seems to occur most readily to the average American, for he is always eager to ignore and evade any law that is not supported by a preponderance of public opinion.

He has no great reverence for law as such, and he is encouraged in that disregard of laws and regulations when he observes the impunity with which they are, in many conspicuous instances, violated and flouted.

He sees, furthermore, that a great deal of sumptuary and otherwise obnoxious legislation receives only hypocritical support from many who were instrumental in securing its enactment, and this decidedly lessens his respect for it.

The way is therefore open for making a law so unpopular that the community will not consent to its enforcement.…

Everyone is familiar with the reluctance with which the average citizen faces the tax collector.

Tax dodging, wherever possible, is practiced by high and low, rich and poor, pious and impious, without distinction, And, in all cases, without the slightest compunction.

Since this habit is indulged in by persons who give no other evidence of dishonesty, it may be believed that the motive is not to shirk a just obligation, but that there is an almost universal feeling that no equivalent ever is received for money thus taken.

This skepticism is due to the common knowledge that the politicians who administer the government are rarely capable business man, are primarily influenced, in the expenditure of the taxpayers’ money, by political considerations or motives of self-aggrandizement, and have every other temptation to become prodigal in dispensing funds the provision of which is not due to their own industry.

Even the most uninformed citizen is aware that all government undertakings are incompetently conducted, that the taxpayers’ money is wasted right and left, that there are hordes of grafters in all such operations, who must be taken care of, and that favoritism, at the expense of efficiency, is everywhere the rule rather than the exception.

On the other hand, all experienced business men know that no private enterprise could ever be successfully conducted by the methods pursued by political management and control, and that, were not the supply of funds for covering government deficits inexhaustible by reason of the power of compulsory taxation, every government project would be bankrupt today.

Small wonder, then, that the harassed and beleaguered taxpayer turns eagerly and naturally to the only mitigation of his distress, which is to evade payment of his taxes wherever possible.

The poll tax, the harshest form of taxation ever conceived, has now been abandoned in many states, for it was discovered that more and more citizens were evading it by the simple expedient of failing to register and vote, since the registration lists were the means relied upon by the assessor for locating the person who had no assessable property.

Expediency, that ever-faithful friend of evolution and progress, has again pointed to a logical and serviceable form of passive resistance.

Therefore, by withdrawing support from the State, where it may be done with impunity, and by ignoring it wherever possible, and where its hand bears most heavily upon the non-invasive citizen, the rigors of governmental interference with individual liberty and with the practice of the principles of Mutualism may be modified by creating a vacuum around the arch aggressor.

all records pertaining to those postings, including “full name, date of birth, physical address, gender, ZIP code, password prompts, security questions, telephone numbers and other identifiers… the IP address,” et (kitchen sink) cetera.

You can find minutes and reports from ’s NWTRCC National Gathering in Cleveland on NWTRCC’s website.

There is typically a statute of limitations for federal tax crimes.

However, during wartime the statute of limitations for crimes “involving fraud or attempted fraud against the United States or any agency thereof in any manner, whether by conspiracy or not” goes into suspended animation “until 5 years after the termination of hostilities as proclaimed by a Presidential proclamation, with notice to Congress, or by a concurrent resolution of Congress” where the definition of “the term ‘war’ includes a specific authorization for the use of the Armed Forces, as described in section 5(b) of the War Powers Resolution (50 U.S.C. 1544(b)).”

There are some indications that the government is seeking to suspend the statute of limitations for federal tax crimes because of the present state of war.

TaxProf Blog reports: “The Treasury Inspector General for Tax Administration yesterday reported that 372,000 taxpayers erroneously claimed education tax credits in , totaling $532 million (an average of over $1,400 improper credit per taxpayer).”

Those tax resisters lucky enough to be expecting a large inheritance may take heart from this story of someone who successfully engineered her will so that her heir could donate to charity exactly enough of her estate so that she would owe no estate taxes on the remainder.

Anti-abortion political pressure has led to Congress inserting language in the upcoming health care legislation that would prohibit taxpayer money from going to pay for abortion.

Tom Tomorrow wonders when people opposed to their tax money being spent on war will get that kind of respect:

Another aspect of the upcoming health care legislation is that it includes a big role for the IRS.

This isn’t because the IRS is particularly skilled at administering social welfare programs (indeed fraud is rampant in programs like the earned income tax credit or those education tax credits mentioned earlier in this post), but because legislators have various incentives to hide the spending behind their legislation by not spending outright but only via tax credits and deductions and such.

Since increasing funding for the IRS is not politically popular, this all may have the effect of saddling the agency with more responsibility without giving it sufficient resources.

When Vivien Kellems resisted the federal income tax withholding system, she was subjected to an unusually intense smear campaign, which included the government intercepting her private mail and making it public, as shown in the following Associated Press account from the :

Anti-tax U.S. War

Plant Owner Called Sweetheart of Nazi Agent

Washington, . — (AP) — Miss Vivien Kellems, Westport, Conn., war contractor who advised businessmen not to pay income taxes, was described in Congress today by Representative John Coffee (Dem., Wash.) as the sweetheart of a Nazi agent in Argentina.

Coffee read to the House of Representatives love letters he said she

exchanged with a German count in Buenos Aires. He told his colleagues Miss

Kellems possessed war equipment blueprints “of inestimable value to the

enemy,” and demanded that the justice department “put an end to this

incredible conspiracy.”

Without disclosing how he obtained it, Coffee said one letter from Miss Kellems to Count Frederick Karl von Zedliz in Buenos Aires was signed “all my love sweetheart, Vivien.”

“I say that Vivien Kellems is a menace to the American war effort,” Coffee

said. “This woman, who is in constant touch with our hated Nazi enemies — this woman, the love of a Hitler fifth column spy in Argentina, admits by her

own statements, that right now in Connecticut, she is engaged in work for the

armed forces of a highly restricted and confidential nature.”

Miss Kellems, whose Connecticut plant makes signal corps equipment, announced in she had skipped her income tax payment and would use the money to set up a post-war reserve for her firm.

She made speeches urging other businessmen to do the same thing, bringing from Treasury secretary Henry Morgenthau the remark:

“To advise citizens to refuse to pay taxes — particularly in time of war — smacks of disloyalty.”

In turn, Miss Kellems charged that the government had squandered billions on “boondoggling.”

Later she announced that she had made one payment on her taxes because she

found she had some ready cash. She denied advocating anything illegal, saying

the law permitted postponement of taxes when a person could not pay. To pay

in full at once she insisted, would spell bankruptcy.

She also charged she was being “violently smeared” and denied a statement, which she attributed then to a radio commentator, that she was engaged to marry Count von Zedlitz.

Coffee said Von Zedlitz was on the British black list as an enemy agent, and

said Miss Kellems’ speech advising business men not to pay income taxes was

made after she received a communication from Von Zedlitz.

He told the House Miss Kellems wrote Von Zedlitz that an astrologist had told her she would “play a part, not only in national affairs, but also in international affairs” and concluded the letter by saying “how could that be if I am not married to you?” He said that indicated her intention of marrying “this agent of the German Reich.”

“This same Miss Vivien Kellems, who advises American business men not to pay

their income tax and support the war effort, admits that she consulted with

the Nazi agent in Buenos Aires on her proposed seditious speaking tour,” the

representative said. “In that same month Von Zedlitz wrote to Miss Kellems …

Wishing her ‘joy’ in the ‘monstrous speaking program.’

“Miss Kellems poses as a patriot; yet she has consistently played the Nazi game,” Coffee said. “Vivien Kellems is today giving aid and comfort to the enemy.

Vivien Kellems is today a tool of the Goebbels propaganda machine.”

Coffee told the House Miss Kellems “is the lady who ran against our own Clare

Boothe Luce in .”

He said it was his contention that any American citizen who deliberately advises American business men not to pay taxes which the law imposes “is guilty of such reprehensible conduct as justifies her prosecution at the hands of the Department of Justice.”

The letters were also leaked to the press.

As far as I know, there was no real evidence that Von Zedlitz was in fact a

Nazi agent or even a Nazi sympathizer. But this did sideline Kellems’s

political career (she had run against Luce in the Republican primary, and had

been planning another run), though she came back as an

anti-Bush Republican

senatorial candidate in the 1950s.

John Coffee lost

his seat in the election of , and never made

a comeback.

Kellems kept up her anti-income-tax fight, saying: “Your vicious Nazi smear technique of the New Deal has been successful in silencing other American citizens who have dared to differ with the views of the present administration.

But since I have nothing to conceal I am not afraid and all your fulminating and personal abuse will not swerve me from my purpose, which is to effect the repeal of the income tax and to persuade congress to pass some sensible tax laws.”

In this world nothing is certain but death and taxes. — Benjamin Franklin

One lady who is resisting this certainty is Vivien Kellems.

At 77 years old, she is tiny and slender with carefully coiffed, silver-gray hair and a face which shows the fine wrinkles of thousands of smiles.

And she is rich.

Vivien Kellems could be the classic example of a benign little old lady, were she so inclined.

She isn’t.

And that has complicated life for a lot of people — most of whom work for the Internal Revenue Service.

Come April 15 every year, many American citizens like to think of Vivien. For

at an age when most of her contemporaries would be content to curl up with

their memories of Rudolph Valentino, Ms. Kellems — businesswoman, feminist

and rebel with a lot of causes — is still an enthusiastic volunteer in a very

long war against the income tax. She has refused to pay any since

, sending in signed but otherwise blank

federal returns.

Sitting amid her antique glass collection while she nibbles hors d’oeuvres served by her maid of 20 years, Ms. Kellems hardly looks like a revolutionary.

But when she talks about the income tax, it’s with an activist’s outrage.

“My fight is in the best American tradition,” she says. “I want to be a test

case. I get these letters from old ladies saying, ‘I couldn’t do it, but I

just want you to know how I feel.’ They’ve given me the courage to go on.”

And they also send contributions to the cause.

And so she fights on, part of the year from the Brentwood, Calif. mansion of her brother Jesse and the rest of the time from her pastoral 100-acre estate in quiet East Haddam, Conn.

Her current crusade is aimed at the federal income tax laws’ discrimination

against unmarried people, whose tax rate can be as much as 20 percent higher

than that for married people. Sheldon Cohen, former commissioner of the

IRS

under President Johnson and now a tax consultant, says, “I think she’s right

about single people. She’s a Don Quixote in this area. Some of the windmills

deserve to be tilted at. But there isn’t any complete justice. Ultimately,

she’s not going to win.”

Vivien Kellems would dispute this.

Now one of the best known and respected tax lobbyists in Washington, she has persuaded New York’s Representative Edward Koch to introduce a bill that would create one tax rate for everyone.

And she is working to get the bill out of the House Ways and Means Committee, where it has been kept languishing for three years by Chairman Wilbur Mills, long the Horatio at the tax reform bridge. “If we can blast the bill out of committee, it’ll sail through Congress,” she says. “Wilbur Mills promised it will be out of committee this session.

Mr. Mills and I are close friends, but he’s let me down four times.

You don’t get a law passed in Washington because it’s just and fair but because it’s politically expedient.”

While she lobbies in Washington with one hand, Ms. Kellems is keeping the

IRS at

arm’s length with the other. Since she first refused to fill in her tax form,

she has been barraged with claims, penalties and interest levied against her — $122,000 worth. But so far she has paid only $813.30 for a medical

deduction on her return which was

disallowed by wrist-slapping

IRS

auditors in . (The

IRS is

planning to take her back to court in .)

“The IRS demanded my records and subpoenaed my accountants to get them,” Ms. Kellems says. “I said that I was pleading the Fourth and Fifth amendments, that my income and my records were my property and could not be seized without a court warrant, and that I didn’t have to answer when it might tend to incriminate me.

Then I got a letter from the IRS saying I had properly pleaded the Fifth and they wished to withdraw the suit.

I haven’t filed now for five years.

They assess interest against me, and I assess interest against them.” She reckons that by — when she stopped paying — the government owed her $72,000 in taxes collected in previous years when she was paying the single person’s rate.

Ms. Kellems in fact tried to sue the

IRS for

$2,939.13, which she said was the penalty she paid on her

taxes for being single. Although she knew

she had little chance of winning, she fought her case all the way to the

Supreme Court. Last spring, that ultimate tribunal refused to consider it.

More recently, Ms. Kellems has been counterattacking the tax system on another front.

The objective was a capital gains and dividends tax program instituted in and in her home state of Connecticut.

Half the objective has been won already: after a drive in which she played a major role, the dividends tax was repealed in .

And, concedes a state tax official with a sigh, she also played a major role in getting the capital gains tax cut in half.

Vivien Kellems was born , in

Des Moines to parents who were both ministers of the Christian Church

(Disciples of Christ). The family moved to Eugene,

Oreg. when she was 2. Vivien

grew up there as the only girl in a family of six children and was always

close to her brothers.

She graduated from the University of Oregon — where she was the only coed on the debating team — and stayed on to complete a master’s degree in economics.

Her elder brother Jesse (he is alive but seriously ill) insisted that Ms. Kellems continue on to her doctorate at Columbia University.

But when Jesse, also a clergyman, ran out of money before Vivien completed her thesis, she went to work, booking appearances for the U.S. Marine Band. (Ms. Kellems is currently completing her doctorate in economics and win soon submit her thesis on “how individuals can act to change the law” to the University of Edinburgh, where Jesse received his Ph.D. 50 years ago.)

Then another brother, Edgar, whom Jesse had put through

MIT, invented a device — the cable grip — for installing, handling and

supporting electrical cables. Ms. Kellems had $1,000 saved, so she staked

Edgar, and together they founded the Kellems Company in

, with Vivien as president. “I started with

one man and vast ignorance,” she recalls. By the time the Kellems sold the

company to Harvey Hubbell

Inc. in

, it was a flourishing enterprise with 135

employees. Since the company was not public, the amount received was not

disclosed.

“I loved the cable grip business,” Ms. Kellems says. “Men always try to hide the fact from women that business is so much fun.

I had no intention of selling, but it became harder and harder — and the tax situation for a small business was incredible.

Then Hubbell came along, and they agreed to keep the factory where it is in Stonington and to keep on all our employees.”

Mrs. Rose Gee, formerly an assistant to Ms. Kellems at the Stonington

operation, says, “If you started to work for her, you would never have thought

of leaving — she was that kind of person. Everybody loved her.”

Well, not quite everybody.

For Ms. Kellems had already begun her long struggle with the IRS.

Round one involved the withholding tax.

“When they passed the withholding tax, it was as a war measure, but they never

took it off,” she says, still a little indignant about the whole thing. “I

mulled that over. Then I was giving a speech at the Biltmore Hotel in Los

Angeles one night in , and I heard myself

saying that I would not collect any more withholding taxes from my employees.

I said I wasn’t going to be an agent for the government. If they wanted me to

be their agent, they’d have to pay me, and I wanted a badge.”

She didn’t get a badge, but she got a lot of flak from the IRS.

Even though her employees were themselves paying their withholding taxes, the IRS hit Kellems with a $7,600 penalty.

After a lengthy court battle, this argument was settled.

The Kellems Company started withholding. “I had to,” she says, “or they would have bankrupted me.” During the 1950s, she took her antitaxation campaign to the public. “When I needed a platform,” she recalls, “I would run for office.

I ran for governor, for senator, for Congress, and lost every time.” She had more success with another cause in Connecticut in , when she sat in a voting booth for nine hours to protest the difficulty of ticket-splitting on the voting machines used in the state.

After toppling over from fatigue, she was finally removed from the polling place.

Subsequently, Connecticut’s voting machines were modified to allow easier vote-splitting.

Through most of her endeavors, Ms. Kellems has remained a loner, turning down

chances to affiliate with such groups as CO$T

(The Committee of Single Taxpayers) because, she says, “I’m not a joiner, I’m

just not that kind of person; basically I’m a Victorian.”

A handsome woman who twice made the nation’s best-dressed list in the early ’40s, Ms. Kellems is not without a trace of feminine vanity.

Pouting after losing the Republican nomination for Congress to Clare Boothe Luce in , she said, “Everybody talks of Clare Boothe’s sex appeal.

Nobody mentions mine.”

She was married at 23 to a World War Ⅰ Navy veteran but left him after two

weeks and got a divorce a year later. Her only other publicly serious romance

involved an engagement during World War Ⅱ to a German businessman long

resident in Argentina — Count Frederic von Zedlitz. Because he was on a

British-American wartime blacklist of German nationals abroad, journalists

Drew Pearson and Walter Winchell accused her of fascist sympathies.

Ms. Kellems insisted that her fiancé was anti-Nazi.

But she was shattered by the allegations, and the engagement dissolved.

In she wistfully told a reporter, “If I had settled down to a normal life, if I had married and raised children, I’d probably never have gone barnstorming around the country on all these crusades.”

Today she is resigned to a single life, saying, “Of course I’ve had my share

of romantic entanglements. At my age, who hasn’t? But I could never marry

now, not with the fight for equality for singles going on.”

Always an ardent feminist, Ms. Kellems has been campaigning in support of the Equal Rights Amendment for women. (She attacked discriminatory work curfew laws in Connecticut as early as the 1940s.) But taxes are her main concern. “This tax fight is stimulating, and it’s fun,” she says. “It takes the place of business; this is a matching of wits, too.

“I’ve met absolutely lovely people in the

IRS,

though. They do terrible things, but my relationship with them is just

fabulous. I get invited to

IRS

parties and they say to me, ‘Keep it up, Miss Kellems.’ I have many, many

friends.” The sentiment appears to be reciprocal.

Banking tycoon J. Pierpont Morgan once said, “If the government cannot collect its taxes, a man is a fool to pay them.” If he had been a little less of a sexist, he and Vivien Kellems would probably have gotten along just fine.

Kellems used to tell her supporters to “enclose a used, dry tea-bag or coffee grounds to spill out on the desk” when writing letters of protest to Congress, as an allusion to the Boston Tea Party — a tactic that has come back in recent years.

These days, though, it’s more likely to result in a HazMat team and an office building lock-down than a simple trip to the wastepaper basket (which, come to think of it, probably makes it a better tactic than ever).

Ed Hedemann of the National War Tax Resistance Coordinating Committee has put

together some interesting charts and tables showing all known prosecutions

and property seizures against

U.S. war tax

resisters since the 1940s:

I wonder if this sort of thing is still going on (from the Ocala Star-Banner):

Tax Resisters To Face Agents

Helena, Mont. (AP) —

The Internal Revenue Service is sending agents to Montana taxpayer meetings to collect names and run tax checks on many who attend, says IRS district director Frederick Nielson.

Nielson said he authorized the monitoring program “some time ago” as tax protests intensified across the state.

The agents focus on speakers who encourage audiences to challenge the federal income tax, but they sometimes compile names of all persons present, Nielson said .

“Those are open, public meetings and our position is that we have as much right to be there as anyone else,” Nielson said.

“We feel that if people are bragging about not filing returns, it’s our obligation to identify those people, pull their returns and see if they are filing.”

An IRS spokeswoman in Washington acknowledged such monitoring, but it was unclear how widespread the practice is nationwide.

Washington (AP) — The Internal Revenue Service threatens to attach salaries or bank accounts of critics of U.S. policy in Viet Nam who refuse to pay their income taxes.

The IRS did not say when it would act, adding it would wait until all facts in each case can be checked.

A spokesman says criminal prosecution also is a possibility in such cases.

The IRS made its warning after a Washington newspaper advertisement carried the names of about 350 persons, saying “we will refuse to pay our federal income taxes voluntarily.”

No mention was made by the IRS of a protestor’s failure to file an income tax return.

This failure carries penalties of its own — 5 per cent monthly of what is owed, up to a maximum of 25 per cent.

The law also provides a penalty of one year in jail and a $10,000 fine for failing to pay the tax.

But the IRS indicated it would rather obtain the taxes owed rather than subject a citizen to criminal prosecution.

When Nixon got caught using the IRS to go after his political enemies, one of the consequences was that the agency — though on the cusp of victory in its battle to seize the home of war tax resister Ernest Bromley — surrendered and returned the home to its rightful owners.

Washington, D.C. (AP) —

A pacifist group’s scheduled protest rally at Internal Revenue Service headquarters turned into a victory celebration after the agency reversed its seizure of a home owned by members of the organization.

While about 40 members of the Peacemakers danced and sang outside, IRS Commissioner Donald Alexander received several of their leaders in his office to confirm the decision to drop all assessments against the 25-year-old group.

The action meant the return of the Cincinnati, Ohio, home of Peacemaker founder Ernest Bromley and several friends active in the organization.

Earlier this year, the IRS technically seized the house against a claim of $33,000 the group allegedly owed in back taxes for the years .

None of the occupants was forced to move out.

Talked With Bromley

A spokesman for Alexander said the IRS district office in Cincinnati decided to reverse its lien upon the property following an interview with Bromley.

As to why Alexander personally met with Peacemaker leaders, the aide would say only “he talks with various groups from time to time.”

Bromley did not attend [the protest/celebration, presumably —♇] because of illness, friends said.

The tax assessment against the Peacemakers had followed a probe in of that group and other anti-war organizations by the now-defunct Special Service unit of the IRS.

According to revelations which surfaced during the Watergate scandal, the unit developed an “enemies” list of about 11,000 individuals and groups with anti-war views.

Alexander has long acknowledged that activity as improper and has promised that the list would no longer be used in tax investigations.

Politically Tainted

In the meantime, the Peacemakers protested the levy on grounds that the case was politically tainted and, moreover, that ownership of the Cincinnati house was not tied directly to the organization and hence was not liable to seizure.

The case attracted considerable controversy in the Cincinnati area, including an 8-1 vote of the City Council to request a congressional investigation of the IRS action.

One Peacemakers spokesman, Chuck Matthei, said the group thanked Alexander for the reversal “despite the recalcitrance” but also told him of suspicions that Special Services files are still active in IRS regional offices.

Moreover, said Matthei, the group vowed to continue its advocacy of non-payment of federal taxes so long as any portion of them go to support the defense program.

Matthei said he and most of the other pacifists still active in the group deliberately live below the taxable income level to avoid criminal liability.

The following comes from the edition of a zine from Cleveland, Ohio that went by the name The Buddhist Third Class Junkmail Oracle:

As a result of the widening war in Vietnam, federal legislation was passed which, in , restored the 10% tax on telephone bills.

“It is clear,” said Rep. Wilbur Mills, who managed the tax legislation in the House, “that the Vietnam and only the Vietnam operation makes this bill necessary.”

[Congressional Record, ]

Congressman Mills was always careful to refer to “our operations in Vietnam.”

But those of us who know its true nature know it is not an operation but a

tragic bloodbath. We know that revenue for the Vietnam war pays for:

napalm, mass bombings, and other attacks on civilian areas resulting in

extermination of thousands of Vietnames — about 200,000 casualties in

the last year and a half;

forcing young Americans into “kill-civilians-or-be-killed” situations.

Over 14,450 G.I.s have been killed

in vietnam;

perpetuating a military dictatorship;

violation of the Nurenberg precedents, the U.N. Charter, and the Geneva Accords of ;

indefinite continuation of war against a people who desire above all to be

alive and to determine their destinly free from foreign domination.

A tax boycott demonstrates that you believe this war to be immoral and/or

illegal and that you are willing to act on this belief.

We boycott the telephone tax because:

it is directly imposed to pay for the Vietnam war;

anyone with a phone can refuse to pay this tax;

the monthly refusal of a small amount of money creates a thorny

collection problem for the Internal Revenue Service.

Over three thousand people in all parts of the country are currently refusing

to pay this war tax. In virtually every case telephone companies have assured

the refusers that their telephone service will not be interrupted.

A recent announcement by

IRS

that in the future phone tax refusers would not be granted personal hearings

is an indication of what a strain we’ve put on their resources. We know that

the San Francisco office of

IRS

even wrote to the Attorney General in Washington asking for help in coping

wth this problem (Washington was unable to help). In an effort to harass phone

tax refusers in the Midwest

IRS has

begun charging what is probably an illegal $5 fine for the privilege of taking

the unpaid taxes from a bank account. Interest at the rate of 6% per year is

also charged. We are encouraging phone tax refusers to respond to the

elimination of the personal hearing by insisting that they have a meeting and

if the request is denied, beginning legal action since the new procedure

amounts to a denial of due process. Those who are fined $5 should also

consider legal action. Clearly, the government’s position vis-a-vis those

opposed to its policies is that in case of conflict between the smooth running

of its machine and the right of individuals to exert whatever influence they

can on policy, individual rights will have to be sacrificed. In America we

usually do it the other way, or so we have been led to believe.

Telephone companies have for the most part been cooperative — even helpful.

Some people in Maryland who couldn’t bring themselves to refusing the tax

compromised by sending a letter of protest with their payment. The phone

company called up and proceeded to explain how one subtracted the tax,

assuming that these customers wanted to refuse the tax but didn’t quite know

how.

This comes from the Minnesota Daily, and gives some rare insight into the government’s anxiety about war tax resisters at the time, and the difficulty it had in responding to the threat in an effective way:

The case of Carole Nelson, a young Minneapolis woman who refuses to pay her federal income tax to support war, could set an important precedent, Richard Oakes, her attorney, said during an interview .

“The government is kind of flailing around, looking for ways of prosecuting tax refusals,” Oakes said.

“They’re exploring various civil and administrative ways to get at this thing.”

Nelson refused to obey a U.S. District Court order requiring her to give tax information to the Internal Revenue Service (IRS) .

She is scheduled for a court hearing to show cause why she should not be held in contempt of court for refusing to obey the order.

Although Sally Buckley, the first war tax resister to be prosecuted locally, was tried under criminal statutes, Nelson’s case has so far been conducted under civil law.

If Judge Earl Larson finds her in contempt of court, he could order her to go to jail with a six-month maximum term until she is ready to pay.

He could also issue a light sentence, ask her to think her refusal over, and then give her another chance to provide the information or he could give her a straight contempt sentence.

All three actions could be challenged in court, Oakes said.

Although he said issuing a fine is rare in contempt cases, Oakes thinks Larson might impose a fine against Nelson comparable to the taxes he thinks she owes.

Paradoxically, since Nelson has said she has very little in assets, she may own [sic] no tax.

The amount she owes cannot be figured until she supplies the IRS with the requested information.

The case is also complicated by the fact that the Washington-based Justice Department lawyer prosecuting the case for the IRS, John Hines, would rather not have to prosecute her.

At a previous hearing, Hines told Nelson, “I want to do this even less than you can imagine. I read Thoreau too.”

“Hines is a decent guy,” Oakes said, noting that Hines could have asked for a contempt citation at that hearing.

“He’s got some personal sympathies.

I don’t think he’d like to see her got to jail.

“The government is quite upset about this case,” Oakes added.

“You can be accused of bank robbery and they won’t fly a guy in from Washington.”

One of Nelson’s friends remarked after the hearing that the cost of flying Hines to Minneapolis probably exceeds whatever tax she may owe.

Oakes said he believes the government’s attention to the case rests on the fact that “taxpaying is basically a voluntary act.

“If everybody quit paying their taxes, the government would go out of business,” he added.

Hines confirmed that the case costs more to pursue than the government expects to gain in tax from Nelson but added that not to prosecute “would set a precedent that we could not afford.

“We have good precedents on our side,” he said.

“It’s an important case to us only in the publicity that would come if we lost it.”

War tax resister Carole Nelson was held in contempt of court for refusing to obey a court order directing her to provide the federal government with information about her financial status.

U.S. District Court Judge Earl Larson sentenced Nelson to imprisonment for a maximum of 10 days “or until she purges herself of the contempt,” (by complying with the order).

Her attorney, Richard Oakes, called the relatively light sentence “nothing short of fantastic.

“I’m amazed. I consider this a victory,” he said.

Nelson was ordered by Larson to present herself to the Internal Revenue Service and fill out a form on her financial status.

She did not comply.

Justice Department tax division attorney John Hines had asked Larson for incarceration of Nelson until she complied with the order.

The maximum imprisonment for contempt is six months.

Hines said the statute the government was trying to get Nelson to obey was intended to combat organized crime.

“I don’t want her (Nelson) to go to jail.

But I’ll do anything to fight organized crime,” Hines, who is involved mainly in organized crime tax cases, said.

In his closing statement Oakes said, “I think the government fears the publicity in this matter more than the consequences.

This is not a person who ought to be incarcerated.”

Oakes also argued that the government could get the information it wanted about Nelson from social security and other government records.

In a statement read from the witness stand, Nelson said it was “a perversion of justice to be here to show cause why I should not be charged with contempt of court for refusing to be an accomplice to killing.”

She is basing her refusal to provide the information on her Christian beliefs.

She has sworn that she has no assets.

If each person obeyed or disobeyed laws according to his conscience, “it would let every citizen be a law unto himself,” Larson said.

Larson said the contempt citation was the first he has issued in the 11 years on the bench.

Oakes said he expects no further prosecution of Nelson.

Some bits and pieces from here and there:

“Will I Get Audited?” — a frequently expressed worry of people contemplating war tax resistance.

The answer: probably not, though it depends on how you go about it.

But here are some responses from the IRS you can expect, and some options for how you can respond in turn.

(From Ruth Benn on the War Tax Talk blog.)

tax resisters across Italy hold up “#IOnonMIammazzo” hashtag signs to demonstrate that they refuse to sacrifice themselves for extortionate taxes

Tax resistance continues its viral spread in Italy, now semi-organized under the “Io Non Mi Ammazzo” (“I won’t kill myself”) banner.

This latest incarnation of what seems to be a growing and converging set of campaigns was spurred by Facebook post by Scordia bartender Giuseppe “Pippo” Barresi in which he said, in part: “I do not mean to be a tax evader, but given the choice of not paying crazy and unnecessary taxes or reducing my family to hunger, I choose the first option.”

Barresi, as with other recent resisters, is claiming a necessity defence under the criminal code and also a Constitutional right to not be subject to unbearable taxation.

“It’s as if my family were threatened by a wild beast.

Only that beast is the state.”

A common argument against tax resistance goes something like this: The government will add penalties and interest and such to the amount you refuse to pay, and when they eventually wring the money out of you, in the end you’ll have given even more financial support to the government than you would have if you’d just paid up in the first place.

Today I’ll show you some evidence that I hope will convince you that this is not a very good argument.

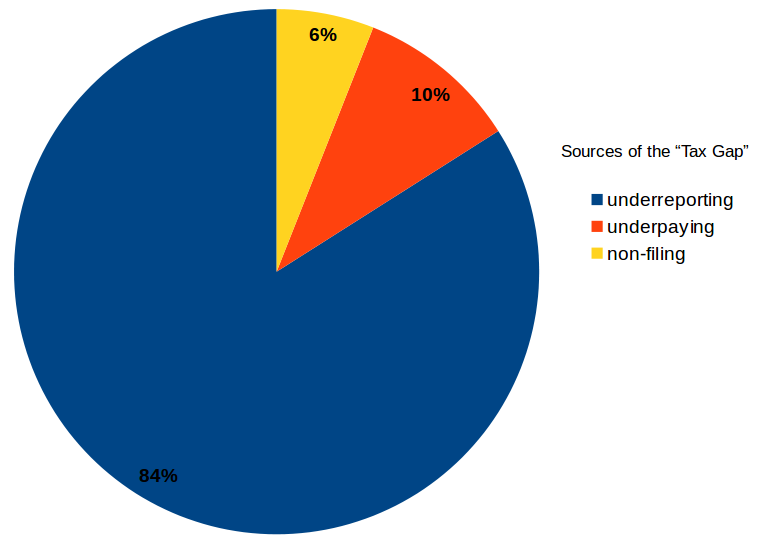

Lots of people don’t pay the IRS what the agency thinks they should.

The IRS has tried to figure out where this missing money is hiding, but their methodology isn’t all that great, and it’s not an easy mystery to solve.

Their best guess is that the vast majority of missing taxes comes from “underreporting” — that is, taxable activities that the IRS never becomes aware of.

For example: if you placed a bet with a friend on the outcome of the Super Bowl, the winner of that bet should have added the amount won to their income and should have paid taxes on it, according to the IRS anyway.

Most people don’t go out of their way to report taxable transactions like these that the IRS wouldn’t learn about on its own, and so a lot of these transactions never get taxed and they stay in the “underground economy.”

An estimated 84% of the “tax gap” comes from unreported taxable activities like these.

Another 6% comes from taxable activities the IRS does learn about, but for which the responsible party never bothers to file a tax return.

The remaining 10% comes from people whose tax debt is registered on paper according to Hoyle, but who never get around to forking over the money.

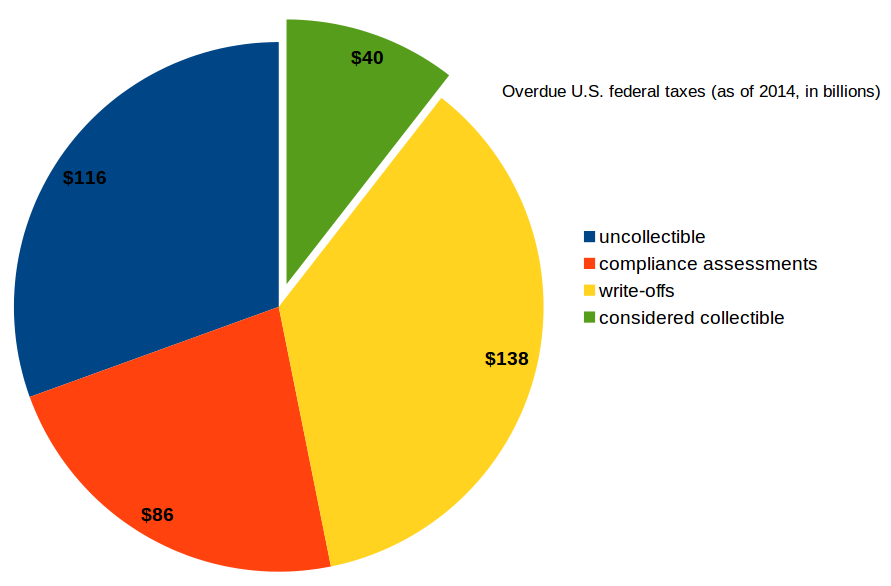

According to IRS financial statements for , there were at that time about $380 billion in outstanding unpaid taxes that it knew about.

This includes about $205 billion in interest & penalties added to the originally-due taxes, but it does not count any taxes that people have thus far successfully evaded by keeping out of the IRS’s view — that is, all the stuff in the 84% blue area above.

It also doesn’t include amounts that the agency can no longer pursue because the statute of limitations has expired.

Of that $380 billion, the agency considers $116 billion to be “currently uncollectible” (“primarily because of the economic situations of the taxpayers”).

Another $86 billion is something called “compliance assessments” — which I think means the IRS tells a taxpayer who hasn’t filed a return (or a fully-revealing one) what the agency suspects the taxpayer would have owed if they had filed accurately, but the taxpayer isn’t going along with it and the controversy is still in limbo.

The agency doesn’t have much confidence in collecting this money either.

There is also a category called “write-offs” that totals $138 billion.

This is tax debt that is hopelessly uncollectible because the taxpayer is bankrupt, insolvent, dead, vanished into thin air, or something of that sort.

That only leaves about ten percent of the total that the IRS considers to be collectible and includes as a potential asset on its financial statements.

So to $175 billion in unpaid taxes, the IRS has added $205 billion in interest & penalties, but it only expects to collect $40 billion of the total (in recent years it has actually collected closer to $46–49 billion per year by means of its enforcement arm, so it may somewhat exceed its expectations).

This I think shows conclusively that people who don’t pay their taxes do not, in the aggregate, ironically end up paying more to the government.

of the $380 billion owed to the IRS in back taxes, the agency only hopes to collect the $40 billion green slice of the pie

For tax resisters — who are typically alive, solvent, and often have seizable assets and income streams — the news isn’t quite as good as this chart would suggest.

But even from juicy targets like us, the IRS fails to seize enough money in penalties and interest from some of us to make up for the money it fails to seize from those of us it lets slip through its clutches.

An informal survey of war tax resisters a few years back, for example, found that the IRS had successfully seized only about 25% of what those resisters had refused to pay.

In addition, it is costly for the agency to deploy its collection apparatus: sending out all of those letters, filing liens & levies, managing the associated bureaucracy — all of that costs money.

The IRS spends about $5 billion dollars on enforcement (including investigations, audits, and collection), and so resisters contribute to this additional cost of the government conscripting our support.

So if you are hesitating to refuse to pay taxes because you worry that by doing so you may inadvertently swell government coffers… I hope this has reassured you that in the aggregate, tax resisters do indeed cost the government money.

Some links of interest:

Tax Resistance Heats Up in the U.S.

Allen D. Madison of the University of South Dakota Law School has written up a good summary of The Legal Consequences of Noncompliance with Federal Tax Laws [in the U.S.].

There’s an important difference between what the IRS can do and what it will do, but if you want to know what it can do, this paper is an authoritative source.

If Stephen Miller and Steven Bannon and Trump continue to run the country and

we have international wars and we have a government that won’t comply with

court orders, we are going to need tax resistance. Tax resistance is the kind

of thing, like general strikes, that people toss around really easily and

say, “We should just not pay our taxes,” but, again, I think this moment is

pretty unique in American history. Tax resistance has been a part of the

history of the United States of America since the beginning… Like a general

strike, it [can] happen if everybody is going to do it. People need to get

together and create a means by which folks can actually feel comfortable not

paying their taxes, putting it into a separate account and getting receipts

for it and all doing it together as a collective political statement.…

Tax resistance is something [with which] we can break their backs, and when

and if it is time, we should do it together.

I recently got a “Notice of intent to seize (levy) your property or rights to property” from the IRS with respect to my unpaid federal taxes.

This is standard procedure.

The IRS does this soon after I don’t respond to their initial letter asking me to pay up.

They send the notice of intent to levy letter by certified mail, meaning I’m to sign for it at the time of delivery, as a way of trying to make it seem more like a big deal than their usual letters.

The letter, and an accompanying copy of Publication 594 (“The IRS Collection Process”) give some more clues about how the government may decide to enforce its new powers to refuse or to revoke passports for people with large amounts of unpaid taxes.

The impression I’d had before is that the law requires the IRS to notify the State Department once somebody’s unpaid taxes (plus penalties and interest) exceeds $50,000, and at that point the State Department may rescind that person’s passport, refuse to issue that person a passport, refuse to renew that person’s passport, or restrict that person’s passport so that it will no longer be good for anything but reentry into the United States.

But I didn’t have much to go on, and I haven’t heard of any cases of this law actually being used yet, so it’s hard to know exactly what to expect.

But here’s how the IRS puts it in Publication 594:

IRS action affecting passports

The Fixing America’s Service Transportation (FAST) Act of , enacted by Congress and signed into law on , requires the Internal Revenue Service to notify the State Department of taxpayers certified as owing a seriously delinquent tax debt.

Seriously delinquent tax debt means an unpaid, legally enforceable federal tax debt of an individual totaling more than $50,000 (including penalties and interest) for which a Notice of Federal Tax lien has been filed and all administrative remedies under IRC § 6320 have lapsed or been exhausted, or a levy has been issued.

If you are individually liable for tax debt (including penalties and interest) totaling more than $50,000 and you do not pay the amount you owe or make alternate arrangements to pay, we may notify the State Department that your tax debt is seriously delinquent.

The State department generally will not issue or renew, and may revoke, your passport after being notified of your seriously delinquent tax debt.

For additional information on passport certification visit www.irs.gov/passports.

The “Notice of intent…” letter contains similar text:

Denial or revocation of United States passport

On , as part of the Fixing America’s Service Transportation (FAST) Act, Congress enacted section 7345 of the Internal Revenue Code, which requires the Internal Revenue Service to notify the State Department of taxpayers certified as owing a seriously delinquent tax debt.

The FAST Act generally prohibits the State Department from issuing or renewing a passport to a taxpayer with seriously delinquent tax debt.

Seriously delinquent tax debt means an unpaid, legally enforceable federal tax debt of an individual totaling more than $50,000 for which, a Notice of Federal Tax lien has been filed and all administrative remedies under IRC § 6320 have lapsed or been exhausted, or a levy has been issued.

If you are individually liable for tax debt (including penalties and interest) totaling more than $50,000 and you do not pay the amount you owe or make alternate arrangements to pay, we may notify the State Department that your tax debt is seriously delinquent.

The State department generally will not issue or renew a passport to you after we make this notification.

If you currently have a passport, the State Department may revoke your passport or limit your ability to travel outside of the United States.

Additional information on passport certification is available at www.irs.gov/passports.

I took another look to see if I could find what the law requires of the State Department once it receives such a certification.

What must they do, versus what may they do.

Here’s what I found:

Authority to Deny or Revoke Passport.—

Denial.–

In general.— Except as provided under subparagraph (B), upon receiving a certification described in section 7345 of the Internal Revenue Code of 1986 from the Secretary of the Treasury, the Secretary of State shall not [emphasis mine —♇] issue a passport to any individual who has a seriously delinquent tax debt described in such section.

Emergency and humanitarian situations.— Notwithstanding subparagraph (A), the Secretary of State may issue a passport, in emergency circumstances or for humanitarian reasons, to an individual described in such subparagraph.

Revocation.–

In general.— The Secretary of State may [emphasis mine –♇] revoke a passport previously issued to any individual described in paragraph (1)(A).

Limitation for return to united states.— If the Secretary of State decides to revoke a passport under subparagraph (A), the Secretary of State, before revocation, may [emphasis mine —♇]–

limit a previously issued passport only for return travel to the United States; or

issue a limited passport that only permits return travel to the United States.

Upon receiving certification, the State Department shall deny your passport application and/or may revoke your current passport.

If your passport application is denied or your passport revoked and you are overseas, the State Department may issue you a limited validity passport good only for direct return to the United States.

I also noticed something new that showed up on my IRS Account Transcripts last month:

I’d never seen this notation before, and hadn’t noticed anything new happen on or about .

That particular 971 code isn’t listed at this voluminous list of IRS transaction codes, nor in the IRS’s own Document 6209 in which these codes are spelled out.

I dug around some on-line and found very little information, but tax agent Patti Logan was also sniffing around on the same trail, and here’s what she uncovered:

…the “Initial levy imposed” that we are finding on some of our clients’ account transcripts… is a first step in identifying which accounts meet the criteria of IRC 7345 for passport revocation, denial or limitation.

There are four criteria for individuals to have their passport sent to the Secretary of State: 1) Tax must be assessed 2) taxpayer must owe over $50,000 3) a levy has been served in the past or 4) a lien was filed on the account.

So, IRS came up with a new code, transaction code 971 with action code 640, which shows up on the transcript with “initial levy imposed.”

This just indicates an account that has had a levy served in the past.

It is being put on all individual accounts where a levy has been served no matter if the taxpayer owes $50,000 or not.

The other criteria must still be met.

So it is not telling the taxpayer that they have been reported to the Secretary of State but it is a first step.…

Another tax day has come and gone, and Ruth Benn of

NWTRCC

reflects on what motivates her to get up and out on the streets to protest

year after year: Why

Bother?

“Civil society organizations” in Beni, North Kivu, in the Democratic

Republic of the Congo, have responded to the government’s unwillingness or

inability to provide security in the area by calling on people to refuse to pay their taxes.

Yesterday I was on a panel concerning “Resisting Taxes in the Trump Era” at the National War Tax Resistance Coordinating Committee’s spring gathering.

Below is a summary of my remarks:

We can no longer reliably extrapolate from long-standing precedent about how the government operates, or how it responds to tax resisters, to anticipate the near future.

While past tax policy changes have been slow, gradual, and predictable, near-future changes are likely to be abrupt, arbitrary, and unstable.

This presents us with new challenges but also new opportunities.

I want to consider five areas the war tax resistance movement in the U.S. should be aware of, observant about, and prepared for.

But it’s too early to draw strong conclusions about any of them:

Changes at the IRS

The possible end of the federal income tax

Expanded government information-sharing

Anti-Trumpery tax resistance

How to resist tariffs

Changes at the IRS

First: the IRS is being significantly degraded and is in disarray.

There have been four acting IRS commissioners already in the first four months of the Trump Administration, serving between four days and six-and-a-half weeks each.

There is no Senate-confirmed commissioner.

In addition there have been thousands of dismissals of probationary IRS employees, and many others have accepted buyout offers to retire early.

Furthermore, the recently-released presidential budget assumes a further 25–50% headcount reduction at the agency.

The enforcement & collection branches have not been spared from this slaughter.

The agency was already on-the-ropes before all this happened.

For years they have lost headcount and their budget has dwindled, even as their responsibilities and the number of taxpayers has increased.

There was briefly some hiring and a budget boost at the agency during Biden’s term, but that hardly had begun to take effect before Trump’s crew came in and eviscerated it.

As a result, we can predict that the already feeble agency will be further incapacitated.

Second: there has been a collapse of the post-Nixon consensus that put a firewall between IRS enforcement and political appointees.

For the last 50 years it would have been considered a serious taboo for the president or one of his political appointees to try to go to the IRS and say “you should audit so-and-so; I think they’re up to something (or: I don’t like them).”

IRS enforcement decisions were firmly in the hands of career IRS employees, not political appointees.

Trump is putting an end to that.

He’s put a political appointee in charge of the IRS Criminal Investigation Division.

He’s being aggressive in using his powers to punish political enemies or to shake down deep-pocketed victims.

We can expect that he will use the IRS in this way, too.

Will this affect American war tax resisters?

Probably not right away.

I don’t think we’re on Trump’s enemies radar, and we’re not attractive shakedown targets.

But if tax resistance becomes a more prominent part of the anti-Trumpery movement, then, yes: expect politically-motivated reprisals.

The possible end of the federal income tax

Trump has repeatedly claimed that he plans to replace the IRS with an “External” Revenue Service, and replace income taxes with tariffs.

Of course, Trump claims a lot of things, and that’s never been a good reason to take those claims seriously.

But there are some other lines of evidence that suggest this may be for real.

Trump’s nominee for IRS Commissioner, Billy Long, when he was in Congress, co-sponsored legislation to abolish the IRS and replace the federal income tax with a sales tax.

This idea of replacing income taxes with consumption taxes has been floating around conservative circles for decades, but hasn’t had enough traction to go anywhere yet.

The “serious people” mostly ignore these proposals as being too onerous to accomplish and too likely to go very badly, but Trump shows strong signs of being willing to do very disruptive things and to not care much if they’ll go badly, so I think we have to consider the possibility.

This is not something Trump could do directly by fiat.

Congress would have to act to eliminate the federal income tax or the Internal Revenue Service.

But potentially Trump could force their hand by 1) unilaterally enacting tariffs, as he can do and has done, and 2) making the IRS so dysfunctional that it can no longer effectively collect income taxes, as he seems to be doing.

At that point, Congress might be faced with a fait accompli and might believe that if it wants to continue to have a budget to spend, it must allow Trump to raise tariffs (or other consumption taxes) to make up for what the IRS is unable to collect.

This is probably not happening right away.

The current Trump budget and tax proposals are for income tax cuts and for cuts to the IRS but not elimination of either.

Where would this leave war tax resisters, who tend to concentrate on the federal income tax as the most important source of war funding?

We would have to retool to resist these new taxes in new ways. (More on this below.)

Expanded information-sharing among federal agencies

A variety of legal firewalls, bureaucratic hurdles, and incompatibilities have prevented federal government agencies from sharing information with each other.

Some of that fell away during the consolidation of the Department of Homeland Security after 9/11.

Now many of the remaining firewalls seem to be dropping to DOGE.

Most news I’ve seen about this is in the immigrant-crackdown context.

For example, the IRS is sharing info from people’s tax returns, and the postal service is sharing information about people’s mailing addresses, to help ICE find immigrants to deport.

Potentially this could make it easier for the IRS to find assets or previously shadowy income.

There’s no sign that this is happening yet, and it would be yet another task for a gutted IRS to try to tackle, so maybe it’s unlikely, but it’s worth keeping on the radar, and we should raise the alarm if anyone notices anything.

Anti-Trumpery tax resistance and war tax resistance

There’s a lot of eagerness among anti-Trumpery activists for some strong, collective action, which could include tax resistance (see for example the National Tax Strike under the Choose Democracy umbrella).

Where does the war tax resistance movement fit in?

Anti-Trumpery tax resistance isn’t “war” tax resistance.

Sure, you can stretch “war” metaphorically to cover deportations, civil liberties collapse, evasion of due process, Constitutional crisis, willful malgovernance, fascism, white supremacy, and so forth, but it’s awkward.

Most of NWTRCC’s outreach and educational material assumes that war and militarism are the focal concern of tax resisters, and to these new resisters this has the potential to be alienating at worst or confusing at best.

Of course, if Trump invades Greenland or Canada or something, then the anti-Trumpery movement will probably develop a strong anti-war focus, and then war tax resistance rhetoric will fit right in.

I suppose we can’t rule that out.

It’s an encouraging sign that the War Tax Resisters Penalty Fund mutual aid program now explicitly welcomes anti-Trumpery tax resisters as well as traditional war tax resisters.

Maybe we can learn from the process they went through as they decided to become more accommodating to a new set of resisters.

Correction: the WTRPF board has since released a statement that says they are not going to extend the fund to cover tax resisters who are not resisting from anti-war motives.

I had based what I said here on a statement from a member of the WTRPF board who apparently misstated the position of the organization.

How to resist tariffs

Trump would seemingly prefer that tariffs permanently make up a predominate portion of federal government income (and therefore military budget income), as they did in the 19th century.

How could war tax resisters continue to resist if this were to come to pass?

Tariffs are taxes that apply to imported goods and that are paid by the U.S. importer.

So you can resist to some extent simply by not importing anything so that you personally do not pay the tax.

But the typical American is going to be paying tariffs indirectly as a consumer of goods whose prices include the costs of tariffs to the importer or manufacturer.

Note that tariffs apply not only to consumer-ready goods (like imported cars) but also to imported raw materials and intermediate manufacturing goods.

For this reason, the prices of many “domestic” products will embed tariffs just as much as do imported ones.

A tax resistance strategy of consuming only “Made in the U.S.A.” domestic goods will not be effective.

Some tactics that might be worth considering if tariffs make up a large amount of military income include:

Smuggling: if tariffs are high, smuggling will become highly profitable and will certainly emerge. We can help nourish that and can redirect our own consumption to smuggled goods.

Domestic manufacture: try to produce and market goods that deliberately and carefully avoid tariffs. Spread awareness about tariff-free goods.

Promote avoidance strategies: there will certainly be loopholes that can be exploited to reduce or eliminate tariffs; we can help importers learn about and use them.

Disrupt the tariff-collection bureaucracy: anything we can do to make the tax collectors’ work more difficult and less efficient will give the Pentagon less to play with.

These tactics (or similar ones) apply also to other consumption taxes that might be in the cards (e.g. a sales tax or use tax).