Philadelphia — The monthly Quaker magazine

Friends Journal has agreed to pay $31,343 as a

settlement with the Internal Revenue Service for the war tax resistance by

its editor, Vinton Dening. That covers five years of taxes

(), $19,623, plus interest.

The IRS

had placed a levy on Dening’s salary, which the magazine’s board of managers

refused to pay. But the board finally agreed to the settlement when counsel

advised that it could not win a court case.

The board supports a bill before Congress that would provide a way for

individuals to direct their tax money to peaceful purposes.

Actually, it was Vinton Deming, with an “m”. He retired from his post

at Friends Journal in

. In he

explained his introduction to war tax resistance in this way:

When I attended Philadelphia Yearly Meeting in the late 1960s I had no way of

knowing that my life would be changed as a result.… [T]he meeting was

wrestling with the question of draft resistance and was trying to prepare an

appropriate minute in support of young Friends faced with the draft. During

a difficult moment in this process a young Friend stood and spoke with deep

emotion; and his words went straight to my heart. It didn’t matter, he said,

what older Friends might say in his support of him and his generation

(through support was needed and appreciated, for sure); what really

mattered to him was that Friends look personally at their own lives to see

how they were connected to warmaking. If they were too old to be drafted (and

most of us were) perhaps they could find other ways to resist the war.

In addition to refusing to withhold taxes from the salaries of tax resisting

employees (see The Picket

Line for ),

employers can also express their solidarity for such resisters by refusing to

comply with salary levies. Here are some examples:

The War Resisters League has a policy of not honoring

IRS

levies against their employees’ salaries. According to

NWTRCC’s guide to organizational war tax resistance, “though the

IRS

continues from time to time to send levies for other employees, they have

not been enforced, and there has been little interaction between the

IRS

and WRL

in recent years.”

Also according to

NWTRCC’s guide,

the National Campaign for a Peace Tax Fund and the Friends Committee on

National Legislation have either resisted levies or established policies

to resist levies should they occur.

The “Fifth Avenue Peace Parade Committee,” which helped fuel the

anti-Vietnam War movement, refused to turn over to the

IRS

the paychecks of Eric Weinberger, a war tax resisting employee.

The Philadelphia Yearly Meeting (of Quakers) has a strong and

well-thought-through policy on how to respond to

IRS

levies of the salaries of resisting employees. Excerpt:

If the conscientious, war-tax-resisting employee requests, in the event that

IRS

serves a levy on Yearly Meeting against the salary, wages or other employee

property alleged to be in the Meeting’s possession, Yearly Meeting will

follow the practice approved on and decline to submit to the levy. In refusing, the Meeting will

set forth its belief that military tax resistance is an appropriate

individual expression of the Friends Peace Testimony and that Yearly Meeting

is led, consistent with its most fundamental beliefs, to resist government

efforts to coerce an employee against their conscience in such historic

Friends’ testimonies.

The New York Yearly Meeting (of Quakers) in

approved a statement in which they agreed

that the meeting would refuse to honor salary levies directed at employees

who were refusing taxes for conscientious reasons.

The Baltimore Yearly Meeting of Friends has a similar policy, and responded

to one levy by telling the

IRS:

“The levy would require the Yearly Meeting to act against our employees’

testimony and witness. The Yearly Meeting is not ready to take that

step.”

The Quaker magazine Friends Journal had a policy

against paying such levies, and initially refused to pay $31,343 in taxes,

penalties, and interest, from the salary of its editor, Vinton Deming. The

magazine eventually gave in when it became clear they could not win a legal

challenge to the levy.

The Christian activist group Sojourners has

a policy of refusing to comply with government levies of the salaries of

its employees who are war tax resisters. Sojourners managing director Joe

Roos says, “To date we have been threatened with levies, with the

confiscation of our property, with arrest and prison terms and, most

recently, with the money we refused to turn over being taken out of my

personal account since the

IRS

views me as a ‘responsible person.’ Despite all these threats, the only

action they have taken is to levy our corporate account, taking the amount

they say is still due plus interest, plus penalty.”

When some American Mennonite farmers resisted the Social Security /

Medicare tax, the

IRS

tried to seize the money owed to them by the Amish-run milk cooperatives

they worked through. According to Brad Igou, who documented such resistance

for the Amish Country News, most cooperative

officials refused to comply.

When the

IRS

ordered the First & Summerfield United Methodist Church in New Haven,

Connecticut, to turn over the salary of their war tax resisting minister,

Carl Lundborg, in , the congregation

voted unanimously to refuse.

The

IRS

tried also to get war tax resisting Catholic pastor Cosmas Raimondi’s

parish to turn over his salary to them in

, but the parish council refused, saying

that “[a]lthough we personally do not feel called to war tax resistance

for ourselves, we do support the right of Father Raimondi to make that

decision according to the dictates of his own conscience before God.”

War tax resistance in the Friends Journal in

War tax resistance was a frequent topic of discussion in the pages of the

Friends Journal in ,

with an increasing emphasis on how Meetings as a body could engage in war tax

resistance, and with at least one Meeting taking the step of recommending that

all of its members begin resisting war taxes.

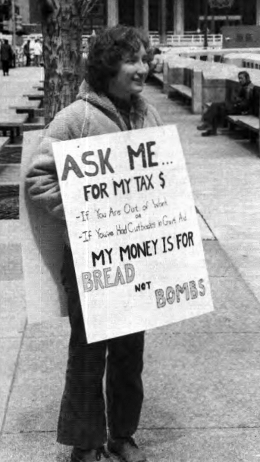

“A tax resister at a vigil in Philadelphia,

”

The issue noted that “a growing

number of Friends bodies” were organizing demonstrations against war taxes around the country:

New Call to Peacemaking approved the idea in one of its workshops in

. The idea of a Good Friday witness was

the subject of an “Epistle to All Friends in America” in

from North Carolina Yearly Meeting

(Conservative). In , Baltimore Yearly

Meeting endorsed the idea and suggested it be broadened to include members of

other churches. Friends Coordinating Committee on Peace endorsed the idea at

its annual meeting in .

The form of witness can be decided independently in each local area.

Participants might gather together for worship followed by public witness.

This could include an offering of letters from individuals, an appeal for

support of the World Peace Tax Fund bill, a vigil at the local

IRS

office, collection of withheld funds from tax refusers to be presented to a

local organization,

etc.

Also:

An effort is underway to collect signatures and funds for an ad in several

newspapers and magazines opposing the payment of military taxes. For a copy

of the proposed ad send SASE to Don Groersma…

A later issue reproduced this “Epistle to All Friends in America” from the

North Carolina Yearly Meeting:

Dear Friends:

Recognizing the potential effectiveness of simultaneous corporate action in

speaking truth to power, North Carolina Conservative Friends urge all Friends

everywhere to join with members of the several yearly meetings, and of the

Mennonites and the Church of the Brethren — persons who, together with

Friends comprise the historic peace churches — in making a witness to

Internal Revenue Service on .

It is urged that all Friends everywhere who are called upon to remit income

taxes to the U.S.

Government, and who are prepared to file an income tax return, do so on that

date and incorporate with their tax returns any one of several forms of

protest. Some examples of such protest include, but are not limited to, the

following:

Enclosing a letter stating Friends’ beliefs about the making of war, and

expressing concern that a large proportion of one’s taxes will be so used

as to violate those beliefs.

Withholding a small, symbolic amount of money deemed by Internal Revenue

Service to be owed as a tax payment, as a gesture of protest of the

war-making portion of our national budget.

Withholding that proportion of the taxes one is called upon to pay which

would otherwise go toward the making of war and war preparations.

Making a public witness, singly or together with others, giving

expression in deed as well as word that Friends stand prepared as a body

of Bible-believing Christians to still take seriously our call to

peacemaking in our increasingly troubled and militarized world.

We commend this epistle to you in the name of our Saviour, who continues to

set before us his standard, and who calls us to be faithful even unto death,

as he was faithful even unto death upon the cross.

Yet more impressively, on , the

Minneapolis and Twin Cities Meetings approved a minute that asked “all members

of our meetings to practice some form of war tax resistance”! That minute was

excerpted in the issue:

…We are called to nonviolent protest in response to preparations for war. We

recognize lovingly that individuals must conscientiously weigh their own

commitment to these traditions in the light of their own personal situations

and obligations. Yet we are asking all members of our meetings to practice

some form of war tax resistance:

To withhold all or a portion of our federal income taxes that go to pay

for war, shifting these resources from preparation for war to the meeting

of human needs;

To aid and support others who refuse to pay war taxes for conscience

sake;

To make every effort to reduce our federal tax liability through

contributions to peace-oriented and life-affirming endeavors;

To reduce our affluence through less than full-time occupations or by

other means to diminish income to or below the level of tax liability,

releasing thereby also time and energy to devote to endeavors related to

domestic and international justice and peace, living simply so that

others in the world may simply live;

To support and seek passage in Congress of the legislation which would

establish the alternative World Peace Tax Fund for receipt of funds from

citizens who cannot in conscience aid in the preparations for modern

warfare; and

To include letters of protest with our income tax statements as well as

to inform the president and our senators and representatives that we can

no longer in conscience share complicity for the current preparations for

war.

Our government and others seem prepared to bring catastrophe to humanity and

nature through the use of devastating weaponry. We recognize that those who

for religious reasons refuse to pay taxes for war are committing acts of

civil disobedience. We, members of the Twin Cities and Minneapolis Friends

Meetings, affirm civil disobedience through war tax resistance to be one

appropriate witness to our religious precepts and to be an expression of deep

concern for our country’s future.

We ask all citizens of other faiths to consider carefully these conclusions

to which we have come and to act in the light of their own consciences.

an ad from the issue of

Friends Journal

David Zarembka, identified as the treasurer of the recently-formed National

War Tax Resistance Coordinating Committee, had an article in the

about the American cultural norm

in favor of violence and the lack of strong taboos against homicide in our

culture. He concluded:

Like the prophets of the Old Testament, we must realize that our whole world

view, the whole intent of our society, is based on a divine misordering of

our lives and society. We must stop. Each individual must stop joining the

military, must stop working for the military in any fashion, must stop owning

stock in corporations that profit from military contracts, and must stop

paying military taxes.

a Friends General Conference ad in the issue of Friends Journal promoted

interest-free loans to the Conference as a way to to keep assets secure

without gaining taxable interest income

One of three “burning concerns” addressed in Saturday sessions at the

Philadelphia Yearly Meeting in

was “The Draft and War Tax Concerns: Toward a Corporate Testimony” — but a

report on the sessions in the issue

noted that “unity could not be achieved” on that point.

The General Board of Friends United Meeting endorsed the World Peace Tax Fund

legislation, according to a note in the issue. The Meeting “calls upon its members to take action in

support of the bill before Congress… The World Peace Tax Fund,

FUM notes,

would provide a legal way for individuals to redirect their taxes ‘to

nonmilitary, peaceful purposes.’ ”

That issue also mentioned that Rahway and Plainfield (New Jersey) Monthly

Meeting had sent out a war tax resistance information packet to all the

monthly meetings in the New York Yearly Meeting.

“Bill Strong, member of the War Tax Concerns Support Committee of

Philadelphia Yearly Meeting, donates war tax resisters’ money to

St. John’s Hospice of Men,

.”

War tax resistance came up at the London (England) Yearly Meeting in

, and some delegates from

Philadelphia noted that the debate seemed very similar to the one Philadelphia

Friends were having. Norma Jacob wrote:

One major preoccupation this year, both in Philadelphia and in London, is the

withholding of taxes. In both places serious reservations were expressed

about the wisdom or the expediency of this particular form of protest against

war, and the arguments are the same. There are, perhaps, some differences in

the law, which may alter the degree to which the employer, in this case

London Yearly Meeting, is to be held civilly responsible. But there was no

reluctance to give support to the Friends House staff members who object to

supporting the military through taxes, even among those who might find

themselves in serious legal trouble as a result of a stand of which they

personally might not approve.

The issue noted that Lorraine

Cleveland had redirected $400 of her taxes to her Meeting so that it could

purchase a copy of the film The Hundredth Monkey

which she hoped could be used to demonstrate that “we have the creativity and

power to change both ourselves and this world.”

At the Lake Erie Yearly Meeting in ,

among the minutes they approved was one “encouraging monthly meetings to

establish meetings for sufferings to aid war tax resisters.” The North Pacific

Yearly Meeting met at

and also took up the issue, though the description given in the

Journal is vague about what they actually decided to

do about it:

During sessions set aside for seasoned concerns, a minute on war tax

resistance was presented by University Friends Meeting

(Wash.). The minute was

introduced and accepted in the context of Friends tradition and the need for

a supportive statement as expressed by the many tax resisters in attendance.

When Friends Journal editor-manager Olcutt Sanders

died in , Vinton Deming took his place.

Deming was a war tax resister, and would later try to get the

Journal to support his resistance by not cooperating

with the

IRS’s

attempts to tax his salary.

The Pacific Yearly Meeting met in

and, among other things, “established a peace tax fund.” The Ohio Valley

Yearly Meeting met

and “approved minutes in support of the World Peace Tax Fund and of

conscientious war resisters.”

The issue included this note:

A War Tax Resistance Minute by Davis

(Calif.) Meeting states,

in part, “We, the members of Davis Friends Meeting, affirm civil disobedience

through war tax resistance to be one appropriate witness to our religious

precepts and to be an expression of deep concern for our country’s future… We

are asking all members of our meeting to practice at least one of the

following forms of tax resistance”: to aid and support others who refuse to

pay war taxes for conscience’s sake; to support the World Peace Tax Fund

legislation; to include letters of protest with our income tax returns as

well as to inform our legislators that we can no longer share complicity in

the current preparations for war; to reduce our affluence and diminish our

income to or below the level of tax liability by living simply; to contribute

to peace-oriented or life-affirming endeavors; and to withhold a portion of

our federal income taxes that go to pay for war, shifting these resources

from preparations for war to the meeting of human needs.

That issue also reprinted a minute from the Washington,

D.C.

Friends Meeting concerning the phone tax:

The U.S. excise

tax on telephones has always been associated with war. Throughout the period

of American military involvement in Indochina, congressional proponents of

this tax said that it was needed to pay for the costs of war.

After the withdrawal of American troops from Indochina, the excise was to be

eliminated. Over the years it was steadily decreased from ten percent to one

percent. In this tax was increased to three

percent.

Friends have a long-standing testimony against participation in war and

preparations for war. At present, the Congress has ignored the popular

mandate for a freeze on the deployment and testing of nuclear weapons, and

has continued to appropriate funds for new weapons systems. Our president has

ignored public opinion polls which show that the majority of people oppose

U.S. military

intervention in Central America, and has proceeded with plans to commit

U.S. forces in

that region. Registration for the draft has been reinstituted.

We strongly urge Friends to consider whether it is appropriate to continue

payment of this war tax on telephones.

In the same issue, Tim Deniger had a letter-to-the-editor about the World

Peace Tax Fund legislation. Although he acknowledged that the proposed law

“does not address the problem of spending for defense versus social welfare;

it is simply a bookkeeping proposition which would ease the consciences of

pacifists” he had written a letter to a senator (Alfonse D’Amato of New York)

to urge him to support it. D’Amato wrote back to explain why he wouldn’t be,

saying in part:

[W]ithholding of tax dollars from the Department of Defense would simply be

an accounting illusion. Total defense spending would not decline. A larger

proportion of the tax dollars of other Americans would merely be used for

military programs. Most likely, it is the non-defense programs which would

end up being underfunded. Thus, despite its lofty intentions, the burden of

S. 880 would fall

most heavily upon the needy receiving benefits from a multiple of federal

social programs.

At the meeting of the Friends

World Committee for Consultation, Section of the Americas, “[r]epresentatives

approved a document outlining the implementation of a War Tax Resistance

Minute that the annual meeting approved [see

♇ 30 July 2013]. Positive responses and

cautionary notes from yearly meetings were considered when the war tax

subcommittee established policy for this FWCC corporate witness.”

The issue had a note about

Quaker Mark Judkins’s war tax protest:

…Mark brought $300 worth of food to the

IRS

center to pay for $78 worth of taxes. The food was not accepted as legal

tender. Police officers prevented the protesters from bringing the food into

the office. Mark announced that he would donate the food to the Milwaukee

Hunger Task Force’s food bank.

And the same issue noted:

War tax resisters in Ann Arbor,

Mich., are planning to run

ads in local and national newspapers and magazines listing the names and

addresses of signers of a statement setting forth their reasons for living in

volunteer poverty (below taxable income level) or refusing to pay some or all

income taxes or the federal excise tax on phones. Friends wishing to become

part of this project should write to War Tax Resistance National Ad Campaign…

War tax resistance in the Friends Journal in

1984 brought the Friends Journal’s second special issue on war taxes, at a time when even its critics acknowledged war tax resistance as a mainstream practice in the Society of Friends.

In a letter-to-the-editor in a issue of the Journal, Tim Deniger, a supporter of the World Peace Tax Fund legislation, had pointed out some of its flaws, for instance that it “does not address the problem of spending for defense versus social welfare; it is simply a bookkeeping proposition which would ease the consciences of pacifists.”

(See ♇ .)

Bill Strong wrote back, and, in a letter that appeared in the issue, defended the bill against its critics.

Excerpts:

[T]he World Peace Tax Fund Bill…[’]s enactment won’t lessen defense spending; Congress will still need to do that.

What it will do is establish a Peace Trust Fund (like the eminently successful highway trust fund), enabling our society to make a striking (i.e., dollar-worthy) commitment to seeking peace (via, for example, funding a peace academy, U.N. peacekeeping forces, the use of mediation, negotiation, and reconciliation techniques — none of which are currently part of U.S. commitments).

As to alternative service for war tax dollars being but an “accounting illusion” or only easing the consciences of pacifists, the same applies to the now-established alternative service of C.O.s. Although men choose alternative service, our government has never lacked the bodies to pursue any conflict any place, any time; but the C.O.’s personal witness still stands for what it is, a man’s conscientious decision not to be a part of the war system.

If we could have C.O. status for men over 20 and all women, allowing them not to pay for war but to have their tax dollars go toward peacemaking, our society would make a new and totally different kind of statement to this violence-weary world.

There’s a little bit of sleight-of-hand here in comparing people who would pay their taxes into a government-run alternative fund with only those conscientious objectors who would be willing to enter government-run “alternative service” in lieu of combat roles (as opposed to the many conscientious objectors who refused to be conscripted into any service whatsoever).

But it’s also important to note that these earlier versions of the “peace tax” scheme were much more conscientious about segregating the “peace tax” payments so that they would pay for new, additional, nonviolent, peace-seeking measures.

This enabled promoters to make a much stronger case in favor of the bill than today’s poor “Religious Freedom Peace Tax Fund” promoters — who have to somehow defend the idea that “peace tax” payers’ dollars will somehow magically get routed just toward the non-military portions of the government’s usual budget.

the cover of the issue of Friends Jounal

The issue of Friends Journal was dedicated to “Our Taxes and Peace” — the second such issue devoted to the war tax issue that I found in the archives.

Vinton Deming, a war tax resister and now the Editor-Manager of the Journal, introduced the issue.

Excerpts:

[W]hat can we do, many of us are asking, to stop the flow of our tax money to the Pentagon?

It feels as if the Society of Friends has come more under the weight of this concern in the past year.

My yearly meeting (Philadelphia) wrestled with the question of tax resistance a year ago, and monthly meetings have been asked to consider the question further as they prepare for yearly meeting sessions this month.

Within my own monthly meeting I have attended clearness meetings this year for members seeking direction and support on the issue.

And I have seen a marked increase in the number of members taking tentative steps to withhold at least a portion of their taxes.

Reports from abroad include London Yearly Meeting’s minute of support this past summer for its employees who seek to hold back the military portion of their taxes.

Robert F. Tatman proposed a Minute on the subject, confidently presenting a target that was well in front of what any meeting had been prepared to accept thus far.

Excerpts:

[W]e are led to declare for ourselves that all participation in war and preparation for war — in any form — is contrary to the Spirit and teachings of Christ.

By this, we mean that membership in the armed forces of the United States or of any country, whether under arms or as a noncombatant; participation in, including registration under, a system of military conscription; acceptance of the privilege of alternative service as a conscientious objector; payment through taxes, both direct and indirect, for wars past, present, and future; and all other forms of participation in the war system, which now holds the world in such deep oppression, are in direct opposition to the Peace Testimony of the Religious Society of Friends.

Friends are advised to examine themselves, their finances, their possessions, and all of their associations to discover whether they are clear of such participation in war and preparation for war, and if they are not, to seek guidance and support from their monthly meetings in their efforts to attain clearness.

We accept that this search for clearness will inevitably bring us, both individually and corporately, into conflict with the laws of the United States and of other countries, and we pledge our full moral, spiritual, and financial support to any Friend or meeting in need of such support as a result of this minute.

We realize that there are many Friends who will not be in full unity with this minute at present, who will feel it is their duty as U.S. citizens to continue paying the taxes demanded of them by the federal government, and to support and counsel cooperation with military conscription.

We recognize the depth of their convictions but stand in loving disagreement with them, and we pledge them, too, our full moral, spiritual, and financial support as they struggle to reach clearness on this concern laid upon us by the Lord.

We are indeed loyal citizens of the United States, but first we are citizens of the Kingdom of God, and the higher law must always take precedence over the lower.

Kingdon W. Swayne went the opposite direction, feeling that Friends had gotten too carried away with war tax resistance and ought to reconsider.

Excerpts:

Most of the current discussion of “war” taxes within the Society of Friends is based on the implicit assumption that those who don’t pay them are morally superior to those who do.

The charge of the Philadelphia Yearly Meeting to that of is to come up with a “stronger minute” on war tax concerns than the one currently on the books, clearly implying that greater “strength” in this area must be morally superior.

In a discussion several months ago at Representative Meeting in Philadelphia, those who obey the law were compared to the Quaker slaveholders of , and not a dissenting voice was raised.

As a member of the substantial majority of Friends who are dutiful taxpayers, I have felt intuitively that my position has every bit as good a moral claim as the contrary view.

I have sought to examine that intuition in two ways: first, to identify the moral assumptions that underlie it and, second, to identify the moral ambiguities in the tax refuser position that render it unattractive to me on moral grounds.

Swayne argued:

It is important to him to be a vigorous participant in the various “circles of community” that he finds himself in, and only to be a disruptive force in those circles in the most extreme circumstances, when productive participation is no longer possible.

He feels that the national circle in the United States has not reached such a stage, and so it’s better to play by the rules.

Friends overemphasize “the dramatic, large-scale evils associated with the national security system” while remaining indifferent to other man-made sources of suffering, for instance “our transportation system [which] has brought more death and injury to U.S. citizens than all the wars of .”

The national security establishment is just a large-scale version of such thoroughly moral defenses as “police forces and locks on houses” — they are not evil in and of themselves, though they can be used in evil ways or can become aggrandized in an evil way.

But war tax resistance treats them as pure evil.

He then described the varieties of resister: the one who reduces his or her income below the tax line (the “most admirable” variety, according to Swayne), the one who tries “limiting but not eliminating federal income tax liability, and paying the required tax” (Swayne considers himself one of these, saying he “does so from prudential rather than pacifist motives” because “I think I give money away more wisely than does Uncle Sam”), and the one who refuses a symbolic “military” percentage of the federal income tax (this, he calls the “mainstream” variety).

He sees problems with this third variety:

It actually means the government gets more money in the end.

The calculation of the “military” percentage is flawed.

“It requires one to assert unequivocally that one’s own reading of the will of God is superior to that of others, not only with respect to goals but with respect to the tactics needed to achieve those goals.”

By filing legal cases contesting government actions against resisters, these resisters undermine their moral position, becoming not civilly disobedient martyrs but mere plaintiffs.

Such war tax resisters incorrectly deny that their position sets a precedent for tax resisters of all sorts.

Law-breaking reflects poorly on the peace movement in the court of public opinion.

But, he concluded:

As for the tax refusers, I hope other Quaker taxpayers will join me in accepting their position, despite its ambiguities, as being in the mainstream of Quaker thought, and therefore entitled to support from Quaker bodies.

I will support them not out of a sense that theirs is the morally superior position, but only because they are taking a greater risk.

Following that, Franklin Zahn promoted phone tax resistance as “a simple way of continuing Friends’ tradition of witnessing for peace.”

He first wrote about why resistance was important (indeed, he felt, as a regressive tax at a time of reduced social welfare spending and tax cuts for the rich, resisting this particular tax could be justified even without reference to military spending), and then explained the mechanics of how to resist and how the phone company is likely to respond.

No one has ever been jailed for refusing the telephone war tax.

Although the tax is small, its refusal by thousands of Friends could be a significant force for peace.

Gandhi, for instance, made good use of a very small salt tax.

Being “effective,” however, need not be the main motive in refusals.

A draft-aged person refuses induction not primarily to be effective but because it is immoral to support war.

The same motivation can apply for tax refusers.

There was also a brief note in that issue about a new “study document” from the National Council of the Churches of Christ on “The Churches and War Tax Resistance,” but it didn’t give much indication about the content or the context in which it had been produced.

The issue brought the news that a group of “peace tax fund” promoters in Canada had incorporated and were planning to pursue a test case in the courts that they hoped would establish a right to conscientious objection to military taxation under the new Canadian Constitution.

Kingdon Swayne’s challenge to what he identified as the orthodox Quaker position in favor of war tax resistance drew some responses that were printed in the issue.

Roland Smith, “a rather recent tax refuser,” thought Swayne’s criticism was “helpful” but not always correct.

In particular, he didn’t think that it was true that war tax resistance always would mean the government would come out ahead in the end, and he felt that the difficult (Swayne called it “arbitrary”) practice of trying to discern the military portion of your tax bill represented “not a drawback but… an opportunity for the refuser to exercise his or her conscience in deciding which percentage of which budget figure to use.”

More troubling, he thought, was the threat to democracy embodied in the idea that people could conscientiously choose to support some decisions of their elected representatives and not others.

Irving Hollingshead denied that “self-righteousness” was behind war tax resistance.

“The moral point is that war and the preparation for mass killing are wrong, and most Friends feel a moral obligation to oppose it.

Tax resistance is merely one tactic consistent with this moral position.”

Tor J.S. Bejnar looked at Swayne’s three varieties of resister and decided that the second variety, to which Swayne (and until recently, Bejnar) belonged, “barely connects spiritual and earthly matters” and so he has decided to move into the first category, which he termed “deliberate poverty.”

Alan Eccleston was glad to see that Friends were “open[ing] ourselves to the question” rather than evading it.

He felt that framing the issue as being about “moral superiority” was counter-productive and judgmental.

And he also felt that more important than strong Minutes from Meetings about war tax resistance was “the continuous witness of those who, under a concern, constantly hold the question before us through their own loving commitment.”

My personal experience suggests that we feel most anxious when we are in a stage of determined avoidance, when, intuitively, we sense something stirring within us for which we believe we are not ready.

All of our defenses are mobilized and we shut ourselves off from that inner stirring — but at a price!

Scott Crom questioned the consequentialism implicit in Swayne’s critique.

“[S]ometimes we are called upon to act in certain ways, or refrain from acting, regardless of the consequences.

Here one does not judge the morality of a choice by its results or its impact, but by something else.

This approach is the one I prefer, and I believe it has ample precedent, both in the Bible and in Quaker history.

The Ten Commandments and the Sermon on the Mount do not say, ‘Thou shalt accomplish such-and-such,’ but speak directly to actions and to attitudes.”

Ben Norris wrote that “Some Quakers are motivated especially towards striving to keep their own lives pure, simple, or consistent, and this inner spiritual state is the focus.

Others note that it is quite impossible to exist outside of some sort of economic and social system… and therefore, such an action as war tax refusal is part of a vastly complex involvement in responsible citizenship, the right ordering of our economic and social systems. Both motivations may exist in the same person.

But to concentrate on which person’s actions, public or private, are ‘more moral’ than someone else’s usurps a judgment not given to mortals, and trivializes both the spiritual and political motivations of rational change in our lives.”

Karl Meyer wrote in to promote his “cabbage patch” method of tax resistance:

the Internal Revenue Service began using a special $500 penalty against people who make protest claims on income tax returns.

This “frivolous tax return” penalty is a significant and intolerable assault on the inalienable rights of freedom of speech and religion.

It seems to me both a challenge and an opportunity for mass civil disobedience by people of conscience.

The only act needed is to assert the rights of conscience on an income tax form.

As an experiment in showing the way, I have begun to file daily protest returns for each day of .

My net income from my work as a carpenter in will be reported and distributed on 365 tax returns, at an average of about $38 per day.

Each return will be addressed to a different employee or office of IRS.

A copy of the daily return will be sent each day to a different newspaper, magazine, public officeholder, or peace organization.

If the IRS imposes penalties for all of my returns, the total assessment may rise to more than $180,000. I have already received notice of one penalty for $500. Of course I don’t intend to pay or allow collection.

I invite Friends to join with me in resisting war taxes and this penalty on the expression of conscience.

This is a good project for people like me, who feel able to protect their income and assets from seizure by IRS.

Some others, whose assets are more vulnerable to collection, may participate by filing protest statements on tax return forms, in the names of some of the victims of U.S. militarism worldwide.

G.M. Smith trotted out the argument that paying taxes is no more of a moral issue because of how the government will spend the money, than handing your wallet over to a violent mugger is because of how he might spend the loot.

He suggested instead of tax resistance that people donate (in a tax-deductible way) to charity.

“Thus, through contributions one could reduce his or her tax liability legally and at the same time be contributing to good in the world.

It is important, however, not to make one’s contributions in a tax-supported area.

There’s nothing government would like better than to dump the entire burden of social services on the private sector and have all those extra tax dollars for bombs.”

Robert R. Schutz questions Swayne’s casual assumption that because the national security apparatus is something like the local police apparatus writ large (and the police are something like the locks on our doors anthropomorphized and handed pistols) that there’s nothing inherently wrong with a military.

Schutz agrees with the theory but denies Swayne’s conclusion.

Rather: “The use of police power may be even less morally defensible than war because it is deliberate, pre-planned, cold-blooded, and because it is entirely mercenary — we hire other people to do our killing for us.”

A report on the annual Philadelphia Yearly Meeting in the same issue noted that “[m]uch of Saturday was taken up with Friends’ wrestling with war tax concerns.”

The minute which finally resulted said, in part, that “Friends are uneasy in conscience that a substantial portion of their tax dollars goes for military purposes”; that we “are ready to support a wide variety of approaches to war tax witness in accord with individual circumstances and leadings”; that “while Friends do not urge one another to undertake civil disobedience, Friends are ready to give strong support to members led to refuse payment of taxes for military purposes”; and that “most Friends strongly endorse passage of the World Peace Tax Fund legislation.”

The minute concluded, “We realize that we have no single or simple answer to the dilemma of praying for peace and paying for war.

We ask for Divine Guidance as we proceed in struggling with the issue of taxes levied for war-related purposes.”

The issue will be considered again at the sessions.

In the issue was a letter from Donna and Jerome Gorman in which they explained how they had extended tax resistance-like techniques to a State-level battle against capital punishment.

They held back a symbolic 1¢ from their electric bill to protest against the Virginia Electric and Power Company’s complicity with the state’s electrocution method of executing prisoners, and later began to also withhold 1¢ from their phone bills in a similar protest because of a state excise tax on phone service.

They saw this largely as a method of getting the attention of people to whom they could then direct anti-death-penalty outreach.

We refer to this economic and tax resistance as “penny resistance.”

Multiple innovations in economic and tax and other forms of resistance are most urgently needed to impede the various methods of carrying out capital punishment.

We pray and we hope that many others will consider joining in this resistance.

Jeff Hunn promoted the War Tax Resisters Penalty Fund in the issue.

He described it this way:

The Tax Resisters’ Penalty Fund is a sort of “mutual aid fund” for war tax resisters.

Formed in , the Penalty Fund is supported by people who contribute small amounts of money periodically to help war tax resisters pay fines and interest levied by the IRS.

Funds contributed are used to help pay not the resister’s original tax burden but what the IRS terms “statutory additions”: interest, penalties, and fines imposed because of war tax resistance.

When each supporter contributes his or her small amount, the total becomes enough to reimburse the resister for the additional cost of his or her witness.

For example, 200 supporters contributing $2.50 each could cover the aforementioned $500 “frivolous” penalty.

The Tax Resisters’ Penalty Fund has grown from 85 supporters in to 400 supporters .

The larger we grow, the bigger an impact we can make and the smaller each supporter’s contribution will need to be.

Finally, in the issue, Dan Merritt reminded people that phone tax resistance was still a good option, and noted that the Claremont, California, Friends Meeting had been refusing to pay the phone tax since the Vietnam War.

War tax resistance in the Friends Journal in

The third of Friends Journal’s special issues on war tax resistance came in , and the topic came up in several other issues besides.

An article by Mary Bye in the issue showed how the arguments for war tax resistance were starting to break the bounds of the tax arena and take hold elsewhere.

Excerpts:

In a letter from the collection department of Philadelphia Electric Company demanded payment for a backlog of refused rate hikes.

I had withheld the 13.7 percent imposed to cover the construction costs of the Salem and Limerick nuclear reactors.

Why did I take this stand?

Looking back over the years for the source of my action, I could see it springing from a long-time insistence upon justice, a small but growing willingness to risk, a perennial sense of grief for suffering, and a blossoming love of the Earth.

These are the qualities of the spirit which began to unfold into action during the early days of the Vietnam War.

Somewhere along the line, I refused to pay the war tax portion of my federal income tax.

Later the Vietnam War ground to a halt when legislation ended financial support for it.

Was it just a coincidence that our war tax resistance preceded this legislation?

Or did citizens modeling the denial of monies not only support the growing disaffection with the war, but also provide a clue to a way to end it?

We had perhaps unwittingly slipped into an old Christian strategy of living as if the Kingdom were here now, and, behold, it manifested a brave, new world, or at least the beginning of one.

War tax resistance seemed an appropriate base upon which to build a new witness of caring for the whole Earth.…

…With crystalline clarity I selected my own utility, Philadelphia Electric, and refused the rate hike for Salem and Limerick.

After 1½ years of refusal, accompanied by monthly explanations, I received a warning letter from the collection department, threatening an end of service.

The initial fright yielded to a decision to continue resisting and move as swiftly as possible to establish my independence from nuclear power forever.

I faced a new, expensive, complicated simplicity: photovoltaic cells, which produce electrical current when exposed to light, and which could free me from bondage not only to nuclear generators but also fossil fuel-fired reactors.

As war tax resistance led me to a lower income, so rate hike refusal was pointing the way to lower energy demands.

My living standard may drop, but the quality of my life soars.

Meanwhile I have discovered that Philadelphia Electric is experimenting with photovoltaics in anticipation of the coming solar age.

If the price is right, I could purchase them there.

After all, nuclear power is the enemy, not the electric company.

This is the vision, but it is a dream deferred or rather only partially realized.

Philadelphia Electric Company and Solarex, which manufactures photovoltaic cells, want to establish a demonstration project at my home that would provide between one-fourth and one-third of the daily demand here for electricity.

The stumbling block is the cost, which would possibly necessitate a 35-year pay-back period.

So I am circling the photovoltaic issue in a holding pattern like a plane above an airport.

I am searching for answers to hard questions: such as what is the equitable balance between the cost of photovoltaics and the wattage generated?

What is a reasonable payback time?

If the cost is rock bottom right now, how do we gather funds?

How do we secure state and government support?

Are churches and meetinghouses able to model this kind of caring for God’s creation?

How do we dream this dream into reality?

I would welcome your suggestions.

an ad in the issue of Friends Journal

That issue also announced a “Conference for Quaker, Mennonite, and Brethren employers, airing ways to deal with war tax resistance by employees.

Sponsored by Friends Committee on War Tax Concerns and New Call to Peacemaking.”

That conference was covered in the issue in an article by Paul Schrag.

Excerpts:

The question of how church organizations can help their employees follow their consciences — and how to deal with the risks involved for both employees and employers — were the issues that 36 Mennonites, Brethren, and Quakers struggled with at the meeting.

The church leaders, organizational representatives and lawyers affirmed their support for individual military tax resisters and for efforts to seek a legislative solution by working toward passage of the U.S. Peace Tax Fund bill in Congress.

They agreed to organize a peace church leadership group to go to Washington, D.C., to support the peace tax bill and to express concerns about tax withholding.

They also agreed to help each other by filing friend-of-the-court briefs if tax resisters are prosecuted and by sharing the cost of tax resistance penalties, if necessary.

People from churches that refuse to withhold federal taxes for employees who oppose paying military taxes shared their experiences with people from churches considering adopting such a policy.

The General Conference Mennonite Church and two Quaker groups are in the first category.

The Mennonite Church is in the second.

The meeting, held at Quaker Hill Conference Center, took place in an atmosphere of excitement generated by a gathering of people from different traditions who share a vision.

One conference participant said it was frustrating that many members of historic peace churches are unwilling to witness against financial participation in preparing for war, although they are opposed to physical participation in war.

Some said it was disappointing that so many people are unwilling to follow their consciences until the government, through the Peace Tax Fund, might allow them to do so legally.

One quoted Gandhi: “We have stooped so low that we fancy it our duty to do whatever the law requires.”

When a church or organization decides to honor employees’ requests not to withhold their federal income tax, it assumes serious risks.

Theoretically, a person in a responsible position who willfully fails to withhold an employee’s taxes can be punished with a prison sentence and a $250,000 fine.

An organization can be fined $500,000.

But such penalties have never been imposed on legitimate religious organizations, nor are they likely to be, said two lawyers at the meeting.

The usual Internal Revenue Service response to war tax resistance is to take the amount of tax owed, plus a 5 percent penalty and interest, from the employee’s bank account.

However, the IRS has not taken even this action against General Conference Mennonite Church employees who are not having their taxes withheld.

They pay the nonmilitary portion of their taxes themselves and deposit the 53 percent that would have gone to the military in a designated account.

The IRS has not touched that account after church delegates approved the policy in .

All church personnel who could be subject to penalties have agreed to accept the risk.

Friends World Committee for Consultation, which has had a nonwithholding policy , has had tax money seized, plus interest and penalties, from its resisters’ bank accounts.

Friends United Meeting adopted a non withholding policy .

Philadelphia Yearly Meeting of the Society of Friends is considering such a policy.

A representative of the Church of the Brethren said he would use input from the meeting to work toward developing a denominational policy on tax resistance.

Lobbying continues for the Peace Tax Fund bill…

The bill would allow people opposed to war taxes to put the portion normally given to the military in a separate fund for peaceful purposes.

The rest of that person’s tax money also would be designated for nonmilitary use…

Whether or not military tax resistance is effective, participants agreed that people’s moral imperative to follow their consciences must be respected.

“No conscientious objector ever stopped a conflict,” said William Strong, a Quaker representative [and treasurer of the Friends Journal Board of Directors].

“But they had to explain what they did, and the vision was kept alive, and those ripples, you don’t know where they stop.”

A postscript noted: “ ‘A Manual on Military Tax Withholding for Religious Employers,’ written by Robert Hull, Linda Coffin, Peter Goldberger, and J.E. McNeil, will be available .”

from the cover to the issue of Friends Journal

The issue was the third special issue on war taxes from the Friends Journal.

It was prompted in part by the fact that the Journal itself had received IRS levies on the salary of its editor, Vinton Deming, who had been refusing to pay income tax .

The Treasurer of the Journal, William D. Strong, explained what was going on in the lead editorial:

The Friends Journal Board of Managers has twice been unable to honor the levy against the wages of our editor, Vint Deming, for unpaid federal taxes.

In our most recent reply to the Internal Revenue Service we stated that:

It is not possible for us as a board to separate our faith and our practice: we must live out our faith.

Our earlier letter… refers to our 300-year-old Peace Testimony.

To more fully describe that part of our beliefs we enclose copies of two sections of Faith and Practice, the book of spiritual discipline of Philadelphia Yearly Meeting.

[“The Peace Testimony” and “The Individual and the State,” pp. 34–38, were shared.]

Our position of noncompliance to the requests of the Internal Revenue Service is not an easy one.

We do not question the laws of the land lightly, but do so under the weight of a genuine religious and moral concern.

We know as well that other religious groups — Mennonites, Brethren, and others — are facing this same difficult dilemma.

For this reason, many of us support the proposed Peace Tax Fund bill in Congress.

The board agreed at our meeting in to make known this continuing witness, both individual and corporate, to you, our readers.

The dilemma is clearly not the Journal’s alone.

Many Quaker institutions in the United States, Canada, and England have faced this challenge.

Beyond the historic peace churches are Catholics, Methodists, and others who are considering the whole question of taxes and militarism.

In February representatives of some 70 institutions came together at the Quaker Hill Conference Center in Richmond, Indiana, for a New Call to Peacemaking consultation on “Employers and War Taxes.”

This followed a Quaker conference at Pendle Hill considering the same concern.

The Journal board has worked at and reached unity in this matter.

We will continue to seek the light in the months and years ahead.

For now, however, we would welcome the support and reactions of our subscribers and readers.

If you’d like to share in this witness with your moral support, let us know.

If you’d like to add practical support, we would welcome it, as we are establishing a Conscience Fund.

We don’t plan extensive legal undertakings at this time, but we know that there can readily be some fees and costs ahead, as well as possible penalties resulting from our refusal to honor the levies from the IRS.

We look forward to the response of our readers. We feel that we cannot host writings in the issues of the Journal on peace and justice, on our testimonies and faith and practice, without, as an employer, living them out to the best of our God-given abilities.

Another article in the special issue was an extract from J. William Frost’s Tax Court testimony in the Deming case, in which he explained the Quaker war tax resistance practice:

The peace testimony has been a basic part of Quaker religious belief .

The testimony has not been static; it has evolved over time as Friends thought out the implications of what it meant to be a bringer of peace.

Some of the most creative actions of members of the Society of Friends have come from the peace testimony.

For example, Friends’ primary contribution to world history is that they began and carried through the antislavery testimony.

Friends became antislavery advocates in , when they realized that the only way one could obtain a black slave was to take him or her captive in war.

Pennsylvania was founded by William Penn for religious liberty.

Penn believed, and so did the early settlers, that to create a Quaker colony meant there would be no militia, no war taxes and no oaths.

These were conceived to be part of religious freedom, and in the early years of Pennsylvania, there was no militia, and there were no war taxes and no oaths.

At first, the Pennsylvania Assembly refused to levy any taxes for the direct carrying on of war.

Instead, after when the British government requested money because it was already beginning its long series of wars with France, the Crown and the Pennsylvania Assembly worked out a series of arrangements.

Those arrangements provided that the Assembly (then composed primarily of Quakers) would provide money for the king’s use or the queen’s use, but the laws also stipulated that that money would not be directly used for military purposes; i.e., there would be almost a noncombat status for Quaker money.

It could be used to provide foodstuffs to be used to feed the Indians, or it could purchase grain or relieve sufferings.

It would not be used to provide guns and gunpowder.

This policy of no direct war taxes, no militia, and no oaths, was followed in Pennsylvania .

In , a group of members of Philadelphia Yearly Meeting began the debate on whether Quakers should pay taxes in time of war.

At this time, some of the most devout Quakers refused to pay a war tax levied by the Pennsylvania Assembly.

And finally the yearly meeting agreed that those whose consciences would not allow them to pay the taxes, should not.

So the heritage of Pennsylvania was that government accommodated the religion.

The Federal Constitution allows for an affirmation, because certain religious rights are antecedent to the establishment of the government, and the government can and will accommodate itself to religious scruples of those people who are conscientious good citizens.

there was less opportunity for tax resistance because there was no direct federal taxation.

The federal government was financed by tariffs, and the tariffs were used to carry out the full operations of government.

(The major exception came during the Civil War, and here the main issues were military service and Quakers’ refusal to pay a substitution tax.)

The main Quaker response to World War Ⅰ was the creation of the American Friends Service Committee.

This organization was designed to allow those young men who did not wish to fight (conscientious objectors) to have an opportunity for constructive service (i.e., to provide relief and reconstruction in the war zone).

Friends conducted relief activities in France, and then later in Germany, Serbia, Poland, and in Russia.

The War Department accommodated itself to Friends.

There was no specific provision in the draft law in World War Ⅰ for conscientious objectors.

The War Department allowed those Friends who wished to serve in the American Friends Service Committee to be furloughed so that they could go abroad to participate in relief activities.

A second way in which the authorities accommodated Friends at that time was in relief money raised by the Red Cross for Bonds.

Much of the Red Cross effort was for military hospitals, and Friends did not wish to support that effort.

Therefore in Philadelphia an agreement was worked out whereby Friends contributed money or bonds which would be earmarked for the American Friends Service Committee or for relief activity rather than for direct war activity.

There were instances in World War Ⅱ of individual Friends refusing to pay war taxes, and the Philadelphia Yearly Meeting officially protested against certain war taxes, but the main movement against war taxes has occurred .

During the Cold War and particularly during Vietnam, war tax resistance has become a major theme in Philadelphia Yearly Meeting.

The Philadelphia Yearly Meeting, , has regularly put a discussion of war taxes on its agenda.

In many ways the Philadelphia Yearly Meeting position on war taxes is like its position was on antislavery before the Civil War: before , virtually all Friends opposed slavery.

, virtually all Friends oppose military taxation.

The difficulty in and in is that Friends are searching for a way to make their religious witness effective.

What Friends want to do is somehow change the focus of a policy which they see as destructive of what is basic to their value system.

In summary, the position of Friends is that religious freedoms preceded and are incorporated into the federal government.

Pennsylvania was founded for religious freedom, and religious freedom meant no taxes for war, no militia service, and the right of affirmation.

Friends think that the federal government incorporated part of that understanding in the affirmation clause in the constitution, in the first amendment, and in the religion clauses in the Pennsylvania Constitution.

Friends think that the government has in good faith tried to accommodate us in our position on military service, and what Friends are wanting from the government now is a like accommodation on a subject which is the same to us as conscientious objection: the paying of taxes which will be used to create weapons to threaten and to kill.

Deming represented himself next, in an article describing his “journey toward war tax resistance.”

Excerpts:

During a difficult moment [in the discussion over the Philadelpha Yearly Meeting’s response to the Vietnam War] a young Friend stood and spoke with deep emotion; and his words went straight to my heart.

It didn’t matter, he said, what older Friends might say in support of him and his generation (though support was needed and appreciated, for sure); what really mattered to him was that Friends look personally at their own lives to see how they were connected to warmaking.

If they were too old to be drafted (and most of us were) perhaps they could find other ways to resist the war.

About 20 years have gone by and I don’t even remember the name of the young Friend who spoke in meeting that day, but his words had a profound impact on me.

As a result of his ministry I decided to begin to seek ways to resist the payment of taxes for warmaking (what another Friend, Colin Bell, would term the “drafting of our tax dollars” for the military).

I should say that there was another motivating force at work on me as well.

My work for Friends in the city of Chester was bringing me into daily contact with poor and black people.

I was learning firsthand about a community — a microcosm of other urban areas across the country — that suffered the debilitating effects of chronic poverty, high unemployment, deteriorating housing, inadequate health care, and inferior public schools.

I was witnessing the insufficient funding of a so-called War on Poverty in Chester while millions of dollars and human lives were being expended in a war against other poor people in Southeast Asia.

I knew I had to do something to end my personal complicity in helping to pay for the war and to redirect these dollars to wage a more life-affirming battle against poverty and injustice here at home.

I soon discovered that it is hard to become a tax resister; there are so many basic assumptions about money and taxes that we have learned.

We are expected to do certain things in our society: when we work, we must pay taxes — this pretty much goes without question.

How else will programs get funded and bills get paid?

And those who don’t pay, well… there’s an institution called the IRS that takes care of such people and will make them pay!

There are so many good reasons for not resisting taxes.

Some of the ones I wrestled with are these:

I can’t get away with it.

IRS will eventually get the money from me anyway and I’ll just end up paying more in the end.

It won’t do any good.

The government is too powerful and they’ll not change their policies because of my symbolic act.

There are better ways to work for peace (i.e. writing letters to Congress, going to demonstrations, etc.)

There will never be a substantial number who will be tax resisters — it’s simply not realistic.

Well, there’s truth in all of these statements, but I had to start anyway.

Not to do so had simply become an even bigger problem for me.

So I began looking at the question of taxes for war and decided to start where I could, with the telephone tax.

I learned that the federal tax on my personal phone had been increased specifically to help pay for the war.

In talking with others who were refusing to pay this portion of their phone bills I learned that the risk was fairly small.

No one I knew about had gone to jail or suffered any severe penalties (beyond having some money taken from a bank account or such).

So my wife and I began to withhold these few dollars each month and include a note to the telephone company explaining our reasons.

This became an educational experience for me.

I started to get used to receiving the impersonal letters from the phone company and later from IRS, and I even came to enjoy the process of writing my own letters in response — I felt good about not paying.

In I began to feel more confident.

The IRS had not locked me up, or even taken any money from me, as I recall, so I gathered my courage and decided to take the next step — to resist paying a portion of my income taxes.

At first I included a letter with my tax form in April and tried to claim a “war tax deduction” and request a return of some of the money withheld from my salary but with no success.

The IRS computers were not impressed with my effort, and they routinely informed me that the tax code did not provide for such a claim.

So I came to a decision: it would be better to have IRS asking me for the money each year rather than my asking IRS.

So beginning in I began to seek ways to reduce the amount withheld from my regular paychecks.

Though some tax resisters at accomplished this by claiming all the world’s children as their dependents (or all the Vietnamese children), I decided to reduce the amount withheld by claiming extra allowances (which were authorized for anticipated medical expenses, etc.) and thus reduce the amount withheld.

Beginning in , when I started to work part-time at Friends Journal, and continuing until , I claimed enough allowances on my W-4 so that no money was withheld from my pay.

For several years as a single parent raising a young child, I lived very modestly, working just part-time and sharing living expenses in a communal house.

During those years I actually got money back from the government when I had paid nothing.

Since , however, after I remarried (and later had two more children) I started to owe money to IRS each year.

So each year at tax time I would write a personal letter to the president to be sent with a copy of my tax form (not completely filled out, usually just with my name and address) explaining why I could not in good conscience pay any taxes until our nation’s priorities changed from warmaking to peacemaking.

I would usually send copies of my letters as well to IRS, my representative in Congress, and friends.

Occasionally I would receive thoughtful responses, once from Congressman William Gray from my district, who is one of the sponsors of Peace Tax Fund legislation in Washington.

After a few years of this, IRS began to make some ominous threats and noises, followed by the first serious efforts to collect back taxes from me.

I should say that I redirected some of the unpaid taxes to peace organizations and poor people’s groups, some into an alternative tax fund, some into a credit union account to earn interest — and some was spent.

On two occasions — once in , again in — I went to tax court.

Each court appearance provided an opportunity to explain my witness more clearly, and to meet others in the community who were tax resisters or who wanted to be supportive.

My first day in court was in Raleigh, North Carolina, and was particularly meaningful.

About 30 of my friends went with me to lend support.

A local peace group baked apple pies and served small slices to people entering the courthouse next to a large “pie chart” that graphically showed the disproportionately small share of our federal taxes going to human services and the large piece to the military.

A local TV station interviewed me and carried a story on the evening news.

A wire service picked up on the story as well, and for several days I received phone calls from people throughout the South.

What occurred inside the courthouse was just as important.

The judge was very interested in my pacifist views:

At one point he ended the hearing and engaged in an extended discussion right in the courtroom of many of the peace issues I had raised.

It became a sort of teach-in on the subject of militarism and peaceful resistance.

Later both he and the young government attorney thanked me for what I shared and complimented me for effectively handling my own legal defense.

(I had elected not to be represented by counsel.)

Though the court eventually ruled against my arguments in the case — which did not surprise me — I feel that the whole experience of going to court was a positive one, as well as an educational experience for others.

And though I was ordered to pay the $500 or so owed in back taxes, I never did — and no further efforts were made to collect.

IRS has been more aggressive, however, in recent years.

Some funds have been seized from a bank account, an IRA was taken, and such efforts are continuing even as I write this article.

Most recently IRS has levied Friends Journal for the tax years for taxes, interest, and penalties totaling about $23,000.

I am grateful that the Journal’s board has declined to accept the levies on my salary… and that the board as a Quaker employer both corporately and as individual members supports my witness.

I don’t know what the future will bring, and frankly I try not to think about it too much.

In the past two years I have changed my approach some.

My wife and I have decided to file a joint return.

Beginning this past summer the Journal started to withhold a little money from my paychecks following my decision to complete the new W-4.

It seems appropriate just now that I devote my time to working on the earlier tax years and to finding ways to support others who are more actively resisting.

I try to stay open as well to seeking other approaches to resistance from year to year.

What are some things that I have learned from all this?

Perhaps I might share these thoughts:

Tax resistance is a very individual thing.

Each of us must find our own way and decide what works best for us.

Resist openly and joyfully, and seek opportunities to be in the company of others along the way.

When you go for an IRS audit, for instance, take some friends with you; when you go to court, make the courtroom a meeting for worship.

Don’t see IRS agents or government officials as the enemy.

Look for opportunities for friendliness, address individuals by name, be open and honest about what you intend to do.

The IRS will soon recognize that a conscientious tax refuser is different from a tax evader.

What might work one year may not the next.

Be flexible and remain open to trying different approaches.

Talking about money is hard, and it is discouraged in our society.

I remember how embarrassed the grownups in my family were when one of my children once asked at the dinner table, “How much money do you have, grandpa?”

Tax resistance helps us to remove some of these barriers, and this is good.

Sometimes our children can educate us, I should say, and provide simple insights to seemingly complex problems.

Just as I was challenged by a young Friend to consider tax resistance 20 years ago, an IRS agent was once set on his heels by my daughter.

During a lull in a long conversation about financial figures, Evelyn (only seven at the time) asked the agent, “Why do you make my daddy pay money for killing people?”

The poor man shuffled his papers, turned beet-red, cleared his throat, and ended the meeting.

There were several responses to the special issue on war tax resistance that were printed as letters-to-the-editor in the issue:

Jim Quigley wrote in to express his “admiration for the act of courage and faith represented by the war tax resisters.”

Karl E. Buff wanted to “encourage Vinton Deming to continue to resist” in the hopes that “[w]ithout easy access to huge sums of money our government would surely have to curtail its war-making propensities.”

He also put in a plug for the Tax Resisters Penalty Fund.

Eddie Boudreau suggested that someone set up a “Conscience Fund” that people could contribute to and that would help defray the legal expenses of folks like Vinton Deming.

Susan B. Chambers wrote in about her technique, which was to consult with a tax expert in order to get into the “zero tax bracket” and to contribute 30% of her income to charity.

“I am pleased not to inconvenience my friends in taking this stand,” she wrote, in what I read as something of a rebuke to those resisters, like Deming, whose resistance becomes an agenda item for their employers (though she didn’t make this explicit).

Robin Greenler wrote to support the Journal’s resistance to helping the IRS collect from Deming.

“The decisions are neither easier nor less important on corporate levels than they are on a personal level.”

Ben Richmond wrote that, for him, the question of whether a tax resister would just end up paying more in the end (with penalties and interest added to the unpaid tax) was the one he found the most difficult.

“I have never found it satisfying to think that the point of the witness was simply to satisfy my personal need for moral purity.”

But he looked into the early Quaker resistance to mandatory tithes for the establishment church and found that Quakers were willing to suffer having property seized worth several times the resisted tithes rather than pay voluntarily.

He notes also that the Quakers eventually won that battle, which is to say there are no longer government-enforced tithes that everyone must pay to an established church.

So, Richmond wrote, “I do not resist military taxes in the expectation or hope that I will succeed in keeping particular dollars from the hands of the military.

But I do expect and hope that, insofar as my resistance is in obedience to the leadings of God, it will play its small part in breaking down the legitimacy of the warmaking machinery, as the early Friends broke down the legitimacy of taxation on behalf of the state church.

I believe that in the end, Christ’s way is not only right but effective, and will prevail.

Our sufferings are small in the overall scheme of things, so I don’t wish to be melodramatic.

But, it seems to me that we cannot afford to follow Jesus for the short haul because in the short run, all that appears is the cross (which, after all is simply shorthand for suffering at the hands of a pagan empire).

Yet, it is the cross which led to the resurrection.”

In , the Friends World Committee for Consultation held their annual meeting.

They decided to retire their “Friends Committee on War Tax Concerns” and establish in its place a “Committee on Peace Concerns.”

On Brian Willson had been run over by a train while blockading the Concord, California Naval Weapons Station in protest against American wars in Central America.

A few days later, while recovering from his injuries, which included a fractured skull and the amputation of both of his lower legs, he issued a statement reasserting his continued commitment to nonviolent activism, which was reprinted in part in the issue, and which included this section:

If we want peace, we can have it, but we’re going to have to pay for it…

Our government can only continue its wars with the cooperation of our people, and that cooperation is with our taxes and with our bodies.

Our actions and expressions are what are needed, not our whispers and quiet dinner conversation.

In the issue, Jonathan Lutz gave an overview of the situation of Quakers in Scandinavia that included this parenthetical aside:

“(To my knowledge, only one Scandinavian Friend is a war-tax resister, but then, the very different political climate must be taken into account.)”

That issue also included this historical note, which it sourced to “the newsletter of Friends World Committee for Consultation, Section of the Americas”:

According to a Canadian publication, For Conscience Sake, Russia was the first nation to establish legislation exempting pacifists from paying war taxes.

“In , thirty British citizens were invited by Czar Alexander Ⅰ to establish a cotton mill in Tamerfors, which is now in Finland.

James Finlayson, the manager, submitted a petition to the Czar signed by the employees from Britain, some of whom were members of the Society of Friends.

The petition asked for freedom of conscience and religion to practice their own religion, and for exemption from military service, war, church taxes, and the taking of oaths.”

The Czar agreed to free Quaker manufacturers from taxes and support of the military.

This is the closest I’ve been able to get to a citation for this claim, and as you see, it’s third-hand and doesn’t refer to an original source.

I have seen references to Finlayson’s getting a charter from the Czar to set up his mill that included some tax incentives, but I haven’t gotten any closer to finding a clear and authoritative indication that the Czar explicitly honored the conscientious objection to military taxation of Quakers at this mill.

A note in the issue read:

John Stoner, executive secretary of Mennonite Central Committee, U.S. Peace Section, writes:

“That little Scripture passage on rendering to God and Caesar has been misused for too long, giving people an excuse for going the wrong way on important questions of ultimate loyalty.”

So John has created a lovely poster with the following words on it:

“We are war tax resisters because we have discovered some doubt as to what belongs to Caesar and what belongs to God, and have decided to give the benefit of the doubt to God.”

The posters are available for ten cents per copy (a real bargain, Friends, we can learn something from our Mennonite friends about good prices).