Tax resistance in the “Peace Churches” →

Quakers →

20th–21st century Quakers →

Lyle & Sue Snider

War tax resistance in the Friends Journal in

Quaker war tax resistance methods and theories diversified and became more developed, as can be seen from the pages of the Friends Journal of .

One thing that stood in the way of some Quakers (and some Quaker organizations)

adopting war tax resistance was a bias toward being law-abiding, and a worry

that civil disobedience might be one step too far on a slippery slope to

anarchy. In the issue, lawyer

(and Quaker) Allen S. Olmsted Ⅱ tried to remove this impediment:

Those who in sweeping terms condemn all law breaking seldom stop to inquire what the law actually is and who declares it.

Is the policeman or the draft board or the tax collector the law?

All of these have been reversed by the Courts time and again.

Is the demonstrator who defies a police ban, a draft resister who refuses to shoulder a rifle, or a citizen who refuses to pay war taxes, ipso facto a law breaker?

These citizens seek to vindicate their lawfulness, i.e. their loyalty to the Constitution, by breaking and then appealing the “law” which the lowest echelon of authority is seeking to enforce.

Perhaps the feature of the war resister’s mind which most clearly differentiates him from other law defiers is his complete loyalty to the spirit, as distinguished from the letter, of the law.

This is most evident in his reaction to the tax laws.

The spirit of the tax laws is, as some of us see it, that the government must go on and all of us should share the expense thereof according to our means.

Let us take the example of a retired school teacher, or minister whose income

is somewhat over the exemption and deductibles. His income tax is, say, $100.

He advises the tax collector that since 70 percent of the government’s income

is used to prosecute an unjust war he is refusing to pay 70 percent of his

tax and encloses his check for $30. He has defied the law and in due course

the government will clamp down on his bank account and collect the $70 plus

penalties.

Now take the example of the man with an income of $100,000, some of which is gained in selling war supplies to the government.

Does he feel that in the spirit of the law he should contribute his fair share to the support of the government from which he has profited so handsomely?

Merely to ask the question seems to most people quixotic, naive and bizarre.

Our wealthy tax avoider employs a man learned in the letter of the law to show him how he may avoid any taxes whatever.

As long as he keeps within the letter of the law he may pound his chest and say “What a smart boy am I.”

The difference between the tax refuser and the tax avoider is twofold: (1)

The first violates the letter of the law, the second does not. (2) The first

is motivated by the love of his country, his brothers, and his God; the other

by the love of himself and his money.

Those who break unjust laws because they are unjust and not for personal profit or convenience, who do so in a humble spirit of submission to the moral law and without breaking the peace, are moving not toward anarchy but away from it.

In the name of all that is holy — and I do mean holy — let us stop calling the nonviolent conscientious law resisters breeders of anarchy.

Immediately following that piece was a poem by Raymond Paavo Arvio that began “I am one with the tax refusers, / The long beards, the jail birds / … / The pacifists / The anarchists”.

And immediately after that was an article by Mary Timberlake that considered

Quaker meetings and Quaker action to be the necessary one-two punch of Quaker

practice:

I learn that 60 percent of all income taxes go to the military.

I must refuse to pay that when my income becomes taxable.

Ten percent of the phone bill is a federal excise tax, an appropriation approved by Congress in solely to provide additional funds for our operation in Vietnam (so reads the Congressional Record).

I have a telephone.

My meeting has a telephone.

Dear Friends, the dollars the government collects from us in this way fall as napalm in Vietnam.

I must refuse to pay all war taxes, urge you to refuse, take my personal funds out of banks so the government cannot get the money by placing a lien on my account; support instead an alternative fund — to send medical aid to North and South Vietnam, to rechannel this money into my own community where it is needed so desperately; to continue this effort after the war ends in Indochina, because what is the sense of winning the arms race and losing the human race?

I do not want to go to prison. but more I don’t want a Vietnamese person or my American brother in uniform (his name is Billy) to die because of a bullet I bought.

The issue opened with a report about a creative action by Peace Investors of Eugene (PIE):

“More Pie for the People, Less for War” is the slogan of a fast-growing alternative fund begun by tax resisters in Eugene, Oregon.

Called Peace Investors of Eugene (PIE), the fund is aimed at redistributing refused tax money to meet human needs by helping to finance a day care center, a free clinic, a crisis switchboard, and a half-way house. the founders of the fund, including members and attenders of Eugene Meeting, handed small slivers of pumpkin pie to persons entering the state employment building and explained, “Sorry we can’t give you more, but the rest goes to the military.” 64 percent of each pie was handed to a person representing the military, and these large pieces were later distributed to local armed forces recruiters.

Other creative actions by tax resisters involved in PIE include providing a peace-oriented tax consultant service and posting notices at places where 1040 forms are distributed advising people of the proportion of the federal budget assigned to war-making.

At the IRS where such notices were prohibited three of the group stamped directly on the forms the phrase, “Warning: more than half of your taxes go for war.” Charles Gray of PIE says the group has grown not only through such actions, but also through their cooperative relationship with people in the community service groups to whom money has been given. “We feel that in a small way, the war machine has been replaced by new and more loving social priorities.”

The issue opened with “Some Friendly Tax Tips” from Meg Dickinson.

Excerpts:

Fortunately for us there has been a dramatic change in tax resistance.

The IRS itself has revised its forms to permit resistance without “falsifying” records, i.e. claiming more dependents than actually exist, a practice that even when done quite openly (with accompanying letters) left something to be desired.

For many… the essential question continues to be how to refuse much larger amounts, so that we are not only protesting but actually removing our taxes from the syndrome of destruction our government seems committed to.

How can we not only protest, but stop paying for, stop buying war?

This is where IRS’s revised W-4 helps.

For wage earners it is always possible to submit a new W-4 to the employer.

The revised one does not even mention the word “dependents.” Instead it asks

how many allowances you claim. “Allowances” is not defined, but is used to

indicate dependents, special conditions such as blindness, and also amounts

of anticipated itemized deductions. If you decide you will itemize your

deductions and claim a peace deduction for the amount that might otherwise go

to military expenditures, you simply add these allowances to those you have

taken for family members,

etc. On the form

you give your employer you enter only the total.

Another part of the IRS revision changes the statement you must sign.

No longer does one “under the penalties of perjury” certify that the number is correct.

Instead one certifies “to the best of my knowledge and belief” that the number is right.

To figure how many allowances to claim, divide your annual salary by $750.

This gives you the total number of allowances in your salary. You then add

the number of allowances you have for family members,

etc., to the

number of allowances that correspond to the percentage of the remainder that

you want to refuse. With $15,000 salary you have 20 allowances. If with a

family of four (4) you wish to refuse 66 percent, subtract 4 from 20 (16

allowances left) and take 66 percent of 16 (13 allowances). Adding 13 to 4,

you take 17 allowances.…

This brings up the question of what to tell your employer.

Obviously individual decisions vary from complete candor to no discussion at all. IRS regulations are clear in making the wage earner, not the employer, responsible for the accuracy of the W-4.

One thing that should be understood is that if you take allowances for

anticipated peace deductions (or Gandhian deductions or Woolman witnesses or

name your own) you are committing yourself to filling out the regular 1040

Form the following April. Unless you have this intention you are

misrepresenting your allowances on the W-4. Prosecution seems unlikely,

according to tax resistance lawyers, but is a possibility.

IRS has

strengthened our claim of legality by actually returning money to surprising

numbers of persons claiming war crimes deductions. There are even instances

of individuals receiving refunds two years in a row.

A frequent question from those who have given tax refusal some thought concerns IRS’s collection.

Doesn’t the government always get the money?

Many who refused the phone tax found it was taken from their bank accounts (with hefty bank charges added sometimes) and felt too little had been accomplished by the action.

The change in this situation lies not with IRS but with the development of creative ways to use the refused funds.

Alternative funds have proliferated over the country, some giving the interest from the accounts to worthwhile projects, some using the whole amount to offer short-term loans to peace and community-oriented groups.

The Philadelphia People’s Bail Fund is in large part using refused taxes for their contingency fund.

Collection can be delayed through a series of routine conferences, usually a

total of four or five in a period of a couple years. These not only allow

dialog with

IRS

people but keep your funds in the service of peace longer. The culmination of

these can be a petitioning of tax court in your own behalf, thus contesting

the constitutionality of various factors involved in taxes and military power.

Tax Resistance may seem complicated, but it is really a very simple concept: finding the ways you support war and removing them from your life.

It is hard indeed to live in such a way as to take away the occasion for all war, but harder still to do it while helping to pay for the Pentagon’s program.

Robert Schultz responded to this with a letter-to-the-editor in the issue in which he wrote that he thought it was folly to try to only resist a certain percentage of the tax or a certain “war tax” (since all the money you give to the government is fungible), and also questioned whether Dickinson’s approach might be “un-Quakerly.” Excerpts:

[T]he encouragement to resort to subterfuges, claiming that you are entitled to certain deductions or allowances according to your particular religious or ideological scruples… does not seem quite honest to me….

I would prefer to come out in the clear and say frankly that I am not paying what the law requires me to pay because I do not approve of either the way, the means, or the end of the payments.

Frankly, I believe that the recommendations suggested, if followed to their logical conclusion, are pointing directly to anarchy and chaos.

Government has to function, and for an individual to take upon himself the responsibility of determining what that functioning should include strikes me as being a bit of arrogance.

I respect the Quakerly concern in regard to war. But I would rather further

it by complete simplicity of living, a renunciation of all unnecessary income

(following the example of John Woolman), a discriminating selection of all I

consume or the services I use, and a careful examination of all sources of my

income.

Also, one should avoid using any article or service upon which a Federal excise tax is levied.

To do otherwise is to negate all one thinks one gains by withholding Federal taxes directly and raises the question of the sincerity of one’s convictions.

Dickinson was also mentioned in the issue, concerning a Tax Court filing in which she was trying to get the government “to return taxes taken from her during .”

She has contributed amounts, comparable to those refused, to organizations she believes would use the money responsibly.

She charges that payment of these taxes makes her an accomplice in war-making and is against her right of religious freedom.

The issue also opened with tales of tax resistance:

“Common Sense” is the name of a storefront tax consulting service set up this spring by members of the Roxbury Alternative Fund.

This group of Boston area tax resisters drew on the expertise of trained tax accountants to provide two services: counseling for tax resisters and aid to anyone in preparing tax forms.

The project ran .

Clients often were poor or working class people.

Many were helped to avoid tax overpayments, and a large degree of friendly communication was established.

Members of Cambridge Meeting started the Roxbury Fund, and several participated in Common Sense.

On the North Columbus (Ohio) Friends Meeting decided to discontinue its telephone service “as the only course on which we are able to unite in meeting the dilemma of the payment or non-payment of the telephone tax.” For the previous two years, the Meeting had been unable to reach a consensus on phone tax resistance.

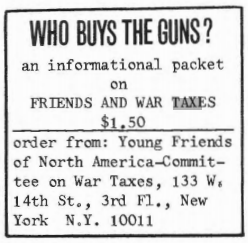

The issue of the Journal announced that “Young Friends of North America” was making available an “informational packet on Friends and War Taxes, including practical suggestions for the Friend troubled over taxation for war” called Who Buys the Guns?

The Southern Appalachian Yearly Meeting and Association met in

. According to a

Journal report on the gathering, “[f]riends were

sobered by a call to be present at the

trial of a Durham,

NC, Friend for

refusal to pay income tax for war purposes.”

In the issue, Marion Dobbert and Jeannette Marquardt proposed what they called “Legal Resistance to War Tax”:

DeKalb, Illinois, Friends have developed a stop-gap measure for resistance to payment of war taxes.

We suggest that all Friends wishing to protest war taxes in a legal manner file form 843 with the IRS for the return of that portion of their taxes which they calculate to be war-related.

This form is used to file for the return of already paid taxes which have been “illegally, erroneously or excessively collected.” Friends should find it easy to claim that collecting taxes to be used for the making of war is as much a violation of their freedom of religion as would be required military service, since both service and tax money involve the individual in the taking of human lives.

The completed Form 843 is sent to the same office where you filed your Form

1040 for the year in question. The commissioner for that office then has six

months to rule on the validity of your claim. If your request to have the war

tax portion of your income tax returned is denied, you may appeal within the

IRS,

or take your case to the proper district court. In either case, you will need

a lawyer.

Each individual can make his filing of Form 843 more effective by sending a letter with the form explaining that you are protesting war taxes, and why.

A copy of this letter should be sent to each senator and representative, along with a covering letter asking for a change in the law to provide an alternative for conscientious objectors who wish to channel their tax money into projects other than military.

DeKalb Friends Meeting has created a committee on Legal Resistance to War

Taxes to collect the names of interested individuals, keep them informed on

what is happening, what they might do to help, and co-ordinate the efforts of

groups throughout the nation. Eventually, we hope to find lawyers who will

help us appeal adverse rulings on our Form 843 claims, both within the

IRS

system and in the courts. Anyone wishing to join in our work may sign the

following and send it to: Legal Resistance to War Tax,

c/o Dan and Marion

Dobbert, 327 River Drive, DeKalb, Illinois 60115.

I am conscientiously opposed to war and must in conscience refuse to pay war taxes.

I will therefore take the legal means open to me to avoid paying such taxes.

As one step to this end.

I join with like-minded people in the Legal Resistance to War Taxes and seek a provision in the tax laws for conscientious objectors.

Signed…

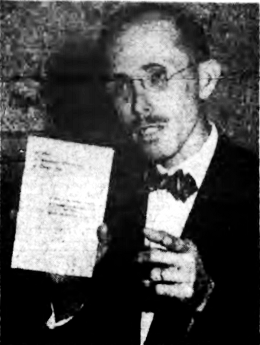

Ernest & Marion Bromley

Ernest Bromley had been resisting the federal income tax since .

Here are some excerpts from a newspaper article on Bromley, whom it identified as “a Methodist minister”:

The Rev. Ernest Bromley, leader of a pacifist tax refusal movement, is shown as he appeared in Nassau , holding a “Call” by 300 ministers for non-registration for the draft.

Forty-three pacifists throughout the country, led by the Rev. Ernest Bromley, who created a stir in Nassau when in a sermon he advised young men not to register for the draft, declared today they would refuse to pay federal income taxes this year as a “civil disobedience” protest against the government’s military expenditures.” [sic.]

A tax refusal committee of Peacemakers, pacifist organization with

headquarters in New York City, announced the stand for 41 of the group. The

Rev. Mr. Bromley now of

Wilmington, Ohio, is chairman of the committee. Another list was issued at

the same time by Walter G. Longstreth, Philadelphia lawyer, which included

11 names, all but two of which were contained in the Peacemakers’ statement.

…He has refused to pay taxes before.

The 25 men and 16 women of the Peacemakers group declared in a statement they

were “determined upon a course of civil disobedience” being “unwilling to

contribute to preparations for war.”

“We plead with our fellow citizens of the United States to join us in acting for peace by refusing to manufacture weapons of war, refusing to serve in the armed forces, and refusing to finance war preparations,” the statement said.

The committee said some would pay no part of their tax, since they maintain

the major activity of the federal government is war, with 80 per cent of the

national budget devoted to “past, present and future wars.” Others will

refuse to pay that percentage of their tax which corresponds with the

percentage which the government spends for military preparations. Some of the

refusers are Quakers, while others are members of various other Christian and

Jewish denominations and some follow a humanist philosophy.

In Albany.

Walter R. Sturr, collector of internal revenue, said imprisonment of the group is unlikely since fraud probably would not be involved.

He said the government would probably move against the group as against others owing tax money and could, as a last resort, seize property or bank accounts.

On the peacemakers’ list is Robert C. Friend, formerly a Unitarian

religious education director in Schenectady, who moved to Los Angeles last

summer where he is engaged in the same kind of work.

Bromley’s stand didn’t make the pages of the Friends Journal until 1973.

In the issue was this note:

Do peace activists have any responsibility for federal income taxes on monies paid through a sharing fund to families whose wage-earners were in prison for draft and war resistance?

This and other important questions are involved in a case brought by the Internal Revenue Service against Marion Bromley, a Cincinnati Quaker, and Ernest Bromley.

The IRS has assessed the Bromleys $9,000 and Gano Peacemakers, Inc., which owns the home where they live, $21,000.

This assessment is based on an IRS contention that the Peacemaker movement is synonymous with Gano Peacemakers, Inc., and that everyone who received checks from the Peacemaker Fund were actually employees of Gano Peacemakers and that therefore income tax, Social Security and other monies should have been withheld from the payments.

The IRS, however, has been informed by many persons that there is a clear distinction between Gano Peacemakers, Inc., and other Peacemaker activities and organizations.

Members also insist that recipients of aid from the sharing fund were not employees.

The Bromleys and Gano Peacemakers,

Inc., are unwilling to

cooperate with

IRS in

its attempt to collect thousands of dollars, mostly for war uses. They are

also unwilling to cooperate with such total misrepresentation. Ernest Bromley

points out that “the spirit and focus of any action should not be on the

protection of property or personal security, but rather on continuing to deny

money to a war-making government and to encourage tax refusal.” If any steps

are taken toward seizure of assets or property of The Peacemaker

or Gano Peacemakers,

Inc.,

a campaign of public education, direct action and publicity will begin in the

Cincinnati area.

In the , the Journal published a follow-up on the case, with an interesting editor’s note attached (note also that Ernest Bromley is now also identified as a Quaker), written by Journal editor James D. Lenhart:

Pacifism and the IRS

“The position of the pacifist is unbearable if he (or she) does not undertake intense, practical action of his (or her) own… We need the firm rock of well-directed action if we are to resist the terrible drift dragging us towards reactions of fear, hatred, and violence.”

Pierre Ceresole

Editor’s Note: With post-Watergate disclosures of apparently illegal activities by officials of the Central Intelligence Agency and the Internal Revenue Service vying for space in national news media with statements by Pentagon spokesmen who are beating the drums for increased military spending in general and continued support for South Vietnam’s President Thieu in particular, the following news from Cincinnati of “intense, practical action” and its consequences probably will not receive very much attention anywhere else.

So we decided to print it here.

Two acres and a house in Gano, twenty miles north of Cincinnati, were purchased by a small group of pacifists in .

In they formed a nonprofit corporation, Gano Peacemakers, Inc. and within eight years had paid off the mortgage on the property.

Meanwhile, Ernest Bromley, a Quaker, had become editor of The Peacemaker, a small newspaper that promotes and publicizes nonviolence.

In , the publishing address was moved to the Gano residence but the records, funds and operations of the corporation and the newspaper were kept entirely separate.

They still are separate.

Between a sharing fund

administered through the newspaper received money from those opposed to the

Vietnam war who wanted to help support dependents of imprisoned war

objectors. Monthly checks were issued to the dependents, most of whom were

mothers of young children. Other expenditures were exclusively for the

newspaper and other literature about nonviolence. There was no paid staff and

all work was done without pay.

Ernest Bromley and his wife; Marion, have refused to pay income taxes for many years as a form of witness to the peace testimony.

It is their claim that the money contributed to the sharing fund was not taxable and that even if it were, the Internal Revenue Service would have to take action against the newspaper.

Instead, IRS made an assessment of almost $25,000 against Gano Peacemakers, Inc. and on two IRS agents posted notices of seizure on the front and back doors of the Gano house where the Bromleys live.

The Bromleys have openly and consistently stated their refusal to pay taxes

for war. In fact, they do not favor going to court to protect their rights

but instead rely on personal witness and public disclosures of the abuse of

power. Ironically, while the Bromleys were taking and proclaiming their

stand, the

IRS’s

recently revealed “Special Services Staff” was secretly investigating

organizations and individuals opposed to United States policies in Southeast

Asia. Its audit of The Peacemaker newspaper began during this same period.

This is what Ernest and Marion Bromley have to say.

“Writing on the day after

IRS

posted a notice of seizure on the house here in Gano, we wanted to let you

know how we were feeling about the threatened sale.

“Of course we would hate to see such a horrendous sum as nearly $25,000 collected by the government for the budget which is so preponderantly spent for weapons, death and destruction.

Since we feel so strongly about that, it seems to us that this is a good time to have attention focused on refusal to pay taxes for war.

There aren’t many other ways people in this country can make meaningful protest about the proposed additional appropriations for Saigon and Phnom Penh, for example.

“If we had been under any illusions about the justice and ‘lawfulness’ of

this system and this government, it might be quite shocking to see

IRS

proceed to seize property on the basis of an entirely false tax claim. There

is no basis whatever for a claim against Gano Peacemakers,

Inc. — and

IRS

knows this. But we have realized for a long time that governments do not

dispense justice — they wield power.

“…we feel the same as we did in the beginning about noncooperation with IRS.

Even though this claim is a very false one, we still feel that the witness is being made.

“We want to call attention to the actions of

IRS in

any way we can, and others may think of ways to do that.”

We invite readers to suggest ways.

Meanwhile, you can write or send telegrams to either or both the District Director of IRS and the Regional Commissioner of IRS, Federal Office Building, Cincinnati, Ohio 45202.

And you can inform others of your actions and urge them to express their opinions, too.

Painful as it might be to law-abiding Friends, you also could consider refusing to pay taxes yourself.

You certainly would be in good, even Friendly, company.

There was a further follow-up in the issue:

Ernest Bromley, a Cincinnati Friend, continues to witness to the whole truth of the Quaker Peace Testimony by refusing to cooperate with the Internal Revenue Service and by steadfastly proclaiming that payment of taxes to support a budget that spends billions for military purposes is wrong.

And he continues to feel the weight of the cross he is bearing.

The IRS

moved to seize his and Marion Bromley’s home… on

. On

Ernest began distributing

leaflets outside the Federal Office Building in downtown Cincinnati. The

leaflets simply and clearly stated the facts as the Bromleys and others saw

them, and clearly and simply pointed out that more than half of the

federal budget will be spent for war or

war-related purposes. On he was

arrested on charges of disorderly conduct and obstructing official business.

While being transported to jail he received a two-inch cut on his head which

officials could not explain. These charges were subsequently dismissed.

In this entire process Ernest Bromley has refused to recognize any authority of the IRS or the courts over himself.

While he was in jail he fasted totally.

When he is physically able, he intends to resume his witness.

The Executive Committee of Friends General Conference, meeting in Cincinnati

, adopted a

minute expressing general agreement that the arrest and charges are

unjustified and supporting “these acts of conscience by Ernest Bromley and

others that issue from leadings of the Spirit. Individual members of the

Committee were encouraged to take specific actions in support of Ernest

Bromley and Peacemakers.” These actions could include messages to the

District Director of

IRS and

the Regional Commissioner of

IRS…

The following illustration comes from the issue:

Signs of the Times

On this house near Cincinnati hang two signs.

One is a notice of seizure placed there by the Internal Revenue Service.

The other sign, written by Josephine Johnson Cannon and placed on the house by members of Community Monthly Meeting in Cincinnati, supports Ernest and Marion Bromley’s refusal to pay taxes as a modern witness to the Quaker peace testimony.

The second sign reads as follows:

Historical Home of the Gano Peacemakers

“This house has sheltered a group of people who live by an extraordinary and unusual code of ethics.

It has been owned by people who do not condone killing, who do not kill, and who do not support killing with their lives or money.

“The Gano Peacemakers believe in equality, and brotherhood, and

practice equality and brotherhood. They believe in the

conservation of natural resources and a simplicity of life, and they

practice the conservation of resources and they live a

simple and productive life. They believe in sharing and they

share. They believe in the principles and essence of the religions

of the world, and they practice these principles.

“This house has a unique significance and should be preserved as a rare historic site for future generations to look upon as a beacon and guidepost for the building of a better way of life.”

As you may remember from earlier Picket Line posts on the Bromleys, the story has a happy ending.

Here is how the Journal put it in its issue:

A verbal commitment was received on , from IRS Commissioner Donald Alexander and IRS Cincinnati District Director Dwight James that the Bromley/Gano Peacemaker House will be returned! Peacemakers presented IRS officials with a detailed analysis of IRS files and actions pointing out that the bases for the confiscation of the Bromley home were shot through with political biases, faulty logic, and lacks of evidence.

At a meeting with Peacemakers that afternoon, IRS officials revealed their decision to return the property: “We realized that IRS was in a no-win situation and decided to do what was right.” Legal technicalities, however, are still being worked out.

Despite this cause for celebration, it must be kept in mind that little has

changed: taxation for warmaking goes on, the production and development of

weapons grows daily funded by our tax dollars, 11,000 persons and

organizations remain on the secret

IRS

enemies list. Again, Friends are urged to take action to stop tax funding of

war and to promote the development of a peaceful and loving world community.

And a follow-up to that came in the issue:

While Marion Bromley and her husband, Ernest, were struggling against the Internal Revenue Service’s illegal seizure of their home in Cincinnati, Marion wrote, “We appreciate the expressions of concern for us personally, and if we are unable to prevent sale of the house we will have to turn to the question of where we would relocate.

But our energies now are directed to exposing the arrogant power methods the IRS revealed in dealing with Peacemakers, and in urging the people who learn of this to take some responsibility for their own support of a government which seems to be permanently locking the people into a war system… We think if enough public clamor is raised about the wholly fraudulent actions of IRS in the matter of seizure of the property of Gano Peacemakers it might cause IRS to remove the lien [Ed. It did.] and more important, it would serve the larger purpose of educating the public about the methods of the warfare state.” [Ed. Did it?]

The next mention of the Bromleys’s tax resistance that I found was, alas, in an obituary notice for Ernest Bromley in the issue.

Excerpts:

In , Ernest was arrested for not paying an automobile tax, the proceeds of which would have gone to help pay for the expense of World War Ⅱ.… Throughout Ernest worked with other Peacemakers on local and national political issues, including integration, opposition to nuclear weapons testing, and war tax refusal.… In the Internal Revenue Service attempted to take their house away.

Their resistance to this effort brought them to the attention of President Richard Nixon and Attorney General John Mitchell.

Ultimately, they were able to keep the house because it belonged to the land trust.

During , despite failing eyesight, Ernest continued to correspond with peace activists and war tax refusers throughout the country.… In his last years, Ernest… maintained his communication with tax refusers, continuing his life-long radical pursuit of peace and justice.

Lyle & Sue Snider

Another case whose coverage began in was that of Lyle Snider.

The issue gave this report:

Lyle Snider, clerk of Durham Meeting and teacher at Carolina Friends School, was arraigned for “willfully filing a false and fraudulent withholding statement.” He had filed a W-4 form in claiming 3 billion dependents — approximately one for every person on earth.

Lyle’s reasoning: “At least half of our tax money will be spent on the instruments of war.

Every person on earth depends on someone in this country to say ‘no’ to the military and to raise a voice to protest militarism.” Both Durham Meeting and the school have passed minutes in support of Lyle’s action.

He faces up to one year of prison.

The issue gave this follow-up:

Tax resister Lyle Snider was tried in Greensboro, NC, for willfully filing a false and fraudulent W-4 form….

Over 80 supporters of Lyle and his wife, Sue, including students and staff from Carolina Friends School and Quakers from several North Carolina meetings, gathered at a pretrial celebration and at the court itself.

Despite conflicts with the court system (Lyle was cited 16 times and Sue once for contempt because of refusal to stand for the judge), Lyle reports, “Sue and I and other supporting witnesses were able to communicate extensively and powerfully on the spiritual nature of our war tax resistance.” The jury required over a day of deliberation to find Lyle guilty.

He was sentenced to 8 months for tax resistance and 30 days for contempt of court, and Sue was given 10 days for contempt.

All sentences are being appealed.

Lyle writes of the trial experience: “We created a presence of love in and

around the courtroom… fused with a strong and unequivocal witness for peace

and nonviolence. Many people felt that the trial… had changed their lives in

a very significant way… The suffering of the Indochinese people is still very

much with us in our thoughts and prayers. We continue to search for ways of

expressing our love and compassion for these people.”

The Sniders were back in the pages of the issue:

North Carolina Friends Lyle and Sue Snider have been acquitted by the Fourth Circuit Court of Appeals of charges stemming from Lyle’s claim of three billion dependents in order to avoid paying war taxes.

The court found that Lyle had engaged in “hyperbole,” not willful fraud, that he was exercising his right of free speech, and that persons may choose not to stand for a judge without being guilty of contempt.

Last summer Lyle was sentenced to nine months in jail after a trial attended by some 80 supporters of the Quaker couple.

At the upcoming national gathering of NWTRCC at Earlham College in Richmond, Indiana, I’m going to be presenting a summary of the history of war tax resistance in the Society of Friends (Quakers).

Today I’m going to try to coalesce some of the notes I’ve assembled about the renaissance of Quaker war tax resistance during the Cold War.

Much of what I have assembled here comes from my close look at the archives of the Friends Journal, the only Quaker publication from this period I have reviewed thoroughly, and so whatever editorial biases that publication may have had may also bias my history of this phase.

There is a lot that happens in this short period of time, and in some places my narrative is going to be condensed into a bunch of bullet-point-like summaries of the rapid-fire events to try to keep up with it all.

The Renaissance ()

The modern war tax resistance movement began in the wake of World War Ⅱ in the United States.

There had been isolated war tax resisters here and there in other places in recent years, and there was a quiet war tax resistance tendency hiding under the surface of the Society of Friends, but things did not come out into the open in any organized and growing fashion until then.

Quakers were not in the forefront of this movement, but Quaker war tax resisters took courage from it, and it wasn’t long before they began trying to reestablish the war tax resistance traditions in the Society of Friends.

The earliest mention of this that I have found from this period concerns Franklin Zahn of the Pacific Yearly Meeting, who was distributing a leaflet on war tax resistance as early as .

A report on the Philadelphia Yearly Meeting that year noted that the subject of war taxes had come up and had led to what sounds like a long and earnest discussion:

Few present felt it right to refuse to pay, nor yet felt comfortable to pay.

Varied suggestions were presented: Send an accompanying letter expressing one’s feeling about war; live so simply that income is below tax level; make no report, but once a year send a check for nonmilitary purposes; engage in peace walks and other minority demonstrations; follow Jesus’ example of rendering unto Caesar the things that are Caesar’s; beware of taking for granted the evils deplored, such as riding on military planes; associate more closely with the Mennonites, who share Friends’ concerns; rise above one’s own shortcomings through personal devotion; work to unite with all Friends Yearly Meetings in refusal to pay taxes.

Nothing can be done unless there is a willingness to suffer unto death.[!]

The blinders put on during the Great Forgetting period were still evident.

An article in a issue of the Friends Journal described “refusal to pay taxes for support of war effort emerging as a new testimony” [my emphasis].

Another article from the same issue, titled “The Quaker Peace Testimony: Some Suggestions for Witness and Rededication” didn’t mention taxes at all.

By this time some Friends in Switzerland had been refusing to pay war taxes (I would guess, under the tutelage of Pierre Cérésole).

In some Quakers in the Pacific Yearly Meeting began to sketch out the initial drafts of a legislative “peace tax” proposal which they envisioned would be a way for conscientious objectors to pay their taxes into a fund that the government could only spend on non-military items.

The idea that there might be a legislative solution that could make tax-paying no longer an act of complicity with war would bob up throughout this period, until, by the end of it, the temptation of lobbying instead of committing to direct action would contribute to the eventual decline of war tax resistance in the Society of Friends.

also, the Yellow Springs Monthly Meeting issued a statement of support for war tax resisters, the first example of new institutional support for war tax resistance in the Society of Friends that I could find from the 20th century.

In there was a burst of excitement about war tax resistance in the Baltimore Yearly Meeting (yet a survey of 350 adults from that meeting found only two or three who were willing to consider actually becoming resisters; whereas almost half of those surveyed were totally unconcerned about their tax money going to the military).

A group of about twenty Quakers, organized by Clarence Pickett and Henry Cadbury, met at the Philadelphia Yearly Meeting to discuss war tax resistance, but they were unable to come up with a consensus statement.

Quaker war tax resister Arthur Evans was imprisoned for three months for his tax refusal.

In the Friends Journal ended what strikes me as a policy of editorial embarrassment about Quakers and war tax resistance by publishing its first article devoted to the practice, and one that also full-throatedly advocated it.

This started a debate in the letters-to-the-editor column and certainly caused more Quakers to confront the question, directly or indirectly.

By the tide was shifting rapidly.

Before this time, individual Quaker tax resisters are unusual enough to highlight individually as being on the cutting-edge; after this, Quaker war tax resistance becomes commonplace enough that individual resisters are exemplars of a larger trend.

In the New York Yearly Meeting promoted war tax resistance in an official statement, and promised financial assistance for any Quakers in the Meeting who might be forced to change jobs or to suffer other financial hardship for their stand.

The statement in part read:

We call upon Friends to examine their consciences concerning whether they cannot more fully dissociate themselves from the war machine by tax refusal or changing occupations.

That was the most concrete advocacy of war tax resistance by a Quaker institution in years.

Franklin Zahn wrote a booklet on Early Friends and War Taxes to reintroduce Quakers to their own history and to further banish the Great Forgetting.

The support from Quaker institutions and publications at this point is often noncommittal and is usually vague about exactly how to go about war tax resistance, which taxes to resist, and how to deal with government reprisals.

There is nothing like the specific, concrete discipline of earlier Quaker Meetings.

This means that Quaker war tax resisters from this period are largely making it up as they go along, conferring with each other informally and organizing, when they are organizing, in groups like Peacemakers, the War Resisters League, and the Committee for Non-Violent Action — that is to say, with non-Quaker groups.

(There was briefly something called the “Committee for Nonpayment of War Taxes” run out of Quaker war tax resister Margaret G. Bowman’s home in , but I have not found much about it.)

Quakers were using a broad variety of tax resistance tactics.

Arthur Evans and Neil Haworth refused to pay some or all of their income taxes or to cooperate with an IRS summons for their financial records.

Johan Eliot redirected twice the amount of his taxes to the United Nations to promote international federalism as a world peace strategy.

Clarissa & Samuel Cooper lowered their family income below the tax line.

John L.P. Maynard and Robert W. Eaton took pay cuts that reduced their incomes to the maximum allowable before federal income tax withholding was mandatory.

Lyle Snyder stopped withholding by declaring three million dependents on his W-4 forms.

Alfred & Connie Andersen stopped filing income tax returns.

Some Quakers fled to Canada as taxpatriates to join the draft evaders there.

Others deposited their taxes into escrow accounts and invited the IRS to seize the accounts while refusing to pay voluntarily.

Lloyd C. Shank advocated “the ‘sneaky’ way” of tax resistance — what many people would call tax evasion — saying “ ‘cheating’ is only an oppressive government’s name for a good man’s refusal to murder.”

Phone tax resistance was beginning to become widespread, and many Quaker meetings began resisting this tax on their office phones (one meeting was unable to reach consensus on resisting the phone tax and compromised by dropping its phone service entirely).

People too timid to resist, and meetings unable to reach consensus on resisting, might instead write their legislators to urge them to enact some form of legal conscientious objection to military taxation.

The most timid groups, like the American Friends Service Committee, urged people to pay taxes “under protest” or to match their war tax payments with additional payments to the AFSC.

Robert E. Dickinson had perhaps the most creative tactic of the bunch.

He designed and built a set of furniture for his home that was formed of interlocking sheets of plywood such that it could be quickly disassembled and hidden away.

He called this “my tax refusal furniture” and meant it to frustrate IRS attempts to seize furnishings from him for back taxes.

Two Quaker employees of two groups within the Philadelphia Yearly Meeting asked their employers to stop withholding income tax from their paychecks, and that Meeting tried to come up with a good policy to follow in such cases.

The fourth Friends World Conference was held in .

The “Protest and Direct Action group” there “called upon Friends in countries party to the [Vietnam] conflict to ‘go as far as conscience dictates in withholding support from their governments’ war-making machinery,’ first by direct communication with those against whom the protest is made, and then if necessary by public witness and individual action, including the possibility of refusal to pay taxes for war.”

U.S. President Johnson called for a 10% income tax surcharge explicitly to fund the Vietnam War.

This would be the first explicit “war tax” (other than, arguably, the phone tax) since World War Ⅱ, and its announcement prompted renewed interest in war tax resistance inside and outside the Society of Friends.

Quakers were, because of this tax, better-enabled to quote the discipline of early Quakers on refusal to pay explicit war taxes as a way of explaining their own stands.

In 203 delegates from “nineteen Yearly Meetings, eight Quaker colleges, fifteen Friends secondary schools, the American Friends Service Committee National Board and its twelve regional offices, and nine other peace or directly-related organizations” met in Richmond, Indiana, to draft a “Declaration on the Draft and Conscription.”

Part of this declaration mentioned the war tax concern:

We call on Friends everywhere to recognize the oppressive burden of militarism and conscription.

We acknowledge our complicity in these evils in ways sometimes silent and subtle, at times painfully apparent.

We are under obligation as children of God and members of the Religious Society of Friends to break the yoke of that complicity.

We also recognize that the problem of paying war taxes has intensified; this compels us to find realistic ways to refuse to pay these taxes.

After only of thaw, some seventy years of Great Forgetting have been melted away, and the Society of Friends has again reached a consensus that Quakers are compelled to refuse to pay war taxes.

President Johnson’s war surtax went into effect in , adding a 7.5% surtax to the income tax returns for , and 10% for (the tax would be extended at a reduced rate into and then abandoned).

Meetings all across the country were discussing and passing minutes on war tax resistance, though few would advocate it in specific and unreserved ways, most choosing instead to voice expressions of unspecified “approval and loving support” for Quakers who felt compelled to resist.

In , the Philadelphia Yearly Meeting passed a relatively strong minute stating:

Refusal to pay the military portion of taxes is an honorable testimony, fully in keeping with the history and practices of Friends…

We warmly approve of people following their conscience, and openly approve civil disobedience in this matter under Divine compulsion.

We ask all to consider carefully the implications of paying taxes that relate to war-making…

Specifically, we offer encouragement and support to people caught up in the problem of seizure, and of payment against their will.

The New York Yearly Meeting decided to begin resisting corporately by refusing to honor liens on the salaries of tax resisting employees (though it could not reach consensus on a refusal to withhold income tax from such employees), and, , by refusing to pay its own phone tax.

The American Friends Service Committee finally decided to do something concrete about the war tax question, but it was a little odd.

They withheld and paid taxes from a war tax resisting employee and then sued the government for a refund.

The strange structure of their process seems to have been a very deliberate way to structure a legal suit for maximum effectiveness, and it did (briefly) show some success.

A court ruled in , on First Amendment freedom-of-religion grounds, that the government could not force the organization to pay the taxes of an objecting employee — alas, the Supreme Court almost immediately, and overwhelmingly, overturned this.

Also in , Susumu Ishitani, a Japanese Quaker, formed a war tax resistance group in Japan — the first example I am aware of from Asia.

By , the Friends Journal’s coverage of war tax resistance is less occupied with advocacy, debate, and the presentation of individual exemplars, and is more concerned with the practical aspects of how Quakers are going about it.

The editorial stance shifts again, to one of more forthright advocacy.

It is assumed that Quakers want to avoid paying war taxes, and the question is how to do so well.

The ending of the U.S. war on Vietnam did not seem to slow the enthusiasm for war tax resistance.

In the Friends Journal devoted an issue to the subject for the first time.

In Robert Anthony began another attempt to get the courts to legalize conscientious objection to military taxation.

It went nowhere, but notably, in a letter to the court, his monthly meeting wrote:

We assert that the free exercise of the Quaker religion entails the avoidance of any participation in war or financial contribution to that part of the national budget used by the military.

If not exaggerated for effect, this statement would be among the strongest yet articulated by a Quaker institution in this renaissance period — not simply expressing support for war tax resisters, or encouraging Friends to consider resisting, but asserting that to practice the Quaker religion necessarily meant to refuse to pay war taxes.

In , Quakers met with their Brethren and Mennonite counterparts to draft a joint statement that encouraged war tax resistance — the “New Call to Peacemaking.”

The Philadelphia Yearly Meeting asked its ongoing representative meeting to draft some formal guidance for Quaker war tax resisters for how they should go about it, and to set up an alternative fund to hold and redirect resisted taxes.

(New England Yearly Meeting began its own alternative fund for resisted taxes .)

By this time war tax resistance is a core part of any discussion of the Quaker peace testimony, and there are increasing calls for Meetings to resist taxes as an institution.

In the Philadelphia Yearly Meeting approved a minute on war tax resistance that pulled its punches a bit:

Our strength and our security are derived from our belief in the reality of a loving God and the oneness of that of God in all people.

In order to say yes to this belief, we must seriously consider saying no to payment of war taxes.

This “seriously consider” compares poorly to discipline of times past (e.g. “a tax levied for the purchasing of drums, colors, or for other warlike uses, cannot be paid consistently with our Christian testimony” [Ohio Yearly Meeting, 1819]).

It also, some Quakers point out, sometimes pales next to the more direct and certain advice from some meetings that young Quaker men resist the draft.

As more Quakers and Meetings feel the pressure to take a stand on war taxes, the more timid ones are increasingly desperate to find ways to do so without actually having to resist.

Silly ideas, like writing “not for military spending” in the memo field of their tax payment checks, and “peace tax fund” ideas proliferate.

By , Quakers in Canada and Australia are floating their own peace tax fund legislation ideas.

Meanwhile, Quakers in England seem to have gotten the tax resisting bug.

The Friends World Committee for Consultation and London Yearly Meeting stopped withholding income taxes from twenty-five war tax resisting employees in , putting the money in escrow.

(This resistance was short-lived; after losing a legal appeal in , they went back to withholding.)

In war tax resistance, according to Friends Journal reports, was a “major preoccupation” of the London Yearly Meeting, and a “burning concern” at the Philadelphia Yearly Meeting (where “unity could not be achieved”).

Lake Erie Yearly Meeting encouraged its Monthly Meetings “to establish meetings for sufferings to aid war tax resisters.”

Pacific Yearly Meeting started an alternative fund.

Smaller Monthly and Quarterly meetings around the country were beginning to take even stronger stands.

The Minneapolis and Twin Cities Meetings approved a minute that asked “all members of our meetings to practice some form of war tax resistance”!

The Davis (California) meeting passed a similar minute.

Monthly Meetings are assembling “clearness committees” to help each other find responses to the war tax problem that are appropriate to their conscientious “leadings.”

also, the Friends General Conference promoted the idea of Quakers giving interest-free loans to them, a thinly-veiled (not explicitly stated) way of hiding assets from IRS:

…Friends loan money to F.G.C. at no interest, which F.G.C. invests to earn income which is used to support the varied programs of the Conference, such as publications, religious education curricula, and the ongoing nurture program.

These loans provide regular dependable monthly income to the Conference, and reduce the interest income on which the lender must pay federal income taxes, while providing the lender with protection against unforeseen financial reversals.

F.G.C. will repay the principal amount within 30 days after receiving a written request from the lender.

All principal amounts are kept in insured investments.

In the Friends Journal, now edited by a war tax resister, devoted another issue to the subject.

Non-resisting Quakers were now very much on the defensive.

One complained that at the Philadelphia Yearly Meeting , taxpaying Quakers like him “were compared to the Quaker slaveholders of , and not a dissenting voice was raised,” but even he had to acknowledge that war tax resistance was “in the mainstream of Quaker thought, and therefore entitled to support from Quaker bodies.”

The meeting itself though could only agree to issue another minute that would “not urge” Friends to resist, but would “give strong support” to those who did.

In , the Friends World Committee for Consultation held a war tax resistance conference in Washington, D.C., and formed a standing “Friends Committee on War Tax Concerns.”

, they held a conference for Quaker organizations that had war tax resisting employees.

The conference was attended by 35 people, including representatives from 21 such organizations.

They were united by an interest in supporting the war tax resistance of their employees in an open and honest fashion, in a way that included the redirection of the resisted taxes to beneficial causes, and that used the “clearness committee” process.

You definitely get the feeling that momentum is building and Quaker war tax resistance is having a vigorous revival.

Unfortunately, though, it seems to me that this is the high-water mark.

In surprisingly little time the tide will begin to recede.

But there is still some forward progress to be made.

In the London Yearly Meeting declared:

We are convinced by the Spirit of God to say without any hesitation whatsoever that we must support the right of conscientious objection to paying taxes for war purposes…

We ask Meeting for Sufferings to explore further and with urgency the role our religious society should corporately take in this concern and then to take such action as it sees necessary on our behalf.

The Friends United Meeting adopted a policy of not withholding taxes from resisting employees as well.

The Philadelphia Yearly Meeting soon followed suit, and refused to withhold federal taxes from three war tax resisters on the payroll (after a legal battle, they would pay “under duress” ).

The Baltimore Yearly Meeting also adopted such a policy, in .

In another conference for employers of tax resisting employees was held, this one expanded to include Mennonite and Church of the Brethren employers.

The Friends Journal got an IRS levy on the salary of its editor, and it devoted a third issue to the topic of war tax resistance.

Some Quakers begin using the tax resistance tactic in the service of other causes, such as opposition to capital punishment or nuclear power.

In an early sign of the receding of the war tax resistance tide, the Friends World Committee for Consultation retired its “Friends Committee on War Tax Concerns” in favor of a “Committee on Peace Concerns.”

From here, sadly, it’s pretty much all downhill.

In the next and final segment of this series on the history of Quaker war tax resistance, I’ll try to describe and explore the second “forgetting.”

Durham, N.C. (LNS) — Lyle

Snider and the Durham Community War Tax Resisters of which he is a member, won

an important victory recently in the Fourth Circuit Court of Appeals.

Reversing an earlier conviction, the court acquitted Snider of charges of

having willfully filed a false and fraudulent

income tax form when he claimed the entire

world as his dependents in order to prevent the withholding of war taxes from

his salary.

Both Lyle and Sue Snider were also acquitted of contempt of court charges

stemming from their refusal to stand when the judge entered and left the

courtroom during the trial in

Greensboro.

Although the court did not deal with the constitutional issue of whether the

tax withholding system violates a Quaker’s freedom of religion, it concluded

that there was no proof of fraudulent intent on Snider’s part. A claim of

having 3 billion dependents could deceive no one, the court said. Rather it

recognized Snider’s act as a symbolic protest against the use of his money to

finance a war.

Similarly, the Sniders’ refusal to stand up before the judge was defended by

the court as another example of “symbolic speech.” The court ruled that a

person may choose not to stand for a judge’s entry or exit for any reason

without being cited for contempt.

While the court’s rulings have cleared Snider of tax fraud and contempt of

court charges, they have not challenged the law which in part prompted his

“symbolic protest” in the first place. Income taxes, automatically withheld by

employers[,] are of course still being used by the government to finance the

military activities in Southeast Asia and elsewhere.

“Sixty per cent of our federal income taxes are going to Defense-related

activities,” estimates Henry Felisone of the New York chapter of War Tax

Resistance. “The Pentagon budget is secret but we don’t believe Nixon’s absurd

figures. Where else is 300 billion dollars going? — not health!”

Felisone pointed out that the administration’s lower figures — closer to 30

per cent — are based on manipulations and huge omissions. For example, before

the draft was ended, costs of administering the draft system were completely

neglected in Nixon’s defense estimates, as well as the Central Intelligence

Agency’s use of “secret funds.”

Several months ago the secrecy of the

CIA’s

budget was challenged as unconstitutional use of taxpayers[’] money, but

defeated by the Supreme Court conservative justices 5-4.

In general, Felisone explained, the government tries to avoid the

constitutional issues raised by the tax laws. Instead of prosecuting people

for tax resistance, the government finds some technicality to prosecute

something else, like fraud. “Indictments for tax refusal would raise too many

political issues,” Felisone said.

“The whole withholding system is unconstitutional,” continued Felisone. “By

automatically withholding your money without going to court, it deprives you

of your constitutional right to due process of law.” Furthermore, Felisone

charged, “You can’t force an employer to do the Internal Revenue Service’s

work. That’s involuntary servitude.”

All these constitutional issues are being raised in a suit co-sponsored by the

Emergency Civil Liberties Union and the War Tax Resistance — which is hoping

to “take the case to the media and the streets, and undermine the withholding

system and the U.S.

military machine it supports.”

Meanwhile, individuals and political groups who refuse to withhold income

taxes continue to be harassed. For whether it’s constitutional or not, if your

taxes haven’t been withheld, the government can confiscate any property,

wages, even remove money from your bank account.

“If the

IRS goes

to a boss and demands a wage check for an employee owing taxes, he hands it

over. If he doesn’t, the next day there are 10 agents auditing his business,”

explained Felisone.

“Don’t give the

IRS this

employment information,” Felisone warned. “If an agent comes to your house,

don’t let him in and don’t speak to him. If you do he can legally grab your

TV and run out with

it. It’s out and out stealing, but it happens.”

While the recent court decision acquitting Snider on Tax fraud does not

resolve these more fundamental constitutional questions, “It sets an excellent

precedent… You can stop your withholding by claiming a large number of

dependents, and they can’t get you on fraud,” said Felisone. If the government

can’t dig up some other technicality, perhaps it will finally be forced to

confront the constitutional and political issues.