Tax resistance in the “Peace Churches” →

Quakers →

20th–21st century Quakers →

William (“Bill”) & Sue Himmelbauer

What happened between the time when Peacemakers was leading the war tax resistance charge and , when the National War Tax Resistance Coordinating Committee was founded?

There was another group, simply called “National War Tax Resistance,” that took the reins during the Vietnam War.

was, as the CNVA Bulletin declared, “The Year of Vietnam.”

Picketing and sit-downs across the country marked the announcement of the first US bombing of North Vietnam on .

These continued throughout the month and much effort was expended gathering signatures for a new appeal, the Declaration of Conscience, circulated by radical pacifist groups, urging civil disobedience.

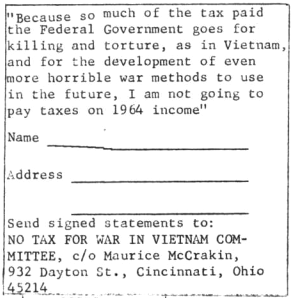

The Peacemakers group in Cincinnati organized a “No Tax for War in Vietnam Committee” calling for tax resistance.

In a separate group — War Tax Resistance, coordinated by Bob Calvert — was established and at the time included some 200 local tax resistance centers across the country.

Nonpayment of war taxes, practiced by Quakers and others, disappeared as a pacifist testimony soon after the Civil War and Thoreau’s famous stand against the U.S. foray in Mexico.

It first reappeared in World War Ⅱ when a few widely scattered individuals refused to pay federal taxes on the grounds that there was no way to prevent a significant part of their money from being used for military purposes.

One resister, Ernest Bromley, was prosecuted and imprisoned for his refusal.

Many others began to inform the Internal Revenue Service that payment violated their principles.

The enactment during World War Ⅱ of a measure which required employers to withhold taxes from their employees caused particular difficulties for pacifists and led to the formation of Peacemakers in .

A Peacemaker committee promoted tax refusal and provided research, literature, action suggestions, and publicity for those in the tax resistance movement.

Although many hundreds of people were refusing to pay income taxes during , the government prosecuted and imprisoned only six: James Otsuka of Indiana, Maurice McCrackin of Ohio, Eroseanna Robinson of Illinois, Walter Gormly of Iowa, Arthur Evans of Colorado, and Neil Haworth of Connecticut.

These imprisonments and the seizure of a few cars and houses by the IRS, served to highlight the tax refusal testimony and establish it as a major nonviolent principle and tactic.

Tax resistance, like other forms of opposition to the military, increased dramatically during the Vietnam War.

In the federal government levied an additional tax on every private telephone, and in a rare moment of candor, admitted that the money would help subsidize the war in Indochina.

Peacemakers, the War Resisters League, and other nonviolent groups urged refusal of this tax and in the following years countless thousands heeded their call.

Under the leadership of Bob and Angie Calvert, War Tax Resistance was formed in as a separate organization to investigate all aspects and ramifications of conscientious tax refusal.

During the war there were over 200 local war tax resistance centers, as well as a number of “alternative life funds” which rechanneled refused tax money back into the local community for constructive purposes.

Many of these continued after the end of the war.

The tactic of claiming enough dependents so that no income tax would be withheld became more widespread as the Vietnam war continued.

Often the tax refuser would make clear the moral grounds for the protest by listing, for example, “all the Vietnamese” as dependents.

Refusing to pay for war by claiming excessive exemptions brought particularly strong response from the government.

A number of people were prosecuted and imprisoned: Jim Shea, Karl Meyer, William Himmelbauer, Mark Riley, Ellis Rece, Carole Nelson, John Leininger, and Martha Tranquilli (a 64-year-old grandmother and nurse).

The tax resistance movement continued after the war and grew to include both pacifists and non-pacifists who could no longer in conscience support the military priorities of the government.

As more and more tax money was directed toward the [Reagan era] military buildup, many activists revived interest in war tax resistance.

Protests were organized each year, and individual resisters tried a variety of means to deny the government money for war.

In , demonstrations were held in Dallas, Atlanta, San Francisco, Los Angeles and other cities and 24 people were arrested at IRS offices in New York City.

The following year, the National War Tax Resistance Coordinating Committee was formed by the Center on Law and Pacifism, Conscience and Military Tax Campaign, WRL, Peacemakers and eighty local groups.

featured the largest show of war tax resistance actions in , including Ralph Dull, an Ohio farmer and tax resister , who drove a truckload of grain to the IRS office as payment for his taxes.

The IRS instituted a “frivolous returns” penalty to discourage the filing of returns with any but the requested information, and some resisters began an insurance fund, pooling their resources to pay fines and interest charges levied against fellow tax resisters.

War tax resistance in the Friends Journal in

War tax resistance continued to come up frequently in the pages of the

Friends Journal in .

In the issue, Clifford Neal Smith

examined radical, communal economic restructuring as one potential Quaker

approach worth considering — not state Communism, but something along the

lines of Hutterite communities that took their inspiration from

Acts 2:45–46: “All that believed were together, and

had all things common; and sold their possessions and goods, and parted them

to all men, as every man had need.” Smith suggested “that Friends give thought

to the possible restructuring of our Meetings into communes” along these lines.

In particular, he thought, “the communal way will recommend itself to Friends

who with to resist the payment of war taxes, for, as the Hutterites have

found, there is a considerable tax saving to the communal way, particularly as

practiced by a religious organization.” He also anticipated that “in the event

that Friendly testimony against the military-industrial complex should become

effective enough to be recognized by the establishment as the real foe of the

present system,” communes would help Quakers be more resilient against the

persecution that would inevitably follow.

In the same issue was a letter-to-the-editor by Philip van der Goes in which

he made the hopeful suggestion that the government allow taxpayers to

designate on their tax forms which federal agencies they want to fund.

In the following issue, Betty Gulick wrote a piece in which she expressed that

Quakers, by “personally lending support to the most violent of societies (our

own) by our taxes, our jobs, our investments, by silence and by our merely

going along with things as they are,” lose the credibility they need to have

to recommend nonviolence to the “aggressive victims of aggressive prejudice

and poverty.”

In that issue also was an article about activists in Puerto Rico who had

constructed a chapel in a

U.S. Navy firing

range on the island of Culebra, in defiance of a Federal injunction. One of

those arrested was Dan Balderston. The article reprinted his statement, from

which I take the following excerpt:

My people, the Quakers, have always insisted that God is to be obeyed and not

men, and that we are neither to be satisfied with the state of things, nor

with a promise of salvation in the hereafter, but live as though the Kingdom

were already here — without doing violence or harming our brother. They

refused to own their brothers as slaves, refused to kill or to pay taxes to

kill — for example, my great-great-grandfather, Lloyd Balderston, refused to

pay war taxes during the Civil War and the government expropriated several of

his hogs. The Quakers have fallen with the rest of the Babylonians, but there

is a remnant which seeks to recall the voice of Jesus to the Society of

Friends, and I think that we of A Quaker Action Group seek to act for that

remnant and to find once more the spirit of the early Christians and the

early Friends.

In seeking the will of Jesus for our time, some of us have been led to break

the laws of the United States — thus A Quaker Action Group sent the sailboat

Phoenix to North Vietnam with medical supplies in violation of the law

against “trading with the enemy,” and thus I have refused to register for

war, and last year refused to pay the ten percent war tax on telephones.…

Jane Meyerding wrote in from prison, where she was serving time for her action

in destroying draft board,

U.S. Attorney, and

FBI records. Excerpts:

We have to stop this war. We have to end the military takeover of our

economy, our minds, and our young men. We have to retake control of this

nation in order to stop its wanton destruction of lives here and abroad.

Of course, these things will not be accomplished simply because we want them

to be. The first step in the direction of change is to look for opportunities

to act effectively. This first step is harder than it sounds. I had to be

practically hit over the head with it before I opened my eyes to see how I

could be useful. (I thank God the action was successful even with my

reluctance to accept disruption of my “business as usual.”)

After the opportunities are discovered, they have to be taken. We

all have opportunities to stop paying war taxes, to publicly remove our

support from the government’s war policies, to “aid and abet” those who take

direct action against the institutions of war. Why do we so often leave the

most radical and risky parts of our witness to the young men who have already

put at least some aspects of their futures in jeopardy by refusing to comply

with the draft?

With so much to be done, we all just have to become activists of one

sort or another. From now on — each time a step away from war and toward peace

needs to be taken — if I do not take it, you will have to; if you do not take

it, I shall have to. None of us can afford to miss any more opportunities.

So, what will I be doing when I get out? As much as I can of what needs to be

done. With as many friends (and Friends) as possible.

The issue noted that the Ann Arbor

(Michigan) Meeting was asking telephone tax resisters to pay their phone bills,

minus the excise tax, as a group, in order to “[p]rotest the obscenity of war.”

Brinton Turkle shared his decision to start resisting in the

issue:

One of the most familiar Quaker stories concerns William Penn’s reluctance to

give up wearing his sword when he became a Friend. With great wisdom (and

some humor, I think), George Fox is supposed to have told William Penn to

wear his sword as long as he could. On , I sent this letter to the Internal Revenue Service and thus took

off a sword I had been wearing long enough:

Sirs:

To repudiate a government that no longer represents me, I am not filing a

federal, state, or city income tax this year.

I am self-employed. In the past, federal taxes I have filed but refused to

pay in protest were simply seized from my savings account. To make my

earnings less accessible for uses I abhor, I have been deliberately remiss

in keeping records of my income and expenses. An accurate assessment of my

taxes is therefore impossible.

I expect harassment and retribution to follow my defiance of a government

that has made my nation the greatest scourge mankind has ever suffered.

Imprisonment may end my career as a creator of books for children. It is a

privilege to be able to bring enrichment and delight to young people. It is

work I do with love and pride. My work is not murder.

I would not release a bomb or pull a trigger. I would not pay another man to

do these things, nor would I buy his weapons.

My Lai stops with me.

Brinton Turkle

How long was it before the awareness of the sheer senselessness of

encumbering himself with a sword caused William Penn to discard it? What a

relief it must have been to him to be rid of it!

It was a long time until the awareness of the enormity of underwriting murder

brought me to the act of civil disobedience I have just committed. About

twenty years ago, I began to see that America’s war machine rolled on our tax

dollars and nothing else. Tentatively, I sent notes to Internal Revenue with

my tax payments disapproving of our national priorities and the Korean war.

When the horrors piled up in Vietnam five years ago, I sent a letter of

protest instead of payment with my federal income tax file. I thought I was

facing prison, but it turned out that I was not a criminal — only a

delinquent. There followed a correspondence of one-sided passion between me

and a computer. Internal Revenue took the money from my savings account with

six percent interest.

The war continued. A Quaker president in the name of peace-seeking opened up

the war in Cambodia and Laos and began to show unmistakable signs of

affliction: Either he was captive to his own overweening ambition, or else he

was in pawn to the Pentagon and the industries it supports. Perhaps he was

doubly afflicted and thus worthy of a compassion that I did not have the

goodness to give him.

Holding in the Light a man to whom truth is a mere expedience, a man who is

using his power to tear our country apart, a man who has caused the death and

maiming of thousands, is beyond my present capabilities. My tax status,

however, as a self-employed person gives me a peculiar opportunity, and I

have grasped it.

I have heard the objections. Some of them I cannot answer. One does what one

must. Swordlessness will never be understood by some.

Father Daniel Berrigan has summed it up for this Quaker:

“…To be right now in some serious trouble with respect to the ‘powers and

principalities’ of this nation means to occupy a most important geographical

position — if one wishes to struggle with others all over the world for their

freedom; and by the same token to be in no trouble at all is to share in what

I take to be a frightening movement towards violence and death. To resist

that movement is one’s choice.”

A choice has been made, and I feel pounds lighter.

The issue brought the news

that the New York Yearly Meeting planned to file a friend-of-the-court brief

in the AFSC lawsuit challenging mandatory employer income tax withholding from

the paychecks of conscientiously resisting employees (see

♇ 15 July 2013). The

issue added that the Meeting

also “agreed to publicize… a two-year-old minute regarding the non-payment of

the telephone tax for war by the Yearly Meeting Office. It urges Friends who

are also nontaxpayers to join in a possible advertisement” and proposed a

“minute on the deliberate nonwithholding of wage tax levies for Internal

Revenue Service when requested by Yearly Meeting employees. The complex

procedure would notify Internal Revenue Service of the percentage of wages not

withheld and the possible setting up of a special fund of these monies for

peaceful uses.”

The “Sufferings” column of the

issue include listings for Paula & Howard Cell, who “[h]ad an automobile

seized by Internal Revenue for refusal to pay the war tax on their telephone,”

for Bill Himmelbauer, who was “[s]entenced to one year in prison for refusal

to pay war taxes on his income. To do this he openly altered his W-4 form,”

and for Lilian & George Willoughby, who “[h]ad an automobile seized by

Internal Revenue for refusal to pay the war tax on their telephone.”

Robin Harper

The issue brings the first

mention of the war tax resistance of Robin Harper, who will periodically

appear in the context of war tax resistance in the magazine for

. His first

appearance comes in the “Sufferings” column:

Robin and Marlies Harper, London Grove Meeting, Pennsylvania: Falsely

assessed, after a decade of resistance to military taxes, for $32,000 in

alleged unpaid taxes, interest, and penalties. The Harpers actually refused

less than $8000, including penalties, over these years.

The “Sufferings” column in the

issue gave an update:

[The Harpers s]ucceeded in convincing

IRS to

reduce its claim upon the family for a decade of unpaid federal income taxes

from thirty-two thousand five hundred dollars to a bit more than seven

thousand dollars.

Robin explained: “Under duress, I sent

IRS

income tax returns for to

set the record straight — a clear compromise in order to protect our family

from great financial hardship should

IRS

proceed to seize such unwarranted sums from me.”

The issue mentioned Harper

among a number of war tax resisters, and described his resistance thusly:

Conscientiously opposed to participation in war of any form, Robin began his

tax resistance in in opposition to the

nuclear arms race. The war in Indochina has deepened his conviction. He

insists that during he contributed $3,385 to “organizations engaged in constructive

programs designed to repair ravages of war abroad and counteract the ugly

wounds inflicted by segregation and discrimination at home…” The

IRS,

however, claims he owes $3,206 plus $1,502 in penalties and $2,700 in

interest. Robin is asking the

U.S. Tax Court to

reject all

IRS

claims for the 10-year period.

In the issue, Harper is

mentioned as being “a member of the War Tax Concern Support Committee” who

addressed the Philadelphia Yearly Meeting about that subject, “urging a

symbolic tax refusal of a small portion of these taxes as a witness to the

Peace Testimony.” Alas, “[a]fter a deep and searching discussion, there

remained some who did not feel comfortable with this kind of witness. Later in

the week a revised minute was presented, and after renewed searching it was

adopted.” No details are given about this revised minute.

I next notice Harper in the Friends Journal

archives in the edition,

which finds him again (still?) battling the

IRS in

court:

In three court hearings, attended by as many as 40 supporters, tax resister

Robin Harper… testified recently that he could not be compelled against his

religious beliefs to participate in the collection of taxes for war purposes.

In the final hearing, Edwin Bronner, Haverford College history professor,

appeared as an expert witness to spell out the 300-year history of the

Friends Peace Testimony.

The government apparently considered the arguments presented, including an

excellent brief prepared by volunteer attorneys, as too compelling.

Department of Justice lawyers abruptly withdrew their subpoena issued to

Harper a year earlier to force him to present documents and answer questions

in federal court in Philadelphia.

In the issue, Harper wrote at length

about war tax resistance in the Society of Friends. He mentioned the cases of

three Philadelphia Yearly Meeting employees who were resisters, and how the

IRS had

filed lawsuits to try to compel the Meeting to levy their salaries.

In her decision in , Judge Norma

Shapiro denied the validity of the [refusal to pay] penalty but upheld the

levy, which the yearly meeting then paid “under duress.” In each instance the

yearly meeting incurred legal expenses, but the individual employee

reimbursed it for the full amount of the actual

IRS

collection.

Harper then proposed a series of queries “for the purposes of discussion and

discernment… mindful that beneath each lies the Grand Query: ‘What does the

Spirit require of me?’ ”:

Query 1: If I am opposed to the military conscription of my body, am I called

to bear witness to the military conscription of my tax dollars?

Query 2: How do I approach the dilemma of paying taxes for constructive

government programs while resisting payment for war preparation?

Query 3: Does the fact that billions of military tax dollars are unearmarked

and hidden “in the mixture” in the

U.S. treasury

lessen my burden to bear witness?

Query 4: Have I sought clearness on what to do with the money I have refused

to pay in military taxes? Are alternative funds that use my refused taxes to

pay for peace and social justice initiatives an adequate spiritual response

from me?

If the Peace Tax Fund were passed by Congress, would the escrow account

thereby established be an acceptable alternative?

Query 5: How much inconvenience or suffering am I prepared to accept for the

“moral disarmament” of my federal taxes, such as penalties and interest on

refused taxes, seizure of bank accounts, salaries, or other assets, or loss

of credit?

Query 6: As a military tax refuser, am I sufficiently sensitive to the impact

my witness may have on loved ones, co-workers and others who may not share my

conviction but whose personal, spiritual, financial, or professional

well-being might be affected by my witness?

Query 7: When a Quaker employer must choose between compliance with

government demands and honoring the conscientious witness of an employee,

where does its allegiance lie? What issues of faith make this decision a

difficult one?

Query 8: Honoring the conscientious witness of an employee may place serious

risk on the Quaker employer, its members, and other employees. How do Friends

institutions balance support of employee conscience against these risks?

Query 9: Should Quaker employers rest easy serving as collectors of federal

military taxes by routinely withholding income taxes from their employees and

remitting them, without protest, to the Internal Revenue Service?

Query 10: When making a strong, public witness against military taxes by

protest or refusal to pay, is a Quaker institution likely to strengthen or

weaken the peace movement? The Religious Society of Friends? The possibility

of doing successfully the work for which the institution was created? (This

query is taken from page 189 of the Handbook on Military

Taxes and Conscience, edited by Linda Coffin…)

In the issue, Harper responded

with a letter-to-the-editor to a critic of war tax resistance as a Quaker

practice who had published a piece . Harper recommended a carefully-designed form of war tax

resistance that might overcome the critic’s objections:

[L]et us suppose a conscientious taxpayer, engaging in open civil

disobedience,

refuses to render 100 percent of her/his federal income tax to

the Internal Revenue Service (say “no” to war).

carefully calculates the tax liability and redistributes the entire

sum to recipients engaged in building up civil society in peaceful

ways, thus excluding any personal benefit. Includes list of

recipients/amounts and a “letter of conscience” along with tax return — a

transparent witness (say “yes” to peace).

declares to

IRS

that he/she recognizes a moral responsibility to contribute to the

general welfare by paying one’s fair share of taxes — hence this

“alternative service” for the tax (taking personal responsibility).

clarifies to

IRS

that the full tax would gladly be paid, provided the government

would assure the taxpayer that it would be spent exclusively for

nonmilitary purposes, as defined by Congress, which is the

legislative architecture of the Religious Freedom Peace Tax Fund Bill,

still pending in Congress (support legal relief for this dilemma of

conscience).

Finally, in the issue, Harper’s

war tax resistance got a mention in an article by Parker J. Palmer, based on a

speech he gave on the occasion of the 80th

anniversary of the founding of the Pendle Hill Quaker Center:

I am going to end with a small story that has big meaning for me. Back in the

day, a wonderful man named Robin Harper was head of buildings and grounds…

Robin was and still is a conscientious war tax refuser. Not only did this

mean the possibility of prosecution and imprisonment, but tax resistance made

very heavy demands on his life. He had to be employed by people who would

agree not to withhold any taxes, which shrinks one’s job opportunities

dramatically, and he could not own any real property that could be seen by

the IRS

as capable of being turned into cash. But he has never done time because his

integrity is so self-evident, not unlike that of John Woolman.

When I was a young man here, I shared Robin’s abhorrence of war (as I do to

this day), but I could not imagine taking the risks and making the sacrifices

required of me. I was at that stage of moral development where I had very

high ethical aspirations and equally high levels of guilt about the way I

continually fell short. One day I went to Robin and told him of my dilemma.

“I believe what you believe,” I said, “and I want to put my beliefs into

action, but I just cannot bring myself to do what you do.”

Robin responded plainly,simply, and with great compassion. “Keep holding the

belief,” he said, “and follow it wherever it may lead you. As time goes on you

will find your own way of resisting violence and promoting peace, one that

fits with your gifts and your calling.” That is Quakerism at its best. That

is community at its best. That is teaching at its best. That is friendship at

its best.

War tax resistance in the Friends Journal in

In the issues of the Friends Journal, more attention is being given to the practical concerns of how to best go about war tax resistance in a way that is most effective and that most honors the Quaker way of going about things.

There’s another example of backlash in the issue: a letter from Stephen C. Conte in which he explains why he is leaving the New York Yearly Meeting for the First Evangelical Friends Church.

He lists a number of reasons, including the New York Yearly Meeting’s positions opposing laws against marijuana possession and homosexuality, and what he sees as a lack of appropriate respect for scriptural authority.

But the first example he mentions is war tax resistance:

The Christian is bound to pay his taxes.

This is the point of the famous “Render to Caesar” passage in Matthew, which we Quakers have been quite willing to quote in support of the Peace Testimony.

We, who are so willing to invoke the authority of certain passages, must likewise accept the authority of all scripture.

I cannot, therefore, as a Christian and a Friend, accept the position of the Yearly Meeting in support of nonpayment of the telephone tax.

My Christian freedom consists in rendering to God my allegiance and love, rather than in playing games with the Internal Revenue Service.

That same issue of the Journal covered the Sweden Yearly Meeting, which seemed to have tried to grapple with the question of war taxes in the most round-about way possible, by suggesting that Quakers “work for establishment of a differentiated tax [which] would mean that part of the tax that goes for military defense could instead be channeled into, for instance, the social sector.”

Sara P. Cory wrote in to the issue to say that for her, phone tax resistance had become “too feeble a gesture” and that she was going to withdraw further from the “life as usual” which was “helping to keep our war economy going” — for example, by giving home-crafted Christmas gifts or donations to charity in place of store-bought items.

The “Sufferings” column of that issue noted that Bill Himmelbauer had finished his prison sentence “for resisting the payment of war taxes.”

In the issue, Donald Ary advised those Quakers who were unwilling to reduce their incomes below the tax line to instead try to take advantage of some of the tax provisions designed to help wealthy people shelter their income from taxes.

For example, consider a Friend who is paying income tax at a twenty-percent rate and has two thousand dollars in a savings and loan account.

If the account is paying five percent interest, the Friend has a one-hundred-dollar income from it and pays a twenty-dollar tax on that income.

If the Friend puts his two thousand dollars into common stocks that pay a dividend of one hundred dollars a year, he pays no tax, as the first one hundred dollars of dividend income is exempt from taxation.

The Friend might choose to send the twenty-dollar saving to American Friends Service Committee.

The war effort is poorer by twenty dollars, AFSC is richer by twenty dollars, and the Friend is four dollars ahead when he deducts his contribution to AFSC.

The value of common stocks can go down, but, remember, the tax laws encourage speculation.

If the Friend sells his stock for one thousand dollars, the whole loss is deducted from his income; therefore eight hundred dollars is the Friend’s loss and two hundred dollars is the government’s. If the stock increases and is sold after six months for three thousand dollars, the tax laws provide preferential treatment for this increased income.

It is classed as long-term capital gain, and the Friend pays ten percent tax on this, rather than the twenty percent he pays on his salary.

“Friends may ask: ‘This is legal, but is it moral?’ ” Ary notes.

I would reply that the tax structure in the United States is grossly immoral, and any participation in it is immoral.

The tax structure is immoral because the taxes are used for war and because the tax laws are an instrument of gross injustice.… Friends who allow their incomes to reach a taxable level must choose the lesser of two evils by minimizing their tax.

Friends have spent too much effort refusing to pay unimportant symbolic taxes, such as the telephone tax.

If Friends were to employ systematically and blatantly the rich people’s tax-avoidance procedures, the people of this country might just sit up and take notice.

In the same issue was a brief note that the “Peace and Social Action Committee” of the Twin Cities Friends Meeting had “recommended that the Meeting not pay the Federal telephone tax, which is used to finance the Vietnam war.”

The issue included a brief review of Robert Calvert’s war tax resistance guidebook Ain’t Gonna Pay for War No More.

In the issue, Horace Champney shared his letter to the IRS.

Excerpt:

Since I returned [from Vietnam] in , I have openly refused to submit any tax return to the Internal Revenue Service.

I have preferred to risk jail than support an immoral, insane war.

This year again, although legally required to file, I must publicly refuse to do so.

I have been deducting the war tax from my telephone bill.

I will gladly pay Federal taxes when my Government turns off on war and mobilizes against real enemies: Pollution, poverty, disease, ignorance, chauvinism, and gadget-hungry, profit-crazed overproduction.

I must urge every compassionate and concerned American, no matter what uniform he wears, to face up to his Government and find his own way to say “No!” to this war.

Henry Thoreau’s famous words to Emerson during the Mexican war — Don’t ask why I am in jail, ask why you are outside!

— are as relevant today as they were one hundred twenty-three years ago.

The “Sufferings” column of that issue led off with the case of Sally Buckley:

Convicted of three counts of claiming extra dependents on a W-4 withholding form.

Sentencing was put off indefinitely by Judge Miles Lord, who expressed reluctance to sentence her.

At he sentenced her to thirty days and stayed sentence for sixty days to give her another chance to pay the taxes.

Her Meeting approved the following minute: “The Twin Cities Friends Meeting supports Sally Buckley in her act of war tax resistance and those of our Meeting and other war tax resisters who have followed their consciences in not contributing to the support of war and the preparation of war.

“In addition, the Meeting takes a further concrete step in support of these actions by withholding its telephone tax as a protest against the Indochina War.”

The “Sufferings” column in the issue moved forward in the magazine to share the page with the masthead and table of contents.

It included these listings:

Ellis Rece, Jr., attender of Augusta Meeting, Georgia: Sentenced to one year in prison with 320 days suspended and fined $500 for refusing to pay taxes that go to the war.

Ellis had openly claimed additional dependents on his W-4 form to prevent deductions from his earnings.

A called meeting for worship was held in Augusta Meetinghouse before the trial.

Mark Riley, attender of Sacramento Meeting, California: Has completed a six-month sentence in Terminal Island Federal Prison for refusing to pay taxes that go for war by altering his W-4 form.

A note on the Baltimore Yearly Meeting in the issue noted that although “[w]e spent much time and prayer on the best methods of protesting the Indochina war, reaching agreement on some, [we were] unable to find unity on corporate involvement in the refusal to pay war taxes.”

In the issue, David Green wrote in to promote a different tack on telephone tax refusal:

, I explained to the secretaries in the law school where I work that I will not use the telephone, either to make or to receive calls, as long as the government continues to impose the war excise tax on its use.

I have told the same thing to the people where I am living.

I commend this course to the consideration of Friends.

I understand and support those who continue to use the telephone while refusing to pay the war excise tax.

Complete telephone refusal does, however, have advantages over telephone-tax refusal.

First, it communicates more effectively.

The telephone-tax refuser can explain his reasons to the government agents who try to collect the tax and to someone in his bank where the government seizes the tax money.

The telephone refuser, however, has repeated opportunities to explain why he cannot be reached by telephone, for either business or social reasons.

Second, the telephone refuser shares in the inconvenience caused by his position.

The telephone-tax refuser inconveniences the government and bank employees, but the telephone refuser finds himself fully involved in the inconvenience his decision causes.

In the past month, I have trudged all over Washington on errands I would have performed in a few seconds by telephone.

On other occasions I have had to write notes and letters instead of making telephone calls.

But this gives some unsought rewards too — there is a real gain in simplicity.

Life is less cluttered, less hectic, if one is not a slave to every jangle of a telephone bell.

And, faced with the effort involved in using only written or face-to-face communication, much is eliminated.

Third, refusing to use telephones withdraws financial support from the telephone company — a prime war contractor — as well as from the government.

And here, as another byproduct, the refuser saves money.

Instead of a considerable charge for long-distance calls, last month I owed nothing.

A refreshing change.

Fourth, telephone refusal eliminates the tax completely instead of merely postponing its collection.

I understand, sympathize with, and support the position of the telephone-tax refuser.

I unite with his desire to be clear of voluntarily paying a tax used only in war-making.

But I ask all Friends to consider that by entirely refusing to use the telephone, they could be clear, not only of voluntarily paying the tax, but of paying the tax at all.

After the death of Ammon Hennacy in 1970, Karl Meyer took up the torch of promoting war tax resistance in the Catholic Worker.

Meyer’s approach was less exhortational and more practical: he pioneered the method of inflating deductions to prevent income tax withholding and wrote an influential early how-to guide on that method. (An embryonic version of what is now NWTRCC’s Practical War Tax Resistance pamphlet #1: “Controlling Federal Income Tax Withholding”.)

Below are some excerpts from the Catholic Worker from the period, starting with an essay by Karl Meyer from the edition:

New Resistance to War Taxes

By Karl Meyer

“Under penalties of perjury, I certify that I incurred no liability for Federal income tax for and that I anticipate that I will incur no liability for Federal income tax for .”

If you can sign that statement, you can stop the withholding of war taxes from your wages.

The statement is the Employee Certification for Form W-4E Withholding Exemption Certificate, which was first published in by the Internal Revenue Service as an alternative to the standard W-4 form.

If your employer doesn’t have it on hand, get it from the local IRS office.

Signing this statement alone provides complete exemption from prior withholding of Federal Income tax, without enumerating dependents or any other specific basis for the exemption.

Who is eligible to claim this exemption?

I say, “everybody.” It is morally impossible to incur a liability to support evil purposes and actions.

Since at least 70% of Federal taxes is spent for military or war-related purposes, and much of the balance for useless or harmful purposes, it is impossible to incur a liability to pay Federal income tax.

Who is eligible to claim exemption according to IRS?

On the back of the W-4E it says, “You may be entitled to claim exemption from withholding of Federal income tax if you incurred no liability for income tax for and you anticipate that you will incur no liability for income tax for .

For this purpose, you incur tax liability if your joint or separate return shows tax before allowance of any credit for income tax withheld.

If you claim this exemption, your employer will not withhold Federal Income tax for your wages.”

According to this definition, you would technically satisfy the requirements for exemption if you file a return for showing no tax due because of the immorality and illegality of U.S. military expenditures, even if IRS subsequently rejects your reasoning and assesses tax against you.

Likewise, if you file no return at all, your non-existent return can not show any tax due.

Now, it has always been a puzzle to me how a person who believes in conscience that taxes should not be paid could file a return showing taxes as a “balance due.”

That is self-contradictory.

If the tax is acknowledged to be due, it ought to be paid.

If it ought not to be paid, it shouldn’t be shown as “due.”

The IRS calls the income tax a “self-assessed tax.” When you file showing tax due, they are empowered to accept your assessment and proceed to collect immediately.

If you show no tax due, even if they disagree with you, they must first reassess the tax themselves and give you extensive opportunities for legal appeals, before they may proceed to collect on their claim.

Therefore, it is foolish and self-defeating to show tax as due, if you sincerely believe that it ought not to be paid.

There are several ways to assert your claim that no tax is due:

you may claim extra exemptions on line 11, on the ground of obligations to all mankind as brothers and members of one family;

you may claim an adjustment of your income on line 17, based on your principled opposition to militarism;

you may itemize a deduction on line 16 of Schedule A, claiming deduction of your whole taxable income on similar grounds.

Perhaps the soundest approach is to file no return at all. (The main disadvantage of this, besides its being illegal, is that IRS agents sometimes file distorted returns in your name, claiming excessive amounts of tax.) I didn’t file for ten years, but IRS agents have filed seven returns in my name showing more than $2000 in tax and penalties due.

On , I filed a return for in a personal interview with E.P. Trainor, the District Director at the Chicago office of IRS.

On the 1040 Form I filled in my name and address.

Under SOCIAL SECURITY NUMBER, I wrote “Peace;” under OCCUPATION, I wrote “Love;” across the face of the return I wrote in bold letters, “WE WONT PAY—STOP THE WAR—STOP THE DRAFT—STOP MILITARISM,” for FIRST NAMES OF DEPENDENT CHILDREN, I wrote “All Men Are Brothers;” under OTHER DEPENDENTS, I claimed “A Vietnamese child killed at Song My, an American soldier killed In Vietnam;” and I filled in a total of three and a half billion exemptions for the whole population of Earth; under BALANCE DUE, PAY IN FULL WITH RETURN, I put “$0.00;” then I signed with my name and the date.

Mr. Trainor and his henchmen haven’t figured that year out yet, but they can’t say I didn’t file.

Before you follow my advice and my example, I wish to speak a word of caution: Everything here is my interpretation.

Don’t expect the IRS, U.S. Attorneys, Federal Juries, or Courts of Appeal to buy a word of it.

In the and issues of the Catholic Worker, I published landmark articles on how to claim sufficient exemptions on the W-4 Form to prevent the withholding of war taxes.

Many people all over the country tried out these ideas effectively, but several last their jobs for persisting, and three were tried and convicted in Federal courts for claiming illegal exemptions.

If you can’t stand heat, stay out of the kitchen.

If you can’t do time, don’t commit crime.

If you have a concern of conscience about paying war taxes, but feel unready to face the possible consequences of the methods of resistance outlined above, the present tax rate provisions give ample opportunity to stop paying war taxes, without violating any provisions of the tax laws, if you are willing to live in reasonable simplicity and voluntary poverty in the spirit of the Catholic Worker movement.

Under the present law an individual may earn up to $1700 a year without any obligation to file a return or pay Federal income tax.

A married person with three dependent children could earn up to $4300 a year without having any tax withheld or due.

Form W-4E was actually introduced by IRS so that such persons, earning less than the minimum yearly taxable incomes by working for only a few months out of the year, would not have taxes withheld and would not have to apply for refunds months after they earned the money.

You can find the complete tables of tax withholding rates and other information in Circular E, Employer’s Tax Guide, available for the asking at your local IRS office.

I do believe that we should all strive to live in a simpler way.

If we work part time for wages and live on less than taxable incomes, we will have extra time to grow, create and do more things for ourselves, or to offer our work as a gift to people in need of it.

Even if we work full time for taxable wages, but successfully resist collection of the taxes, we should still live simply in order to share our surplus money with others who are in need.

I have done this all my adult life and intend to go on with it.

One hundred and eighty years ago, our brother rebel Tom Paine wrote:

…were an estimation to be made of the charges of Aristocracy to a Nation, it will be found nearly equal to that of supporting the poor.

The Duke of Richmond alone (and there are cases similar to his) takes away as much for himself as would maintain two thousand poor and aged persons.

Is it then any wonder that under such a system of Government, taxes and rates have multiplied to their present extent?

In stating these matters, I speak an open and disengaged language dictated by no passion but that of humanity.

To me who have not only refused offers because I thought them improper, but have declined rewards I might with reputation have accepted, it is no wonder that meanness and imposition appear disgustful.

Independence is my happiness, and I view things as they are, without regard to place or person; my country is the world, and my religion is to do good.

(The Rights of Man, Modern Library edition, page 241)

If we do not live by these principles, how are we different from the warfare state we condemn?

The budget and accounting methods of the Federal administration are confusing.

They have recently been modified to deliberately de-emphasize the role of military expenditures as a proportion of the Federal budget, enabling Nixon to claim that they count for less than 50%.

This has been done by counting all separately raised and earmarked revenues, such as Social Security revenues and payments, as part of one budgetary total.

Then the large Social Security payments can be thrown in the pot and counted at part of domestic expenditures for health and welfare.

Rejecting this ruse, it is possible without detailed analysis to estimate that between 70% and 80% of all Federal income and excise tax revenues is spent for military programs and purposes that are intimately related to the cost of past and present military activities.

Acceding to individual judgment this estimate might include veterans benefits, space research and technology, various “international affairs” programs, certain “Justice Department” activities, a percentage of the general administrative expenditures, and the interest and principal payments on the national debt, incurred primarily as a cost of World War Ⅱ and the Cold War.

Awareness of these facts, plus the explanation of new methods of resistance, contributed to a tremendous growth in the movement of war tax resistance in .

In late a national coordinating center called War Tax Resistance was established in New York.

Its periodical bulletin, Tax Talk, lists 181 local centers of contact people all over the country.

Simple nonpayment of the federal excise tax itemised on telephone bills is the easiest and most common form of principled tax resistance.

War Tax Resistance estimates that more than 100,000 people are now participating in this action. IRS agents expend great effort in collecting very small amounts of this tax, and they are hopelessly behind in their efforts to collect.

I have paid no excise tax on telephone service and IRS has succeeded in collecting only $8.00 so far.

War Tax Resistance has a basic leaflet on phone tax resistance.

War Tax Resistance estimates that 15,000 people participate in some form of income tax nonpayment, as a principled protest against militarism.

We speak of those who consciously and explicitly relate to the war tax resistance movement, because we know that millions of our countrymen, from the highest to the lowliest, participate in tax resistance or evasion, largely because of unarticulated opposition to the basic policies of government.

They will be our allies if their protest can become articulate and organized.

The most promising development in was the significant number of people who began to successfully resist payment of all or most of the income tax amounts that would be claimed under Federal law and regulations.

Until the number of such total tax resisters was small and almost exclusively limited to self-employed persons or others who derived most of their income from sources not subject to withholding tax.

In articles for the Catholic Worker ( and ) I explained how to beat the withholding tax by claiming enough exemptions on the W-4 Form that no tax could be withheld from one’s wages.

Widely reprinted and circulated in leaflet form, these articles offered an effective tax resistance method to almost any wage earner who had the courage to try it and risk the possibility of prosecution or harassment sometime in the future.

In his last letter to me before his death, Ammon Hennacy, a pioneer influence in our war tax resistance movement, glumly predicted that from fear of going to jail, there wouldn’t be more than a handful in the country that would take up my idea.

But Ammon was wrong in this case.

I know that many have taken it up, and they are growing in numbers, because I keep hearing from them, particularly those in the Chicago area.

Thousands of dollars have been held back from the military machine and donated to alternative uses that meet the real needs of people.

This movement will continue to grow from roots that are deep in the American tradition.

The ideas of Thoreau’s Essay on Civil Disobedience, fruit of his brief imprisonment for war tax resistance, are well-known today.

But a century before Thoreau our forefathers made their stand for independence in resistance to unjust taxes.

Both the American Revolution and the French Revolution were organized around the issue of resistance to taxation.

Tom Paine understood this well because he was active in both.

In he published in England a powerful polemical tract on The Rights of Man to stir the people of England to a similar revolt.

His most persistent theme of grievance is the criminal burden of war taxes imposed on the people by power hungry men in government.

He vividly describes the genesis of the French Revolution, including the refusal of the Parliament of Paris, in , to register the edicts of the King and Government seeking to enforce new taxes:

While the Parliament were sitting in debate on this subject, the Ministry ordered a regiment of soldiers to surround the House and form a blockade.

The members sent out for beds and provisions, and lived as in a besieged citadel; and as this had no effect, the commanding officer was ordered to enter the Parliament House and seize them, which he did, and some of the principal members were shut up in different prisons…

But the spirit of the Nation was not to be overcome, and it was so sensible of the strong ground it had taken, that of withholding taxes, that it contented itself with keeping up a sort of quiet resistance, which effectively overthrew all the plans at that time formed against it.

(Rights of Man, Modern Library edition, page 149)

On this strong ground let us also take our stand for a quiet battle, more effective against wrong, more productive for good purposes than any other I can think of.

Yours for a gentle revolution

Karl Meyer

Permission is granted to anyone interested to reproduce this article in whole or in part.

If it is reproduced in part, please indicate editing and deletions.

List of sources for information and communication:

War Tax Resistance

839 Lafayette Street

New York. N.Y. 10012

Phone (212) 477‒2970

Send $1 and ask for

WTR Handbook

Hang Up On War telephone tax refusal leaflet.

reprint of Karl Meyer’s Fund For Mankind article from CW

or send more to help with their crucial work of coordinating the communication and work of the movement.

The Peacemaker

10208 Sylvan Avenue

Cincinnati, Ohio 45241

A valuable periodical for all who are interested in draft resistance, tax resistance, and radical life styles.

Send $4 for a subscription, plus their Handbook on Nonpayment Of War Taxes, which includes many informative case histories.

I further recommend that all tax resisters contribute a substantial percentage of the money not paid to the Peacemakers Sharing Fund at the same address.

The Fund is a valuable channel of mutual aid for war resisters and their families, when they suffer from imprisonment or financial hardship as a result of their stand.

Karl Meyer

1209 West Farwell Street

Chicago, Illinois 60628

Phone (312) 764‒3620

Call me or write to me for personal counseling and encouragement.

If you write, send two six cent stamps for my reply and any leaflets I may send you.

Dorothy Day visited war tax resister Art Harvey and brought back this story ( issue):

I visited Art Harvey of South Ackworth, New Hampshire who has a mall order book shop handling a great number of books by and about Gandhi.

Art and Ammon Hennacy served six-month-terms in Sandstone Prison in Minnesota for trespassing on a missile base some years ago.

He carries on a practical application of Karl Meyer’s tax refusal (see article in this issue) by having teams of workers in orchards where they prune trees, harvest apples and later blueberries and work seven months of the work and live in a style which frees them from the payment of taxes for war.

Perhaps about a hundred are engaged in this way of life, which results usually in some settling in communities of the moshavim variety, each having some small acreage and a house built by themselves Considering the New England climate, no small achievement!

It certainly means an emphasis on the ascetic, on sacrifice.

The Karl Meyer article she mentioned follows:

War Tax Resistance

by Karl Meyer

On , charges were filed in federal district court in Chicago against Bill Himmelbauer, Mike Fowler and myself.

In separate cases, we are accused of falsely claiming exemptions from federal tax, to which we were not legally entitled.

Mike Fowler, a student at the University of Chicago, is charged on two counts of filing false W-4 forms with his employer.

The maximum penalty for each count is one year in jail.

Bill Himmelbauer is charged on one count.

He and Sue Himmelbauer joined with us in late in starting the Chicago Area Alternative Fund for tax resistance money, and then moved to Pittsburgh where they became ringleaders in War Tax Resistance activities.

I am charged on five counts for W-4s executed in .

Through eleven years of “one man revolution” I had successfully resisted payment of almost all federal income taxes claimed from me, mainly by claiming enough exemptions on W-4 Withholding Exemption Certificates that no tax was withheld from my wages.

The tax man did nothing beyond ineffectual attempts to collect.

Then suddenly in the one man revolution exploded into a growing movement of effective war tax resistance by the withholding exemption method.

Suddenly the tax man got worried.

Suddenly he started prosecuting withholding tax resisters around the country: , Jim Shea, Alexandria.

Virginia; , Sally Buckley and Dennis Richter, Minneapolis, Minnesota; , Paul Malinowski, and Donald Callahan, Philadelphia, Pennsylvania; , James Smith, Springfield, Missouri; and now, three more in Chicago.

On , IRS Intelligence Agents Sam Miele and Alan Leksander visited me at home.

They confronted me with copies of five W-4 forms for , and two articles from the Catholic Worker for and , “A Fund For Mankind Through Effective Tax Resistance” and “Clarification On Tax Withholding.”

These are the articles which launched the wave of withholding tax resistance action in .

I acknowledged authorship of the five W-4s and the two CW articles.

On , I received a letter from the Chief of the Intelligence Division of IRS:

“The current investigation by the Intelligence Division is nearing completion… consideration is being given to recommending that criminal proceedings be instituted against you…”

I was invited to a hearing with Group Supervisor Ralph A. Weber.

At the hearing I presented a statement of my position and various other relevant literature and documents to Internal Revenue Service.

Statement to Internal Revenue Service, Intelligence Division Hearing:

My name is Karl Meyer.

My immediate family includes my wife Jean and three children, William, 7 years old, Kristin, 3 years old, and Eric, 2 months old.

In South Vietnam, Cambodia and Laos there are many families like ours.

I gladly accept a responsibility toward them, like that which I bear toward my own children.

These other families, these other children are the ones who were machine-gunned in a trench at My Lai, and are being killed in many other ways every day that the war continues In Indo-China.

There are also the soldiers of both sides, Americans and Aslans, who are also the victims of the war, who are dying by the thousands as it continues.

Upwards of 80% of all federal income tax revenues are devoted to purposes intimately related to American wars and military activities, past and present.

In the name of my family, of the families of Indo-China, of the soldiers of both sides and all other victims of International militarism, I claim a complete exemption from all federal taxes that finance military activities.

Yes, I have claimed ten or more exemptions on several W-4 exemption certificates. I have claimed exemption from tax for myself and my family, for several others who have lived in our household and received their primary financial support from me, and for these others, the families of Indo-China, and all the victims of war.

In a peaceful and nonviolent society the job of collecting assessments for social purposes might be a useful occupation.

But the man who collects taxes for the United States government today makes himself a direct accomplice in some of the most horrible crimes of our age.

You have already told me that you are considering compounding these crimes by beginning a criminal prosecution against me.

I and my family have already made some sacrifices in the struggle against war, but they have been as nothing compared to the suffering of our brothers and sisters who are in Vietnam, Cambodia and Laos.

We ask you today to recognize just one basic human right, our right not to participate in acts of war against them.

Even if you refuse to recognize that right, we will still refuse to pay federal taxes that continue the war in Indo-China and the militarization of our society.

This is all that I have to say.

Karl Meyer

After I received the letter from IRS, I went in to talk with my supervisor in the huge hospital bureaucracy in which I was employed.

I expected her to be unsympathetic, and even hostile to me as a source of trouble for her.

After thirty years of working her way toward the top of the bureaucracy, it had seemed to me she lived and breathed the system and its rules, though I respected her even so for the great strength of her character.

But now when I told her directly of my long struggle against the war and of the imminent threat of criminal prosecution, she smiled at me from deep within, and expressed her own strong opposition to the war and her respect and support for me.

“Mr. Meyer” she said, taut with emotion, “I am black.

From all of my experience I know that when you fight the system in this ‘democratic’ country they are going to make you pay for it.”

Then she told me something of her own struggle.

After a long talk she asked me, "Wasn’t there a girl here in Chicago who took that same stand (war tax resistance) several years ago?”

Yes, there certainly was.

Eleven years later, another black woman in Chicago still remembered the courageous witness of Eroseanna Robinson, the very person whose example set my feet on the path of determined tax resistance, back in 1960 — Eroseanna Robinson who refused to pay taxes, who defied the order of Judge Robson to give information about her income in spite of a one year sentence for criminal contempt, who fasted one hundred and eight days and won her own release from federal prison by the strength of her resistance.

Now, on , the charges against Fowler, Himmelbauer and Meyer were announced.

That night we picketed and leafleted at the Main Post Office where special postmen were on duty to receive last minute returns from thousands of more tractable Chicagoans.

We haven’t yet received official notice or summons, but from the records filed in court David Finke has found that the three cases are assigned to three separate Judges for trial.

I am to be summoned for an initial hearing in the court of Judge Joseph Sam Perry.

I plan a simple and direct defense. I plan to represent myself without an attorney.

I will ask for a jury trial at the earliest possible date.

I will not base my defense on legalities.

I will simply seek to convince the jury, judge, prosecutor and everyone else that I have done what is right and in accord with inalienable rights of personal judgment, and that I should not be declared guilty or penalized for my actions.

If I am convicted and sentenced to prison, we have been thinking that Jean will apply for public aid for the financial support of our family.

We feel that if the State insists on tearing from the family its source of support, the State should bear the cost of providing other means.

We prefer to see the resources of the movement devoted to the needs of poor people in this country and abroad who have no other recourse.

This is just one of the reasons why I do not desire a costly legal defense or primary financial support from the movement, though we welcome the personal support of our friends.

The form of encouragement and support that we will value most highly will be if our friends in the movement take our troubles and our resolve as an example, to stop paying war taxes and to devote the greatest possible part of their income to sharing with the victims of international war and of the war of rich against poor.

This is why we of the Chicago Area Alternative Fund have saved nothing for our own protection, but have already given away all of our war tax resistance money to meet the immediate needs of others.

If you want to read the articles that launched the present movement of withholding tax resistance by explaining the method, and incidentally brought upon us our small tribulations, you may send two eight cent stamps to:

War Tax Resistance

339 Lafayette Street

New York, New York 10012

and ask for their reprint, “A Fund For Mankind Through Effective War Tax Resistance.”

To get in touch with us about the trial, write to:

Karl Meyer

1209 West Farwell

Chicago, Illinois 60626

Phone 764‒3620

The issue reported on how the court ruled in Karl Meyer’s case:

Karl Meyer Sentenced to Two Years, $1,000

By David Finke

On in the court of federal district Judge Joseph Sam Perry, Karl Meyer appeared in his own behalf to answer a 5-count “criminal information” charging that he falsely and fraudulently filed W-4 income tax withholding exemption certificates.

Having successfully negotiated with the U.S. Attorney, Karl got the government to drop three of the five counts (which he had said he could prove the accuracy of).

He then entered a plea of “nolo contendere,” which the judge accepted as a finding of “guilty,” on the other two counts.

A two-week presentence investigation was then ordered. while Karl remained free without bond.

, Karl returned to court with about 25 friends, supporters, and fellow tax resisters, and personally accompanied by his 7-year-old son William.

Before imposing sentence, Judge Perry with great decorum and civility said he would hear from both the government and the defendant, whose absolute right to represent himself without attorney would be respected.

Assistant U.S. Attorney Kocoras then launched into a most amazing and accurate summary of Karl’s career of leadership in the movement of War Tax Resistance:

Not only has Karl not filed a tax return , he has encouraged others to join with him in resisting federal taxes!

And he has explained publicly exactly what he is doing and how other people can do the same.

Kocoras read extensively from articles that Karl had written for Catholic Worker, including those memorable (but to Kocoras damning) phrases, “If you can’t do time, don’t commit crime,” and “If you can’t stand the heat, don’t put your hand in the fire.”

The prosecutor hit the issue squarely on the head, then, when he said:

“What is at stake here is the integrity of the income tax law.”

The government is obviously worried about the possibility of widespread, undetected, mass-based tax resistance if Karl’s ideas should catch on and not be deterred.

The prosecutor closed his remarks by observing that federal taxes support all programs of government including the operation of Judge Perry’s court.

Karl was then asked to present his statement to the court, the Judge being very cordial again.

With brevity and simplicity, Karl pointed out that federal taxes (unlike the city and state taxes which he pays) are “overwhelmingly devoted to warfare,” and that during the course of his life between sixty and seventy per cent have gone to pay for military ventures.

In conscience, Karl said, he cannot and must not cooperate with the financing of killing.

As he began to explain how his resistance had always been done openly and publicly, the Judge dramatically changed his tone and manner.

In rapid sequence he interrupted Karl to say that being open is no excuse — “You can openly and publicly rob a bank!” — “this defendant is showing no penitence, this is obviously not a case for probation, and there is no point in wasting anymore time.”

Karl was immediately sentenced to the maximum penalty on both counts (one year, $500), with the sentences to run consecutively, although he might consider making the sentences concurrent if Karl showed a “change of heart.”

The Judge was about to call the next case when an older man, Solomon Goldman, appeared at Karl’s side from the audience, shook his hand, and loudly declared, “Karl Meyer, my grandchildren will thank you.

You are a man of peace.” Judge Perry was astounded; exclaimed to Mr. Goldman “You’re not an attorney!” and ordered him removed from the building.

Then a bit of confusion set in.

The Judge was ordering the marshal also to remove Karl, but the marshal was still involved with Mr. Goldman.

Karl was asking if he could give his briefcase to his friends, was told it could be gotten from the lockup.

Bill Himmelbauer (another convicted W-4 tax resister) was by this time at Karl’s side getting the briefcase, various people were waving two-fingered peace signs to Karl and saying “Goodbye!” as he walked out, and the Judge (whose courtroom was still understaffed) was on his feet shouting “No demonstrations!

There will be no demonstrations in here!

I’ll have you all in jail for contempt.

Clear the courtroom!” as we slowly filed out.

I’ve been informed that Karl will be sent to Sandstone, Minnesota, federal prison, after about two weeks in Cook County Jail in Chicago.

Several friends have seen him already, and report that he’s the same old Karl:

He has put his hand in the fire, and he can stand the heat as well as anyone.

(See Letter Column for Karl’s letter.

The story of his action bears repeating. ―Editor’s comment.)

Karl Meyer’s letter follows:

From Prison

Cook County Jail Chicago, Illinois

Dear Dorothy and C.W. family,

I received a letter from Kathy Bredine telling me of your call, and I was very pleased to receive your message.

Here I am permitted to write and receive mall from anyone, but I will probably be here only a few more days, before “shipment” to a federal “Facility.” There I will have a restricted mailing list; how many names I will not know until I get there; but I have been planning to put you on the list, near the top.

The letters will be for all of you, from A Prisoner.

I hope that you will not be cut from the list for being a single woman and not a relative, even though more than twice my age.

Rules are rules (though I am not sure that that is one of them), and the crime of which I stand convicted is that I claimed a familiar relationship of brotherly responsibility for the very lives of a people not in my own line of genetic descent, at least for several generations, and not even born on the same continent between the St. Lawrence River and the Rio Grande.

I was a little stunned to receive the maximum penalty for that crime, one year on each of two counts, to be served consecutively, plus $1000 in fines, though it is my prudential practice to go into court prepared and expecting to get the maximum.

Nevertheless, I keep forgetting that when these judges see a sheet of convictions as long as mine (however humane the motivations that lie behind it) going back for fourteen years, they can’t seem to see beyond that sheet, and they have a reflexive reaction to go for the maximum.

Of course it is appropriate that I should be the first person to start serving time for claiming exemptions from war taxes on the W-4 Form, since, being a child of Dorothy Day and Ammon Hennacy, it is not my way to conduct guided tours to the jailhouse door and not go in myself.

A number of statements were torn from the context of my writings by the U.S. Attorney to be quoted against me, and he particularly dwelt on that prison aphorism. “If you can’t do the time, don’t commit the crime,” which I have often repeated.

In the light of that reality, I might have done differently myself if I had known the severity of the penalty that would come down on me.

For a person without a family of small children, two years is nothing to speak of; but for people having the care of small children such as my own, William—aged 7, Kristin—aged 4, and Eric—aged 5 months, it is a serious thing for them to be fatherless for such periods of time, I think; that is why we must emphasize that there are practical ways, fully within the range of any ordinary working person, to withdraw financial support from the murder of Vietnamese families without going outside U.S. law and without taking the risks of imprisonment that I hare unfortunately taken.

Now, after a year and a half of widespread experience, we can gauge the response of the federal government to the withholding exemption method of war tax resistance.

Nine people have been prosecuted to date, and a sentencing pattern of one year on each count seems to be emerging.

The withholding exemption method of war tax resistance remains very important and useful for persons who measure the personal risk and decide that it is proper for them to take it.

But, particularly for those of us with families, it will be useful to develop ideas on how we can be true to our deepest convictions about our responsibilities to mankind, without coming into such open confrontation with the laws of the U.S.

Many people have talked with me about working toward conscientious objector provisions under the federal tax laws that would allow war objectors to earmark their social tax assessments for exclusively peaceful purposes.

As to practical effect, such provisions already exist under the tax laws of the U.S.

We need only the generosity and honesty in our ideas to take advantage of them.

For instance, under the present tax laws, a family of five could retain income of $4350 for personal use without having to pay any income tax.

In addition they would be entitled to an itemised deduction from taxable income for up to 50% of their gross income if donated to broad categories of recognized charitable and socially positive purposes.

Thus a family of five could easily have an income of at least $8700, give half of it for peaceful purposes, and legally owe no federal tax on the balance.

This is a general figure that does not take account of many deductions and exemptions that might increase that figure.

Many people feel that it is not possible for a family of five to live decently on $4350 a year in the United States.

Our own family experience, in urban Chicago, one of the higher priced areas of the country, indicates that it is quite reasonable and possible to set a family budget at that level.

The factor which has required us to use a higher income has been our contributions to the support of several other people outside our immediate family, at St. Stephen’s House of Hospitality, whom we could not legally claim as dependents for exemption from taxation.

Over the past three years our personal household has lived on a budget averaging about as follows: rent, including heat—$135 a month; food, clothing and household items—$135; hospitalization insurance—$16; Social Security deductions—$30; public transportation—$23; gas—$3; electricity—$8; phone—$8.

That totals $385 a month, very close to the minimum we are talking about; but we are far from having explored all potentials for less expensive living; our rent is higher than necessary because we live in a desirable location in northern Chicago, one block from the lakefront, and our food budget could be cut somewhat by different and more careful buying methods that we have not taken the time to explore; we could cut our electric bill in half and do without a phone, if necessary.

Yet, I can not describe our life as one of sacrifice or hardship.

Thus I believe that if we are honest about our commitment to a peaceful coexistence with other people and other societies, we must and can learn to live in a way of voluntary simplicity that is compatible with equality among people.

And it isn’t even illegal.

Yours, with a large part of my love.

Karl Meyer — a Prisoner for Peace

P.S. The Bldg. Dept has been after us about the house on Mohawk St., which now stands alone amid vacant lots on all sides where other houses were torn down.

I have found places for two of the three men who remained of our household there; Lemont had to go back to the TB Sanitarium; Roy, who was with us , I have gotten on public aid and found him a decent place in a residential hotel; Richard has been with us but he is able to look after himself.

The building will soon be condemned and torn down.

Frank Marfla, of our Alternative Fund group, will visit the men and look after them while I am in jail.