How you can resist funding the government →

about the IRS and U.S. tax law/policy →

how is tax law/policy/administration changing? →

predictions of future tax policy

Senator Charles Grassley, who chairs the Senate Committee on Finance, on gave a more coherent picture of future tax policy than mortals could glean from Dubya’s rambling press conference:

We should look for as much permanence of previously enacted tax relief measures as possible.

Taxpayers should see no lapse in tax relief.

Continued economic growth depends on that.

We likely will act to extend key tax breaks set to expire at , such as the college tuition deductibility and the low-income savers’ credit.

Both of these are very useful to people trying to live under the tax line — I, for instance, rely on the retirement savings tax credit (what Grassley calls “the low-income savers’ credit”).

I didn’t realize it was scheduled to expire next year.

So I hear that the Democratic party took over Congress , and I was unable to keep myself from thinking of it as good news.

As one wag put it in blogland, it’s the sort of relief you might feel when maggots come to eat out the gangrenous flesh that’s poisoning you.

I didn’t plan to make much of it here, but while the Democrats may not be expected to do anything noble or good, they’re almost certain to do something different.

And for those of us resisting taxes by swinging on the tax law trapeze, that means more uncertainty than usual.

How will tax law change?

The Democrats are promising a wealth of new and expanded tax credits, which sounds good (to us, I mean), except that they’re also promising fiscal responsibility, which presumably means that while they’re giving out these credits with one hand, they’ll be taking back something else with the other — on this, no surprise, they’re less forthcoming.

I’ll let you know what I hear.

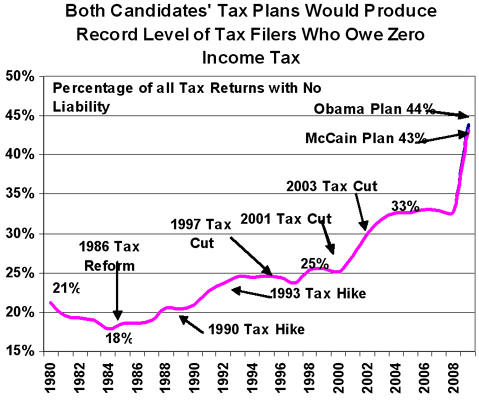

The Tax Foundation puts a lot of effort into tracking down and analyzing those of us in the United States who don’t pay any federal income tax because we’re not liable for any — a group that’s been growing for more than two decades and now includes about a third of American households.

The Foundation, which subscribes to the “Lucky Ducky” interpretation of this phenomenon, sees this as a bad thing.

When they discuss it, they have a tendency to pretend there are no such things as FICA, inflation, excise taxes, corporate taxes, sales taxes and other state taxes, and so forth, and so they will claim that these lucky duckies are “nonpayers” who “have no tax liability” because their “entire tax liability” is “wiped out” by various credits and deductions that legislators use “to funnel money to groups of people they want to reward” who then end up “disconnected from the cost of government.”

The subsequent Wall Street Journal editorial about how awful the government is to the virtuous rich then just about writes itself.

According to the most recent IRS statistics for , some 45.6 million tax filers — one-third of all filers — have no [federal income] tax liability after taking their credits and deductions.…

Tax Foundation estimates show that if all of the Obama tax provisions were enacted in , the number of these “nonpayers” would rise by about 16 million, to 63 million overall [44%].

If all of the McCain tax proposals were enacted in 2009, the number of nonpayers would rise by about 15 million, to a total of 62 million overall [43%].

Of course, all this has to be taken with a big, bumper-sticker-laden grain of salt.

Obama & McCain are promising lots of things, and neither one is likely to be faithful to those promises once it actually comes time to try to push legislation through Congress.

If you put money into a traditional

IRA or

401k, that much of your income is sheltered from taxes — until you retire, and

then you have to include withdrawals from your retirement accounts as

potentially-taxable income.

But if you put money into a Roth

IRA or

401k, it’s the other way around. You pay taxes on the money you earned and put

into the accounts in the year you earn it, but then, when you withdraw from

your Roth accounts in retirement, you get the money tax-free.

At least, that’s how it’s supposed to work. In setting things up this way,

Congress made an implicit promise that the Congresses of the future won’t

change the law to tax all of your Roth money a second time when you withdraw

it. And Congress doesn’t have the power to bind future Congresses like that.

Future Congresses are going to be scrambling to find money to pay off all the

wars, bailouts, benefit programs, and so forth that today’s Congresses are

authorizing but neglecting to fund.

The U.S. Congress

has created a situation in which, after 2010, there may be a significant

number of taxpayers holding an enormous amount of wealth the return on which

they will claim should be permanently exempt from tax. This paper examines

the policy choices available to Congress should it come to regret having

allowed the creation of these tax-prepaid accounts. It focuses first on the

general nature of traditional retirement accounts, and the ways in which

Congress has and could be expected in the future to alter the terms of these

accounts. It concludes that Congress should feel free to change the tax

treatment and other terms of these accounts in ways that might significantly

affect the value of existing accounts, just as it should feel free to change

the tax treatment of any other asset or investment position. It then

considers whether there is anything different about the tax pre-paid

IRAs,

especially those that are converted traditional

IRAs.

It concludes that although the claims of the holders of these accounts are

qualitatively different from the holders of other tax-preferred investments,

they should not be viewed as sufficiently different to render such accounts

immune from any change. Nevertheless, the potential power of these claims

suggests that Congress should avoid creating them in the first place.

The IRS has something called the Federal Payment Levy Program, which is designed to intercept payments coming from the federal government to people who have tax debts.

According to this report, “the bulk of FPLP levy payments have historically been related to Social Security benefits.”

At one point there was a hardship income threshold under which the government would not seize social security benefits to reclaim taxes, but the government phased this out and finally eliminated it at the beginning of .

The Taxpayer Advocate noted that this was further impoverishing some people on fixed-incomes who were already below the poverty line, and proposed a new filter.

The IRS has agreed to implement a “low income filter” that “will exclude taxpayers from the FPLP if their estimated income (based on internal IRS data) is less than 250 percent of the poverty level.”

This change is due to begin in .

The “internal IRS data” the report speaks of here it tries to explain in a footnote:

To compute the taxpayer’s income, where the taxpayer has filed a tax return for the most recent year or two, the IRS will use the greater of the total positive income from that return, or income based on payor documents filed with IRS for that year.

Where no such return was filed, the IRS will use payor documents for the most recent tax year.

To determine family size, which is a component of the federal poverty level computation, the IRS will use the family unit size claimed on the taxpayer’s most recent return filed for the last two years, or if no such return is filed, the IRS will assume a family unit size of one.

Although people with low-incomes may be saved from having their social security seized via FPLP in this way, the IRS may still use other collection techniques.

For instance, they may seize the bank account your social security payment is deposited into, thus saving you from a partial levy only to hit you with a 100% seizure.

Or they may file a “paper levy” to attach 100% of future social security payments until the unpaid tax is collected.

For low-income tax resisters, this will require vigilance.

Still, the Advocate predicts that this change “will protect hundreds of thousands of taxpayers from economic damage and unnecessary interaction with the IRS.”

According to the Advocate, “many of the collection policies and practices in place today have little empirical justification even as they violate the spirit, if not the letter, of the IRS Restructuring and Reform Act of and result in unnecessary harm to taxpayers.

For example, despite the fact that IRS levies and Notice of Federal Tax Lien filings increased by approximately 590 percent and 475 percent, respectively, [see The Picket Line, ], overall inflation-adjusted collection revenue declined by approximately 7.4 percent over the same period.”

The IRS appears to be systematically exaggerating the effectiveness of its collection efforts by attributing any revenue collected during the collection process, even things like subsequent tax refunds being automatically intercepted before they’re sent, as being attributable to the activities of collections personnel.

Also, “[t]here is an astonishing lack of transparency as to what is included in the revenue figures and how they are computed.”

The hardship standards that the IRS uses to determine whether a tax debt is collectible (that is, is there anything to seize, and will seizing it effectively throw the taxpayer onto government assistance, thus robbing Peter to pay Peter) don’t take into account things like credit card debt, school loans, and medical bills.

In many cases, they’re trying to get blood from a stone.

The IRS tends to file official lien notices haphazardly, without much regard for whether they are effective.

Their policy seems to be: when an account reaches a certain threshold of unpaid balance, file a a notice of federal tax lien.

This even though very little collection revenue comes from liens and though a lien notice like this can make it more difficult for delinquent taxpayers to get back on their feet financially.

(These notices make the “secret lien” filed against all delinquent taxpayers part of the public record, available to potential creditors and employers and landlords and such, and put the lien into effect so that the IRS can skim money, for instance if the taxpayer sells property or has accounts receivable.)

Taxpatriatism appears to be rife.

According to the report, “[i]t is estimated that more than seven million American citizens reside abroad.

Although U.S. citizens are required to file U.S. income tax returns regardless of their residency status, IRS data show that only 462,340 taxpayers (or 6.6 percent) filed returns from a foreign address in tax year 2007.”

The “offer in compromise” program — in which people with large tax debts they can’t pay off can enter into an agreement with the government to pay a portion of their debt, comply fully with the tax laws for five years, and have the remainder of their debt forgiven — has become useless for most people.

Now, in order to use this program, you have to pay a fee and submit a substantial down-payment along with your application (which involves “more than 100 steps in a 44-page package”) — and then your application may still be declined.

Weirdly, the IRS processes our 1040 forms before it processes the W-2s and 1099s that substantiate the income we report.

This makes it easy for fraudsters to understate their income and get refunds before the government knows anything is wrong.

“The IRS is experiencing high levels of new individual taxpayer payment delinquencies in categories that could produce high levels of subsequent noncompliance.”

Music to my ears.

Prospects for big tax reform legislation are considered pretty slim, but it can be a good idea to keep track of which tax reform ideas are being taken seriously in Congress, as they sometimes get rolled into other bills as offsetting revenue-raisers or for other reasons, and they may also be part of some future tax reform bill or grand budget compromise.

, Max Baucus, chairman of the Senate Finance Committee, released his tax reform plan.

Among the elements that caught my eye:

“Banks must report the existence of bank accounts, including accounts on which no interest was earned, during the taxable year.”

This helps to confirm a suspicion held by some of us in the war tax resistance community who have noticed that the IRS seems less likely to levy non-interest-bearing accounts, as though it only notices those accounts that it receives 1099-INT reports about.

“The State Department is authorized to revoke passports of individuals with seriously delinquent tax debts in excess of $50,000.” I’ve seen proposals like this floated before that haven’t gone anywhere, but the writing is on the wall: this is definitely a mainstream proposition in the hells of Congress.

The proposal would require more people to file electronically.

For instance, if you have your income tax return done by a professional, that professional would be required to file your return electronically (you would no longer have the option of asking for a printout and filing the paper return).

Software that prints paper returns would have to print the data using a machine-readable barcode in addition to the human-legible form.

You could still file a paper return by filling it out long-hand in the old-school way (that’s what I do).

“The IRS is granted authority to use the Department of Health and Human Services’ National Directory of New Hires to verify employment data.”

Not sure if this might have ramifications for resisters who switch jobs to avoid salary levies.

The proposal calls for reviewing and revamping the system of tax penalties, but has no details about how (instead it requests comments).

Because some penalties aren’t indexed for inflation, usually review-and-revamp means “increase.”

Yesterday I was on a panel concerning “Resisting Taxes in the Trump Era” at the National War Tax Resistance Coordinating Committee’s spring gathering.

Below is a summary of my remarks:

We can no longer reliably extrapolate from long-standing precedent about how the government operates, or how it responds to tax resisters, to anticipate the near future.

While past tax policy changes have been slow, gradual, and predictable, near-future changes are likely to be abrupt, arbitrary, and unstable.

This presents us with new challenges but also new opportunities.

I want to consider five areas the war tax resistance movement in the U.S. should be aware of, observant about, and prepared for.

But it’s too early to draw strong conclusions about any of them:

Changes at the IRS

The possible end of the federal income tax

Expanded government information-sharing

Anti-Trumpery tax resistance

How to resist tariffs

Changes at the IRS

First: the IRS is being significantly degraded and is in disarray.

There have been four acting IRS commissioners already in the first four months of the Trump Administration, serving between four days and six-and-a-half weeks each.

There is no Senate-confirmed commissioner.

In addition there have been thousands of dismissals of probationary IRS employees, and many others have accepted buyout offers to retire early.

Furthermore, the recently-released presidential budget assumes a further 25–50% headcount reduction at the agency.

The enforcement & collection branches have not been spared from this slaughter.

The agency was already on-the-ropes before all this happened.

For years they have lost headcount and their budget has dwindled, even as their responsibilities and the number of taxpayers has increased.

There was briefly some hiring and a budget boost at the agency during Biden’s term, but that hardly had begun to take effect before Trump’s crew came in and eviscerated it.

As a result, we can predict that the already feeble agency will be further incapacitated.

Second: there has been a collapse of the post-Nixon consensus that put a firewall between IRS enforcement and political appointees.

For the last 50 years it would have been considered a serious taboo for the president or one of his political appointees to try to go to the IRS and say “you should audit so-and-so; I think they’re up to something (or: I don’t like them).”

IRS enforcement decisions were firmly in the hands of career IRS employees, not political appointees.

Trump is putting an end to that.

He’s put a political appointee in charge of the IRS Criminal Investigation Division.

He’s being aggressive in using his powers to punish political enemies or to shake down deep-pocketed victims.

We can expect that he will use the IRS in this way, too.

Will this affect American war tax resisters?

Probably not right away.

I don’t think we’re on Trump’s enemies radar, and we’re not attractive shakedown targets.

But if tax resistance becomes a more prominent part of the anti-Trumpery movement, then, yes: expect politically-motivated reprisals.

The possible end of the federal income tax

Trump has repeatedly claimed that he plans to replace the IRS with an “External” Revenue Service, and replace income taxes with tariffs.

Of course, Trump claims a lot of things, and that’s never been a good reason to take those claims seriously.

But there are some other lines of evidence that suggest this may be for real.

Trump’s nominee for IRS Commissioner, Billy Long, when he was in Congress, co-sponsored legislation to abolish the IRS and replace the federal income tax with a sales tax.

This idea of replacing income taxes with consumption taxes has been floating around conservative circles for decades, but hasn’t had enough traction to go anywhere yet.

The “serious people” mostly ignore these proposals as being too onerous to accomplish and too likely to go very badly, but Trump shows strong signs of being willing to do very disruptive things and to not care much if they’ll go badly, so I think we have to consider the possibility.

This is not something Trump could do directly by fiat.

Congress would have to act to eliminate the federal income tax or the Internal Revenue Service.

But potentially Trump could force their hand by 1) unilaterally enacting tariffs, as he can do and has done, and 2) making the IRS so dysfunctional that it can no longer effectively collect income taxes, as he seems to be doing.

At that point, Congress might be faced with a fait accompli and might believe that if it wants to continue to have a budget to spend, it must allow Trump to raise tariffs (or other consumption taxes) to make up for what the IRS is unable to collect.

This is probably not happening right away.

The current Trump budget and tax proposals are for income tax cuts and for cuts to the IRS but not elimination of either.

Where would this leave war tax resisters, who tend to concentrate on the federal income tax as the most important source of war funding?

We would have to retool to resist these new taxes in new ways. (More on this below.)

Expanded information-sharing among federal agencies

A variety of legal firewalls, bureaucratic hurdles, and incompatibilities have prevented federal government agencies from sharing information with each other.

Some of that fell away during the consolidation of the Department of Homeland Security after 9/11.

Now many of the remaining firewalls seem to be dropping to DOGE.

Most news I’ve seen about this is in the immigrant-crackdown context.

For example, the IRS is sharing info from people’s tax returns, and the postal service is sharing information about people’s mailing addresses, to help ICE find immigrants to deport.

Potentially this could make it easier for the IRS to find assets or previously shadowy income.

There’s no sign that this is happening yet, and it would be yet another task for a gutted IRS to try to tackle, so maybe it’s unlikely, but it’s worth keeping on the radar, and we should raise the alarm if anyone notices anything.

Anti-Trumpery tax resistance and war tax resistance

There’s a lot of eagerness among anti-Trumpery activists for some strong, collective action, which could include tax resistance (see for example the National Tax Strike under the Choose Democracy umbrella).

Where does the war tax resistance movement fit in?

Anti-Trumpery tax resistance isn’t “war” tax resistance.

Sure, you can stretch “war” metaphorically to cover deportations, civil liberties collapse, evasion of due process, Constitutional crisis, willful malgovernance, fascism, white supremacy, and so forth, but it’s awkward.

Most of NWTRCC’s outreach and educational material assumes that war and militarism are the focal concern of tax resisters, and to these new resisters this has the potential to be alienating at worst or confusing at best.

Of course, if Trump invades Greenland or Canada or something, then the anti-Trumpery movement will probably develop a strong anti-war focus, and then war tax resistance rhetoric will fit right in.

I suppose we can’t rule that out.

It’s an encouraging sign that the War Tax Resisters Penalty Fund mutual aid program now explicitly welcomes anti-Trumpery tax resisters as well as traditional war tax resisters.

Maybe we can learn from the process they went through as they decided to become more accommodating to a new set of resisters.

Correction: the WTRPF board has since released a statement that says they are not going to extend the fund to cover tax resisters who are not resisting from anti-war motives.

I had based what I said here on a statement from a member of the WTRPF board who apparently misstated the position of the organization.

How to resist tariffs

Trump would seemingly prefer that tariffs permanently make up a predominate portion of federal government income (and therefore military budget income), as they did in the 19th century.

How could war tax resisters continue to resist if this were to come to pass?

Tariffs are taxes that apply to imported goods and that are paid by the U.S. importer.

So you can resist to some extent simply by not importing anything so that you personally do not pay the tax.

But the typical American is going to be paying tariffs indirectly as a consumer of goods whose prices include the costs of tariffs to the importer or manufacturer.

Note that tariffs apply not only to consumer-ready goods (like imported cars) but also to imported raw materials and intermediate manufacturing goods.

For this reason, the prices of many “domestic” products will embed tariffs just as much as do imported ones.

A tax resistance strategy of consuming only “Made in the U.S.A.” domestic goods will not be effective.

Some tactics that might be worth considering if tariffs make up a large amount of military income include:

Smuggling: if tariffs are high, smuggling will become highly profitable and will certainly emerge. We can help nourish that and can redirect our own consumption to smuggled goods.

Domestic manufacture: try to produce and market goods that deliberately and carefully avoid tariffs. Spread awareness about tariff-free goods.

Promote avoidance strategies: there will certainly be loopholes that can be exploited to reduce or eliminate tariffs; we can help importers learn about and use them.

Disrupt the tariff-collection bureaucracy: anything we can do to make the tax collectors’ work more difficult and less efficient will give the Pentagon less to play with.

These tactics (or similar ones) apply also to other consumption taxes that might be in the cards (e.g. a sales tax or use tax).