How you can resist funding the government →

a survey of tactics of historical tax resistance campaigns →

switch to cash →

see also

The National Taxpayer Advocate reports to Congress each year on the state of the tax system and the burden on the taxpayer.

The latest report, released today, includes some tidbits about the underground economy, sources of the tax gap, and unkind enforcement follies like this one:

Criminal Investigation Refund Freezes.

The IRS Criminal Investigation function (CI), through its Questionable Refund Program (QRP), places a “freeze” on hundreds of thousands of refund claims each year that it believes may contain indicia of fraud.

CI personnel currently review the refund claims and “determine” whether they are fraudulent — without notifying taxpayers that their claims are under review and without giving taxpayers an opportunity to present documentation supporting their positions.

, the Taxpayer Advocate Service (TAS) received more than 28,000 requests for assistance from taxpayers whose refunds had been frozen.

TAS studied a randomly selected sample of nearly 500 cases to determine the ultimate disposition of these cases.

When TAS assisted the taxpayers, CI ultimately agreed to issue the full amount of the refund claimed (or more) in 66 percent of the decided cases and to issue a partial refund in an additional 14 percent of the decided cases.

Thus, taxpayers received a full or partial refund in 80 percent of frozen-refund cases brought to TAS.

The median Adjusted Gross Income (AGI) of these taxpayers was $13,330, and the median refund was $3,519. Thus, the refund constituted, on average, more than 26 percent of the claimant’s AGI for the year, and the taxpayers were required to wait, on average, more than 8½ months to receive their refunds.

The National Taxpayer Advocate believes that the QRP is an important program to protect against tax fraud, but the IRS must implement procedures to notify taxpayers that their refunds have been frozen, provide taxpayers with an opportunity to submit documentation, and bring cases to a quicker resolution.

This certainly affects those of us using the DON Method of tax resistance — particularly those of us who rely on getting our refunds before April 15th so we can make an IRA deposit in time to declare it on the previous year’s return.

The report also notes:

The Cash Economy.

Underreported income (and related self-employment tax) from the so-called “cash economy” is probably the single largest component of the “tax gap.”

It may exceed $100 billion per year.

Because income from the cash economy is not subject to information reporting, many of the IRS’s traditional means of enforcement are unlikely to be effective in addressing it.

The IRS has a number of initiatives that could be effective if coordinated and pursued more aggressively.

However, no single function coordinates research, outreach, and compliance initiatives aimed at improving reporting compliance among cash economy participants.

Nor does the IRS give these initiatives the same level of attention as other initiatives, such as those addressing tax shelters or the Earned Income Tax Credit (EITC).

The IRS must develop a comprehensive strategy for addressing the cash economy if it is to significantly reduce the tax gap.

Expanding on this summary, the full report says:

According to the IRS, taxpayers report:

99 percent of the income subject to withholding (e.g., wages),

96 percent of the income subject to third-party information reporting (e.g., interest), and

68 percent of the income not subject to withholding or information reporting (e.g., inventory sales proceeds).

This percentage drops to 20 percent for income earned by certain sole proprietors (called “informal suppliers”) who operate “off the books” on a cash basis in areas such as street vending, door-to-door sales or moonlighting in a trade or profession.…

The IRS has no direct estimate of the portion of the tax gap attributable to the so called “cash economy.”

However, according to IRS estimates:

More than 60 percent of the tax gap is attributable to self-employed individuals.

Eighty percent of the tax gap is attributable to underreporting of tax.

About 43 percent of the tax gap, $134 billion to $155 billion, is attributable to underreporting by self-employed individuals.

Over 80 percent of all individual underreporting is attributable to understated income rather than overstated deductions.

These estimates suggest that self-employed taxpayers who file returns but underreport their income (or self-employment taxes) represent the single largest component of the tax gap, accounting for more than a third of the gap and over $100 billion per year.

Further, the IRS’s estimates may understate the portions of the tax gap attributable to the cash economy because such noncompliance is inherently difficult to detect.

Taxpayers, including the self-employed, primarily underreport income that is not subject to third-party information reporting, i.e., income earned in the cash economy.

Practitioners confirm that the IRS is frequently unable to deter or detect underreporting among cash economy participants.

Research suggests that the cash economy is growing.

According to one estimate the “underground economy,” which includes both the cash economy and illegal activities, increased from four percent of the U.S. Gross National Product in to nine percent in .

A recent study suggests that between nine and 29 percent of the workers in Los Angeles County California are paid in cash and do not have federal or state payroll taxes withheld.

The cash economy may grow even faster as cash transactions move to the Internet.

To address some of this, the Advocate’s office suggests:

Measures to Reduce Noncompliance in the Cash Economy.

The IRS estimates that the annual federal tax gap for was between $257 billion and $298 billion.

The IRS receives about 130 million income tax returns each year.

Thus, every taxpayer is forced to pay an average $2,000 “surtax” each year to subsidize noncompliance.

IRS data show that the highest rate of noncompliance by far is attributable to transactions that are not reported to the IRS on a Form W-2, Form 1099, Schedule K-1, or similar form.

These unreported transactions occur largely in the so-called “cash economy.”

To reduce the tax burden on compliant taxpayers, we recommend that Congress (1) create a three-pronged reporting and payment system that encourages compliance in certain cash economy transactions by (a) instituting backup withholding on payments to taxpayers who have demonstrated “substantial noncompliance”; (b) releasing backup withholding on payments to “substantially noncompliant” taxpayers who have demonstrated “substantial compliance” and agree to schedule and make future estimated tax payments through the IRS Electronic Funds Transfer Payment System (EFTPS); and (c) providing that payors will not be required to institute backup withholding on payments to independent contractors that present payors with a valid IRS “compliance certificate”; (2) require the IRS to promote the making of estimated tax payments through EFTPS; (3) authorize voluntary withholding agreements between independent contractors and service recipients; and (4) require third-party information reporting for certain payments to corporations with 50 or fewer shareholders.

Probably easier said than done, but I wouldn’t be at all surprised to see some moves in this direction.

Another tax-gap source mentioned in the report is misreporting capital gains and losses on the sale of stocks and mutual funds.

Apparently there is no reliable reporting mechanism for the price at which an investor buys such a thing (the “basis”), so when the taxpayer reports the difference between the sale price and the purchase price, the IRS has to either take it on faith or perform a full-scale audit to force the taxpayer to cough up documentation:

Many financial institutions through which investors own stocks and mutual funds (“brokers”) do not currently keep track of an investor’s basis in the stocks or mutual funds, and no brokers report basis information to both taxpayers and the IRS on a Form 1099-B.

The absence of information reporting creates serious problems for many taxpayers and the government alike.

For taxpayers, tracking basis can be extraordinarily complex and many taxpayers seeking to comply with the law find that they simply cannot do so with accuracy, leaving them exposed if audited.

From the government’s perspective, the absence of information reporting enables underreporting by taxpayers who deliberately overstate their basis (thereby reducing their gain or even generating a loss), because they know the IRS generally cannot detect errors in basis reporting in the absence of an audit.

One recent estimate puts the revenue loss to the government from such underreporting at $250 billion over the next 10 years.

A while back, I started looking for examples of ways tax resisters have organized mutual aid pacts to help diffuse the effects of government retaliation.

In the course of doing the research, though, I started collecting examples instead of a larger variety of collective projects resisters and their sympathizers have used in support of tax resistance.

Here are some of the examples I found:

Tax resister “insurance”

For instance, the Breton Association in

France, which organized to “form a common stock or fund… to indemnify the

subscribers for any expense they may be put to by their refusal to pay any

illegal contributions imposed upon the public.”

Another example was the Association

of Real Estate Taxpayers in

Chicago, which formed a cooperative legal fund to fight an offensive legal

battle against the tax.

American war tax resisters today can use the War Tax Resisters Penalty

Fund to defray penalties and interest seized by the

IRS.

The fund is raised as-needed by asking subscribers to contribute an equal

amount.

The oath of the Regulator tax resistance movement in the North Carolina

colony bound its signers to “bear an equal share in paying and making up

[the] loss” if “any of our company be put to expense or under any

confinement.”

Communes, collectives, and co-housing projects.

Some tax resisters have formed mutual support communities.

Whiteway Colony

was founded to try to live up to Tolstoyan ideals. The members of the

Bijou and

Agape communities live below a taxable

income so as to avoid paying taxes.

Supporting resisters as an employer

Some members of the Restored Israel of

Yahweh ran a construction business and agreed not to withhold federal

taxes from the wages of those employees who were fellow-members and who were

resisting taxes.

Vivien Kellems refused to withhold

taxes from her employees’ wages, saying: “They are all free American

citizens, thoroughly capable of performing all of the duties and

responsibilities of citizenship for themselves. And so, from this day, I am

not collecting nor paying their income taxes for them.”

Charles Kanjama recently urged Kenyans

to begin a tax resistance campaign, and said that to foil pay-as-you-earn

withholding, “participating employers and employees can enter into a

voluntary contract to convert monthly employment into quarterly or

half-yearly employment, thus effectively delaying tax liability for several

months.”

British nonconformists and women’s suffrage activists a century ago also

used this tactic. Auctions became rallies, with speeches and banners and

crowds that could number in the thousands. Supporters would pack the auction

house and refuse to leave their seats. On some occasions, violence broke

out. In some cases, auctioneers refused to handle goods that had been seized

for tax refusal.

Simply boycotting the auctions and refusing to buy seized goods is one way

communities offer support. It was part of the Quaker “Discipline” to refuse

to buy seized goods. When Valentine Byler’s horse was seized for non-payment

of the social security tax, “no Amish came to bid on the horses and, due to

a lack of bidders, they went for a good price, with the harnesses ‘thrown

in’ by the auctioneer.”

Pay cash so as not to leave a paper trail

Jessica Ramer and a

Claire

Files contributor brought this idea up. If you pay in cash

whenever you can, you give the recipient the opportunity to decide whether

or not to declare the income.

Cash tips are easy to under-report. I asked about that recently and was

told that most people pay with credit card/debit card and that the

government now uses a percentage method for tips. They look at the charged

meals, look at the number of total meals served, and then look at the

charged tips to figure out how much cash tips you received.

(100 meals served. 50 paid with card, tipping 15%. the government

calculates 15% from 100 meals even if cash tips are only 10%)

You can help out by tipping more when paying with cash or better yet, when

you pay with card, put 1% tip on it and put the rest out as cash. I even

leave a note for the server saying “this is your money, don’t

tell your boss, or the government. share it with the buss boy if that is

the policy.” This will help lower the average tip figures, but

still give the nice server what they have earned.

Use barter to avoid taxable/seizable transactions

Karl Hess found people willing to barter with him as he was dodging

IRS

seizures:

The other day I welded up a fish-smoking rack for a family in Washington,

D.C. It will earn me a year’s supply

of smoked fish. At about the same time, I helped a friend dig a foundation.

He’ll help me lay the concrete blocks for a workshop. Part of my pay for a

lecture at a New England college was the use of the school’s welding shop,

to make some metal sculptures. Three such sculptures have paid my

attorney’s fees in maintaining the tax resistance which is the reason

barter has become such an integral part of my life.

Manufacture and sell goods as alternatives to taxed products

Before the American Revolution, colonists who opposed Britain’s economic

control boycotted British products and began to produce homespun cloth,

alternatives to tea, and so forth. Gandhi’s independence campaign in India

made the wearing and production of homespun cloth central to the opposition,

and the Salt March was focused on the illegal production of untaxed,

non-foreign-monopoly salt.

An example today is home-brewed beer (which beats the excise tax on

alcoholic beverages).

Buycotts and boycotts that favor resisting businesses

One report from World War Ⅰ-era America noted that this was a technique used

by those who opposed the “Liberty Bonds”:

Efforts to prevent banks from handling the bonds have centered chiefly in

Wisconsin, Minnesota, North Dakota, South Dakota, Montana, Missouri and

Oklahoma. The President of a Wisconsin bank has advised the Treasury that

his depositors, mostly Germans, or of German parentage, have withdrawn

many thousands of dollars from his bank because he aided the First Liberty

Loan.

These depositors, he added, had taken their accounts to two rival banks on

the understanding that those banks would not aid the second Liberty Loan.

The two banks, he reported, were not aiding the loan in any way.

Many banks have felt the pressure of German influence in this propaganda,

reports indicate. So pronounced was the movement that the States of

Minnesota, North and South Dakota, and Montana recently decided that they

would withdraw State funds from any bank which did not support the loan.

Social boycotts / shunning / noncooperation with tax collectors

Adolf Hausrath writes of Roman-occupied Judaea,

The people knew how to torment these officials of the Roman customs with

the petty cruelty which ordinary people develop with irreconcilable

persistency, whenever they believe this persistency to be due to their

moral indignation. In consequence of the theocratic scruples about the

duty of paying taxes, the tax-gatherers were declared to be unclean and

half Gentile.… among the Jews the words

“tax-gatherersand sinners,”“tax-gatherers and Gentiles,”“tax-gatherers and harlots,”

“tax-gatherers, murderers and robbers,” and similar insulting

combinations, were not only ready on the tongue and familiar, but were

accepted as theocratically identical in meaning. Thrust out from all

social intercourse, the tax-gatherers became more and more the pariahs of

the Jewish world. With holy horror did the Pharisee sweep past the lost

son of Israel who had sold himself to the Gentile for the vilest purpose,

and avoid the places which his sinful breath contaminated. Their

testimony was not accepted by Jewish tribunals. It was forbidden to sit

at table with them or eat of their bread. But their money-chests

especially were the summary of all uncleanness and the chief object of

pious horror, since their contents consisted of none but unlawful

receipts, and every single coin betokened a breach of some theocratic

regulation. To exchange their money or receive alms from them might

easily put a whole house in the condition of being unclean, and

necessitate many purifications. From these relations of the tax-officials

to the rest of the population, it can be readily understood that only the

refuse of Judaism undertook the office.

A social boycott of tax collectors was practiced in the years before

the American revolution. John Adams wrote:

At Philadelphia, the Heart-and-Hand Fire Company has expelled Mr. Hughes,

the stamp man for that colony. The freemen of Talbot county, in Maryland,

have erected a gibbet before the door of the court-house, twenty feet

high, and have hanged on it the effigies of a stamp informer in chains,

in terrorem till the Stamp Act shall be repealed; and

have resolved, unanimously, to hold in utter contempt and abhorrence

every stamp officer, and every favorer of the Stamp Act, and to

“have no communication with any such person, not even to speak to

him, unless to upbraid him with his baseness.” So triumphant is the

spirit of liberty everywhere.

Harassment of tax collectors was a signature action of the Whiskey

Rebellion. An early published resolution of the rebels read in part:

[W]hereas some men may be found amongst us, so far lost to every sense of

virtue and feeling for the distresses of this country, as to accept

offices for the collection of the duty:

Resolved, therefore, That in future we will consider such persons as

unworthy of our friendship; have no intercourse or dealings with them;

withdraw from them every assistance, and withhold all the comforts of life

which depend upon those duties that as men and fellow citizens we owe to

each other; and upon all occasions treat them with that contempt they

deserve; and that it be, and it is hereby most earnestly recommended to

the people at large to follow the same line of conduct towards them.

Tax collectors were tarred-and-feathered in America, both before and after

the revolution — the violent expulsion of tax collectors was a frequent

technique of the Whiskey rebels. Tax collectors have been the targets of

violent reprisal at many times and in many places. Because of this,

governments have often had to pay high salaries — or, frequently,

percentages of the take — to convince collectors to take on the job, which

only increases the resentment of those being collected from.

During the French Revolution and its aftermath, customs houses were burned

by mobs, tax rolls were destroyed, excise collectors were made to renounce

their jobs and then were run out of town — or in some cases killed.

The first Boer War was triggered when an armed group of Boers seized a

wagon that was being auctioned after it was distrained for resisted taxes.

The Whiskey rebels threatened to destroy the stills of those distillers

who complied in paying the excise tax.

Boycotts / social boycotts of non-resisters

If a tax resisting movement is large enough, it may be able to dissuade

people from paying taxes through boycotts or social boycotts of people

who are tax compliant. In Massachusetts, a group enforced a boycott of

taxed British imports by declaring that

…we further promise and engage, that we will not purchase any goods

of any persons who, preferring their own interest to that of the public,

shall import merchandise from Great Britain, until a general importation

takes place; or of any trader who purchases his goods of such importer:

and that we will hold no intercourse, or connection, or correspondence,

with any person who shall purchase goods of such importer, or retailer;

and we will hold him dishonored, an enemy to the liberties of his country,

and infamous, who shall break this agreement.

Maintain solidarity in the face of divide-and-conquer tactics

In

Germany, the government attempted to break a tax resistance movement by

offering to moderate its enforcement efforts against people who could show

that they had limited means. Karl Marx, who was promoting the resistance at

the time, saw this as a divide-and-conquer tactic:

The intention of the Ministry is only too clear. It wants to divide the

democrats; it wants to make the peasants and workers count themselves as

non-payers owing to lack of means to pay, in order to split them from

those not paying out of regard for legality, and thereby deprive the latter

of the support of the former. But this plan will fail; the people realizes

that it is responsible for solidarity in the refusal to pay taxes, just as

previously it was responsible for solidarity in payment of them.

Keep a record of the “sufferings” of resisters

The Quakers responded to persecution by keeping careful records of

individuals who had suffered thereby. In the archives of Quaker meetings,

you can find lists of people who had resisted militia taxes or tithes for

establishment church ministers, and what property was distrained by which

tax collector.

Sign petitions and public advertisements, engage in public protests

When the American Amish were trying to resist compulsory enrollment in the

social security system, 14,000 of them signed a petition to Congress.

During the Vietnam War, public advertisements were taken out by tax

resisters. In , for instance,

448 writers and editors put a full-page ad in the New

York Post declaring their intention to refuse to pay taxes for the

Vietnam War. The signatories included James Baldwin, Noam Chomsky, Philip K.

Dick, Betty Friedan, Allen Ginsberg, Paul Goodman, Paul Krassner, Norman

Mailer, Henry Miller, Tillie Olsen, Grace Paley, Thomas Pynchon, Susan

Sontag, Benjamin Spock, Gloria Steinem, Norman Thomas, Hunter S. Thompson,

Kurt Vonnegut, and Howard Zinn.

Protests, rallies, pickets, and the like have been a part of many

large-scale tax resistance campaigns.

Hold resisters’ property as an informal trustee

Some resisters who are vulnerable to property seizure find sympathetic

friends who are willing to hold the resisters’ property in their

names as a way of foiling seizure. Some war tax resister

alternative funds function

partially as “warehouse banks” that hold deposits of war tax resisters.

When a frustrated tax collector seized Ammon Hennacy’s protest signs

as he was picketing the

IRS

office — claiming that he planned to auction them off to pay Hennacy’s tax

debt — a friend of Hennacy helped him make new signs, each one marked “this

sign is the personal property of Joseph Craigmyle.”

Keep in contact with resisters and express support

After the press reported that Valentine Byler’s horse had been seized by the

IRS

as he was plowing his field, he got letters of support from all across

the country.

Form groups for mutual support & coordinated decision-making

Here there are too many examples to list.

Give financial aid to evicted rent strikers

When the Irish Land League launched its rent strike, it claimed that

“The funds will be poured out unstintedly to all who may endure

eviction in the course of the struggle. Our exiled brothers in America may

be relied on to contribute, if necessary, as many millions in money as they

have thousands, to starve out the landlords and bring the English tenantry

to its knees.”

Comfort and aid imprisoned resisters

The trick to supporting imprisoned tax resisters is to respect their real

needs and desires. When “someone interfered,” as Thoreau put

it, and paid his taxes in order to spring him from his night in jail, they

thought wrongly that they were doing Thoreau a favor, “for they

thought that my chief desire was to stand the other side of that stone wall.”

Juanita Nelson tells of the support she received in jail, where she had

been taken in her bathrobe from her home. Her supporters took the time to

learn how to support her in a way that was appropriate to her resistance:

Two fellow pacifists, one of them also a tax refuser, had been permitted

to come to me, since I would not go to them. I asked them what was

uppermost in my mind, what they’d do about getting properly dressed?

They said that this was something I would have to settle for myself. I

sensed that they thought it the better part of wisdom and modesty for me

to be dressed for my appearance in court. They were more concerned about

the public relations aspect of getting across the witness than I was. They

were also genuinely concerned, I knew, about making their actions truly

nonviolent, cognizant of the other person’s feelings, attitudes and

readiness. I was shaken enough to concede that I would like to have my

clothes at hand, in case I decided I would feel more at ease in them. The

older visitor, a dignified man with white hair, agreed to go for the

clothes in a taxicab.

They left, and on their heels came another visitor. She had been told that

in permitting her to come up, the officials were treating me with more

courtesy than I was according them. It was her assessment that the chief

deputy was hopeful that someone would be able to hammer some sense into me

and was willing to make concessions in that hope. But he had misjudged

the reliance he might place in her — she was not as critical as the

men. She did not know what she would do, but she thought she might wish to

have the strength and the audacity to carry through in the vein in which I

had started.

And she said. “You know, you look like a female Gandhi in that robe.

You look, well, dignified.”

That was my first encouragement. Everyone else had tended to make me feel

like a fool of the first water, had confirmed fears I already had on that

score. My respect and admiration for Gandhi, though not uncritical, was

deep. And if I in any way resembled him in appearance I was prepared to

try to emulate a more becoming state of mind. I reminded myself, too, that

I had on considerably more than the loincloth in which Gandhi was able to

greet kings and statesmen with ease. I need not be unduly perturbed about

wearing a robe into the presence of his honor.

Support the families of imprisoned resisters

When Gandhi was preparing the groundwork for a tax refusal campaign in

India, he noted that the Indian National Congress “should undertake

to feed the wives and families of those who may be imprisoned.”

Study the law, give legal support

When Elizabeth Cady Stanton was contemplating a tax resistance campaign for

women’s suffrage in the United States, she noted, “One thing is

certain, this course will necessarily involve a good deal of litigation,

and we shall need lawyers of our own sex whose intellects, sharpened by

their interests, shall be quick to discover the loopholes of retreat.”

Combine redirected taxes for dramatic charity giveaways

Larry Rosenwald wrote, of this technique, “To sit on the Grants and

Loans Committee of New England War Tax Resistance, and to dispense the

interest on refused taxes to a youth group in Chelsea, a video for cable

television on United States involvement in Central America, and a

people’s garden in Roxbury is to be reminded of the ideal community,

however blurred and fragmented, that war tax resistance is done on behalf

of, in the hope of helping to make it clear and whole.”

Can you think of any I’ve missed?

Jeffrey Tucker has a good article up at LewRockwell.com about the underground economy.

According to Winchester’s article that I referenced above, self-employed folks report fewer than half of the transactions that aren’t otherwise automatically reported to the government.

In other words, if someone pays them in cash, there’s less than a 50% chance the government will find out about it.

Tucker’s article is about these cash transactions, and how you can frequently get a better deal on goods and services by paying in cash because those you pay know that cash transactions (on which they can evade taxes) are more valuable than transactions that leave a paper trail (and which then get whittled down by the government).

Some recent links from here and there related to tax resistance:

International

Here’s an interview with Tommaso Cerno, who has recently launched a tax strike for gay rights in Italy.

“Only one weapon of resistance remains to us: to evade the state that does not recognize our rights at the only place where it does consider us equal: when we pay taxes.”

Tax resistance plays a role in the anti-bullfighting movement in Galicia, to pressure the government not to allocate public funds to events that feature bullfighting.

The Suepples public employees union in Venezuela, saying that employee salaries have not kept up with tax hikes, made a declaration of tax resistance.

“We aren’t just refusing for the fun of it, we refuse because we’re broke,” said finance secretary Adela Otaiza.

The government is using astronomical inflation to ratchet up taxes and ratchet down public employee wages to make up for drops in oil revenues and a poorly overmanaged socialist economy.

Procedurally Taxing takes a closer look at the new law that allows the government to deny or rescind passports of people with large tax debts.

(My own debt is getting large enough that it may trigger this within a couple of years, so I’m paying close attention.)

This article asks if a bankruptcy that removes or reduces your tax debt is sufficient to also remove the passport restrictions.

Read the comments, too.

The Institute for Justice has scored another victory against IRS civil forfeiture, successfully winning back Ken Quran’s life savings that the agency tried to steal from him.

Cash transactions are harder to tax (or to ban) because they don’t leave as much of a trace.

So governments have begun floating ideas to discourage or eliminate cash.

The latest salvo was a New York Times editorial encouraging the government to eliminate the $100 bill.

Jesse Maceo Vega-Frey recalls his time with Juanita & Wally Nelson, and his own ambivalent experiences with war tax resistance, in an article for the Boston Review.

I stumbled on this quote, shared recently by “tandy_jack” on Instagram, from the back of a Joan Baez album:

We paid the taxes that bought the war that hired the men and dropped the fire that burned the huts and killed the people who then were the bodies that Scott counted.

It’s a rotten thing to brainwash someone into doing the dirty part of the killing while we stay at home.

It’s a rotten thing to pretend the war is coming to an end when it’s only taken to the air.

And in if you don’t fight against a rotten thing you become part of it.

What I’m asking you to do is take some risks.

Stop paying war taxes, refuse the armed forces, organize against the air war, support the strikes and boycotts of farmers, workers, and poor people, analyze the flag salute, give up the nation state, share your money, refuse to hate, be willing to work… in short, sisters and brothers, arm up with love and come from the shadows.

virtual cash

exiled American dissident Edward Snowden made waves recently by promoting tax resistance to the incoming Trump regime

National governments are trying to discourage cash, so as to eliminate the sorts of anonymous, untraceable transactions that are difficult to tax.

For example, the government of India recently made a surprise announcement that 500 and 1,000 rupee notes would no longer be legal tender after a certain deadline.

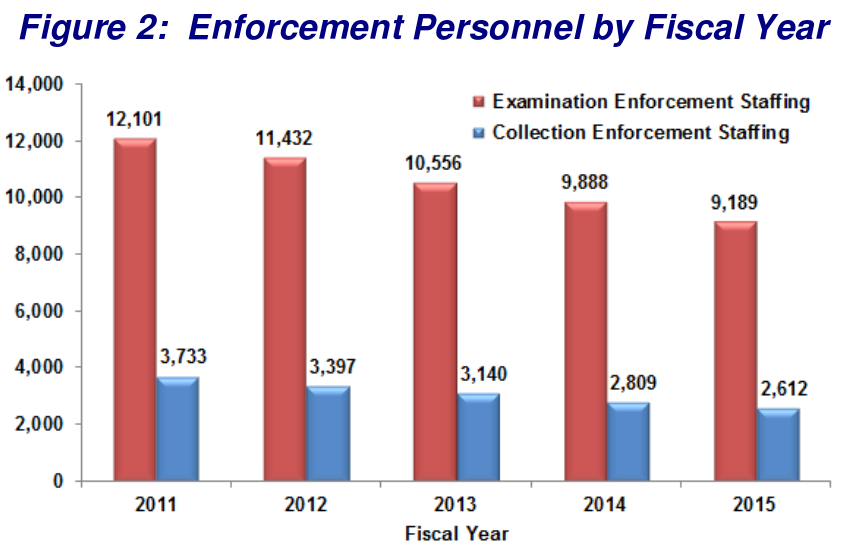

If the IRS does decide to crack down on virtual currencies, it may have to do so with virtual employees, as its real enforcement staff numbers have been dropping year after year:

This article, concerning another TIGTA report, gives a good indication of how strapped the agency is.

Even when shown that there’s money on the table that just needs to be picked up (in this case, high-income people who haven’t filed income tax returns but whom the agency knows about), the IRS complains it doesn’t have enough people to do the picking.

Some links of interest that have flashed by my browser in recent days:

In “I Gave My Waitress a ‘Libertarian Tip’: Taxation Is Theft!” Ed Krayewski considers the tactic of leaving cash “gifts” when paying for restaurant meals with your credit card, rather than adding a “tip” to the bill, as a way of trying to keep the tip from registering as anyone’s taxable income.