Tax resistance in the “Peace Churches” →

Quakers →

20th–21st century Quakers →

Larry & Lisa Kuenning

War tax resistance in the Friends Journal in

There was hardly an issue of the Friends Journal in that did not at least mention war tax resistance, and some issues covered the topic in depth.

In the issue was an article by Scott Benarde about the Quaker community of Monteverde in Costa Rica.

Excerpts:

In , a year after the sentencing [of Marvin Rockwell for draft resistance], Rockwell and the small Quaker community of Fairhope made national news.

In a short article, Time magazine mentioned that “for the first time in history a group of Quakers were planning to leave the U.S. because of their peace-loving convictions.”

Seven Quaker families — including Marvin Rockwell and his parents — twenty-five or thirty people in all, had decided to move to the Central American Republic of Costa Rica.

, Marvin Rockwell recounts why he left the U.S. and what has happened to him since settling 5,000 feet up in the steep, rugged mountains of Costa Rica.

“We had a growing dissatisfaction with what we in Fairhope thought was a military build-up, a wartime economy.

We wanted to be free of paying taxes in a war economy,” Rockwell says in a soft, yet deliberate, voice.

“When the judge sentenced us he said, ‘If you’re not willing to defend your country, you should get out.’

So we began to think seriously of that possibility.”

That issue also brought the news that Quaker Richard Catlett “has been indicted on criminal charges of willful failure to pay income tax for three years” (the indictment was actually for failure to file).

The issue — under the theme “Can the Government Cancel Conscience?”

— had many mentions of war tax resistance.

The opening article, by Ruth Kilpack, began:

Ten years ago, at the height of the Vietnam War, a Friend spoke directly to my condition at Philadelphia Yearly Meeting when he said, “Many of us support our sons’ conscientious objection to serving in the armed forces.

But what about ourselves?

Do those of us who are beyond draft age, or not otherwise subject to the draft, conscientiously object to giving our money for war?”

For me, this struck deep, as did the words, “Two things are needed to fight a war: warm bodies and cold cash.”

For the first, the full flush of youth is required for combat.

For the second, there is no age limit for those who must pay tax funds, over half of which are channeled directly into wars, past, present, and future.

Everyone is involved.

By the payment of taxes, all are required to support the “national defense,” or whatever the current euphemism is.

Kilpack’s article concerned the legal case of Robert Anthony, who was appealing his tax case on religious freedom grounds.

What Bob Anthony’s case was about that day was an effort to break the longstanding precedent set by the case of A.J. Muste, the great peace activist, who in had challenged the U.S. government in the matter of paying taxes for war.

The court had then ruled that the income tax does not interfere with religious practice.

Whatever attempts have been made since that time to break that precedent-and there have been many-have been thwarted, federal judges repeatedly refusing to examine the deep issues involved: the issues of rights of conscience and the First Amendment’s protection of religious belief.

As it turned out, according to Anthony, “the court came up with a complete backing of the government’s right to cancel conscience for the sake of the taxing system.”

The same issue reprinted excerpts from a letter that Media Monthly Meeting had sent to the court that was hearing the Anthony case, in which it said:

As a Meeting, we have consistently backed and encouraged [Anthony’s] position on military taxes.

We believe that any citizen who on the basis of religion or conscience is opposed to paying for armaments or war should not be compelled by the tax laws to pay taxes for these purposes.

Refusal to participate in any way in killing and warfare is a basic principle of the Quaker faith.

…Robert Anthony’s refusal of military taxes constitutes an essential and consistent implementation of Quaker religious principles.… We assert that the free exercise of the Quaker religion entails the avoidance of any participation in war or financial contribution to that part of the national budget used by the military.

In the same issue, Bruce & Ruth Graves wrote of how their war tax resistance had grown out of their conscientious objection to the draft.

[O]ur early married years were largely those of family and professions, years in which we were no longer pressured by government to form external written attestations of belief to satisfy the draft board.

After all, we had done that.

What else could just we two do to alter this evil?

The pacifist ideas could safely rest — or could they?

In retrospect, those beliefs that had been yanked forth from us by society, perhaps too early in our lives, needed more time to mature, to become integrated into our very beings.

Perhaps ten years of integration preceded our realization that a different and subtler written attestation of belief was being required of us by our society.

This attestation was made not once, but every year and it was an attestation of beliefs we did not believe.

It was a lie.

It was our income tax return.

We signed it every year, and thus gave money, without objection, to buy the tools of war, even though we did not believe in killing.

It was subtle because it was money and did not look like death.

But when you put them together, it is a contract.

…All of this occurred during a time when militarism increasingly permeated national policy.

Here, then, we finally reached a point where the idea of our financing the arms race became unbearable.

After all, warfare was becoming more automated, thus relying far more on the expenditure of tax money than on the conscription of lives.

In fact, it now appears that conscientious objection itself may be tending toward irrelevance, unless the concept is expanded beyond the confines of the Selective Service system — especially for those over draft age.

At this point we changed our tax returns into something we could in conscience sign and our remittance checks into contracts for the Internal Revenue Service.

Each year, the item “Foreign Tax Credit” and about fifty percent of our normal tax “due” was entered.

Carrying that credit over to the first page as instructed, we showed each year on our signed returns a credit balance due us from the IRS.

To reduce IRS profit from interest and penalty, we still paid tax “owed” as calculated normally, but our check required the IRS to promise to refund the war tax we claimed by their endorsement because of a restrictive clause we placed on the back of the check.

Rather than our refund, the IRS has usually sent a notice for us to sign, correcting our return.

We have never signed these, because that means agreeing to the original war tax.

Yet the IRS seems to need our agreement to resolve each case legally — that is, unless it should decide to initiate proceedings against us in U.S. Tax Court.

That, in fact, happened to us in for tax year .

From here, the Graveses write about their frustrations with the legal system, which seems eager to latch onto superficial technicalities to avoid having to face head-on the issue of whether the government can force people to violate such core tenets of conscience as “thou shalt not kill” via the tax system.

They also express the need they feel for a stronger and more sustaining national war tax resistance organization:

At present, the community of war tax resistance appears to us to be a loosely-structured communications network of interpersonal contacts, newsletters, and small organizations perhaps not always widely known.

Entrance to this network, we presume, is often gained through need for help by individuals who then grow, gain experience, and are later able to help other newcomers in their various situations.

Whether they do help others or just gradually fade out of the network, however, is crucial to the power of the community.

If we, ourselves, were to fade out as our own tax problems become less immediate, for example, the experience and knowledge we will have gained (even though far from complete) would be lost to the others.

It would seem to be a sad waste to have this process repeated over and again for each member passing through the community.

There are a few organizations emphasizing war tax resistance (e.g., WTR, Peacemakers, etc.), from which a range of handbooks and information is available for individual action.

Some may provide counseling: for example, we have recently learned that CCCO is in liaison currently with the Philadelphia Office of War Tax Resistance (WTR), thus affording the wider range of counseling needed by this more recent form of conscientious objection.

They added:

There are other courses of individual action besides variations on how to fill out a tax return.

One such course is to reduce one’s income to a level of lower — or no — taxation.

For some, this would mean a change in profession, or else a donation of one’s professional services to his or her current employer.

If it is not desirable to put that kind of commitment into that particular employer’s pockets, one can give away up to fifty percent of taxable income to tax deductible organizations, thereby reaching three simultaneous objectives: a) continue one’s profession, b) support human interests of choice, and c) decrease war tax payments.

Tax liability on interest income can also be reduced by buying tax-exempt bonds or shares in exempt bond funds.

Both Individual Retirement Accounts and Deferred Tax Annuities (sometimes available through the employer) enable the postponement of income to retirement years, when, hopefully, the World Peace Tax Fund Act will have become law.

This provides a reasonable chance for legally claiming the exemption on a part of current income, the exempted funds then being redirected to the WPTF Trust Fund for uses more closely aligned with human values.

Also in that issue was an update on the Richard Catlett case, in which he was charged with “willfully and knowingly failing to file income tax returns for ” — he in fact hadn’t filed .

The Brandywine Peace Community wrote in with “some fundamental questions of reality and responsibility” for Quaker taxpayers.

The community ran an alternative fund “comprised of refused war taxes, personal savings, and group deposits, [that] makes interest-free loans to groups working for social change or providing change-oriented services.

Thus, the alternative fund is a small-scale act of beating swords into plowshares and initiating our own peace conversion program.”

Also:

In past January–April tax seasons, the Brandywine group and its supporters have been present at local IRS offices, presenting the option of war tax resistance, and posing the question, “H-bombs or Bread?” with peace tax counseling available.

The issue shared the story of John and Louise Runnings, who…

…have withheld payment of their income taxes in order, as they state, “to resolve the conflict between the spirit that dwells within and the violence implicit in surrendering our substance to the building of the war machine.”

They have submitted a brief to this effect to the Ninth Circuit Court of Appeals.

The Runnings feel that since their action makes them answerable to “those Quakers whose light allows them to pay the federal tax,” they must plead their case before the Society of Friends as well as before the Federal Court.

In doing so, they stress the fact that they share Friends’ testimonies against war but feel that these testimonies will be muted if they are not supported by actions which speak louder than words.

They question how we can “speak truth to power” when so large a part of our income supports that power.

They invite Friends to join them “in taking those uncomfortable actions which put us in conflict with the government rather than with the Spirit.”

That issue also brought the update that Robert Anthony’s appeal to the U.S. Third Circuit Court of Appeals had been rejected.

It also noted that, according to the Albuquerque Monthly Meeting’s newsletter, the Philadelphia Yearly Meeting and the AFSC were contributing to the legal expenses in the case.

At the Philadelphia Yearly Meeting, according to the Journal, “[a] minute on nonpayment of taxes for military purposes was adopted” — but not one that required much explanation, apparently.

A letter from Austin Wattles appeared in the issue in which he encouraged the Journal to continue to cover war tax resistance, saying that to him, “[t]he movement seems to be growing.”

He told of the support he had received from Meetings in his area — specifically the Old Chatham (New York) Monthly Meeting and Worcester (Massachusetts) Meeting.

He concluded:

[T]ax resistance can have its penalties.

You don’t have money to send your kids to college if you change your profession in a way not to pay withholding tax.

I think certainly one reason so few Friends have considered this witness is it can hurt one’s profession so seriously.

It’s not only losing the wages, but Friends enjoy doing a good job where they are working and don’t know how else they can live.

I like Quakers very much.

I’ve always been an active Friend.

But I feel our being part of the world to the degree we are prevents us from following Christ if the price is too high.

Molly Arrison also had a letter in that issue, but she thought war tax resistance “to be a most unrealistic and disrupting idea” because it would lead to a slippery slope of every citizen withholding taxes for whatever items of government spending they disapproved of, leading to “50 million contingencies” that would overwhelm the government’s revenue system.

She recommended that Quakers instead “orchestrate consistent barrages of phone calls, letters, and lectures until the general public has more influence than the Pentagon.”

David Scull considered this same argument in a letter in the issue:

We wish not to pay taxes for what we so strongly disapprove of.

But there are those who equally strongly feel that government contributions to the United Nations, or government money to pay for abortions, violate their principles.

It would not be difficult to compile a long list of purposes objected to; of course we say that our cause is a matter of high principle, but one person’s principle is another’s foible.

Is there some guideline which would make it easier to distinguish between two paramount obligations when they seem to be in conflict, one to support those purposes which our society has determined (no matter how imperfectly) to be for the common good, and the other to obey our consciences?

It seems to me that this can best be judged by our willingness to make some tangible sacrifices on behalf of conscience.

Scull went on to say that this made him skeptical of the World Peace Tax Fund plan: “[I]f I understand it correctly, there is no personal sacrifice involved.

It is just too easy to say to the government, ‘Please send my money where I want it to go instead of where you want it to go.’ ” He suggested improving the World Peace Tax Fund idea by “add[ing] the principle of personal sacrifice”:

Suppose I say, “Instead of $1000 which you say I owe you, here is $1100 as evidence of my sincerity; now will you allocate it in these ways?

That is how much extra I am willing to pay for the privilege of having my money not go to pay for machines of war.”

The inclusion of such a sacrificial element in the WPTF program would make a great deal of difference in my own ability to argue for it, and I think it would make a very convincing argument as we work toward its widespread acceptability.

…When we ask to relieve our consciences because of the way our money is spent, we should be… willing to put a price tag on the privilege.

A letter-to-the-editor in response to Scull’s argument, from Bill Samuel, thought that while the personal-sacrifice angle “has some surface attractiveness…”

Put another way, the proposal amounts to a government tax on conscience, which is quite a different matter from a voluntary personal sacrifice.

Not only is it morally questionable for the government “to put a price tag on” conscience, but some legal authorities believe it would constitute unconstitutional discrimination as well.

The World Peace Tax Fund bill would not be a special privilege.

Rather, the WPTF bill is a practical means of implementing the rights of conscience guaranteed by the First Amendment to the U.S. Constitution.

Like women, blacks and homosexuals, pacifists should take the position that we need not earn our rights but that they should be respected as a matter of course in a free and pluralistic society.

There is, of course, nothing wrong with the concept of people of conscience making a sacrifice for their deeply held beliefs.

Rather than impose a ten percent tax on conscience, concerned Friends might send an amount equal to ten percent of their tax payment to the National Council for a World Peace Tax Fund…

Corporately, Friends can also act to support those working to secure the right of pacifists not to pay for war.

One yearly meeting recently agreed to give $1,500 to the NCWPTF and several monthly meetings include the NCWPTF in their budgets.

Mennonites and Brethren each give a full time volunteer service worker to the NCWPTF.

While Friends do not have the kind of organized volunteer service effort that the other historic peace churches have, meetings can do their part by together contributing enough to support a full-time salaried worker.

Ross Roby also had some words to say about Scull’s argument against the World Peace Tax Fund plan.

He first begged for “immediate self-sacrificial labor and giving, on behalf of passage of a WPTF bill” and then wrote:

I would like to remind those who, like David Scull, have “difficulty with the World Peace Tax Fund as presently offered,” that there is nothing sacred and immutable about the present wording.

We can be quite certain that, when Congress takes a serious scrutiny of provisions for an alternative fund for C.O.s, much rewriting will be done.

The final bill. when passed, may look very different from the WPTF bill as now published.

He suggested that conscientious objectors to military spending should “soft pedal” the arguments amongst themselves over the details of the WPTF plan and instead concentrate on trying to convince the government to enact “a change in the income tax laws that will allow ‘free exercise of religion’ and give us the opportunity to build institutions for nonviolent solutions to international conflict with our present war tax dollars.”

His advice seems to have been followed, and the current campaign for “peace tax fund” legislation seems to have become so unwilling to use critical judgment and so eager to pass legislation of any sort that it has ended up backing a bill that would do nothing to help people with genuine conscientious objection to supporting military spending, nothing to reduce the military budget, and indeed nothing to increase spending on nonviolent conflict resolution — and yet even this bill has gone nowhere in Congress.

Such is the cost of “soft pedaling” internal debate.

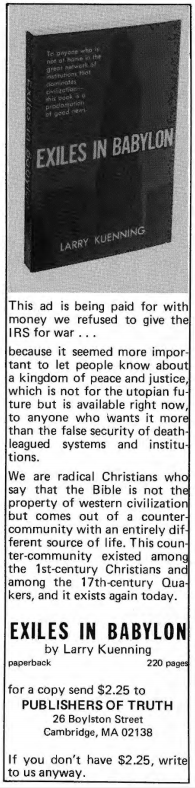

an ad in the issue of Friends Journal

John J. Runnings confronted Molly Arrison’s argument more head-on in the letters-to-the-editor column of the issue.

Excerpt:

Our actions are determined by the degree of urgency we feel.

When our house is on fire we may exit by way of an upstairs window rather than by the conventional route via the stairs.

Many of us see the arms race as a fire out of control, and we are so adverse to feeding the flames that we are prepared to suffer considerable discomfort rather than do so.

So we break the law and are prepared to suffer the penalty.…

To break the law openly and expose oneself to the wrath of the power structure is to witness to the urgency and depth of one’s convictions.…

The early Quakers started at the places that Molly suggests, in the heart and in the community, but they went further.

They broke the law.

And they got themselves hanged and imprisoned; and they were heard above the contending clamors of their day.

And when the Constitution was written it contained provisions for freedom of religion and freedom of speech.

Modern Quakers continue, as of old, to work from the heart and in the community, but if we are to outshout the Pentagon we will have to use a louder and more urgent voice than we have used heretofore.

Perhaps more and more and more of us will have to break the law.

Franklin Zahn also responded to Arrison’s slippery-slope argument: “In practice, the portion of federal income tax for the military is far greater than for any other item.

Currently thirty-six percent goes for present costs and another estimated seventeen percent for past wars.

Objectors to smaller items would not find withholding worth the bother… [W]ords alone eventually lose all effect if no one ever acts.

But if a few other than war objectors choose to refuse, I see no objection to their doing so.”

Sally Primm interviewed Lucy Perkins Carner for the issue.

Among other topics, Carner addressed her war tax resistance:

[Q:] “Did you ever consider not paying part of your tax?”

[A:] “Oh yes, for years I’ve taken out of my income tax payment a portion that the Friends Committee on National Legislation says is equal to what the Pentagon gets.

Then I write a letter to the income tax people.

It’s good propaganda.

I send copies to my representatives in Congress and the President.

“I know my failure to pay isn’t going to impoverish the Pentagon, but it’s good propaganda.

They go to your bank and get the money.

I send them a copy of the letter, too.

Some people have refused to give them the information and go to jail as a result, but I’m not heroic.

They get it out of my bank every year.

“The bank has a right to charge for that, a service charge.

Well, in the last few years, believe it or not, I’ve received a letter from the bank saying they won’t make the charge any more.[”]

[Q:] “Why did they say that?”

[A:] “Well, that just shows you what good propaganda will do.

They know why I’m doing it.”

[Q:] “And how long have you done this?”

[A:] “I don’t know; when I became a pacifist, whenever that was [around the end of World War Ⅰ, according to another part of the article —♇].

I don’t even know when the income tax started.”

The issue covered the “New Call to Peacemaking” in which representatives from the three historic “peace churches” (Quakers, Mennonites, and Brethren) got together to try to put some oomph behind their peacebuilding efforts.

There was actually less about war tax resistance in this article than in much of the mainstream media coverage of the Call — perhaps because the civil disobedience angle was thought to be more newsworthy or attention-catching.

Here is where taxes were mentioned in the Friends Journal coverage:

The Friends Committee on National Legislation points out that all the federal income taxes withheld from your paycheck from January 1 to June 23 go for military purposes.

Not until June 24 do you begin to support any other part of the budget.

Especially in recent years — in light of increasing military budgets and the trend toward fewer soldiers and more expensive weapons systems — many conscientious objectors have chosen to witness against war by refusal to pay voluntarily those federal taxes that will be used to fund present, past, and future wars.

Some have done this by lowering their income below the taxable level; others who owe taxes have refused to pay the portion that would go for the military.

In the same issue, Robert C. Johansen wrote about the challenge of putting forward a pacifist alternative to mainstream political thinking.

In the course of that, he wrote:

Even though their goals are radical in the sense of seeking fundamental system change, political moderates will feel most comfortable using conventional means of education, consciousness-raising, lobbying, campaigning, organizing, and personal witness.

Those people who have tried such means and found them weak and insufficiently penetrating politically will search for other actions, such as tax resistance and civil disobedience, that convey a seriousness and urgency more equivalent to the threat of planetary militarization.

Maynard Shelly gave the Mennonite perspective in the wake of the New Call conference, and claimed that “[r]esistance to the payment of war taxes is becoming the witness of choice for a growing number of Mennonites.”

Charles C. Walker wrote in to the issue to suggest a token $1 resistance to the Pennsylvania state income tax as a way of protesting against its anticipated adoption of capital punishment.

The issue noted in its calendar that the Media Pennsylvania Friends Meetinghouse would be hosting a “National Military Tax Resistance Workshop” that would be “[i]ntroducing the program and services of the newly organized Center on Law and Pacifism.”

War tax resistance in the Friends Journal in

War tax resistance remained very much on the agenda at the Friends Journal at the beginning of the Reagan era of aggressive military build-up in .

A letter from Jenny Duskey in the issue read, in part:

I belong to a community of disciples called Publishers of Truth.

Our testimony is that Christ’s disciples can have no part in war or preparation for war, and that this means not joining the military or being drawn into legally designated “alternatives” to conscription even when the law demands, as well as not paying taxes destined for military use when we can refuse them.

“Publishers of Truth” (see also the advertisement pictured in ♇ ) was centered around Larry and Lisa Kuenning, who came to prophesy an emerging paradise on Earth, centered on Farmington, Maine.

I’m tempted to do some further research in this direction, but am afraid of getting lost in some interesting by-ways.

Lisa Kuenning was a collaborator with Timothy Leary, and for a time an important figure in the psychedelic renaissance.

Last I checked, the Kuennings were running Quaker Heritage Press, which specializes in reprints of old Quaker books.

The issue had an in-depth article by Richard K. MacMaster on Christian Obedience in [American] Revolutionary Times, that included a discussion of Quaker responses to war taxes and militia exemption taxes.

Excerpts:

The Pennsylvania Assembly voted on to recommend to conscientious objectors “that they cheerfully assist in proportion to their abilities, such persons as cannot spend both time and substance in the service of their country without great injury to themselves and families.”

This would be a subsidy to poorer Associators, men who could not supply themselves with a musket and bayonet and needed help from their neighbors.

It was a far cry from the kind of nonpolitical relief work that the sects had in mind.

The Continental Congress did not help matters when it decreed in that members of the Peace Churches should “contribute liberally in this time of universal calamity, to the relief of their distressed brethren.”

Were these distressed brethren the poor of Boston or poor families in their own neighborhood or George Washington’s makeshift army camped on the hills overlooking Boston harbor?

The Peace Churches took the Congressional resolve as a last-minute reprieve and insisted that their contributions were for the poor, even though the money would be turned over to the County Committee.

“For we gave it in good faith for the needy,” a Lancaster County Brethren pastor explained, “and the man to whom we gave it gave us a receipt stating that the money would be used for that purpose.”

The Lancaster County experience was repeated in other Pennsylvania counties and in other colonies where Quakers, Brethren, and Mennonites were numerous.

Most communities tried voluntary contributions, but in Frederick County, Maryland, and Berks County, Pennsylvania, the committees levied fines on men of military age who did not drill with the Associators.

The nonresistant sects had fallen into a trap.

No matter how they labeled them, the authorities understood their voluntary contributions as donations to the war chest.

And if contributions failed to come voluntarily, they were already preparing for compulsory payment of money as an equivalent to military service.

Time was running out on the Peace Churches by .

Soon after the elections, military associators began petitioning the Pennsylvania Assembly that

some decisive Plan should be fallen upon to oblige every Inhabitant of the Province either with his Person or Property to contribute towards the general Cause, and that it should not be left, as at present, to the Inclinations of those professing tender Conscience, but that the Proportion they shall contribute, may be certainly fixed and determined.

These petitions asked much more than an increased tax assessment on the conscientious objectors.

The petitions explicitly stated that every member of the community had an obligation to make some contribution to the common cause; the additional tax would be a concession to those who could not meet that obligation on the field of battle.

The Peace Churches rightly put their case on the high ground of religious freedom.

Quakers expressed their “Concern on the Endeavours used to induce you to enter into Measures so manifestly repugnant to the Laws and Charter of this Province, and which, if enforced, must subvert that most essential of all Privileges, Liberty of Conscience.”

They asked the Assembly not to infringe the solemn assurance given them in Penn’s Charter, “that we shall not be obliged ‘to do or suffer any Act or Thing contrary to our religious Persuasion.’ ”

The revolutionary government rose to the challenge.

All sixty-six members of the Philadelphia Committee proceeded in a body to the Assembly chamber to present their response to the Quaker address to the Speaker of the House.

The same day, the Assembly heard petitions from the Officers of the Military Association of the City and Liberties of Philadelphia and from a Committee of Privates.

They first narrowly construed the grant of religious freedom in the Charter and threw out of court the sectarian contention that religion was more than a Sunday worship service.

We cannot alter the Opinion we have ever held with Regard to those parts of the Charier quoted by the Addressors, that they relate only to an Exemption from any Acts of Uniformity in Worship, and from paying towards the Support of other religious Establishments, than those to which the Inhabitants of this Province respectively belong.

The representation from the Committee of Privates went still further.

They insisted that “Those who believe the Scriptures must acknowledge that Civil Government is of divine Institution, and the Support of it enjoined to Christians.”

Quakers ought not to question what governments did, according to this Committee of Privates, but simply obey; God had ordained the powers and thereby gave sanction to every action of the state.

The lines were thus clearly drawn between the sectarian view of supremacy of conscience and the secular view of the primacy of the state.

The Mennonites and Church of the Brethren simply set down the limits of what they could do in good conscience.

Their petition made little difference to the course of events.

The day after the Mennonite and Brethren statement was read the Pennsylvania Assembly voted to require everyone of military age who would not drill with the Associators “to contribute an Equivalent to the time spent by the Associators in acquiring the military Discipline.”

Later in , the Assembly imposed a tax of two pounds and ten shillings on non-Associators, which would be remitted for those who joined a military unit.

Under new pressure from the Associators they raised the tax to three pounds and ten shillings in .

The Pennsylvania Constitutional Convention incorporated the principle of taxing conscientious objectors as an equivalent to military service in the Declaration of Rights they adopted.

It made explicit what most Patriots already believed:

That every Member of Society hath a right to be protected in the Enjoyment of Life, Liberty and property and therefore is bound to Contribute his proportion towards the Expence of that protection and yield his personal Service when necessary or an equivalent… Nor can any Man who is conscientiously scrupulous of bearing Arms be justly compelled thereto if he will pay such equivalent.

Participation in warfare was a universal obligation, in their view, falling equally on every citizen; those who could not fight must pay others to fight in their place.…

The Assembly and the Convention clearly intended to make the Peace Churches pay for war and imposed the tax as an avowed equivalent to military service.… Religious pacifists carried the whole burden of the tax.

But a tax imposed on conscientious objectors as an equivalent to joining the army and intended for the military budget definitely infringed on the religious liberty guaranteed by William Penn’s Charter.

The war tax issue thus arose in a context of freedom of conscience curtailed for those whose Christian faith forbade their “giving, or doing, or assisting in any Thing by which Men’s Lives are destroyed or hurt.”

Maryland and North Carolina followed Pennsylvania’s example in levying a special tax on conscientious objectors; the North Carolina law made payment the grounds for exemption from actual service with the army.

Virginia and several other states required conscientious objectors to hire substitutes to take their place whenever their company of militia was drafted for combat duty.

Special tax assessments for military purposes passed every state legislature as the war dragged on.

And the rapidly depreciating Continental and state paper money that fueled a run-away inflation was itself a war tax.

Wherever Quakers, Mennonites, or Brethren lived, the problem of paying for war soon caught up with them

Could a valid distinction be made between military service and war taxes?

The Reverend John Carmichael, Scottish Presbyterian pastor in Chester County, Pennsylvania, had little sympathy with the nonresistant sects who refused to pay war taxes, but he saw no distinction between fighting and paying the cost of war.

In Rom 13, from the beginning, to the 7th verse, we are instructed at large the duty we owe to civil government, but if it was unlawful and anti-Christian, or anti-scriptural to support war, it would be unlawful to pay taxes; if it is unlawful to go to war, it is unlawful to pay another to do it, or to go do it.

Some Brethren, Mennonites, and Quakers agreed that no real distinction could be made and consequently refused to pay taxes levied for military purposes.

In his sermon, Carmichael spoke of Mennonites “who for the reasons already mentioned will not pay their taxes, and yet let others come and take their money, where they can find it, and be sure they will leave it where they can find it handily.”

They would not resist the tax collector in any way; but they could not cooperate in wrongdoing by voluntarily paying war taxes.

The law took this practice into account and permitted collectors to seize the property of those would not pay their own taxes.

Quakers officially discouraged payment of war taxes and militia fines.

Many Friends went to jail for their refusal and still a larger number allowed the authorities to take horses, cattle, furniture, farm implements and tools to pay their taxes.

They refused to accept any money from the sale of their goods over and above the tax and fine.

In the Shenandoah Valley and in other Quaker communities, their neighbors found rare bargains when the sheriff sold a Quaker farmer’s property for taxes and purposely kept the bidding low.

Virginia Yearly Meeting protested to the authorities about the sale of slaves, freed by their Quaker masters in defiance of the law, who were taken up and sold to pay their former masters’ war taxes.

Refusal to pay taxes for military purposes had a close parallel in Quaker refusal to pay taxes to support an established Church; they accepted the right of civil government to appropriate money for either purpose, but denied that civil government could coerce their consciences, even at the cost of jail sentences.

This was a minority position among English and American Friends, even after John Woolman prodded their conscience on war taxes.

Woolman’s influence can be seen in a circular letter issued by Philadelphia Yearly Meeting in , when Braddock’s defeat left Pennsylvania exposed to French and Indian raids and the Assembly ordered new taxes for mounting a fresh campaign.

The tax was a general one, including military appropriations with all the other functions of civil governments, but Friends agreed “as we cannot be concerned in wars and fightings, so neither ought we to contribute thereto by paying the tax directed by the said act, though suffering be the consequence of our refusal.”

The issue in was much clearer: the taxes were levied entirely for military purposes and intended as an equivalent to military service.

With the passage of years, Friends had the meaning of nonresistance in much sharper focus and a much greater number accepted the challenge of faithful discipleship.

Mennonites also responded to the challenge by refusing to pay war taxes.

When the Pennsylvania Assembly passed an act in to require a tax of three pounds and ten shillings from everyone of military age who refused to turn out with the militia, Mennonite opinion was divided.

Christian Funk, bishop in the Franconia congregation, allowed payment of the tax and tried to convince his brother ministers.

But refusal to pay war taxes had taken deep roots in the Mennonite tradition by .

The mere rumor that Funk permitted payment of the tax was enough to bring complaints against him at the time of preparation for the Lord’s Supper in and to lead to his ouster from the ministry.

All of the preachers and a great many other Mennonites in eastern Pennsylvania opposed payment of the tax.

Andrew Ziegler, bishop in the Skippack congregation, spoke for them, when he declared: “I would as soon go into the war, as to pay the three pounds ten shillings if I were not concerned for my life.”

Zeigler and others could see little difference between fighting and paying for war.

In the face of a long-standing tradition of paying taxes without questioning the purpose of the tax, men of faith testified from their own conscience that for them there could be no distinction between refusing to fight and refusing to pay for war.

These Mennonites, Brethren, and Quakers willingly accepted the penalty for their conscientious objection to war taxes in imprisonment and loss of property far in excess of the tax.

Their action reminded their brethren of the need for careful discrimination in rendering to Caesar the things that are really Caesar’s. They refused to let a majority vote in the legislature be their conscience and rejected the easy way of confusing Caesar’s will with the will of God.

In the same issue, Bill Durland of the Center on Law and Pacifism reviewed the attempts to get a sympathetic court hearing in the United States for the argument that conscientious objection to military taxation is a Constitutionally-protected right of citizens.

He described the founding of the Center in by himself, Robert Anthony, Bruce & Ruth Graves, Barbara & Howard Lull, Peter Herby, and Richard McSorley, and then described the various avenues of appeal the group was pursuing in the U.S. Supreme Court.

Anthony put his legal argument this way: to be compelled to pay war taxes “would force [him] to accept a creed, and practice a form of worship foreign to his convictions, and to establish as the only normative religious belief and practice, that adhered to by most Christian denominations, i.e., that it is both a Christian and an American duty to fight in just wars and pay for them.”

The Supreme Court wasn’t interested.

The Center tried again with the Graves’ case, asserting that the First Amendment’s assertion that “Congress shall make no law… prohibiting the free exercise [of religion]” means that the governmental interest in having an efficient and uncomplicated tax system is trumped by the citizen’s right to a religious practice that forbids funding war.

Again, the Supreme Court turned up its nose.

The Center then made an attempt with the Lulls & Peter Herby as petitioners.

As the First Amendment arguments had failed to make any headway, this time they made a Hail Mary pass with a Ninth Amendment argument.

“This amendment recognizes that there are certain fundamental, inalienable rights not enumerated in the Constitution which the people possess that are preexisting to any constitution, are inherent in the individual, and are not subject to divestment either partially or completely by the state.

These rights have also been called ‘natural’ and are those held by an individual in a state of absolute liberty.

In contracting to enter into a state of society, the people collectively, and the person individually, only divest themselves of those natural rights which they expressly relinquish by enumeration.”

Nice try, but the Supreme Court yet again denied cert.

The article notes that in addition to First Amendment-based arguments, “each of the three cases raised at the Federal Court level a compelling legal position based on International Law and, in particular, the Nuremberg Principles.”

(Not compelling enough, apparently.)

An article in the same issue, by William Strong, profiles war tax resister Bruce Chrisman.

Excerpts:

[H]e cannot pay that portion of his federal taxes that he knows will be used for preparations for war.

For that, he is serving a criminal sentence that includes one year of humanitarian service without pay, three years of probation, a fine of $2,400 for court costs, and the payment of all back taxes due.

He deems this result a moral victory, however — the sentence could have been up to one year in prison and a $10,000 fine.

Over the years Philadelphia Yearly Meeting’s minutes have reflected the repeated return of the war tax concern.

In a striking, sensitive minute was approved.

The unity reached at that time calls upon “all Friends to continue to search themselves deeply on their responsibility to separate themselves from preparations for war.”

Where does that searching lead?

“We encourage dialogue between conscientious war tax refusers and other concerned people struggling with the issue of paying war taxes.

We seek to build a community of deeply committed persons.”

Friends offer their real support — spiritual, moral, legal, and material — to that growing community, and close the minute by reaffirming:

Our strength and our security are derived from our belief in the reality of a loving God and the oneness of that of God in all people.

In order to say yes to this belief, we must seriously consider saying no to payment of war taxes.

Philadelphia Yearly Meeting’s “War Tax Concerns Support Committee” works to carry out that minute.

Its mandate is broad, from war tax refusal and resistance, questing for administrative (IRS) and judicial relief, to a spectrum of wholly positive approaches.

The committee seeks “legislative relief” in pursuing the World Peace Tax Fund law that proposes alternative service for war taxes, for conscientious objectors to monetary conscription.

In the war tax concerns section of our Peace Testimony, as in most fields of Quaker endeavor, certain Friends are ’way out front.

They have been going down a committed road for years.

George and Lillian Willoughby, Bob Anthony, Lorraine Cleveland, and Robin Harper in Philadelphia Yearly Meeting come to mind.

“Not to worry” — most of us are beginners, and we don’t need to catch up.

What stride do we take this year — or this quarter — in the Light? We tackle the big issues by taking the next step, getting a bit more involved.

Saying “no” to that small, lingering, now two percent Vietnam War telephone tax, which does indeed produce a billion dollars in direct war taxes, is one such step.

Adjusting our withholding so that we take more control of our tax payments, with more options, is another.

Or do we match what the government requires of us in war taxes with comparable contributions to peace organizations?

Everyone ultimately decides his own next step, but often it comes out of shared, caring discussion with other Friends, “wrestling as I am, with the harder questions of our faith and practice.”

That issue also had a few short notes that mentioned war tax resistance:

“In Japan, COMIT (Conscientious Objection to Military Tax) is planning to sue the government for breach of constitution by taxing for war.”

“In Switzerland, 300 people belonging to the group ‘Pour une Politique de Paix Active’ refused to pay their military tax or some part of the duty levied for national defense.”

“[N]ine members of the Pacific Yearly Meeting Peace Committee testified ‘against rendering unto Caesar that which is God’s’ by declaring their solidarity with those Friends who refuse to cooperate with war taxes and draft registration.

Some seventeen others present at the yearly meeting also signed the statement.”

“A statement from Orange County Meeting asks: ‘If we recognize our involvement in militarism through the payment of taxes used for military purposes but do not act to end such involvement, then are we not hypocritical to tell Friends faced with registration to refuse military service?’ ”

The issue included a mention that the Australian Yearly Meeting was pursuing its own Peace Tax Fund plan “as a method of allowing taxpayers to direct a proportion of their tax to peace purposes instead of military spending.”

The issue noted that a “Historic Peace Church Task Force on Taxes is preparing a packet of study materials to provide information on the biblical basis of war taxes and the World Peace Tax Fund… together with suggestions for personal and political action.”

Maurice McCracken wrote in to the issue to chide anti-war activists for their timidity.

Excerpts:

Indeed it is a feeble gesture to do what we do not believe in; even though we protest doing it.

The only valid protest is resistance and complete noncooperation with what we believe to be wrong.

[A] law… threatens anyone who advises a young man not to register for the draft with the same penalty as the non-registrant — a possible prison sentence of five years and a possible fine of $5,000. In the draft registration resistance movement I find that considerable time is spent on how to counsel young men about registration so it will not appear that we are actually advising them not to register.

Why this hesitancy and timidity?

I not only advise young men of draft age not to register.

I urge them not to register.

This military juggernaut which threatens to destroy all human life and all animal and plant life on the planet must be stopped.

It must be resisted at the point of not filing a federal income tax return and of not registering for the draft.

A thief-says, “Your money or your life.”

The Pentagon says, “Your money and your life!”

I refuse to give either one!

Won’t you join me?

In the issue, E. Raymond Wilson tried to envision a “Quaker Peace Program” that would be adequate to the challenges of .

He advocated working toward a more powerful U.N., drastic disarmament, global economic/social development with an emphasis on underdeveloped areas, and active reconciliation of global adversaries.

Much of this work would involve lobbying and other pleading with powerful people whose inclinations are largely in the opposite direction; but there was also a nod toward conscientious objection:

an ad in the issue of Friends Journal

Friends should seriously consider the recommendations of the Second New Call to Peacemaking Conference that individuals should withhold all or part of their income tax going to military and war appropriations, now estimated at more than forty-eight percent of the budget controlled by Congress.

War tax resistance came up at the Philadelphia Yearly Meeting in .

War tax resister John Beer wrote down some questions that people had about resisting, and in a Friends Journal issue , Bill Strong (of the Meeting’s “War Tax Concerns Support Committee”) answered them.

The questions were:

“If we refuse $100 of our federal war taxes and give it to some organization working for peace, what steps will the IRS take?”

“What options do we have in dealing with the IRS actions?”

“Is the initial letter we send with our tax return, stating the reasons for our tax refusal, important in terms of the subsequent legal proceedings?”

“Should we get help from a lawyer or tax refusal group in composing the letter?”

“What kind of advice can you provide which will allow us to profit from the experience of those who are already refusing to pay war taxes?”

“What happens to persons who refuse war taxes year after year?”

Some excerpts from the answers give a window into how war tax resistance was practiced by Quakers and by Meetings:

Both at Celo (NC) Meeting and at Central Philadelphia Meeting members asked others to share their examination or audit with IRS agents.

The first was in the refusers’ home, the latter in a federal office building.…

One Friend has been refusing for 23 years.

His witness continues and collection is still in the future, so much of the obligations of the early years have lapsed.

Another Friend, whose refusal goes back even further, has had the funds due taken at irregular intervals from her checking account.

A report in the issue noted that the Lake Erie Yearly Meeting in had “considered a minute on war tax concerns” based on queries from the New Call to Peacemaking Conference:

“If we believe that fighting war is wrong, does it not follow that paying for war is wrong?

If we urge resistance to the draft, should we not also resist the conscription of our material resources?”

The minute concluded: “We reassert the historic peace witness of the Society of Friends.

We commit ourselves to wrestle with the contradictions between our testimony and our government’s tax regulations.

To continue quiet payment for war preparations is to the conditions for war.”

Each meeting was urged to appoint a representative to the World Peace Tax Fund.

Finally, the issue brought a meditation on “the peaceable kingdom” by Susan Furry.

She believed that the Kingdom of God, the peaceable commonwealth, was “at hand” as Jesus said it was, and that it was the duty of Christians to “begin to live there.”

She reflected on how she came to include war tax resistance in her vision of how to carry this out:

an ad in the issue of Friends Journal

…I felt that I had to begin to look into the question of war tax resistance.

This led to a long period of study and self-examination.

To me, becoming a war tax resister meant making a final commitment to pacifism, and I didn’t do it lightly.

It took a lot of prayer and thought and the help and support of many people in my meeting to bring me to a point of clearness, where I know, solidly and comfortably, that this action is right for me.

Since then I have found myself being led not only to resist war taxes for myself but also to speak about it to others and to offer counsel and support to those who are considering this action.

I have helped prepare a packet called “Quakers and War Taxes” which is on sale at my meeting and have been involved in setting up the New England Friends Peace Tax Fund, an escrow fund for tax resisters under the care of my yearly meeting: I’ve been given a lot of encouragement to continue and to grow in my tax resistance activities through the support of others in my meeting, many of whom are not tax resisters themselves but friends who recognize that it is the right thing for me to do.

I’ve found that obedience to the divine leading I have felt in this matter has brought me closer to God, has given me new courage, and has opened me to further leadings.

In practical terms, war tax resistance seems to be a futile, irrational, and perhaps risky undertaking.

I think by now I’ve probably heard all the possible arguments against it.

The only answer I can really give is, “This is something I must do, to be faithful to my conscience and my understanding of God’s will.”

For it is part of the foolishness of God, which is wiser than human wisdom, as Paul tells us in First Corinthians.

It requires me to acknowledge my dependence on God’s guidance and strength.

I don’t know where my action will lead in practical terms, but I trust God to make use of it; I don’t know what the consequences will be for me personally, but I trust God to help me to face them.

In one way or another, perhaps, peacemaking may bring all of us to that place of acknowledging our dependence on God.

For me it has come through tax resistance.

For another it may come through the old dilemma about Hitler or through an experience of physical violence on the street.

In any case one comes to a place where one has to say, “I don’t know what will happen, but I place my trust in the God of love and accept the consequences.”

In coming to rely on God more, I have begun to learn that God really is dependable.

I have felt God working through the beautiful support I have received from many individuals and from my meeting.

I’ve been to tax court twice and was sustained by a powerful sense of God’s presence.

I’ve faced the certainty of financial loss and found that it doesn’t trouble me as much as I feared it would.

However, I still worry about the future; I haven’t reached the point where I can really leave it all in God’s hands.

Sometimes I even wonder about going to jail.

Right now the government isn’t prosecuting many war tax resisters, but it is always a possibility.

My actions are not very unusual; there are over forty war tax resisters in my meeting alone and many more in New England.

I know many people who have sacrificed more and taken greater risks for peace than I have.

But I have learned that when you follow God one step down the road, God usually asks you to take another step.

Who knows what God may ask of me in the future?

I have friends who have gone to jail for conscience’ sake, and I wonder if I could face that if it came to me.

My action in refusing to voluntarily pay taxes for war is largely symbolic — like the early Christians who refused to put a pinch of incense on Caesar’s altar.

Is it worth the risk to make a symbolic gesture?

Such questions take me back to the Christian roots of my faith.

I know that my way of thinking about these things and the language I use do not work for everybody, but these are the symbols which make sense to me, so I must use them.