Tax resistance in the “Peace Churches” →

Mennonites / Amish →

Robert E. Dickinson

War tax resistance in the Friends Journal in

By , references to war tax resistance in the Friends Journal had become more casual and matter-of-fact, but also less urgent and less thorough.

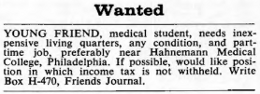

ad in the Friends Journal

In the issue, the pseudonymous history columnist for the Journal, “Now and Then,” examined the tradition of tax and tithe resistance in the Society of Friends:

Render Unto Caesar

For some years Friends have been aware of an anomaly in their traditional response to military requisitions.

When they have been conscripted for military service, they have officially and in large numbers refused to go.

Many governments have made provision for this expression of conscience.

This has taken the form of allowing the payment for a substitute by the conscript, or some form of alternative service.

Many Friends have accepted the latter.

But when our money is demanded, particularly as part of a more general tax, although we know its ultimate purpose is for war, only sporadically have Friends objected.

Without recounting again all the data in our history in this matter, I inquire here why this curious contradictory situation has come to exist.

Young men stubbornly refuse actual direct participation in war and do so with the sympathy of their parents, but the latter usually have contributed in money to the very cause to which their sons refused to contribute their bodies.

And governments have usually provided no alternative to military payments.

A recent Yearly Meeting memorandum lists several of the reasons (excuses?) why Friends have abstained from refusing war taxes.

Many of these reasons simply are practical considerations.

But the first one on the list is the gospel phrase: “Render unto Caesar…”

The context of these words of Jesus is precisely that of a general Federal tax.

They are therefore not taken out of context when applied to modern Federal taxation.

Compared with them, there is nothing in the Gospels so explicitly quotable for or against military service.

In former times… as well as today, this text has been repeatedly referred to by Friends in extenuation of their complicity by means of tax payment in the waging of war.

Why is this?

Does it mean that Friends follow Jesus most readily when he seems to have left specific instructions, while where he is less specific they arrive at the stance of war resister in spite of this contrast?

Undoubtedly, elsewhere in Quakerism we see evidence of Biblical literalism alongside of an almost contradictory dependence on the Spirit.

Or is the contrast between submitting to war taxes and refusal of war service due to the fact that the latter problem for a long time rarely arose, at least in England?

While militia dues were refused as early as , compulsory military service scarcely began there until our own time.

Another Quaker financial refusal was early and widespread.

That was of tithes levied on agricultural produce for “priests’ wages.”

No single ground of resistance and persecution was so durable in our history.

The money was for support of the official “hireling” ministers.

Why was tax money to support war-making not equally obnoxious?

I wonder whether today “Render unto Caesar” can, as a saying of Jesus, bear the weight that we give it when without twinge of conscience we pay taxes of which so large a share finances war.

At one time Friends — or at least some Friends — did refuse taxes levied exclusively for war costs.

They distinguished them from what they called “mixed taxes.”

It is not like Jesus to legislate on explicit social problems — and if he did, are we to take his words as rules for our own late generation?

His followers did not always or in other respects blindly obey the government.

When Caesar ordered pagan sacrifice in the following centuries, Christians would not offer even the token pinch of incense.

In those days, Christians also refused participation in war.

Under some circumstances, obedience to “the powers that be” seemed commendable; under others, Christians knew they must obey God rather than man.

Indeed, neither historical scholarship nor grammar leaves the intention of the Gospel saying quite so sweeping in its bearing.

According to Luke, Jesus was accused of forbidding to give tribute to Caesar.

Some modern students of the Gospels suspect that behind their present portrait lies a much more politically nonconformist Jewish subject of Rome.

The saying I quoted ends “…and unto God the things that are God’s.” Was not this the real thrust of original injunction?

Perhaps Jesus never really answered the question, “Is it lawful to give tribute to Caesar or not?

Shall we give or shall we not give?”

And the apparent command to give tribute to Caesar may be only an analogy or a conditional clause, vindicating the major obedience — obedience to God.

In the same issue, David Nagle wrote in with his own lesson from history.

He brought up the case of Joshua Maule, who at the time of the American Civil War was resisting a tax that was very similar to the recently-enacted Vietnam War income tax surcharge.

Maule had written:

On this ground [the Scriptures] we believe the testimony stands and our discipline is established, which is clear against “paying taxes for the express purpose of war.”

For war destroys that which is God’s, and invades the things which have not been committed to Caesar.

And when the civil government commands us to co-operate in this work, either by personal service or payment of money for that express purpose, if we render unto God the things that are His, we should decline all voluntary payment of money demanded for the direct support of war, and be willing to suffer and bear whatever may be permitted to come upon us; rendering ourselves into the hands of the Lord, and trusting in him.

Nagle wrote: “I was impressed by the resemblance of this situation to ours today.

The only significant difference seems to be that in the backsliders were in the minority and today few Friends have the courage to refuse to pay a tax intended expressly for the war effort, such as the present ten percent surtax.

I ask that Friends give this concern the solemn consideration it deserves and seek the will of the Lord in regard to future actions.”

Also in that issue, Robert E. Dickinson wrote a curious piece, accompanied by photos, on “My Tax Refusal Furniture” — “a set of furnishings that easily could be moved or disposed of” that Dickinson designed and built after he was served an IRS seizure notice for “my property, including my furniture.”

When the authorities are at the door, the furniture can be demounted to flat slabs of plywood for ease in moving and storage.

The issue quoted from a statement issued by Hanover Monthly Meeting when it decided to start resisting the phone tax — “with regret but under compulsion of conscience” — and from statements issued by Alura and Donald Dodd, who had decided to pay their taxes into an escrow account rather than to the federal government.

In the issue, in an article mostly devoted to the Christian obligation of tithing, the issue of tax resistance sneaked in:

I suspect that the observance of tithing has fallen off partially as a result of the churches’ betrayal of their own stewardship.

They have diverted to the needs of their own buildings and grounds that which should have been held in trust for all.

They have faithfully received and have paid into the storehouses (or banks) but have stood guard to make sure that nothing but the interest flowed out.

They have tied strings to their giving, withholding from those who do not meet with their approval and forgetting that God, whose stewards they should be, causes the rain to fall upon the just and the unjust alike.

Tithes, it seems to me, should not be given or withheld in an effort to bring pressure upon God or to coerce the workings of the Spirit.

If we have lost faith that our own religious body is not administering its trust with true compassion for our troubled world, we may be well advised, not to renounce tithing, but to seek another storehouse — perhaps a church in the ghetto — where the Spirit may be less hedged about with anxiety and paternalistic caution.

And here, I believe, is the relationship — and the difference — between paying taxes and tithing.

We should continue to render unto Caesar that which is Caesar’s, including obedience and respect as well as taxes, for so long as they are his due and his requirements are not in conflict with those of God.

If the government turns away from righteousness, forsakes justice and mercy, and puts our taxes to ungodly uses instead of caring for all of its people, I believe we have the right to refuse and to reallocate to constructive causes that percentage of our income which is assessed as tax.

On the other hand, our allegiance to God is paramount.

Under any and all circumstances we are required to render unto God that which is God’s including our tithes.

However, just as we may need to consider withdrawing our financial support from a government that is not doing what a government is supposed to do, we may wish to consider reallocating our tithes if our own religious body fails to be responsive to the Spirit of Christ which is the foundation of our faith.

A report on the Philadelphia Yearly Meeting’s annual sessions in the same issue mentioned, but only in passing, that there had been “three called sessions on tax refusal and the Black Manifesto” over the past year.

A report on the General Conference for Friends in the issue reprinted a “query” that had been proposed by the “discussion group on tax refusal and tax avoidance”:

Have Friends considered their implication in the immoral war system through the payment of telephone excise and Federal income taxes, which are largely used for military purposes, and have they sought ways in which to make clear their testimony against such immorality by refusing, when possible, payment of such taxes and/or avoiding tax payments by changing their life style to live below or at a lower level of tax liability, bearing in mind that the spirit in which such action is taken is crucial and that divine guidance should undergird the individual’s response?

An article on individual spiritual growth in the issue casually included tax resistance as one of the issues a spiritual seeker might be expected to confront:

What do you do when you come to a stumbling point or dead end in your search?

(Examples: Defining or identifying God, refusing to pay taxes, accepting the label “religious,” surrendering autonomy to a group, praying privately, and teaching one’s beliefs about religion to one’s children.)

That issue also reprinted a sarcastic notice from the Fifteenth Street (New York) Preparative Meeting’s newsletter:

Special offer for complacent Friends!

The Peace and Social Action Program of New York Yearly Meeting is offering for sale two copies (paperback) of the Journal of John Woolman.

These copies are unique in that all the radical passages have been removed by mechanical excision.

They were cut to prepare a pamphlet of Woolman excerpts called, “John Woolman on Seeds of War and Violence in our Possessions, Consumption, Taxpaying, and Lifestyles.”

The special clearance price, only $19.95 a copy.

Which is a bargain, considering that it saves you the trouble of removing these passages yourself!

The issue noted that the Saint Louis Monthly Meeting was administering an escrow account to accept money from Friends who were refusing to pay the Federal excise tax on phone service.

Don Kaufman’s book “What Belongs to Caesar?” was reviewed in the issue.

The reviewer was sympathetic to the book’s thesis — that war tax resistance and Christianity are compatible — but thought the book “would be even more valuable if the author had felt as free to quote from the Bible as he was to quote from other books and articles.”

At the upcoming national gathering of NWTRCC at Earlham College in Richmond, Indiana, I’m going to be presenting a summary of the history of war tax resistance in the Society of Friends (Quakers).

Today I’m going to try to coalesce some of the notes I’ve assembled about the renaissance of Quaker war tax resistance during the Cold War.

Much of what I have assembled here comes from my close look at the archives of the Friends Journal, the only Quaker publication from this period I have reviewed thoroughly, and so whatever editorial biases that publication may have had may also bias my history of this phase.

There is a lot that happens in this short period of time, and in some places my narrative is going to be condensed into a bunch of bullet-point-like summaries of the rapid-fire events to try to keep up with it all.

The Renaissance ()

The modern war tax resistance movement began in the wake of World War Ⅱ in the United States.

There had been isolated war tax resisters here and there in other places in recent years, and there was a quiet war tax resistance tendency hiding under the surface of the Society of Friends, but things did not come out into the open in any organized and growing fashion until then.

Quakers were not in the forefront of this movement, but Quaker war tax resisters took courage from it, and it wasn’t long before they began trying to reestablish the war tax resistance traditions in the Society of Friends.

The earliest mention of this that I have found from this period concerns Franklin Zahn of the Pacific Yearly Meeting, who was distributing a leaflet on war tax resistance as early as .

A report on the Philadelphia Yearly Meeting that year noted that the subject of war taxes had come up and had led to what sounds like a long and earnest discussion:

Few present felt it right to refuse to pay, nor yet felt comfortable to pay.

Varied suggestions were presented: Send an accompanying letter expressing one’s feeling about war; live so simply that income is below tax level; make no report, but once a year send a check for nonmilitary purposes; engage in peace walks and other minority demonstrations; follow Jesus’ example of rendering unto Caesar the things that are Caesar’s; beware of taking for granted the evils deplored, such as riding on military planes; associate more closely with the Mennonites, who share Friends’ concerns; rise above one’s own shortcomings through personal devotion; work to unite with all Friends Yearly Meetings in refusal to pay taxes.

Nothing can be done unless there is a willingness to suffer unto death.[!]

The blinders put on during the Great Forgetting period were still evident.

An article in a issue of the Friends Journal described “refusal to pay taxes for support of war effort emerging as a new testimony” [my emphasis].

Another article from the same issue, titled “The Quaker Peace Testimony: Some Suggestions for Witness and Rededication” didn’t mention taxes at all.

By this time some Friends in Switzerland had been refusing to pay war taxes (I would guess, under the tutelage of Pierre Cérésole).

In some Quakers in the Pacific Yearly Meeting began to sketch out the initial drafts of a legislative “peace tax” proposal which they envisioned would be a way for conscientious objectors to pay their taxes into a fund that the government could only spend on non-military items.

The idea that there might be a legislative solution that could make tax-paying no longer an act of complicity with war would bob up throughout this period, until, by the end of it, the temptation of lobbying instead of committing to direct action would contribute to the eventual decline of war tax resistance in the Society of Friends.

also, the Yellow Springs Monthly Meeting issued a statement of support for war tax resisters, the first example of new institutional support for war tax resistance in the Society of Friends that I could find from the 20th century.

In there was a burst of excitement about war tax resistance in the Baltimore Yearly Meeting (yet a survey of 350 adults from that meeting found only two or three who were willing to consider actually becoming resisters; whereas almost half of those surveyed were totally unconcerned about their tax money going to the military).

A group of about twenty Quakers, organized by Clarence Pickett and Henry Cadbury, met at the Philadelphia Yearly Meeting to discuss war tax resistance, but they were unable to come up with a consensus statement.

Quaker war tax resister Arthur Evans was imprisoned for three months for his tax refusal.

In the Friends Journal ended what strikes me as a policy of editorial embarrassment about Quakers and war tax resistance by publishing its first article devoted to the practice, and one that also full-throatedly advocated it.

This started a debate in the letters-to-the-editor column and certainly caused more Quakers to confront the question, directly or indirectly.

By the tide was shifting rapidly.

Before this time, individual Quaker tax resisters are unusual enough to highlight individually as being on the cutting-edge; after this, Quaker war tax resistance becomes commonplace enough that individual resisters are exemplars of a larger trend.

In the New York Yearly Meeting promoted war tax resistance in an official statement, and promised financial assistance for any Quakers in the Meeting who might be forced to change jobs or to suffer other financial hardship for their stand.

The statement in part read:

We call upon Friends to examine their consciences concerning whether they cannot more fully dissociate themselves from the war machine by tax refusal or changing occupations.

That was the most concrete advocacy of war tax resistance by a Quaker institution in years.

Franklin Zahn wrote a booklet on Early Friends and War Taxes to reintroduce Quakers to their own history and to further banish the Great Forgetting.

The support from Quaker institutions and publications at this point is often noncommittal and is usually vague about exactly how to go about war tax resistance, which taxes to resist, and how to deal with government reprisals.

There is nothing like the specific, concrete discipline of earlier Quaker Meetings.

This means that Quaker war tax resisters from this period are largely making it up as they go along, conferring with each other informally and organizing, when they are organizing, in groups like Peacemakers, the War Resisters League, and the Committee for Non-Violent Action — that is to say, with non-Quaker groups.

(There was briefly something called the “Committee for Nonpayment of War Taxes” run out of Quaker war tax resister Margaret G. Bowman’s home in , but I have not found much about it.)

Quakers were using a broad variety of tax resistance tactics.

Arthur Evans and Neil Haworth refused to pay some or all of their income taxes or to cooperate with an IRS summons for their financial records.

Johan Eliot redirected twice the amount of his taxes to the United Nations to promote international federalism as a world peace strategy.

Clarissa & Samuel Cooper lowered their family income below the tax line.

John L.P. Maynard and Robert W. Eaton took pay cuts that reduced their incomes to the maximum allowable before federal income tax withholding was mandatory.

Lyle Snyder stopped withholding by declaring three million dependents on his W-4 forms.

Alfred & Connie Andersen stopped filing income tax returns.

Some Quakers fled to Canada as taxpatriates to join the draft evaders there.

Others deposited their taxes into escrow accounts and invited the IRS to seize the accounts while refusing to pay voluntarily.

Lloyd C. Shank advocated “the ‘sneaky’ way” of tax resistance — what many people would call tax evasion — saying “ ‘cheating’ is only an oppressive government’s name for a good man’s refusal to murder.”

Phone tax resistance was beginning to become widespread, and many Quaker meetings began resisting this tax on their office phones (one meeting was unable to reach consensus on resisting the phone tax and compromised by dropping its phone service entirely).

People too timid to resist, and meetings unable to reach consensus on resisting, might instead write their legislators to urge them to enact some form of legal conscientious objection to military taxation.

The most timid groups, like the American Friends Service Committee, urged people to pay taxes “under protest” or to match their war tax payments with additional payments to the AFSC.

Robert E. Dickinson had perhaps the most creative tactic of the bunch.

He designed and built a set of furniture for his home that was formed of interlocking sheets of plywood such that it could be quickly disassembled and hidden away.

He called this “my tax refusal furniture” and meant it to frustrate IRS attempts to seize furnishings from him for back taxes.

Two Quaker employees of two groups within the Philadelphia Yearly Meeting asked their employers to stop withholding income tax from their paychecks, and that Meeting tried to come up with a good policy to follow in such cases.

The fourth Friends World Conference was held in .

The “Protest and Direct Action group” there “called upon Friends in countries party to the [Vietnam] conflict to ‘go as far as conscience dictates in withholding support from their governments’ war-making machinery,’ first by direct communication with those against whom the protest is made, and then if necessary by public witness and individual action, including the possibility of refusal to pay taxes for war.”

U.S. President Johnson called for a 10% income tax surcharge explicitly to fund the Vietnam War.

This would be the first explicit “war tax” (other than, arguably, the phone tax) since World War Ⅱ, and its announcement prompted renewed interest in war tax resistance inside and outside the Society of Friends.

Quakers were, because of this tax, better-enabled to quote the discipline of early Quakers on refusal to pay explicit war taxes as a way of explaining their own stands.

In 203 delegates from “nineteen Yearly Meetings, eight Quaker colleges, fifteen Friends secondary schools, the American Friends Service Committee National Board and its twelve regional offices, and nine other peace or directly-related organizations” met in Richmond, Indiana, to draft a “Declaration on the Draft and Conscription.”

Part of this declaration mentioned the war tax concern:

We call on Friends everywhere to recognize the oppressive burden of militarism and conscription.

We acknowledge our complicity in these evils in ways sometimes silent and subtle, at times painfully apparent.

We are under obligation as children of God and members of the Religious Society of Friends to break the yoke of that complicity.

We also recognize that the problem of paying war taxes has intensified; this compels us to find realistic ways to refuse to pay these taxes.

After only of thaw, some seventy years of Great Forgetting have been melted away, and the Society of Friends has again reached a consensus that Quakers are compelled to refuse to pay war taxes.

President Johnson’s war surtax went into effect in , adding a 7.5% surtax to the income tax returns for , and 10% for (the tax would be extended at a reduced rate into and then abandoned).

Meetings all across the country were discussing and passing minutes on war tax resistance, though few would advocate it in specific and unreserved ways, most choosing instead to voice expressions of unspecified “approval and loving support” for Quakers who felt compelled to resist.

In , the Philadelphia Yearly Meeting passed a relatively strong minute stating:

Refusal to pay the military portion of taxes is an honorable testimony, fully in keeping with the history and practices of Friends…

We warmly approve of people following their conscience, and openly approve civil disobedience in this matter under Divine compulsion.

We ask all to consider carefully the implications of paying taxes that relate to war-making…

Specifically, we offer encouragement and support to people caught up in the problem of seizure, and of payment against their will.

The New York Yearly Meeting decided to begin resisting corporately by refusing to honor liens on the salaries of tax resisting employees (though it could not reach consensus on a refusal to withhold income tax from such employees), and, , by refusing to pay its own phone tax.

The American Friends Service Committee finally decided to do something concrete about the war tax question, but it was a little odd.

They withheld and paid taxes from a war tax resisting employee and then sued the government for a refund.

The strange structure of their process seems to have been a very deliberate way to structure a legal suit for maximum effectiveness, and it did (briefly) show some success.

A court ruled in , on First Amendment freedom-of-religion grounds, that the government could not force the organization to pay the taxes of an objecting employee — alas, the Supreme Court almost immediately, and overwhelmingly, overturned this.

Also in , Susumu Ishitani, a Japanese Quaker, formed a war tax resistance group in Japan — the first example I am aware of from Asia.

By , the Friends Journal’s coverage of war tax resistance is less occupied with advocacy, debate, and the presentation of individual exemplars, and is more concerned with the practical aspects of how Quakers are going about it.

The editorial stance shifts again, to one of more forthright advocacy.

It is assumed that Quakers want to avoid paying war taxes, and the question is how to do so well.

The ending of the U.S. war on Vietnam did not seem to slow the enthusiasm for war tax resistance.

In the Friends Journal devoted an issue to the subject for the first time.

In Robert Anthony began another attempt to get the courts to legalize conscientious objection to military taxation.

It went nowhere, but notably, in a letter to the court, his monthly meeting wrote:

We assert that the free exercise of the Quaker religion entails the avoidance of any participation in war or financial contribution to that part of the national budget used by the military.

If not exaggerated for effect, this statement would be among the strongest yet articulated by a Quaker institution in this renaissance period — not simply expressing support for war tax resisters, or encouraging Friends to consider resisting, but asserting that to practice the Quaker religion necessarily meant to refuse to pay war taxes.

In , Quakers met with their Brethren and Mennonite counterparts to draft a joint statement that encouraged war tax resistance — the “New Call to Peacemaking.”

The Philadelphia Yearly Meeting asked its ongoing representative meeting to draft some formal guidance for Quaker war tax resisters for how they should go about it, and to set up an alternative fund to hold and redirect resisted taxes.

(New England Yearly Meeting began its own alternative fund for resisted taxes .)

By this time war tax resistance is a core part of any discussion of the Quaker peace testimony, and there are increasing calls for Meetings to resist taxes as an institution.

In the Philadelphia Yearly Meeting approved a minute on war tax resistance that pulled its punches a bit:

Our strength and our security are derived from our belief in the reality of a loving God and the oneness of that of God in all people.

In order to say yes to this belief, we must seriously consider saying no to payment of war taxes.

This “seriously consider” compares poorly to discipline of times past (e.g. “a tax levied for the purchasing of drums, colors, or for other warlike uses, cannot be paid consistently with our Christian testimony” [Ohio Yearly Meeting, 1819]).

It also, some Quakers point out, sometimes pales next to the more direct and certain advice from some meetings that young Quaker men resist the draft.

As more Quakers and Meetings feel the pressure to take a stand on war taxes, the more timid ones are increasingly desperate to find ways to do so without actually having to resist.

Silly ideas, like writing “not for military spending” in the memo field of their tax payment checks, and “peace tax fund” ideas proliferate.

By , Quakers in Canada and Australia are floating their own peace tax fund legislation ideas.

Meanwhile, Quakers in England seem to have gotten the tax resisting bug.

The Friends World Committee for Consultation and London Yearly Meeting stopped withholding income taxes from twenty-five war tax resisting employees in , putting the money in escrow.

(This resistance was short-lived; after losing a legal appeal in , they went back to withholding.)

In war tax resistance, according to Friends Journal reports, was a “major preoccupation” of the London Yearly Meeting, and a “burning concern” at the Philadelphia Yearly Meeting (where “unity could not be achieved”).

Lake Erie Yearly Meeting encouraged its Monthly Meetings “to establish meetings for sufferings to aid war tax resisters.”

Pacific Yearly Meeting started an alternative fund.

Smaller Monthly and Quarterly meetings around the country were beginning to take even stronger stands.

The Minneapolis and Twin Cities Meetings approved a minute that asked “all members of our meetings to practice some form of war tax resistance”!

The Davis (California) meeting passed a similar minute.

Monthly Meetings are assembling “clearness committees” to help each other find responses to the war tax problem that are appropriate to their conscientious “leadings.”

also, the Friends General Conference promoted the idea of Quakers giving interest-free loans to them, a thinly-veiled (not explicitly stated) way of hiding assets from IRS:

…Friends loan money to F.G.C. at no interest, which F.G.C. invests to earn income which is used to support the varied programs of the Conference, such as publications, religious education curricula, and the ongoing nurture program.

These loans provide regular dependable monthly income to the Conference, and reduce the interest income on which the lender must pay federal income taxes, while providing the lender with protection against unforeseen financial reversals.

F.G.C. will repay the principal amount within 30 days after receiving a written request from the lender.

All principal amounts are kept in insured investments.

In the Friends Journal, now edited by a war tax resister, devoted another issue to the subject.

Non-resisting Quakers were now very much on the defensive.

One complained that at the Philadelphia Yearly Meeting , taxpaying Quakers like him “were compared to the Quaker slaveholders of , and not a dissenting voice was raised,” but even he had to acknowledge that war tax resistance was “in the mainstream of Quaker thought, and therefore entitled to support from Quaker bodies.”

The meeting itself though could only agree to issue another minute that would “not urge” Friends to resist, but would “give strong support” to those who did.

In , the Friends World Committee for Consultation held a war tax resistance conference in Washington, D.C., and formed a standing “Friends Committee on War Tax Concerns.”

, they held a conference for Quaker organizations that had war tax resisting employees.

The conference was attended by 35 people, including representatives from 21 such organizations.

They were united by an interest in supporting the war tax resistance of their employees in an open and honest fashion, in a way that included the redirection of the resisted taxes to beneficial causes, and that used the “clearness committee” process.

You definitely get the feeling that momentum is building and Quaker war tax resistance is having a vigorous revival.

Unfortunately, though, it seems to me that this is the high-water mark.

In surprisingly little time the tide will begin to recede.

But there is still some forward progress to be made.

In the London Yearly Meeting declared:

We are convinced by the Spirit of God to say without any hesitation whatsoever that we must support the right of conscientious objection to paying taxes for war purposes…

We ask Meeting for Sufferings to explore further and with urgency the role our religious society should corporately take in this concern and then to take such action as it sees necessary on our behalf.

The Friends United Meeting adopted a policy of not withholding taxes from resisting employees as well.

The Philadelphia Yearly Meeting soon followed suit, and refused to withhold federal taxes from three war tax resisters on the payroll (after a legal battle, they would pay “under duress” ).

The Baltimore Yearly Meeting also adopted such a policy, in .

In another conference for employers of tax resisting employees was held, this one expanded to include Mennonite and Church of the Brethren employers.

The Friends Journal got an IRS levy on the salary of its editor, and it devoted a third issue to the topic of war tax resistance.

Some Quakers begin using the tax resistance tactic in the service of other causes, such as opposition to capital punishment or nuclear power.

In an early sign of the receding of the war tax resistance tide, the Friends World Committee for Consultation retired its “Friends Committee on War Tax Concerns” in favor of a “Committee on Peace Concerns.”

From here, sadly, it’s pretty much all downhill.

In the next and final segment of this series on the history of Quaker war tax resistance, I’ll try to describe and explore the second “forgetting.”

This is the fourteenth in a series of posts about war tax resistance as it was reported in back issues of Gospel Herald, journal of the (Old) Mennonite Church.

War tax resistance really picked up steam in the Mennonite Church in , as the coverage in Gospel Herald shows.

In a “workshop on war taxes” was held “at the Hively Mennonite Church, Elkhart, Ind. Resource persons are Al Meyer, John Howard Yoder, David Habegger, Art Gise, and Carl Landes…” Gospel Herald’s report on the conference noted:

Christian response to war taxes was discussed by about 100 participants in a workshop in Elkhart, Ind.

The weekend was sponsored by the Elkhart Peace Fellowship, the General Conference Mennonite Central District Peace and Service Committee, and other regional church peace and service committees.

Michael Friedmann of the Elkhart Peace Fellowship said many of the participants felt the war tax question involved a shift in life-style to reduce involvement in the military-industrial complex.

Al Meyer, a research physicist at Goshen College, Goshen, Ind., suggested to the group that one does not start by changing the laws to provide legal alternatives to payment of war taxes, but by refusing to pay taxes.

We need to give a clear witness, he said.

Meyer did not oppose payment of war taxes because he was opposed to government as such, but because he did not give his total allegiance to government.

He felt it was his responsibility to refuse to pay the immoral demands of government.

“No alternative will be provided by the federal government until a significant number of citizens refuse war taxes,” he said.

The annual tax collection time is at hand.

How do you respond to the 1040 and other tax forms?

An increasing number of Mennonites are asking what it means to render to Caesar what belongs to him and in particular to render to God what belongs to Him.

Two seminars are planned to study this question: , Akron Mennonite Church; Bally Mennonite Church.

The purpose will be (1) to learn what the Bible says for and against paying taxes, (2) to share with and support each other as the Spirit leads, and (3) to examine what choices are available in nonpayment of taxes used for war purposes.

The schedule allows for considerable discussion time.

Howard Charles, Goshen Biblical Seminary, will be the resource person.…

War Tax Meeting Set

A meeting for people who are disturbed by American policy in Southeast Asia and who question payment of war taxes is planned for at Hebron Mennonite Church, Buhler, Kan. The meeting, sponsored by the Western District Peace and Social Concerns Committee of the General Mennonite Church, will be a time to exchange ideas and tell of actions already taken.

Two seminars on taxes, “Jesus and the 1040 Form” seminars, were held at the Akron Mennonite Church and the Bally Mennonite Church, respectively.

Approximately 70 persons participated.

Howard Charles, Goshen Biblical Seminary, was the resource teacher on biblical passages dealing with taxes.

Other input was given by Melvin Gingerich and Grant Stoltzfus on examples of tax refusal from history.

Wesley Mast presented options in payment and nonpayment of taxes.

Walton Hackman gave a breakdown of the present use of tax dollars, 75 percent of which go toward war-related purposes.

War taxes also would come up at another Mennonite forum, as announced in the issue:

On the Swiss Farm at Bluffton College, Bluffton, Ohio, Mennonite collegians will meet.

, to “rap” about the kind of life-style they want to adopt.

Intentional communities, ways to avoid American materialism and consumerism, how to avoid complicity with militarism through paying taxes that support past, present, and future wars, and the role of women will be ingredients in the discussions of the conference.

Rudolf Gnaegi, Swiss defense minister, has announced that 32 Protestant and Roman Catholic clergy will be prosecuted if they persist in their refusal to perform military service or to pay “defense taxes.”

In Switzerland, all males over 20 — including the clergy — are subject to military service and annual retraining service periods.

Conscientious objection is not recognized.

Those who refuse to serve in the military are liable to prison terms.

The 32 clergymen, all from French-speaking cantons, announced in a joint letter to the Defense Ministry that they would not report for military service nor pay taxes earmarked for defense because they felt the Army served only “economic and financial interests.”

The letter charged further that whenever the Army was used in the country, it was used “against workers, peasants, and young people.”

Mr. Gnaegi, chief of the Military Department, told newsmen it was “incredible” that “in a free and evolving society like Switzerland’s,” clergymen should refuse completely “to share the difficult task of national defense.”

A second issue brought to the Council was that of payment of war taxes.

After extensive discussion, the Council agreed to ask Walton Hackman, secretary-elect of MCC Peace Section, to serve as resource person in further discussion of the issue in the meeting of the Council.

Meanwhile, Council members will take their homework seriously by continued study in preparation for carrying the question to the church.

In “What Belongs to Caesar” (), Robert E. Dickinson explained how he had come around to the war tax resistance position:

Although I was a conscientious objector to war in the Second World War, I have justified the paying of war taxes to myself with the quote from Jesus, “Render unto Caesar…” As violence has escalated in our world I have become increasingly uneasy with this concept.

With the reading of What Belongs to Caesar? a discussion on the Christians’ response to the payment of war taxes by Donald D. Kaufman, I realized that Christ’s statement was not to be taken too literally but needed to be placed in context.

It has become increasingly clear to me that my own reasons for paying war taxes was one of protecting property and job, neither of which are ultimate Christian values.

The now well-documented illegality of the war as substantiated by the publication of the Pentagon Papers and the fact that the individual citizen is to be held responsible for his acts as established in the Nuremberg Trials are further factors in my decision.

As an architect I do not wish to emulate the German architect, Albert Speer, who sold his soul to the state for professional advancement.

It seems to me that Christians who refuse to serve in the military but at the same time pay for war put themselves in the unenviable position of paying someone else to fight their wars for them.

With God’s leading I will do my best not to do this.

Meanwhile, other Mennonites were refusing to pay their war taxes while redirecting them to alternative funds.

The telephone excise tax was a popular target for anti-war activists.

This account comes from the edition:

An increasing number of people are sending war tax monies to Mennonite Central Committee, instead of paying them to the United States Government for military use, said Calvin Britsch, MCC assistant treasurer.

Contributions of tax money are of two kinds, Britsch said.

More people are refusing to pay the federal tax levied on the use of telephones.

This 10 percent tax is seen as a direct source for military expenditures.

People who refuse this tax simply subtract the 10 percent from their telephone bill and send it instead to MCC.

Ron Meyer tried to relax the hold that the traditional Render-unto-Caesar interpretation had on many Mennonites, in his article “Reflections on Paying War Taxes.” This was also the first mention I found in Gospel Herald of peace-tax-fund legislation:

[Render-unto-Caesar summary omitted] When He answers, “Give to Caesar what is Caesar’s and to God what is God’s,” he doesn’t make a solid commitment one way or the other.

Instead, Jesus makes it apparent that His follower should decide what of his belongs to the government and what to God.

He does not tell the Christian that his tax money should be given without thought to the government, an interpretation that seems to be quite prevalent today.

In contrast to this interpretation, some American Christians now are questioning the morality of voluntarily paying taxes which support the U.S. government’s military policies.

The income tax is the main source of revenue for warfare: 60 to 75 percent of it is used for military purposes.

The 800-member Goshen College Mennonite Church determined that the amount of money its members “gave” for military purposes through the income tax was almost twice as much as church giving in that congregation.

Though Christ’s work cannot be measured by dollars alone, the thought of paying twice as much for war as for the church and its mission of peace is disturbing.

It is almost impossible not to support the war in Vietnam, however indirectly, if one lives in U.S. today.

Even a small purchase may be supporting a company which has been awarded government contracts for war materials.

If one does refuse to pay war taxes, the government will take the amount from his bank account or personal possessions.

The question then arises, “Why resist the tax if you end up supporting the war effort anyway?”

Tax resisters answer this by saying that one’s intention must be more than just trying to “keep his hands clean.”

The real purpose of war tax resistance is to provide a witness against the war and the ways in which tax money is being used for military purposes.

There are various approaches to war tax resistance for one who decides upon this type of peace witness.

Many tax resisters refuse to pay the 10 percent telephone tax that is to be used expressly for war.

The telephone company usually regards this as a matter between the government and the individual (if notified of the reason for the refusal) and will not cut off phone service.

IRS may take the money from a bank account or send men to the home.

Telephone tax resisters have found that talking to IRS men gives them an excellent chance to witness.

Because of the tax-withholding policy of most employers, nonpayment of income taxes is more difficult.

In this case, if there is any extra tax due each year, the resister may refuse to pay this as a token gesture.

Letters of protest sent in with tax forms are also indicative of the taxpayer’s stance for peace.

Some resisters earn less than the taxable income level for their number of dependents.

This level starts at $1724.99 per year for no dependents.

Those resisting in this way pay no income tax at all.

If one is self-employed, it is a relatively simple matter not to pay the 60 to 75 percent of the income tax used for war.

The tax resister simply deducts this percentage from the amount he must give.

This is not to say that the government won’t take the amount eventually from the individual’s personal property.

An alternative to the war tax system, presently under discussion by various groups, is the World Peace Tax Fund.

This proposal, drawn up by a group of University of Michigan law students, suggests that an individual’s tax money that would go for war purposes could be channeled into a world peace fund if he so wished.

This is similar to the Selective Service Conscientious Objector provision in which an alternative to compulsory military service is provided.

If this proposal is put through Congress, it will provide a peace witness that is within the law.

Its inherent danger is that people may become less bothered by the killing if they aren’t paying for it.

Total noncooperation with the Internal Revenue Service, similar to noncooperation with the Selective Service, is not extensive, since IRS is set up for peaceful purposes as well as channeling money for war.

The consequences of war tax resistance have not proven severe so far, yet the decision is weighty, since legally one could be fined and imprisoned for tax evasion.

Most Christian tax resisters hold that if one decides to take this stand, he must remember that his real object cannot be to “keep his hands clean.”

He must be led by a desire to witness for peace and against violence and war.

Even a simple refusal to pay a telephone tax may influence someone to follow Christ’s way of peace.

There are many Christians who are sincerely opposed to resisting the government in the ways that have been discussed here.

And there are many also who feel that by paying war taxes, they are giving to Caesar what is God’s. Whatever a believer’s decision about the war tax issue, it should be carefully and prayerfully considered with the way of Christ firmly in mind.

The Gospel Herald editor, “D.” (John M. Drescher) endorsed this in a editorial: “When approximately 70 percent of the tax dollar is going to war, a foremost frontier of faith may well be the kind of witness we bear in refusing to finance killing.”

He followed this up with a second editorial in the issue — “Taxes for War”:

Approximately 70 percent of income taxes go to pay for war and all of the 10 percent telephone tax goes to pay for war.

What is the responsibility of those who believe that war is contrary to the Spirit and teaching of Christ?

Should we not seek an alternative in paying taxes when the government’s primary need is for our money, just as hard as we sought an alternative service when the government needed our bodies?

Those who understand what is happening in the automated war and have a concern for life are asking questions like the above with growing seriousness.

Some simply dismiss the whole question by saying, “Render to Caesar the things which are Caesar’s, and to God the things which are God’s.” Could this be a cop out?

Might Christ not be laying upon us the obligation to decide what is Caesar’s and what is God’s?

Or was He saying that we will need to decide whether we are Caesar’s person or God’s person?

Isn’t it strange that, over the years, many of those who used this Scripture to say that we should pay our taxes without question, did not render unto God even what was required under the Old Testament?

As a church we are even today much more obedient in rendering to Caesar what he demands than to God what is His.

Look at it this way.

Suppose Caesar should demand a 10 percent telephone tax to wipe out Jews or Indians or blacks in the United States.

What would be our reaction?

Would we willingly and without question render it to Caesar?

How would that be different than demanding a 10 percent tax to wipe out Vietnamese?

What would we say if it were levied to bomb Lancaster, Goshen, or Hesston?

Or to bring it closer.

Suppose Caesar would level a 10 percent tax to pay for the extermination of Mennonites.

Would we encourage everyone to “render unto Caesar what he asks for”?

Would such a 10 percent tax be any different than paying a 10 percent tax for killing Vietnamese?

If so, what is the difference?

Since Caesar receives all his rights from God, does not he forfeit these rights when he violates them?

What is our duty to use money to restrain injustice and to advance right?

For additional study help and discussion, order and study the paperback, What Belongs to Caesar, by Donald D. Kaufman, Herald Press.

As a church, we are at the point where we must somehow come to grips with what we will do about giving our money to support war.

Dealing with a problem of this proportion will be costly.

It may demand a different life-style, the loss of property and institutions.

We can be assured, however, that the way of obedience, even though it leads through the wilderness and death, is the way of Christ.

Out of death we believe there is always a resurrection.

And how our world needs resurrection life!

Sixteen years ago, the country told me I had to join the army.

I told them I was a Christian and I could not do it.

Now, the country tells me I must give it money so it can pay other people to fight and kill.

Once again, I must say I cannot, because I am a Christian.

A very large portion of the taxes we pay, as well as a number of special taxes, go directly to help fight the war.

I have told the government that because Jesus said I should not kill, I cannot pay these, and that instead I give that amount to the church to use in helping people our country makes homeless.

At least one speaker brought up war tax resistance at “Mission ” ():

One speaker took the open mike to make a statement on the war in Vietnam.

He felt that the government is not leveling with us.

Therefore, we should find some way to disengage ourselves as a people — perhaps through nonpayment of certain taxes.

Resolutions urging Unitarian Universalists to refuse payment of the telephone excise tax, and calling for strong gun control laws were approved by delegates to the 11th annual Unitarian Universalist Association General Assembly.

Action on the controversial issues was taken by 678 delegates, the smallest number of delegates in the history of the Association.

Stating that the telephone excise tax “was levied specifically by Congress in to finance the war in Vietnam,” the resolution calls on “all Unitarian Universalists to refuse payment of the telephone excise tax” and urges the UU Association “to refuse such payments also.”

Legal counsel for the 375,000-member Association told delegates that refusal to pay the tax is considered a criminal offense carrying a one-year jail sentence or $10,000 fine or both.

Some feedback from Gospel Herald readers followed:

I want to commend your courage in writing the editorial, “Taxes for War” ( issue).

Your words seem clearly to be in the spirit of Jesus.

Asking the question, “Suppose Caesar would level a 10 percent tax to pay for the extermination of Mennonites.

Would we encourage everyone to ‘render unto Caesar what he asks for’?” brings the argument for nonpayment of war taxes home with blunt but true force.

We are personally searching for the Christian way with regard to the payment of our taxes.

Your editorial shed additional light to our pilgrimage.

Thanks for your two editorials recently (“We Merely Pay to Kill” and “Taxes for War”).

They, along with Maynard Shirk’s “Plea from Saigon” and Don Blosser’s "But, Daddy,” point out our silent complicity in financing the destruction, rather than Jesus’ call to love, of our Vietnamese neighbors.

Our silence indicates the complacent neglect of our individual responsibility as Christians and our corporate responsibility as the church to be God’s reconciling community in this world.

We cannot be silent or complacent in our militarized society and still name Jesus our Lord!

Paul said, "And be not conformed to this world: but be ye transformed by the renewing of your mind” (Rom. 12:2).

It appears that our renewal has not yet occurred.

Our churches have not become God’s liberated zones.

As an ex-VS-er I recently learned that MCC paid about $1,500 in federal telephone tax during alone, a tax that "Vietnam and only the Vietnam operation makes this bill (federal phone tax) necessary,” according to Rep. Wilbur Mills of the House Ways and Means Committee (Congressional Record of ).

Our other church agencies and our churches are no different from MCC in this respect.

As John A. Lapp wrote in the MCC Peace Section Newsletter, , “Each institution has wittingly or unwittingly developed its program not simply because this is what the Lord or the brotherhood wants us to do but also because this is what IRS allows us to do” (italics mine).

Yes, Brother Drescher, we do not have to worry about rendering to Caesar his due, for he collects by force.

But God only receives voluntary service, which we continually cut short because of submission to government or some other reason.

Our fruits indicate what kind of trees we Mennonites are — comfortable, quiet, complacent.

As Jesus’ disciples we must say no to paying for others or machines to destroy our neighbors, just as the Mennonite Church has said no to participating actively in such destruction, as Jesus said no to Peter fighting enemies with a sword.

As we say no individually we must encourage our churches and agencies to also say no to war taxes as corporate bodies, even if it costs something such as the tax exemption privilege, or property, or social status.

Being “renewed of mind” in witnessing to Jesus’ way of reconciling love for all people.

For as disciples we can value nothing more.

In the name of Christianity, let’s keep balanced on this idea of withholding “war taxes.”

Every person that works in any industry or food production, helps to produce commodities that are used by the army.

So why not talk about laying off from work so many days or withholding so many head of cattle?

Even if we did that the army would still get its share of what did go on the market.

And if we hold back part of our taxes, the army will get what it needs out of what we do pay.

In the days when Paul lived, Rome was just as corrupt as America has been, and still Paul says in Romans 13 that we should pay to “all their dues.”

Alcohol is a much worse killer than war is, why not start doing something about it?

Remembering Paul was living under one of the most cruel and bloody governments of all time and he knew that much of the tax money went to pay the Roman army, which not only put wicked people to death but many, many Christians as well, yet admonished the Roman Christians, “Pay your tax” without any strings attached.

In the editorial, “Taxes for War,” () you quote, “Render to Caesar…” and you say, “Might Christ not be laying upon us the obligation to decide what is Caesar’s and what is God’s?”

You are not suggesting that each of us should decide for himself how much tax he ought to pay and what he wants his tax money used for, are you?

That is getting pretty far out it seems to me.

I think Paul is telling us in Romans 13 that the government as ordered by God is responsible, (1) to provide for our needs, v. 3, (2) to protect us, v. 4, and we in turn shall pay the government the taxes that are laid upon us, with no strings attached as to how they should use our money.

The government is not accountable to us but to God and He will hold them responsible for their actions.

Romans 12:19.

May I express appreciation for the good articles in the issue of Gospel Herald which dealt with our response to war.

I was especially glad for the editorial, “Taxes for War,” and for the “Testimony on Taxes.”

My husband and I have been part of a group in our congregation which studied Donald D. Kaufman’s book, What Belongs to Caesar? and as a result we and others have been seeking to live an altered life-style which will proclaim our commitment to Christ’s way of love.

We too have felt that the way of obedience may be costly.

Reading such testimonies in the Gospel Herald gives us courage to continue to learn what discipleship in this area means.

I am glad to hear that you are concerned about war taxes.

I’m sure that a lot of people share this same concern.

However, I must say that your concern is probably little more than the academic cloak worn by the average “pious Christian."

Why do I say this?

There is a very simple answer to the problem of war taxes for the person who is truly concerned.

I’m not talking about the “Oh, isn’t that a shame” set.

I’m talking about those who see the sadness and weep.

Those who lock themselves in their rooms and beat on their mattresses in anguish.

The answer is simply don’t earn enough money to have to pay taxes.

It is the only legal recourse we have at the present time.

Some say they cannot live on that amount of money, and I say hogwash!

Who is your God?

Did He tell you that you need a six-room house?

Did He tell you that you need a new car, a television, or an air conditioner?

Did He even tell you that you need electricity, running water, or a living-room rug?

My God didn’t. My God said, “Love Me more than you love anything in this world.

Love your neighbor more than you love yourself.

Remember the rich man who would not give up his riches to follow Christ.

I say that every one of us is rich, and anyone who cannot part with his riches cannot love the Lord, for we cannot serve two gods.

We can continue with our present stewardship (pittance that it is) and still not have to pay taxes.

I am not suggesting that we quit working, but I am suggesting that we refuse salaries which cause us to have to pay taxes.

A married couple can now earn $2,300 and be exempt from taxes.

A family with children, even more.

I don’t expect very many people to take this seriously, for God only opens the eyes of a few However, I want to express my love to those of you who will think I am a little crazy.

After reading D.D. Kauffman’s book What Belongs to Caesar?, listening to and reading testimonies from tax protesters, and thinking about the subject, I had arrived at about the same conclusions that Bro. Mason presents.

I suppose it is to my discredit that I am unwilling to act on these conclusions as he apparently has done.

It has been said that the entire science of economics is summarized in the statement, “There is no such thing as free lunch.”

And I would like to suggest that our tax liabilities represent that which we owe unto Caesar in return for the material blessings and luxuries that we enjoy under Caesar’s system.

Remember that the Pharisees, who were admonished to "Render unto Caesar the things that are Caesar’s,” had confessed their involvement in the Roman economic system by their possession of Caesar’s coinage.

As Bro. Mason has so ably pointed out, it is within our power to arrange our affairs in such a way that Caesar is also willing to reduce our tax liability if we are willing to give the money unto God.

Unfortunately, it costs us 100 cents to give a dollar unto God through the church, and only 20 cents if we elect to pay the tax and keep the dollar for ourselves.

The issue brought news that the Central Conference of American Rabbis had decided to resist the phone tax corporately:

In protest against the war in Vietnam, the Central Conference of American Rabbis (CCAR) has instructed its executive vice-president to withhold payment of the federal telephone excise tax which, it said, supports the Vietnam war.

The CCAR said it is the first Jewish organization to approve this act of civil disobedience in protest of the Vietnam war.

The action was taken after consultation with lawyers.

At the same time, the Reform rabbis urged in a resolution the movement’s sister institutions — the Hebrew Union College — Jewish Institute of Religion and the Union of American Hebrew Congregations — to follow a similar course of action.

Individual members of the conference were called upon “as an act of personal moral responsibility” to withhold the telephone tax.

The CCAR has protested the Vietnam war .

A report on the “Lamb’s War” camp meeting noted that a war tax resistance break-out group had formed.

A pseudonymous “Letter to My Home Church” reprinted in the issue mentioned how uncomfortable the churchgoer was with the casual taxpaying and patriotism encountered in the (also pseudonymous) congregation:

I have heard comments from you people like “I’m glad to pay my taxes for the privilege of living in a ‘free’ country.”

Oh yes, Cherrydale has certainly become patriotic.

We pay hundreds of thousands of dollars to IRS each year knowing that 60 percent goes to pay for killing.

The killers rest at ease knowing that they have allowed us an alternative.

We can be conscientious objectors.

There were objections to the “peace tax fund” legislation idea almost from the very beginning, as Richard Malishchak’s “Some Thoughts on Peace Taxes” () shows.

He makes a good effort at rebutting those objections, but it’s interesting to note how few of his defenses still apply to the pathetically watered-down Religious Freedom Peace Tax Fund Act that promoters are pushing today:

Should it be legal to pay for peace?

Some Thoughts on Peace Taxes

by Richard Malishchak

From The Reporter for Conscience Sake

The World Peace Tax Fund Act, which was introduced several months ago in the House of Representatives, has spawned controversy, strangely enough, among the very people and groups who are most in sympathy with the desired goals of the Act.

The Tax Fund Act would permit taxpayers to claim status as Conscientious Objectors to taxation for military purposes.

Small segments of the peace movement which have no interest in tax resistance/objection have naturally been cool to the proposed legislation.

But doubts have been raised even in the tax resistance movement.

The national War Tax Resistance office is deciding this month whether to throw their support behind the Tax Fund Act, and local WTR groups have been encouraging reader responses in their newsletters.

Being a human creation, the World Peace Tax Fund Act is flawed.

Some of the doubts expressed about the Act do have merit.

Yes, there is the danger that individuals would use a Conscientious Objector tax provision simply to soothe their own consciences, while taxes for military expenditures are collected from other people and the killing continues.

But has war tax resistance done any better on this point?

The tax resistance movement has yet to demonstrate that resistance alone is an effective tool.

The money is frequently collected anyway from the resister and used in the general fund, and the resister is liable to become an unwilling war-taxpayer.

Nor is a large-scale prison witness, large enough to effect a change in national consciousness by itself, a realistic possibility.

As important as acts of individual witness are, the military budget remains monstrous.

Ironically the military budget is likely to increase in the coming fiscal year (see the July Tax Talk from WTR, 339 Lafayette St., New York 10012).

It may also be true that legal channels for tax objection would siphon off some potential resisters into the “system.”

But would this number be significant in relation to the new objectors who would otherwise shy away from “illegitimate” protest?

Furthermore, if the government is still getting the money to buy death and suffering, what is the difference whether an individual protester is called a “resister” or an “objector”?

There is naturally a palpable personal difference between the witness of the objector and that of the resister.

But the World Peace Tax Fund Act is no threat at all to those who would continue to choose resistance.

Those who resist war taxation, like those who resist the draft, are in the vanguard of the peace movement and so must be especially careful to avoid the snare of moral elitism, a “more-resistant-than-thou” attitude that may obscure the common goal.

In the case of taxes, the common goal would seem to be to spend more on life and less on death.

And in addition to its overall importance, the Tax Fund Act contains two especially significant provisions toward this end.

First of all, the bill would provide for positive peace expenditures: the objector’s allotted “peace taxes” would not go into the general fund but into the World Peace Tax Fund and from there into designated peaceful activities.

Second, the Secretary of the Treasury would be obligated to inform every taxpayer, on the tax return instruction booklet, of the existence of the Peace Tax Fund and the qualifications for participation.

This provision could be momentous.

Combined with a vigorous tax counseling network, which is already beginning, it could become an effective consciousness-raising instrument.

In recent years, for example, the percentage of Conscientious Objectors recognized by the Selective Service System has been between one and two percent of the total number of registrants.

The vast majority of these men became Conscientious Objectors or recognized they were Conscientious Objectors after being confronted with an actual choice between morally opposite courses of action.

Most taxpayers, however, write their annual check to IRS or claim their refund with a minimum of decision-making.

If informed every year by the government in the official IRS publication that paying war taxes is not an inevitability, would one or two out of every 100 taxpayers choose to pay for peace instead?

If yes, the impact would be far beyond what tax resistance alone can achieve.

Admittedly a hopeful answer to this question assumes a basic “good will” on the part of most Americans, and that lack of information is the best ally of the war makers.

Yet how many of today’s draft Conscientious Objectors knew that they were Conscientious Objectors before they registered for the draft or before they became “draft-eligible”?

Not even a local draft board would deny a Conscientious Objector claim on the grounds that the registrant was not born a Conscientious Objector.

In the words of Joan Baez’ new album, which she dedicates in part to war tax refusal, more and more people must be encouraged to “come from the shadows.”

This is exactly what a Conscientious Objector tax provision would do.

(A recent Detroit poll, incidentally, showed support for the war tax refusal of Jane Hart, wife of the Michigan Senator, by 55 percent of the survey sample.)

If the Tax Fund Act does not cut the military budget directly, it would at least be likely to help produce an awareness of government expenditures that will cause people to think about, and consciously choose, to buy either peace or war, rather than passively “permitting” the government to buy war on their behalf.

This public awareness of where their dollars are going is, in turn, bound to be reflected in the actions of voter-conscious legislators.

If the people truly want peace, it will be easier for them to have it.

The World Peace Tax Fund Act is an important piece of legislation.

It will need all the help it can get, first to be taken seriously by “old guard” Congressmen, and later to be pushed through the wall of opposition that will form.

Draft resisters, military Conscientious Objectors, draft Conscientious Objectors, and tax resisters must begin to form the wedge of support behind this bill.

No one else will.

In “Thankful for What, When You Have All You Need?” (), Atlee Beechy wrote, “We may not be able to do too much about our governments’ (U.S. and Canada) priorities but we should be able to make a frontal attack on our priorities as Christians.

Is it my responsibility that my tax dollars go for military purposes?”

Finally, a report on the MCC Peace Assembly noted that there was a break-out group to discuss war tax resistance.

And “Stan Hostetter publicly declared his objection to war taxes and presented a check to the MCC Peace Section in lieu of tax payments which would be used for war.”