IRS figures show that 0.65 percent of all individual taxpayers — roughly one in 150 — were audited in , up from 0.57 percent the year before.

The audit rate among taxpayers with incomes of $100,000 or more rose to 1.06 percent from 0.86 percent.

In , by contrast, the overall audit rate for individuals was 1.67 percent, and that for high-income taxpayers was 3.21 percent.…

The agency also pointed to a more than 9 percent jump — to $35.5 billion — in money collected from taxpayers as a result of enforcement efforts.

The amount had been nearly flat at about $32 billion for .

At the same time, Everson said, IRS surveys indicate that the number of Americans who “believe it is okay to cheat on their taxes,” had risen to 17 percent , from 11 percent in .…

Much of the recent rise in audits was among what the IRS calls correspondence audits, in which the agency writes a letter to a taxpayer asking him or her to justify something on the return, such as the amount of mortgage interest deducted.

“Field” audits, in which the taxpayer meets face to face with an IRS employee, climbed slightly to 206,457 in from 205,134 .

In , there were 761,850 field audits, according to agency figures.…

The IRS figures also noted a continuing upturn in the number of levies, liens and seizures — key collection tools whose use fell drastically in the wake of Senate Finance Committee hearings in that were highly critical of the agency and resulted in enactment of the reform law.

As with audits, though, all three remained far below levels of the .

Seizures of taxpayer property declined the most: 399 compared with 10,449 in .

America’s largest corporations are less likely to face an Internal Revenue Service audit than at any time in the past decade.…

IRS statistics show that the number of corporate audits has tumbled , when 2 percent of all corporations and 26 percent of companies with more than $10 million in assets were audited.

, 0.87 percent of all corporations and 12 percent of the $10 million-plus companies were audited.

There’s more money to be made by auditing big corporations rather than ordinary schmoes, you’d think, right?

Well, maybe, but it’s harder to get at because the corporations are better able to fight back.

Here’s how IRS Commissioner Mark Everson put it :

“The length of time it takes us to complete the audit of a large, complex corporation is five years from the date the return is filed, which in most cases is already eight and one-half months after year end.

And these figures don’t include the appeals process, which runs another two years before the matter is settled or goes to court.

That means that half of our current inventory of large cases is from .

In today’s rapidly changing world, we might as well be looking at transactions from the Civil War.”

In recent Picket Line entries I’ve taken note of the annual April IRS ritual of puffing up its chest and talking tough about audits and enforcement — usually accompanied by a handful of well-timed indictments.

, the New York Times has crunched the numbers for us, and… yeah: turns out it’s all bluster.

Audits slipped again in , continuing a trend that’s been going on for .

The IRS, intensifying its crackdown on tax dodgers, plans to increase the number of tax audits it conducts .

The agency will focus more of its resources investigating taxpayers with incomes of $100,000 and above.

Agents will also examine more returns of high-income taxpayers in search of what they call abusive shelters, or transactions with no real economic purpose other than dodging taxes.

The agency will devote particular attention to abusive transactions involving parking money in offshore accounts.

While IRS officials won’t discuss specifics of audit targets, they are expected to focus more on self-employed workers who deal largely in cash.

Congress recently raised the IRS budget to $10.68 billion, which includes an increase in money earmarked for enforcement activities.

The Transactional Records Access Clearinghouse keeps a close eye on what the U.S. government is up to, and can be pretty relentless in trying to shine a light in the dark corners of the bureaucracy.

They’ve battled the IRS in court to try to get the agency to be more forthcoming with its statistics, and they won, but the IRS continues to drag its heels.

[O]nly 30 of the nation’s thousands of millionaires were subject to a face-to-face IRS audit in .

The very small number selected for the traditional and sometimes intensive audits were drawn from 184,054 individual tax returns reporting a total positive income of $1 million or more.

…the audit rate for America’s wealthiest taxpayers is substantially lower than for the poorest.…

Restricting the comparison to the agency’s comprehensive face-to-face audits, taxpayers reporting less than $25,000 in total positive income were six times more likely to be audited than those reporting $200,000 or more in income.

When the simpler and far more common correspondence audits are combined with the face-to-face audits, the poor taxpayers were still almost twice as likely to be audited as the wealthy.

And there’s more in the report.

The overall gist of it seems to be that the IRS is inflating its audit numbers by targeting the returns of poorer people and smaller businesses — both because their returns tend to be simpler and easier to audit, and because the people who file such returns have a harder time fighting back.

See the IRS response here.

They claim that the audit numbers that TRAC reports for millionaires are the result of the IRS changing the way it reports its data, and don’t accurately represent the rate of audits.

In war tax resistance circles, there have been whispers of a recent increase in the speed and number of IRS enforcement actions such as liens and levies.

The bottom line for our enforcement efforts shows that dollars collected rose again last year.

There’s a strong trend line going up.

was a watershed year for us, with a number of big initiatives that helped push enforcement revenues up 10% to $47.3 billion.

In , enforcement revenues — the monies we get from our collection, examination, and document matching activities — increased to a record $48.7 billion.

The press release breaks down the numbers a little more thoroughly.

For instance, sure enough:

In our collection activities, levies and liens continue to top their levels.

Levies increased by 36% to 3,742,276. Liens rose nearly 20% to 629,813.

These numbers are data but the IRS seems over-eager to jump from that to conclusions about the underlying situation.

Are increased enforcement efforts leading to more enforcement revenue, or is there just more tax money in general lying around for audits to discover — either because improving financial markets have caused people and corporations to owe more than in recent years or because they are more likely to be trying to illegally evade their taxes?

Hard to say.

I’m even more skeptical of the IRS’s own spin on the numbers when I learn how resistant the agency is to providing the raw data to groups like Transactional Records Access Clearinghouse so that they can do independent analyses.

(TRAC characterizes it as “continuing intransigence and unwillingness to providing public access to detailed statistics about many agency activities, along with a closed-door policy on releasing any meaningful results from taxpayer-financed studies on how our tax system is functioning.”)

Today, for instance, TRAC released its own analysis of IRS audit numbers for big corporations (which “controlled 90% of all corporate assets and received 87% of all the corporate income”).

TRAC finds that “the annual audit rate for these corporations, all with assets of $250 million or more, while increasing in has now receded to about the level it was in and is much lower than levels that prevailed a decade or more ago.”

In addition, the number of hours that the IRS spends on each of these audits has declined.

In , it spent 1,210 hours per audit of such corporations; in , it spent 958. But perhaps it is just being more efficient and effective and doesn’t need to spend as much time as it used to?

TRAC’s opinion:

Some economists and tax experts believe that other explanations are possible, namely that a massive surge in non-compliance is believed to have swept through corporate America.

Although government enforcement activities can be measured, accurately tracking the number individuals or corporations who secretly decide to break the law is extremely difficult.

In recent years, however, [IRS] Commissioner Everson, his immediate predecessor and many others have argued that case-by-case evidence strongly suggests more and more corporations are skirting the law.

The bottom line: a real increase in the number of non-compliant taxpayers may explain the increase in enforcement revenues.

Therefore, while it is true that enforcement dollars are up, particularly for recommended audit adjustments among the largest corporations, the reason remains unclear.

In the face of lowered coverage and audit hours, this increase could be due to a more effective IRS audit program.

However, if corporate noncompliance is up, it could be that the dollars require less effort to find.

TIGTA notes that while the IRS has been increasing its enforcement activity (audits, and so forth) in recent years, this isn’t so impressive when seen on a somewhat larger timescale:

Many compliance activities increased and results improved during .

, the IRS has been reversing many of the downward trends in compliance activities that had occurred in prior years.…

The use of collection enforcement tools was greater and enforcement revenue collected continued to increase (to $48.7 billion), but the total dollar amount of uncollected liabilities increased to $271 billion.…

The overall percentage of tax returns examined increased by just over 4%, and the number of field examiners increased by just over 9%.

However, the percentage of tax returns examined is still 27% lower than it was in .

The number of tax returns of individuals examined increased.

However, 82% were conducted via correspondence examinations, which are usually not as comprehensive as face‑to‑face examinations.

The number of corporate tax returns examined decreased 1%, after increasing 71% in .

However, the number of these examinations has decreased 59% since .

The IRS has just released its audit figures for .

Audits are up across-the-board.

This in spite of not having significantly more enforcement personnel or budget.

In the past, a closer look at the numbers has shown that they’ve accomplished this miracle by emphasizing “correspondence” audits over “field” audits.

It looks like this is again the case.

While about three-quarters of the total audits the IRS conducts are correspondence audits, more than 90% of the increase in audits this year comes from correspondence audits.

The agency also seems to be backing off on audits of large corporations.

These have the potential to be big-bucks items, but they also take a lot of time and a lot of personnel — both of which can be redeployed to increase the numbers elsewhere.

Indeed, the larger the large corporation, the stronger the drop-off in enforcement in recent years.

Corporations in the $50–100 million asset range have seen their likelihood of an audit drop from 16.4% to 11.4%; those in the $100–250 million range have gone from 17.5% to 12.1%; those above $250 million have dropped from 44.1% to 27.2%.

The strategy may be a wise one.

“Overall, enforcement revenue reached $59.2 billion, up from $48.7 billion in and nearly $34.1 billion in .”

On the other hand, this increase could reflect increased tax evasion rather than more effective enforcement — the same sized slice but of a larger pie.

Levies, liens, and seizures are all up over last year’s numbers.

After last year’s leap over the previous year from 2,743,577 levies to 3,742,276, this year’s increase is much more modest: to 3,757,190.

The IRS did fewer audits and collected less money in its enforcement efforts than in .

A new report says that with 2% fewer employees working on enforcement cases, the amount of money the agency collected in this way dropped by almost 5%.

The rate of audits fell across the board for both businesses and individuals — following a recent trend, this auditing drop was most dramatic for wealthy individuals and big businesses.

You may remember that Indian Prime Minister Modi abruptly removed high-denomination bank notes from the ranks of legal tender in . This was meant to strike a knockout-blow at the underground economy by forcing people to use more legible, traceable economic transactions than anonymous cash. It doesn’t seem to have worked. Despite the significant short-term inconvenience and blow to the economy, the amount of cash currency in circulation quickly recovered to its previous levels and is now back on-trend to where it was before the experiment. You may have heard calls to eliminate the U.S. $100 bill, for similar motives. This experience may discourage such an effort.

The National War Tax Resistance Coordinating Committee held a national conference in Washington, D.C. .

Here’s a write-up by one of the attendees. Unfortunately they got tangled up in ongoing actions by leftist activists who were trying to occupy the Venezualan embassy there on behalf of the brutal, disastrous Maduro regime.

It has been a disappointing thing to see groups like NWTRCC, CodePink, Veterans for Peace, and United for Peace and Justice carrying water for the cruel Maduro tyranny as though that were the only way to oppose disingenuous U.S. machinations there.

It puts a shameful stain on what’s left of the U.S. peace movement every time a group like this uses a phrase like “the legitimate democratic Maduro government of Venezuela”.

A number of items that have been in the news lately concern how the U.S. tax system has become increasingly corrupt and imbalanced in favor of wealthy tax evaders.

Stories like this tend to damage what’s known in tax wonk circles as “taxpayer morale” — the willingness of citizens to pay their taxes without evasion or the necessity of harsh arm-twisting and draconian oversight.

For example:

The New York Times pointed out that in California, local governments and corporations have rigged the sales tax system in such a way that a portion of the sales tax people pay is gifted to the same companies who collect it.

In other words, the sales tax becomes a “bonus profit” to those companies, collected from consumers and enforced by law.

Millions of former U.S. tax filers appear to have dropped out — not filing returns in the last filing season.

One theory is that the tax reform legislation that came into effect last year caused some people to owe where they hadn’t before, or to owe more, and that they decided not to file as a result.

Three million people who received refunds in didn’t file at all in .

There’s been another report put out about the “tax gap” (the difference between what’s owed and what’s collected) in the U.S.

However it still uses largely stale numbers, updating them largely based on estimates and trends rather than evidence.

Some links from here and there:

Logan Marie Glitterbomb, at the Center for a Stateless Society, advocates a campaign of gradually transitioning to cryptocurrency as a way of facilitating war tax resistance.

Such a campaign would “allow for us to take direct action against the war machine, by refusing to fund it.

The campaign encourages people to move at least $1 of fiat per day into their choice of cryptocurrency.

The goal is to aid individuals in a gradual transition away from fiat and into using crypto as their primary currency without asking people to dive in all at once.”

The Civic Alliance for Justice and Democracy, a movement opposing the Ortega regime in Nicaragua, is trying to gather support for a civil disobedience campaign that would feature tax resistance as a key tactic: “Tax resistance to withhold economic oxygen from the regime for repression.”

The “Blue and White National Unity” group has signed on to the call.

They hope to pressure the regime to release political prisoners and to fulfill agreements it made in negotiations during previous strikes.

The Ortega regime released 100 political prisoners to try to lure the opposition back to the negotiating table (not including tax resistance leader Irlanda Jerez, who has been tortured in prison, and is still being held).

The IRS is redesigning its W-4 form.

This is the form that employees fill out when they start a new job, or when they want to change how much tax is withheld from their paychecks.

The new form, though still in the drafting process, looks like it’s going to be much more complicated.

This may also, alas, complicate the process for people wanting to get started with tax resistance by reducing the amount withheld from their paychecks.

I thought this was interesting: I’d heard that the IRS could step in and claim top priority in a bankruptcy — pushing other creditors aside as it helps itself to what’s left of your assets.

But what I didn’t realize is that this apparently only applies to the tax part of your tax debt: not to any interest & penalties the IRS has applied.

For those, the agency has to get in line like everyone else.

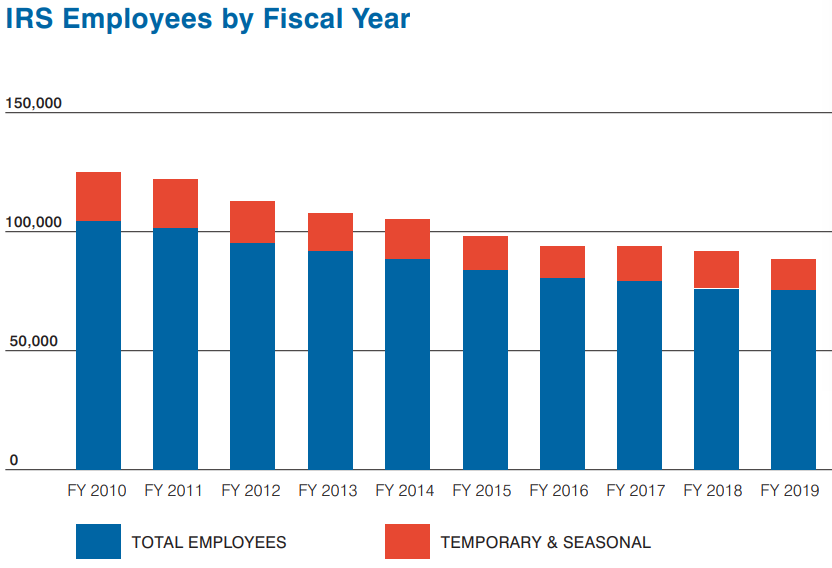

The IRS lost more than 29,618 full time positions … These losses directly correlate with a steady decline in the number of individual audits during the past nine years.

The IRS anticipates up to 31 percent of its current workforce (about 19,719 full-time employees) will retire within , creating a significant risk of a large knowledge and experience gap for the nation’s tax agency.

The audit rate for individuals declined to 0.45% for , down from 0.9% in , according to IRS data.

Even a decade ago, the audit rate was sharply lower than in , when the agency audited about 2.5% of individual returns.

The IRS now has fewer auditors than at any point since World War Ⅱ.

One of the enforcement challenges the report names is the “syndicated conservation easement” dodge.

Let’s say you own a big hunk of property somewhere.

Instead of developing it, you donate the right to develop on the property to a land trust or some such organization that is dedicated to preserving wetlands or the greenbelt or something, and so your property goes undeveloped.

That forgone development was worth something, and in giving it away you gave away something of value, so you can get a tax deduction for that.

But the scam part comes in by fudging how much the foregone development is worth.

You basically pay someone to sign off on a phoney assessment that inflates the value of the donation way beyond what it’s worth.

Furthermore you then sell out bits of this potential tax deduction to other taxpayers (that’s the “syndicated” part), who only have to pay in the real value of the property in order to get their cut.

So they get a deduction that far exceeds their investment.

But it would take resources for the IRS to figure out the source of the deduction, trace it back to the property in question, figure out what’s fishy about the assessment, get it reassessed, prosecute someone, and so forth.

And the IRS is doing just that, with dozens of court cases pending.

But they’re popping up quicker than the IRS can suppress them.

A recent news article put it this way:

The imperviousness of the scam’s promoters and investors has left tax experts flummoxed.

“Boy, it isn’t like the old days, when people were fearful of the IRS,” said Steven Miller, who oversaw enforcement and tax-exempt organizations during his 25 years at the IRS and is now national tax director with consulting firm Alliantgroup.

“I’m worried people aren’t afraid of the cop on the beat any more.”

[T]he syndicated deals are structured in a way that insulate the wealthy individual investors, leaving the promoters and outside lawyers to do battle with the IRS.

Their fight is fueled with “audit reserves” of as much as $1 million that are set aside as part of every syndication partnership.

Some deals even offer “audit insurance” from Lloyds of London to offset disallowed write-offs.

Anabaptist World features a letter from Harold A. Penner urging Mennonites to redirect their war taxes to the Mennonite Church USA Peace Tax Fund.

And here is some more news about the ongoing troubles at the IRS.

This CNN Business story goes in some depth into how a loose coalition of activists forced the IRS into an embarrassing and costly retreat from its plan to use facial recognition technology to verify the identity of taxpayers using its online account portal.

This note from the National Taxpayer Advocate gives more details about the IRS plan to stop issuing certain enforcement action notices while it tries to deal with the enormous backlog of unprocessed returns and other correspondence.

For example: “If a taxpayer’s account has been assigned to one of the IRS’s automated levy programs (ALPs), the IRS is also suspending the levies made by those programs…”

The agency will also not be able to pursue many new levies because in order to do so, it must first send the taxpayer a letter informing them of their right to request a Collection Due Process hearing, and they’ve temporarily stopped the automatic sending of those letters.

Some 53,000 IRS employees are still on remote work — about two-thirds of the agency’s workforce, which an IRS spokesperson characterized as “a maximized telework posture.”

But privacy rules prevent remote processing of the millions of paper tax returns mailed to the IRS, as well as the examination of returns with discrepancies from IRS records, the issuance of refunds and dealing with other taxpayer mail.

The Transactional Records Access Clearinghouse at Syracuse University issued a report showing that the IRS audits the poorest American households at five times the rate as the rest.

This seems to be an effect of the agency’s plummeting rate of audits of the well-to-do combined with its increasing use of cheap-and-easy “correspondence audits” against low-income taxpayers who apply for the Earned Income Tax Credit.

As the National Taxpayer Advocate puts it:

The IRS correspondence audit process is structured to expend the least amount of resources to conduct the largest number of examinations — resulting in the lowest level of customer service to taxpayers having the greatest need for assistance.

Last Summer, the U.S. House of Representatives passed a spending bill that would have boosted the IRS budget.

That bill got bogged down in Congress before anything could come of it.

A recent appropriations bill resurrected the IRS budget boost, but pared it way back, so now the agency budget will only rise by 6%.

These days that’s hardly enough to keep up with inflation.

And the appropriations bill restricts how various parts of the increase can be spent, so some parts of the agency budget — tax enforcement for example — will see even smaller increases.