How you can resist funding the government →

the tax resistance movement →

birth of the modern American war tax resistance movement →

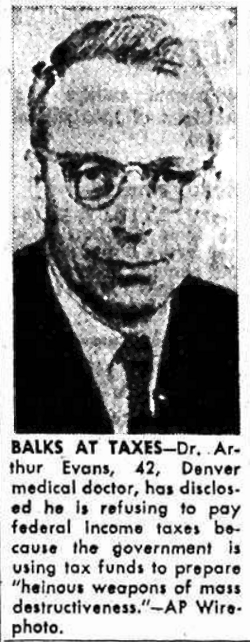

Arthur Evans

Arthur Evans, one of the few Americans to spend any time behind bars for war tax resistance, died at age 89.

In , Evans defied an order to turn over his financial records to the government and was jailed for 90 days.

From the

New York Times:

Pacifist Ends Jail Term

Denver, (AP) —

Dr. Arthur Evans, a Quaker,

left the city jail after serving a

90-day sentence for refusing to turn over his financial records to the

Internal Revenue Service.

Dr. Evans, a Denver physician,

has for years refused to pay that portion of his Federal income taxes that he

says is earmarked for military spending.

What happened between the time when Peacemakers was leading the war tax resistance charge and , when the National War Tax Resistance Coordinating Committee was founded?

There was another group, simply called “National War Tax Resistance,” that took the reins during the Vietnam War.

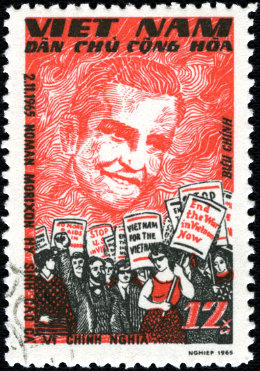

was, as the CNVA Bulletin declared, “The Year of Vietnam.”

Picketing and sit-downs across the country marked the announcement of the first US bombing of North Vietnam on .

These continued throughout the month and much effort was expended gathering signatures for a new appeal, the Declaration of Conscience, circulated by radical pacifist groups, urging civil disobedience.

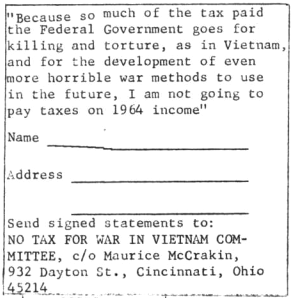

The Peacemakers group in Cincinnati organized a “No Tax for War in Vietnam Committee” calling for tax resistance.

In a separate group — War Tax Resistance, coordinated by Bob Calvert — was established and at the time included some 200 local tax resistance centers across the country.

Nonpayment of war taxes, practiced by Quakers and others, disappeared as a pacifist testimony soon after the Civil War and Thoreau’s famous stand against the U.S. foray in Mexico.

It first reappeared in World War Ⅱ when a few widely scattered individuals refused to pay federal taxes on the grounds that there was no way to prevent a significant part of their money from being used for military purposes.

One resister, Ernest Bromley, was prosecuted and imprisoned for his refusal.

Many others began to inform the Internal Revenue Service that payment violated their principles.

The enactment during World War Ⅱ of a measure which required employers to withhold taxes from their employees caused particular difficulties for pacifists and led to the formation of Peacemakers in .

A Peacemaker committee promoted tax refusal and provided research, literature, action suggestions, and publicity for those in the tax resistance movement.

Although many hundreds of people were refusing to pay income taxes during , the government prosecuted and imprisoned only six: James Otsuka of Indiana, Maurice McCrackin of Ohio, Eroseanna Robinson of Illinois, Walter Gormly of Iowa, Arthur Evans of Colorado, and Neil Haworth of Connecticut.

These imprisonments and the seizure of a few cars and houses by the IRS, served to highlight the tax refusal testimony and establish it as a major nonviolent principle and tactic.

Tax resistance, like other forms of opposition to the military, increased dramatically during the Vietnam War.

In the federal government levied an additional tax on every private telephone, and in a rare moment of candor, admitted that the money would help subsidize the war in Indochina.

Peacemakers, the War Resisters League, and other nonviolent groups urged refusal of this tax and in the following years countless thousands heeded their call.

Under the leadership of Bob and Angie Calvert, War Tax Resistance was formed in as a separate organization to investigate all aspects and ramifications of conscientious tax refusal.

During the war there were over 200 local war tax resistance centers, as well as a number of “alternative life funds” which rechanneled refused tax money back into the local community for constructive purposes.

Many of these continued after the end of the war.

The tactic of claiming enough dependents so that no income tax would be withheld became more widespread as the Vietnam war continued.

Often the tax refuser would make clear the moral grounds for the protest by listing, for example, “all the Vietnamese” as dependents.

Refusing to pay for war by claiming excessive exemptions brought particularly strong response from the government.

A number of people were prosecuted and imprisoned: Jim Shea, Karl Meyer, William Himmelbauer, Mark Riley, Ellis Rece, Carole Nelson, John Leininger, and Martha Tranquilli (a 64-year-old grandmother and nurse).

The tax resistance movement continued after the war and grew to include both pacifists and non-pacifists who could no longer in conscience support the military priorities of the government.

As more and more tax money was directed toward the [Reagan era] military buildup, many activists revived interest in war tax resistance.

Protests were organized each year, and individual resisters tried a variety of means to deny the government money for war.

In , demonstrations were held in Dallas, Atlanta, San Francisco, Los Angeles and other cities and 24 people were arrested at IRS offices in New York City.

The following year, the National War Tax Resistance Coordinating Committee was formed by the Center on Law and Pacifism, Conscience and Military Tax Campaign, WRL, Peacemakers and eighty local groups.

featured the largest show of war tax resistance actions in , including Ralph Dull, an Ohio farmer and tax resister , who drove a truckload of grain to the IRS office as payment for his taxes.

The IRS instituted a “frivolous returns” penalty to discourage the filing of returns with any but the requested information, and some resisters began an insurance fund, pooling their resources to pay fines and interest charges levied against fellow tax resisters.

A friend of mine, 43 year old Arthur Evans, a medical doctor with offices in

Denver, Colorado, was sent to jail by Judge Alfred A. Arraj of the Denver district court, for his

refusal to pay his part of the income tax (about 50%) which would be used for

the annihilation of the human race. He sent it, instead, to the United

Nations, to promote peace in the world.

In a statement circulated by him to his friends he says in part: “My lawyer,

the judge, and other lawyers, tell me that there is no law, no constitutional

provision that provides for the individual to refuse to pay taxes for

annihilation. So I go to jail, for I will not, I cannot in conscience be

party to financing the means to annihilation. The Jews under Hitler were

taxed to buy their crematoriums. The same happens here — but it is not only

the Jews who finance their means of destruction — it is almost every income

earner in the United States. This is called democratic because we are all

taxed alike.”

Letters of approval have been pouring in to

Dr. Evans, and since he is

only allowed to write very few, his mother in Philadelphia has taken up the

task of acknowledging them, sending at the same time a typewritten sheet

explaining the affair in detail.

, another

man (who is now considered one of America’s greatest) was picked up in

Concord, Mass. on the

way to his shoemaker, and brought to jail because he had refused to pay his

poll tax to a government he thought misguided and evil because it allowed

slavery and was also at that time waging a war with Mexico to extend its

slaveholding territory. I mean, of course, Henry David Thoreau. Out of that

incident came his famous Civil Disobedience, which

influenced Gandhi and Nehru; Thoreau’s ideas are very much alive in many

parts of the globe today. Strange, how history repeats itself!

Some day, perhaps after another century (if we escape a war of annihilation),

Dr. Evans will be spoken of

with appreciation and respect. We have a way of crucifying the great while

they are with us, and of exalting them after they are gone. At present a

medical doctor is doing laundry duty as a “trusty” in the Jefferson County

Jail in Golden, Colorado, and he may like to hear from you.

Adele Wehmeyer

Rallies outside the courthouse or prison are one way of supporting resisters who are looking at doing time for taking their stand (see The Picket Line for ), and supporting their families while they’re being held captive is another (see The Picket Line for ).

Other ways to show support are to accompany resisters as they go to prison, to visit them or correspond with them while they are inside, and to be there to meet them when they are released.

Today I’ll give some examples of these ways of showing support for imprisoned tax resisters.

Sylvia Hardy

Accompanying resisters to prison

When elderly council tax rebel Sylvia Hardy was threatened with jail in , her supporters organized a convoy of cars to accompany her to the jail as a show of support.

In , Annuity Tax resisters in Edinburgh, Scotland, would go to prison in a parade of protesters.

One description of such a procession read:

[H]e was marched off to the Calton Jail, accompanied by the usual hasty muster of people carrying flags and poles, having placards on which were a variety of devices and inscriptions…

His daughter, a fine young woman, in a fit of heroic indignation which overmastered her grief and the natural timidity of her sex, seized one of the flags, and would have walked before her father to prison with the crowd, but was prevented by him and the interference of the humane bystanders.

When Kate Harvey went to prison for her resistance as part of the Women’s Tax Resistance League, fellow-resisters Charlotte Despard and Mary Anderson accompanied her to the prison gates.

When Elizabeth Knight was imprisoned on similar charges, she was accompanied to Holloway by resisters Florence Underwood and Isabel Tippett.

Visiting resisters in prison

Thomas Story, an English Quaker who was visiting the American colonies, was able to help two Quakers from Rhode Island who were in prison for not paying a militia exemption tax after having been drafted and refusing to fight.

Story helped them hold a Quaker meeting in the prison itself, and also (having some legal experience) tried to assist them in court.

When Zerah Colburn Whipple was imprisoned for failing to pay a war tax in , it was a comfort to him to have friends on the outside trying to get in.

He wrote: “Our friend John J. Copp, proved himself a true friend indeed.

Knowing that I would be lonely in the jail, he visited me every day after he learned that I was there, and when the keeper refused him admission, he demanded it as his right to visit his client, and claimed the right to see me alone too, which was granted.”

The Trafalgar Square Defendants’ Campaign helped to organize prison visits to people who had been imprisoned in the Poll Tax rebellion.

Corresponding with imprisoned resisters

I’ve done a lot of volunteer work with the Prison Literature Project in Berkeley, California.

Most of the letters we get are from prisoners requesting books — which makes sense, because that’s the sort of letter we explicitly ask for.

But a pretty hefty percentage of the letters we get are just expressing gratitude for the books and letters we previously sent — heartfelt, often heartbreaking gratitude, especially since many of the prisoners are of limited means and can barely afford to put a stamp on a letter.

This impresses on me how meaningful it is for people behind bars to get letters from friends outside.

The Anarchist Black Cross of New York City held a letter-writing evening for imprisoned war tax resister Carlos Steward in .

Brian Wright was the first person thrown in prison for Poll Tax resistance, during the rebellion in the United Kingdom, in .

While there he received over 800 cards and letters from supporters.

The Trafalgar Square Defendants’ Campaign made it a policy to ensure that at least one personal letter per prisoner per week came from someone in the campaign.

When Kate Harvey had barricaded herself in her own home to try to defeat government attempts to seize her property for taxes, a supporter sent her a poem to keep her mood up:

Good luck, my friend, I wish to thee,

In thy brave fight ’gainst tyranny.

Bracken Hill Siege will bring good cheer

To those who hold our Freedom dear,

And fight the good fight far and near.

And when oppression is out-done,

And Liberty, at last, is won,

When women civic rights possess,

They’ll think, I hope, with thankfulness,

Of those who bore the battle’s stress.

When a Colorado doctor was jailed for refusing to pay federal income taxes that fund weapons of mass destruction, it was reported that “[l]etters of approval have been pouring in to Dr. Evans, and since he is only allowed to write very few, his mother in Philadelphia has taken up the task of acknowledging them, sending at the same time a typewritten sheet explaining the affair in detail.”

Welcoming resisters back from prison

The campaign to resist Thatcher’s Poll Tax organized a march to Brixton Prison, which held most of the resisters then in custody.

Police attacked the march and arrested 135 people.

“That evening,” says campaign volunteer Danny Burns, “volunteers were sent to every police station to welcome those who were released on bail.”

This served not only to show solidarity, but also to make the arrested people aware of the legal support available to them and to encourage them to cooperate in their defense.

When Constance Andrews of the Women’s Tax Resistance League was released after having been jailed for a week for failure to pay a dog license tax, “a very large crowd — described in the local press as ‘an immense gathering’ — collected outside the prison to cheer Miss Andrews on her release.”

A procession with suffrage banners walked along with Andrews as she walked from the prison to a reception held in her honor.

When Mark Wilks was released from prison for failure to pay his wife’s income tax in , the Women’s Tax Resistance League held a reception for the Wilkses, saying that “not only do they wish to do honour to those who have made such a brave stand for tax resistance, but to use the occasion, as one of many others, to keep before the public mind the necessity for the alteration of the laws.”

Katsuki James Otsuka served a 120-day sentence for refusing to pay war taxes to the U.S. government (and then refusing to pay the fine he was given for his initial refusal) in .

A group of supporters demonstrated outside the prison at the time of his anticipated release, though “four carloads of state police” broke up the demonstration at one point, smashing a picket sign that read “You did right in refusing to pay taxes for A-bombs.”

During the white supremacist rebellion against the Reconstruction state government in Louisiana a man named Edward Booth was imprisoned for 24 hours for refusing to pay a license tax.

[I]t was agreed among his immediate personal friends, the members of the tax resisting association and their sympathizers, to make a grand demonstration, at the hour of his release, and escort him to his place of business, to show their sympathies, and in what approbation he was held for having become the object of an oppression, in the defence of his personal rights.

Before the hour of his release, a large concourse of people assembled before the doors of the prison, to hail the deliverance of the prisoner, and the anteroom was thronged with friends anxious to proffer the hand of sympathy and condolence. …

Mr. Booth filed out of the room and stepped into a carriage in waiting, amid rousing cheers and a stirring air from the band.

The carriage led off, followed by the band and the large concourse of people, who gradually fell into an orderly line of twos, to the number of about 400.

The marchers hung an effigy of the Reconstruction governor from a lamp post while loudly cheering.

When the procession reached Booth’s place of business, he gave a speech thanking the crowd for their support and urging them to renew their resistance.

William Tait, editor of Tait’s Edinburgh Magazine, was imprisoned for refusing to pay the Annuity Tax in that city, which went to support the official church, of which Tait was not a member.

After four days, he was released.

The Scotsman covered the story:

[Tait] stepped into the open carriage, drawn by four horses, which stood on the street…

At this moment, one of the gentlemen in the carriage, waving his hat, proposed three cheers for the King, and three cheers for Mr. Tait, — both of which propositions were most enthusiastically carried into effect.

The procession was then about to move off, when, much against the will of Mr. Tait and the Committee, the crowd took the horses from the carriage, and with ropes drew it along the route of procession…

As the procession marched along, it was joined by several other trades, who had been late in getting ready; and seldom have we seen such a dense mass of individuals as Prince’s Street presented on this occasion.

In the procession alone, there were not fewer than 8,000 individuals; and we are sure that the spectators were more than thrice as numerous.

Mr. Tait was frequently cheered as he passed along, — and never, but on the occasion of the Reform Bill, was a more unanimous feeling witnessed than on that which brought the people together yesterday afternoon.

Here are a handful of artifacts relating to the American war tax resistance

movement circa .

First, some relics that were filed alongside a letter from Herbert Sonthoff to

W. Walter Boyd (though I think this filing may be arbitrary and that the

letters are not related to each other):

At this late date it is pointless to muster the evidence which shows that the

war we are waging in Vietnam is wrong. By now you have decided for yourself

where you stand. In all probability, if you share our feelings about it, you

have expressed your objections both privately and publicly. You have witnessed

the small effect these protests have had on our government.

By ,

every American citizen must decide whether he will make a voluntary

contribution to the continuation of this war. After grave consideration, we

have decided that we can no longer do so, and that we will therefore withhold

all or part of the taxes due. The purpose of this letter is to call your

attention to the fact that a nationwide tax refusal campaign is in progress,

as stated in the accompanying announcement, and to urge you to consider

refusing to contribute voluntarily to this barbaric war.

Signed:

Prof. Warren Ambrose

Mathematics, M.I.T.

Dr. Donnell Boardman

Physician, Acton, Mass.

Mrs. Elizabeth Boardman

Acton, Mass.

Prof. Noam Chomsky

Linguistics, M.I.T.

Miss Barbara Deming

Writer, Wellfleet, Mass.

Prof. John Dolan

Philosophy, Chicago University

Prof. John Ek

Anthropology, Long Island University

Martha Bentley Hall

Musician, Brookline, Mass.

Dr. Thomas C. Hall

Physician, Brookline, Mass.

Rev. Arthur B. Jellis

First Parish in Concord, Unitarian-Universalist, Concord, Mass.

Prof. Donald Kalish

Philosophy, U.C.L.A.

Prof. Louis Kampf

Humanities, M.I.T.

Prof. Staughton Lynd

History, Yale University

Milton Mayer

Writer, Mass.

Prof. Jonathan Mirsky

Chinese Language and Literature, Dartmouth College

Prof. Sidney Morgenbesser

Philosophy, Columbia University

Prof. Wayne A. O’Neill

Graduate School of Education, Harvard University

Prof. Anatol Rapoport

Mental Health Research Institute, University of Michigan

Prof. Franz Schurmann

Center for Chinese Studies, University of Calif., Berkeley

Dr. Albert Szent Gyorgy

Institute for Muscle Research, Woods Hole, Mass.

Harold Tovish

Sculptor, Brookline, Mass.

Prof. Howard Zinn

Government, Boston University

* Institutions listed for informational

purposes only

P.S. The No Tax for

War Committee intends to make public the names of signers, hence if you wish

to add your signature, early return is desirable. Contributions are needed,

and checks should be made payable to the Committee.

The committee will publish the above statement with names of signers at tax

deadline — .

Send signed statements to: NO TAX FOR WAR COMMITTEE,

c/o

Rev. Maurice McCrackin,

932 Dayton St., Cincinnati,

Ohio 45214.

For additional copies of this form, put number you will distribute and name

and address on the following lines:

No. _____ Name ____________________

Address _________________________

Signers So Far

Meldon and Amy Acheson

Michael J. Ames

Alfred F. Andersen

Ross Anderson

Beulah K. Arndt

Joan Baez

Richard Baker

Bruce & Pam Beck

Ruth T. Best

Robert & Margaret Blood

Karel F. Botermans

Marion & Ernest Bromley

Edwin Brooks

A. Dale Brothington

Mrs. Lydia Bruns

Wendal Bull

Mrs. Dorothy Bucknell

John Burslem

Lindley J. Burton

Catharine J. Cadbury

Maris Cakars

Robert and Phyllis Calese

William N. Calloway

Betty Camp

Daryle V. Carter

Jared & Susan Carter

Horace & Beulah Champney

Ken & Peggy Champney

Hank & Henry Chapin

Holly Chenery

Richard A. Chinn

Naom [sic] Chomsky

John & Judy Christian

Gordon & Mary Christiansen

Peter Christiansen

Donald F. Cole

John Augustine Cook

Helen Marr Cook

Jack Coolidge, Jr.

Allen Cooper

Martin J. Corbin

Tom & Monica Cornell

Dorothy J. Cunningham

Jean DaCosta

Ann & William Davidon

Stanley F. Davis

Dorothy Day

Dave Dellinger

Barbara Deming

Robert Dewart

Ruth Dodd

John M. Dolan

Orin Doty

Allen Duberstein

Ralph Dull

Malcolm Dundas

Margaret E. Dungan

Henry Dyer

Susan Eanet

Bob Eaton

Marc Paul Edelman

Johan & Francis Eliot

Jerry Engelbach

George J. Etu, Jr.

Mary C. Eubanks

Arthur Evans

Jonathan Evans

William E. Evans

Pearl Ewald

Franklin Farmer

Bertha Faust

Dianne M. Feeley

Rice A. Felder

Henry A. Felisone

Mildred Fellin

Glenn Fisher

John Forbes

Don & Ann Fortenberry

Marion C. Frenyear

Ruth Gage-Colby

Lawrence H. Geller

Richard Ghelli

Charles Gibadlo

Bruce Glushakow

Walter Gormly

Arthur Goulston

Thomas Grabell

Steven Green

Walter Grengg

Joseph Gribbins

Kenneth Gross

John M. Grzywacz, Jr.

Catherine Guertin

David Hartsough

David Hartsough

Arthur Harvey

Janet Hawksley

James P. Hayes, Jr.

R.F. Helstern

Ammon Hennacy

Norman Henry

Robert Hickey

Dick & Heide Hiler

William Himelhoch

C.J. Hinke

Anthony Hinrichs

William M. Hodsdon

Irwin R. Hogenauer

Florence Howe

Donald & Mary Huck

Philip Isely

Michael Itkin

Charles T. Jackson

Paul Jacobs

Martin & Nancy Jezer

F. Robert Johnson

Woodbridge O. Johnson

Ashton & Marie Jones

Paul Jordan

Paul Keiser

Joel C. Kent

Roy C. Kepler

Paul & Pauline Kermiet

Peter Kiger

Richard King

H.A. Kreinkamp

Arthur & Margaret Landes

Paul Lauter

Peter and Marolyn Leach

Gertrud & George A. Lear, Jr.

Alan and Elin Learnard

Titus Lehman

Richard A. Lema

Florence Levinsohn

Elliot Linzer

David C. Lorenz

Preston B. Luitweiler

Bradford Lyttle

Adriann van L. Maas

Ben & Sue Mann

Paul and Salome Mann

Howard E. Marston, Sr.

Milton and Jane Mayer

Martin & Helen Mayfield

Maurice McCrackin

Lilian McFarland

Maureen & Felix McGowan

Maryann McNaughton

Gelston McNeil

Guy W. Meyer

Karl Meyer

David & Catherine Miller

James Missey

Mark Morris

Janet Murphy

Thomas P. Murray

Rosemary Nagy

Wally & Juanita Nelson

Marilyn Neuhauser

Neal D. Newby, Jr.

Miriam Nicholas

Robert B. Nichols

David Nolan

Raymond S. Olds

Wayne A. O’Neil

Michael O’Quin

Ruth Orcutt

Eleanor Ostroff

Doug Palmer

Malcolm & Margaret Parker

Jim Peck

Michael E. Pettie

John Pettigrew

Lydia H. Philips

Dean W. Plagowski

Jefferson Poland

A.J. Porth

Ralph Powell

Charles F. Purvis

Jean Putnam

Harriet Putterman

Robert Reitz

Ben & Helen Reyes

Elsa G. Richmond

Eroseanna Robinson

Pat Rusk

Joe & Helen Ryan

Paul Salstrom

Ira J. Sandperl

Jerry & Rae Schwartz

Martin Shepard

Richard T. Sherman

Louis Silverstein

T.W. Simer

Ann B. Sims

Jane Beverly Smith

Linda Smith

Thomas W. Smuda

Bob Speck

Elizabeth P. Steiner

Lee D. Stern

Beverly Sterner

Michael Stocker

Charles H. Straut, Jr.

Stephen Suffet

Albert & Joyce Sunderland, Jr.

Mr. & Mrs. Michael R. Sutter

Marjorie & Robert Swann

Oliver & Katherine Tatum

Gary G. Taylor

Harold Tovish

Joe & Cele Tuchinsky

Lloyd & Phyllis Tyler

Samuel R. Tyson

Ingegerd Uppman

Margaret von Selle

Mrs. Evelyn Wallace

Wilbur & Joan Ann Wallis

William & Mary Webb

Barbara Webster

John K. White

Willson Whitman

Denny & Ida Wilcher

Huw Williams

George & Lillian Willoughby

Bob Wilson

Emily T. Wilson

Jim & Raona Wilson

W.W. Wittkamper

Sylvia Woog

Wilmer & Mildred Young

Franklin Zahn

Betty & Louis Zemel

Vicki Jo Zilinkas

Following this was a page explaining how to go about resisting:

For those owing nothing because of the Withholding Tax.

Such persons write a letter to the Internal Revenue Service, to be filed

with the tax return, stating that the writer cannot in good conscience

help support the war in Vietnam, voluntarily. The writer

therefore requests a return of a percentage of the money collected from

his salary.

Note: Of course, the

IRS

will not return the money. However, the writer has refused to pay for the

war voluntarily and has put it in writing. This symbolic action

is not to be belittled since anybody who does this allies himself with

those who will withhold money due the IRS.

For those self-employed or owing money beyond what has been withheld from

salary.

Such persons write a letter to be filed with the tax return, stating that

the writer does not object to the income tax in principle, but will not,

as a matter of conscience, help pay for the war in Vietnam. The writer is

therefore withholding some or all of the tax due.

Note: In all cases, we recommend that copies of these letters be sent to the

President and to your Senators.

Remarks:

The Internal Revenue Service has the legal power to confiscate money due

it. They will get that money, one way or another. However, to obstruct the

IRS

from collecting money due (by not filing a return at all, for example)

seems less important to us than the fact that each is refusing to pay

his tax voluntarily. With this in mind, many of us are placing the

taxes owed in special accounts and we will so inform the

IRS

in our letters.

Willful failure to pay is punishable by a fine of up to $10,000 and up to

a year in jail, together with the costs of prosecution. So far, the

IRS

has prosecuted only those who have obstructed collection (by refusing to

file a return, by refusing to answer a summons,

etc.).

Usually, the

IRS

has collected the tax due plus 6% interest and possibly an added fine of

5% for “negligence”. The fact that the

IRS

has rarely, if at all, prosecuted tax-refusers to the full

extent of the law does not mean they will not do so in the future.

Finally, an article from the edition of The Capitol East Gazette:

Two thousand anti-war leaflets on telephone tax refusal were distributed in Capitol East on , by members of CHOICE, a group of local residents who are withdrawing their support for the Vietnam war.

The leaflet explains that the 10% phone tax was enacted in specifically to raise money for the Vietnam war.

According to CHOICE, the phone company will not remove a person’s telephone if he refuses to pay the tax.

The company asks refusers to state why they are withholding the tax and then turns the matter over to the Internal Revenue Service.

According to CHOICE, there are presently 25 known tax refusers in the Capitol Hill area.

Those desiring CHOICE’s leaflet are asked to call LI 6‒9836.

War tax resistance in the Friends Journal in

Issues of the Friends Journal from give some additional hints of the reemergence of war tax resistance as a widespread practice in the Society of Friends… and also the first example of the backlash against it.

The lead editorial in the issue concerned “Taxes for War” and covered the war tax resistance of Quakers in England.

The article begins: “Friends in England are under the weight of the same concern that occupies American Friends: what can, or should, we do about taxation for military purposes?”

…short of outright refusal to pay taxes there seems no way out for those objecting to militarism.

The voluntary payments to U.N. funds, such as various Friends groups are making, will undoubtedly contribute to easing the moral burden, yet these sensitive donors would be the last ones to claim that their voluntary self-tax is a satisfactory solution to the problem.

The editorial then describes a quirk of British tax law by which if a taxpayer there “ ‘covenants’ a certain annual amount to a charity for seven years, the Internal Revenue will then, as The Friend (London) reports, pay over to the charitable organization ‘a sum equal to the tax normally payable on the amount of the covenant.’

The ‘charity,’ then, receives not only the contribution but also the tax paid upon it.

On the average a subscriber to a charity will have to pledge one half of his normal tax payment in order to recover that proportion usually allocated to armaments.”

While “far from flawless” and while “this plan exists only in England,” this plan “nevertheless affords some moral relief,” the editorial states.

This is the first in-depth discussion of a practical war tax resistance method in the pages of the Friends Journal, but it is only “practical” to most of its readers in the abstract — as something Friends in the old country might do.

As with the Journal’s earlier coverage of Quaker war tax resisters in Costa Rica, or of war tax resisters Milton Mayer, A.J. Muste, and Maurice McCracken, the magazine still seems most comfortable when talking about war tax resistance as something that other people do and American Quakers admire.

The article can be seen as a hunt for an excuse: “If only we had a law like the British do, we could resist our war taxes… maybe some day we will have one, perhaps we can even advocate for one, but until then there’s nothing we can do.”

Another example of the “there’s nothing we can do” point of view, in the same issue of the Journal, comes in a report on the Philadelphia Yearly Meeting, whose sessions were held :

Our sympathy was aroused for businessmen and taxpayers trapped in the war system and, recognizing our common sense of guilt, we acknowledged the fact that all enterprise is thus enmeshed.

The next paragraph begins “We were encouraged to break out of this trap…” but no mention of resisting war taxes follows.

The issue includes an article about the United Nations that includes this observation about those countries, like the U.S.S.R., that “have refused to contribute to U.N. projects of which they disapprove”:

There is a puzzling similarity between the attitude of these countries toward the U.N. budget and the attitude of those pacifists who refuse to pay income tax because they disapprove of some of the projects of the United States Government.

Note: “those pacifists” and not “those Friends” or “those Quakers.”

Again, there’s deniability about whether Quakers are the sort of people who do this sort of thing.

But here is a letter-to-the-editor, from Wilmer J. Young of Wallingford, Pennsylvania, that shows how war tax resistance was beginning to reawaken in the Society:

The following letter, signed by Clarence Pickett and Henry Cadbury, was sent to about twenty persons:

Dear Friend:

Many Friends have for years felt uneasy about paying that part of their income tax which goes into preparation for war.

A very few have refused to pay; but the majority of Friends have felt this to be an ineffective way to protest, or they have felt for various other reasons that this was not the way for them to bear witness for peace.

At the same time, many of them have been unhappy at not bearing a clear witness in this regard.

The signers of this letter invite thee to attend a meeting of a small group of Friends who feel concern in this matter.

We hope to discuss whether there is some action (perhaps not in violation of any law) which would be a clear indication of our position on war preparation, and might have some meaning both to the participants themselves, on one side, and to the general public, on the other.

Our consideration will of course be looking toward next year, as it is already too late for this.

Most of those invited to this meeting attended it.

There was an earnest and searching discussion for two hours.

However, no consensus appeared and no action was taken.

Some of us who are clear that we cannot pay this tax can but wonder whether it is weak intelligence or misguided conscience that has led us to our decision.

The issue included a report on “The Peace and Social Order Committee of the Young Friends Committee of North America,” which

…concerned that many Friends have lost the meaning of the peace testimony, organized a peace caravan this summer.

The seven Young Friends who joined in this Peace Caravan traveled in the Middle West asking Friends: “What does the Peace Testimony mean?

Is it relevant to our personal lives and our national policies?

If so, what is required of us?”

The article suggested some “Queries” that could be used to delve into questions like these, including this one: “Do we consider Christ’s teachings to love our enemies and do good to those who persecute us when we make decisions about our attitude toward military training and taxation for war?”

The same issue of the Journal contains the first example of backlash against war tax resistance I found in that magazine — a letter to the editor by Harold H. Perry in which he says that tax resisters are “by implication” showing a lack of support for all the good things the government does: not just the usual list of roads, schools, and the like, but even “many and considerable civilian services of the military establishments such as the work of the Corps of Engineers and much of the research that aids civilians, including medical and health benefits.”

He acknowledges that some resisters redirect their taxes to things of less-questionable benefit, but says that “[t]his may be laudable theoretically, but if widely practiced or permitted would lead to endless confusion, imbalance, and injustice.”

He concludes by encouraging Quakers to instead “work through established democratic machinery” to try to get their ideals reflected in government behavior.

A friend of mine, 43 year old Arthur Evans, a medical doctor with offices in Denver, Colorado, was sent to jail by Judge Alfred A. Arraj of the Denver district court, for his refusal to pay his part of the income tax (about 50 pct.) which would be used for the annihilation of the human race.

He sent it, instead, to the United Nations, to promote peace in the world.

In a statement circulated by him to his friends he says in part: “My lawyer, the judge, and other lawyers, tell me that there is no law, no constitutional provision that provides for the individual to refuse to pay taxes for annihilation.

So I go to jail, for I will not, I cannot in conscience be party to financing the means to annihilation.

The Jews under Hitler were taxed to buy their crematoriums. The same happens here — but it is not only the Jews who finance their means of destruction — it is almost every income earner in the United States.

This is called democratic because we are all taxed alike.”

Letters of approval have been pouring in to Dr. Evans, and since he is only allowed to write very few, his mother in Philadelphia has taken up the task of acknowledging them, sending at the same time a typewritten sheet explaining the affair in detail.

A little over a century ago, in , another man (who is now considered one of America’s greatest) was picked up in Concord, Mass. on the way to his shoemaker, and brought to jail because he had refused to pay his poll tax to a government he thought misguided and evil because it allowed slavery and was also at that time waging a war with Mexico to extend its slaveholding territory.

I mean, of course, Henry David Thoreau.

Out of that incident came his famous Civil Disobedience, which influenced Gandhi and Nehru; Thoreau’s ideas are very much alive in many parts of the globe today.

Strange, how history repeats itself!

Some day, perhaps after another century (if we escape a war of annihilation), Dr. Evans will be spoken of with appreciation and respect.

We have a way of crucifying the great while they are with us, and of exalting them after they are gone.

At present a medical doctor is doing laundry duty as a “trusty” in the Jefferson County Jail in Golden, Colorado, and he may like to hear from you.

How would the Friends Journal cover this?

Would it, as in the earlier case of Milton Mayer (see ♇ 5 July 2013), mention it but try to downplay its connection to Quaker practice?

Let’s see.

In the issue is a three-paragraph piece in the “Friends and Their Friends” section on the case:

Arthur Evans, Denver physician and member of the Society of Friends, went to jail on for three months because he has refused to pay part of his federal income taxes and because he would not produce his financial records.

For at least twenty years the doctor has paid to Internal Revenue Service only the proportion of his income tax which corresponds to the percentage of the national budget devoted to non-military purposes.

The part he has not paid to IRS he has devoted to charitable purposes and to agencies working for world peace.

Not until , when he declined to file an income tax return, has he been personally pursued by IRS, which heretofore had subtracted from his bank account amounts he was refusing to pay.

So the magazine is forthrightly recognizing this tax resister as one of its own flock, though its coverage is considerably more subdued than even the example from the mainstream media that I quoted above.

(Incidentally, if the Journal article is accurate and Evans was resisting as early as , this would put his resistance well in advance of that of the Peacemakers of , which I usually think of as the birth of modern American war tax resistance.)

The Evans case got another mention , in the issue, which reprinted excerpts from his letter to the Director of Internal Revenue (and which also explicitly identifies Evans as “a Friend”).

“We doctors have pledged to serve life,” Evans wrote:

I find no way to finance mass murder — be it called war, defense, or security — and be true to this pledge.

I care about life and the dignity of each individual, and desire to serve people everywhere, no matter who they are religiously, nationally, or racially.…

I cannot voluntarily fund that overwhelming part of my nation’s budget that finances acts based on retaliation, based on fear and hatred psychology, based on threats of injury and killing-in short, acts based on returning evil for evil.…

If this results in my going to jail for breaking laws that support injustice, slavery, death, and destruction, then in jail, with Martin Luther King, Henry David Thoreau, Peter, and Paul, I will attempt to serve wherein I can.…

“Thou shalt not kill” and “Thou shalt love thy neighbor [which includes thy enemy] as thyself” are precious laws of life to doctors and to all who would cooperate with the Christ.… Many men still believe… that they can deal with the evil acts of men by destroying the men who do these acts.

Yet I know no one who believes that conflicts… are resolved by mass murder.… The majority have not yet discovered that love is the only power that overcomes evil.…

I will continue to pay that percent of my tax liability that goes for nonmilitary acts of my government and enclose $200 toward same.

I am sending double the amount I am not paying for war to Quaker House at the United Nations for transmission to the United Nations Organization for its technical assistance program.

War tax resistance in the Friends Journal in

a Vietnamese postage stamp featuring Norman Morrison

On , a 31-year-old American Quaker named Norman Morrison went out to the sidewalk in front of U.S. Secretary of Defense Robert McNamara’s office in the Pentagon, doused himself in kerosene, and set himself on fire as a protest against the American war on Vietnam.

His suicide stunned the Society of Friends and made more urgent the already percolating questions about the moribund Quaker peace testimony and how much Friends were willing to put on the line for it.

This is reflected by the increased attention given in the pages of Friends Journal in to the issue of war tax resistance.

In , a “Friends’ Conference and Vigil on the War in Vietnam” asked the “Friends Coordinating Committee on Peace… to prepare a bulletin urging Friends to consider how paying taxes and buying war bonds involved them in financing the military.”

A number of Quakers signed a “No Taxes for Vietnam War” tax refusal vow that was organized by Maurice McCracken’s “No War in Vietnam Committee.”

These included, according to the issue of the Journal, “Franklin Zahn, Bob and Marj Swann, Arthur Evans, Bradford Lyttle, Johan W. Eliot, Staughton Lynd, Wilmer Young, George and Lillian Willoughby, and Marion C. Frenyear.”

The lead editorial in that issue was entitled “To Pay or to Protest?” and the author was determined to give no definitive advice on either side of that question.

The editorial begins by stating the case for Quaker taxpayer misgivings, then moves on to note that “a few pacifists” have been resisting, and to claim that “this year the number of tax-refusers will be far greater than ever before,” while other taxpayers who share their misgivings are either unwilling to take on the risks of tax resistance or believe that such an action amounts to “dodging the law and leaving someone else to carry a burden which they themselves will not assume.”

The editorialist then quotes from a letter written by a resisting employee “to her employing group” (why so coy about which group?) in which she writes that while she would be happy to “pay twice as much as required by the present law” for the more benign things the government buys, “I cannot bring myself to furnish money to be used in a way that will bring death to fine young American boys and men and also to Vietnamese men, women, and children.”

If “the employing group” were to cooperate in her request to stop withholding income tax from her salary, the editorialist wonders, “[w]ill it (or its members) be penalized?”

This is another strange example of the Journal taking an issue that was obviously a direct concern to Quakers and to Quaker Meetings, and trying to abstract it and cast it off into the distance somewhere in order to consider it dispassionately and indecisively.

From here the editorialist compares the Quaker war tax resister of today to the Quaker abolitionist “in the years before the Civil War when some members wanted to give all-out aid to the cause of abolition while others counseled caution, advocating strict adherence to the letter of such laws as those requiring fugitive slaves to be returned to their masters.”

Nowadays we tend to view with shame the historical evidence that all Friends did not work wholeheartedly for the abolition of slavery; will the time come when the Friends who follow after us have a similar feeling about those of their predecessors (including the present writer) who lacked the courage to resist conscription of their dollars to do the killing that they themselves refused to do?

After a quick detour through “There are those who say… there are others who counterargue…” territory, the editorialist recommends that people interested in tax refusal contact the Committee for Nonpayment of War Taxes or the Peacemakers, and gives their addresses.

Finally, there is a brief nod in the direction of war tax resistance being a time-honored Quaker practice.

The editorialist mentions that Franklin Zahn has authored a booklet on “Early Friends and War Taxes,” which includes the quote that ends the editorial, from the letter sent by John Woolman & co. to their fellow-Friends in :

Raising sums of money [for] purposes inconsistent with the peaceable testimony we profess… appears to us in its consequences to be destructive of our religious liberties; we apprehend many among us will be under the necessity of suffering, rather than consenting thereto by the payment of a tax for such purposes.

In the issue, an article about a Quaker movement in which people voluntarily taxed themselves 1% of their income for the support of the United Nations began this way: “All Friends, whether or not they would refuse to take up arms, are caught up in the military machine through payment of Federal income tax.”

This seems to indicate that there was still a blind spot that was making it difficult for some Quakers to even see the various alternatives to paying the federal income tax.

A report on the Philadelphia Yearly Meeting in the same issue noted:

After consideration, the Yearly Meeting concurred with the concern of the Friends Peace Committee that fresh attention be given to the effort to devise a formula acceptable to the Internal Revenue Service and to Congress, which would permit persons to withhold that proportion of their income taxes applicable to military purposes and apply it to constructive purposes of government.

Because a Monthly Meeting secretary and a youth worker for the Peace Committee have asked their employers to cease withholding income tax from their salaries, the problem is being thrust upon the Yearly Meeting.

Friends, whatever their judgments about a particular action, are sympathetic toward those who engage in it for reasons of conscience.

In furtherance of its concern… the Friends Peace Committee received authorization to seek personal conferences with officials of the Internal Revenue Service to acquaint them with the basis and reality of the concern to refuse payment of taxes for military purposes.

Perhaps such conversations may increase understanding on the part of the officials and may enable them, while carrying out their duty and enforcing the law, to understand and respect the refusers.

A conference at Pendle Hill “on the search for peace” in , concerned the “basic question… [of] whether the militaristic society in which we all live could be influenced through techniques of reason or whether religious pacifists, in their deep alienation, should rather seek a more radical strategy of protest.”

At one point, according to the coverage in the issue of the Journal, William Davidon “spoke frankly and clearly on the moral philosophy behind his refusal to pay those taxes which, he felt, would support the war in Vietnam.”

Martin A. Klaver contributed the lead editorial in the issue — “More on Tax-Refusal” — which is worth reproducing completely here as a good overview of the issue of war tax resistance as it stood at that time:

“Friends Journal,” writes John R. Ewbank, patent attorney and a member of Abington Meeting, Jenkintown, Pa., “might well mention the ‘mildest form of tax-refusal for Milquetoasts’: the refusal to pay the federal tax on telephone usage when billed for it.

The telephone company can carry the accumulated unpaid tax until it equals the deposit, and then assess a charge for nominal discontinuance and reconnection, so that the penalties for prolonged persistence are paid to the phone company instead of to the government.

How long it is worth while to carry the protest is a matter of individual judgment…”

For nearly a hundred years, John Ewbank adds, Americans have not been faced with a levy so conspicuously labeled “war tax” as this revived tax on telephone usage.

According to his letter to the telephone company, “The publicity connected with the telephone tax has been so specifically related to the Vietnam war, and I am conscientiously so opposed to the Vietnam war, that my payment herewith omits the $1.03 federal tax.

There are so few opportunities for protest — even feeble, futile protest — that [this] becomes one of the few available gestures.”

For Milquetoasts or not, feeble or not, the gesture is a form of civil disobedience differing more in degree than in kind from refusal to pay the federal income tax — or that part of it that goes for war.

It seems a little unfair to make it at the expense of the telephone company, which is thereby put to added trouble and expense, if only in its bookkeeping department, but it is a protest.

This year, it appears, the thin ranks of those refusing to pay income taxes for reasons of conscience were somewhat augmented.

An release from the office of A.J. Muste cites a statement signed by 360 persons, declaring that they would refuse to pay taxes voluntarily as long as United States forces continue to be used “in violation of the U.S. Constitution, international law, and the United Nations Charter.”

The release says that some signers are leaving the money they owe the government in banks, where the Internal Revenue Service can seize it, while others will contribute it to CARE, UNICEF, or similar agencies.

It also notes that, according to the Internal Revenue Code, “willful refusal to pay taxes may be punished by jail sentences of up to one year and fines as high as $10,000.”

This is not tax-refusal for Milquetoasts, although in the past fines and jail sentences have been rare indeed.

The law is enforced by placing a lien on the tax refuser’s property or attaching his salary.

There have been a number of instances where actions instituted against individuals were simply dropped.

But if tax-refusal should reach important proportions, the present seemingly casual attitude might change; the IRS might decide that it must do something to show that it is not virtually inviting more and more trouble.

Philadelphia Yearly Meeting was concerned this year with the problem posed by employes of two Quaker groups who have asked their employers not to withhold federal taxes from their salaries.

The Yearly Meeting’s Peace Committee is not only seeking a solution to this problem but is also seeking special conferences with Internal Revenue Service officials to acquaint them with the reasons why some Friends refuse to pay their taxes.

During the Yearly Meeting’s discussion it was brought out that Friends Committee on National Legislation for some time has been exploring the possibility of drafting legislation in this area making it possible for Americans who have conscientious objections to having their property used for war to pay equivalent taxes for other uses.

A number of congressmen have been receptive to the idea, but so far no formula has been found that promises to attract the necessary support.

Meanwhile most Quakers (like this one) pay their income taxes (including the reimposed telephone tax) without a murmur.

But there is a consensus on a fundamental: Friends’ basic belief that in matters of conscience each individual must choose his own course.

If that course brings him into conflict with government, he must decide for himself what he must do: obey in silence, obey and at the same time protest, or resort to civil disobedience of one kind or another.

Whether any government can grant any of its citizens the “right” to violate any of its laws is open to debate.

The citizen can hardly lay claim to such a right, yet when he feels that he has a duty to break the law, when he says, “God helping me, I can do no other,” then we must accord him our respect.

The issue noted that “two young Quaker workers… have voluntarily taken drastic cuts in salary rather than pay taxes for war in Vietnam.”

The two were John L.P. Maynard and Robert W. Eaton, who reduced their incomes to the maximum allowable before federal income tax withholding began — something on the order of $75 per month.

The Conservative branch of the Ohio Yearly Meeting met in .

According to William P. Taber, Jr.’s report on the meeting, “we asked our members to consider supporting tax refusal and the sending of aid to the civilians of all Vietnam.”

On the other hand, at the Westerly (Rhode Island) Monthly Meeting, the message was more mixed: “Many Friends feel that not to pay their taxes is disrespect for the law, breeding anarchy.

Yet they deplore the fact that their tax money is being used to prosecute a morally indefensible war in Vietnam.”

The best they could come up with was to approve a suggestion that Friends accompany their tax payments with a statement of protest.

The pseudonymous history columnist “Now and Then” took up the issue of war tax resistance in the issue:

A scruple against paying taxes which directly or indirectly support war has had a long if sporadic history among members of the Society of Friends.

It received official support in London in when decision was made that fine or punishment for such refusal could be reported by the meeting in the annual listing of “sufferings for Truth.”

At Philadelphia Yearly Meeting every year lately this concern has been voiced by individuals.

In the Meeting went so far as to authorize some minor action on the subject, including a delegation to visit the Internal Revenue authorities and to explain the tender conscience of the increasing number of Friends who refuse part or all of their Federal income tax.

The most intensive consideration of the matter among the Meeting’s membership appears to have occurred more than two centuries ago.

Before the Pennsylvania Assembly was asked by the mother country to supply men and funds for British military enterprises in the colonies.

The Quaker legislators, when they complied, did so uneasily, with the excuses that it was for defense or that the money was voted nominally for the sovereign’s use and that they were not responsible for what use the king (or queen) chose to make of it.

They also accepted as a permanent unqualified mandate the words of Jesus, “Render unto Caesar the things that are Caesar’s.” Sometimes Friends distinguished as acceptable mixed taxes and as unacceptable those taxes that were definitely labeled for war.

We are indebted to John Woolman’s Journal (Chapter Ⅴ) for an account of the exercise that arose in Philadelphia Yearly Meeting both in and in .

In the former year a committee was appointed which issued an epistle expressing the feeling that “the large sum granted by the late act of Assembly for the King’s use is principally intended for purposes inconsistent with our peaceable testimony,” and that “as we cannot be concerned in wars and fightings, so neither ought we to contribute thereto by paying the tax directed by the said act, though suffering be the consequence of our refusal.”

Woolman speaks of the conference on the subject “as the most weighty that ever I was at.”

There was not unanimity in the group.

Some who felt easy to pay the tax withdrew, but twenty-one substantial Friends subscribed the epistle; they included John Woolman, John Churchman (who also mentions the matter in his Journal), Anthony Benezet, John Pemberton, and Samuel Fothergill, an English public Friend visiting America.

In the Yearly Meeting of the matter was opened again, and a committee of about forty Friends were appointed to consider “whether or no it would be best at this time publicly to consider it in the Yearly Meeting.”

Visitors from other Yearly Meetings — including John Hunt and Christopher Wilson from England — were asked to join the committee.

The decision was negative.

There was difference of opinion on the subject, and “for that and several other reasons” the committee unanimously agreed that it was not proper to enter into public discussion of the matter.

Meanwhile it recommended that Friends of differing opinions “have their minds covered with fervent charity towards one another.”

One wonders why the different result from two years before and what were some of the “other reasons.”

Part of the answer, I think, is to be found in a letter to John Hunt and Christopher Wilson, sent to them by the Meeting for Sufferings in London.

This letter is dated and is signed by Benjamin Bourne, clerk.

I shall quote it as I have copied it from the manuscript minutes of the Meeting.

It falls in date between the two Philadelphia Yearly Meetings described above, at the second of which Hunt and Wilson were present and in a position to transmit the urgent advice of London Friends.

The main purpose of their mission to Pennsylvania, as is well known, was to prevent the home government’s proposed requirement of an oath for members of the Assembly by asking Friends to refuse to run for election.

The British Friends asked the government to let them attempt first to bring about the purging of the Assembly of Quakers.

In this they succeeded to the extent that most Friends withdrew from the Assembly; thus the threat was averted.

Evidently the same pressure was exercised to encourage Friends to pay provincial war taxes to the British crown and particularly not to publicize their scruple against paying them.

But neither the minutes of Philadelpha Yearly Meeting for (under ) nor its epistles — whether to London Yearly Meeting or to its own members — are so explicit as the letter.

After repeating the primary commission to the English delegates to try “to prevail on Friends in Pennsylvania to refuse being chosen into Assembly during the present commotions in America” and “to make them fully sensible of their danger, and how much it concerns them, the Province, and their posterity to act conformably to this request and the expectations of the government,” the letter continues:

And as you will know that very disadvantageous impressions have been made here by the advices given by some Friends against the payment of a tax lately laid by the provincial assembly, it is recommended in a particular manner that you endeavour to remove all occasions of misunderstanding on this account, and to explain and enforce our known principles and practice respecting the payment of taxes for the support of civil government agreeable to the several advices of the Yearly Meeting founded on the precept and example of our Saviour.

May that wisdom which is from above attend you in this weighty undertaking, and render your labours effectual for the purposes intended that you may be the happy instruments of averting the dangers that threaten the liberties and privileges of the people in general and restore and strengthen that union and harmony which ought to subsist in every part of our Christian Society.

Two brief lists were delivered with the above letter: extracts from London Yearly Meeting minutes of , , , , and , in which the payment of dues to the government is inculcated; and titles of Acts of Parliament, seven chapters in four Acts from the reigns of William and Mary and Queen Anne, “wherein it is expressed that the taxes are for carrying on a war.”

The final phrase was to leave no doubt that English Friends encouraged no escape on the ground that a Quaker conscience could assume the doubtful or peaceful purpose of the legislation.

The grounds on which the scruple among Friends was silenced in are clear.

Friends had long paid such taxes and wished to obey the laws.

If Pennsylvania Friends refused to vote for them as assemblymen or to collect them as tax collectors or to pay them as subjects, the liberties enjoyed in the colony, such as permitting affirmations in place of oaths, would be terminated.

The exhortations in the gospels and New Testament epistles in favor of paying Caesar his dues were applicable.

The early Quaker examples of civil disobedience in other matters were forgotten, and the relevance of the continuing Quaker testimonies against personal participation in war and against the payment of tithes was not cited.

In the latter area Friends were resolutely against payment and suffered ruinous distraints.

Evidently dues for the support of “hireling ministers” seemed more obnoxious than taxes for the prosecution of war.

If Colonial Friends disagreed with the practice of Friends in England or even with one another they would expose the Society to disharmony.

When Woolman’s Journal was reprinted in England in the whole section on paying or not paying taxes was omitted, but in America the problem already was taking a different form.

Friends and others had opposed taxation without representation when the Stamp Act was passed in .

With the outbreak of the Revolution the issue was one of using continental currency or of paying taxes to support war against Great Britain.

This, many American Friends (like Job Scott) and Meetings were willing openly to oppose.

The New York Yearly Meeting issued a statement “on the tragic situation in Vietnam,” saying that it represented “a supreme test” to “the spiritual vitality of the Religious Society of Friends.”

The statement, reprinted in the issue of the Journal included this point:

We call upon Friends to examine their conscience concerning whether they cannot more fully dissociate themselves from the war machine either by tax refusal or by changing their occupations.

The issue noted that “the newsletters of several Friends’ organizations” are encouraging their readers to “protest your telephone war tax” but also suggests that in some cases the protest was a pretty pathetic one: “Stickers saying ‘The Vietnam War Tax Included in This Bill Is Paid Only Under Protest’ are available from the American Friends Service Committee.”

The following issue included a letter-to-the-editor from Franklin Zahn in which he encouraged a more practical approach: “Each month I pay all of my phone bill but 7 percent, informing the company it is against my conscience to pay the direct war tax.

For five months the company added the unpaid balances to each new bill, then wrote it was referring the unpaid total to Internal Revenue Service and wiping my bill clean of debt… How will Internal Revenue handle this?

Past experience with unpaid income taxes indicates IRS may ask for payment but make no bank account seizure until the amount totals more than $5, at which time it takes an extra 6 percent (per annum) as fine.

Not paying direct war taxes is part of Quaker peace testimony.

Don’t pay for a wrong number.”

Franklin Zahn

We’ve encountered Franklin Zahn before.

He was listed as the contact person for “a leaflet on tax refusal” in a issue, and also something described as “the historical material” on the subject — “Early Friends and War Taxes” (perhaps the same leaflet).

Here is some more of his work:

In the issue, he responded in a letter-to-the-editor to an article that apparently suggested “that Friends drop their middle-class attitude of changing law and join the less privileged whose only method has been evading law.”

Zahn responded:

A basic test for conscience is the categorical imperative: What happens if everybody else did the same?

For [draft] evasion, I can see only the tightening up of conscription law.

For open resistance, however, the end of conscription.

For myself, personally beyond the applicable age, the corresponding form of resistance is refusal to pay war taxes.

If everyone in the world practiced it, the result would be close to total elimination of war.

I recently harbored an AWOL who jumped ship fifteen minutes before it sailed for Vietnam, but a better Quaker witness and confrontation would have been for both of us openly to declare our civil-military disobedience — he, his desertion; I, my aiding and abetting, and face the penalties for our actions.

But maybe I should rejoice in that having evaded the law I have lost some middle-classness.

In the issue, he suggested that the spirit of the gospels meant that the “Render Unto Caesar” episode should be interpreted anew:

In the matter of war taxes, were Jesus addressing Christian stewards of God’s wealth who were citizens in a free democracy and responsible for its conduct and were be to pick up an American coin with its inscription, “In God We Trust,” his words might very well be:

If the God you trust is Mars, pay your taxes to him.

In the issue, he gave “a historical summary” of how Quakers had dealt with the issue of war taxes:

With war taxes as with slavery, John Woolman stands out as the pioneer in getting the Society of Friends to face the issue.

His motivation in bringing the concern to Philadelphia Yearly Meeting in came from the increasing willingness of the Quaker government of the colony of Pennsylvania to vote money for war.

The Quaker Assembly had begun to weaken in its peace testimony in .

First it had refused to vote £4000 for an expedition into Canada, forthrightly saying, “It was contrary to their religious principles to hire men to kill one another.”

But later they voted £500 “for the Queen” as a token of their respect, with a rider saying, “The money should be put into a safe hand till they were satisfied from England it should not be employed for the use of war.”

But in a similar request resulted in £2000 being voted, with Isaac Norris echoing Fox in explaining: “We did not see it to be inconsistent with our principles to give the Queen money notwithstanding any use she might put it to, that not being our part but hers.”

That same year William Penn reputedly wrote the Queen (I have not found historical verification): “Our civil obedience is only due to Christ, not to confound the things of God with Caesar’s; for no man can be true to Him that’s false to his own conscience, nor can he extort from it a tribute to carry on any war, nor ought true Christians to pay it.”

[I also have been unable to find a source for this quote —♇]

Whatever influence the letter may have had, the fact seems to be that none of the £2000 voted “for the Queen’s use” was spent on the military expedition.

But the principle of passing the buck for war seems to have been established in the Assembly, which took the view that while Quakers refused to bear arms themselves they did not condemn it in others.

In the Assembly told the Governor it could not vote money for war, but acknowledged that on the other hand it had obligations to aid the government.

The crisis, however, came in the French and Indian War in , when individual taxpayers decided they could no longer pass the war buck to the Assembly.

In of that year John Churchman and other Friends met with Assembly Friends, and about twenty of them said, in part:

“…As the raising sums of money, and putting them into the hands of committees, who may apply them to purposes inconsistent with the peaceable testimony we profess, …appears to us in its consequences, to be destructive of our religious liberties; we apprehend many among us will be under the necessity of suffering, rather than consenting thereto, by the payment of a tax for such purposes; and thus the fundamental part of our constitution may be essentially affected, and that free enjoyment of conscience by degrees be violated;…”

The setting for this ultimatum is of interest: Quaker tax-payers, one-third of the population of the colony, Quaker Assemblymen a majority in a legislature which had non-Quakers like Benjamin Franklin — the most important person in the colony.

The Assembly, when the vote came, said it could not give money for munitions but that, as a “tribute to Caesar,” it was voting £4000 for “bread, beef, pork, flour, wheat, or other grain.”

The Governor who had received the request from New England for a grant to buy a different granular material, told the Assembly that their term “other grain” meant gunpowder and so spent the money.

Woolman’s thoughts about war taxes and his journeying to Philadelphia Yearly Meeting that year with his concern are familiar in his Journal.

One passage, however, seems pertinent to as Friends urge a divided Congress to cut off war funds:

“Some of our members who are officers in civil government are… called upon in their respective stations to assist in things relative to the wars… if they see their brethren united in payment of a tax to carry on the said wars, may think their case not much different, and so might quench the tender movings of the Holy Spirit in their minds.”

On , he; Churchman and others drew up an Epistle to Pennsylvania Friends:

“…The large sum granted… is principally intended for purposes inconsistent with our peaceable testimony; we therefore think that as we cannot be concerned in wars and fightings, so neither ought we to contribute thereto, by paying the tax directed by said act, though suffering be the consequence of our refusal.… Though some part of the money to be raised… is said to be for such benevolent purposes as supporting our friendship with our Indian Neighbors and relieving the distresses of our fellow-subjects, who have suffered in the present calamities, …we could most cheerfully contribute to those purposes, if they were not so mixed, that we cannot… show our hearty concurrence therewith without at the same time assenting to… practices which we apprehend contrary to the testimony which the Lord hath given us to bear…”

The “tax” committee of Yearly Meeting decided that refusal should be an individual matter, and in we find Friends like Joshua Evans conscious there was no solid front: “I found it best for me to refuse paying demands on my estate which went to pay the expenses of war, and although my part might appear at best as a drop in the ocean, yet the ocean, I considered, was made of many drops.”

The effect of such witness was not to stop the war but, as Woolman may have felt of even greater importance, to help Quaker legislators to be true to their own “tender movings.”

In that year the last of the Quaker Assemblymen had resigned and no more ran for the office — in Franklin’s approving words, “choosing rather to quit their power than their principle.”

The 70-year experiment of a Quaker government came to an end over the question of war taxes.

By , according to James Pemberton, it was clear the war-makers were extracting their toll: “The tax in this country [is] pretty well collected and many in this city particularly suffered by distraint of their goods and some being near cast into jail.”

Two decades later, when the bigger test of the Revolutionary War came and the “fighting” Free Quakers separated, tax refusal was so well established that some Quakers appear almost to have over-reacted.

In The Quakers in the American Colonies, Rufus Jones writes:

“There was plenty for the overseers to do in these early days of the war.… Shutting their hearts against the pleadings of mercy for their brothers and sons who had joined the ‘associators’ or paid war taxes, or placed guns for defence upon their vessels, or paid fines for refusing to collect military taxes, or in any way aided the war on either side, they cleared the Society of all open complicity with it.

The offense was reported to one Monthly Meeting, and at the next the testimony of disownment would go out.”

While by today’s permissive standards of the Society such peace witness seems more hysterical than historical, we need to be aware that in this period as in the Civil War, “tax” sometimes meant the substitutionary amount paid in lieu of military service by COs.

In New England the question of paying war taxes to the rebelling colonial governments was the precipitating cause for the split-off of Free Quakers.

There, as elsewhere, when the Revolutionary War broke out, Friends generally agreed they should not pay specific war taxes but on “mixed” taxes — the subject of the 1755 Epistle in Pennsylvania — there was no consensus.

Job Scott in New England Yearly Meeting was the most erudite and detailed advocate of not paying mixed taxes.

In his essay, subtitled “A truly conscientious scruple with respect to the payment of such taxes as are in part demanded for and applied to the support of war and fighting,” and addressed to “Friendly reader,” he reasoned in 1780:

“Now then, if a collector of taxes comes to me and in Caesar’s name demands a tax of £20 which I am persuaded is so far mixed, part for war and part for other charges, that my conscience forbids my paying it… I am not to blame for not paying it: if Caesar pleaseth to separate them I can gladly pay the one part and refuse the other.… though magistry be a divine ordinance, yet it does not follow that every requisition of the civil magistrate ought to be actively obeyed, anymore than because it is a duty indispensable and incumbent on all mankind to pay all their just debts, that therefore we must pay all demands however unjust.”

Tradition-minded Friends who used the Caesar argument sometimes pointed to George Fox who in , paying a specific war tax for the Dutch war, made a distinction between this and direct military service.

But the homeland of Quakerdom by had also moved towards tax refusal; in London Yearly Meeting minuted its censure on “the active compliance of some members with the rate (tax) for raising men for the Navy” and directed local Friends to have such cases under their care.

Those who paid war taxes without even waiting for the process of distraint were considered to have acted “inconsistently.”

In less material on taxes was published by Friends.

Perhaps there is here a fruitful field awaiting some researcher of yearly and quarterly minutes [indeed there is –♇].

Was there less interest in the problems, or was refusal taken for granted?

Did non-Friend Thoreau’s ringing call to refusal in the Mexican-American War preempt the field?

Whatever the reasons, as Friends face today’s violence with its automated battlefields and nuclear missiles — where the conscription of human bodies for mass armies may become less important — and conscription of money for sophisticated technology more important — the relevancy of the tax question to a modern, effective peace testimony has reached an all-time high.

In its issue, the Journal noted that the IRS had made a half-hearted attempt to seize Zahn’s “1955 Dodge station wagon” for $6.58 in resisted phone tax.

Although contemplating lying in front of the car as a final protest before the towing, Franklin calmly removed his personal effects from the car and showed no agitation at this seizure of his property.

At the last minute, however, the IRS men suddenly removed the chains, saying, “We just got new orders — we’re calling off the dogs.”

The mood changed from one of tense formality to joviality as the men left.

“It was as though,” Franklin says, “they were glad the little bluff had failed.”

A letter-to-the-editor from Zahn appears in the issue, in which he responds to “a frequent objection to war tax refusal: that it logically leads to a host of other tax refusal.”

He suggests that because military expenses are such an overwhelming part of the federal budget, only war resisters are likely to find tax resistance to be a tempting tactic.

And anyway, “if a few other than war objectors choose to refuse, I see no objection to their doing so.”

In the issue, Zahn writes in to make a fresh case for war tax refusal:

In refusing personal service, one considers one’s integrity — conscience: Can I be part of a machine geared to agony and death?

But often a different criterion is applied to refusal to pay: How effective a protest is it?

If the protest-value of tax refusal is the only consideration, Friends may feel the effort is better spent in writing a legislator or phoning the White House.

(But I have found that a letter to the government saying I am refusing to pay war taxes is one letter officials never ignore.)

Arguments against the effectiveness of war tax refusal can be self-fulfilling prophecies.

Friends may not wish to join a public witness which is so small it attracts little notice — therefore it remains small.

Yet it is possible that an announcement of intention to pay no further war taxes would be the most single effective act against the arms race that members of the Society of Friends could take.

But sudden, dramatic decisions for effectiveness are not in the manner of Friends.