How you can resist funding the government →

about the IRS and U.S. tax law/policy →

IRS incompetence →

enforcement effort/results →

failure to collect even when it knows about tax debt or wins tax convictions

From another link on the Tax Policy Center’s web site, I read that according to the IRS, 79% of filers who use “known abusive devices” to avoid paying taxes (the bogus theories I’ve been writing about in recent Picket Line entries) and 75% of those who don’t bother to file returns never have to pay up even though the IRS has caught them!

This is from testimony by Leonard E. Burman before the House Ways and Means Committee a few months ago.

Burman was complaining that with billions and billions of dollars going uncollected, the IRS had decided it was going to concentrate the bulk of its new enforcement efforts on catching Earned Income Tax Credit cheats — in other words, the working poor.

Today’s grab-bag:

Conversations with the IRS — what happened when a war tax resister who hadn’t filed in years finally got called on the carpet by an IRS agent.

A follow-up on Health Savings Accounts answers two questions about the new tax-sheltered savings plans:

1) Are you obligated to withdraw from the accounts to pay your health expenses, or can you keep the sheltered money there as an additional IRA-like investment?

2) What happens to your Health Savings Account when you die?

The Treasury Inspector General for Tax Administration has issued a scathing report on the failures of IRS enforcement efforts:

[O]f 172 tax convictions studied, more than $2.5 million in back taxes, interest and penalties went unpaid by people who ignored the terms of their sentences.

For example, the IRS’s criminal investigations division closed 37 cases with probationary periods ending .

Of those 37, only six complied with their sentences, which included payment of back taxes, penalties and interest, the report said.

In 11 cases, the convicted tax evaders were not at fault, since the IRS failed to inform them of the terms of their penalties.

In 12 cases of known noncompliance, the IRS’s criminal investigators did not bother to notify the criminals’ probation officers or the criminal courts.

“To say that it looks like the IRS is dropping the ball in these cases would be an understatement,” Sen. Max Baucus of Montana, the ranking Democrat on the Senate Finance Committee, said in a statement.

“We’ve caught the criminal, prosecuted the crime and handed out the sentence.

Seeing that the sentence is enforced should be the easiest part of the whole process.”

“The old saying is, ‘If you can’t do the time, don’t do the crime.’

Now it seems you don’t have to do the time or even pay a dime,” Sen. Charles E. Grassley (R-Iowa), the committee’s chairman, said in a statement.

Here’s a great idea for a revenue booster:

Let’s say you’re a government that’s wrongfully convicted somebody and therefore imprisoned an innocent person for years.

Why should you have to pay for that person’s food and lodging all those years when that prisoner had no legal right to such good treatment?

(I’m reminded of the government of China charging condemned victims’ families for the bullets used to execute them):

Agency initiates steps for selective draft — “The government is taking the first steps toward a targeted military draft of Americans with special skills in computers and foreign languages”

A new GAO financial audit of the IRS includes some interesting numbers about their success in collecting from people who don’t pay what the IRS says they owe.

“The unpaid assessment balance includes amounts owed by taxpayers who file returns without sufficient payment as well as amounts assessed through the IRS enforcement programs.” More than half of this (57%) “consists of interest and penalties and is largely uncollectible.”

Of the total unpaid balance, 23% are taxes and penalties that the IRS has independently assessed without the taxpayer or a court agreeing to the assessment (for instance if someone doesn’t file a tax return and so the IRS generates its own estimate of what the person owes).

“Due to the lack of agreement, they have less potential for future collection…”

Another 40% is considered a “write-off” — because the taxpayer is dead, bankrupt, out-of-business, vanished-into-thin-air, or something of the sort.

The remaining 37% is further divided into a “collectible” portion (23% of the 37%, only 8.5% of the total) and an “uncollectible” portion (77% of the 37%)—

…due primarily to the taxpayer’s economic situation, including individual taxpayers who are unemployed, are currently in bankruptcy or have other financial problems. Except for bankruptcy situations, the IRS may continue collection actions for 10 years after the assessment.

Thus, these accounts may still ultimately have some collection potential if the taxpayer’s economic condition improves.

The IRS, when trying to collect unpaid taxes from people, intends to leave them enough to live on.

To this end, they have a set of standards for how much income and possessions they won’t steal from you.

This is based on your gross monthly income — meaning that if you’re already more fortunate income-wise, they’ll let you hold on to more (presumably because you’ve become accustomed to a higher-income lifestyle and it would be more of a hardship for you to lose more than it would be for someone not so fortunate).

It’s also partially based on your family size and the cost-of-living where you live.

If you are only bringing in enough money to make ends meet, by these standards, the IRS will not try to levy your income.

But you might be surprised at just how much that is:

[O]f the $247 billion in unpaid taxes owed as of , $23 billion, or almost 10 percent, is owed by tax debtors IRS has designated as being in financial hardship; therefore, IRS does not attempt to collect their outstanding tax debt.

IRS allows tax debtors earning up to $84,000 — almost twice the median income for all households in the United States — to be designated as being in financial hardship.

In total, IRS has placed tax debtors collectively owing over $6 billion in tax debt in its top financial hardship income threshold of between $76,000 and $84,000. Because they have been designated by IRS as being in financial hardship, although they are earning relatively high incomes, these tax debtors are excluded from the FPLP and do not face other tax collection action from IRS.

, IRS almost tripled the maximum amount it allows tax debtors to earn before being subject to collection action, far above the rate of inflation.

IRS could not provide us any data analysis that supported those increases.

As a result of those large increases, almost two-thirds of all tax debt IRS has designated as being in financial hardship is owed by tax debtors IRS allows to earn more than the national median household income before their unpaid tax debt again becomes subject to IRS collection action.

In contrast, in , no tax debtor with a financial hardship designation was allowed to earn more than the median household income without becoming subject to collection action.

Furthermore:

The effect of IRS’s collection policy regarding financial hardship tax debtors who accumulate new debt is essentially to both cease collection of old debt and not require tax debtors to pay the current taxes they owe.

Allowing such tax debtors to continually not pay current taxes without consequence appears to be giving tax debtors with financial hardship designations an additional exemption from paying current taxes as well as old tax debt and may contribute to the noncompliance of other taxpayers.

Because:

[E]ach tax debtor who is allowed to avoid filing required tax returns or paying current taxes, or who is perceived to live well while facing little tax collection consequence, represents not only less money for vital federal programs but one more advertisement for others to do the same.

The National Taxpayer Advocate’s office released its annual report to Congress .

There’s a wealth of interesting information in there (well, interesting if you’ve got some tax geek in you).

Some things that caught my eye:

“With regard to IRS’s stepped-up enforcement activity over the past few years, we are beginning to see signs that taxpayer rights are not being protected as well as they have been in recent years, particularly in the collection process.

Perhaps this is almost inevitable when enforcement is ramped up quickly and pressure is applied to program managers to show results, but we believe it is important to highlight our concerns and for the IRS to take our concerns seriously to avoid the risk that the enforcement over-zealousness which plagued the agency in will recur.”

“In , the IRS reported more delinquent tax dollars as ‘currently not collectible’ than it actually collected on active balance due accounts (TDAs), installment agreement accounts, and offers in compromise (OIC) combined.”

“IRS studies and external experts in collection confirm that collection cases 24 months past due generally yield less than 15 cents on the dollar and after three years are practically uncollectible.”

“Some aspects of the [private debt collection] plans reflect dramatic departures from IRS practice and impact taxpayer rights.

We would like to discuss some of the specifics in this report, but the IRS has advised us that much of the information in the PCA operational plans and calling scripts is designated as ‘proprietary information,’ and generally cannot be released without the consent of the PCAs.

The operational plans and calling scripts describe such things as belated Fair Debt Collection Practices Act (FDCPA) warnings and psychological techniques used to coax debtors into paying.”

(The report recommends that the private debt collection initiative be entirely scrapped.)

The IRS has been using an automated process of attaching 15% levies to federal payments to people with tax delinquencies.

Most typically, this is used to seize a portion of Social Security payments.

The IRS has used this power against people well below the poverty line, although for other sorts of levies and seizures it does take financial hardship into account.

How’s that IRS private debt collection agency program going?

Let’s ask the National Taxpayer Advocate:

It is not meeting revenue projections.

It is not more successful than the IRS at finding hard-to-locate taxpayers.

It is significantly less successful than IRS employees at fully resolving taxpayer past due accounts.

And:

The I.R.S. had expected private companies to collect $88 million but has now lowered that to as little as $23 million.

The collectors are paid almost a fourth of the money they bring in.

When the costs of government oversight are added in, [National Taxpayer Advocate Nina E. Olson] said, the program may even lose money.

Indeed:

Significantly, and contrary to projections made as recently as in , the expenses of the program to date exceed the revenue the program has generated.

“The cash economy is growing.

The percentage of all income subject to third party information reporting fell from 91.3 percent in to 81.6 percent in .

Moreover, the IRS expects the number of individual returns from small business or self-employed taxpayers to grow by about 33 percent , while the number of individual returns from other taxpayers is expected to decline by about 2 percent over the same period.”

, the IRS assessed $10 million in penalties against professional tax preparers for various forms of preparer misconduct.

But the agency only managed to collect $2 million of this $10 million.

It seems that tax preparers know the difference between a dog bark and a dog bite.

For tax year , the IRS identified more than 1.2 million cases in which someone failed to file a tax return even though they had taxable income.

In cases like these, the IRS creates a substitute tax return for the person, which (usually) results in a “default assessment.”

But, “the IRS collected just under two percent of the taxes assessed through the automated process, a sign that this method is not increasing filing and payment compliance.”

The IRS responds: “We… do not agree with the suggestion that dollars collected is the best measure of the effectiveness of these assessments.

Each assessment abated or adjusted reflects the submission of a return or other response by the taxpayer after the ASFR default assessment has been made — a clear indication <voice="darth vader">the taxpayer has been successfully brought into compliance</voice>.”

“A disregarded entity is a single member Limited Liability Company (LLC) that has not elected to be classified as a corporation.

It is called a disregarded entity because the owner reports business activity as if the entity did not exist.

For example, if the single member is an individual taxpayer, (LLC transactions are reported on the owner’s Form 1040 as if it is a sole proprietorship.

The compliance detection issue results from the owner of a disregarded entity using the tax identification number of an entity that does not have a filing requirement.

The IRS document matching program cannot match the disregarded entity income with the true owner and the income may go unreported.)”

“The earnings of an S corporation are taxed as ordinary income to its shareholders.

Unlike partnership or sole proprietor earnings, however, S corporation earnings are not subject to self-employment tax.

This difference in treatment gave rise to a tax planning strategy that treats shareholder compensation payments as distributions of profit to avoid payroll taxes.

Under this approach, officer/shareholders take no salary or a nominal salary and receive the remaining compensation as tax-free distributions.

The corporation saves payroll taxes and the shareholder ultimately pays only income taxes on his or her share of the corporate profits and avoids paying Social Security and Medicare taxes.”

However… “the IRS has repeatedly challenged and won the shareholder wage issue in court, [but] it is still used as a tax planning strategy.”

The IRS reported 18% more “Taxpayer Delinquent Accounts” in than in .

81% of these accounts involved tax years before , and many are “inactive.”

The Taxpayer Advocate purports to believe the following:

The United States tax system is based on a social contract between the government and its taxpayers — taxpayers agree to report and pay the taxes they owe and the government agrees to provide the service and oversight necessary to ensure that taxpayers can and will do so.

Without that unspoken agreement, tax administration in a modern democratic society could not function.

Thus, the government’s ability to raise revenue through voluntary tax compliance — the most efficient and economical form of tax compliance — rests on taxpayers’ belief that the government will honor its end of the social contract.

This “unspoken agreement,” says the Taxpayer Advocate, is overdue to be spoken — in the form of “a formal Taxpayer Bill of Rights” (which, since “a tax system that embeds rights also expects its taxpayers to conduct themselves in such a manner as to ensure those rights are not abused,” will also be “a statement of taxpayer obligations.”)

Naturally, this articulation of the unspoken agreement is not going to take the form of an actual negotiation or agreement.

It’s to be a top-down declaration emitted by Congress or the IRS for our benefit.

Apparently, it’s pretty simple and low-risk to file fraudulent tax returns claiming that you qualify for thousands of dollars in refunds.

The IRS will cut you a check, then maaaaaybe somewhere down the road they’ll notice something fishy, then maaaaaaybe they’ll catch you, then maaaaaaaaybe they’ll try to get the money back.

No fooling.

Here’s a story about one of the ones they caught up with.

He took in half a million dollars over three years this way — and all he had to do was just to pull the numbers out of his butt.

Nothing fancy.

It was only accidentally, “after federal agents learned that Fisher had cheated a local car dealer out of $1.2 million and used that money to buy gold bars and silver coins,” that the tax fraud was uncovered incidentally to that investigation.

A recent TIGTA audit found out that this sort of fraud is a billion-dollar problem for the IRS.

The agency issued an estimated $1 billion in potentially fraudulent refunds, four times what it originally estimated, and then didn’t bother to further investigate half a million of the returns with discrepancies.

Their Criminal Investigation division tracked down about $189 million of that billion, but left $894 million on the table.

They simulated a bureaucratic organization and randomly assigned participants to be in a high-power role (prime-minister) or low-power role (civil servant).

The prime-minister could control and direct the civil servants.

Next, the researchers presented all participants with a seemingly unrelated moral dilemma from among the following: failure to declare all wages on a tax form, violation of traffic rules, and possession of a stolen bike.

In each case, participants used a 9-point scale (1: completely unacceptable, 9: fully acceptable) to rate the acceptability of the act.

However, half of the participants rated how acceptable it would be if they themselves engaged in the act, while the other half rated how acceptable it would be others engaged in it.

The researchers found that compared to participants without power, powerful participants were stricter in judging others’ moral transgressions but more lenient in judging their own:

“power increases hypocrisy, meaning that the powerful show a greater discrepancy between what they practice and what they preach.”

This effect is stronger when the powerful people believe they have come by their power legitimately or deservedly.

Peter J. Reilly continues his series touching on war tax resistance at his Forbes.com blog.

In this episode, he takes a second look at the court case in which William Ruhaak tried to assert a legal right to conscientious objection to military taxation, saying that Ruhaak’s argument isn’t so frivolous after all.

In another post, Reilly looks at the “paper tiger” of IRS tax enforcement, and shows how most taxpayers, if they keep their tax debt under $10,000, can get away with letting the statute of limitations expire and never have to pay it.

Cindy Sheehan has done a further write-up on her tax resistance: “I vowed that I would never, ever pay a penny to this government in the form of income taxes again, because: A) My oldest son was priceless to me and I feel this nation owes me and B) other people’s sons and daughters all over the world are precious to me and I refuse to fund their murder, torture, displacement, etc.… I will defer paying my taxes as long as slaughter abroad is the foreign policy of this government, economic terrorism is the paradigm here at home and the Bush mob continues to roam the world as unrepentant criminals.”

The report says that in , the IRS gave up on 482,611 outstanding tax debts (representing about $6.7 billion dollars) as uncollectible because the taxpayer could not be found or could not be contacted.

The Inspector General analyzed a sample of these cases and found that in more than half of them, “there was no evidence that [IRS] employees completed all of the required research steps” before giving up.

The report gives some insight into what sorts of investigative tools the IRS uses (or is supposed to use) to track down hard-to-find taxpayers.

These are (using terminology as used in the report):

telephone directories

IRS’s Information Returns Processing data [basically, the agency’s record of the past nine years of tax returns]

send a postal tracer

motor vehicle records

employment commissions

courthouse records for real and personal property

local licensing when the taxpayer owns a business

online resources (Accurint) [which “includes motor vehicle records, courthouse records, and licensing information”]

Integrated Data Retrieval System tax return research, if the due date of the last filed return was within the past two years

Currency and Banking Retrieval System research when Integrated Data Retrieval System research reflects that a taxpayer has filed a Foreign Bank Account Reporting form, and possible use of a Tax Attache for International accounts

“Local management may require that additional information sources be checked, for example U.S. Coast Guard and local licensing agencies where boat ownership is common.”

“A field call to the taxpayer’s last known address”

“…check utility companies, to see who is paying the bills at the taxpayer’s address and how the bills are paid, for a possible levy source”

“secure and analyze a full credit report”

“Request a passport check when the taxpayer travels outside the United States frequently or there is reason to believe the taxpayer travels outside the United States frequently… [and] Consider requesting that a taxpayer be placed on the Department of Homeland Security lookout list if you have been unable to locate or contact the taxpayer and if they live outside the U.S. or travel outside the U.S.”

Both of these sources, alas, redact the dollar amounts that mark thresholds at which the IRS either turns up the heat or throws in the towel.

Some war tax resistance news that has scrolled by on my screen in recent days:

Erica Weiland, at the War Tax Talk blog, has

uncovered a case of successful war tax resistance from the archives of

NWTRCC’s

newsletter. The anonymous resister in question filed income tax returns,

refused to pay the amount “owed,” and then began to watch those unpaid

amounts disappear behind the statute-of-limitations curtain and beyond the

reach of the

IRS.

The resister made some attempts to make collection more difficult — not

owning big-ticket property, setting up a “gift annuity” and outright giving

money away to make current assets less-collectible, moving accounts from

bank to bank — but in part it seems to be

IRS

negligence or laziness that gets the credit. Good enough for government

work!

Canada’s Globe and Mail published

an obituary for Eldon Comfort,

a World War Ⅱ vet who became an anti-war activist. It quotes from a letter

he sent to the minister of revenue in :

Today, modern technology has introduced weapons of mass destruction. Their

cost is staggering. … So, in a very real sense when I pay my income tax, I

am complicit in the deployment of such armaments.

I am, therefore, claiming conscientious objection to the conscription of

my tax for military purposes. The percentage of the federal budget

designated for

DND

is deemed to be 8.1 per cent, so I have reduced my income tax by that

amount. This portion is being directed to

Conscience Canada’s peace

tax fund.

When the Canadian military operations were restricted to peacekeeping (in

its restricted sense), to search and rescue, and to succour during

national natural disasters, I had no quarrel with paying my taxes in full.

When the priority for the resolution of conflict, once again, becomes a

peaceful and diplomatic enterprise, I shall resume full payment.

Greg Slepak recognizes that by paying his taxes he becomes complicit in

what the government does with his tax money, but he has chosen a different

approach to that of conscientious war tax resisters. Instead of no longer

paying for the government’s misdeeds, he has identified one of the victims

of these misdeeds and

attempted to compensate him in proportion to how much he’d victimized him.

“To such a person, I have a sense of… indebtedness, as though I

owe him something. After thinking on it, I realized there might be some

truth to that.”

I recently became aware that a biography of Maurice McCrackin has been put on-line, including a chapter that covers his introduction war tax resistance and the early days of the Peacemakers group.

His tax resistance began, according to the book, when Wally Nelson noticed the pacifist minister removing toy guns and other war toys from those in a donation pile, and told him: “Do you ever think that next March 15 [then the income tax filing deadline] you’ll be paying for real guns?”

The next chapter covers his imprisonment for refusing to cooperate with an IRS summons.

Another chapter concerns his removal as a minister by officials of his Presbytery who were upset about his war tax resistance.

Matt Hisrich at the Quaker Libertarians blog takes issue with Quaker organizations who frame their opposition to government military spending in terms of reallocating that spending to other government priorities.

Excerpts:

This approach puts forth the false notion that national governments sit

atop vast reserves of wealth that should be spent on nonviolent rather

than violent ends.…

National governments cannot spend new wealth without either issuing new

debt (that will have to be repaid) or extracting it directly from

taxpayers through the implicit or explicit threat of violence. If Quakers

(or anyone else for that matter) want to be known as “Champions of Peace,”

it would be better to strive toward a reduction in the war spending that

seeks to keep funds in the hands of individuals to peacefully pursue their

own ends instead of merely shifting line items in national budgets. The

former focuses on individual and local empowerment, and the latter focuses

on somehow “winning” in the national political game.

A common argument against tax resistance goes something like this: The government will add penalties and interest and such to the amount you refuse to pay, and when they eventually wring the money out of you, in the end you’ll have given even more financial support to the government than you would have if you’d just paid up in the first place.

Today I’ll show you some evidence that I hope will convince you that this is not a very good argument.

Lots of people don’t pay the IRS what the agency thinks they should.

The IRS has tried to figure out where this missing money is hiding, but their methodology isn’t all that great, and it’s not an easy mystery to solve.

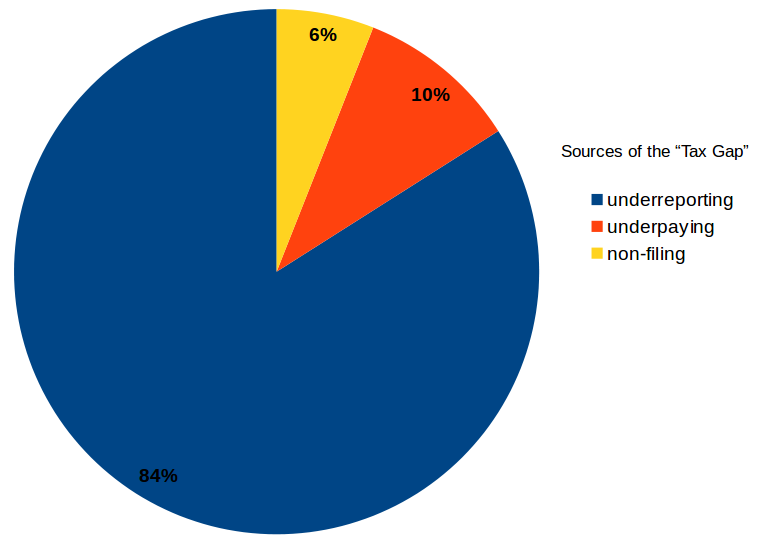

Their best guess is that the vast majority of missing taxes comes from “underreporting” — that is, taxable activities that the IRS never becomes aware of.

For example: if you placed a bet with a friend on the outcome of the Super Bowl, the winner of that bet should have added the amount won to their income and should have paid taxes on it, according to the IRS anyway.

Most people don’t go out of their way to report taxable transactions like these that the IRS wouldn’t learn about on its own, and so a lot of these transactions never get taxed and they stay in the “underground economy.”

An estimated 84% of the “tax gap” comes from unreported taxable activities like these.

Another 6% comes from taxable activities the IRS does learn about, but for which the responsible party never bothers to file a tax return.

The remaining 10% comes from people whose tax debt is registered on paper according to Hoyle, but who never get around to forking over the money.

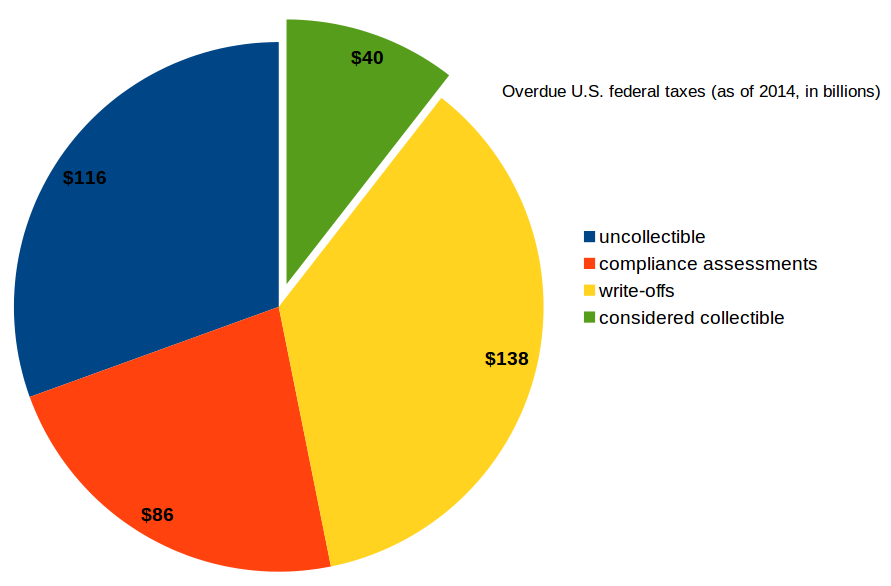

According to IRS financial statements for , there were at that time about $380 billion in outstanding unpaid taxes that it knew about.

This includes about $205 billion in interest & penalties added to the originally-due taxes, but it does not count any taxes that people have thus far successfully evaded by keeping out of the IRS’s view — that is, all the stuff in the 84% blue area above.

It also doesn’t include amounts that the agency can no longer pursue because the statute of limitations has expired.

Of that $380 billion, the agency considers $116 billion to be “currently uncollectible” (“primarily because of the economic situations of the taxpayers”).

Another $86 billion is something called “compliance assessments” — which I think means the IRS tells a taxpayer who hasn’t filed a return (or a fully-revealing one) what the agency suspects the taxpayer would have owed if they had filed accurately, but the taxpayer isn’t going along with it and the controversy is still in limbo.

The agency doesn’t have much confidence in collecting this money either.

There is also a category called “write-offs” that totals $138 billion.

This is tax debt that is hopelessly uncollectible because the taxpayer is bankrupt, insolvent, dead, vanished into thin air, or something of that sort.

That only leaves about ten percent of the total that the IRS considers to be collectible and includes as a potential asset on its financial statements.

So to $175 billion in unpaid taxes, the IRS has added $205 billion in interest & penalties, but it only expects to collect $40 billion of the total (in recent years it has actually collected closer to $46–49 billion per year by means of its enforcement arm, so it may somewhat exceed its expectations).

This I think shows conclusively that people who don’t pay their taxes do not, in the aggregate, ironically end up paying more to the government.

of the $380 billion owed to the IRS in back taxes, the agency only hopes to collect the $40 billion green slice of the pie

For tax resisters — who are typically alive, solvent, and often have seizable assets and income streams — the news isn’t quite as good as this chart would suggest.

But even from juicy targets like us, the IRS fails to seize enough money in penalties and interest from some of us to make up for the money it fails to seize from those of us it lets slip through its clutches.

An informal survey of war tax resisters a few years back, for example, found that the IRS had successfully seized only about 25% of what those resisters had refused to pay.

In addition, it is costly for the agency to deploy its collection apparatus: sending out all of those letters, filing liens & levies, managing the associated bureaucracy — all of that costs money.

The IRS spends about $5 billion dollars on enforcement (including investigations, audits, and collection), and so resisters contribute to this additional cost of the government conscripting our support.

So if you are hesitating to refuse to pay taxes because you worry that by doing so you may inadvertently swell government coffers… I hope this has reassured you that in the aggregate, tax resisters do indeed cost the government money.

Some bits and pieces from here and there:

war tax resistance

Jesse Maceo Vega-Frey recalls his time with Juanita & Wally Nelson, and his own ambivalent experiences with war tax resistance, in an article for the Boston Review.

I stumbled on this quote, shared recently by “tandy_jack” on Instagram, from the back of a Joan Baez album:

We paid the taxes that bought the war that hired the men and dropped the fire that burned the huts and killed the people who then were the bodies that Scott counted.

It’s a rotten thing to brainwash someone into doing the dirty part of the killing while we stay at home.

It’s a rotten thing to pretend the war is coming to an end when it’s only taken to the air.

And in if you don’t fight against a rotten thing you become part of it.

What I’m asking you to do is take some risks.

Stop paying war taxes, refuse the armed forces, organize against the air war, support the strikes and boycotts of farmers, workers, and poor people, analyze the flag salute, give up the nation state, share your money, refuse to hate, be willing to work… in short, sisters and brothers, arm up with love and come from the shadows.

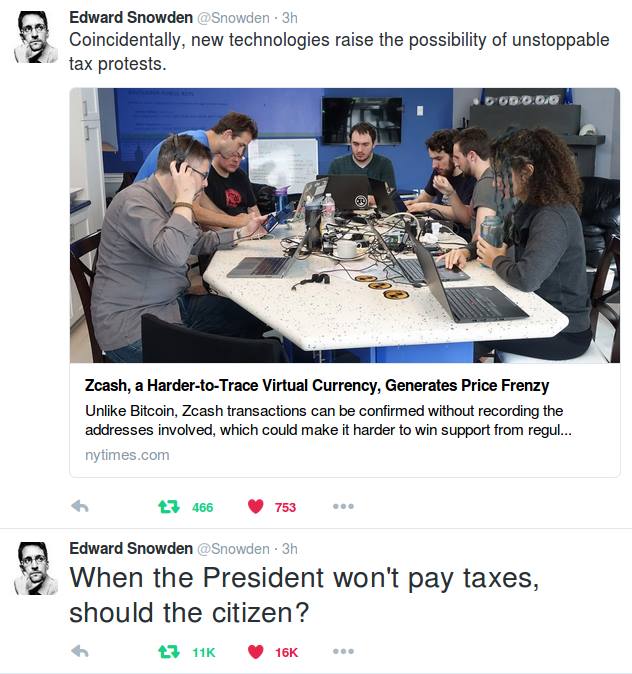

virtual cash

exiled American dissident Edward Snowden made waves recently by promoting tax resistance to the incoming Trump regime

National governments are trying to discourage cash, so as to eliminate the sorts of anonymous, untraceable transactions that are difficult to tax.

For example, the government of India recently made a surprise announcement that 500 and 1,000 rupee notes would no longer be legal tender after a certain deadline.

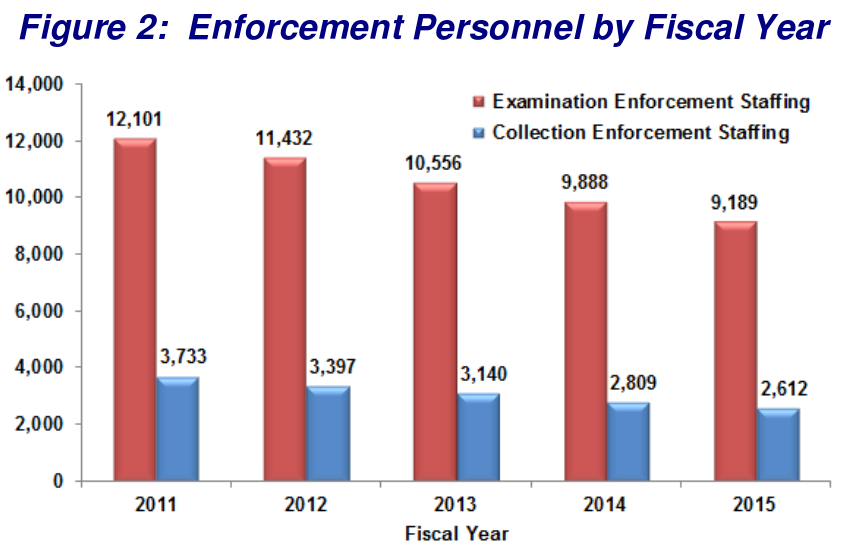

If the IRS does decide to crack down on virtual currencies, it may have to do so with virtual employees, as its real enforcement staff numbers have been dropping year after year:

This article, concerning another TIGTA report, gives a good indication of how strapped the agency is.

Even when shown that there’s money on the table that just needs to be picked up (in this case, high-income people who haven’t filed income tax returns but whom the agency knows about), the IRS complains it doesn’t have enough people to do the picking.

Some recent links of note:

The IRS has announced that not only will it issue stimulus payments and Paycheck Protection Program loans to people and businesses even if those people or businesses are behind on their taxes, but also that the agency will not levy bank accounts into which those payments are deposited — for 24 weeks in the case of PPP loans, or 8 weeks in the case of stimulus payments.

Current IRS policy says that agents should contact taxpayers before issuing a levy to ask whether the account in question recently received such a payment.

If so, they are supposed to refrain from levying until the proper number of weeks have passed.

If the IRS tries to levy a bank account in which you have recently deposited such a check, you can protest this and the IRS is supposed to release the levy.

In either case, this should give you plenty of time to empty out the account so that a future levy attempt will fail.

I fear that waiting out the ten year statute of limitations on collections is becoming a reasonable strategy and that many “taxpayers” have caught on and that the IRS, when it comes to collection, is to a significant degree bluffing.

My overall takeaway from the [recent Treasury Inspector General for Tax Administration] report is that the IRS has a lot of outstanding receivables that it does nothing about.

That made me want to look more closely at the numbers.

Working with the spreadsheets is a little frustrating.

They don’t answer all the questions I would like answered, but it does give a pretty clear idea that the IRS is something of a shadow of its former self.

At , the balance of assessed tax, penalties and interest (ATPI) was $114.2 billion spread among 10.4 million accounts.

In that year IRS filed 1,096,376 notices of federal tax lien and requested 3,606,818 levies on third party.

IRS wrote off $14.6 billion that had expired due to the ten year statute.

At ATPI was $125.8 billion spread among 11.2 million accounts.

There were 543,604 liens and 782,735 levies.

$34.2 billion expired due to the ten year statute.

It is important to remember that when we are talking about collections, we are talking about tax that has already been assessed.

This has nothing to do with people who have not filed or who underreported income and have not gotten caught.

That is an entirely different kettle of fish.

Through my decades of tax practice, the notion of flat out not paying assessed tax was not something that was in my bag of tricks.

It has slowly dawned on me that this is a thing.

A tax strike by restaurants and bars in Italy has begun.

The strike is being organized by Movimento Imprese Ospitalità, which is a project of the tourist industry branch of the General Confederation of Italian Industry.

It is protesting continued tax collection at a time of collapsing business during the Covid pandemic.

I’ve seen a few more articles that give some additional details about the latest tax strike in South Kivu:

The campaigns have been organized and led by what are vaguely referred to as “la société civile” (civil society).

This refers to some sort of preexisting groups, but I don’t really understand what they are.

They seem to be non-governmental organizations that sometimes behave as parallel governments or service providers, other times as sorts of citizens’ unions or chambers of commerce.

Guillermo Incer Medina, in Confidencial, evaluates the tactics used by the protesters in Nicaragua who have been struggling with the Ortega regime.

He concludes that the best high-impact, low-risk action would be tax resistance from a small number of large-scale taxpayers.

Excerpt:

In Nicaragua, 94% of the total tax collection comes from large taxpayers (a large taxpayer is a company that has large volumes of transactions and, therefore, that collects taxes such as VAT, IR — and others– in large amounts.

Examples of these could be supermarket chains, large importers, large commercial establishments, or large agro-industrial consortia).

In our country, the sectors with the largest taxpayers are industry, commerce, finance, transportation, and services.

In these sectors, large taxpayers collect more than 90% of the total taxes of their respective sector (which is to say that of every 100 córdobas that is collected from taxes in each sector, 90 córdobas are contributed by large taxpayers and only 10 córdobas by mid-sized and small ones).

Furthermore, in areas such as liquors, beers, soft drinks, and fuel, the large taxpayers collect 100% of the total taxes.

Why is this important?

Because the dictatorship needs taxes to maintain its repressive apparatus and its patronage politics.

If you take the oxygen out of their horror machine and purchase of consciences, you take away their room for maneuver.

“Let’s do a consumer strike!” said COSEP and AMCHAM representatives every time we demanded a national strike.

This is a mistake for two reasons: 1) for a consumer strike to have a real and not symbolic effect, requires that millions of unorganized Nicaraguans, including pro-government people, decide to deprive themselves of consuming goods that are difficult for them to obtain due to the precarious living conditions in which we live, 2) it is useless for us to stop consuming (not paying VAT) if companies still pay the State taxes such as IR and others (one must keep in mind that those who directly “deliver” taxes to the State are not we the consumers, but they are the collectors — the companies).

What can one do then?

The action that could have the greatest impact at the lowest cost and in the shortest term is tax resistance from the large taxpayers, which is nothing more than the large companies stopping payment of taxes to the dictatorship for a period long enough to oblige them to make concessions for his departure.

“They are going to close us down!”, the big businesses say immediately.

But it is not likely that the government will close large companies due to how this would look to foreign investment, and due to the political cost of sending thousands of people into the streets.

Furthermore, if they close large companies, this would in practice have the same effect as tax resistance, since they would stop receiving their taxes.

“We are exposing thousands to unemployment!”, they also say… more jobs are being jeopardized by letting this political and humanitarian crisis drag on and by the coming interruption of CAFTA and ADA, if the dictatorship continues to do what it wants and stays five more years.

“It’s too risky!”

It is more risky to put your body on the line in a march or a roadblock, or to go on a hunger strike in a church and get shot, cut off your services, and imprison those who want to help you.

There is no large, medium, or small company that is worth more than a human life.

Tax resistance is more feasible than other actions of high-risk and low-impact (such as a chain of express pickets or coordinated sit-ins) because it does not require the coordination of thousands of unorganized people.

To promote tax resistance, it is enough that a few of the largest companies, which are already organized in chambers, agree, stand firm, and coordinate among themselves.

Gig workers in Serbia used to be more or less income-tax free, apparently.

Not any more. A new law not only makes them liable for income tax, but requires them to cough up taxes for the last five years.

Marchers in Belgrade protested the new tax law.

The Mennonite Church USA is holding a Cost ☮f War webinar .

Mennonite war tax resisters will be among the presenters.

The war tax resistance movement in Spain does a periodic census of war tax resisters there, asking them how much they resisted and, if they redirected the taxes, where they redirected.

I don’t know how representative census-responders are of the war tax resistance movement there.

I have a feeling that if we tried the same thing in the United States, we’d get a pretty small percentage of resisters responding.

We’re not very good survey people.

But anyway, according to their census the 258 people who responded to the Spanish survey redirected €18,088 to 92 different projects.

The average resister redirected €70.

Follow the link for more details.

Peter J. Reilly, at his Forbes tax blog, writes about the “hey hey just don’t pay” tax strategy.

He writes about war tax resisters who see their tax debts erased by the statute of limitations and notes:

I find this situation demoralizing.

I believe that making an effort to be reasonably tax compliant (Perfection is impossible unless your situation is pretty simple) is one of the duties of good citizenship.

I also used to believe that it was prudent even for people who are of the “taxation is theft” school of thought.

I am doubtful of the latter now.

It is still too risky for my taste, but I can’t make the argument that scofflaws are being reckless.