Tax resistance in the “Peace Churches” →

Brethren →

Louise & Phil Rieman

Much of the anti-war movement has lately turned away from marching and pleading with legislators and such and has decided to try to make the U.S. less eager to make war by exacerbating its “human resources” shortage.

I think this new focus shows promise.

It has a concrete, measurable goal that can be reached incrementally, results can potentially be seen both on a large scale and on a very human scale, and it is an actual, non-symbolic impediment to militarism, making it more difficult and more expensive.

There is a danger, though, that by focusing on encouraging desertion and conscientious objection within the military, and on discouraging recruiting, the anti-war movement will fall in to the easy habit of regarding its struggle as something that mostly involves other people — members of the military and potential recruits — changing their behavior.

One way to address this is to remind people that conscientious objection is for everyone.

A good example of this is provided by the Church of the Brethren Christian Citizenship Seminar, which was held in New York and Washington, D.C.:

Former conscientious objectors (COs) Enten Pfaltzgraff Eller and Clarence Quay shared the stories of their struggles, as did more more recent COs Andrew Engdahl and Anita Cole.

Eller and Quay each chose not to register and instead did alternative service, although Eller’s service came after a lengthy court case.

Engdahl and Cole arrived at their decisions after entering the military, and they asked for reclassification.

“When Jesus said ‘Love your enemies and pray for those who persecute you,’ that has to be now, not later,” Eller said.

“You have to struggle with where God is calling you and how you’re going to follow.”…

Several speakers addressed a different form of conscientious objection, war tax resistance.

Phil and Louise Rieman of Indianapolis and Alice and Ron Martin-Adkins of Washington, D.C., explained why they had decided not to pay the portion of their taxes that support military operations — and the consequences that can come with that choice.

Marian Franz of the National Peace Tax Fund provided additional background on this form of witness.

“If we say that war is wrong, and we believe war is wrong, then why would we pay for it?” Louise Rieman said.

“It was more than I expected,” said Chrissy Sollenberger, a youth participant from Annville, Pa.

“I didn’t think there was so much about conscientious objection to talk about.

I just thought it was saying no to being drafted, but it’s so much more than that.…

It feels like we have more power now to make those choices.”

So lately I’ve been being very urban homesteader — baking bread, brewing beer and sake, making yogurt, weeding the garden, canning soups.

I’ve been looking for a paying gig, too, which I think partially explains my sudden explosion of home usefulness: it gives me something productive to do while I wait for résumés and bids to be ignored.

What I haven’t been doing much is writing anything substantial for The Picket Line.

Sorry ’bout that.

Meanwhile all sorts of interesting things have backed up in my bookmarks, waiting for me to add some insight or context before passing them on for you to enjoy.

I think instead I’ll just let them spill out here and trust you to fill in the blanks:

Francois Tremblay wonders if taxpayers become complicit in what their tax dollars support. He weighs the arguments for both sides (no, because their participation is legally required; and yes, because their participation is nonetheless voluntary) and then engages in some spirited give-and-take with his readers.

War tax resisters Phil and Louise Baldwin Rieman died in a car accident shortly after .

There have been several remembrances of the couple on-line, such as this one from the Church of the Brethren.

Murray Rothbard writes about ending tyranny without violence (through withdrawal of consent) and the nearly 500-year-old insights of Étienne de La Boétie.

The Taxpayer Advocate said in its annual report that American taxpayers pay — above and beyond what they actually are charged in taxes — nearly two hundred billion dollars just trying to do the paperwork involved in taxpaying.

Our local paper did the math and put a number on a conclusion that should have been pretty obvious: it’s much cheaper to take public transit than to drive.

According to their figures, it costs Bay Area drivers about $1,000 per month to get where they’re going by car instead of by bus and rail.

Hell, we pay that much for rent.

A writer for Rebelión notes that Europe’s public is sick of spending so much on the military and asks, “is tax resistance not therefore justified, an investment in the struggle for what is worth the trouble of defending instead of the military costs that impede this to a great extent?” (en español)

Finally, U.S. nuclear weapons spending topped $52 billion (and that’s only counting what we’re allowed to know about).

Compare that to the budget of your favorite government agency, business, or non-profit.

Here’s a piece from the New York Times that mostly concerns the efforts of the promoters of “Peace Tax Fund” legislation in the United States but also touches on American war tax resisters:

War Resisters: ‘We Won’t Go’ to ‘We Won’t Pay’

You could hardly find a more problematic time for pacifists who do not want their taxes spent on the military.

But the recent wave of patriotic fervor has only reinvigorated the efforts of one tiny, determined group.

“On , I was told I should lay low for a while,” said Marian Franz, executive director of the National Campaign for a Peace Tax Fund.

“Now I have been told this is the time.

As the war grows, so does the antiwar movement.”

For more than three decades, the National Campaign for a Peace Tax Fund has petitioned the federal government for a way to earmark the tax revenues that would go to the military — usually around 50 percent — for nonmilitary purposes, like education or health care.

Like conscientious objectors who in the past were offered an alternative to military service, these resisters say the First Amendment protects their ethical or religious objections to paying for war with their taxes.

Like other groups that have struggled to reconcile the obligations of citizenship with antiwar beliefs, the campaign has had a marked increase in inquiries from the public over the last year.

At the Center on Conscience and War, a Washington-based national nonprofit group that works for the rights of conscientious objectors, phone calls quadrupled right after and are now about 4,000 a month, double the usual number, said J. E. McNeil, the center’s executive director.

Mary Loehr, the coordinator of the National War Tax Resistance Coordinating Committee, an organization based in Ithaca, N.Y., that links 50 groups opposing war or weapons, has also seen a surge in interest.

“Starting , we have had a call a day from people asking for information, and our busy season is usually January through April,” she said.

“I would get 70-year-old women from the Midwest saying: ‘I don’t want to pay for this. Will it hurt my Social Security?’ ”

The debate over whether it is justifiable to withhold tax money from the military was waged on religious, philosophical and legal grounds even before supporters managed to have a bill on the matter introduced in Congress.

Derrick Bell, a visiting professor at the New York University Law School and an expert on constitutional issues, says the law doesn’t allow people to pick and choose where their tax money goes, as if they were at a buffet.

“When particular groups try to exempt themselves from having their tax money support a particular government activity, there is no legal precedent for that,” he said.

Professor Bell said the prevailing standard was that the “free exercise” of religion clause in the First Amendment was violated only if a law was shown to be irrational or unreasonable, or that someone suffered some special harm from it.

He noted, too, that even the right to be a conscientious objector to military service was established by statute and theoretically could be overturned by Congress.

“There is nothing written in stone,” Professor Bell said.

“Even the ‘free exercise’ clause has been variously interpreted.”

Opponents of the tax initiative commonly cite the fear that exempting some taxpayers for their religious beliefs would open a floodgate of claims from others objecting to federal support for everything from the arts to AIDS research.

Last year, for instance, a bill was introduced in the Illinois Legislature that would allow taxpayers who are against the death penalty to have the portion of their taxes that finances executions go to schools.

The bill, which never had any significant support, was killed.

But advocates counter that pacifism, often grounded in religious belief, is in a category by itself.

“Whenever you come up with a new issue, you hear ‘slippery slope,’ ‘Pandora’s box,’ ” said Ms. McNeil of the Center on Conscience and War, who is also a lawyer.

“There is no floodgate.

A minuscule amount of taxpayer money goes to pay for abortion or the death penalty, and other issues are political, not religious.”

In the United States, there has been a long religious and ethical tradition of opposition to war.

During the 19th century, Henry David Thoreau refused to pay taxes because he opposed slavery and the military.

The Mennonites, the Quakers and the members of the Church of the Brethren, who belong to what are known as historic peace churches because of their pacifist tradition, all refused to take part in the American Revolution.

They laid the foundation for the creation in of the Selective Service Alternative Service Program for conscientious objectors, which started with World War Ⅱ.

Until then, there was no legal recognition for conscientious objection.

During World War Ⅰ, 17 soldiers who were conscientious objectors even received death sentences in a military court, although none were carried out.

In the United States Supreme Court ruled that the criteria for conscientious objection could be broadened to include men who were not members of any religious denomination and in to include those who did not profess belief in a Supreme Being but had ethical or moral convictions against war.

Ms. Loehr, 44, who has been a war tax resister for 22 years, estimates that about 5,000 people around the country currently withhold taxes because of their objections to war and military spending.

Some tax resisters purposely keep their earnings too low to be taxed, she said, while some are self-employed and refuse to pay estimated tax; and some claim an abundance of tax exemptions so their employers cannot take the money from their paychecks.

The Rev. Michael J. Baxter, national secretary for the Catholic Peace Fellowship in South Bend, Ind., and a professor of theology at Notre Dame University, predicts resistance will rise.

“I think as the U.S. gets ready to go to war in Iraq, there will be more tax resisters,” he said.

“Sometimes during war, the place that good Christians belong is in jail.”

His group has already begun advising conscientious objectors in case the draft is revived, he said.

In June, to put a human face on their ideals, the National Campaign for a Peace Tax Fund put together a 15-page booklet featuring the smiling images and often sad tales of tax resisters across the country.

Some of the resisters profiled donate the taxes that they estimate would go to the military to other causes.

Others have been imprisoned or lost their assets because of tax evasion.

They say they have reached their convictions about the immorality of war through their religious beliefs or the influence of thinkers like the Rev. Dr. Martin Luther King Jr.

As pacifists and pastors in the Church of the Brethren, Phil and Louise Baldwin Rieman argue that contributing funds to war is the same as killing.

For 30 years they have given about 60 percent of their taxes to civil rights and peace programs, despite Internal Revenue Service threats of liens against their bank accounts, wage-garnishment letters sent to churches where they worked and government seizure of their family van.

“We will look back on war someday like we did on slavery,” said Mr. Rieman, who lives in Indianapolis.

A conscientious objector during the Vietnam War, he completed two years of alternative service.

“It feels lonely sometimes, but mostly it feels frustrating,” said Mrs. Rieman, 56, describing the couple’s long odyssey.

“We can’t buy a house, we can’t buy a car.

We don’t enjoy the feeling of religious freedom they say we enjoy in this country.”

Stanley M. Hauerwas, a professor of theological ethics at Duke Divinity School, said many religious traditions had a history of resistance to laws they considered immoral, those statutes supporting slavery being prime examples.

Even the way that the standards for conscientious objection have changed, from requiring membership in a pacifist church to simply allowing the adherence to certain ethics, shows a government grappling with what constitutes religion, Professor Hauerwas said.

Is it ethics, beliefs, membership?

The Peace Tax Fund bill would amend the Internal Revenue Code, setting up a nonmilitary fund to which pacifists could contribute the tax money that would otherwise go to the military.

Introduced in by Representative Ron Dellums, Democrat of California, it has been reintroduced every year since and had 35 supporters in the House of Representatives during Congress’s last session.

“ changed the equation once again,” said Representative Eliot L. Engel, Democrat of New York, a two-time co-sponsor of the bill who no longer supports it.

“A case could be made that if every American decided they didn’t like certain policies and decided to withhold taxes, it would be a problem.

It wreaks havoc with government.”

But Representative John Lewis, Democrat of Georgia, the bill’s current sponsor and a veteran of the civil rights movement, said should not make a difference in supporting the rights of conscientious objectors.

Other groups may have their own objections to the way federal taxes are spent, he said, but his philosophy was “you try to take the ones that have the largest meaning to the largest number of individuals.”

“We will put on a whole new effort when we come back to Congress,” said Mr. Lewis, an ordained Baptist minister.

“Look at the military budget.

We have enough bombs, we have enough missiles, we have enough guns.”

Some bits and pieces from here and there:

The creative activists of the Free Keene movement are at it again.

This time they’ve formed a group called “Robin Hood of Keene” that shadows parking enforcement officers on their rounds and quickly fills expired meters before they can reach them to write out tickets.

Members of the group place cards under windshield wipers that read,

“Your meter expired; however, we saved you from the king’s tariffs, Robin Hood and his Merry Men.

Please consider paying it forward,” and includes an address where donations can be sent.

Alleging that the Robin Hooders have “repeatedly and intentionally taunted, interfered with, harassed, and intimidated” the meter officers, the city has filed for a restraining order (the activists insist that this has nothing to do with any intimidation or harassment on their part, but with the city’s loss of revenue from the thousands of parking tickets they have prevented).

In the filing, parking enforcement officer Linda Desruisseaux said,

“Besides following me, crowding around me, making video recordings of my activities, and placing coins in expired meters to prevent me from writing tickets, these individuals repeatedly taunt and harass me, asking why I am stealing peoples’ money and telling me to get another job…

In particular, Graham Colson likes to taunt me by saying,

‘Linda, guess what you’re not going to do today — write tickets.’…

The taunting and harassment tends to get worse when there is a group, as they try to one-up each other at my expense.”

The IRS scandal that all the frogs are croaking about is largely a steaming pile of political bullshit… but the winds are blowing the smell directly into the offices of the IRS, which which is making it an unpleasant place to do business:

A former Internal Revenue Service official who ran the unit now at the center of scandal says the agency is about to be hit by a wave of resignations that he fears will hobble its operations.

“I think there’s going to be a significant number of departures from the agency,” said Marcus Owens, a Washington attorney who served as director of the exempt-organizations’ office .

The same post is now occupied by Lois Lerner, who has come under fire for her agency’s treatment of conservative groups.

“That’s going to have an impact on tax collections and tax administration,” said Mr. Owens, who said he thinks the controversy has been overblown.

Mr. Owens, who worked for the IRS for 25 years, said a number of IRS officials have talked to him about their plans to leave.

He said the investigations underway have crushed morale, while some IRS officials are starting to get threatening anonymous calls at home.

In the other IRS scandal, the one that to me seems more actually scandalous, the agency has backed down from its repulsive legal opinion that Americans have no legitimate privacy expectations in their email communications, so agency investigators should feel free to rifle through them without bothering to get a warrant.

The new policy says the agency won’t aim to read your email at all if it is only pursuing a civil action against you, and will “in all cases” obtain a warrant when trying to get your email from whichever Internet service provider is storing it, when pursuing criminal cases.

Fran Quigley at Counterpunch takes another look at the Transform Now Plowshares case, and in particular how the government progressively ratcheted up a misdemeanor trespassing charge against the three pacifists until now they stand convicted of federal terrorism felonies, awaiting sentencing from jail as they’ve been deemed violent criminals too dangerous to release.

The fabled Greek crackdown on tax evasion seems mostly for show: “of the estimated 13 billion euros that government officials say is owed by Greece’s 1,500 biggest tax debtors, only about 19 million euros [≈0.1%] has been collected in .”

In readers of the Messenger learned the legal how-tos of war tax resistance, while even the conservative Brethren Evangelist was willing to publish “New Call to Peacekeeping”’s summons to war tax resistance.

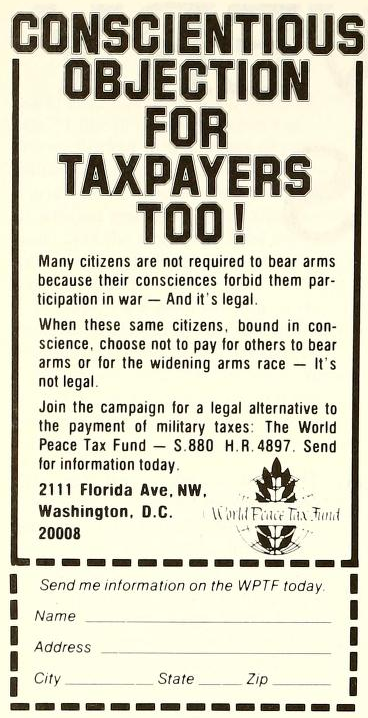

an ad promoting the World Peace Tax Fund, from the edition of the Messenger

As had become common at this point, discussion of the World Peace Tax Fund bill often overshadowed war tax resistance when war taxes were discussed.

The bill was boosted in

(source),

(source), and

(source).

Here’s another example mention, from an profile of Charles Anderson (source):

Charles admits some pangs of conscience over his life-style.

His own affluence is difficult for him to reconcile with peacemaking, since he believes that the gap between the prosperous and the poor breeds violence.

His payment of tax, more than half of which is used for military purposes, is also stressful.

Support of the World Peace Tax Fund is an effort to resolve this personal conflict.

In the magazine reported that the Mennonites seemed to out in front of the Brethren on the war tax issue (source):

Church as tax collector protested by Mennonites

Delegates attending a special meeting of the General Conference Mennonite Church in Minneapolis in voted to launch a vigorous campaign to exempt the church from acting as a tax collector for the state.

The 500 delegates at the conference, called to discern the Christian response to militarism, passed the resolution by a nine to one margin.

A central focus of discussion was tax resistance already being practiced among Mennonites and the request of one such person, a General Conference employee, that the church stop withholding war taxes from her wages.

The General Board denied her request because it is illegal for an employer not to act as a tax collector for the Internal Revenue Service.

Delegates affirmed that decision but instructed the General Board to vigorously search for legal avenues to exempt the church from collecting taxes so individuals employed by the church would be free to follow their own conscience.

The issue profiled Ralph Dull, and noted that “throughout the past 25 years… the Dulls have withheld from their taxes the portion allotted to the military.” (source)

“Sometimes you get so frustrated, you just have to do something,” Ralph said.

For the past two years Ralph and others have taken food to the IRS as a witness that taxes should be used for feeding the hungry instead of supporting the military.

“I’m not sure it does any good, but it raises the issue.”

Phil Rieman wrote in to the issue, urging Brethren to stick together in order to overcome the fear of government reprisals when considering war tax resistance (source).

The issue reprinted a lengthy article by William Durland, a lawyer who founded the Center on Law and Pacifism (and later helped found NWTRCC), on the practical and legal aspects of war tax resistance:

When President Carter’s military tax budget for was criticized, he replied that he would not apologize for it.

While recommending cutbacks in health, education and human needs, he increased the portion of the budget allocated to bombs and bullets.

Many Christians are beginning to realize that they cannot use mammon for murder and expect a welcome at the millennium.

So they are looking for advice on ways to refuse complicity with the war machine.

Recently the Center on Law and Pacifism was organized in Philadelphia to serve people who need advice and support in the relationship of their radical religious, pacifist convictions to the laws which attempt to obstruct their conscientious objection to violence.

One of the main projects of the Center has been to aid people in their quest for information on how to be military tax refusers.

The Center is in the process of publishing such a study and the following is an overview of that report.

People want to know how to withhold their taxes, what happens if they do so and what legal remedies exist for them to witness to their conscientious objection in the courts of this land.

Usually people who are in this position are employees.

So we will talk about them first, then the employer, the corporation, the income tax refuser and the telephone tax refuser.

Employees receive their income in the form of wages which are subject to withholding before they see their check.

Employees must fill out a W4 form with their employer.

The W4 form determines the amount of money to be withheld from each paycheck.

The more allowances you claim the less money is withheld.

You are allowed a number of allowances on your W4 form depending upon how many dependents you have and what your anticipated itemized deductions are.

The employer determines how much money to withhold from your weekly paycheck on the basis of your W4 form.

Therefore, in order to reduce or eliminate withholding, you can file a new W4 form claiming more allowances.

There is nothing fraudulent about this procedure as long as you inform the IRS when you file your income tax return as to why you took the allowances on your W4 form.

When it comes time for your income tax, it is important that it be consistent with this claim.

This is done by taking a war tax deduction on your income tax form under “miscellaneous deductions.”

This is one of four methods to avoid withholding.

The second method is by working in an occupation exempt from the withholding law.

A third method is by becoming self-employed as a consultant or independent contractor.

Fourth, by earning less than a taxable income you can avoid not only withholding, but also any income tax liability whatsoever.

If you are successful in computing the sufficient number of allowances — which will constitute rendering your withholding to a point where you can take your deduction on your income tax — then no further problem remains until that time for the employee.

However, should the employee choose not to use the allowance method, but rather to ask the employer not to withhold any of the withholding tax, then there is a problem for both employer and employee.

The Internal Revenue Code of , as amended, requires employers making payment of wages to deduct and withhold from such wages a tax determined in accordance with IRS tables.

The employer is liable for the amount required to be deducted and withheld.

Any employer who fails is liable to the IRS for that amount plus a civil penalty equal to the tax amount.

There is also a criminal penalty of $10,000 fine and/or five years imprisonment for willful failure to pay or collect the amount due.

Some employers have wanted to protect the right of their employees to exercise their rights of conscience even though the employer does not share the same viewpoint.

In this event, employers have refused to withhold and have been taken to court.

Eventually they wind up paying and requiring the employee to reimburse them.

But what if the whole corporation becomes a war tax refuser, rather than just one of its employees?

In that event the corporation will not withhold any tax at all because they are conscientiously opposed to paying military taxes.

Recently we have seen some organizations which were created on radical religious, pacifist principles beginning to refuse to pay military taxes as a corporation rather than simply to support the conscience of one or more of their employees.

They see this as their own witness to the immorality of war taxes.

There is a possibility of losing tax-exempt status and other rights, but they are willing to witness in this way and suffer for conscience’s sake.

Everyone who makes a minimum amount of money a year is required by law to file an income tax return.

Whether you made your money as an employee, an employer or are self-employed, you must file form 1040 and complete Schedule A (“Itemized Deductions”) in order to take an income tax deduction for war.

Those who are self-employed can write in a “war tax credit” instead of a deduction, and simply withhold a percentage of the tax owed and send a letter to the IRS explaining what they are doing.

Another popular way of resisting military taxes has been refusal to pay the tax on the telephone bill.

In times past, the IRS took quite a bit of time tracing down telephone tax refusers.

Since the end of the Vietnam War, this has not been the case, although we have heard of one case recently where the telephone company closed down the service of a telephone tax refuser.

Whatever category you are in, you must decide how much to refuse and what you are going to do with that money.

Many organizations, such as the World Peace Tax Fund and the various chapters of War Resisters League, are equipped to advise you on the breakdown of the national budget.

But generally, from year to year, the military portion of the budget is calculated anywhere from 35 percent to 53 percent, depending upon whether current military expenditures for past wars are included.

For those who wish to put their money to good use while it is being withheld, there are various alternative funds which invest in human resources and use your money for that purpose.

Many people hope that the World Peace Tax Fund Act — designed to allow the taxpayer to earmark a specific amount of tax money to go into a federal fund to be used only for peaceful purposes — will be approved by Congress soon.

What happens when you take these steps?

How do you cope with the IRS?

No matter what category of refuser you are, what generally is going to happen to you is something like this:

If a tax is owed, a notice of tax will be sent to you.

The IRS is required to issue this bill which is a demand for payment.

You are then required by law to make payment within 10 days of the date of this bill.

If the tax remains unpaid after the 10-day period, a statutory lien is automatically attached to your property.

The law also provides for interest and penalty for late payment at this time.

Once this notice of tax lien has been filed at your courthouse, it becomes a matter of public record and may adversely affect your business transactions or other financial interests.

It could impair your credit rating; therefore, it is normally filed only after the IRS has sent you a second notice of deficiency and tried to contact you personally, giving you the opportunity to pay.

After the lien has been filed, a levy may be taken.

A levy is the taking of property to satisfy tax liability.

The tax may be collected by a levy on any property belonging to you.

In the case of levies being made on salaries or wages, you will usually be given written notice, in addition to the notice of demand, at least 10 days before the levy is served.

Generally, court authorization is not required before a levy action is taken, unless collection personnel must enter private premises to accomplish their levy action.

The only legal requirements are that the taxes are owed and that the notice and demand for payment have been sent to your last known address.

In taking a levy action, the IRS first considers levying on such property as wages, salaries and bank accounts.

Levying on this type of property is referred to as a seizure.

Willful failure to file or pay income tax can result in a criminal sentence of one year and/or $10,000 fine.

However, we know of no cases which have ever resulted in criminal penalties, except where there is a total failure to file any income tax form at all.

When you receive your notice of deficiency from the IRS, you will also be notified that you may elect to appeal your case to the US Tax Court;

if you decide to do so within 90 days of that time, the IRS process against you is halted for the duration of the case.

Several people have gone to Tax Court following this procedure, although in no case has anyone “won” there.

The Center on Law and Pacifism has advised and supported people filing cases in Tax Court and on the Appellate and US Supreme Court levels also.

If you lose your case in Tax Court, you may appeal to higher courts, and ultimately to the Supreme Court.

These appeals are based on the First Amendment free exercise of religion and other constitutional provisions.

Many of us are presently refusing 35 to 50 percent or more of our income taxes.

For others just beginning to consider war tax refusal, or those reluctant to refuse taxes in those quantities, a new project called People Pay for Peace, under the auspices of the Center on Law and Pacifism, offers an opportunity to participate.

The Center is coordinating this symbolic tax refusal movement by new reformers who withheld from their tax returns a few dollars, symbolizing their witness against military armament.

The amount is so small that it is unlikely the IRS will try to levy it.

Multiplied by thousands of people, this small amount will constitute a significant conscientious objection to payment for war.

There is still time to build the kingdom, time to protest armaments, time to create a spiritual community for those who turn from the idols of fear.

If I were to say to you, “I will not kill my neighbor, but I will pay someone else to do it,” would you not hold me accountable?

If we refuse to kill our neighbor but allow our government to do it with our money, are we not to be held accountable?

But then we must witness and suffer the consequences of our military tax refusal for conscience’s sake.

This is the price some Christians are paying for peace in .

According to another article in that issue, of 200 people who responded to a “Survey on Life-Style Changes” in an earlier issue of the magazine, 20% had taken the step of “keeping income down in order not to pay taxes.” Another 25% wanted nothing to do with such a step. (source)

I was a little surprised to see the fairly conservative Brethren Evangelist devote several pages of its issue to reprinting part of the Statement of the Findings Committee of the “New Call to Peacekeeping” conference (source).

The Brethren Church was not (as the Church of the Brethren was) a partner to this conference, but they did send an observer.

The magazine was careful in its preface to say: “The printing of this Statement does not mean that either the Peace Coordinator [Doc Shank of the Brethren Church, who attended the conference] or the Brethren Publishing Company endorses it in its entirety. It is our hope that it will be read carefully and with an open mind.”

Mention of tax resistance was brief in the published excerpt (“We urge the development of support groups within congregations and meetings for those individuals who are working at peace issues such as war tax resistance, simple lifestyles, and nonviolent action.”) but this makes for a rare positive mention in this usually more stodgy magazine.

In the magazine followed up with a second excerpt from the Statement (source).

This one was more explicit and direct:

We call upon members of the Historic Peace Churches to seriously consider refusal to pay the military portion of their federal taxes, as a response to Christ’s call to radical discipleship.

We challenge ourselves and also our congregations and meetings to uphold war tax resisters with spiritual, emotional, legal, and material support.

We call on our church and conference agencies to enter into dialogue with employees who ask, for reasons of moral conviction, that their taxes not be withheld.

We suggest that alternative “tax” payments be channeled into a peace fund initiated by the New Call to Peacemaking or into existing peace funds of constituent groups.

We call on our denominations, congregations and meetings to give high priority to the study of war tax resistance in our own circles and beyond.

Another element of the statement gave a thumbs-up to the World Peace Tax Fund legislation.

There were a couple of horrified letters to the editor that followed, from Brethren who didn’t want to see their church tangled up with the anti-war movement, but otherwise not much discussion.

In , Brethren churches had to make tough choices of how far to go to support their war tax resisting pastors in battles with the government.

At the Annual Conference , the Church approved a position paper recommending that congregations consider civil disobedience in such cases.

The issue of Messenger reported on how, in the wake of a discouraging Supreme Court decision in an unrelated case, “[t]he General Conference Mennonite Church has put on hold a war tax lawsuit against the Internal Revenue Service.” (source)

, the magazine reported on a Brethren congregation that struggled to decide how far to go to support a war tax resisting pastor:

After agonizing debate.

Prince of Peace Church of the Brethren, South Bend, Ind., voted to comply with an order to pay the Internal Revenue Service part of the wages of pastor Louise Rieman, a war tax resister.

Prince of Peace is the first Church of the Brethren congregation to be faced with the tax-resistance issue.

Louise Rieman and her husband, Phil, have been withholding a percentage of their taxes to protest military spending, and have also withheld information about bank accounts from which the IRS could take tax money.

When the church was asked to hand over part of her wages, the Riemans asked the church board to refuse.

The board passed a resolution that supported the Riemans and denied the IRS request.

But the resolution was defeated 20 to 16 when it was sent to the church council for consideration by the entire congregation.

The debate focused on the biblical basis for and against tax resistance, the moral implications of breaking the law, and preservation of the congregation amidst the controversy.

, in response to a Northern Indiana District query, Annual Conference formed a committee to study war tax resistance.

A report is expected at the conference in Baltimore.

An Oregon congregation, however, decided to take a stronger stand (from the issue):

Peace Church of the Brethren, in Portland, Ore., has voted unanimously to refuse to comply with an Internal Revenue Service effort to collect war taxes owed by pastor Rick Ukena.

The congregation also voted to issue a public statement explaining the decision, and to raise funds to pay any fine arising from noncompliance with the IRS.

Ukena and his wife, Twyla Wallace, have withheld taxes , and the government has seized the money each of those years.

IRS actions against war tax protesters have become speedier and more severe under the Reagan Administration, and this year a levy was imposed against the church.

After a committee explored alternatives with an attorney and with Chuck Boyer, Church of the Brethren peace consultant, a special congregational meeting was held to consider the options.

“Most inspiring was the way the church took it on without my insistence,” said Ukena.

“People were really trying to discern the Spirit.”

Earlier this year, Prince of Peace church in South Bend, Ind., voted to comply with an IRS order regarding pastor Louise Rieman (see [above]).

Ukena was a conscientious objector in and says tax resistance has become a way of life for him.

“I would encourage people to not take the action,” he cautioned, “unless they’re aware of what they’re doing.”

“It was a really scary decision at first,” he added.

“We really prayed and talked to others and read the Bible to determine what was right.

It’s nice to fear God more than the IRS.”

Shirley Whiteside wrote in to applaud the Peace Church’s stand (source):

I rejoice to see this kind of integrity supported within the church.

I hope that one day the greater church will realize our hypocrisy.

To officially proclaim “All war is sin,” while we are party to war with no visible resistance, decries our loyalty to the gospel we claim.

At the Annual Conference, the Church of the Brethren decided whether or not to take a stronger stand that might include corporate civil disobedience.

By a supermajority, they voted to do so:

What started out at the Annual Conference as a study on war tax resistance came out of the Conference as a position paper.

The job of the study committee on war tax consultation was to answer the basic question of how an institution should respond to employees who object to payment of the part of their taxes that goes for military support, said Phillip Stone, General Board member and chairman of the committee.

In its list of recommendations, the committee suggested that “congregations and church-related institutions give consideration to a range of extra-legal options.”

Included is the option of corporate civil disobedience by supporting an employee involved in war tax resistance.

Moderator Paul Hoffman said that by recommending civil disobedience the study paper became a position paper, and needed a two-thirds majority — which it did receive from the delegate body.

Preceding the listing of extra-legal options was a listing of legal means by which institutions could support employees involved in tax resistance.

The committee stated that only after legal means were exhausted should an institution enter into civil disobedience.

In conclusion, the committee called on the larger church community to give support to any church-related organization involved in civil disobedience.

This statement is conspicuously absent from the Church of the Brethren Resolutions & Statements listed on the official Annual Conference website today.

I’m not sure how to explain that.

Maybe we’ll find out as I continue to hunt through the archives.

We need to name the huge expenditures for weapons for what it is, blasphemy against the goodness of God’s creation, a sin we commit together.

In light of this reality I would like to pass on a suggestion from the New Call to Peacemaking Conference at Elizabethtown College :

Instead of focusing on the division between those who pay and those who resist war taxes, let’s all join together in witnessing against war taxes even though we do this in different ways.

Some will witness to people in government through letters accompanying or sent concurrently with their tax payment and returns.

Some will reduce their income or increase their giving in ways as to decrease or eliminate war taxes.

Some who pay under protest will support by word and deed brothers and sisters who withhold a portion or all of their taxes.

Some of us will continue to witness our strong concern through withholding monies in civil disobedience to the tax laws.

This attitude and these actions are consistent with our Annual Conference decisions on this issue.

The issue reported on the war tax resistance debate as it was taking place in the General Conference Mennonite Church (source), and the issue followed up with a report of Church employees who had asked the church to stop withholding war taxes from their salaries (source).

Another news brief in the issue described the World Peace Tax Fund as a bill that “would amend the Internal Revenue Service Code so that conscientious objectors could have their tax payments spent for nonmilitary purposes,” and reported on lobbying efforts.

The issue gave another example of corporate tax resistance in the Church of the Brethren:

The Michigan District board has instructed its district personnel to withhold the Federal excise tax on district telephone bills.

It is forwarding the resolution to the Internal Revenue Service and to congressional representatives.

The withheld funds will be redirected to a Michigan District Peace Tax Fund and used by the district witness commission.

The action was based on Annual Conference statements of , , and .

The board “commend(s) this witness to all Brethren, local congregations, the General Board, and Annual Conference for their study and prayerful consideration,” and also encourages other forms of witness, such as lobbying for the World Peace Tax Fund Bill.

A profile of Brethren Volunteer Service volunteers Steve & Sue Williams in the issue included this detail:

Another attraction to volunteer service for the Williamses was their desire not to pay taxes for war purposes.

Before they married, Steve was a tax resister, withholding a certain amount of money as a protest against the government’s using his taxes for the military.

But Sue was uncomfortable with tax resistance and, after they married, they began looking for an alternative.

One was simply to make a lot of donations to charity.

“Before BVS we were working full-time and giving a lot of money away,” Steve said.

“We began looking for a way to give away time and not money.”

I also found this article in The Morning News of Wilmington, Delaware (). Excerpt:

Brethren still withholding taxes

How to protest “sin of war” is on denomination’s conference agenda

by Eileen C. Spraker and Stephanie Whyche Staff reporters

In , the Vietnam War sparked members of the Wilmington Church of the Brethren not to pay the church’s federal telephone excise tax for a year.

Although that war is dead, tax-withholding among members of the Church of the Brethren is very much alive.

How to support Brethren institutions and individuals who choose to withhold “war taxes” will be on the denomination’s agenda during their national conference, which opens in Baltimore.

Traditionally, the denomination has held to the belief that all war is sin.

Brethren 35 years ago established the Brethren Volunteer Service for conscientious objectors as an alternative to military service.

Some members of the church, for reasons of conscience, have chosen to withhold part or all of their taxes to avoid supporting the military.

A paper to be presented at the Baltimore meeting will discuss the lawful choices available to such people, the church’s position on civil disobedience, and support for institutions and people pursuing tax resistance.

“This is one of the most timely issues we have right now,” says the Rev. Allen T. Hansell, pastor of the Wilmington Church for the Brethren.

According to Hansell, some employees of the six Brethren Colleges and employees in at least one of the Brethren retirement homes are currently involved in tax resistance efforts.

But some are less than successful because their employers are withholding taxes from their employees’ pay in accordance with regulations.

“The issue is these employees, on the basis of conscience, don’t want this money withheld.

Legally, the employers are bound.

That’s why this issue is coming before the conference,” Hansell said.

What’s more, Hansell said, although there’s “no war right now, the telephone excise tax continues,” even though Congress promised to discontinue it once the Vietnam war had ended.

During the Vietnam War, members of Hansell’s church, in Richardson Park, stirred up a lot of controversy because they refused to pay the church’s federal telephone-excise tax.

The action was because of their belief that part of the tax was financing the war.

“Our concern was to make a witness of the issue that this money was going directly to the war effort,” Hansell said.

“It was a matter of principle.”

The proposal to be presented before the conference calls upon employers of employees involved in military tax-resistance efforts to take the issue seriously and maintain open dialogue with their employees.

It does not recommend that church institutions get involved in tax resistance efforts, but if they do, it calls upon the denomination to support that effort through such methods as legal assistance.

Other recommendations will suggest that Brethren seek voluntary wage reductions, and that they work with the Mennonites and Society of Friends to bring about changes through legislation.

One of the best debates I have seen about the biblical basis for tax obedience or tax resistance was found in the Messenger in .

In the issue, the Messenger hosted a debate between Vernard Eller and Dale Aukerman on the biblical basis for war tax resistance or obedient tax payment:

The report to Annual Conference of the Committee on Taxation for War shows a great diversity of opinion within the committee itself.

Accordingly, there is at present no inclination to try for any change of policy.

Rather, the recommendation is for a churchwide study of the Conference statements already on the books.

And because I find myself highly in favor of this proposal, I offer this article as a contribution to the study for which the reports calls.

I address myself solely to the matter of scriptural evidence and interpretation.

Accidentally, as it were, I have been doing major research on the subject — for a book even now in press.

I had no intention of studying tax resistance per se, but was addressing the much broader question of how a Christian should relate to the host of regimes, parties, and ideologies competing with each other in the effort to direct and control society.

My mentors in the matter make up a 150-year-long string of biblically oriented thinkers who constitute the modern theological tradition I feel comes closest to Brethrenism.

These people are Soren Kierkegaard, J.C. and Christoph Blumhardt, Karl Barth, Dietrich Bonhoeffer, and Jacques Ellul.

And as I chased them down on my particular topic, I found them regularly going to the New Testament tax passages.

It became apparent that this was not so much their doing as that of the Bible itself.

The logic of the move is this:

The all-dominating political reality of Palestine during the New Testament period was that of a most evil and vicious Roman regime occupying, oppressing, and eventually destroying the homeland of the Jewish people (and earliest Christians).

Over against this power was pitted that of the Jewish liberationists and freedom fighters commonly known as the Zealots.

Thus, the pattern of political decision forming the context not only of our tax passages but of all New Testament political counsel is one that applies as well to almost any issue, ancient or modern:

One can either (1) legitimize the presently established regime as representing God’s will for the nation, or (2) follow God’s will in supporting the efforts of the revolution against that regime.

“Revolution” here does not necessarily imply terrorism, guerrilla warfare, or other forms of physical brutality, but identifies any bringing to bear of political power in the effort to overthrow an evil regime or to pressure it into becoming good.

By its very nature, of course, the gospel would have as much as prohibited Christians from any desire to legitimize a cruel and pagan Roman Empire.

Yet, also, by its very nature, the gospel would make it very tempting for Christians to align themselves with liberation movements and efforts at just revolution.

Accordingly, on the one hand the New Testament consistently refuses to encourage any legitimizing tendencies — while on the other hand it actively discourages the greater temptation of revolution.

And “tax revolt” — i.e., withholding taxes as a power-play against government evil — becomes the New Testament’s regular signal and symbol of Zealot liberationism in particular and, in general, all forms of revolution.

(It is significant that this symbol has Christianity opposed to revolutionism quite prior to and apart from its physical violence.)

Regarding particularly the exegesis of Mark 12, in addition to the five thinkers named above I consulted four contemporary New Testament specialists: Martin Hengel, Gunther Bomkamm, Leander Keck, and Howard Clark Kee.

All nine scholars are in total agreement, each reading the tax passages in the context of the historical situation described above.

In the process, the scriptures come clear, manifesting their theological consistency as warnings against Christian involvement in political revolutionism.

My researchers are not exhaustive; but I failed to come across even one reputable scholar doing serious biblical exposition who concludes that these passages actually imply a support for (or even a leaving room for) Christian tax resistance.

The crucial New Testament passages are three:

Mark 12 — which is actually Mark 12:13–17 (the fact that both Matthew and Luke later pick up the incident for their own Gospels adds no new meaning but does corroborate the significance it held in the eyes of the early church);

Romans 13 — which is actually Romans 12:14–13:10;

and Matthew 17 — which is actually Matthew 17:24–27.

All of my nine, except the Blumhardts, address the Mark 12 passage — and all agree as to its reading.

The earliest writer, Kierkegaard, says it best.

(Consider that, in the historical context, to make Jesus “king” or to call him “Messiah” politically could mean nothing other than “revolutionary leader against Rome.”)

The small nation to which Jesus belonged was under foreign domination, and naturally all were intent upon the thought of shaking off the foreign yoke.

Hence they would acclaim him king.

But, lo, when they show him a coin and would constrain him against his will to take sides with one party or the other — what then?

Oh, worldly passion of partisanship, even when thou callest thyself holy and patriotic — nay, so far thou canst not stretch as to break through his indifference… No, he posits the infinite yawning difference between God and the Emperor: “Give unto God what is God’s!” For they with worldly wisdom would make it a question of religion, of duty to God, whether or not it was lawful to pay tribute to the Emperor.

Worldliness is so eager to embellish itself as godliness, and in this case God and the Emperor are blended together in the question,… that is to say, the question takes God in vain and secularizes him [by implying that whether the Emperor does or does not get his tax coin is an issue somehow related to or comparable with whether God does or does not get what belongs to him].

But Christ draws the distinction, the infinite distinction, and he does this by treating the question about paying tribute to the Emperor as the most indifferent thing in the world, regarding it as something which one should do without wasting a word or an instant in talking about it — so as to get more time for giving God what belongs to God.

Barth, Bonhoeffer, and Ellul speak a single mind on the Romans 13 passage.

Each finds it to be in complete agreement with Mark 12;

Ellul thinks that Romans 13 even shows that Paul was familiar with the Mark 12 incident.

Yet Barths’s exposition is easily the most extended and insightful of the three:

The revolutionary seeks to be rid of the evil by bestirring himself to battle with it and to overthrow it.

He determines to remove the existing ordinances, in order that he may erect in their place the new right…

The revolutionary must, however, own that, in adopting his plan, he allows himself to be overcome of evil (Rom. 12:21)… What man has the right to propound and represent the “New,” whether it be a new age, or a new world, or a new spirit?…

Overcome evil with good.

What can this mean but the end of the triumph of men, whether this triumph is celebrated in the existing order or by revolution?… There is here no word of approval of the existing order; but there is endless disapproval of every enemy of it.

It is God who wishes to be recognized as He that overcometh the unrighteousness of the existing order…

Even the most radical revolution — and this is so even when it is called a “spiritual” or “peaceful” revolution — can be no more than a revolt; and that is to say, it is in itself simply a justification and confirmation [not of God’s “new” but] of what already exists [namely, one human ideology or another]…

For this cause ye pay tribute also (Rom. 13:6).

Ye are paying taxes to the State.

It is important, however, for you to know what ye are doing.

If I might interpret: If you are paying those taxes as a positive legitimization of the state and its evil activity, you are wrong.

If, on the contrary, you are withholding those taxes as an act of protest and defiance against the evil of the state, you are wrong again.

“But what other option is there?”

Well, if Jesus is correct that Caesar’s image on the coin is proof enough that it belongs to him, then, rather than saying that we do pay him taxes, would it not be more correct to say that we do not try to stop him from taking what is his, do not revolt, do not return evil for evil?

As Barth puts it, “It is important for you to know what you are doing.”

The Matthew 17 incident is not as crucial as the first two; only a couple of our scholars mention it — and that merely in passing.

However, the words Jesus speaks on this occasion are as significant as anything we find on the subject.

In the process of explaining why he pays the tax, Jesus forestalls any idea that a Christian’s payment of taxes is to depend upon the relative righteousness or unrighteousness of the collecting regime.

He says, in effect, that no human regime is righteous enough for the Christian ever to owe it anything.

No, there is only one Father and King of whom Jesus knows himself and his followers to be “sons.”

No one except that “father” can claim anything from these “children.”

So the kings of the earth will have to do their collecting from “others,” not from Jesus and the children of God.

Thus, when Jesus goes on to say that he chooses to pay the tax even though he doesn’t owe it, he is saying that Christian payment never is made as recognition of either the rights or the righteousness of the State.

No, it is made to regimes good, bad, and indifferent — and that sheerly out of obedience to God’s command to love, not revolt, and not cause offense.

It strikes me that the word of God speaks quite clearly on the matter of tax resistance — and that that word is hardly in support of the practice.

I do fully honor the conscientious integrity of those who feel led to withhold some of their taxes; but I cannot confirm that leading as being biblical.

Rendering to Caesar [con]

by Dale Aukerman

If the explosive power of the Hiroshima bomb is thought of as the width of a lead pencil, the destructive potential of the current nuclear arsenals is the height of Mount Everest.

If the United States were to explode a bomb each day to destroy a city, the present stockpile would last more than one hundred years.

The Reagan administration plans to build 1,700 additional nuclear bombs a year and press ahead in an arms buildup that is taking us into the war that can destroy God’s earthly creation.

Or to give just one example of the increasing ghastliness of conventional weapons, white phosphorus bombs have a sticky jelly, which adheres to the human body, burns at a temperature of more than 3000° Centigrade for at least 24 hours, and turns victims into agonized human torches.

The United States has been supplying these bombs to a number of countries, including El Salvador and Israel, which used them against civilians in its invasion of Lebanon.

As for the huge sums in federal tax dollars needed to purchase all these weapons and much more.

Brother Vernard Eller seems to say:

No problem; we have the clear command of Jesus to pay up.

After the Romans destroyed Jerusalem in , they changed the Temple tax mentioned in the Matthew 17:24–27 story into a tax for the temple of Jupiter Capitolinus in Rome.

Some governments have levied taxes so exorbitant as to leave children and others starving.

Certain taxes have been imposed specifically for financing a war.

A government could use half its budget to keep masses of people in concentration camps or to run a network of brothels for the diversion of the male population.

Vernard evidently says: No problem basically;

Christians go by the command of Jesus.

According to the Friends Committee on National Legislation, $350 billion or 55 percent of the 1984 federal budget went to military spending and the cost of past wars.

Figured on a per-capita basis, the fraction of that for the Church of the Brethren membership was $255 million.

All Brethren church-related giving for the year was somewhat over $55 million.

As Vernard sees it, we need not to be troubled that hundreds of millions of Brethren dollars go to finance the arms buildup;

paying is “the most indifferent thing in the world.”

Vernard’s greatest service to us Brethren has come through his insistence that, if we claim to be a New Testament church, we must strive to live by the New Testament.

I stand with him in that insistence.

If Jesus in Mark 12:17 was saying that disciples of his should pay without question every tax levied by whatever government they are under, that, for us, should settle it.

But did Jesus say that?

Vernard failed to find “even one reputable scholar” whose treatment of the passage would leave open the option of Christian tax resistance.

I would call his attention to some.

A.M. Hunter writes: “This was an ad hoc answer, not a fixed and permanent rule for every situation.”

Jean Lasserre gives this interpretation:

“Jesus is not passing any judgment on the lawfulness of the Roman tribute;

He is speaking only of this particular coin.

It represents the things that are Caesar’s, not a foreign tyrant’s right to exact a tribute.

In other words, Jesus recognizes Caesar as having the right to the coin but not to the tribute.

This is what disconcerts His questioners and breaks their trap.”

Francis Wright Beare comments,

“The famous saying leaves untouched the fundamental problem: how are we to draw the line between the legitimate requirements of the society to which we owe allegiance, and the demands of loyalty to God?”

The insight of Paul S. Minear is most helpful:

“By his reply Jesus forced them, as students of the law, to decide for themselves where to draw the line between God’s jurisdiction and Caesar’s…

The riddle remains that each must solve for himself or herself.

Keep in mind that the first audience for this riddle was neither the crowd nor the disciples, but only their adversaries.”

Jacques Ellul, whom Vernard points to as one of the six thinkers decisively supporting the pay-without-question interpretation, states in The Ethics of Freedom that Jesus “refuses to answer the question whether he is for or against Caesar or whether taxes should be paid or not.”

In any case, appealing to the authority of European theologians within other church traditions has not for Brethren been a main way of discovering what faithful discipleship to Christ is.

Those enemies of Jesus thought they had the perfect trap.

If Jesus said, “Don’t pay the tax,” they would denounce him to the Roman authorities.

If he said, “Pay the tax,” they would trumpet that to the common people, who hated the tax as symbolizing Rome’s repressive occupation of their country.

His enemies could spread the word:

“The Messiah is to liberate us from Roman rule, but this fellow supinely tells us to pay the tax.”

The reply, “Don’t pay the tax,” would have pleased Jesus’ adversaries the most, and that they did not get.

According to the interpretation Vernard advocates, they did receive the other answer, “Pay the tax,” and could proceed with their strategy contingent on that reply.

That is, their trap did catch Jesus.

But the close of the story in each Gospel brings out that the trap did not succeed.

“And they were not able in the presence of the people to catch him by what he said; but marveling at his answer they were silent” (Luke 20:26).

Jesus had not said, “Pay the tax.”

Jesus’ enemies were intent on exposing him as a collaborator, if not a Zealot revolutionary.

When they produced the detested Roman coin, they — not Jesus — were exposed as the collaborators.

When the Jewish leaders brought Jesus to Pilate, they accused him of “forbidding us to give tribute to Caesar” (Luke 23:2).

They would hardly have used that accusation if Jesus a short time before, in a public context charged with excitement about him, had counseled payment of the tribute.

Usually people quote, “Render to Caesar the things that are Caesar’s,” and omit the rest.

This pernicious misuse of the saying has had immense significance in the history of the West.

Vernard emphasizes that the second part of Jesus’ reply is vastly more important than the first, but he remains within the traditional interpretation by holding that on the matter of taxes we can take the first part and know its meaning for us without the second part.

Brethren historically have held that young men should not simply comply with whatever notice comes from a draft board and that what can rightly be given to the government has to be discerned in relation to giving ourselves totally to God.

Brethren who are deeply concerned about paying money into a monstrously expanding military buildup are not advocating refusal of all taxes, complete noncooperation with government, or trying to overthrow it.

But we believe that we can come to a Christian understanding of taxes that should be handed over to the government only in the light of Jesus’ supremely central command that we give ourselves fully to God.

The crucial issue is whether the first part of Jesus’ reply is taken by itself as a clear, sweeping command or whether it is seen as a riddle calling for the discernment that can come within our striving to love God and follow Jesus.

Jesus, as a Jewish male between the ages of 14 and 65, was subject to the Roman poll tax of one denarius a year.

We have no record that he paid it (his adversaries could have cornered him on that point) — or that he did not pay it.

But in Matthew 17:24–27, the tax in question was for the Temple in Jerusalem.

Jesus told Peter that children of the heavenly King are free from any obligation to pay taxes, but “not to give offense… give the shekel to them for me and for yourself.”

Here too Jesus did not command that all taxes are to be paid regardless.

(Much of what Vernard finds in the passage is not there at all.)

The key consideration is that one not give offense, cause others to fall away from faith.

Had Jesus refused to pay the Temple tax, he would have appeared to reject the Mosaic law (Exodus 30:11–16) and the Temple itself.

But in some circumstances paying a tax can constitute giving offense, impelling others away from God.

When national leaders are stumbling blindly toward slaughtering unimaginable multitudes of those for whom Christ died, casual payment of all the money asked for toward their mad projects amounts to abetting them in their fateful falling away from God.

To resist paying such taxes can provide opportunities for pointing agents of government to Jesus as Lord.

On the Romans 13 passage John Howard Yoder writes:

“Verse 7 says ‘render to each his due’; verse 8 says ‘nothing is due to anyone except love.’

Thus the claims of Caesar are to be measured by whether what he claims is due to him is part of the obligation of love.

Love in turn is defined (verse 10) by the fact that it does no harm.”

Paul was probably restating the teaching of Jesus found in Mark 12:17 and his Master’s call to the most careful discrimination between what under God can be rightly rendered to the ruling authority and what cannot.

Thus we have cogent reasons for concluding that Vernard’s article, the Brethren tradition of paying all taxes without question, and the Annual Conference Statement on Taxation for War (of which Vernard was a principal writer) depend on a mistaken understanding of the words of Jesus.

There is no easy answer— certainly not in four Greek words in Mark 12:17 taken by themselves.

In this issue we need together to seek a fresh discernment of what from us belongs to God.

Bob Gross wrote a letter-to-the-editor in response, in which he made this point (source):

Eller may not realize that for many Brethren who feel led to refuse to pay taxes for war, the primary reason is not the one his article cautions against.

Rather than “an act of protest and defiance against the evil of the state,” our non-payment is a simple, humble attempt to refrain from contributing to that evil.

This is not done in a quest for purity or out of guilt.

It comes from a desire to be more conformed to the will of God and to witness to God’s kingdom.

John Stoner from the Mennonite Central Committee also wrote in to reiterate that “When Jesus was asked, by people wishing entrap him, ‘Is it lawful to pay taxes to Caesar or not?’ his answer was not ‘Yes.’ ” (source)

Barry Shutt, on the other hand, took the point of view that war tax resistance was not an effective response, and should be discouraged for that reason (source). Excerpts:

[A] legitimate concern for any witness is the question of effectiveness.

One could seriously question if violating the law is very effective in a society where most people believe it is best to work within the system to initiate change.

And if tax resistance only leads to the tax resister paying more money to the government in fines and penalties, the question of effectiveness becomes an even greater concern.

The point to be made, of course, is, “How do we work effectively to bring about change?” When the system provides adequate means by which one can voice concerns and attempt to change priorities, tax resistance as a means to bring about change becomes even more questionable.

If tax resisters would argue that effectiveness is not the primary concern or objective but simply the witness alone is the objective, then one should ask if simply writing letters of protest to our elected officials is any less of a witness?

If God hears prayers made from the privacy of the prayer closet, God surely takes note of witnesses made through the less conspicuous channels available for us to voice our concerns.

Being fined or arrested may not be necessary, and I would suggest neither is tax resistance.

A further letter in support of resistance, by Dale Hess, did not add much new to the argument, but, in implicit contradiction to Shutt, said of war tax resistance: “The importance of this type of peace witness is hard to overestimate” (source).

The Annual Conference had assembled yet another committee to issue yet another report about war tax resistance, and that committee reported on its work in .

The messenger reported on their recommendations (source):

The assignment from last year’s Annual Conference was two-fold.

In response to a request that the committee study and recommend how Brethren should respond to the dilemma of paying taxes for war, the committee chose not to write a new position paper.

Instead it recommends that Brethren undertake an extensive study of earlier position papers and then determine more specifically what, in addition to the previous papers, is called for in the query.

The committee was also asked to make a recommendation about General Board payment of the federal telephone excise tax.

The committee recommends that the decision be made by the board itself, because of the liability of individual officers.

In action for war growing out of a General Board query of , delegates approved a study committee’s recommendation that the church undertake its own study of previous position papers before deciding whether a new paper on taxation for war is desired.

The General Board is to prepare a study packet and to compile responses from across the denomination.

In an unusual move, the delegates extended the life of the study committee, directing it to recommend to the Cincinnati Conference a process to complete the study.

The same committee, assigned to respond to a Michigan District query about telephone tax redirection, recommended (and Conference approved) that any decision about whether the General Board should withhold the federal telephone excise tax should be made by the Board, since its staff could be held liable.

“A gratified war tax study committee regrouped after finding it had two more years of life.

Clockwise from left:

Chuck Boyer, Gary Flory, Phil Rieman, Dick Buckwalter, Vi Cox.”

A letter in the issue dissented from the war tax resistance craze on the grounds that “many non-Christian people who deeply resent having to support welfare programs” would use the same logic to avoid their taxes (source).

, a group of Brethren showed up at the Lombard, Ill., Internal Revenue Service office and tried to pay part of their taxes with bags of groceries.

The group from Bethany Theological Seminary included about 33 students and faculty member Dale Brown, and they wanted to let the IRS know that they objected to paying taxes for war.

“I believe in paying taxes, but not for defense,” said Brown.

The group took about $160 worth of food to the IRS and contributed about the same amount to peace organizations.

IRS officials refused the groceries, which were then given to local food pantries and soup kitchens.

The hows and whys of war tax resistance continued in the pages of the Messenger in , as Cliff Kindy made the case for voluntarily simplicity and living on an income below the tax line.

In the Messenger printed an opinion piece by Barry Shutt that had attacked war tax resistance on the grounds that it was ineffective.

This somewhat novel argument prompted some rebuttals in the issue (source).

L. William Yolton (of the National Interreligious Service Board for Conscientious Objectors) wrote that Shutt’s arguments were of the same sort that conscientious objectors to military service hear —

“Are there not other evils to be resisted? So don’t resist this one.” “There are differences of opinion among Christians about an issue, so let us wait to do the good until all are agreed.” “If you do not do this evil, then someone else will be drafted in your place to do it, so you must do evil.”

— and Brethren know by now not to bend to such arguments.

David W.

Fouts said that his own experience was proof that writing protest letters was a poor form of witness compared to resistance:

For years I enclosed a carefully composed letter with my tax return protesting the use of my tax dollars for military purposes, but I have yet to receive a single reply from an IRS or other administrative official.

My actions apparently spoke louder than my words.

However, when I withheld 10 percent of my income taxes to protest the proportion spent on nuclear weapons, I received repeated attention from the IRS in the form of letters demanding payment and threatening to confiscate my property.

Cliff Kindy wrote in for the issue to recommend a non-disobedient form of tax refusal (source).

It has been good to see the issue of paying taxes for war highlighted in Messenger.

The issue for our family has been “Who is Lord?”

Is Caesar Lord, through the channels of IRS?

Or is Jesus?

Caesar calls for our money and our life, and, yet, Jesus calls for our all.

To which will we respond in obedience?

(We cannot have two masters.) We fret about the consequences of breaking the law, and yet seem unconcerned about the possibility of falling into the hands of the living God (Heb. 10:31).

Certainly God, who asks us to stand over against the powers of death, will care for us in our obedience.

We must venture obedience.

It is too easy to assume that in this instance obedience to God leads directly to disobedience to Caesar.

For those who struggle over that concern, there is a possible answer.

To limit one’s income to below the taxable level is not illegal, and, although still extravagant by the world’s standards, is moving in the direction of standing with God’s little people.

We as a church have not examined seriously the results of living at an income level that does not require missiles, bombers, and Trident submarines to protect it.

You might like to try it for a few years.

Several questions for those who pay taxes for war:

1) Do you give more money to the church than you pay to IRS?

More than you pay to IRS for the 50-to-70-percent portion of your tax that is military-related?

2) How large would that military-related percentage need to get before you would say “No”?

3) If that percentage of the federal income tax were going to finance houses of prostitution or liquor warehouses, would you pay it?

4) If it would be proper for a Christian to channel monies to the Peace Tax Fund (if such a proposal is ever passed for conscientious objectors), does that not imply that we should feel some urgency even now to pay those dollars toward similar purposes?

(Does the law of the land ever define the Law of God?)

5) If we spoke the passages of Matthew 22:21, Mark 12:17, and Luke 20:25 with the same emphasis Jesus probably had, (“Render to Caesar the things that are Caesar’s, and to God the things that are God’s”), might we not also find “…this man… forbidding us to give tribute to Caesar…” (Luke 23:2)?

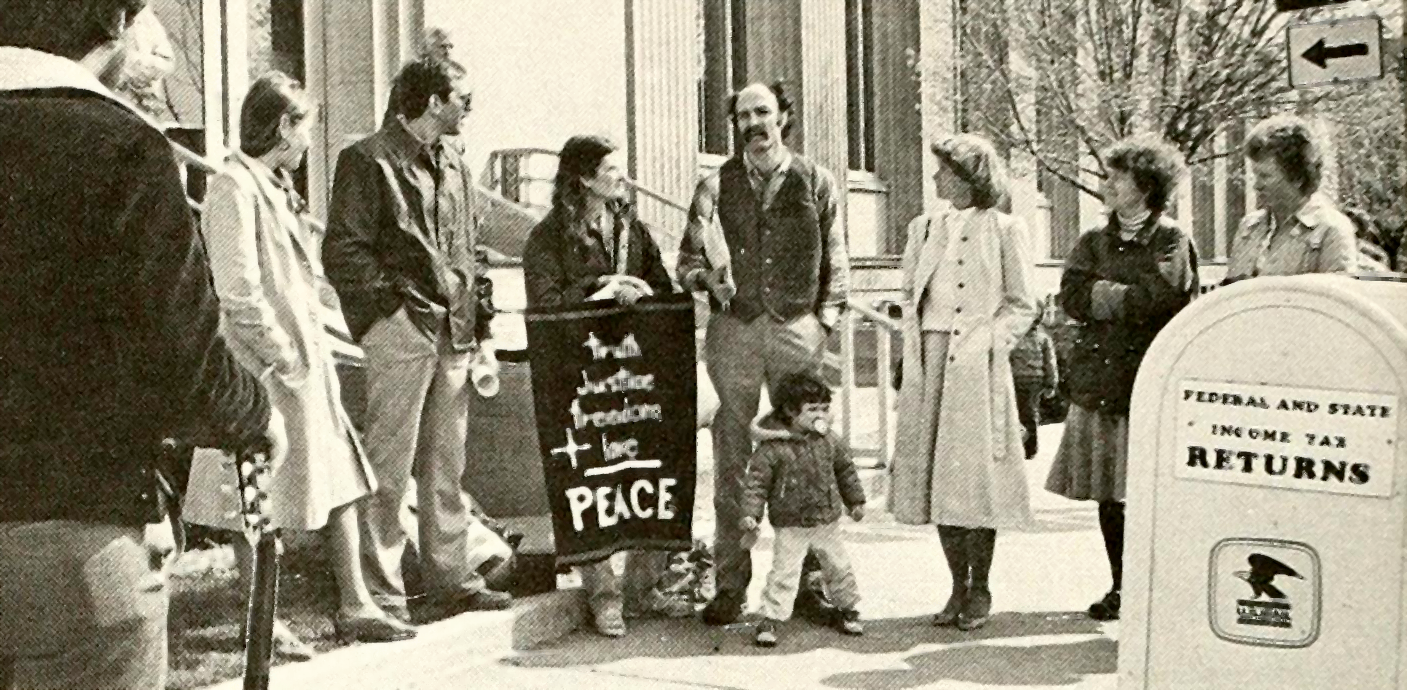

Ten Christians in Kalamazoo, Mich., gathered in front of the courthouse to voice their opposition to military funding.

Representing the Catholic Church, the Mennonite Church, and the Church of the Brethren, they withheld a total of $6,400, the portion of their income taxes that they claimed would help fund the military budget.

Deanna Brown, pastor of the Skyridge Church of the Brethren, thought twice before joining the peace demonstration, since she didn’t want to be misunderstood by other Christians.

“But because of my vocation as a disciple of Christ,” she said, “I feel called to make this witness and to say there is another way — the way of reconciliation, humility, service — and that’s the way of Jesus Christ.”

Added Steve Senesi: “We are not opposed to taxes.

The point today is to speak to where those funds go and how they are spent.”

The withheld tax money was given to five local social service agencies:

Center City Housing, Loaves and Fishes (a clearinghouse for emergency food pantries), Habitat for Humanity, Kalamazoo Diaconal Conference, and Kalamazoo Youth Ministry.

“Deanna Brown and Terry Ciszek (to left of banner), of the Kalamazoo Church of the Brethren, joined others who were opposing the use of tax dollars for military purposes.”

The issue brought news of Brethren who had been arrested in demonstrations opposing U.S. militarized foreign policy (source), including:

Phil Rieman, co-pastor of the Ivester church in Grundy Center, Iowa, was part of an effort to link the payment of tax dollars and US funding of the contras [Nicaraguan insurgents].

He and 10 others were arrested after refusing to leave the IRS building in Waterloo.

In the subsequent 2-day jury trial all 11 defendants were found “not guilty” by all six jurors on the grounds that the demonstration was justifiable.