Freund gives a brief overview of the history of conscientious tax resistance

that seems to me to understate it, though it’s possible that in

less evidence was easily available.

[I]t was not until the Vietnam War that tax resistance became a significant form of Christian witness against war.

One of the early Vietnam-era tax resisters was William Faw, a minister of the Church of the Brethren, one of the historic peace churches.

Faw had not come to my attention before, but Freund tells his story as follows:

William Faw: “Here I Stand; I Cannot Do Other”

William Faw was born in in Nigeria where his parents were missionaries for the Brethren Church.

His father took a post teaching at Bethany Seminary, and the family moved to Chicago where Bill grew up.

He went to college in Indiana and then attended the seminary until his graduation in .

While at school Faw was compelled to confront the issue of the draft. “Both my

parents were pacifists so I had decided early on that I would either be a

resister or a conscientious objector; I could not accept a student or

ministerial deferment in good conscience,” explains Faw. Despite his religious

background it still required a two-year battle with the draft board to obtain

his CO

status. By the time he received

CO status

he had a family and was never required to perform alternative service.

He received his first assignment in at the Douglas Park Church of the Brethren, a poor, multiracial community on the West Side of Chicago.

It was during this period that Bill Faw became a tax resister.

Faw explains that decision, saying, “I was a self-employed pastor and my wife was not working so we had control over our tax payments.

Since my wife was also a pacifist, we felt that it was necessary to protest the Vietnam War.

The question was, ‘How can we do this together?’ We spoke with several other Brethren who had been refusing taxes and listened to political leaders who opposed the war.

By early we decided to refuse to pay our taxes in full knowledge that it could lead to criminal punishment.”

When the time came to file their income tax

return, the Faws sent the

IRS a

long letter explaining why there was no check enclosed. Other resisters had

engaged in resistance by refusing even to file a return, but Faw believed that

a religious witness should be made in an open and public manner. The Faws’

letter made clear the personal struggle which accompanied their decision:

We refuse to willingly contribute to a “war machine” which is engaged in the very brutal war in Vietnam… In the past we felt that the ambiguities of tax paying outweighed the war-tax issue.

That is, our government’s expenditures for foreign aid, law enforcement, programs in health, education, and welfare, agriculture, urban redevelopment, and poverty fighting are worthy of support… Events have occurred which lead us to reconsider our responsibilities as citizens.

We feel we can be true to our national citizenship only if we oppose a so-called “non-war” that has not been constitutionally declared.

We feel that we can be true to our international citizenship as spelled out at the Nuremberg Trials only if we disassociate ourselves from and actively protest our unjust, illegal, morally deplorable, aggressive offensive against human beings in Vietnam.

But most basically we feel that we can be true to our Christian discipleship

only if we oppose… the seizure of God’s prerogative by the United States in

attempting to become the philosophical, theological, executive, legislative,

judicial, and policing agency for the entire world; only if we oppose the

exploiting of American “racism” by

A-bombing, napalming,

scatterbombing Asians; only if we oppose the mode of “evangelistic effort”

our nation is making in Vietnam to show the Buddhists what being a

“Christian” nation means…

Thus we are led to withhold our income tax and to seek constructive alternative ways of sharing our income… In God’s name, and under his judgment, we pray that we might choose the best path to make our witness.

…As a result, they chose to donate the tax money to the Canadian Friends Service Committee for the relief of war victims.

They were well aware that some of those victims who would be helped by their money were North Vietnamese and Viet Cong; they believed this action to be consistent with Jesus’ command to “love your enemy.”

The Faws refused to pay their income taxes for the next five years, donating

the funds to various international relief agencies. The Internal Revenue

Service sent an agent to attempt to obtain the taxes directly. When this

failed the

IRS

placed a levy on the Faws’ bank account and was able to collect the back

taxes. The Faws were not threatened with criminal penalties.

Freund says the Faws were also resisting their phone tax, but returned to being taxpayers in the wake of the Paris Peace Accords.

However, as of the writing of the book, they were planning to become resisters again by refusing a percentage of their income tax:

The continuing military buildup, especially nuclear weapons, has led us to resume tax resistance… We are being lulled into accepting more and more.

Johnson tried to give us guns and butter, but Reagan’s policy of sacrificing butter for guns represents a barbaric reversal of priorities.

Freund asked about the practical effectiveness of individual tax resistance.

…Faw conceded that it would be far more powerful if institutions were to openly advocate and practice tax resistance. “If one church did it, even a small one like the Brethren, the Mennonites, or the Quakers, it would have a tremendous impact on some of the liberal mainline denominations,” Faw believes.

However, even the New Call To Peacemaking, a grassroots movement within the historic peace churches begun in , of which Faw was the local chairman for two years, has failed to adopt a position of total resistance to war taxes.

This has been a source of frustration for Bill Faw, but he nevertheless believes in the importance of individual witness, “I would still do it even if no one else did.

There comes a point, with Vietnam or the arms race, where you say, ‘I’m not going to participate in that, no matter what the cost.’ It’s kind of like Martin Luther saying, ‘Here I stand; I cannot do other.’ ”

Freund then briefly described “A Simple Methodology” for Christians who were considering war tax resistance, covering the options of 1) paying taxes under protest, 2) voluntary poverty, 3) refusal to pay.

He then tried to discern what sort of guidance might be found in the Bible, considering the difficult “Render unto Caesar” and “the powers that be are ordained of God” sections in particular.

Then he returns to the problem of the lack of institutional support for war tax

resistance among Christian churches:

War Taxes: Where the Churches Are

Bill Faw and tax attorney William Durland express frustration that the churches, as national institutions, have not taken clear positions in support of tax resistance.

Durland, who counsels tax resisters, says, “Some church body will have to declare that it stands by the Gospel and not by the IRS.

This could have a chain reaction effect and lead to a coalition of churches to make it work.”

What holds them back? According to Faw, many Brethren have expressed “concern

for the biblical ambiguities regarding taxes, concern over the maintenance of

a certain respectability, and fear of the consequences.” Durland is somewhat

more cynical, “The Pope speaks out against war and then honors the Italian

Army.”

What is the position of the churches?

The historic peace churches, representing 400,000 members in the United States, have been discussing the issue since .

In , the Church of the Brethren recommended that, “Although the Brethren cannot agree as to whether tax withholding is proper, they can all recognize the propriety of using the means of dissent which the social order itself recognizes… We recommend that all who feel concern be encouraged to express their protests through letters accompanying their tax returns, whether accompanied by payment or not.” Many employees of these churches have not been satisfied with this position and have urged church agencies to refuse to withhold their federal taxes, a violation of the law.

The American Friends Service Committee (AFSC), responded by challenging the constitutionality of withholding as an infringement on the right of religious expression.

In the Supreme Court ruled in AFSC v. U.S. that a lower court ruling in favor of the AFSC was invalid and ordered AFSC to continue to withhold.

The AFSC has complied with that order since.

Pressure from employees of the Mennonite Church to refuse to withhold led to the following resolution adopted in , “We request the General Board to engage in a serious and vigorous search to pursue all legal, legislative, and administrative avenues for achieving a conscientious objector exemption from the legal requirement that the conference withhold income taxes from its employees.”

The New Call to Peacemaking

(NCP), a

more radical caucus within the three peace churches, has gone somewhat

further. In and again in

the

NCP

called upon members of the historic peace churches “to seriously consider

refusal to pay the military portion of their federal taxes, as a response to

Christ’s call to radical discipleship.” However, attempts to go further and

adopt a position which called “paying for war a sin parallel to the sin of

fighting war” was rejected. As one pastor at the meeting said, “We are calling

my congregation into deep water when they haven’t even gotten their toes wet.”

The mainline Protestant denominations have reacted cautiously or ignored the issue.

There is a growing movement within the Unitarian Universalist Association to take a position in favor of tax resistance.

One of the leaders of this effort is Rev. Philip Zwerling of the First Unitarian Church of Los Angeles.

He says, “Nowhere is military madness more manifest than in the nuclear arms race… and on one day of the year — April 15 — we break down and pay for it all… Is it not moral schizophrenia to blithely pick up the tab for the military mania that we speak out against?

It’s time to put our money where our mouth is.” However, for all the strength of this statement, the denomination as a whole has not adopted this position.

At the General Conference of the United

Methodist Church a resolution was adopted calling for support of those “who

conscientiously object to the payment of taxes for military purposes.” Here,

too, the group stopped short of calling on church agencies themselves to

engage in tax resistance.

Although large numbers of Roman Catholics are engaged in various forms of tax resistance, the church has taken no official position.

According to Father Bryan Hehir, Associate Secretary for International Justice and Peace of the U.S. Catholic Conference, “We have no policy on tax resistance… and I have not adopted a position intellectually on it.” Activist and author Father Daniel Berrigan thinks this position is becoming increasingly untenable, “More and more the question of paying federal taxes is going to become a question of conscience.

The government is stealing money and turning it into blood money.

We’re going to be pushed into a corner on whether we can recognize… our Christianity.”

Freund then recapped the example of (Catholic) Archbishop Raymond Hunthausen.

Excerpts:

Addressing the Pacific Northwest Synod of the Lutheran Church in America… Hunthausen surprised his audience by suggesting what form their action might take, “I would like to share a vision of an action which could be taken: simply this — a sizable number of people in the State of Washington, 5,000, 10,000, a half million people refusing to pay 50 percent of their taxes in nonviolent resistance to nuclear murder and suicide… Form 1040 is the place where the Pentagon enters all of our lives, and asks our unthinking cooperation with the idol of nuclear destruction.

I think the teaching of Jesus tells us to render to a nuclear-armed Caesar what that Caesar deserves — tax resistance.”

Reaction in the community was mixed, but leaders of eight other Christian

denominations in Seattle announced their general support for the stand of the

Archbishop… However, they stopped short of endorsing tax resistance, saying

they would “encourage discussion of tax resistance” and offer support to

“those who refuse to pay taxes in protest of the arms race.”

At the time of his speech the Archbishop openly stated that he himself had not yet refused to pay taxes, but that it was troubling his conscience.

Several months later he acted.

In a pastoral letter published in the Seattle archdiocesan newspaper, Hunthausen declared, “After much prayer, thought, and personal struggle, I have decided to withhold 50 percent of my income taxes as a means of protesting our nation’s continuing involvement in the race for nuclear arms supremacy… I am saying by my action that in conscience I cannot support or acquiesce in a nuclear arms buildup which I consider a grave moral evil.”

…However, Pacific Northwest United Methodist Bishop Melvin Talbert said that “while the city’s ecumenical leadership is supportive of Hunthausen, none has indicated that he or she is prepared to follow suit with similar personal acts of tax resistance.”

Freund ends the chapter with a nod to the World Peace Tax Fund Bill idea, taking it at face value and noting that “[c]hurch support is broad.”

After something of a lull in the mid-1960s, in the war tax resistance debate filled the pages of the Church of the Brethren’s Messenger magazine.

(Other Brethren periodicals were silent on the issue that year so far as I could tell.)

In the General Brotherhood Board decided it was time to polish up the peace witness of the Church of the Brethren.

And in preparation for this, it produced “a paper clarifying various stances on the payment of taxes for military uses… [which] cited various options now open and urged efforts to seek a further alternative for those who, because of conscience, oppose supporting war causes.” (source)

This included “urging the government to adopt a provision by which persons conscientiously opposed to paying taxes for military purposes may be granted some alternative, much as conscientious objection is permitted in draft legislation.”

On the matter of alternatives in the payment of federal income tax for war uses, a study committee report was presented and adopted by the General Brotherhood Board.

The report was prompted by various inquiries by Brethren, the most recent from the Pacific Southwest Conference board of administration.

The report enumerated as present options (1) paying the taxes, (2) attaching to the payment a statement of protest on the portion used for war purposes, (3) holding one’s income to a level not subject to taxation, and (4) refusing to pay all taxes or the portion of taxes used militarily, as a witness and a protest.

While not endorsing one alternative above another, the paper, like the proposed revision in the Annual Conference Statement on War, did recommend that efforts be made to secure tax laws permitting a constructive alternative to the payment of income taxes for war.

The board statement also proposed that publicity be given to such steps as the withholding of the federal telephone tax levied in support of the war in Vietnam.

Towards implementation, the board asked the administrative committee of the Brotherhood staff to study the implications of the paper and to bring subsequent proposals in .

One type of question raised by board members in discussion was whether the board itself, in its own operations, might withhold payment on the telephone tax.

A Brethren Peace Fellowship began to congeal, and in one of its early regional meetings: “At several points discussion centered on the possibilities for tax refusal and draft resistance and on proposing an Annual Conference statement on civil disobedience” (source).

The Annual Conference did end up putting out a statement based on the General Brotherhood Board’s recommendation (source):

Another new section deals with taxes for war purposes.

The statement on this point was amended in discussion on the floor of Conference to include a preliminary sentence indicating that although Brethren accept the need for paying taxes for constructive purposes, the church opposes the use of taxes by the government for war purposes and military expenditures.

Specific suggestions dealing with approaches to paying war taxes on the part of members were put in a permissive form, leaving the action to the conscience of the individual.

At the same time, churches and church-related institutions were urged to study the problem of paying taxes for war purposes and even to make a careful review of funds that they might possibly have invested in bonds that would support war.

The approach of civil disobedience is alive in our day.

Knowing that the telephone tax we pay finances the Vietnam war, some individuals do not include money in their payments for the federal tax.

They write across their bills, “No money for war,” or some similar statement.

A new surtax requiring ten percent additional tax money earmarked for Vietnam has been demanded by our government.

Some who believe that war is contrary to the will of God will question themselves, “Is it right to ask our young men to refuse to bear arms even if for some this may mean jail, if we as adults are willing to finance the devastation?”

The edition included an article that discussed the recent progress of the discussion about war tax resistance, and the search for a legal alternative, in the Church of the Brethren:

For the Christian pacifist, where is the conflict of loyalty to God and to the state felt more pervasively than in taxation?

And as the nation’s military expenditures skyrocket, persons of peace persuasion are moved to ask: If alternatives are allowable when it comes to putting one’s time and body on the military line, ought not a similar provision pertain to putting one’s taxes there?

The answer, as called for by a variety of concerned spokesmen, is for a legal, constructive, alternative tax arrangement for persons conscientiously opposed to paying taxes for war and military purposes.

The appeal for such a plan has been heard off and on for a quarter of a century.

For the Church of the Brethren, the matter came more sharply into focus when Annual Conference inserted in its Statement on War a section on taxes for war purposes.

Alternative use: “While the Church of the Brethren recognizes the responsibility of all citizens to pay taxes for the constructive purposes of government, we oppose the use of taxes by the government for war purposes and military expenditures,” the new section declared.

“For those who are conscientiously opposed to paying taxes for war purposes, the church seeks government provision for an alternative use of such money for peaceful, non-military purposes.”

The statement, recognizing that members will differ in their responses, cited four positions on the payment of federal taxes for war purposes which are evident:

to pay taxes willingly.

to pay the taxes but to express a protest to the government.

to refuse to pay all or part of the taxes as a witness and a protest.

to limit voluntarily one’s income or use of taxable services to a low enough level so as not to be subject to taxation.

To implement the concern, the Conference statement urged all members, congregations, institutions, and boards to pursue the matter with serious study and to act “in response to their study, to the leading of conscience, and to their understanding of the Christian faith.”

Dilemma: The appeal for study and action was prompted by concern over the “ever-growing portion” of the federal budget going for military purposes, according to a statement on “Taxes for War Purposes” adopted by the Brethren Service Commission .

The commission paper pointed up the dilemma which this escalation of war funds poses for “peace-minded people and conscientious objectors to war who put their trust in the power of love, non-violence, and international cooperation rather than military might.”

Sparked by a request from the Pacific Southwest Conference Board of Administration for a study of federal income tax alternatives, the Brethren Service study committee asserted that the church’s stance historically has been to oppose participation in war; at the same time it has taught responsible citizenship.

“The Christian should appreciate and support the worthy functions which government performs.

He should willingly obey the state in matters on which he has no contrary moral conviction.

On the other hand, he should be alert to occasions when government neglects or misuses its trust from God.

When he is profoundly convinced that God forbids what the state demands, it is his responsibility to express his convictions.

Such expression may include disobedience of the state,” the commission paper quoted from the Annual Conference statement on “Church, State, and Christian Citizenship.”

Pre-Vietnam: In its own background study the Brethren Service committee noted that while the nonpayment of taxes on conscientious grounds has been a movement of the past 25 years, the concern has “a long and honorable history.

Early Christians refused to pay taxes to Caesar’s pagan temple in Rome; many historic peace church members refused to pay taxes during the French and Indian wars, the Revolutionary War, and the Civil War; strugglers for independence in India, under Gandhi’s influence, refused to pay taxes to the British Empire.”

The study committee recounted a series of efforts which the Brethren Service Commission has made in seeking tax alternatives.

The General Brotherhood Board had urged explorations with government “to the end that an acceptable constructive alternative be provided for all those persons who, by reason of religious training and belief, conscientiously object to the payment of that portion of income taxes going for military defense.”

At Brethren Service’s initiative, representatives of eight peace agencies, each genuinely interested in seeking a suitable tax alternative, met in in Washington, D.C., for a strategy session.

The consensus was that there was little likelihood of the government’s providing a tax alternative until tax protestors and objectors created sufficient administrative difficulties that the government would decide it would be less vexing to provide a tax alternative.

Subsequent efforts by a follow-up committee and other efforts in liaison with the Mennonites and the Friends proved to no avail.

Legislators who had introduced measures calling for tax credits for contributions to the United Nations, which had been looked upon as possibly one alternative designation of tax funds, received little support from the public or from Congress for their proposals.

In a response to a related query the Annual Conference urged Brethren Service to continue efforts to develop an acceptable proposal for an alternative tax arrangement.

According to the study committee, all efforts to date have failed to find or gain sufficient support for a tax law provision or administrative formula that would satisfy Congress, the Bureau of Internal Revenue, and conscientious objectors.

Wider forum: For the next step, the appeal of Annual Conference and of the Brethren Service Commission is for the question on the payment of taxes for war purposes to receive a wider airing among members and congregations.

Copies of two major resource items, “Statement on War” and “Taxes for War Purposes,” were mailed in to pastors and to Witness and Brethren Service chairmen.

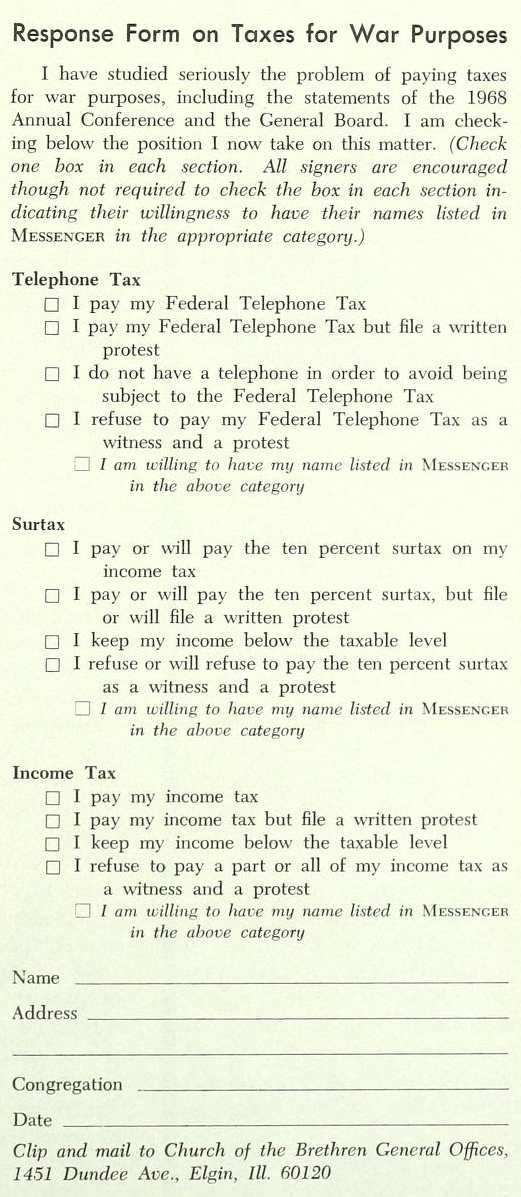

The issue of Messenger [see below] will feature a symposium with spokesmen for each of the four stances on the handling of tax payments.

A response coupon in the same issue will enable readers to report their own stand on the payment of three taxes used heavily for war use, the federal excise tax on telephone service, the recent ten percent surtax on income tax, and the income tax itself.

The names of persons willing to have their positions identified may be published.

Readers also are invited to submit letters to Readers Write to share testimonies and viewpoints on the matter.

Institutions and boards are likewise asked to study the payment of war taxes.

The General Board, through its Administrative Committee is examining the implications at the denominational level.

Ralph E. Smeltzer, who is coordinating the study emphasis, stressed the hope “that individuals, classes, study groups church boards, congregations, and all church institutions and related boards will come to their own thought-out positions.”

Accompanying that article was this sidebar, taken from the statement on “Taxes for War Purposes”:

Paying war taxes

Present positions

Four Positions on the payment of federal taxes for war purposes are evident:

Payment of taxes.

Persons who favor the government’s war and military policies willingly pay their taxes for these purposes.

Other taxpayers judge the constructive functions of government to outweigh the unacceptable activities.

Others feel that responsible citizenship requires the payment of all taxes.

Some who oppose the use of taxes for war feel that the risks and efforts involved in opposing such use of taxes are not worth the negligible results.

Payment of taxes under protest.

Persons who follow this alternative usually file a letter with appropriate government officials protesting the use of any of their tax money for war purposes or military expenditures.

Frequently they urge the government to use their tax money only for peaceful and constructive purposes…

Sometimes such persons ask government leaders to amend the nation’s tax laws, especially the income tax law, to provide an alternative opportunity… to designate the use of their tax dollars for peaceful and constructive purposes either through United States government functions or United Nations operations.

Limitation of income or use of service to nontaxable level.

Some persons are led by their consciences to limit voluntarily their income to such a low level that it will not be subject to federal taxation for war purposes.

Likewise they may not install a telephone or use other services which are subject to similar federal taxation.

They may endeavor to avoid participating in all those aspects of economic life which contribute to or support war and military operations…

Nonpayment of taxes or portions thereof.

Persons who follow this alternative refuse to pay all or part of the taxes asked by the government.

They engage in this form of civil disobedience because they conscientiously object to the use of their money by the government for war or military purposes and because they want to make a more vigorous protest against the government’s war policy and military policy.

Sometimes these persons contribute an equal amount to the United Nations or a private peace agency as a positive witness to their position.

The Federal Income Tax and the Federal Telephone Tax are presently the taxes most frequently refused by conscientious objectors.

Refusal to pay such taxes might possibly be considered a violation of Internal Revenue Code, Section 7203, which would be a misdemeanor subject to a fine up to $10,000 and jail up to one year.

However, the experiences of conscientious objectors to federal taxes for war purposes during the past several years indicate that the government is not interested in pressing possible criminal charges but in trying to collect the taxes here or there with interest.

The Internal Revenue Service usually attaches the salary or bank account of the nonpayer and collects the tax plus six percent interest from the date the tax was due.

The nonpayment of the Federal Income Tax or portion thereof is carried out by those who have payment control over all or part of their income tax return and who refuses to pay all or a portion of the money owed.

The nonpayment of the Federal Telephone Tax or a portion thereof is carried out by refusing to pay that part of one's monthly telephone bill and sending with each remittance a written explanation of why that portion is not included.

Telephone companies have indicated that refusal to pay this tax will not result in interruption of telephone service.

Telephone companies turn over to the Internal Revenue Sendee the responsibility for collecting such unpaid taxes.

The phone company treats refusal as a matter between the customer and the government.

Some companies continue to carry the refused tax on the telephone bill as an “unpaid balance,” others do not.

The issue asked four authors to each give his perspective on the war tax issue (“Debaters of the war tax question include Russell V. Bollinger, dean of students at Manchester College in Indiana; Charles E. Zunkel, pastor of the Crest Manor church, South Bend, Indiana; David B. Rittenhouse, pastor of several congregations in West Virginia; and William Faw, pastor of the Douglas Park church in Chicago”) and included a survey readers could fill out and send in to the Messenger in which they could say which action they were taking:

In recent actions of Annual Conference and of the General Board, members of the church have been urged to study seriously the problem of paying taxes used for war purposes and to act in response to their study.

The church recognizes that its members will believe and act differently in regard to the payment of taxes when a significant percentage goes for war purposes and military expenditures.

Four major positions on the payment of federal taxes for war purposes are evident:

Some will pay the taxes willingly; some will pay the taxes but express a protest to the government; some will voluntarily limit their incomes or use of taxable services to a low enough level so that they are not subject to federal taxation; and some will refuse to pay all or part of the taxes as a witness and a protest.

As an aid to discussion and action Messenger has invited four spokesmen to comment on these alternative positions.

There is also a response form that may be used individually or by groups to indicate how readers stand on this controversial topic. ―Editor

Why I Pay Taxes Used for War Purposes

by Russell V. Bollinger

Though I write in defense of the first position, namely, that the Christian ought to pay his taxes willingly, it should be clear that I have no objection to the second, which adds only some form of verbal or written protest against the defense budget.

Those who take the third position seem to me to be evading the issue.

They resolve their personal dilemma by abdicating their responsibility to society.

The fourth position constitutes an abdication of personal responsibility in an attempt to correct a social evil.

It should be very clear that I share and have always supported the Brethren peace position, which can be amply documented from the New Testament.

Under debate here are particular forms of protest or obstruction against war.

Such forms of protest, like all actions of Christians and of the church, must be tested against what Jesus both said and did.

In order to identify and to underscore some basic considerations affecting this discussion, it seems to me necessary to examine an assumption on which many such actions as tax withholding have been proposed and some implemented.

Considerable promotion has been given, for example, to the slogan, “Government Is the Christian’s Business.”

I have always objected strenuously to this concept, especially to its adoption as a slogan.

At best, the statement is misleading; at its worst it grossly distorts the Christian’s concept of his central task.

Government is the citizen’s business, whether he be Christian, Jew, or pagan.

To be sure, the Christian’s citizenship will be exercised in the light of his faith — but never as the central or major focus of his activity as a Christian.

He has accepted an enormously more urgent and significant “business” — to order his own life after Jesus’ teaching and example and to strive to win others to the same commitment.

Whatever the Christian’s proper role in government, it must always be secondary among his priorities.

Otherwise, it must seem strange that Jesus and Paul so clearly advised subjection to civil government, at least in all ordinary circumstances, and do not appear to have spent time or energy attempting to reform or even influence a very corrupt government at Rome.

I propose, under the foregoing assumptions, two considerations which for me justify willing payment of taxes, even if portions of the tax budget go for objectionable purposes.

First, it is a matter of reasonable doubt whether any government could long operate under a system by which tax paying is made subject to the range of possible “conscientious” objections to selected government activities.

Let us suppose that such groups as the Amish were to withhold that portion of their taxes which goes to support all education beyond the common school.

They declare opposition to secondary and higher education on grounds of conscience.

Suppose all Christian Scientists were to withhold a percentage of their taxes allotted to medical research and facilities.

Suppose we Brethren were to withhold taxes because welfare funds are sometimes so administered as to endanger or destroy normal family life or because Department of Agriculture funds are paid to large-scale farmers for nonproduction of food and fiber.

These and many more may with equal logic be considered matters of conscientious objection.

Happily, under our system of government, we have ample opportunity to present and defend other points of view, but the democratic social theory neither contemplates nor condones obstructionism.

There is reason to question whether Brethren leaders can support tax withholding with integrity while at the same time they discourage “designated giving” to the Brotherhood budget.

If churchmen be urged to support the total church budget, without discrimination, but citizens be exhorted to support only such governmental budget items as they can approve in good conscience, we may ask whether tax withholding is supported in principle or only opportunistically, as a strategy.

It is surely axiomatic that all forms of human association are possible only because of some surrender of personal freedoms and preferences.

Since in our society we have adequate legal, educational, and constitutional avenues for expressing our views to government, to withhold taxes for what we happen to disapprove (and who can differentiate between “conscientious,” philosophical, emotional, and mystical disapproval?) comes perilously close to asking for the benefits of government while shirking its responsibilities.

In short, the proposal to withhold all or a part of one’s tax obligations for reasons of individual or corporate conscience must be conceded to contribute to a fragmentation of society that tends toward anarchy.

Second, tax withholding on whatever grounds with the purpose of preventing selected government activity is essentially a method of force which Brethren in particular should reject.

All attempts to change the behavior, attitudes, or values of mature, responsible persons by force are degrading and destructive of personhood.

There seems to be no point in arguing that the purpose of such withholding is simply a symbolic form of protest.

Kant’s categorical imperative in ethics tests a proposed act in terms of whether it could be universalized.

Since tax withholding quite obviously cannot be universalized without destroying government, it clearly suffers by such an ethical criterion.

No thoughtful observer of the contemporary scene can deny a trend toward the substitution of force for persuasion, of compulsion for rational debate, to bring about social change.

The civil rights movement, the student protests, the Poor Peoples’ Campaign in some of its expressions and slogans are illustrations.

The church seems in imminent danger of succumbing to this trend, although it is both unworthy and out of character for Christians.

The ultimate indictment of the method of force is of course that it cannot succeed except in appearance.

An attack on the war system ought to proceed by using available means to demonstrate its futility, its ineffectiveness, and its immorality — none of which ends tax withholding can serve.

At most it seems a crude and primitive way of attracting attention to one’s cause.

From time to time the Christian, as a citizen, may properly make representation to government concerning his views, his desires, and his concerns.

Our impatience to reconstruct the world after our own particular blueprint must not lead us into betraying noble ends by the use of unworthy means.

Why I Pay the War Tax Under Protest

by Charles E. Zunkel

In order to be consistent the conscientious objector to war must face the whole range of his involvement with war.

In addition to participation in the military is certainly his concern for the use of his tax money for military purposes.

This is especially true now that so much of one’s income tax is being used for war.

When my wife and I came clearly to this conviction in and decided that we must do something about it, I wrote the Department of Internal Revenue, sharing copies of my letter with the President and declaring our concern and our intention to refuse payment of the percentage of our income tax which would be used for war [see ♇ 31 May 2020].

I made it quite clear that we were not unwilling to pay the tax, but we were objecting to its being used for war.

We wanted it used for constructive, peaceful purposes.

I received a very courteous reply, reiterating my words, but advising us and urging us to pay the tax.

I then wrote, asking if we could pay this percentage for the United Nations, Food for Relief, or Peace Corps, programs of the federal government which we considered peaceful and worthy.

Internal Revenue replied that it was not in their province to disperse the funds, only to collect them.

In the meantime, I conferred with one who had refused to pay the income tax and learned that, if we did not pay, the tax would be collected by taking it from our bank or savings account or by confiscation and selling personal property.

An additional penalty of five percent would be imposed.

We decided we did not want to provide the extra five percent for war to carry out our refusal, when the tax would eventually be collected anyway.

Instead, we decided to write two checks each time, one designated for “peaceful purposes: United Nations, Food for Relief, Peace Corps,” in the percentage amount of the federal taxes for war.

The other for the remaining percentage amount we marked “undesignated.”

Since the federal government has the power to use the tax money as it wishes, not as we may designate, the checks were cashed and no comment was or ever has been given.

Periodically to accompany the checks I have written letters voicing our concern and protest to the President and the Secretary of State.

While this method does not keep our money from supporting war, it seems to us the only viable way for us to protest, since we earn enough to have to pay the tax and since we do not want the added five percent penalty to provide more funds for war.

If enough persons or families used this method and the process became publicized, it would be an educational program which might build conscience in others and eventually lead to the provision for tax exemption of the sort we now have for military service.

Legislative bills have been prepared for this purpose but have not been introduced because the lack of public support would assure their defeat.

In the meantime, we would hope that the Brethren, Mennonites, Friends, and others concerned might send to the President a delegation asking for tax alternatives, as was done to secure an alternative to military service.

Regarding the surtax or the telephone excise tax, we believe that, because these are small enough amounts of one’s total tax and that they are clearly all for war purposes, they can and should be refused, even though the five percent penalty will be added and they will be collected.

Education could win sufficient popular support for objectors to war tax payment and make possible the passage of legislation that will provide alternatives for the worthy use of tax money which would otherwise be spent to support war.

Keep Income Below the Taxable Level

by David Rittenhouse

While serving in BVS 1-W Program, Merle Grouse, a fellow BVSer, and I were traveling by train from Turkey to Germany.

During an all-night ride through Yugoslavia, we talked with a young Yugoslavian who said that he had been taught that capitalism could not exist without war.

In all innocence we strongly disagreed.

During , the Church of the Brethren sponsored a work camp in Altoona, Pennsylvania, for the unemployed after the railroad shops changed from steam to diesel.

There, at the end of a hot summer day, a group of men sat on the steps talking about their hope for a job.

One remarked, “I guess we will have to wait for another war before we get work.”

So it is that with the event of the Vietnam War and the resulting defense contracts, we are forced to admit that which some had suspected.

Though I do not believe that this war economy is the inevitable result of capitalism, the war is definitely with us, even if not by design.

It is high time that vocal Brethren pacifists be called to attention by our consciences about our direct involvement in war through taxes.

It has been a natural temptation, when Christian ethics are frustrated by the real world in which we live, to turn inward in an attempt at individual purification and character refinement as a goal that is within reach.

I do not in any sense want to encourage this type of denial of the implications of Christ’s teachings, for we must accept the fact that we cannot disassociate ourselves from the economy in which we live.

In all our expressions of protest there must still be the humble recognition that the curse of Habakkuk is there: “Woe unto him who builds a city on blood.”

But there are ways in which individual citizens can exercise freedom of belief as persons.

Living on a limited income is one of these forms of witness.

Voluntarily limiting one’s income requires us to reevaluate our standard of values.

We are encouraged to find satisfaction in meaningful activity instead of in possession of things.

It is in keeping with the Christian concept that persons and beliefs are more important than property.

It is related to the spirit of the verse in Hebrews 10:34, “You joyfully accepted the plundering of your property, since you know that you yourselves had a better possession and an abiding one.”

Our family includes my wife and me, four children, and many guests.

For seven years our income has been below the taxable level.

This does not mean to us that we are pure and uninvolved in a war economy.

Rather it has freed us to pastor six country churches that could not compete on a minimum salary for pastoral leadership.

This, then, is the exciting part of the idea of limiting one’s income.

It frees Brethren pastors, teachers, doctors, builders to go to the places of greatest need, regardless of the salary offered.

Consider Partial or Total Tax Refusal

by William Faw

“Render unto Caesar the things that are Caesar’s and unto God the things that are God’s.” What do we owe Caesar? Many Christians would say that we owe him complete obedience in all things: We must kill for him, pay for his wars, even exterminate a people for him as Hitler commanded and as we may be doing in Vietnam.

But Brethien have said “No” to that type of obedience.

We have said that we will render unto Caesar constructive citizenship and support for constructive programs.

We have insisted, though, that Christ’s commandment that we love our enemies forbids us to kill in Caesar’s name.

The early Christian church and the Church of the Brethren were born in civil disobedience, saying with Peter to the government, “We must obey God rather than men” (Acts 5:29).

Paul, who in Romans 13 calls us to “be subject to the governing authorities,” spent much time in jail because of civil disobedience when the command of Caesar conflicted with the command of God.

Many of us have refused to participate in military service but have unflinchingly paid taxes to support that same war machine, seemingly unaware of the contradiction involved.

Where your treasure is, there will be your heart also!

Our pocketbooks support the wars that our bodies shun!

What this amounts to is that we are paying for others to kill for us.

If God has not given us authority to kill, how can we give Caesar the authority to kill in our name and with our money?

We have often thought that the payment of taxes is a morally neutral issue.

How can it be that when our taxes are financing the extermination of the Vietnamese people?

Once you decide to object conscientiously to tax involvement in war, you must make many secondary moral decisions.

You might elect to pay your taxes but send a letter of protest which states your preference to pay a portion to the United Nations if such an alternative should become available.

It is possible that enough protest letters could strengthen congressional attempts to offer such an alternative tax-payment provision.

Or you might decide to refuse payment of taxes until such an alternative should become available, just as you might refuse to enter military service even if there were no legal alternatives to it.

If you refuse payment you must decide whether to withhold the percentage that would go into military use (some say eighty percent) or to withhold the total amount.

If you choose the first path you might reason that you are paying for constructive programs of government while refusing to support the military.

If you decide on total withholding you might give one or both of the following reasons:

One, since you cannot designate where a paid portion would go, eighty percent of what you pay still goes to the military; and two, a goal of peacemaking may be to hold back eighty percent of the government’s total revenue so that it would have to eliminate its military expenditures, in which case the total withholding of the few tax refusers is a bigger step than their partial withholding.

If you are willing to consider partial or total tax refusal, you will need to think through the mechanics and consequences of it.

If you are totally or partially “self employed” (a minister, small businessman, farmer, babysitter, public speaker) and thus have control over all or a portion of your income tax withholding, the procedure might be to withhold all or part of your quarterly estimate payments or listing the accumulated “other income” on your tax form and refuse payment on that.

If all your taxes are withheld by your employer you can at least send a letter of protest to the government with your income tax forms (send letters to the President and to congressmen as well as to IRS) and refuse to pay the ten percent federal excise “war tax” on telephone service.

In fact, refusing on both taxes should be considered if that is possible.

If the additional income taxes recently accepted to finance the Vietnam conflict had been passed as a surtax, each of us would have had the opportunity to pay or refuse to pay it.

Instead, it will be withheld by employers in the same way as normal income tax.

The Internal Revenue Code lists several categories of “tax delinquency” with consequences ranging from collecting, with six percent per annum interest, from bank accounts, salary, or, rarely, the seizure of personal property, to a fine up to $10,000 and jail up to one year.

I and others have been assured by IRS agents that there is little chance that the federal government will prosecute us until they have collected the billions of dollars in crime syndicate tax fraud.

Regarding the telephone tax, “In no case so far has phone service been discontinued because the refusal is, according to law, a matter between the refuser and the government” (War Resisters League pamphlet, “Resist Vietnam War Taxes”).

Telephone tax collection has followed the income tax procedure, with no prosecutions recorded to date.

The consequences may be negligible, but the risk must be understood and considered.

You must decide within the framework of your beliefs, of the limits of your control over your taxes, and of the personal and social risks involved.

There is one thing you cannot escape: the moral implications of financing mass murder!

The article was accompanied by a survey form for readers to fill out and return to the Messenger:

Floyd Irvin, an early Brethren adopter of war tax resistance, explained the evolution of his resistance tactics in the issue:

I have always felt that the payment of taxes for the support of our government’s killing agency — the military — is wrong.

As a Christian I am exhorted to love my neighbors and my enemies, not to kill them, and to overcome evil with good.

I am mindful of the command, “Render to Caesar the things that are Caesar’s.”

But I also consider that in a democracy the citizens are the rulers — the Caesars.

So in this nation I, as a sovereign citizen, have a tremendous responsibility for the actions of my nation.

As a sovereign citizen and as a Christian I am obligated to render unto God loyalty in expressing love for my neighbor and for my enemy.

And as a co-ruler with my fellow citizens, I must lead my nation to do the same.

I cannot help my nation kill people who are God’s children.

In a democracy I express my sovereign rights and obligations not only by my vote but also sometimes by protest.

My protest, even if it is expressed by non-cooperation, need not be, and should not be, termed “force” in the same sense in which destroys life.

Withholding taxes from war financing is noncooperation in that which destroys God’s highest creation, man.

Peter, who exhorted us to be subject to human institutions, did not always obey government orders.

To be loyal to the laws of God is not anarchy.

Our own government, with allies, condemned and punished German citizens for being loyal to their government’s orders when they were wrong.

Withholding taxes to be used for killing my fellowman is a means of expressing my moral disapproval of an immoral act.

This may be considered by some to be wrong.

But becoming involved in killing is also wrong.

Which is the greater wrong?

And how best express my disapproval is the question to consider.

In I withheld seventy-five percent of my income taxes — that being the approximate amount of the federal budget used for military purposes.

I gave the amount withheld to UNICEF, an agency of the United Nations.

By this donation I expressed my social responsibility.

The publicity that followed was a testimony for peace.

But it led to my removal from a responsible position and the office of superintendent of the church school of a leading congregation in our town.

I also found that the government can, if it will, collect all the taxes due, in one way or another.

They got my taxes by a devious method.

My business was such that had the government seized a truck or other property essential to my business, it would have caused considerable inconvenience to many of my 1,500 customers.

So, considering all, for some years I paid my taxes under protest.

I finally decided that for me the best way to avoid paying for military operations was to reduce my income.

So I retired early.

I have most of my investments in real estate.

If I have a prospective sale for a piece of property, the profit of which would put me in an income tax paying bracket, I deed that property to a church or to a charity institution and let that organization deed it to the purchaser.

So I receive no profit.

Or I may get a contract for many small payments over a period of years, making a low income each year.

I use all my exemptions and live on my exempted income.

The above plan works satisfactorily for me.

In , Brethren continued to resist war taxes, and a new “777 Club” campaign attempted to nudge non-resisters into a small, baby-steps form of war tax resistance.

The issue of Messenger covered the legal battle of war tax resister Bruce Chrisman:

“Our hearts go with our treasure to war when we must pay war taxes,” said Bill Faw of Reba Place Fellowship.

He was speaking at a worship service in support of Bruce Chrisman and his appeal for the right to refuse to pay war taxes.

Chrisman appeared before the US Court of Appeals for the Seventh Circuit in Chicago in .

He was appealing his conviction for failing to file a proper income tax return.

Bruce and his wife, Maryanne, farm near Ava, Ill.

The argument against Chrisman (and others in similar cases) is that he broke the law when he failed to file the proper income tax return.

Chrisman believes that such an argument misses the point — that his freedom of religion is violated by the court’s insistence that he pay even those taxes that go towards war.

Chrisman’s attorney, A. Jeffrey Weiss, argued that the first amendment of the Constitution prohibits laws that interfere with the “free exercise” of religion.

Weiss contended that the US government violates this clause by requiring full payment of taxes from citizens whose faith demands that they not pay for war.

The General Conference Mennonite Church (GCMC) filed an amicus curiae (friend of the court) brief in Chrisman’s behalf.

The brief gave historical precedents for withholding war taxes.

It also stated the GCMC officially supports “Christian pacifists who refuse to pay taxes to be used for military purposes.”

Although Chrisman is not a Mennonite, he is closely associated with the GCMC.

After his conviction, Chrisman expected to receive a two-year prison sentence.

But , when he stood before the judge for sentencing, he explained that he didn’t mind paying taxes.

In fact, he said, he would not object to paying more than his share of taxes if those taxes relieved human suffering.

The judge gave him the unusual sentence of one year’s service in Mennonite Voluntary Service.

He spent the year doing peace work and visiting prisons.

He and Maryanne plan to serve another year.

Chrisman does not expect word on his appeal before since a written ruling from the court usually requires between three and six months.

If his conviction is upheld, Chrisman intends to carry his appeal further.

U.S. military support of the government of El Salvador became another reason to refuse taxes, when in the issue Jorge Lara-Braud was quoted addressing Church of the Brethren higher-ups (source):

“To what extent,” he asked, “will we US Christians be used to finance the repression of those who are seeking the Kingdom of God?” He urged tax resistance as one way of resolving the agony of giving the government money to kill other Christians.

That issue also reported on a new “Brethren Discipleship Group” and noted, somewhat vaguely, that “They also refuse to pay ‘willingly those taxes which support war’ ” (source).

The Annual Conference reaffirmed its support for the World Peace Tax Fund legislation (source), but:

An amendment urging refusal to pay military-related taxes was ruled out of order, although recognized as a related issue.

Concern was raised that the WPTF represented an “easier way to be Christian” than direct refusal to pay taxes.

But war tax resistance was still a going concern.

From the issue:

Three General Board staff families have taken a stand against war by withholding part of their federal income taxes.

Chuck and Shirley Boyer, Ralph and Mary Cline Detrick, and Miller and Phyllis Davis protested the use of their tax dollars for defense spending by giving the amount withheld to other organizations.

Miller Davis, director of the New Windsor Service Center, and Phyllis withheld $100, which they sent to the General Board.

Peace consultant Chuck Boyer said that he and his wife, Shirley, had periodically withheld income taxes .

, they and the Detricks, of life cycle ministries, each gave $50 to the local school board to demonstrate their support of public non-military programs.

“We don’t mind paying taxes,” says Mary Detrick.

“That’s why we chose to pay the same amount to a public institution.

It feels like a little bit of leaning toward justice.”

Adds Ralph Detrick: “It’s a symbolic protest of how the government spends our money.

We choose to make a nuisance.”

Like the Detricks, Boyer acknowledges that tax resistance currently is little more than a “nuisance” to the federal government.

But he points out that such a protest could have an impact “if 20,000 or 30,000 Christians did involve themselves.”

Boyer and the Detricks stress that their personal decisions are not intended to tell others what to do.

Rather, they hope to raise questions and to give support to other Brethren families who have chosen to take the same stand.

“It’s not the kind of thing I like to do.

People probably think I’m a real radical,” says Boyer.

“It’s a struggle within me to find what it means to be faithful,” he concludes, “but something has to be done, and this is it for now.”

And there was this attempt to get some more-timid Brethren to take symbolic baby-steps into tax resistance, from :

Jesus does not tell us to give Caesar everything he asks for.

Nor does he specify what is Caesar’s and what is God’s.

The 777 Club is one way to resist war taxes and maintain one’s Christian integrity.

by Karen Zimmerman and Bill Puffenberger

What started out as a sharing experience for a few Sundays at the Eiizabethtown Church of the Brethren expanded into a class lasting 12 weeks.

The Topic? “War Tax Resistance.”

After a brief initial discussion of the topic we began an in-depth study of several key biblical passages.

This led to other experiences — a visit with Paul and Loretta Leatherman (originators of a 777 plan of war tax resistance);

a visit to the Mennonite Central Committee Headquarters to share with a group of Mennonites who have been practicing various types of war tax resistance; the sponsorship of a Sunday morning mini-workshop in the local congregation; and a Sunday morning dialog with our local congressional representative, Robert Walker.

As a result of these experiences, some members of the class have offered to share their time and ideas on this issue with other churches in Atlantic Northeast District.

As newcomers to the field of war resistance, it was rewarding to have the opportunity to talk with the Leathermans — 10-year veterans.

Over the years they have tried various methods to withhold the portion of their taxes that are used for war.

Eventually, the Internal Revenue Service got its money, but it was not an easy process and it provided the Leathermans an opportunity to witness to their local IRS agent, their bank representative, their employers, and others about their opposition to war and their necessity for funding it.

In an effort to have more people join them and hopefully to attract the attention of law-makers in Washington, the Leathermans initiated a 777 plan.

They propose withholding a symbolic amount of $7.77 (or some variable thereof) as a war tax deduction.

Because present US tax laws do not provide for this kind of deduction, many members of the class used the 1040 long form and wrote in the words “War Tax Credit” on line 46.

A brief letter of explanation was then attached to the form.

In addition, more detailed letters explaining our views were sent to our local congress members and to the President.

We recognize that this is indeed a symbolic protest since in most cases the government has already taken the taxes or will take unpaid taxes from our future paychecks.

Even though the taxes will eventually be collected, we think it is a matter of integrity to say by our actions, words, and letters how we feel about this issue.

The number 777 was chosen for its biblical significance and symbolism.

Seven is the biblical symbol for perfection.

Seven is the numerical framework for God’s Creation, especially the Sabbath.

Jesus tells us to forgive “seventy times seven.”

To us Eiizabethtown tax resisters the number had even greater significance — our church address is 777 Mount Joy Street.

We studied in detail two biblical references on taxes: Mark 12:13–17 and Romans 13:1–7.

Our study convinced us that we cannot assume that the law of the land is the sole judge of our moral decisions.

We must see obedience to government in the context of the command to live in peace with all persons.

In light of the increasing militarism of the present administration in Washington it is particularly urgent that Brethren consider the issue of war tax resistance.

Can we be satisfied that conscientious objection by only our 18 to 26-year-old youth is an adequate stance to maintain?

What is to be required of us who are outside this age classification?

In a world that is warring with a technology fueled more by money than by personnel, most of us are relatively unaffected by the draft.

While our bodies are not being used, our dollars are being conscripted for war purposes.

What kind of integrity is this?

How can we conscientiously pray for peace and at the same time pay for war?

We urge Brethren to take another look at Christ’s teachings as well as our denomination’s peace position.

We feel we have a convincing argument that the current military build-up is diametrically opposed to God’s law to love one another.

We are hopeful other Brethren join with us who are taking this symbolic war tax deduction of $7.77 (or $77.77 or $777.77) as a way of maintaining our Christian integrity and at the same time letting our government know that there are some people out there who oppose the current excessive military build-up.

We are not in principle opposed to the payment of taxes (which support many worthwhile endeavors).

We are opposed only to the payment of taxes for war-like means (which we see as destructive and unchristian).

We all have a choice: We can quietly pay our war taxes and support preparations for war or we can noisily refuse to pay (even a symbolic amount) and work untiringly for the cause of peace.

We members of the 777 Club probably cannot arrest the current military build-up, but we will have at least set the record straight that we cannot mouth the words of peace and at the same time willingly pay into an ever-growing war chest.

We seek to avoid a kind of Christian schizophrenia as we refuse to pay for that which is destructively unchristian.

The Bible Monitor never flinched from its strict if somewhat blinkered interpretation of render-unto-Caesar.

From “Serving God and Caesar,” the lead article in the issue:

The Christian’s duty includes paying his taxes.

Even Jesus paid his tribute money.

The money of our land is very clearly marked as the legal tender of the land, therefore it should be rendered back to the government.

Although we may not approve of all uses made of our tax money, we dare not be selective in what we pay.

We do indirectly receive a benefit, at least in the eye of the world, from our taxes.

Again in , only the Messenger (of those Brethren periodicals I reviewed) covered war tax resistance, but they did so often.

In a Brethren church in Indiana hosted a war tax resistance workshop:

A concern for active Christian peacemaking was the motivation for the gathering of over 50 people from at least seven religious traditions .

The event, sponsored by the Peace Action Committee of the Northern Indiana District and held at Prince of Peace Church of the Brethren, was a war tax resistance workshop led by Dale Aukerman of the Brethren Peace Fellowship.

The two main body presentations dealt with “our peacemaking and the end of the world,” and “war tax resistance as seen from the perspective of Matthew 18:15–17.” Participants were called to “claim the sovereignty of God and take our Christian discipleship seriously.

The key to our peace witness is to strive to be faithful to God.”

The workshop is one of a growing number being held throughout Brethren churches, often in conjunction with other denominations.

The groups explore nuts-and-bolts alternatives of withholding taxes and support each other in maintaining the witness under Internal Revenue Service pressure, as well as sharing the vision of peace inherent in faithfulness to God.

“Participants in the war tax resistance workshop led by Dale Aukerman (lower left corner) explore peacemaking theology and alternatives of withholding taxes.”

Kevin Zimmerman shared the thinking that went into his war tax resistance in the issue of Messenger (source).

Excerpt:

Although my body is not being conscripted to support war, my tax money is, and at this point in history which do the military powers need more?

My money!

As Dale Brown notes, “If it becomes possible through automated warfare to kill and destroy with unmanned aircraft and minimal personnel, then the witness of withholding economic support may become an issue of even greater importance to the conscientious Christian peacemaker.”

I am not opposed to supporting my government or paying taxes to my government.

But I believe when our government goes directly against Christ’s teachings we are to follow Christ.

Peter and the apostles found themselves forced to resort to civil disobedience in an attempt to fulfill Christ’s teachings and, when arrested, responded, “We must serve God rather than men” (Acts 5:29).

I would like to see Congress pass the bill supporting the World Peace Tax Fund.

That portion of my taxes supporting our military could instead be put into this fund to be used for such peaceful purposes as United Nations activities, research into nonviolent solutions to international conflicts, disarmaments efforts, and international education and welfare.

In this way I can support my government as well as the peaceful lifestyle demonstrated by Christ.

Christianity has never been and will never be a spectator sport.

We are commanded to go out and spread the word by helping our neighbors and sharing their burdens, but also by letting our government know too, by letter or by civil disobedience, when they have broken God’s laws.

By sharing my feelings, I hope others will seriously and prayerfully consider how their tax money is being spent, their role in our military machine, and Christ’s teachings to “love our enemies.”

The issue covered the Supreme Court ruling against Old Order Amish who wanted their conscientious objection to the social security system allowed by law (source).

Excerpt:

When the case reached the Supreme Court, Chief Justice Warren E. Burger agreed with the IRS, saying, “The tax system could not function if denominations were allowed to challenge tax systems because tax payments were spent in a man-er that violates their religious belief.”

Such an attitude could seriously hamper efforts to establish an alternate peace fund into which conscientious objectors could channel taxes that now fund military budgets.

That issue also announced the formation of a “Tax Resister’s Penalty Fund” (still going strong today as the War Tax Resisters Penalty Fund):

Dave Leiter, of North Manchester, Ind., is heading up a network of people interested in distributing the burden of penalties or interest levied against military tax resisters.

An example of such support would be for 200 people to share a $500 penalty by each contributing $2.50. If interested, write the Tax Resister’s Penalty Fund…

Another article in the same issue, on possible responses to the nuclear arms race (source), recommended war tax resistance as one of the possibilities:

Refuse to pay some of your Federal income taxes as a witness to your faith.

If you’re scared, try a small amount like $7.77. If that’s too scary, at least send a letter describing the difficulty of praying for peace and paying for war.

Mike and Carol Zuercher Stern shared their war tax resistance journey in a letter-to-the-editor in the issue (source):

The way a person spends money is an indicator of one’s personal priorities.

In the past year (perhaps more clearly than any other time in recent history) our country has corporately demonstrated what it considers to be most important by how it spends money.

Top priority is military superiority over all other nations — bigger and better bombs, submarines, missiles, and napalm.

As Christians and conscientious objectors to war, we cannot accept this national priority as though it were our own.

We oppose the building of weapons whose ultimate use means the shedding of human blood.

Each April 15 we are reminded of our personal participation in funding a national priority which we believe stands in direct contradiction to our Christian faith.

Our response each year has been to file all the legally required tax forms while witnessing by a variety of symbolic protests against the use of tax dollars for weapons of war.

This year we felt compelled by conscience to refuse to pay the entire amount of taxes which had not been withheld already from our salaries.

This $438, less than 25 percent of our total tax obligation for the year, will be given instead to charitable organizations.

In doing so, we affirm our commitment to the gospel of love, healing, and reconciliation.

That issue also reported on Ralph Dull’s theatric tax resistance protest:

Ralph Dull, of the Brookville, Ohio, Church of the Brethren, has refused to pay a portion of his income taxes each year as a protest against military spending.

This year he chose a new way to draw attention to the issue.

On he pulled up in front of the Federal Building in downtown Dayton to offer the Internal Revenue Service 325 bushels of corn in lieu of taxes owed.

The action was “to dramatize and emphasize the need for the Federal government to turn its priorities around and support constructive people programs,” Dull said, “rather than use our resources for an arms race that is murderous and suicidal.”

He asked the IRS to sign a statement acknowledging the value of the grain and guaranteeing that its value would be used only for non-military purposes.

When the IRS refused to sign.

Dull sold the corn to a local elevator.

A check for about $777 was made out to Church World Service and given to the National Farmers Organization’s Food for Poland project.

“Apart from the religious aspect of this issue,” said Dull, “what this symbolic action lifts up for consideration is human decency.

It is vulgar to squander material and human resources while there is so much opportunity to relieve existing human misery.”

a classified ad from the issue

An article from the issue, focused on resistance to draft registration, noted in passing that “The United Methodist Church… said [in ], ‘We… support all those who conscienttiously object to preparation in any specific war or all wars; to cooperation with military conscription; or to the payment of taxes for military purposes; and we ask that they be granted legal recognition.”

A report on the Annual Conference in that same issue noted that war tax resistance was a last-minute addition to the agenda:

Brethren war protesters who decide to withhold tax money going to war purposes may find their employers less than enchanted with the idea.

Brethren employers may be sympathetic to the idea but are up against federal regulations to withhold taxes.

So what’s a body (such as Annual Conference) to do?

Acting on a late-breaking query from Northern Indiana District, Annual Conference elected a committee of five to study the problem and report in .

The committee is charged to come up with helpful guidance for church institutions so they can adequately respond to their employees employees who wish to withhold their “war taxes.”

The study was approved, despite at least one speaker grousing that he hadn’t “heard one good thing about the US government this week.”

Chances are he was correct.

The Annual Conference of the Church of the Brethren will not be remembered as an exercise in flag-waving patriotism.

For the majority of the delegates to Wichita, judging by the voting record, patriotism was best evinced in responsibly and prayerfully calling one’s government to account in the areas of justice and peace.

That committee would include Dale W. Brown, William R. Faw, Ramona Smith Moore, Phillip C. Stone, and Marty Smeltzer West.

In the issue, Ingred Rogers reported on a war tax resisters’ alternative fund that her Brethren church established:

The Manchester Church of the Brethren has established a “Fund for Life” as an expression of support for those who feel moved to refuse payment of war taxes.

This was a significant step in a long process of soul-searching and consciousness-raising.

The process began in when several members formed a tax-concerned group.

Driven by the conviction that to contemplate nuclear holocaust is sin against God and humanity, we came together to discuss how to express our conscientious objection to war taxes.

Careful reading of the Bible convinced us that the Scriptures give no single, absolute statement about payment of taxes.

But we are indeed called to obey God above all, and trusting in weapons of mass destruction is clearly idolatrous.

From the beginning, we saw our action as an effort to maintain faithfully the Brethren peace testimony.

It became increasingly important to us to allow the church to make a witness on behalf of tax resisters.

Our denomination as a whole had already committed itself to recognition of war-tax resistance as a form of conscientious objection.

Now it was a matter of asking for support from the local congregation that had nurtured us and had had a vital influence on tiie formation of our peace position.

After the first church board discussion on the issue, the tax group prepared a proposal for a Fund for Life.

The original draft provided that resisters would deposit in the fund the money withheld from taxes.

Money unclaimed by the Internal Revenue Service was to become the property of the Manchester church as a completed gift by the original depositor and used for peace work.

As in an escrow account, money up to the amount deposited could be returned to the individual if the IRS should claim the sum.

The church board raised two objections.

If the money can be returned in full to the original depositor once the IRS demands it, where is the witness, the risk, the sacrifice?

If the church holds money owed to the government, might the whole congregation legally be implicated?

The board decided to bring the proposal to the next council meeting for discussion, and to delay a final vote for another six months to allow the congregation to reflect upon the issue of war-tax resistance.

The resulting education program was thorough and rewarding.

As expected, we met with disagreement and heated debate.

A second draft suggested that the money should be a completed gift from the beginning without strings attached.

Also, money deposited would not necessarily have to be withheld from taxes; anyone could contribute as an expression of support.

The tax group found this second draft more true in some ways to the original intent.

Both drafts were presented in Sunday school classes.

After three more modifications, the group settled on this wording:

The congregation leaves the withholding of war taxes to the individual conscience of each member or friend.

Any member or friend of the Manchester Church of the Brethren may contribute money to the Fund for Life.

The income from said gifts and the gifts themselves shall be used by the church for activities that are expressly peace-making, including the support of those persons mentioned in item four.

None of these gifts or the income from said gifts shall be used for the operating budget of the church.

Upon request, our congregation shall financially assist any member or friend who withholds war taxes if the Internal Revenue Service presses for collection of his/her tax liability.

Such contributions shall come from the fund or from special contributions of individual members of the congregation.

This latest version was adopted by the church in the .

Our need for education and discussion on this subject increases.

Every year we are painfully made aware of the shift in priorities in our national budget; every year more billions are sacrificed for weapons which will destroy God’s creation.