In earlier Picket Line entries, I’ve attempted to translate sections from the latest edition of the Spanish Handbook of Economic Disobedience (see , , and ).

I was starting to attempt to translate another section, but it looked familiar, and it turns out I already translated an earlier version of it as it appeared in a booklet called ¡Rebelaos! last year.

This seems to be an expansion of the original, however, so I’ll work my way through it again:

Tax resistance as a strategy of rebellion

As has been explained earlier, civil disobedience is a fundamental tool for raising popular empowerment on the path to self-management.

The General State Budget for 2013 poses another attack on the needs of the people. It cuts among others 14.% from the education budget, 19.6% from culture, 3.1% from health (added to 6.9% from last year), while increasing by 33% the payment of interest on the debt.

While a progressive privatization of all that is public takes place, while blaming the crisis for causing a lack of resources, while pilfering public money in the interest of those on high, the genuinely public projects on which we are working below generally suffer from a lack of such resources which would enable them to develop. To reverse this situation, it is necessary to derive a significant amount of these resources by direct means through tax resistance.

For this reason, with this publication, we share in the call to begin and extend an action of tax resistance against the Spanish State and towards those who control it, with consequent action to demonstrate that we will not pay their debts, because we do not recognize the present Constitution. Tax resistance that serves to fund the self-management of assemblies and collectives, and from them, to give absolute priority to the participatory funding of resources that we consider genuinely public.

Practical guide to income tax resistance

This is a suggestion for people who make their tax return for 2013 and subsequent years.

It is a manageable option for people who want to (or need to) remain part of the official economy, and therefore cannot afford fines or similar penalties.

This is a proposal inspired by war tax resistance, which for years has worked successfully in the Spanish State, performing this action concerning the 6% of the tax return that corresponds to military spending. But in this case, added to this percentage would be other items that we consider unjust.

You can choose these items according to your own criteria, or join in the proposed campaign of tax resistance launched by Right of Rebellion, which will be more than 25% of each participant’s income tax, and consists of the following parts of the State budget, from a total of €408,033 million, which is the budget for 2013.

In these budgets for 2013, the % of items that we have chosen as the most repulsive, rose up to 31.39% while in 2012 they remained about 29%.

Similarly, and because the main thing is to reach more and more people, we have fixed on this 25%, that is ¼ of the State budget, which is already a major challenge.

Item 2013 Budget Percentage Total Tax Resistance €128,083,979,200 31.39% Total State Budget €408,033,918,210 100% Public debt redemption €62,319,842,350 15.27% Public debt interest €38,589,550,000 9.46% Military defense €13,708,330,000 3.36% Security police €1,209,238,886 0.30% Prison system €1,129,743,730 0.28% Monarchy €7,933,710 0.01% Senate €51,900,640 0.01% Elections and political parties €67,439,960 0.02% Church €110,000,000 0.03% The filer, as a tax resister, must file the tax return; it won’t work not to. If you work as an employee, your company already pays your taxes directly to the State for you, so your tax resistance can only be applied as an application for a refund.

With your tax return, you can declare as tax resistance all of those items that you don’t agree to pay taxes for, and reclaim the money.

You can then distribute this money in a manner that you consider more consistent with your notions. To do this, at the time of filing, you must follow these steps:

- Always make out your tax return.

- Do not simply assent to the estimates filled in by the Treasury. It could be that the Treasury had some error in the data. It is difficult to have considered all of our possible deductions, or if it has, on more than one occasion there have been errors (and often not in its favor).

- In the case of not reaching the established minimum it is not advisable to stop filling out your tax return.

Anyone can do this. You do not have to be an employed worker or to have formal income. You can object as a retired person, a student, or an unemployed person, since the state grabs taxes from everyone with both hands and this is the only real opportunity to recover some of this exaction.

If you do not reach the minimum established by law for making a tax return, it is still important that you do (or at least that you do the calculations), since you will probably come out with a refusal (they have to refund money). If you determine that you come out with a payment, it does not follow that it is necessary to submit it.

How to make an income tax return for individuals practicing tax resistance

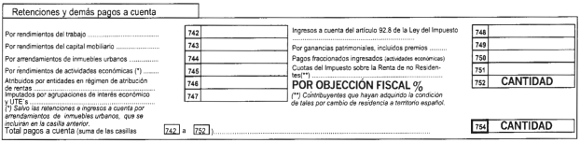

- The first thing you have to do is to fill in the forms for your income tax return. This can be done by hand or with the PADRE program. The other methods (confirmation of the statement by telephone or Internet) do not allow for tax resistance.

At this point your return is filled out up to the point of the tax liability (box 741) with the amounts withheld by your employer and by banks. Next, in box 752, you must specify a percentage of tax resistance, depending on one or many budget items you have chosen to resist (see the image below) and fill it in. If box 752 is already filled in, you can use one of the other free boxes between 742 and 751. From here, we end the tax statement by calculating the resulting tax.- To complete the statement you must pay the calculated amount of resisted tax to the usual account of the entity, collective, etc. you have chosen. Specify on the accounting: “Income derived from the 2013 tax resistance” and keep the statement that the bank provides. It is important that you allocate this money to projects near you, so you can directly verify how you yourself, with your taxes, are nourishing a nearby project, while at the same time your money is not going towards purposes you do not believe in.

- Then all that remains is to send a letter from the resister to the Treasury Department, which will be attached to the return, along with a receipt of payment to the chosen entity, collective, or project. You can take as a model the letter in the appendix; download it from the website of Right of Rebellion: www.derechoderebelion.net/modelo-de-carta-para-hacienda/ or else go to the nearest office of disobedience.

It is very important that in the letter you specify the budget items to which you are declaring your tax resistance, and that the amount calculated is the sum of the percentage of these chosen items.- The next step is to deliver the return to whichever tax office or else to the bank branch where you have an account. In doing this, whether in one place or the other, they will certainly tell you that they want only the tax return and not your other statements. You have to explain to them that we are doing tax resistance (and we can seize this opportunity to explain to that person what this consists of), that the responsibility is ours, and that we want to put into the tax return envelope the three documents: the tax return, the letter of resistance, and the bank receipt.

- Finally, it is important that you provide the information about your resistance to the Office of Economic Disobedience, so that it does not remain an individual act between you and the Treasury. It is critical to know the number of people who have used their right of tax resistance, so we urge you to fill out the tax resistance census sheet. You can also ask for a paper version. This census is purely statistical.

Some reflections on the experience of tax resistance last year

- It appears to be the case that if the tax return is filled in by hand, it is more expensive for the Treasury to examine it and therefore it is more difficult for them to detect the resistance.

- There have been some cases in which the Treasury has sent a request asking for the amount resisted, ignoring the declaration of resistance. These cases have always been of large quantities. It appears that in general, they don’t examine quantities less than 150 euros.

- Based on the previous points, it is especially important to strengthen the tax resistance budget so that it can respond in a collective form to the needs for help from resisters. You can make this helpful resistance with your resistance budget. Also to be attempted will be a crowdfunding campaign on the internet to help this resistance budget throughout the year.

Auditing the national debt, a tool to defend the refusal to pay an odious debt

As you have read on previous pages, the principal item toward which tax resistance is directed is the external debt (23%). So we added information specific to the motivation of tax resistance against this item.

As has happened in other countries, and in the light of 15-M, in Spain a campaign to audit the external debt has been generated. The reform of the Spanish Constitution that made the payment of interest and principal on the debt the top priority of the general budget, gave more force, if anything, to the need for this audit. As auditoriaciudadana.net says: “A debt that we were never aware of and that we were unable to review or assent to. A debt that is essentially of private banks. A debt that, now, they point out to us as the worst of the problems and that they make us directly responsible with a constitutional obligation to repair it. A debt that forces us to cut our investment in our social services and that condemns us to the worst of the social distresses.”

We do not want to pay your debt!

Consequently, the Spanish people are put with the debt under the blackmail of the financial markets. It is illegitimate debt which is newly contracted to pay old debt and to implement policies that harm the social and economic rights of the citizenry.

A large part of the debt is illegitimate because it stems from a policy that has favored a tiny minority of the population at the expense of the overwhelming majority of citizens.

The State has guaranteed the private debt of private companies and financial institutions to enable them to borrow at an adequate rate of interest. This implies that, subsequently, the ratings agencies issued a poor assessment of the capability to repay the debt and that the risk premium of the State soars. Therefore, the fact of endorsing private businesses or financial institutions make the State (and therefore the citizens) have to pay higher interest on the debt.

To guarantee private entities entails that creditors require an increasing ability to pay on the part of the State which stops concerning itself about other essential functions which, itself, it has to take on.

Can a government legally decide not to pay its debt because its population is in danger? Yes, because the legal argument from necessity of the State fully justifies it. The State of necessity corresponds to a situation of danger to to the existence of the State, for its political or economic survival. The economic survival relates directly to the resources that a State can provide to continue to satisfy the needs of the population, in matters of health, education, etc.

Mechanisms for resistance to the VAT

There are a variety of techniques available to a self-managed company or cooperative to stop paying the VAT to the State and to dedicate that payment to a self-managed project.

Some of them are:

- Declaring, if the VAT is yours to pay, an amount smaller than that which would apply, and with this, financing an assembly or project of your choice.

- To justify this lower payment you must gather various invoices in your name. These invoices can be made in various ways without endangering the legal cover of the action.

- If you are certain that your company will not continue and is going to close, in place of paying the State you can begin to send the VAT amounts, or the part of them that you assume, to the assemblies in your zone or to self-managed projects, whichever you most prefer.

- If you want to continue as a company and need a way to make this process sustaining, you can open and close a business every 3 or 4 years. In this way, when the Treasury goes after you to pay your VAT, the company would be bankrupt and you would generate another.

- If you are a member of a cooperative or nonprofit entity that declares VAT, you can ask for a receipt for your personal expenses with the VAT identification number of this entity and donate these receipts to have them deducted from your income and not to have to pay VAT.

- If, after all of these receipts, your self-managed cooperative has to pay VAT, you can make receipts with your personal ID number; simply after receiving the money billed, donate it back to the same cooperative.

To put these options in context, we have to take into account that the inquiries the Treasury makes to people or businesses who send receipts, in order to monitor the payment of taxes, are limited and easy to foresee. By model 347 of VAT, by 30 April, you must present a list of clients and suppliers with whom you have had more than €3,000 in annual business. Therefore, nothing prevents us from making receipts, as an individual and in a completely anonymous form, to a cooperative for less than €3,000 and not to make a VAT declaration. Even though the cooperative does make one. That is, while the cooperative accounted for it in order to deduct it from the VAT to pay, the individuals who billed do not declare it as income.

Since the cooperative is not obligated to declare who are its suppliers, the Treasury will not have information about our irregularities. The only information with which it can count on is the global balance of VAT, from which they cannot identify this type of irregularities, since one cannot know that the VAT has passed between individuals and has also been interlinked between businesses.

Resistance to the quarterly personal income tax: usually the cooperative will pay the Treasury the quarterly personal income tax from the person who has invoiced it, but it is not required to do so if this is not specified on the bill, so also in this case if there is any irregularity, it is the individual who is responsible for it and not the cooperative.

In this sense, the current Individual Income Tax Law, Law 35/2006 of 28 November, established four tax brackets and a top marginal rate of 43%. Brackets:

- Up to €9,050 gross annually, the withholding is 0%.

- Between €9,051 and €17,460 gross annually applies a marginal rate of 24%.

- Between €17,361 and €32,360 gross annually applies a marginal rate of 28%.

- Between €32,361 and €52,360 gross annually applies a marginal rate of 37%.

- After €52,361 gross annually applies a marginal rate of 43%.

Therefore, it is reasonable to have receipts without quarterly personal income tax and that the cooperative does not have to withhold, because, when this happens, it can be understood that the party issuing the invoice is in the 0% personal income tax bracket, and for this reason does not pay said tax.

So, to sum up all that has been said, the only irregularity on the part of individuals corresponds to the action of not paying the VAT. To this end it is important to add that the people who enlist in self-managed projects that have a low billing rate are not so obligated, so in order to protect themselves legally, a person can bill the cooperative, and at the same time, pay another professional for certain services (or pay daily expenses) to balance their VAT. So, in a totally legal manner, he could declare each trimester a VAT near zero. It would be indeed a way of moving from an individual VAT payer to an individual who cancels out his VAT.

Another circumstance entirely would be that of bankrupt persons. You can issue bills for your work in a completely carefree way, because in the course of an inspection, the most that you could receive would be a fine, which they would have no way to make you pay. This way, bankrupt people have the easiest time of anyone in supporting these processes of reducing VAT payments in favor of cooperatives and entities who collaborate.

Note: There are some guidelines to follow so that you avoid the risk of criminal sanctions from actions of this sort:

- It is necessary to have a document that certifies the expense.

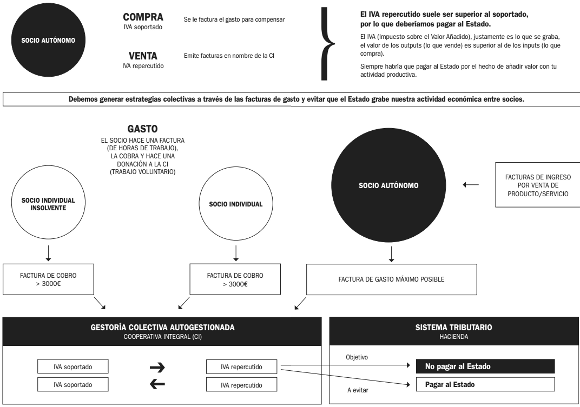

- Invoices must be sent by someone who really does engage in the activity being billed for, so that it can be demonstrated that the activity took place. And there must be economic transactions or billing declarations between the two parties (see the graph on the center pages)

Okay… with that I’m going to call it a day. There’s a lot more that follows, but there’s only so much translating I can do at a stretch.